Individual Assignment 2: Taxation Case Study

VerifiedAdded on 2019/09/26

|7

|1989

|148

Practical Assignment

AI Summary

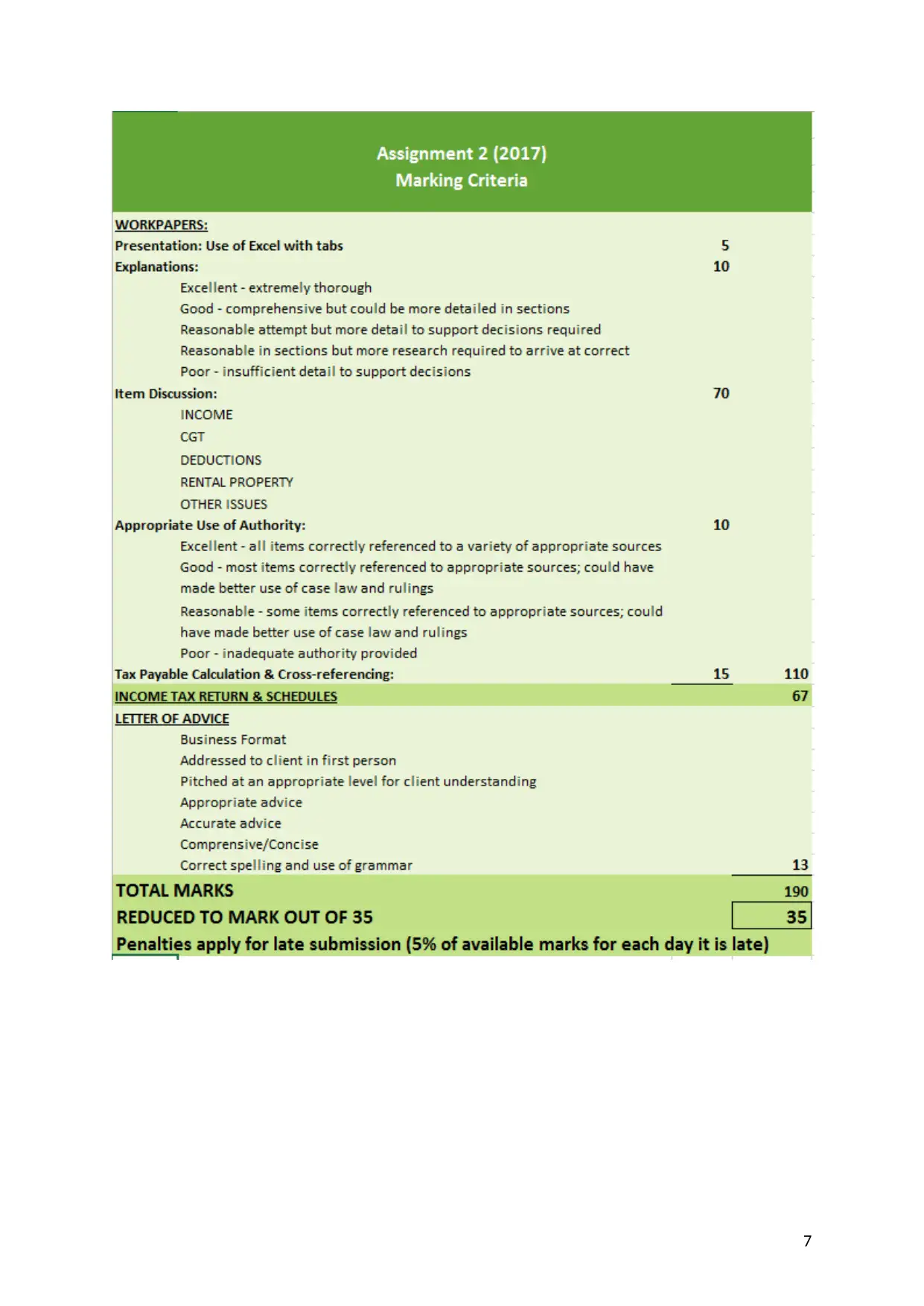

This assignment is a practical case study focusing on Australian taxation. Students are required to prepare workpapers, calculate taxable income and income tax payable for a client (using their own name), prepare an individual tax return using Handitax software, and write a professional letter of advice summarizing the client's tax situation. The case study involves various income sources (employment income, dividends, capital gains from share sales) and deductions (car expenses, rental property expenses, donations). Students must demonstrate their understanding of relevant tax legislation, case law, and rulings, providing detailed explanations and justifications for their calculations and decisions. The assignment emphasizes thorough record-keeping and professional communication in the letter of advice, advising the client on future tax planning and record-keeping improvements. The assignment is weighted at 35% of the course grade and is due in Week 11.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.