Benefits of IFRS Adoption

VerifiedAdded on 2023/03/31

|9

|1845

|374

AI Summary

This article discusses the benefits of adopting International Financial Reporting Standards (IFRS) for companies. It covers the increased comparability with other international firms, improved accounting quality, and access to capital from external sources. The adoption of IFRS helps companies attract investors, expand globally, and reduce perceived corruption. It also provides opportunities for professionals in finance and opens up career prospects. Overall, adopting IFRS can give companies a competitive edge in the global market.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INDUSTRY ENGAGEMENT 1

Industry Engagement

Author’s Name

Institutional Affiliation

Professor’s Name

Course

City and State

Date

Industry Engagement

Author’s Name

Institutional Affiliation

Professor’s Name

Course

City and State

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INDUSTRY ENGAGEMENT 2

Industry Engagement

Introduction

International Financial Reporting Standards basically known as IFRS are the set rules that

ensure financial statements are equal in all parts of the world. The International Accounting

standard board issue out financial reporting standards which should be applied in making of

financial statements. IFRS encompasses several accounting activities like, the statement of

financial position, statement of changes in equity, statement of cash flow and statement of

comprehensive income. The International Accounting Standard Board ensures that the set rules

are transparent, reliable and similar round the globe. Furthermore, they govern how companies

should control their accounting hence coming up with a consistent language in accounting and

statements hence guiding investors in making financial decisions.

Theoretical Review

The theory of cost principle focuses on recording of asset as required. Also, the asset can

be depreciated overtime depending on the kind of asset (Oulasvirta, 2016, p 8). Some may be

depreciated as long for 30 years while the others can be depreciated depending on the estimated

economic life. The depreciated is guided by the accounting standards used by the country.

Therefore, the theory is relevant since IFRS give international presentation of depreciations of

assets so that they can be comparable to other international companies. Further, the multinational

companies need to have a uniform presentation of financial report that can make it easier to

determine asset acquisition and depreciation across all the branches.

According to the theory of institution, it explores the resilient aspects of social structure

(Lok, 2017, p.22). Companies need to be organized and changed until they become stable.

Industry Engagement

Introduction

International Financial Reporting Standards basically known as IFRS are the set rules that

ensure financial statements are equal in all parts of the world. The International Accounting

standard board issue out financial reporting standards which should be applied in making of

financial statements. IFRS encompasses several accounting activities like, the statement of

financial position, statement of changes in equity, statement of cash flow and statement of

comprehensive income. The International Accounting Standard Board ensures that the set rules

are transparent, reliable and similar round the globe. Furthermore, they govern how companies

should control their accounting hence coming up with a consistent language in accounting and

statements hence guiding investors in making financial decisions.

Theoretical Review

The theory of cost principle focuses on recording of asset as required. Also, the asset can

be depreciated overtime depending on the kind of asset (Oulasvirta, 2016, p 8). Some may be

depreciated as long for 30 years while the others can be depreciated depending on the estimated

economic life. The depreciated is guided by the accounting standards used by the country.

Therefore, the theory is relevant since IFRS give international presentation of depreciations of

assets so that they can be comparable to other international companies. Further, the multinational

companies need to have a uniform presentation of financial report that can make it easier to

determine asset acquisition and depreciation across all the branches.

According to the theory of institution, it explores the resilient aspects of social structure

(Lok, 2017, p.22). Companies need to be organized and changed until they become stable.

INDUSTRY ENGAGEMENT 3

Processes like norms, rules, and routine are established to guide social behavior. The adoption of

IFRS is in line with the theory, since it a process that makes the organization more stable ad able

to compete adequately with other firms. The change of organization through the adoption of a

ruled based accounting standard help the company to position itself in a batter place both locally

and internationally.

