Financial Analysis Report: Jackdaw Ltd. Performance (MGT5014)

VerifiedAdded on 2022/12/30

|11

|2593

|69

Report

AI Summary

This report provides a comprehensive financial analysis of Jackdaw Ltd., an online sports equipment retailer, based on its 2019 and 2020 financial statements. The analysis includes the calculation and evaluation of various financial ratios, such as Return on Capital Employed (ROCE), Net Profit Margin, Gross Profit Margin, Current Ratio, Acid Test Ratio, Debtor Collection Period, Creditor Payment Period, Inventory Turnover Ratio, Gearing Ratio, Dividend Cover Ratio, Interest Cover Ratio, Earnings Per Share (EPS), and Price-Earnings (P/E) Ratio. The report evaluates the company's performance over the two years, highlighting a decline in key financial metrics in 2020 compared to 2019. Furthermore, the report compares Jackdaw Ltd.'s financial ratios with industry averages, revealing areas where the company underperforms. The report also discusses the usefulness and limitations of ratio analysis and suggests additional information that could enhance the evaluation. The analysis concludes that Jackdaw Ltd.'s financial performance in 2020 was less effective than in 2019 and below industry standards.

Individual Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Ratio calculation..........................................................................................................................3

Evaluation of ratio........................................................................................................................7

Ratio evaluation in comparison to the industry average..............................................................8

Additional information that can enhance the evaluation.............................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Ratio calculation..........................................................................................................................3

Evaluation of ratio........................................................................................................................7

Ratio evaluation in comparison to the industry average..............................................................8

Additional information that can enhance the evaluation.............................................................9

REFERENCES..............................................................................................................................10

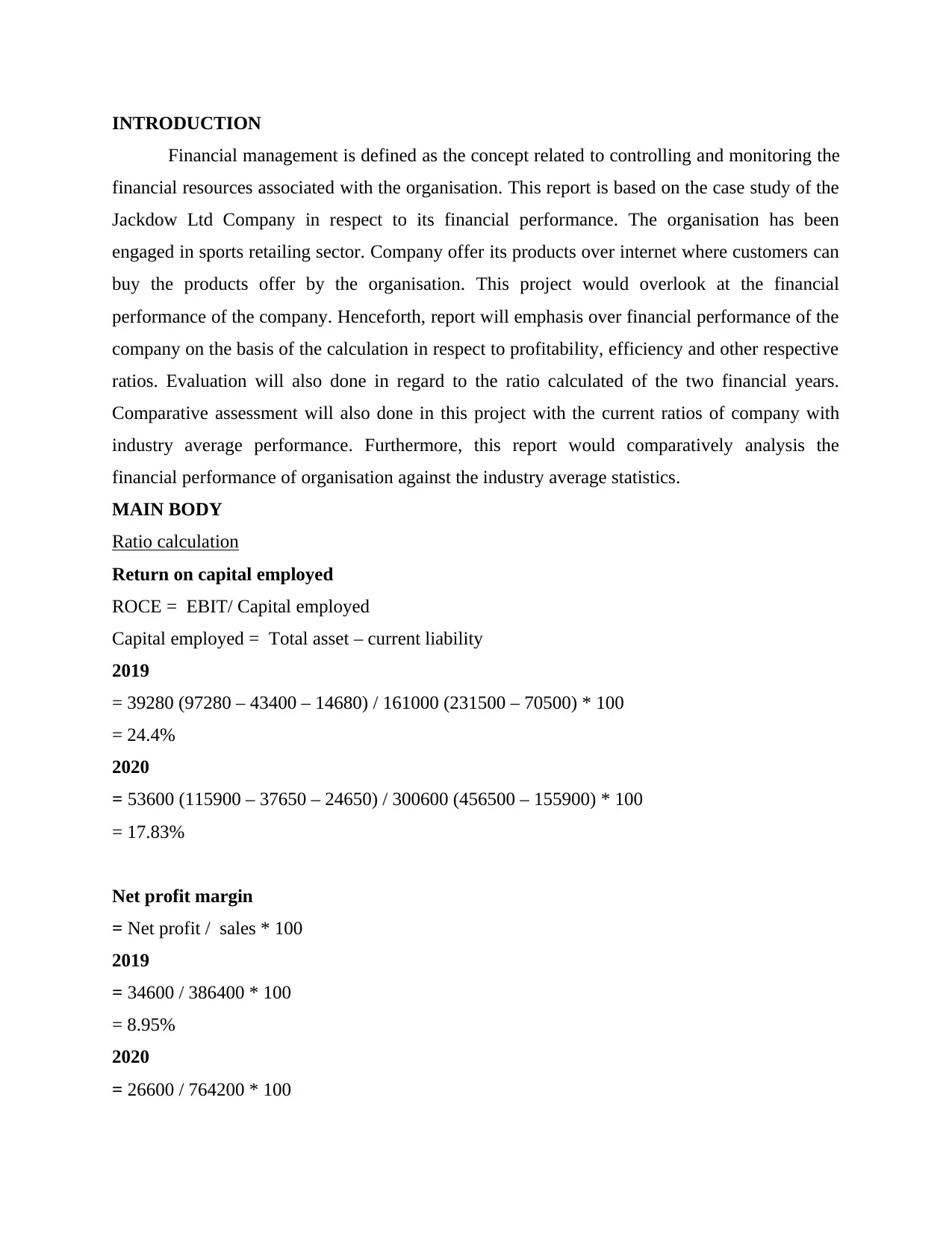

INTRODUCTION

Financial management is defined as the concept related to controlling and monitoring the

financial resources associated with the organisation. This report is based on the case study of the

Jackdow Ltd Company in respect to its financial performance. The organisation has been

engaged in sports retailing sector. Company offer its products over internet where customers can

buy the products offer by the organisation. This project would overlook at the financial

performance of the company. Henceforth, report will emphasis over financial performance of the

company on the basis of the calculation in respect to profitability, efficiency and other respective

ratios. Evaluation will also done in regard to the ratio calculated of the two financial years.

