City Sky and Emma's Tax Implications: GST and Capital Gains Tax

VerifiedAdded on 2021/02/21

|9

|2778

|38

Project

AI Summary

This individual project analyzes the Goods and Services Tax (GST) and capital gains tax (CGT) implications for two scenarios. The first case involves City Sky, a property investment and development company, seeking to claim input tax credits for legal services related to apartment construction. The analysis determines the eligibility of these credits based on Australian GST laws, considering factors like business registration and the nature of the services. The second case examines Emma's tax return, focusing on CGT implications from the sale of land, shares, and a stamp collection. The project calculates capital gains and losses, considering acquisition costs, expenses, and relevant tax regulations, including exemptions for assets acquired before specific dates. The project applies Australian taxation guidelines to determine tax liabilities and deductions for each transaction, providing a comprehensive overview of CGT calculations and implications.

INDIVIDUAL PROJECT

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

Issue.............................................................................................................................................3

Rules............................................................................................................................................3

Application...................................................................................................................................4

Conclusion...................................................................................................................................5

QUESTION 2...................................................................................................................................5

Rules............................................................................................................................................6

Application...................................................................................................................................7

Conclusion ..................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

2

QUESTION 1...................................................................................................................................3

Issue.............................................................................................................................................3

Rules............................................................................................................................................3

Application...................................................................................................................................4

Conclusion...................................................................................................................................5

QUESTION 2...................................................................................................................................5

Rules............................................................................................................................................6

Application...................................................................................................................................7

Conclusion ..................................................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

2

QUESTION 1

Issue

The given case about the company dealing in property investment and the development.

Company has purchased a piece of vacant land in South Brisbane for construction of 15

apartments for selling out. City sky has availed the services of a local lawyer for providing legal

services related to the development work related to the apartments. Lawyer charged fees of $

33000. An established sole proprietor business is run by Maurice Blackburn with turnover of

around $ 300000 per year. In the present question company wants to avail the input tax credit

related to the services provided by lawyer. It is is to be identified whether input tax credit can be

availed by company for the legal services assuming that City Sky is registered under GST.

Rules

Property Tax

Property tax is tax on property value of property value. Governing authority levies the property

tax of the relevant jurisdiction where the property is situated. Property in Australia is taxed over

both levels which are State and Council. Stamp duty is generally known as state tax.

Land tax is state tax which is to be assessed each year on value of the property but in most of the

states there is exemption related to land tax (Varela, 2016).

GST

The goods and service tax is levied on supply. It is value added tax on sale of goods & services.

GST is levied is levied over most of the transactions which are incurred in production process, in

most transaction GST is refunded to parties in production chain other than final customers. GST

is to be paid by person who is providing taxable supply.

Every Australian having the turnover above the threshold limit is required to register under GST

(Millar, 2017). Businesses having turnover below the threshold limit have the option of being

registered.

Activities are treated as enterprise if land is bought with motive of reselling it at a profit. The

term property include land, land & buildings.

GST can be claimed by purchasers of real state property if

Buyer is registered for GST

There should be tax invoice on purchase on which GST has been paid.

Property should be used for carrying on enterprise.

3

Issue

The given case about the company dealing in property investment and the development.

Company has purchased a piece of vacant land in South Brisbane for construction of 15

apartments for selling out. City sky has availed the services of a local lawyer for providing legal

services related to the development work related to the apartments. Lawyer charged fees of $

33000. An established sole proprietor business is run by Maurice Blackburn with turnover of

around $ 300000 per year. In the present question company wants to avail the input tax credit

related to the services provided by lawyer. It is is to be identified whether input tax credit can be

availed by company for the legal services assuming that City Sky is registered under GST.

Rules

Property Tax

Property tax is tax on property value of property value. Governing authority levies the property

tax of the relevant jurisdiction where the property is situated. Property in Australia is taxed over

both levels which are State and Council. Stamp duty is generally known as state tax.

Land tax is state tax which is to be assessed each year on value of the property but in most of the

states there is exemption related to land tax (Varela, 2016).

