Business Decision Making Report: Investment & Tesco Analysis

VerifiedAdded on 2022/12/28

|11

|3046

|155

Report

AI Summary

This report, prepared for the Business Decision Making course, provides a comprehensive analysis of investment appraisal techniques used in business decision-making. It begins by evaluating two machine models, Duke and Earl, using payback period, accounting rate of return, net present value, and internal rate of return. The analysis includes detailed calculations and a comparative report for senior management, recommending the optimal investment choice. The report then shifts focus to Tesco Plc, assessing its financial structure from 2017 to 2019, evaluating key financial ratios, discussing the limitations of accounting ratios, and identifying factors affecting Tesco's performance. The report concludes with a summary of findings and recommendations, offering insights into financial decision-making and corporate performance evaluation.

Business Decision

Making

1

Making

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Investment........................................................................................................................................3

appraisal techniques........................................................................................................................3

Payback period:- ....................................................................................................................3

Accounting rate of return:- ....................................................................................................4

Net present Value :-................................................................................................................5

Internal rate of return (IRR) :- ...............................................................................................6

Analysis report of accounting techniques...............................................................................6

Decision analysis of accounting techniques:-.........................................................................7

Analysis of Tesco Plc. ....................................................................................................................8

Evaluation of the financial structure of Tesco plc..................................................................8

for the year 2017 – 2019........................................................................................................8

Limitation of accounting ratio:-..............................................................................................9

Factor affecting Tesco Plc:-....................................................................................................9

Conclusion ......................................................................................................................................9

References......................................................................................................................................10

2

Introduction......................................................................................................................................3

Investment........................................................................................................................................3

appraisal techniques........................................................................................................................3

Payback period:- ....................................................................................................................3

Accounting rate of return:- ....................................................................................................4

Net present Value :-................................................................................................................5

Internal rate of return (IRR) :- ...............................................................................................6

Analysis report of accounting techniques...............................................................................6

Decision analysis of accounting techniques:-.........................................................................7

Analysis of Tesco Plc. ....................................................................................................................8

Evaluation of the financial structure of Tesco plc..................................................................8

for the year 2017 – 2019........................................................................................................8

Limitation of accounting ratio:-..............................................................................................9

Factor affecting Tesco Plc:-....................................................................................................9

Conclusion ......................................................................................................................................9

References......................................................................................................................................10