Comparative assessment will also done in this project with the current ratios of company with

industry average performance. Furthermore, this report would comparatively analysis the

financial performance of organisation against the industry average statistics.

MAIN BODY

Ratio calculation

Return on capital employed

ROCE = EBIT/ Capital employed

Capital employed = Total asset – current liability

2019

= 39280 (97280 – 43400 – 14680) / 161000 (231500 – 70500) * 100

= 24.4%

2020

= 53600 (115900 – 37650 – 24650) / 300600 (456500 – 155900) * 100

= 17.83%

Net profit margin

= Net profit / sales * 100

2019

= 34600 / 386400 * 100

= 8.95%

2020

= 26600 / 764200 * 100

Financial management is defined as the concept related to controlling and monitoring the

financial resources associated with the organisation. This report is based on the case study of the

Jackdow Ltd Company in respect to its financial performance. The organisation has been

engaged in sports retailing sector. Company offer its products over internet where customers can

buy the products offer by the organisation. This project would overlook at the financial

performance of the company. Henceforth, report will emphasis over financial performance of the

company on the basis of the calculation in respect to profitability, efficiency and other respective

ratios. Evaluation will also done in regard to the ratio calculated of the two financial years.

Comparative assessment will also done in this project with the current ratios of company with

industry average performance. Furthermore, this report would comparatively analysis the

financial performance of organisation against the industry average statistics.

