Assessing Clients' Loan Application and Borrowing Options

VerifiedAdded on 2022/12/23

|46

|12076

|72

AI Summary

This document discusses the assessment of clients' loan application and borrowing options. It covers topics such as legislative requirements, borrowing capacity, repayment requirements, security, concessions, and potential risks. The document provides data and analysis to support the assessment.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

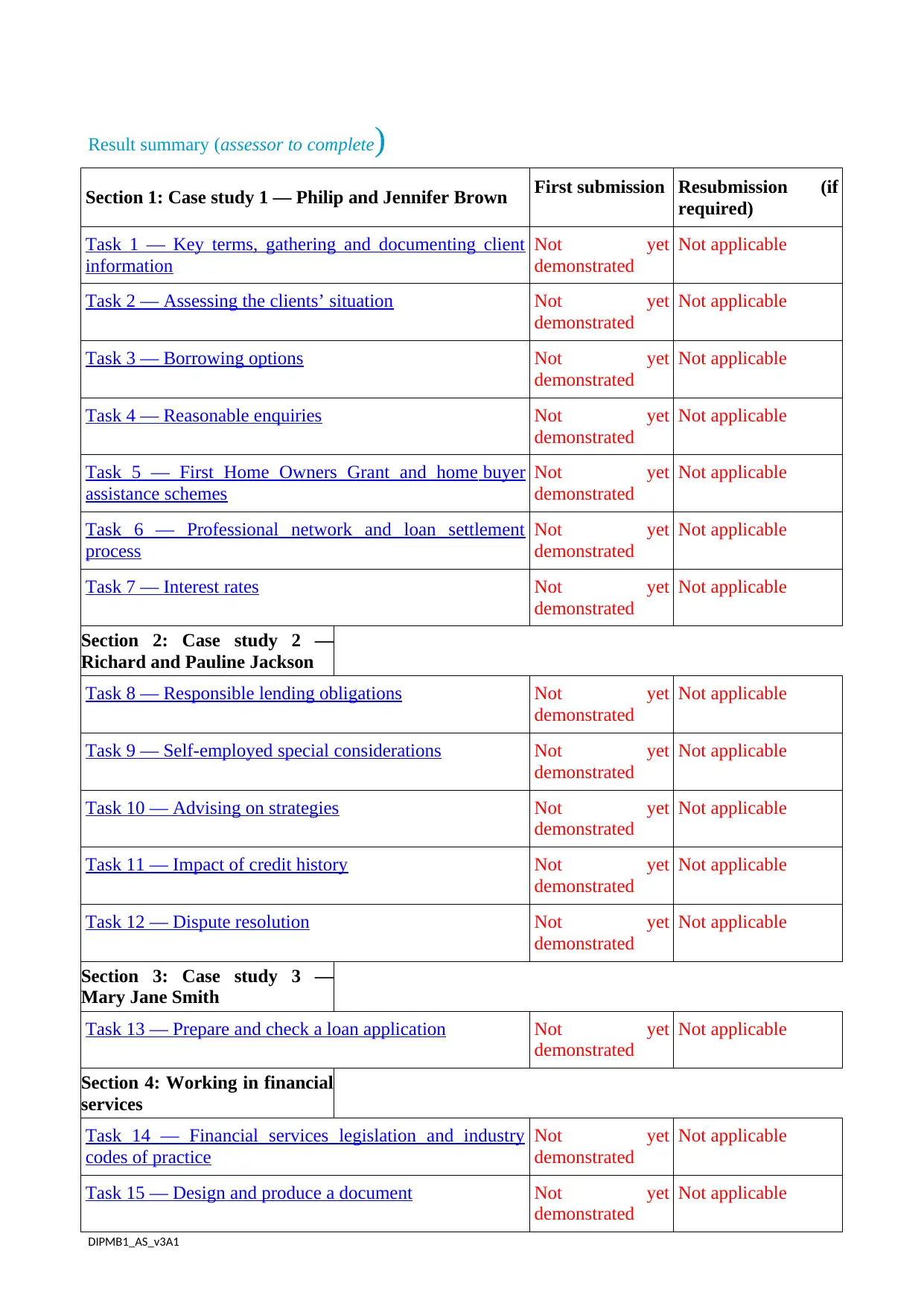

Result summary (assessor to complete)

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if

required)