2

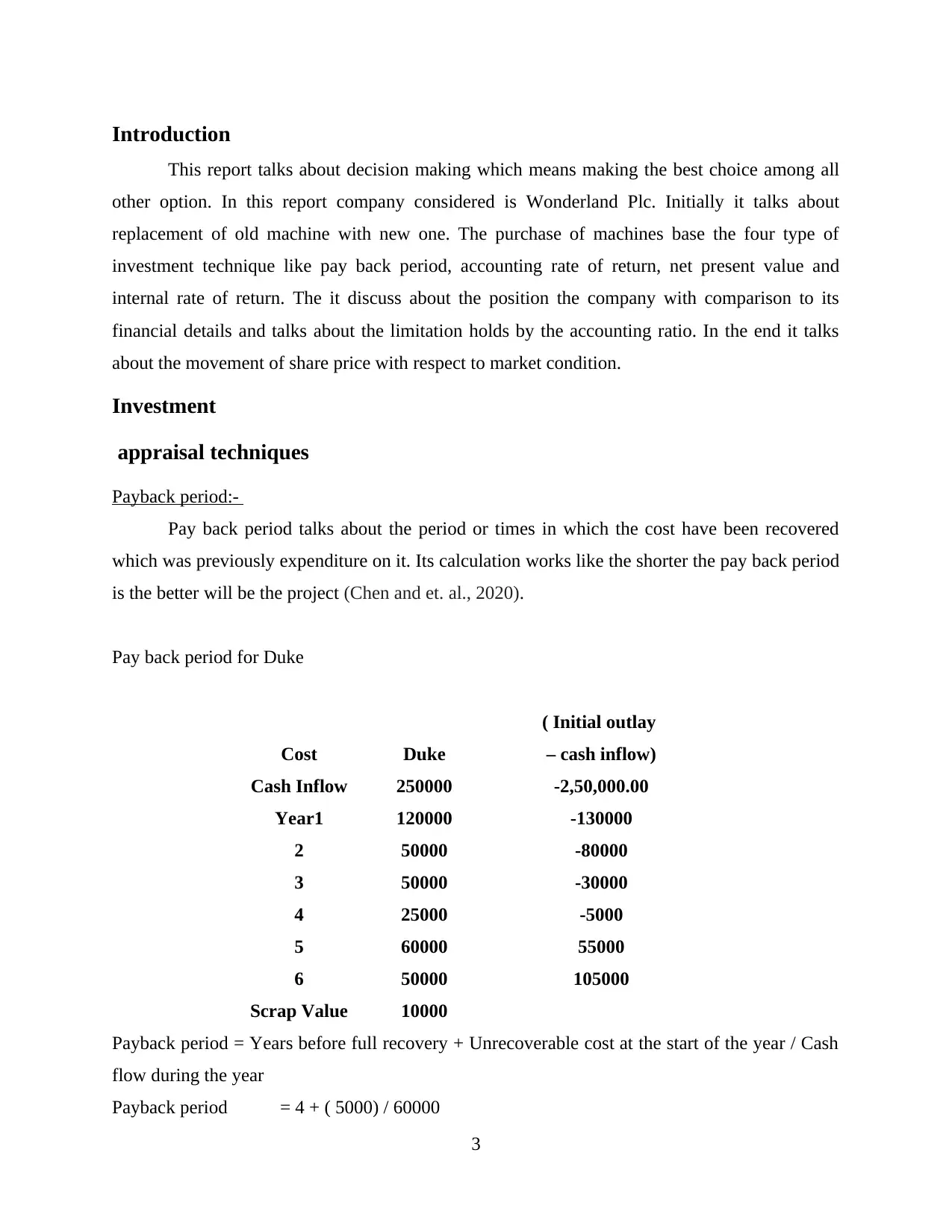

Introduction

This report talks about decision making which means making the best choice among all

other option. In this report company considered is Wonderland Plc. Initially it talks about

replacement of old machine with new one. The purchase of machines base the four type of

investment technique like pay back period, accounting rate of return, net present value and

internal rate of return. The it discuss about the position the company with comparison to its

financial details and talks about the limitation holds by the accounting ratio. In the end it talks

about the movement of share price with respect to market condition.

Investment

appraisal techniques

Payback period:-

Pay back period talks about the period or times in which the cost have been recovered

which was previously expenditure on it. Its calculation works like the shorter the pay back period

is the better will be the project (Chen and et. al., 2020).

Pay back period for Duke

Cost Duke

( Initial outlay

– cash inflow)

Cash Inflow 250000 -2,50,000.00

Year1 120000 -130000

2 50000 -80000

3 50000 -30000

4 25000 -5000

5 60000 55000

6 50000 105000

Scrap Value 10000

Payback period = Years before full recovery + Unrecoverable cost at the start of the year / Cash

flow during the year

Payback period = 4 + ( 5000) / 60000

3

This report talks about decision making which means making the best choice among all

other option. In this report company considered is Wonderland Plc. Initially it talks about

replacement of old machine with new one. The purchase of machines base the four type of

investment technique like pay back period, accounting rate of return, net present value and

internal rate of return. The it discuss about the position the company with comparison to its

financial details and talks about the limitation holds by the accounting ratio. In the end it talks

about the movement of share price with respect to market condition.

Investment

appraisal techniques

Payback period:-

Pay back period talks about the period or times in which the cost have been recovered

which was previously expenditure on it. Its calculation works like the shorter the pay back period

is the better will be the project (Chen and et. al., 2020).

Pay back period for Duke

Cost Duke

( Initial outlay

– cash inflow)

Cash Inflow 250000 -2,50,000.00

Year1 120000 -130000

2 50000 -80000

3 50000 -30000

4 25000 -5000

5 60000 55000

6 50000 105000

Scrap Value 10000

Payback period = Years before full recovery + Unrecoverable cost at the start of the year / Cash

flow during the year

Payback period = 4 + ( 5000) / 60000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