MAIN BODY

Ratio calculation

Return on capital employed

ROCE = EBIT/ Capital employed

Capital employed = Total asset – current liability

2019

= 39280 (97280 – 43400 – 14680) / 161000 (231500 – 70500) * 100

= 24.4%

2020

= 53600 (115900 – 37650 – 24650) / 300600 (456500 – 155900) * 100

= 17.83%

Net profit margin

= Net profit / sales * 100

2019

= 34600 / 386400 * 100

= 8.95%

2020

= 26600 / 764200 * 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 3.48%

Gross profit margin

= Gross profit / sales * 100

2019

= 97280 / 386400 * 100

= 25.17%

2020

= 115900 / 764200 * 100

= 15.16%

Current ratio

= Current asset / current liability

2019

= 96500 / 70500

= 1.37

2020

= 144500 / 155900

= .93

Acid test ratio

= current asset – inventory / current liability

2019

= 96500 – 51200 / 70500

= .643

2020

= 144500 – 85300 / 155900

= .38

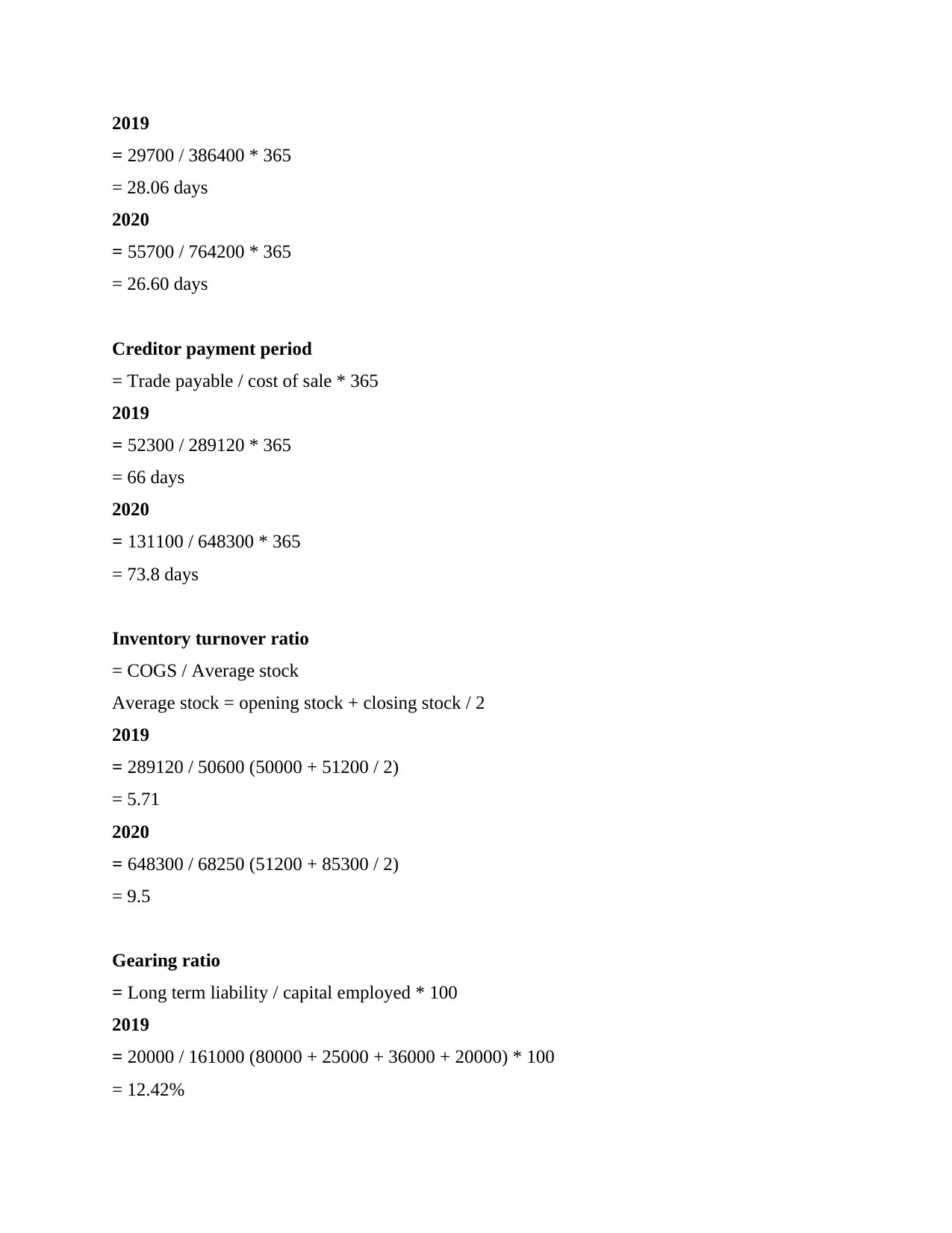

Debtor collection period

= Debtor / sales * 365

Gross profit margin

= Gross profit / sales * 100

2019

= 97280 / 386400 * 100

= 25.17%

2020

= 115900 / 764200 * 100

= 15.16%

Current ratio

= Current asset / current liability

2019

= 96500 / 70500

= 1.37

2020

= 144500 / 155900

= .93

Acid test ratio

= current asset – inventory / current liability

2019

= 96500 – 51200 / 70500

= .643

2020

= 144500 – 85300 / 155900

= .38

Debtor collection period

= Debtor / sales * 365

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2019

= 29700 / 386400 * 365

= 28.06 days

2020

= 55700 / 764200 * 365

= 26.60 days

Creditor payment period

= Trade payable / cost of sale * 365

2019

= 52300 / 289120 * 365

= 66 days

2020

= 131100 / 648300 * 365

= 73.8 days

Inventory turnover ratio

= COGS / Average stock

Average stock = opening stock + closing stock / 2

2019

= 289120 / 50600 (50000 + 51200 / 2)

= 5.71

2020

= 648300 / 68250 (51200 + 85300 / 2)

= 9.5

Gearing ratio

= Long term liability / capital employed * 100

2019

= 20000 / 161000 (80000 + 25000 + 36000 + 20000) * 100

= 12.42%

= 29700 / 386400 * 365

= 28.06 days

2020

= 55700 / 764200 * 365

= 26.60 days

Creditor payment period

= Trade payable / cost of sale * 365

2019

= 52300 / 289120 * 365

= 66 days

2020

= 131100 / 648300 * 365

= 73.8 days

Inventory turnover ratio

= COGS / Average stock

Average stock = opening stock + closing stock / 2

2019

= 289120 / 50600 (50000 + 51200 / 2)

= 5.71

2020

= 648300 / 68250 (51200 + 85300 / 2)