Task 1 — Key terms, gathering and documenting client

information

Not yet

demonstrated

Not applicable

Task 2 — Assessing the clients’ situation Not yet

demonstrated

Not applicable

Task 3 — Borrowing options Not yet

demonstrated

Not applicable

Task 4 — Reasonable enquiries Not yet

demonstrated

Not applicable

Task 5 — First Home Owners Grant and home buyer

assistance schemes

Not yet

demonstrated

Not applicable

Task 6 — Professional network and loan settlement

process

Not yet

demonstrated

Not applicable

Task 7 — Interest rates Not yet

demonstrated

Not applicable

Section 2: Case study 2 —

Richard and Pauline Jackson

Task 8 — Responsible lending obligations Not yet

demonstrated

Not applicable

Task 9 — Self-employed special considerations Not yet

demonstrated

Not applicable

Task 10 — Advising on strategies Not yet

demonstrated

Not applicable

Task 11 — Impact of credit history Not yet

demonstrated

Not applicable

Task 12 — Dispute resolution Not yet

demonstrated

Not applicable

Section 3: Case study 3 —

Mary Jane Smith

Task 13 — Prepare and check a loan application Not yet

demonstrated

Not applicable

Section 4: Working in financial

services

Task 14 — Financial services legislation and industry

codes of practice

Not yet

demonstrated

Not applicable

Task 15 — Design and produce a document Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if

required)

Task 1 — Key terms, gathering and documenting client

information

Not yet

demonstrated

Not applicable

Task 2 — Assessing the clients’ situation Not yet

demonstrated

Not applicable

Task 3 — Borrowing options Not yet

demonstrated

Not applicable

Task 4 — Reasonable enquiries Not yet

demonstrated

Not applicable

Task 5 — First Home Owners Grant and home buyer

assistance schemes

Not yet

demonstrated

Not applicable

Task 6 — Professional network and loan settlement

process

Not yet

demonstrated

Not applicable

Task 7 — Interest rates Not yet

demonstrated

Not applicable

Section 2: Case study 2 —

Richard and Pauline Jackson

Task 8 — Responsible lending obligations Not yet

demonstrated

Not applicable

Task 9 — Self-employed special considerations Not yet

demonstrated

Not applicable

Task 10 — Advising on strategies Not yet

demonstrated

Not applicable

Task 11 — Impact of credit history Not yet

demonstrated

Not applicable

Task 12 — Dispute resolution Not yet

demonstrated

Not applicable

Section 3: Case study 3 —

Mary Jane Smith

Task 13 — Prepare and check a loan application Not yet

demonstrated

Not applicable

Section 4: Working in financial

services

Task 14 — Financial services legislation and industry

codes of practice

Not yet

demonstrated

Not applicable

Task 15 — Design and produce a document Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