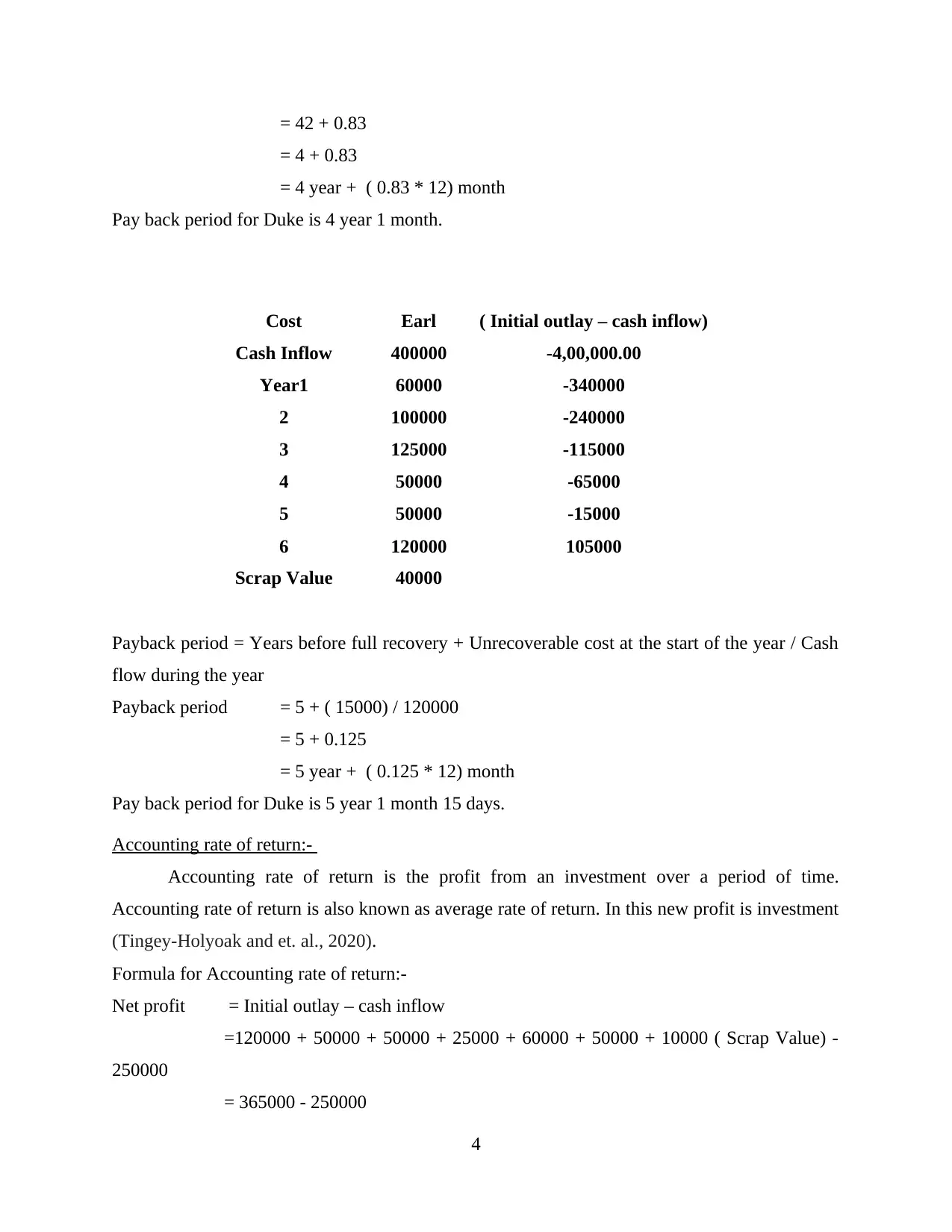

= 42 + 0.83

= 4 + 0.83

= 4 year + ( 0.83 * 12) month

Pay back period for Duke is 4 year 1 month.

Cost Earl ( Initial outlay – cash inflow)

Cash Inflow 400000 -4,00,000.00

Year1 60000 -340000

2 100000 -240000

3 125000 -115000

4 50000 -65000

5 50000 -15000

6 120000 105000

Scrap Value 40000

Payback period = Years before full recovery + Unrecoverable cost at the start of the year / Cash

flow during the year

Payback period = 5 + ( 15000) / 120000

= 5 + 0.125

= 5 year + ( 0.125 * 12) month

Pay back period for Duke is 5 year 1 month 15 days.

Accounting rate of return:-

Accounting rate of return is the profit from an investment over a period of time.

Accounting rate of return is also known as average rate of return. In this new profit is investment

(Tingey-Holyoak and et. al., 2020).

Formula for Accounting rate of return:-

Net profit = Initial outlay – cash inflow

=120000 + 50000 + 50000 + 25000 + 60000 + 50000 + 10000 ( Scrap Value) -

250000

= 365000 - 250000

4

= 4 + 0.83

= 4 year + ( 0.83 * 12) month

Pay back period for Duke is 4 year 1 month.

Cost Earl ( Initial outlay – cash inflow)

Cash Inflow 400000 -4,00,000.00

Year1 60000 -340000

2 100000 -240000

3 125000 -115000

4 50000 -65000

5 50000 -15000

6 120000 105000

Scrap Value 40000

Payback period = Years before full recovery + Unrecoverable cost at the start of the year / Cash

flow during the year

Payback period = 5 + ( 15000) / 120000

= 5 + 0.125

= 5 year + ( 0.125 * 12) month

Pay back period for Duke is 5 year 1 month 15 days.