= 9.5

Gearing ratio

= Long term liability / capital employed * 100

2019

= 20000 / 161000 (80000 + 25000 + 36000 + 20000) * 100

= 12.42%

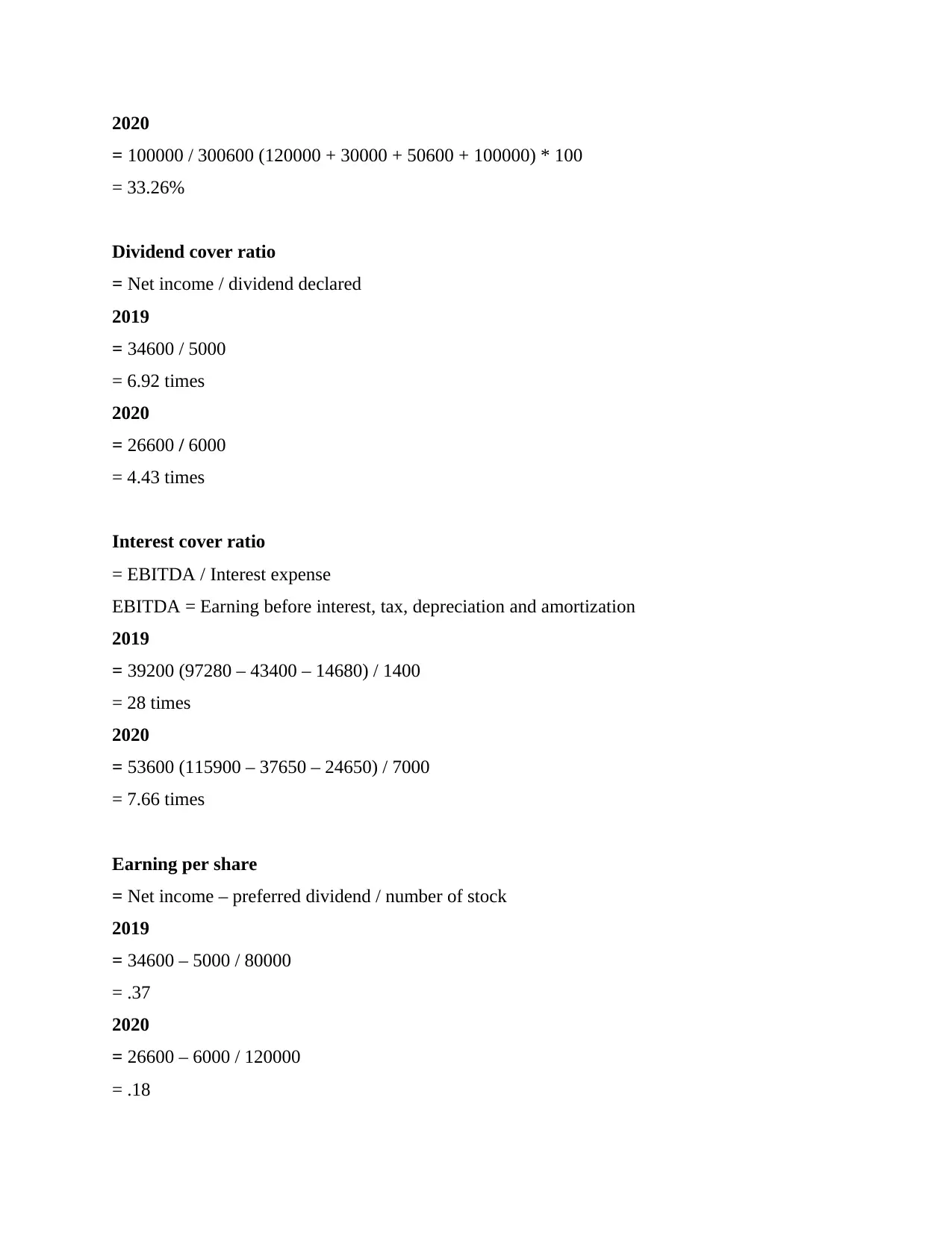

2020

= 100000 / 300600 (120000 + 30000 + 50600 + 100000) * 100

= 33.26%

Dividend cover ratio

= Net income / dividend declared

2019

= 34600 / 5000

= 6.92 times

2020

= 26600 / 6000

= 4.43 times

Interest cover ratio

= EBITDA / Interest expense

EBITDA = Earning before interest, tax, depreciation and amortization

2019

= 39200 (97280 – 43400 – 14680) / 1400

= 28 times

2020

= 53600 (115900 – 37650 – 24650) / 7000

= 7.66 times

Earning per share

= Net income – preferred dividend / number of stock

2019

= 34600 – 5000 / 80000

= .37

2020

= 26600 – 6000 / 120000

= .18

= 100000 / 300600 (120000 + 30000 + 50600 + 100000) * 100

= 33.26%

Dividend cover ratio

= Net income / dividend declared

2019

= 34600 / 5000

= 6.92 times

2020

= 26600 / 6000

= 4.43 times

Interest cover ratio

= EBITDA / Interest expense

EBITDA = Earning before interest, tax, depreciation and amortization

2019

= 39200 (97280 – 43400 – 14680) / 1400

= 28 times

2020

= 53600 (115900 – 37650 – 24650) / 7000

= 7.66 times

Earning per share

= Net income – preferred dividend / number of stock

2019

= 34600 – 5000 / 80000

= .37

2020

= 26600 – 6000 / 120000

= .18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

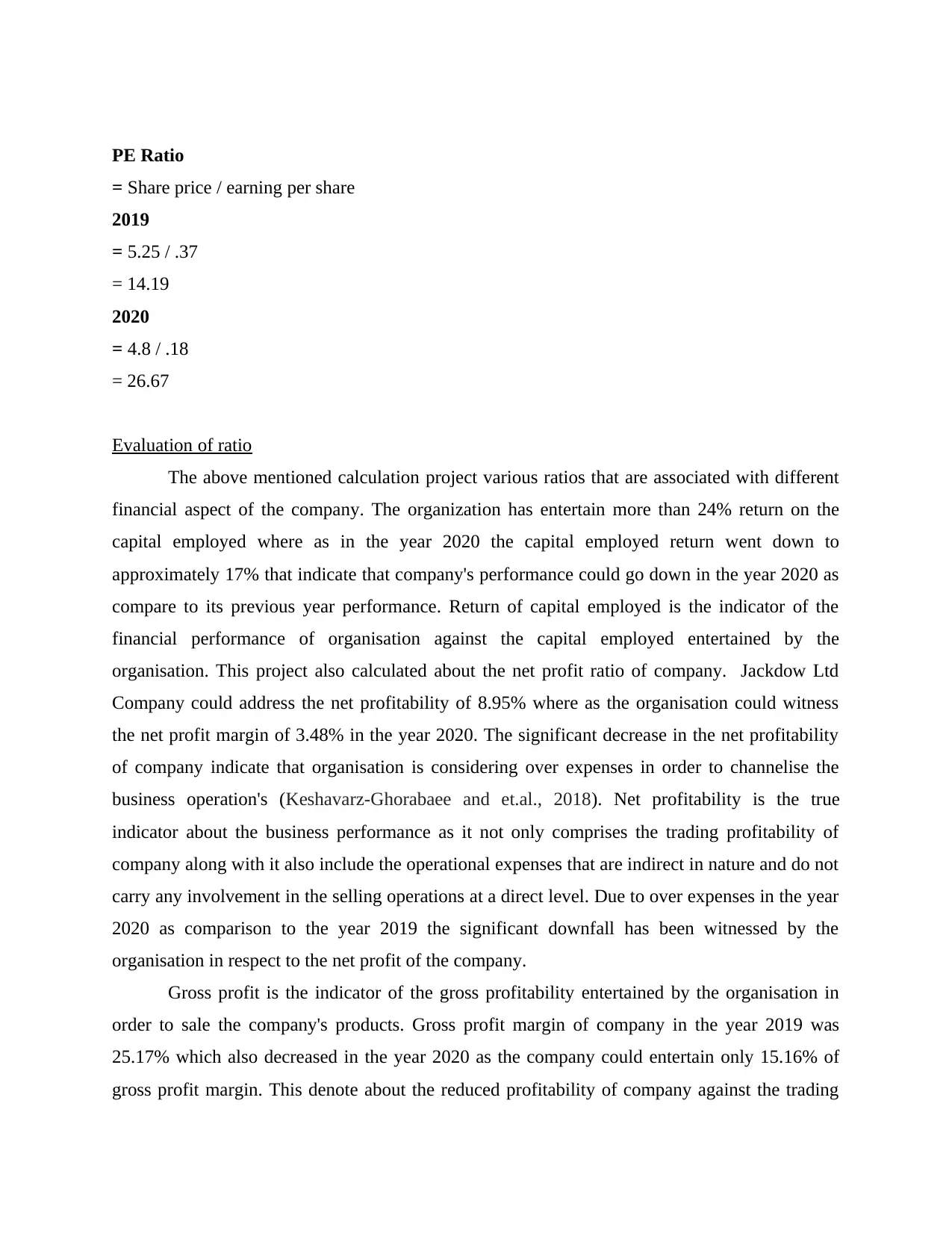

PE Ratio

= Share price / earning per share

2019

= 5.25 / .37

= 14.19

2020

= 4.8 / .18

= 26.67

Evaluation of ratio

The above mentioned calculation project various ratios that are associated with different

financial aspect of the company. The organization has entertain more than 24% return on the

capital employed where as in the year 2020 the capital employed return went down to

approximately 17% that indicate that company's performance could go down in the year 2020 as

compare to its previous year performance. Return of capital employed is the indicator of the

financial performance of organisation against the capital employed entertained by the

organisation. This project also calculated about the net profit ratio of company. Jackdow Ltd

Company could address the net profitability of 8.95% where as the organisation could witness

the net profit margin of 3.48% in the year 2020. The significant decrease in the net profitability

of company indicate that organisation is considering over expenses in order to channelise the

business operation's (Keshavarz-Ghorabaee and et.al., 2018). Net profitability is the true

indicator about the business performance as it not only comprises the trading profitability of