GST

The goods and service tax is levied on supply. It is value added tax on sale of goods & services.

GST is levied is levied over most of the transactions which are incurred in production process, in

most transaction GST is refunded to parties in production chain other than final customers. GST

is to be paid by person who is providing taxable supply.

Every Australian having the turnover above the threshold limit is required to register under GST

(Millar, 2017). Businesses having turnover below the threshold limit have the option of being

registered.

Activities are treated as enterprise if land is bought with motive of reselling it at a profit. The

term property include land, land & buildings.

GST can be claimed by purchasers of real state property if

Buyer is registered for GST

There should be tax invoice on purchase on which GST has been paid.

Property should be used for carrying on enterprise.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

GST can't be claimed if seller is using marginal scheme of GST.

There are conditions that can lower or limit the entitlements to GST credits, like renting out

commercial flats built for sale on rent.

When GST is required to be paid -

If the turnover of company providing supply is less than $75000, then it is not required

to pay GST. When buying or selling commercial property number of transactions for which

GST credits are available on related expense like fees of solicitor, fees to agent of real

state(Adam and Yusof, 2018.). It is included when:

When any property is bought or sold as taxable sale or either as sale of going concern.

When property is bought or sold where margin scheme was in use.

GST credit on related expense is not applicable if :

When property sold is classified as input taxed supply.

When property bought is not used for carrying out enterprise.

When an Vacant land is acquired it is generally treated as capital asset on which capital gain

tax is applicable but purchase by real state dealer is not a capital asset. It is the business of the

purchaser to buy and develop land for resale. There are deductions available if the land is

purchased for building dwelling that will be rented or sold (Pearl, 2016). Deductions are

available like council rates, interest on loan and other holding costs.

Australian Taxation

Australian taxation office provides the rules and guidelines relating to the GST. Purchase

of land for construction of residential apartments for resale are covered under taxable supply.

GST will be charged on sale by company. In the construction of apartments there are various

levels at which GST is paid by company for completing the construction of apartments.

Application

As per the norms and guidelines provided under the GST laws there are transactions for which

input tax credit is available. Applying the above laws and provisions given for GST on purchase

of land GST credit is available for expenses related to the purchase of land which will be used

for construction of apartments. Company is a real state investor and developer that purchases

land for construction therefore purchase of land by such company is part of its business. The

purchase of land is not capital asset therefore provisions related to property tax are not

applicable to company (Millar, 2017). Services availed by company from lawyer are for guiding

4

There are conditions that can lower or limit the entitlements to GST credits, like renting out

commercial flats built for sale on rent.

When GST is required to be paid -

If the turnover of company providing supply is less than $75000, then it is not required

to pay GST. When buying or selling commercial property number of transactions for which

GST credits are available on related expense like fees of solicitor, fees to agent of real

state(Adam and Yusof, 2018.). It is included when:

When any property is bought or sold as taxable sale or either as sale of going concern.

When property is bought or sold where margin scheme was in use.

GST credit on related expense is not applicable if :

When property sold is classified as input taxed supply.

When property bought is not used for carrying out enterprise.

When an Vacant land is acquired it is generally treated as capital asset on which capital gain

tax is applicable but purchase by real state dealer is not a capital asset. It is the business of the

purchaser to buy and develop land for resale. There are deductions available if the land is

purchased for building dwelling that will be rented or sold (Pearl, 2016). Deductions are

available like council rates, interest on loan and other holding costs.

Australian Taxation

Australian taxation office provides the rules and guidelines relating to the GST. Purchase

of land for construction of residential apartments for resale are covered under taxable supply.

GST will be charged on sale by company. In the construction of apartments there are various

levels at which GST is paid by company for completing the construction of apartments.