Accounting rate of return:-

Accounting rate of return is the profit from an investment over a period of time.

Accounting rate of return is also known as average rate of return. In this new profit is investment

(Tingey-Holyoak and et. al., 2020).

Formula for Accounting rate of return:-

Net profit = Initial outlay – cash inflow

=120000 + 50000 + 50000 + 25000 + 60000 + 50000 + 10000 ( Scrap Value) -

250000

= 365000 - 250000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 115000/-

Average profit = Net profit / Number of year

= 115000 / 6

= 19166.67

Average annual profit x 100

Initial investment

= 19166.67 x 100

250000.00

= 0.0767 * 100

= 7.67 %

Duke holds 7.67% accounting rate of return 7.67%

Formula for Accounting rate of return:-

Net profit = Initial outlay – cash inflow

=60000 + 100000 + 125000 + 50000 + 50000 + 120000 + 40000 ( scrap value) +

4000000.00

= 545000 - 4000000.00

= 145000/-

Average profit = Net profit / Number of year

= 145000 / 6

= 24166.67

ARR =Average annual profit x 100

Initial investment

= 24166.67 x 100

400000.00

= 0.0604 * 100

= 6.04 %

Earl holds 6.04% accounting rate of return.

Net present Value :-

Net present value helps us to determine the profitability in terms of today. It is calculated

by discounting the future cash inflows by certain rate and reduced in the net profit (Eraña-Diaz

and et. al., 2020).

Net preset value = (Cash flow) i _ Initial investment

( 1 + Discounting rate)

= (120000) i + (50000) i …...n _ 250000

( 1 + 8%)^1 ( 1 +8%)^2

= 290233.79 – 250000

5

Average profit = Net profit / Number of year

= 115000 / 6

= 19166.67

Average annual profit x 100

Initial investment

= 19166.67 x 100

250000.00

= 0.0767 * 100

= 7.67 %

Duke holds 7.67% accounting rate of return 7.67%

Formula for Accounting rate of return:-

Net profit = Initial outlay – cash inflow

=60000 + 100000 + 125000 + 50000 + 50000 + 120000 + 40000 ( scrap value) +

4000000.00

= 545000 - 4000000.00

= 145000/-

Average profit = Net profit / Number of year

= 145000 / 6

= 24166.67

ARR =Average annual profit x 100

Initial investment

= 24166.67 x 100

400000.00

= 0.0604 * 100

= 6.04 %

Earl holds 6.04% accounting rate of return.

Net present Value :-

Net present value helps us to determine the profitability in terms of today. It is calculated

by discounting the future cash inflows by certain rate and reduced in the net profit (Eraña-Diaz

and et. al., 2020).

Net preset value = (Cash flow) i _ Initial investment

( 1 + Discounting rate)

= (120000) i + (50000) i …...n _ 250000

( 1 + 8%)^1 ( 1 +8%)^2

= 290233.79 – 250000

5

= 40233.79 /-

Net preset value = (Cash flow) i _ Initial investment

( 1 + Discounting rate)

= (60000)1 + (100000) 2 …...n _ 400000

( 1 + 8%)^1 ( 1 +8%)^2

= 410259.09 – 400000.00

= 10259.09

Internal rate of return (IRR) :-

Internal rate of return helps to determine the rate at which potential investment is going to

earn. Internal rate of return is consider as a discounting rate which make all cash flow value to

zero. This rate is also used in an cash flow analysis in discounting (Toma, Delen and Moscato,

2020).

Formula for IRR = 0 = CF0 + (CF1 / 1 + IRR) + (CF2/ 1 + IRR)^2 + … (CFn/ 1 + IRR) ^ n

= (120000) + (120000) ….… ...n _ 250000

( 1 + IRR)^1 ( 1 +IRR)^2

= 290233.79 – 250000

= 14.04 %

Formula for IRR = CF0 + (CF1 / 1 + IRR) + (CF2/ 1 + IRR)^2 + … (CFn/ 1 + IRR) ^ n

= (60000) i + (100000) i …...n _ 250000

( 1 + IRR)^1 ( 1 +IRR)^2

= 290233.79 – 250000

= 8.77%

Analysis report of accounting techniques

Payback period is used by management to determine weather to investment in an

investment or avoid it. Payback period holds one negative point time value of money(TVM).