company along with it also include the operational expenses that are indirect in nature and do not

carry any involvement in the selling operations at a direct level. Due to over expenses in the year

2020 as comparison to the year 2019 the significant downfall has been witnessed by the

organisation in respect to the net profit of the company.

Gross profit is the indicator of the gross profitability entertained by the organisation in

order to sale the company's products. Gross profit margin of company in the year 2019 was

25.17% which also decreased in the year 2020 as the company could entertain only 15.16% of

gross profit margin. This denote about the reduced profitability of company against the trading

= Share price / earning per share

2019

= 5.25 / .37

= 14.19

2020

= 4.8 / .18

= 26.67

Evaluation of ratio

The above mentioned calculation project various ratios that are associated with different

financial aspect of the company. The organization has entertain more than 24% return on the

capital employed where as in the year 2020 the capital employed return went down to

approximately 17% that indicate that company's performance could go down in the year 2020 as

compare to its previous year performance. Return of capital employed is the indicator of the

financial performance of organisation against the capital employed entertained by the

organisation. This project also calculated about the net profit ratio of company. Jackdow Ltd

Company could address the net profitability of 8.95% where as the organisation could witness

the net profit margin of 3.48% in the year 2020. The significant decrease in the net profitability

of company indicate that organisation is considering over expenses in order to channelise the

business operation's (Keshavarz-Ghorabaee and et.al., 2018). Net profitability is the true

indicator about the business performance as it not only comprises the trading profitability of

company along with it also include the operational expenses that are indirect in nature and do not

carry any involvement in the selling operations at a direct level. Due to over expenses in the year

2020 as comparison to the year 2019 the significant downfall has been witnessed by the

organisation in respect to the net profit of the company.

Gross profit is the indicator of the gross profitability entertained by the organisation in

order to sale the company's products. Gross profit margin of company in the year 2019 was

25.17% which also decreased in the year 2020 as the company could entertain only 15.16% of

gross profit margin. This denote about the reduced profitability of company against the trading