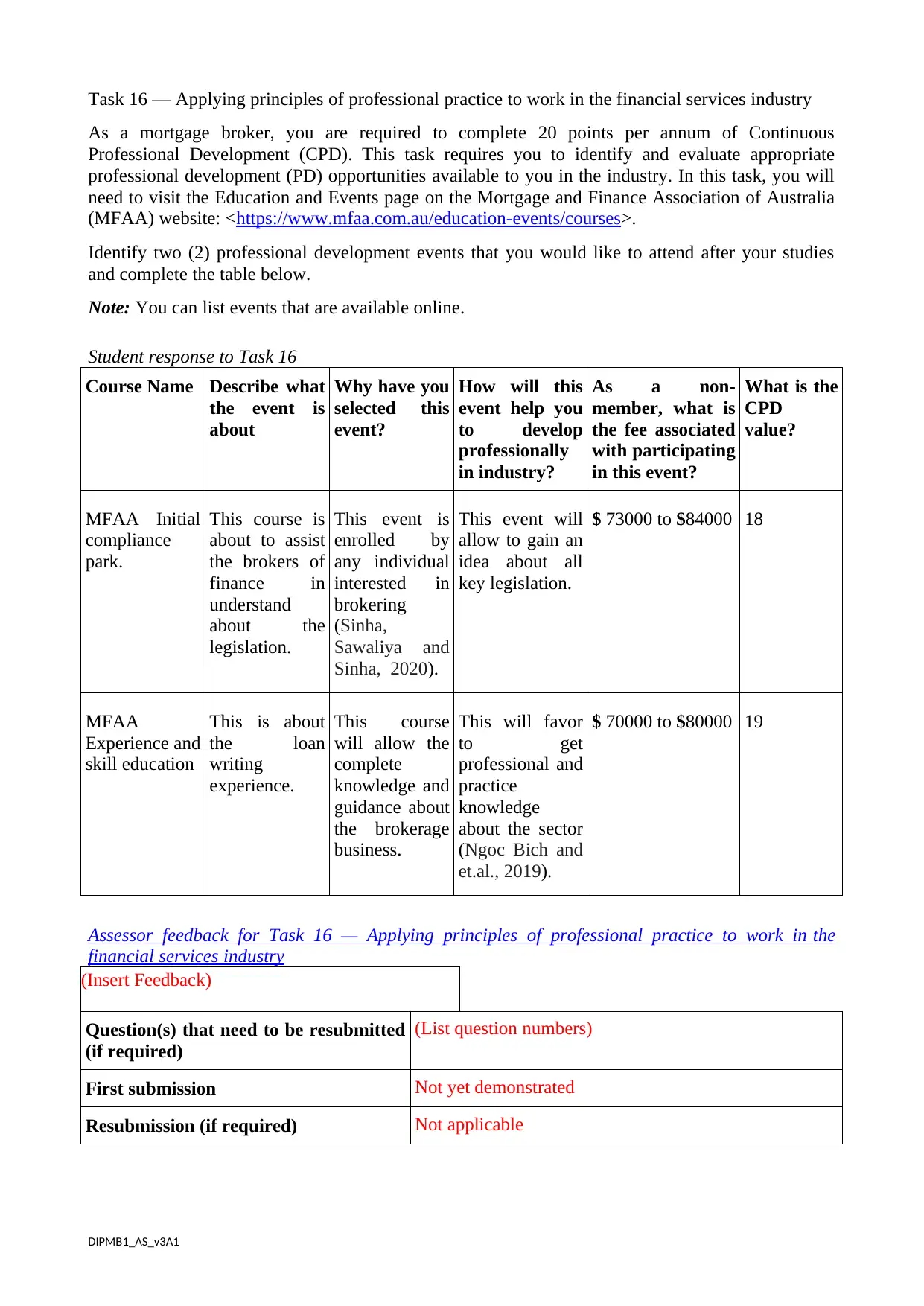

Task 16 — Applying principles of professional practice to