The agency theory is also relevant in the adoption of new accounting standards since it is

expensively employed to predict and explain performance of external auditor (Mihret and Grant,

2017, p.703). The theory is used to settle the issues that arise between the principals and those

they have entrusted to run the business. According to the theory it suggests that the agent need to

act in the best interest of the principal. The theory directs on how the auditing should be done

and also predicts the internal auditor’s function and responsibility. It provides a theoretical

framework on how the adoption of IFRS can benefit the agents by placing the company in a

more competitive edge compared to using other accounting standards. It is necessary to use the

globally accepted accounting reports so that it can help in expansion of the business which works

for the best interest of the owners

Opportunity

The IFRS provides a company with opportunities that makes it better to compete locally

and internationally. Adoption of IFRS increases the chance of cross-border listing which comes

with increased demand of the products in the international market. So the company can exploit

the opportunity by gathering the available resources to avail the products to global customers.

Additionally, the company can expand through subsidiary development into other countries to

exploit the opportunity.

Processes like norms, rules, and routine are established to guide social behavior. The adoption of

IFRS is in line with the theory, since it a process that makes the organization more stable ad able

to compete adequately with other firms. The change of organization through the adoption of a

ruled based accounting standard help the company to position itself in a batter place both locally

and internationally.

The agency theory is also relevant in the adoption of new accounting standards since it is

expensively employed to predict and explain performance of external auditor (Mihret and Grant,

2017, p.703). The theory is used to settle the issues that arise between the principals and those

they have entrusted to run the business. According to the theory it suggests that the agent need to

act in the best interest of the principal. The theory directs on how the auditing should be done

and also predicts the internal auditor’s function and responsibility. It provides a theoretical

framework on how the adoption of IFRS can benefit the agents by placing the company in a

more competitive edge compared to using other accounting standards. It is necessary to use the

globally accepted accounting reports so that it can help in expansion of the business which works

for the best interest of the owners

Opportunity

The IFRS provides a company with opportunities that makes it better to compete locally

and internationally. Adoption of IFRS increases the chance of cross-border listing which comes

with increased demand of the products in the international market. So the company can exploit

the opportunity by gathering the available resources to avail the products to global customers.

Additionally, the company can expand through subsidiary development into other countries to

exploit the opportunity.

INDUSTRY ENGAGEMENT 4

There is a drastic growth in the demand of professionals who are well versed with IFRS.

Many countries and companies across the world are adopting the international standard of

accounting. Furthermore, professionals in finance who long to exceed in their careers should

look into taking the IFRS certificate so that to improve their career prospects. Banks and

insurance companies are demanding for IFRS professionals. On the other hand, many non-

financial companies have slowly adopted IFRS. Audit companies also have a higher need of

hiring consultants with IFRS certificate. It is also beneficial to IFRS experts because they have

the ability to start consultancy firms which they control. Lastly, professionals of IFRS have the

opportunity to be given the role of training in the finance education.

Benefits

Increased comparability

According to Null, 2016 (p. 1203) the firms that have adopted the use of International

Financial Reporting System increased the level of comparability with other international firms.

The purpose of the study was to build a greater understanding on the transitioning from GAAP to

IFRS. Further it explored the several literatures and assembled issues of corporate governance

and how it effectively helps in the adoption of IFRS.

Ramesh (2019, p. 3) carried out a study that focused investigating the perception of IFRS

adoption by organisation. The firs need a sense of uniformity in accounting standards to make it

easier to compare with other international organisation. The benefit of comparability helps to

attract investors both in the local market and external market. Therefore, ability to compare the

financial reports it list the firm in cross border making a company able have a competitive

advantage compared to those firms that have not adopted. According to Das and Saha (2017, p.

There is a drastic growth in the demand of professionals who are well versed with IFRS.

Many countries and companies across the world are adopting the international standard of

accounting. Furthermore, professionals in finance who long to exceed in their careers should

look into taking the IFRS certificate so that to improve their career prospects. Banks and

insurance companies are demanding for IFRS professionals. On the other hand, many non-

financial companies have slowly adopted IFRS. Audit companies also have a higher need of

hiring consultants with IFRS certificate. It is also beneficial to IFRS experts because they have

the ability to start consultancy firms which they control. Lastly, professionals of IFRS have the

opportunity to be given the role of training in the finance education.