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

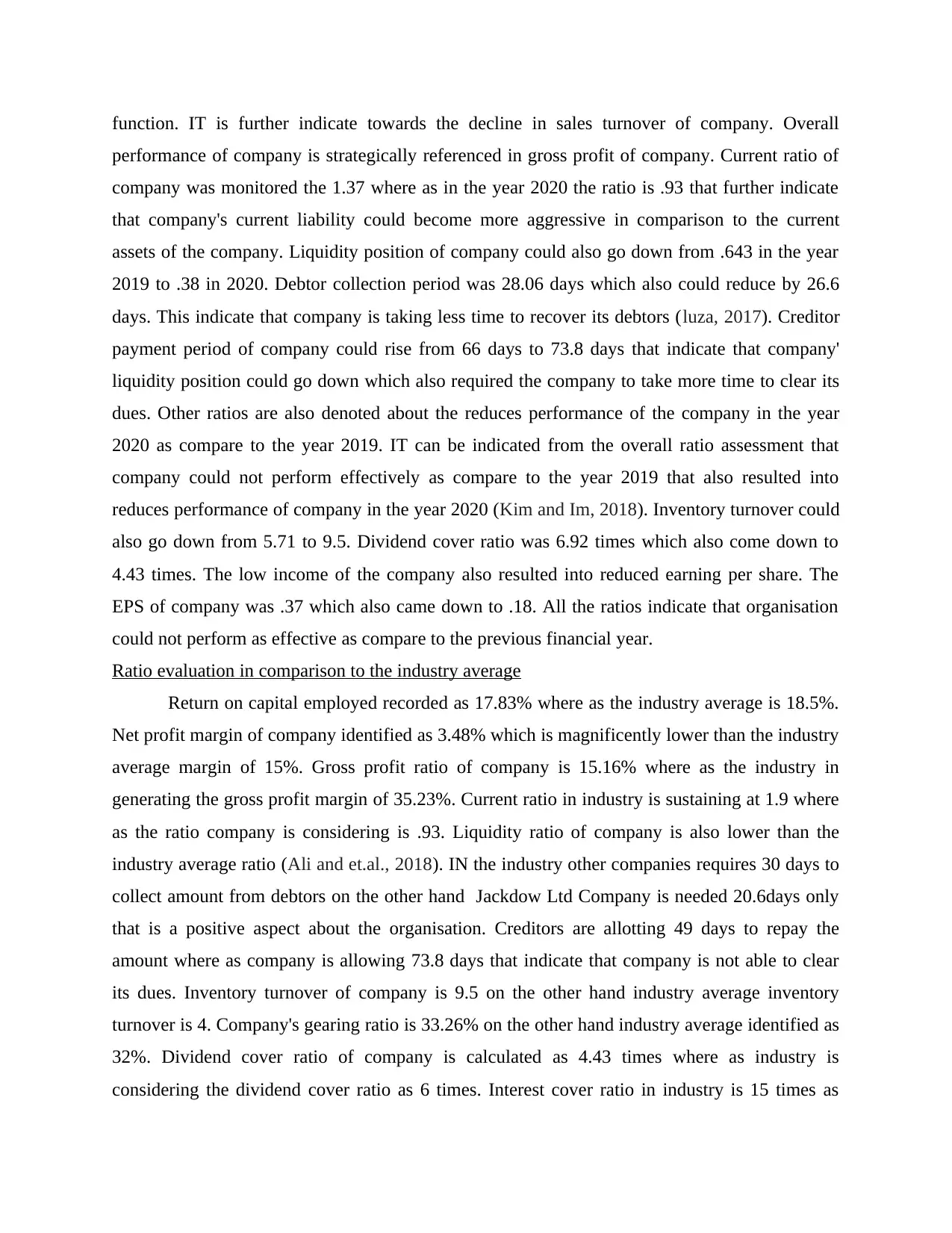

function. IT is further indicate towards the decline in sales turnover of company. Overall

performance of company is strategically referenced in gross profit of company. Current ratio of

company was monitored the 1.37 where as in the year 2020 the ratio is .93 that further indicate

that company's current liability could become more aggressive in comparison to the current

assets of the company. Liquidity position of company could also go down from .643 in the year

2019 to .38 in 2020. Debtor collection period was 28.06 days which also could reduce by 26.6

days. This indicate that company is taking less time to recover its debtors (luza, 2017). Creditor

payment period of company could rise from 66 days to 73.8 days that indicate that company'

liquidity position could go down which also required the company to take more time to clear its

dues. Other ratios are also denoted about the reduces performance of the company in the year

2020 as compare to the year 2019. IT can be indicated from the overall ratio assessment that

company could not perform effectively as compare to the year 2019 that also resulted into

reduces performance of company in the year 2020 (Kim and Im, 2018). Inventory turnover could

also go down from 5.71 to 9.5. Dividend cover ratio was 6.92 times which also come down to

4.43 times. The low income of the company also resulted into reduced earning per share. The

EPS of company was .37 which also came down to .18. All the ratios indicate that organisation

could not perform as effective as compare to the previous financial year.

Ratio evaluation in comparison to the industry average

Return on capital employed recorded as 17.83% where as the industry average is 18.5%.

Net profit margin of company identified as 3.48% which is magnificently lower than the industry

average margin of 15%. Gross profit ratio of company is 15.16% where as the industry in

generating the gross profit margin of 35.23%. Current ratio in industry is sustaining at 1.9 where

as the ratio company is considering is .93. Liquidity ratio of company is also lower than the

industry average ratio (Ali and et.al., 2018). IN the industry other companies requires 30 days to

collect amount from debtors on the other hand Jackdow Ltd Company is needed 20.6days only

that is a positive aspect about the organisation. Creditors are allotting 49 days to repay the

amount where as company is allowing 73.8 days that indicate that company is not able to clear

its dues. Inventory turnover of company is 9.5 on the other hand industry average inventory

turnover is 4. Company's gearing ratio is 33.26% on the other hand industry average identified as

32%. Dividend cover ratio of company is calculated as 4.43 times where as industry is

considering the dividend cover ratio as 6 times. Interest cover ratio in industry is 15 times as

performance of company is strategically referenced in gross profit of company. Current ratio of

company was monitored the 1.37 where as in the year 2020 the ratio is .93 that further indicate

that company's current liability could become more aggressive in comparison to the current

assets of the company. Liquidity position of company could also go down from .643 in the year

2019 to .38 in 2020. Debtor collection period was 28.06 days which also could reduce by 26.6

days. This indicate that company is taking less time to recover its debtors (luza, 2017). Creditor

payment period of company could rise from 66 days to 73.8 days that indicate that company'

liquidity position could go down which also required the company to take more time to clear its

dues. Other ratios are also denoted about the reduces performance of the company in the year

2020 as compare to the year 2019. IT can be indicated from the overall ratio assessment that

company could not perform effectively as compare to the year 2019 that also resulted into

reduces performance of company in the year 2020 (Kim and Im, 2018). Inventory turnover could

also go down from 5.71 to 9.5. Dividend cover ratio was 6.92 times which also come down to

4.43 times. The low income of the company also resulted into reduced earning per share. The

EPS of company was .37 which also came down to .18. All the ratios indicate that organisation

could not perform as effective as compare to the previous financial year.

Ratio evaluation in comparison to the industry average

Return on capital employed recorded as 17.83% where as the industry average is 18.5%.