Corporate finance all aspect considers TVM factor but pay back period not consider it. If an

investment is give high cash inflow in initial year then the later one, earlier one have more value

then later one. Pay back period have advantage also it is easy to calculate, it helps identifying the

liquidity and how quickly investment return money measure the risk of time(Nanda, Bhol and

Misra, 2020).

Accounting rate of return is a part of capital budgeting which helps in determining

quickly profitability of an investment. Major advantage of accounting rate of return is it helps in

comparing the many project at once and able to decide weather the should go for an investment

or acquisition because it shows in the percentage form. Another advantage of accounting rate of

return is it help in spreading the depreciation cost over the period of time. It holds some

6

Net preset value = (Cash flow) i _ Initial investment

( 1 + Discounting rate)

= (60000)1 + (100000) 2 …...n _ 400000

( 1 + 8%)^1 ( 1 +8%)^2

= 410259.09 – 400000.00

= 10259.09

Internal rate of return (IRR) :-

Internal rate of return helps to determine the rate at which potential investment is going to

earn. Internal rate of return is consider as a discounting rate which make all cash flow value to

zero. This rate is also used in an cash flow analysis in discounting (Toma, Delen and Moscato,

2020).

Formula for IRR = 0 = CF0 + (CF1 / 1 + IRR) + (CF2/ 1 + IRR)^2 + … (CFn/ 1 + IRR) ^ n

= (120000) + (120000) ….… ...n _ 250000

( 1 + IRR)^1 ( 1 +IRR)^2

= 290233.79 – 250000

= 14.04 %

Formula for IRR = CF0 + (CF1 / 1 + IRR) + (CF2/ 1 + IRR)^2 + … (CFn/ 1 + IRR) ^ n

= (60000) i + (100000) i …...n _ 250000

( 1 + IRR)^1 ( 1 +IRR)^2

= 290233.79 – 250000

= 8.77%

Analysis report of accounting techniques

Payback period is used by management to determine weather to investment in an

investment or avoid it. Payback period holds one negative point time value of money(TVM).

Corporate finance all aspect considers TVM factor but pay back period not consider it. If an

investment is give high cash inflow in initial year then the later one, earlier one have more value

then later one. Pay back period have advantage also it is easy to calculate, it helps identifying the

liquidity and how quickly investment return money measure the risk of time(Nanda, Bhol and

Misra, 2020).

Accounting rate of return is a part of capital budgeting which helps in determining

quickly profitability of an investment. Major advantage of accounting rate of return is it helps in

comparing the many project at once and able to decide weather the should go for an investment

or acquisition because it shows in the percentage form. Another advantage of accounting rate of

return is it help in spreading the depreciation cost over the period of time. It holds some

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

disadvantage are that is doesn't include the time value of money it mean will differentiate

anything if there is high cash flow in early stage then the later one. It will also affects the cash

timing means it will show same return if all the amount is going to receive in the last year of the

whole time period(Şahin, 2020).

NPV show the project net value after deducting investment cost then give the present

value of an investment. The advantage of using the NPV is it helps determining many project

value at base level. It also consider time value of money factor in a cash inflow. It helps in

making decision by comparing the projects value. Net present value lack at deciding the

investment when their the value of investment differs. The rate at which investment's cash inflow

is discounted that rate have no set guide lines to determine it. Discounted rate can be different on

every persons perspective. One more disadvantage of NPV is it doesn't include any type of

depreciation cost or sunk cost in it which sometimes make difference in real aspect of business

(Olson and Wu, 2020).

IRR (Internal rate of return) is a method of calculating rate of return in an investment.

The internal means in IRR that it doesn't include the external factor like inflation rate or risk of

finance. The advantage of IRR is it include the factor time value of money which major point in

every calculation. Simplicity is its added advantage which helps in interpreting it in very simple

way. It makes easy the ranking for the project because in present in percentage it makes easier to

determine the project. It's major focus is to increase the return on investment. The hight the IRR

the more desirable the project will be. The disadvantage of IRR is the scale of investment is

ignore by it mean a investment of 1000 with 18% rate and 200 with 50% return according to IRR

55% is better but in absolute terms 18% have higher returns which make it on a back foot. IRR

shows a wrong image for the project where reinvestment made it some times shows

wrong(negative) value for fix period time because in the future that also going to generate

revenue with high rate(Zhu, Meng and Chen, 2020).