Benefits

Increased comparability

According to Null, 2016 (p. 1203) the firms that have adopted the use of International

Financial Reporting System increased the level of comparability with other international firms.

The purpose of the study was to build a greater understanding on the transitioning from GAAP to

IFRS. Further it explored the several literatures and assembled issues of corporate governance

and how it effectively helps in the adoption of IFRS.

Ramesh (2019, p. 3) carried out a study that focused investigating the perception of IFRS

adoption by organisation. The firs need a sense of uniformity in accounting standards to make it

easier to compare with other international organisation. The benefit of comparability helps to

attract investors both in the local market and external market. Therefore, ability to compare the

financial reports it list the firm in cross border making a company able have a competitive

advantage compared to those firms that have not adopted. According to Das and Saha (2017, p.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INDUSTRY ENGAGEMENT 5

21) in Indian firms were forced to adopt IFRS, in order to meet agent demands and facilitate

international practices. Therefore, it helps the firm to integrate in the global market. Through

international accounting practices from an investor point of view, they can be able to compare

performance with others in the international level. So it is clear that the investor have high trust

for firms that use IFRS due to ability of comparing different performance. In the event, that the

firm tey use local accounting report standard, they become least attractive to investors.

Improved quality

Christensen, Lee, Walker and Zeng, (2015, p.45) conducted a research to examine the

managerial financial reporting incentives and found out that adoption of IFRS increased

accounting quality. Through a single-country setting in Germany showed that although it was

voluntary to adopt the accounting report but due the benefits it was becoming mandatory for

organizations. The quality of IFRS, was assessed through multiple constructs like earnings

management, time loss recognition and value relevance. All the identified constructs adds up to

the quality of the IFRS. As a result, it makes the firm to be more competitive since people are

likely to trust firms that use such kind of reporting method. Further, it reduces the chances that

the management can interfere with the true value of the reports.

Vidal-García, and Vidal (2016, p 39) focused a research on IFRS and how it has resulted

to increased Foreign Direct Investment. The research showed that companies that have adopted

IFRS have been able to invest directly in countries that are non-IFRS reporting. From the study it

also highlights develop ability of the firm to be listed across border, they are able to invest in

other countries for growth and expansion. They are seen with the ability to provide quality

services to the countries that they invest in.

21) in Indian firms were forced to adopt IFRS, in order to meet agent demands and facilitate

international practices. Therefore, it helps the firm to integrate in the global market. Through

international accounting practices from an investor point of view, they can be able to compare

performance with others in the international level. So it is clear that the investor have high trust

for firms that use IFRS due to ability of comparing different performance. In the event, that the

firm tey use local accounting report standard, they become least attractive to investors.

Improved quality

Christensen, Lee, Walker and Zeng, (2015, p.45) conducted a research to examine the

managerial financial reporting incentives and found out that adoption of IFRS increased

accounting quality. Through a single-country setting in Germany showed that although it was

voluntary to adopt the accounting report but due the benefits it was becoming mandatory for

organizations. The quality of IFRS, was assessed through multiple constructs like earnings

management, time loss recognition and value relevance. All the identified constructs adds up to

the quality of the IFRS. As a result, it makes the firm to be more competitive since people are

likely to trust firms that use such kind of reporting method. Further, it reduces the chances that

the management can interfere with the true value of the reports.

Vidal-García, and Vidal (2016, p 39) focused a research on IFRS and how it has resulted

to increased Foreign Direct Investment. The research showed that companies that have adopted

IFRS have been able to invest directly in countries that are non-IFRS reporting. From the study it

also highlights develop ability of the firm to be listed across border, they are able to invest in

other countries for growth and expansion. They are seen with the ability to provide quality

services to the countries that they invest in.