Application

As per the norms and guidelines provided under the GST laws there are transactions for which

input tax credit is available. Applying the above laws and provisions given for GST on purchase

of land GST credit is available for expenses related to the purchase of land which will be used

for construction of apartments. Company is a real state investor and developer that purchases

land for construction therefore purchase of land by such company is part of its business. The

purchase of land is not capital asset therefore provisions related to property tax are not

applicable to company (Millar, 2017). Services availed by company from lawyer are for guiding

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company related to legal obligation which company is required to comply with. The lawyer

has charged fees for his services and raised GST invoice for the same. Lawyer is having annual

turnover of $300000 which means lawyer must be a registered professional who is paying GST

for its services. By this is clear that company has obtained services from registered dealer and

therefore GST paid on invoice can be claimed as input tax credit (James, 2018). Company can

take input tax credit when services are related to the business activity. Services like solicitor

fees or fees of real state agent are given input tax credit because they are related to the

purchase or sale of property. Applying GST laws company will avail the input tax credit for

services which are incurred for bringing the product to finished stage.

Conclusion

It is concluded from the study above for input tax credits that City Sky can claim

input tax credit. The services of lawyer was taken so that it can guide company for the legal

framework that are required to be complied by the company. Services were related to the

development of apartment that will be resold by company. When expenses are related to the

business on which GST is paid by company it can receive input tax credit for the same.

Therefore services received from lawyers for the development work are available for GST

input credit. The fees charged by lawyer of $33000 is for business and tax invoice is raised for

the services. Company can claim credit at given rates for the GST charged on invoice.

Australian taxation office has given provisions and guidelines regarding every transaction on

which GST credits are available and where it is not available.

QUESTION 2

Issue

Emma is planning to prepare the tax return for the year 2015. Emma has incurred

various transaction during the year on which Capital Gain tax may apply. She sold block of

land for $ 1000000 which was purchased as an investment in the year 1991. Land was purchased

by her for $250000 in addition with $5000 and $ 10000 for stamp duty and legal fees. Loan was

taken for funding the purchase of land on which interest of $32000 was paid by her. During the

ownership period she incurred expenses amounting to $22000 for water, council rates and for

insurance (Langenmayr, 2017). Emma also incurred legal fees of $5000 for resolving the dispute

with neighbour regarding the issue relating to use of land. She spent $ 27500 for removing the

5

has charged fees for his services and raised GST invoice for the same. Lawyer is having annual

turnover of $300000 which means lawyer must be a registered professional who is paying GST

for its services. By this is clear that company has obtained services from registered dealer and

therefore GST paid on invoice can be claimed as input tax credit (James, 2018). Company can

take input tax credit when services are related to the business activity. Services like solicitor

fees or fees of real state agent are given input tax credit because they are related to the

purchase or sale of property. Applying GST laws company will avail the input tax credit for

services which are incurred for bringing the product to finished stage.

Conclusion

It is concluded from the study above for input tax credits that City Sky can claim

input tax credit. The services of lawyer was taken so that it can guide company for the legal

framework that are required to be complied by the company. Services were related to the

development of apartment that will be resold by company. When expenses are related to the

business on which GST is paid by company it can receive input tax credit for the same.

Therefore services received from lawyers for the development work are available for GST

input credit. The fees charged by lawyer of $33000 is for business and tax invoice is raised for

the services. Company can claim credit at given rates for the GST charged on invoice.

Australian taxation office has given provisions and guidelines regarding every transaction on

which GST credits are available and where it is not available.

QUESTION 2

Issue

Emma is planning to prepare the tax return for the year 2015. Emma has incurred

various transaction during the year on which Capital Gain tax may apply. She sold block of

land for $ 1000000 which was purchased as an investment in the year 1991. Land was purchased

by her for $250000 in addition with $5000 and $ 10000 for stamp duty and legal fees. Loan was

taken for funding the purchase of land on which interest of $32000 was paid by her. During the

ownership period she incurred expenses amounting to $22000 for water, council rates and for

insurance (Langenmayr, 2017). Emma also incurred legal fees of $5000 for resolving the dispute

with neighbour regarding the issue relating to use of land. She spent $ 27500 for removing the

5

large number of pine trees from the land before making it available for sale. She also incurred

advertisement, legal and agent fees for the sale of land amounting to $ 25000.