Decision analysis of accounting techniques:-

As per the comparison of machine duke and earl the conclusion is made in the favour of

Duke machine because if the analysis is made on pay back period Duke machine got an

advantage 1 year and 15 days. duke machine pay back period is 4 year 1 month and earl machine

7

anything if there is high cash flow in early stage then the later one. It will also affects the cash

timing means it will show same return if all the amount is going to receive in the last year of the

whole time period(Şahin, 2020).

NPV show the project net value after deducting investment cost then give the present

value of an investment. The advantage of using the NPV is it helps determining many project

value at base level. It also consider time value of money factor in a cash inflow. It helps in

making decision by comparing the projects value. Net present value lack at deciding the

investment when their the value of investment differs. The rate at which investment's cash inflow

is discounted that rate have no set guide lines to determine it. Discounted rate can be different on

every persons perspective. One more disadvantage of NPV is it doesn't include any type of

depreciation cost or sunk cost in it which sometimes make difference in real aspect of business

(Olson and Wu, 2020).

IRR (Internal rate of return) is a method of calculating rate of return in an investment.

The internal means in IRR that it doesn't include the external factor like inflation rate or risk of

finance. The advantage of IRR is it include the factor time value of money which major point in

every calculation. Simplicity is its added advantage which helps in interpreting it in very simple

way. It makes easy the ranking for the project because in present in percentage it makes easier to

determine the project. It's major focus is to increase the return on investment. The hight the IRR

the more desirable the project will be. The disadvantage of IRR is the scale of investment is

ignore by it mean a investment of 1000 with 18% rate and 200 with 50% return according to IRR

55% is better but in absolute terms 18% have higher returns which make it on a back foot. IRR

shows a wrong image for the project where reinvestment made it some times shows

wrong(negative) value for fix period time because in the future that also going to generate

revenue with high rate(Zhu, Meng and Chen, 2020).

Decision analysis of accounting techniques:-

As per the comparison of machine duke and earl the conclusion is made in the favour of

Duke machine because if the analysis is made on pay back period Duke machine got an

advantage 1 year and 15 days. duke machine pay back period is 4 year 1 month and earl machine

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pay back period is 5 year 1 month 15 days. Hence short the period is the more lucrative an

investment become (Ostaev and et. al., 2020).

On analysing the accounting rate of return aspect duke holds a rate of return on

investment of 7.67% and earl holds a 6.04% return. ON having almost same types of cash

inflow duke get advantage because it holds low amount of investment. It can be seen that duke

holds a advantage in return which add one more point in the list of buying duke machine.

Second last point is a most important point among other because it talks about in absolute

number if there number the investment will also get differ. Duke machine investment hold a

current value of 40233.79/- and earl holds a current value of 10259.09/-. Earl having higher cash

inflow still it have lower NPV because its cash flows are arriving in later years and Duke major

inflow arriving in the early years of investment. This point also says investment in duke will be

beneficial.

Last point about IRR which make information how wonderland Plc get to know at what

rate it will be going to earn from the investment. On analysing the IRR part it states that duke

earns at a rate of 14.04% rate and earls earn at rate of 8.77% rate. On analysing the above

techniques wonderland plc will going invest in the duke machine because it holds several

positive points (Rani and Kant, 2020).

Analysis of Tesco Plc.

Evaluation of the financial structure of Tesco plc

for the year 2017 – 2019.

Tesco plc is British multinational retailer. Headquartered situated in England. Tesco Plc.

It a discussion is made of performance of Tesco, it is facing a weak performance growth in gross

profit shows profit where cost of good is reduced from sales. As its profit margin are reducing

the for the continuous three year it shows a high values of good are consumed by the company.

Return on total asset(ROA) show how much profit is generating with current asset which is used

in production or other things(Toma, Delen and Moscato, 2020). It is also reducing which is not a

good sign for the company. Third ratio is ROCE(Return on capital employed) which show about

the efficiency of generating profit from its capital it is also continuously reducing. All three

measure are showing a negative performance sign for the company.

8

investment become (Ostaev and et. al., 2020).

On analysing the accounting rate of return aspect duke holds a rate of return on

investment of 7.67% and earl holds a 6.04% return. ON having almost same types of cash

inflow duke get advantage because it holds low amount of investment. It can be seen that duke

holds a advantage in return which add one more point in the list of buying duke machine.

Second last point is a most important point among other because it talks about in absolute

number if there number the investment will also get differ. Duke machine investment hold a

current value of 40233.79/- and earl holds a current value of 10259.09/-. Earl having higher cash

inflow still it have lower NPV because its cash flows are arriving in later years and Duke major

inflow arriving in the early years of investment. This point also says investment in duke will be

beneficial.