INDUSTRY ENGAGEMENT 6

According to a study conducted by Houqe and Monem (2016, p.365), it was found that

IFRS reporting reduces perceived corruption both in developed and developing countries. There

is great significance in the use of IFRS since the investors and stakeholders perceive the firm as

less corrupt. Moreover, there is ability to control effects of political effects and economic

development. Having considered a sample of 104 countries for the study, then there is increased

reliability on the results. Ability to reduce political influence, economic development of a

country and corruption, they adds up to the improved quality of the inacail reports. Therefore, it

benefits the firm through increased loyalty from the customers and also attracts more market to

the company.

Access to capital

Bassemir (2018, p. 257) investigated why private firms consider adopting the IFRS. The

research showed that they adopt the report system due to their financing needs. Though there was

limited financial data of the private organisation, the researcher was able to identify that private

firms have higher chances of expansion and growth. To finance such objectives they seek for

external funds from financial institutions to finance the objectives. So, the firms that have

adopted the IFRS, the lenders can be able compare the financial reports with other firms to

understand they capability to repay debts. So, a company can be able to access capital to expand

and grow in the international market which can be able to be competitive due to economies of

scale.

Nurunnabi’s (2018, p.172) study aimed to evaluate the perceived costs and benefits

associated with IFRS and identified the ability to access funds externally. Through interviews

done with stakeholders in Saudi Arabia there are challenges of lack of qualified staffs in the

According to a study conducted by Houqe and Monem (2016, p.365), it was found that

IFRS reporting reduces perceived corruption both in developed and developing countries. There

is great significance in the use of IFRS since the investors and stakeholders perceive the firm as

less corrupt. Moreover, there is ability to control effects of political effects and economic

development. Having considered a sample of 104 countries for the study, then there is increased

reliability on the results. Ability to reduce political influence, economic development of a

country and corruption, they adds up to the improved quality of the inacail reports. Therefore, it

benefits the firm through increased loyalty from the customers and also attracts more market to

the company.

Access to capital

Bassemir (2018, p. 257) investigated why private firms consider adopting the IFRS. The

research showed that they adopt the report system due to their financing needs. Though there was

limited financial data of the private organisation, the researcher was able to identify that private

firms have higher chances of expansion and growth. To finance such objectives they seek for

external funds from financial institutions to finance the objectives. So, the firms that have

adopted the IFRS, the lenders can be able compare the financial reports with other firms to

understand they capability to repay debts. So, a company can be able to access capital to expand

and grow in the international market which can be able to be competitive due to economies of

scale.

Nurunnabi’s (2018, p.172) study aimed to evaluate the perceived costs and benefits

associated with IFRS and identified the ability to access funds externally. Through interviews

done with stakeholders in Saudi Arabia there are challenges of lack of qualified staffs in the

INDUSTRY ENGAGEMENT 7

country. In addition, Mo and Lee (2018, p. 2545) study shows that both public and private firm

chose to adopt IRS so that they can be able to access financial markets. The lenders trust on the

financial statements reported using IFRS and they will provide funds to them compared to other

firms using different reporting standards.