Another transaction was of sale of 1000 shares for $50.85 which were purchased b y her

in year 1982 for $3.5 per share. She also paid brokerage on sale of 2%. Sale of stamps collected

which were purchased by Emma from private collector for $60000 in 2015. Last transaction is

related to sale of piano. Emma wants to know the capital gain tax implication relating to the

following transactions so that it can prepare the tax return for the year 2015.

Rules

Australian Taxation

When an capital asset is sold real state or shares, generally capital gain or loss is made.

Capital gain or loss is the difference between cost of acquisition and cost of sales. Capital gain

and losses are required to be reported in income tax return of an individual. It is known as

capital gain tax but is part of income tax return only. When a capital gain is made it is made part

of the assessable income and can increase significantly the tax required to be paid (Thuronyi and

Brooks, 2016.). Tax on capital gain is not withheld therefore assessee would be required to

work out the tax liability. Capital loss cannot be claimed against other income of the assessee

but can be used against capital gain for reducing it. All assets acquired after September 20, 1985

are subjected to capital gain tax unless excluded specifically. Assets acquired for the personal

use are exempt from GST like car, home and other assets like furniture etc.. Capital gain or loss

is to be reported in the year when contract for disposal is entered.

The capital gain tax can be calculated using the discount method. For calculating the

capital gain tax through discounting model assessee should be an individual, super fund or trust.

CGT event has occurred after September, 21 1999. Asset is acquired 12 months before

occurrence of CGT event. The indexation method is not chosen by the individual for calculating

the capital gain tax. Discount percentage rate is 50% after deducting all capital losses and

unapplied capital losses of earlier years. Capital gain tax is applicable on sale of shares. The

individual will attract the same provision on sale of shares as they are also the retained for

more than 12 months (Devereux and Vella, 2018). There are ex emptions for capital assets a

cquired before September 20, 1985.

Collectibles include antiques, metals, stamps, coins etc., and has extra value because of

its rarity. Tax rate is applicable at maximum of 28% at the time of sale. Tax is applicable on the

6

advertisement, legal and agent fees for the sale of land amounting to $ 25000.

Another transaction was of sale of 1000 shares for $50.85 which were purchased b y her

in year 1982 for $3.5 per share. She also paid brokerage on sale of 2%. Sale of stamps collected

which were purchased by Emma from private collector for $60000 in 2015. Last transaction is

related to sale of piano. Emma wants to know the capital gain tax implication relating to the

following transactions so that it can prepare the tax return for the year 2015.

Rules

Australian Taxation

When an capital asset is sold real state or shares, generally capital gain or loss is made.

Capital gain or loss is the difference between cost of acquisition and cost of sales. Capital gain

and losses are required to be reported in income tax return of an individual. It is known as

capital gain tax but is part of income tax return only. When a capital gain is made it is made part

of the assessable income and can increase significantly the tax required to be paid (Thuronyi and

Brooks, 2016.). Tax on capital gain is not withheld therefore assessee would be required to

work out the tax liability. Capital loss cannot be claimed against other income of the assessee

but can be used against capital gain for reducing it. All assets acquired after September 20, 1985

are subjected to capital gain tax unless excluded specifically. Assets acquired for the personal

use are exempt from GST like car, home and other assets like furniture etc.. Capital gain or loss

is to be reported in the year when contract for disposal is entered.

The capital gain tax can be calculated using the discount method. For calculating the

capital gain tax through discounting model assessee should be an individual, super fund or trust.

CGT event has occurred after September, 21 1999. Asset is acquired 12 months before

occurrence of CGT event. The indexation method is not chosen by the individual for calculating

the capital gain tax. Discount percentage rate is 50% after deducting all capital losses and

unapplied capital losses of earlier years. Capital gain tax is applicable on sale of shares. The

individual will attract the same provision on sale of shares as they are also the retained for

more than 12 months (Devereux and Vella, 2018). There are ex emptions for capital assets a

cquired before September 20, 1985.