Last point about IRR which make information how wonderland Plc get to know at what

rate it will be going to earn from the investment. On analysing the IRR part it states that duke

earns at a rate of 14.04% rate and earls earn at rate of 8.77% rate. On analysing the above

techniques wonderland plc will going invest in the duke machine because it holds several

positive points (Rani and Kant, 2020).

Analysis of Tesco Plc.

Evaluation of the financial structure of Tesco plc

for the year 2017 – 2019.

Tesco plc is British multinational retailer. Headquartered situated in England. Tesco Plc.

It a discussion is made of performance of Tesco, it is facing a weak performance growth in gross

profit shows profit where cost of good is reduced from sales. As its profit margin are reducing

the for the continuous three year it shows a high values of good are consumed by the company.

Return on total asset(ROA) show how much profit is generating with current asset which is used

in production or other things(Toma, Delen and Moscato, 2020). It is also reducing which is not a

good sign for the company. Third ratio is ROCE(Return on capital employed) which show about

the efficiency of generating profit from its capital it is also continuously reducing. All three

measure are showing a negative performance sign for the company.

8

Liquidity ratio show the cash strength in a company and speak a lot about its cash inflow

and outflow. As per the current analysis Tesco don't have good liquidity and current ratio both

are below one which is not a good performance indicator but Tesco is getting better with its

liquidity performance for continuous three year it is a good sign.

Efficiency ratio are those which show how effectively a company operation like

frequency of ordering, number of days trade receivable are paid and how early the debtor pay

their debt. Healthy inventory ratio is about where a company order its stock between 5 to 10 days

Tesco plc order a little bit later but its ratio is increase in long run. Accounts receivable and

payable depends on the industry to industry. Tesco plc account receivable and payable is looking

good because company receive early and have to pay later in the industry.

Gearing ratio talks about the owner equity to borrowed fund and Tesco plc is highly risky

with its borrowing . The way its is leading in gearing ratio it probably lead to bankruptcy in the

market. More then 100 hundred gearing ratio is considered highly risky.

Limitation of accounting ratio:-

They are various limitation to accounting ratio like company can change their financial

figures in their financial statement and the ending period of the year to improve their ratios.

Accounting ratio ignore the external factor of the environment like inflation. Many ratio use

historical prices to see better pictures. Accounting ratio never include the quality with provide by

the company and consider monetary view. Their lack of standardization in the ratio every person

uses have its own perspective on using it and in last ratio show only a last picture to the viewer

not the whole aspect of the company or its decision for being better. In consideration Tesco price

have significantly dropped from the high peak in 2019 as its ratio shown lower

performanceOstaev and et. al., 2020).

Factor affecting Tesco Plc:-

The factor affecting the Tesco plc share price are it financial performance throughout the

year. The cost factor was important for the company in 2019 due to covid-19 cost for the

production cost has increased significantly that has affected the. Today's market holds innovation

to the top which has affected the Tesco market plc and reduced its market share with significant

level. The company have its presence to the international market but still it is depend on the

United kingdom market place on a singal change in policy effects the company.

9

and outflow. As per the current analysis Tesco don't have good liquidity and current ratio both

are below one which is not a good performance indicator but Tesco is getting better with its

liquidity performance for continuous three year it is a good sign.

Efficiency ratio are those which show how effectively a company operation like

frequency of ordering, number of days trade receivable are paid and how early the debtor pay

their debt. Healthy inventory ratio is about where a company order its stock between 5 to 10 days

Tesco plc order a little bit later but its ratio is increase in long run. Accounts receivable and

payable depends on the industry to industry. Tesco plc account receivable and payable is looking

good because company receive early and have to pay later in the industry.

Gearing ratio talks about the owner equity to borrowed fund and Tesco plc is highly risky

with its borrowing . The way its is leading in gearing ratio it probably lead to bankruptcy in the

market. More then 100 hundred gearing ratio is considered highly risky.

Limitation of accounting ratio:-

They are various limitation to accounting ratio like company can change their financial

figures in their financial statement and the ending period of the year to improve their ratios.

Accounting ratio ignore the external factor of the environment like inflation. Many ratio use

historical prices to see better pictures. Accounting ratio never include the quality with provide by

the company and consider monetary view. Their lack of standardization in the ratio every person

uses have its own perspective on using it and in last ratio show only a last picture to the viewer

not the whole aspect of the company or its decision for being better. In consideration Tesco price

have significantly dropped from the high peak in 2019 as its ratio shown lower

performanceOstaev and et. al., 2020).