Net profit margin of company identified as 3.48% which is magnificently lower than the industry

average margin of 15%. Gross profit ratio of company is 15.16% where as the industry in

generating the gross profit margin of 35.23%. Current ratio in industry is sustaining at 1.9 where

as the ratio company is considering is .93. Liquidity ratio of company is also lower than the

industry average ratio (Ali and et.al., 2018). IN the industry other companies requires 30 days to

collect amount from debtors on the other hand Jackdow Ltd Company is needed 20.6days only

that is a positive aspect about the organisation. Creditors are allotting 49 days to repay the

amount where as company is allowing 73.8 days that indicate that company is not able to clear

its dues. Inventory turnover of company is 9.5 on the other hand industry average inventory

turnover is 4. Company's gearing ratio is 33.26% on the other hand industry average identified as

32%. Dividend cover ratio of company is calculated as 4.43 times where as industry is

considering the dividend cover ratio as 6 times. Interest cover ratio in industry is 15 times as

compare to the company's own average as 7.66 times. Company could generate earning per share

is .18 where as the industry average is .36. PE Ratio of the industry is 26 and of the company is

26.67. All the above figures denote that company is not able to perform as effective as other

companies operating in the same industry (Caudron and et.al., 2018).

Ratio analysis Usefulness and limitation

Usefulness: Ratio analysis is used as a powerful tool of financial analysis. It shows the

numerical or quantitative relationship between figures of financial statement to know the strength

and weakness of the firm and knows the current financial position performance (Bednarek,

2016). Followings are the advantages of the Ratio analysis:

Forecasting and planning: computing ratio analysis of change in cost, sales, profits and

other facts by taking last few financial year of the company. This help the company to

forecast and plan the current year activities (Nurkasheva, and et.al., 2020).

Budgeting: Budgets are prepared for the various department by the helps of ratio

analysis. For example sales budget is prepared on the basis of past sales.

Cost effective: ratio analysis maintain the cost and performance of different division for

the company by analysing the previous financial data.

Inter firm comparison: it shows the efficiency and inefficiency of the two different firm

that can be compared and measured to improve the performance of the firm.

Operation efficiency: Efficiency of management and utilization of asset are indicated by

ratio analysis. Proper utilization of assets results in solvency of the firm depend on the

sales revenue (Chalu, Lubawa, 2018).

Limitations

Limitation of financial statement: Ratio are analysis which are recorded in the financial

statement but this statement can be suffered from numbers limits and may affect the

quality of analysis and the ratio analysis cannot become fully trusted.

Historical information: financial statements are the historical information which don no

reflect the current condition of the firm and is not useful to predict the future and analysis

the future condition occur in the company.

Different accounting policies: Two different firms carries different accounting policies

regarding valuation of inventories, charging depreciation make the data and accounting

ratio create differences and non comparable between the two companies.

is .18 where as the industry average is .36. PE Ratio of the industry is 26 and of the company is

26.67. All the above figures denote that company is not able to perform as effective as other

companies operating in the same industry (Caudron and et.al., 2018).

Ratio analysis Usefulness and limitation

Usefulness: Ratio analysis is used as a powerful tool of financial analysis. It shows the

numerical or quantitative relationship between figures of financial statement to know the strength

and weakness of the firm and knows the current financial position performance (Bednarek,

2016). Followings are the advantages of the Ratio analysis:

Forecasting and planning: computing ratio analysis of change in cost, sales, profits and

other facts by taking last few financial year of the company. This help the company to

forecast and plan the current year activities (Nurkasheva, and et.al., 2020).

Budgeting: Budgets are prepared for the various department by the helps of ratio

analysis. For example sales budget is prepared on the basis of past sales.

Cost effective: ratio analysis maintain the cost and performance of different division for

the company by analysing the previous financial data.

Inter firm comparison: it shows the efficiency and inefficiency of the two different firm

that can be compared and measured to improve the performance of the firm.

Operation efficiency: Efficiency of management and utilization of asset are indicated by

ratio analysis. Proper utilization of assets results in solvency of the firm depend on the

sales revenue (Chalu, Lubawa, 2018).

Limitations

Limitation of financial statement: Ratio are analysis which are recorded in the financial

statement but this statement can be suffered from numbers limits and may affect the

quality of analysis and the ratio analysis cannot become fully trusted.

Historical information: financial statements are the historical information which don no

reflect the current condition of the firm and is not useful to predict the future and analysis

the future condition occur in the company.

Different accounting policies: Two different firms carries different accounting policies

regarding valuation of inventories, charging depreciation make the data and accounting

ratio create differences and non comparable between the two companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lack of standard of comparison: there is no fix standard of comparison of the ratios.

For an instance current ratio is said to be ideal if current assets are twice of current

liabilities. But this is not an ideal comparison between the two as there may be different

scenario with the firms. So it can be said that if the current assets is slightly more than

current liabilities than it may be perfect (Lamprecht, and Guetterman, 2019).

Quantitative analysis: ratios are based on the quantitative analysis only and qualitative

factors are ignored while calculating the ratios.

Additional information that can enhance the evaluation

The above calculated ratios are enough to assess about the financial performance of the

company. There are plenty of other ratios also available that can be calculated like asset turnover

ratio and many such ratios that also evaluate the overall performance of company in different

manner (Murphy and et.al.,2016). IT can be indicated that company's liquidity position is not

much effective that also influence the ability of the organisation to clear its dues. Company is

taking moire time to clear its creditors that is challenging to the brand value of company which

further affect the performance of the organisation.

CONCLUSION

This report analysis the performance of the company for the financial year 2019-2020. Which

shows the performance of 2019 is much better than performance in financial year 2020. Whereas

compare to industry standard the company also not perform above the standard.