Collectibles include antiques, metals, stamps, coins etc., and has extra value because of

its rarity. Tax rate is applicable at maximum of 28% at the time of sale. Tax is applicable on the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profits made on sale of collectibles. Capital gain on sale of collectables is exempt if prescribed

conditions are satisfied by the collectables. Sale of collectables which were kept for less than

one year capital gain would be taxable as per regular income (Åstebro, 2017.).

Application

Emma for the tax return of year 2015 has incurred capital transactions which are

required to be reported in her tax return.

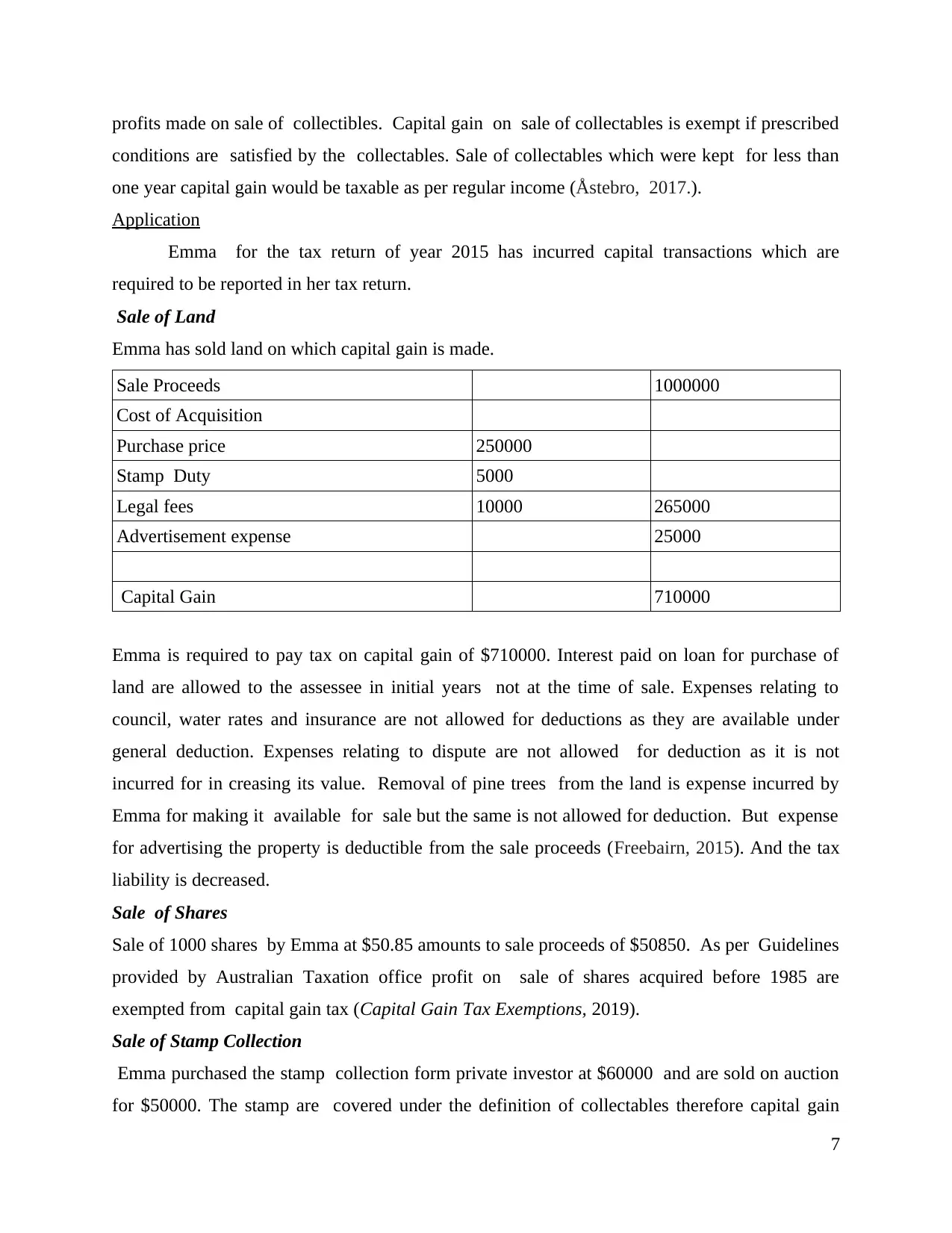

Sale of Land

Emma has sold land on which capital gain is made.