Factor affecting Tesco Plc:-

The factor affecting the Tesco plc share price are it financial performance throughout the

year. The cost factor was important for the company in 2019 due to covid-19 cost for the

production cost has increased significantly that has affected the. Today's market holds innovation

to the top which has affected the Tesco market plc and reduced its market share with significant

level. The company have its presence to the international market but still it is depend on the

United kingdom market place on a singal change in policy effects the company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

This report talks about the financial aspect of the company and decision making. Report

show four type of financial decision making technique. Discuss about two project and conclude

by analysing the project duke is better. Further it talks about many financial ratio and proceed for

analysing Tesco plc ratio statement.

10

This report talks about the financial aspect of the company and decision making. Report

show four type of financial decision making technique. Discuss about two project and conclude

by analysing the project duke is better. Further it talks about many financial ratio and proceed for

analysing Tesco plc ratio statement.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and journal

Chen, J. M. and et. al., 2020. Decision-making in cruise operations management: A double-

hurdle approach. Research in Transportation Business & Management. 37. p.100524.

Eraña-Diaz, M.L. and et. al., 2020. Optimization for Risk Decision-Making Through Simulated

Annealing. IEEE Access. 8. pp.117063-117079.

Nanda, S., Bhol, B. P. and Misra, S., 2020. business intelligence and decision making influence

Bancassurance system. Odisha Journal of Social Sciences. 7(1).

Olson, D. L. and Wu, D. D., 2020. Guest Editorial Special Issue: Modeling Support to Various

Levels of Decision-Making. IEEE Transactions on Systems, Man, and Cybernetics:

Systems. 50(10). pp.3728-3730.

Ostaev, G. Y. and et. al., 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga. 9(27). pp.319-332.

Rani, B. and Kant, S., 2020. An Approach Toward Integration of Big Data into Decision

Making Process. In New Paradigm in Decision Science and Management .pp. 207-215..

Springer, Singapore.

Şahin, M., 2020. Hybrid Multicriteria Group Decision-Making Method for Offshore Location

Selection Under Fuzzy Environment. Arabian Journal for Science and

Engineering. 45(8). pp.6887-6909.

Tingey-Holyoak, J. and et. al., 2020, February. Cost-Informed Water Decision-Making

Technology for Smarter Farming. In International Conference on Intelligent Human

Systems Integration (pp. 404-408). Springer, Cham.

Toma, I., Delen, D. and Moscato, G., 2020. Impact of Loss and Gain Forecasting on the

Behavior of Pricing Decision-making. business world. 19. p.20.

Zhu, X., Meng, X. and Chen, Y., 2020. A novel decision-making model for selecting a

construction project delivery system. Journal of Civil Engineering and

Management. 26(7). pp.635-650.

11

Books and journal

Chen, J. M. and et. al., 2020. Decision-making in cruise operations management: A double-

hurdle approach. Research in Transportation Business & Management. 37. p.100524.

Eraña-Diaz, M.L. and et. al., 2020. Optimization for Risk Decision-Making Through Simulated

Annealing. IEEE Access. 8. pp.117063-117079.

Nanda, S., Bhol, B. P. and Misra, S., 2020. business intelligence and decision making influence

Bancassurance system. Odisha Journal of Social Sciences. 7(1).

Olson, D. L. and Wu, D. D., 2020. Guest Editorial Special Issue: Modeling Support to Various

Levels of Decision-Making. IEEE Transactions on Systems, Man, and Cybernetics:

Systems. 50(10). pp.3728-3730.

Ostaev, G. Y. and et. al., 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga. 9(27). pp.319-332.

Rani, B. and Kant, S., 2020. An Approach Toward Integration of Big Data into Decision

Making Process. In New Paradigm in Decision Science and Management .pp. 207-215..

Springer, Singapore.

Şahin, M., 2020. Hybrid Multicriteria Group Decision-Making Method for Offshore Location

Selection Under Fuzzy Environment. Arabian Journal for Science and

Engineering. 45(8). pp.6887-6909.

Tingey-Holyoak, J. and et. al., 2020, February. Cost-Informed Water Decision-Making

Technology for Smarter Farming. In International Conference on Intelligent Human

Systems Integration (pp. 404-408). Springer, Cham.

Toma, I., Delen, D. and Moscato, G., 2020. Impact of Loss and Gain Forecasting on the

Behavior of Pricing Decision-making. business world. 19. p.20.

Zhu, X., Meng, X. and Chen, Y., 2020. A novel decision-making model for selecting a

construction project delivery system. Journal of Civil Engineering and

Management. 26(7). pp.635-650.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.