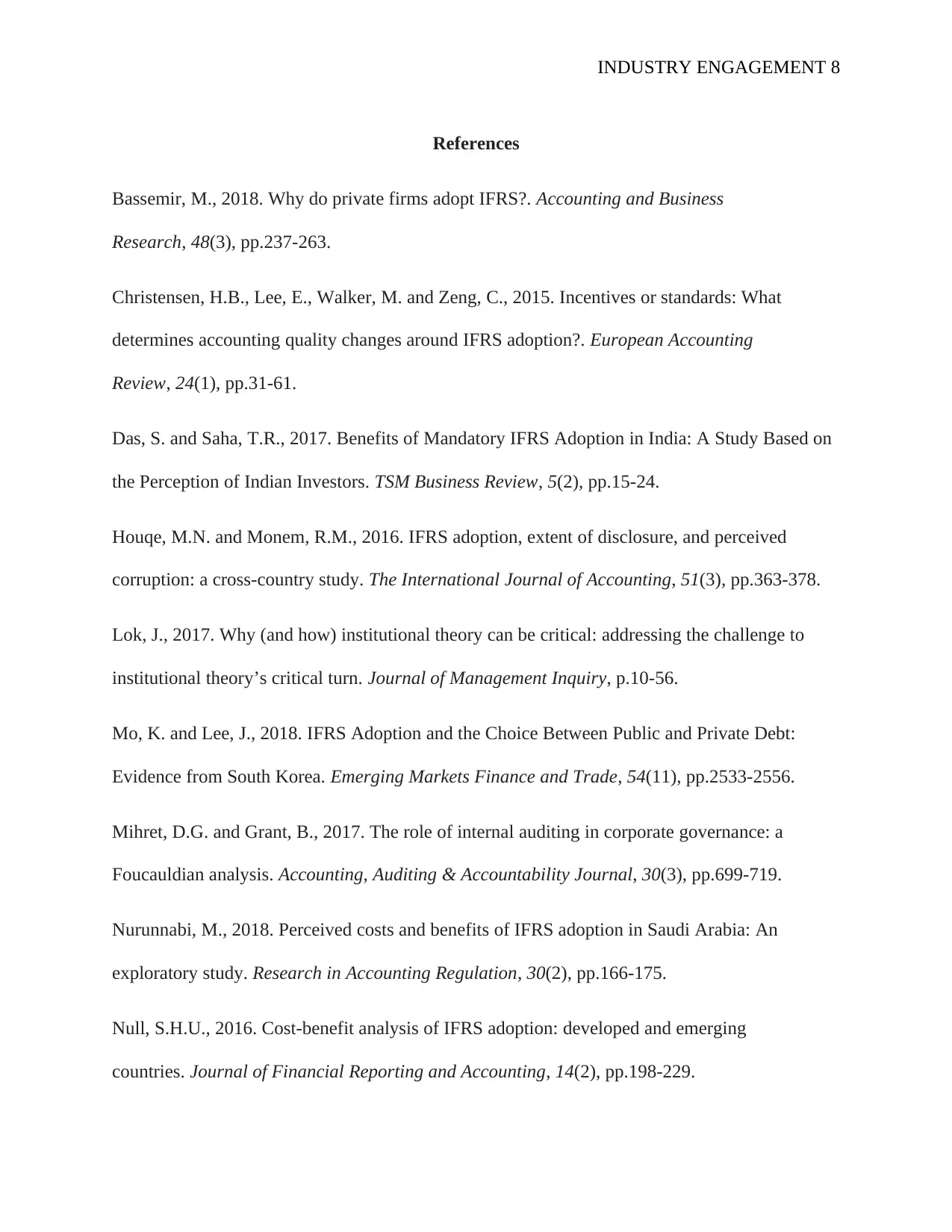

Conceptual Map

Dependent Variables Independent Variables

Increased comparability

Access to capital from external

sources

Improved quality

Adoption of International

Financial Reporting Standard

country. In addition, Mo and Lee (2018, p. 2545) study shows that both public and private firm

chose to adopt IRS so that they can be able to access financial markets. The lenders trust on the

financial statements reported using IFRS and they will provide funds to them compared to other

firms using different reporting standards.

Conceptual Map

Dependent Variables Independent Variables

Increased comparability

Access to capital from external

sources

Improved quality

Adoption of International

Financial Reporting Standard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INDUSTRY ENGAGEMENT 8

References

Bassemir, M., 2018. Why do private firms adopt IFRS?. Accounting and Business

Research, 48(3), pp.237-263.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Das, S. and Saha, T.R., 2017. Benefits of Mandatory IFRS Adoption in India: A Study Based on

the Perception of Indian Investors. TSM Business Review, 5(2), pp.15-24.