Sale Proceeds 1000000

Cost of Acquisition

Purchase price 250000

Stamp Duty 5000

Legal fees 10000 265000

Advertisement expense 25000

Capital Gain 710000

Emma is required to pay tax on capital gain of $710000. Interest paid on loan for purchase of

land are allowed to the assessee in initial years not at the time of sale. Expenses relating to

council, water rates and insurance are not allowed for deductions as they are available under

general deduction. Expenses relating to dispute are not allowed for deduction as it is not

incurred for in creasing its value. Removal of pine trees from the land is expense incurred by

Emma for making it available for sale but the same is not allowed for deduction. But expense

for advertising the property is deductible from the sale proceeds (Freebairn, 2015). And the tax

liability is decreased.

Sale of Shares

Sale of 1000 shares by Emma at $50.85 amounts to sale proceeds of $50850. As per Guidelines

provided by Australian Taxation office profit on sale of shares acquired before 1985 are

exempted from capital gain tax (Capital Gain Tax Exemptions, 2019).

Sale of Stamp Collection

Emma purchased the stamp collection form private investor at $60000 and are sold on auction

for $50000. The stamp are covered under the definition of collectables therefore capital gain

7

conditions are satisfied by the collectables. Sale of collectables which were kept for less than

one year capital gain would be taxable as per regular income (Åstebro, 2017.).

Application

Emma for the tax return of year 2015 has incurred capital transactions which are

required to be reported in her tax return.

Sale of Land

Emma has sold land on which capital gain is made.

Sale Proceeds 1000000

Cost of Acquisition

Purchase price 250000

Stamp Duty 5000

Legal fees 10000 265000

Advertisement expense 25000

Capital Gain 710000

Emma is required to pay tax on capital gain of $710000. Interest paid on loan for purchase of

land are allowed to the assessee in initial years not at the time of sale. Expenses relating to

council, water rates and insurance are not allowed for deductions as they are available under

general deduction. Expenses relating to dispute are not allowed for deduction as it is not

incurred for in creasing its value. Removal of pine trees from the land is expense incurred by

Emma for making it available for sale but the same is not allowed for deduction. But expense

for advertising the property is deductible from the sale proceeds (Freebairn, 2015). And the tax

liability is decreased.

Sale of Shares

Sale of 1000 shares by Emma at $50.85 amounts to sale proceeds of $50850. As per Guidelines

provided by Australian Taxation office profit on sale of shares acquired before 1985 are

exempted from capital gain tax (Capital Gain Tax Exemptions, 2019).

Sale of Stamp Collection

Emma purchased the stamp collection form private investor at $60000 and are sold on auction

for $50000. The stamp are covered under the definition of collectables therefore capital gain

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

would be applicable if they are kept for more than a year (Faccio and Xu, 2015). Here Emma

has sold asset at loss of $10000, but it will not be adjusted against capital gain as the collection

was not capital asset as they were kept for less than one year (Capital Gain Tax, 2019).

Sale of Piano

Capital loss of $50000 on sale of piano can be adjusted against capital gains of Emma. Gain on

sale of personal asset are exempt if they are purchased for less than $10000.

Conclusion

From the above rules and regulations it can be concluded that Emma has to pay capital gain tax

on sale of land. Gain on sale of shares are exempted where loss on sale of collectables are not

adjusted against gain. Loss on sale of piano is allowed for adjustment as it was purchased after

September, 1999 and purchased for $ 80000. The income tax return of Emma for the year 2015

will include following transactions related to capital gains or losses.

8

has sold asset at loss of $10000, but it will not be adjusted against capital gain as the collection

was not capital asset as they were kept for less than one year (Capital Gain Tax, 2019).

