Detailed Financial Analysis and Budget Report for Twin Rivers Cafe

VerifiedAdded on 2023/01/17

|7

|1863

|45

Report

AI Summary

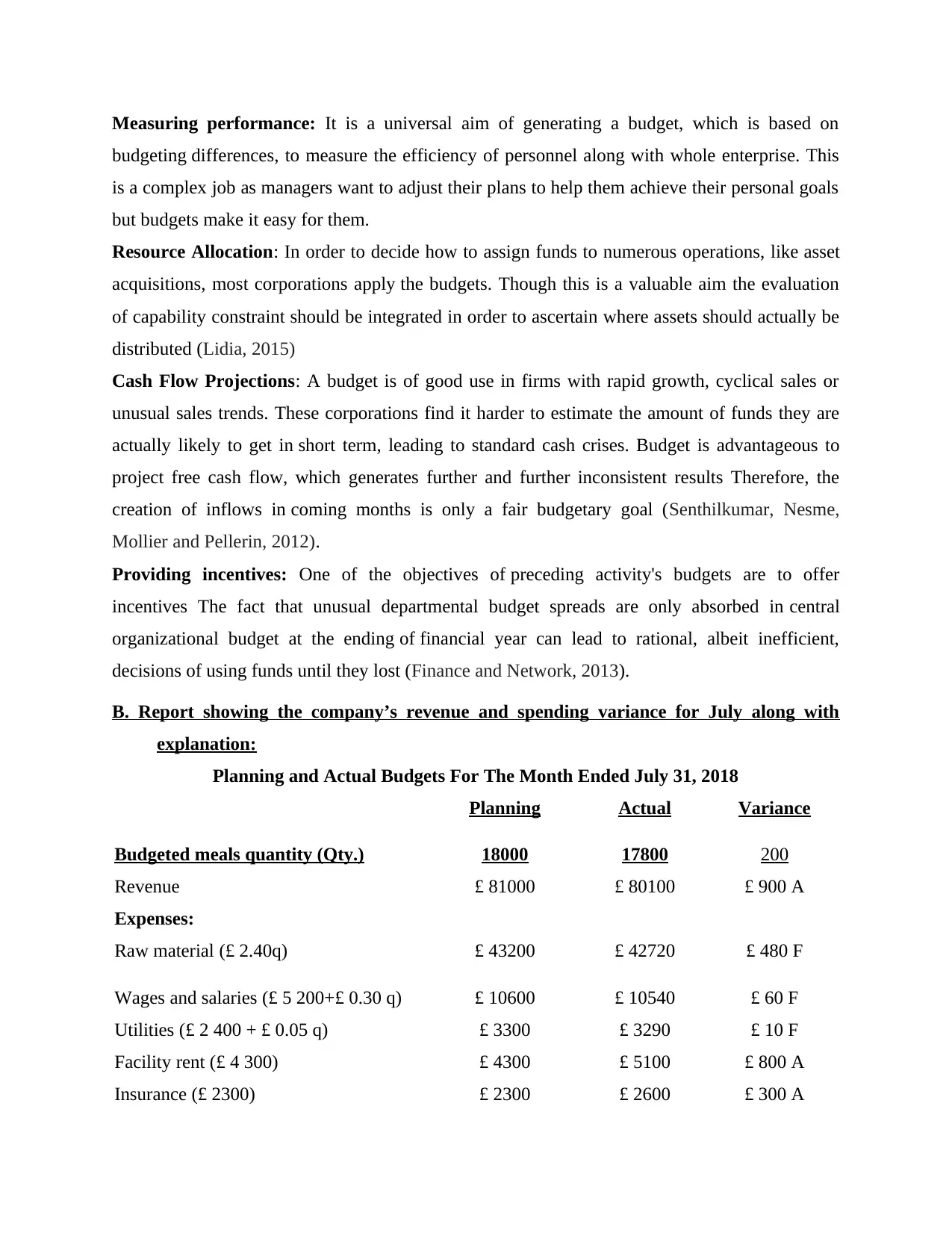

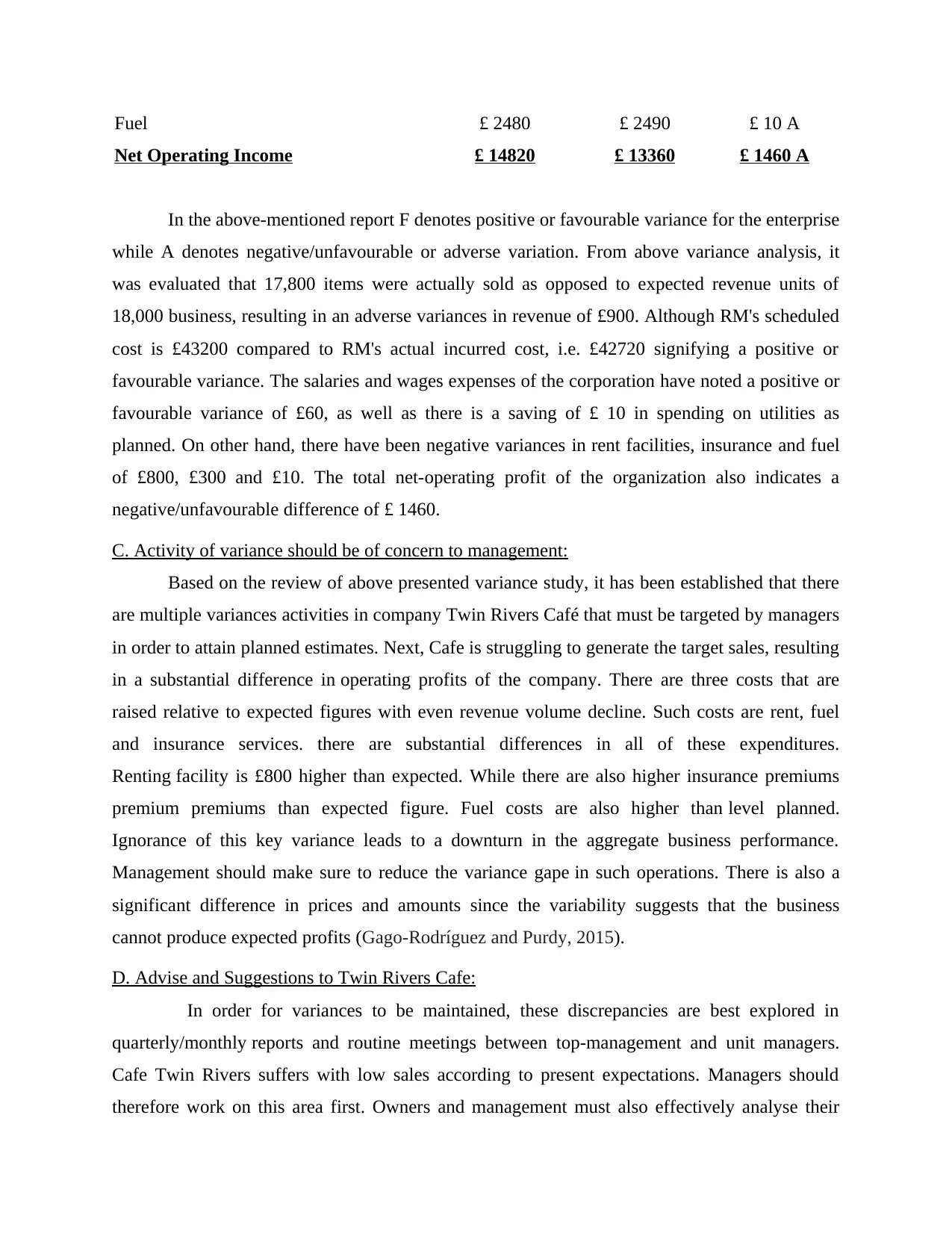

This report presents a detailed budget analysis for Twin Rivers Cafe, focusing on the objectives of budget preparation, variance analysis, and recommendations for financial improvement. It examines the company's revenue and spending variances for July 2018, highlighting favorable and unfavorable variances in areas such as revenue, raw materials, wages, utilities, facility rent, insurance, and fuel. The analysis identifies key areas of concern for management, including declining sales and increased costs in rent, insurance, and fuel. The report provides actionable advice and suggestions to Twin Rivers Cafe, such as the need for quarterly/monthly variance reports, sales target optimization, and effective cost categorization and control. The conclusion emphasizes the importance of budgets in assessing business performance and making strategic decisions for enhanced financial results.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.