Recommendation: the company should control their indirect expenses which result in

better performance and net profit increased. Whereas the company should focus on their

increasing current asset and control the current liabilities which improve the current ratio of the

company.

For an instance current ratio is said to be ideal if current assets are twice of current

liabilities. But this is not an ideal comparison between the two as there may be different

scenario with the firms. So it can be said that if the current assets is slightly more than

current liabilities than it may be perfect (Lamprecht, and Guetterman, 2019).

Quantitative analysis: ratios are based on the quantitative analysis only and qualitative

factors are ignored while calculating the ratios.

Additional information that can enhance the evaluation

The above calculated ratios are enough to assess about the financial performance of the

company. There are plenty of other ratios also available that can be calculated like asset turnover

ratio and many such ratios that also evaluate the overall performance of company in different

manner (Murphy and et.al.,2016). IT can be indicated that company's liquidity position is not

much effective that also influence the ability of the organisation to clear its dues. Company is

taking moire time to clear its creditors that is challenging to the brand value of company which

further affect the performance of the organisation.

CONCLUSION

This report analysis the performance of the company for the financial year 2019-2020. Which

shows the performance of 2019 is much better than performance in financial year 2020. Whereas

compare to industry standard the company also not perform above the standard.

Recommendation: the company should control their indirect expenses which result in

better performance and net profit increased. Whereas the company should focus on their

increasing current asset and control the current liabilities which improve the current ratio of the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ali, M. S. and et.al., 2018. Channel estimation and peak-to-average power ratio analysis of

narrowband internet of things uplink systems. Wireless Communications and Mobile

Computing, 2018.

Bednarek, P., 2016. Evaluating the usefulness of quantitative methods as analytical auditing

procedures. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu. (434). pp.9-

18.

Caudron, C. and et.al., 2018. Seismic Amplitude Ratio Analysis of the 2014–2015 Bár arbunga‐

Holuhraun Dike Propagation and Eruption. Journal of Geophysical Research: Solid

Earth. 123(1). pp.264-276.

Chalu, H. and Lubawa, G., 2018. Using financial statements to analyze the effects of multiple

Borrowings on SMEs financial performance in Tanzania. Inter. J. Res. Methodol. Soc.

Sci. 1(4). pp.87-107.

Keshavarz-Ghorabaee, M. and et.al., 2018. An extended step-wise weight assessment ratio

analysis with symmetric interval type-2 fuzzy sets for determining the subjective

weights of criteria in multi-criteria decision-making problems. Symmetry.10(4). p.91.

Kim, D. and Im, M., 2018. What makes red quasars red?-Observational evidence for dust

extinction from line ratio analysis. Astronomy & Astrophysics. 610. p.A31.

Kluza, K., 2017. Risk assessment of the local government sector based on the ratio analysis and

the DEA method. Evidence from Poland. Eurasian Economic Review. 7(3). pp.329-351.

Lamprecht, C. and Guetterman, T.C., 2019. Mixed methods in accounting: a field based

analysis. Meditari Accountancy Research.

Murphy, E. K. and et.al.,2016. Signal-to-noise ratio analysis of a phase-sensitive voltmeter for

electrical impedance tomography. IEEE transactions on biomedical circuits and

systems. 11(2). pp.360-369.

Nurkasheva, N., and et.al., 2020. Current Issues of Accounting and Evaluation of Financial

Instruments in Accordance with International Financial Reporting Standards. Journal of

Talent Development and Excellence. 12(1). pp. 6026-6033.

Books and Journals

Ali, M. S. and et.al., 2018. Channel estimation and peak-to-average power ratio analysis of

narrowband internet of things uplink systems. Wireless Communications and Mobile

Computing, 2018.

Bednarek, P., 2016. Evaluating the usefulness of quantitative methods as analytical auditing

procedures. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu. (434). pp.9-

18.

Caudron, C. and et.al., 2018. Seismic Amplitude Ratio Analysis of the 2014–2015 Bár arbunga‐

Holuhraun Dike Propagation and Eruption. Journal of Geophysical Research: Solid

Earth. 123(1). pp.264-276.

Chalu, H. and Lubawa, G., 2018. Using financial statements to analyze the effects of multiple

Borrowings on SMEs financial performance in Tanzania. Inter. J. Res. Methodol. Soc.

Sci. 1(4). pp.87-107.

Keshavarz-Ghorabaee, M. and et.al., 2018. An extended step-wise weight assessment ratio

analysis with symmetric interval type-2 fuzzy sets for determining the subjective

weights of criteria in multi-criteria decision-making problems. Symmetry.10(4). p.91.

Kim, D. and Im, M., 2018. What makes red quasars red?-Observational evidence for dust

extinction from line ratio analysis. Astronomy & Astrophysics. 610. p.A31.

Kluza, K., 2017. Risk assessment of the local government sector based on the ratio analysis and

the DEA method. Evidence from Poland. Eurasian Economic Review. 7(3). pp.329-351.

Lamprecht, C. and Guetterman, T.C., 2019. Mixed methods in accounting: a field based

analysis. Meditari Accountancy Research.

Murphy, E. K. and et.al.,2016. Signal-to-noise ratio analysis of a phase-sensitive voltmeter for

electrical impedance tomography. IEEE transactions on biomedical circuits and

systems. 11(2). pp.360-369.

Nurkasheva, N., and et.al., 2020. Current Issues of Accounting and Evaluation of Financial

Instruments in Accordance with International Financial Reporting Standards. Journal of

Talent Development and Excellence. 12(1). pp. 6026-6033.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.