Sale of Piano

Capital loss of $50000 on sale of piano can be adjusted against capital gains of Emma. Gain on

sale of personal asset are exempt if they are purchased for less than $10000.

Conclusion

From the above rules and regulations it can be concluded that Emma has to pay capital gain tax

on sale of land. Gain on sale of shares are exempted where loss on sale of collectables are not

adjusted against gain. Loss on sale of piano is allowed for adjustment as it was purchased after

September, 1999 and purchased for $ 80000. The income tax return of Emma for the year 2015

will include following transactions related to capital gains or losses.

8

REFERENCES

Books and Journals

Adam, M.N.H. and Yusof, N.A.M., 2018. A Comparative Study on the Burden of Tax

Compliance Costs amongst GST Registered Companies in Malaysia and Abroad. Journal

of Science, Technology and Innovation Policy. 3(2).

Åstebro, T., 2017. The private financial gains to entrepreneurship: Is it a good use of public

money to encourage individuals to become entrepreneurs?. Small Business

Economics. 48(2). pp.323-329.

Devereux, M.P. and Vella, J., 2018. Debate: Implications of Digitalization for International

Corporate Tax Reform. Intertax. 46(6). pp.550-559.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis. 50(3). pp.277-300.

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review. 48(4). pp.357-368.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia.(2018). 47.

Langenmayr, D., 2017. Voluntary disclosure of evaded taxes—Increasing revenue, or increasing

incentives to evade?. Journal of Public Economics. 151. pp.110-125.

Millar, R., 2017. UberX drivers supply taxi travel and so must be registered for GST: Uber BV v

Commissioner of Taxation [2017] FCA 110. World Journal of VAT/GST Law. 6(1). pp.47-

54.

Pearl, D., 2016. The Policy and Politics of Reform of the Australian Goods and Services

Tax. Asia & the Pacific Policy Studies. 3(3). pp.405-411.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Varela, P., 2016. What are progressive and regressive taxes?(Doctoral dissertation, The

Australian National University Canberra).

Online

Capital Gain Tax Exemptions. 2019.[Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Capital Gain Tax. 2019.[Online]. Available through : <https://www.ato.gov.au/General/Capital-

gains-tax/>.

9

Books and Journals

Adam, M.N.H. and Yusof, N.A.M., 2018. A Comparative Study on the Burden of Tax

Compliance Costs amongst GST Registered Companies in Malaysia and Abroad. Journal

of Science, Technology and Innovation Policy. 3(2).

Åstebro, T., 2017. The private financial gains to entrepreneurship: Is it a good use of public

money to encourage individuals to become entrepreneurs?. Small Business

Economics. 48(2). pp.323-329.

Devereux, M.P. and Vella, J., 2018. Debate: Implications of Digitalization for International

Corporate Tax Reform. Intertax. 46(6). pp.550-559.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis. 50(3). pp.277-300.

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review. 48(4). pp.357-368.

James, K., 2018. Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia.(2018). 47.

Langenmayr, D., 2017. Voluntary disclosure of evaded taxes—Increasing revenue, or increasing

incentives to evade?. Journal of Public Economics. 151. pp.110-125.

Millar, R., 2017. UberX drivers supply taxi travel and so must be registered for GST: Uber BV v

Commissioner of Taxation [2017] FCA 110. World Journal of VAT/GST Law. 6(1). pp.47-

54.

Pearl, D., 2016. The Policy and Politics of Reform of the Australian Goods and Services

Tax. Asia & the Pacific Policy Studies. 3(3). pp.405-411.

Thuronyi, V. and Brooks, K., 2016. Comparative tax law. Kluwer Law International BV.

Varela, P., 2016. What are progressive and regressive taxes?(Doctoral dissertation, The

Australian National University Canberra).

Online

Capital Gain Tax Exemptions. 2019.[Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Capital Gain Tax. 2019.[Online]. Available through : <https://www.ato.gov.au/General/Capital-

gains-tax/>.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.