work in the financial services industry

Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

work in the financial services industry

Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

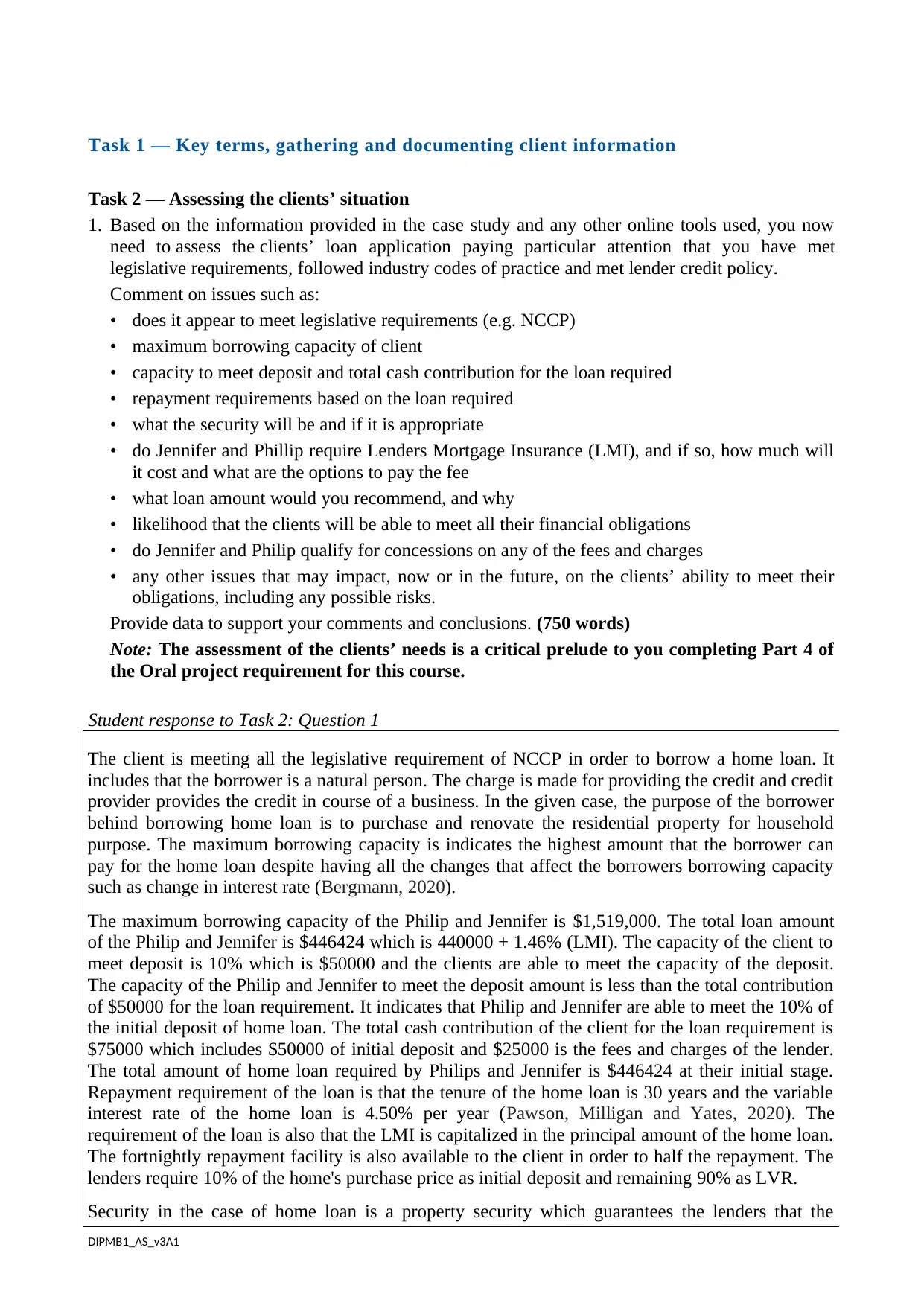

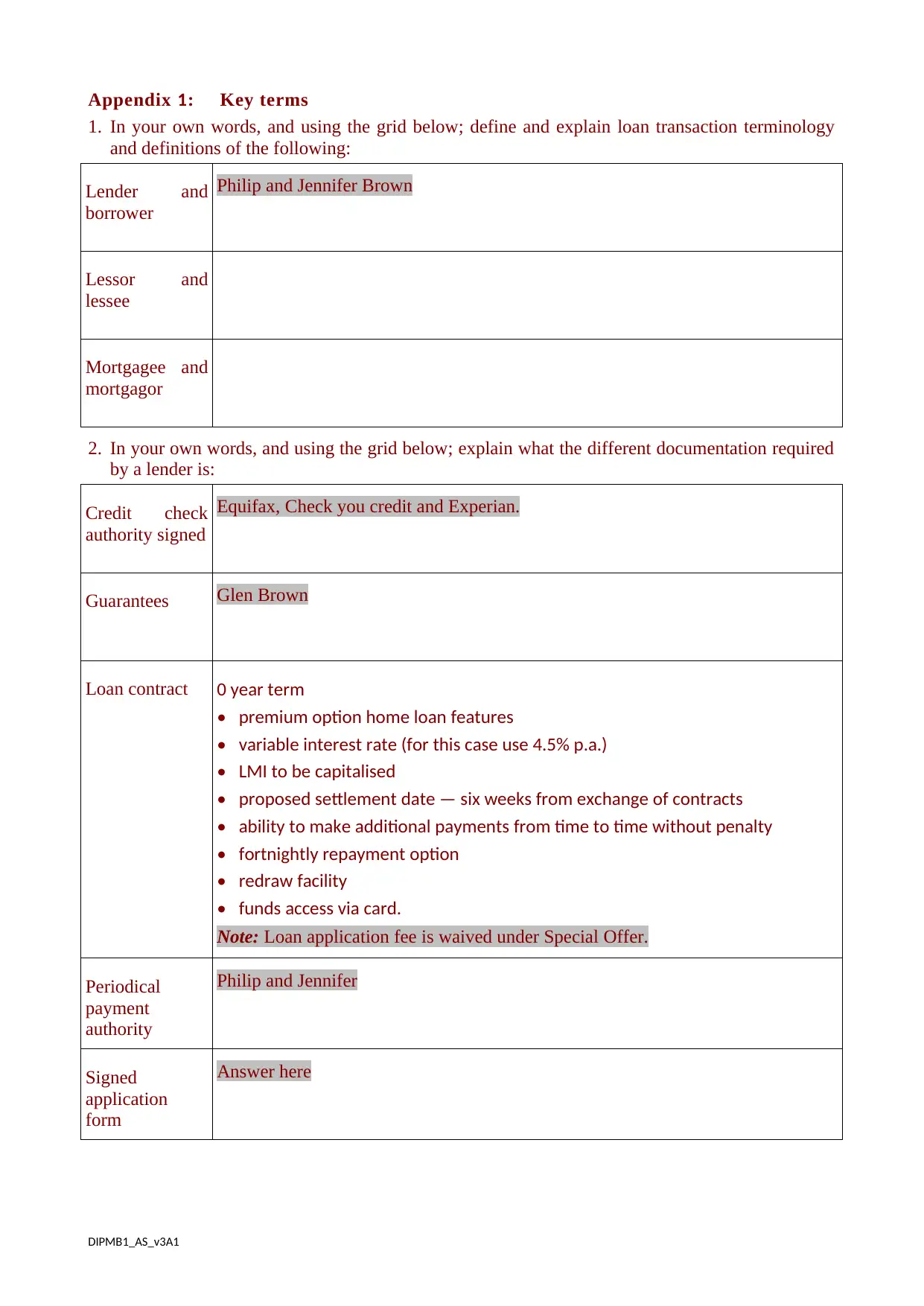

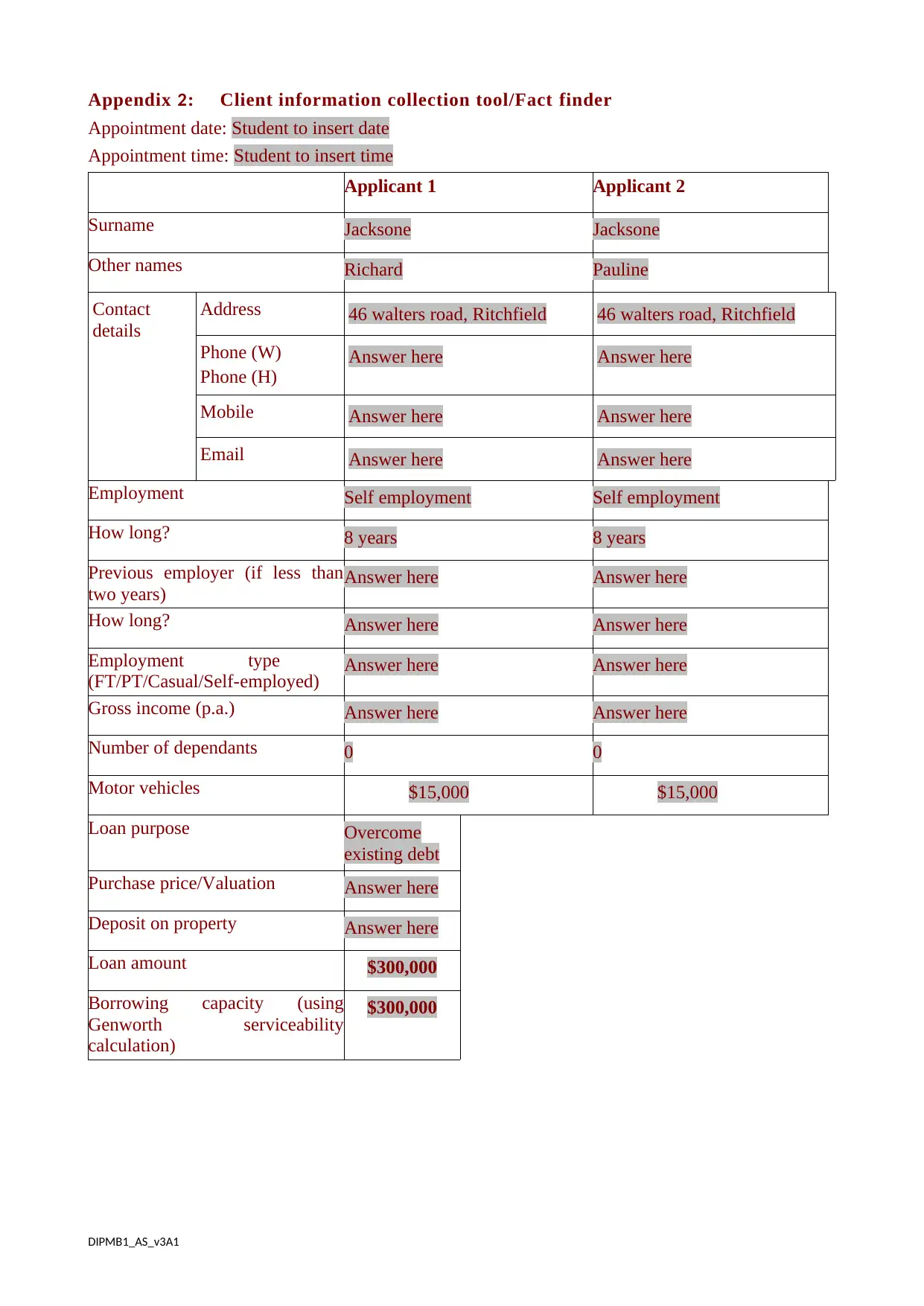