Houqe, M.N. and Monem, R.M., 2016. IFRS adoption, extent of disclosure, and perceived

corruption: a cross-country study. The International Journal of Accounting, 51(3), pp.363-378.

Lok, J., 2017. Why (and how) institutional theory can be critical: addressing the challenge to

institutional theory’s critical turn. Journal of Management Inquiry, p.10-56.

Mo, K. and Lee, J., 2018. IFRS Adoption and the Choice Between Public and Private Debt:

Evidence from South Korea. Emerging Markets Finance and Trade, 54(11), pp.2533-2556.

Mihret, D.G. and Grant, B., 2017. The role of internal auditing in corporate governance: a

Foucauldian analysis. Accounting, Auditing & Accountability Journal, 30(3), pp.699-719.

Nurunnabi, M., 2018. Perceived costs and benefits of IFRS adoption in Saudi Arabia: An

exploratory study. Research in Accounting Regulation, 30(2), pp.166-175.

Null, S.H.U., 2016. Cost-benefit analysis of IFRS adoption: developed and emerging

countries. Journal of Financial Reporting and Accounting, 14(2), pp.198-229.

References

Bassemir, M., 2018. Why do private firms adopt IFRS?. Accounting and Business

Research, 48(3), pp.237-263.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Das, S. and Saha, T.R., 2017. Benefits of Mandatory IFRS Adoption in India: A Study Based on

the Perception of Indian Investors. TSM Business Review, 5(2), pp.15-24.

Houqe, M.N. and Monem, R.M., 2016. IFRS adoption, extent of disclosure, and perceived

corruption: a cross-country study. The International Journal of Accounting, 51(3), pp.363-378.

Lok, J., 2017. Why (and how) institutional theory can be critical: addressing the challenge to

institutional theory’s critical turn. Journal of Management Inquiry, p.10-56.

Mo, K. and Lee, J., 2018. IFRS Adoption and the Choice Between Public and Private Debt:

Evidence from South Korea. Emerging Markets Finance and Trade, 54(11), pp.2533-2556.

Mihret, D.G. and Grant, B., 2017. The role of internal auditing in corporate governance: a

Foucauldian analysis. Accounting, Auditing & Accountability Journal, 30(3), pp.699-719.

Nurunnabi, M., 2018. Perceived costs and benefits of IFRS adoption in Saudi Arabia: An

exploratory study. Research in Accounting Regulation, 30(2), pp.166-175.

Null, S.H.U., 2016. Cost-benefit analysis of IFRS adoption: developed and emerging

countries. Journal of Financial Reporting and Accounting, 14(2), pp.198-229.

INDUSTRY ENGAGEMENT 9

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, pp.1-9.

Özcan, A., 2016. Assessing the effects of IFRS adoption on economic growth: A cross country

study.

Ramesh, D., 2019. Insight towards Adoption of International Financial Reporting Standards

(IFRS) in India. Insight towards Adoption of International Financial Reporting Standards (IFRS)

in India (January 6, 2019).

Vidal-García, J. and Vidal, M., 2016. IFRS harmonization and foreign direct investment.

In Analyzing the Relationship between Corporate Social Responsibility and Foreign Direct

Investment (pp. 31-48). IGI Global.

Oulasvirta, L., 2016. Accounting Principles. Global Encyclopedia of Public Administration,

Public Policy, and Governance, pp.1-9.

Özcan, A., 2016. Assessing the effects of IFRS adoption on economic growth: A cross country

study.

Ramesh, D., 2019. Insight towards Adoption of International Financial Reporting Standards

(IFRS) in India. Insight towards Adoption of International Financial Reporting Standards (IFRS)

in India (January 6, 2019).

Vidal-García, J. and Vidal, M., 2016. IFRS harmonization and foreign direct investment.

In Analyzing the Relationship between Corporate Social Responsibility and Foreign Direct

Investment (pp. 31-48). IGI Global.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.