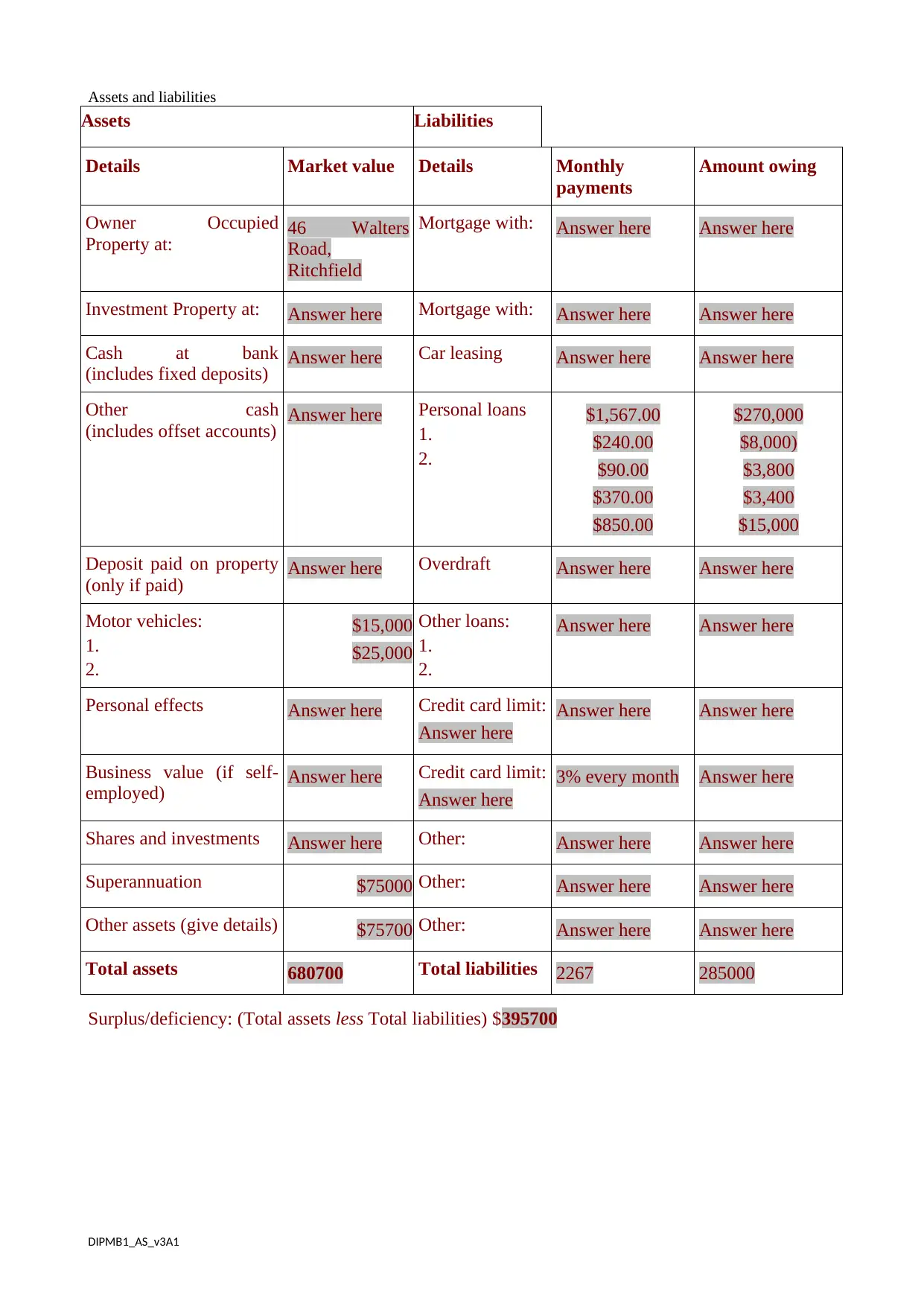

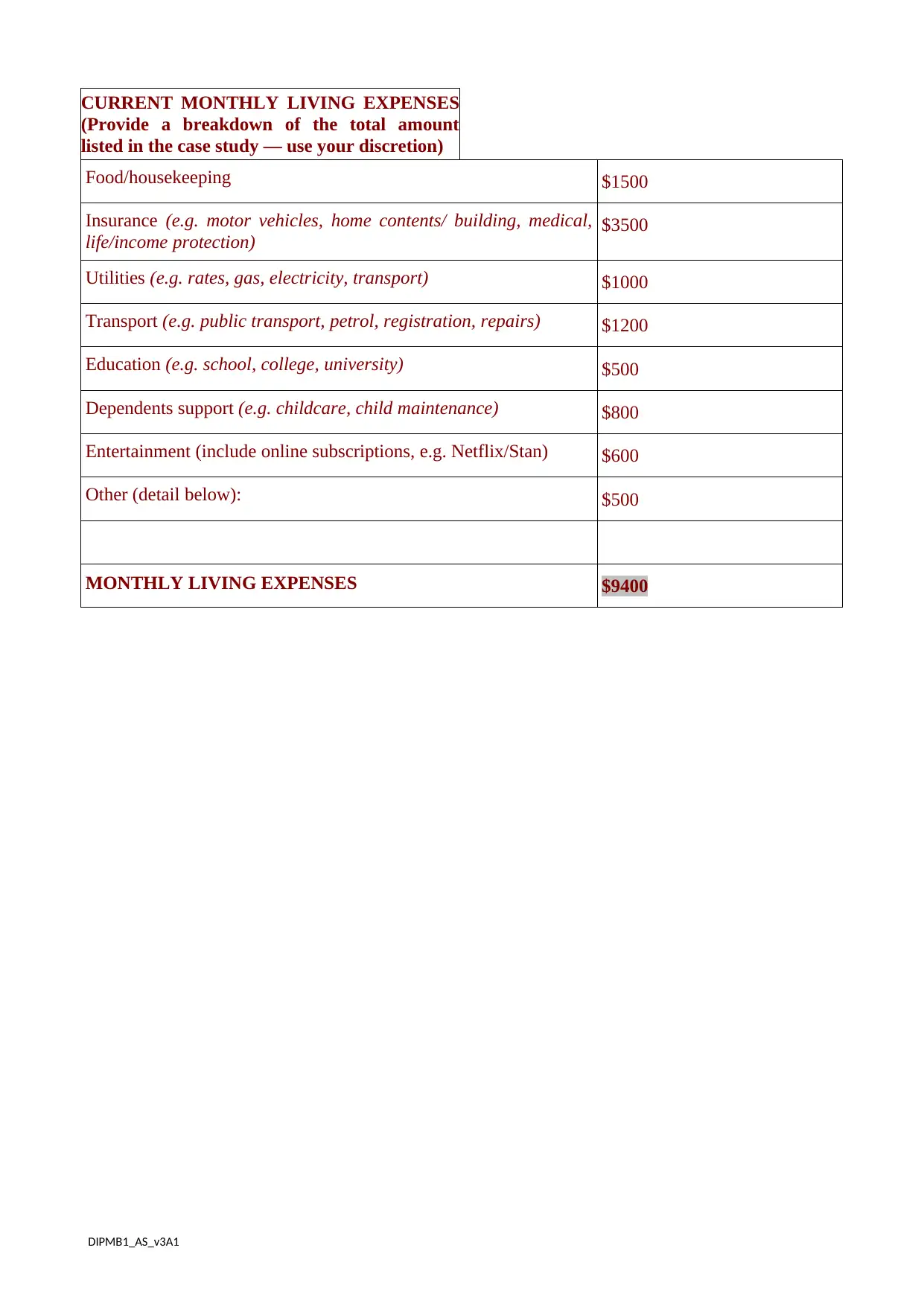

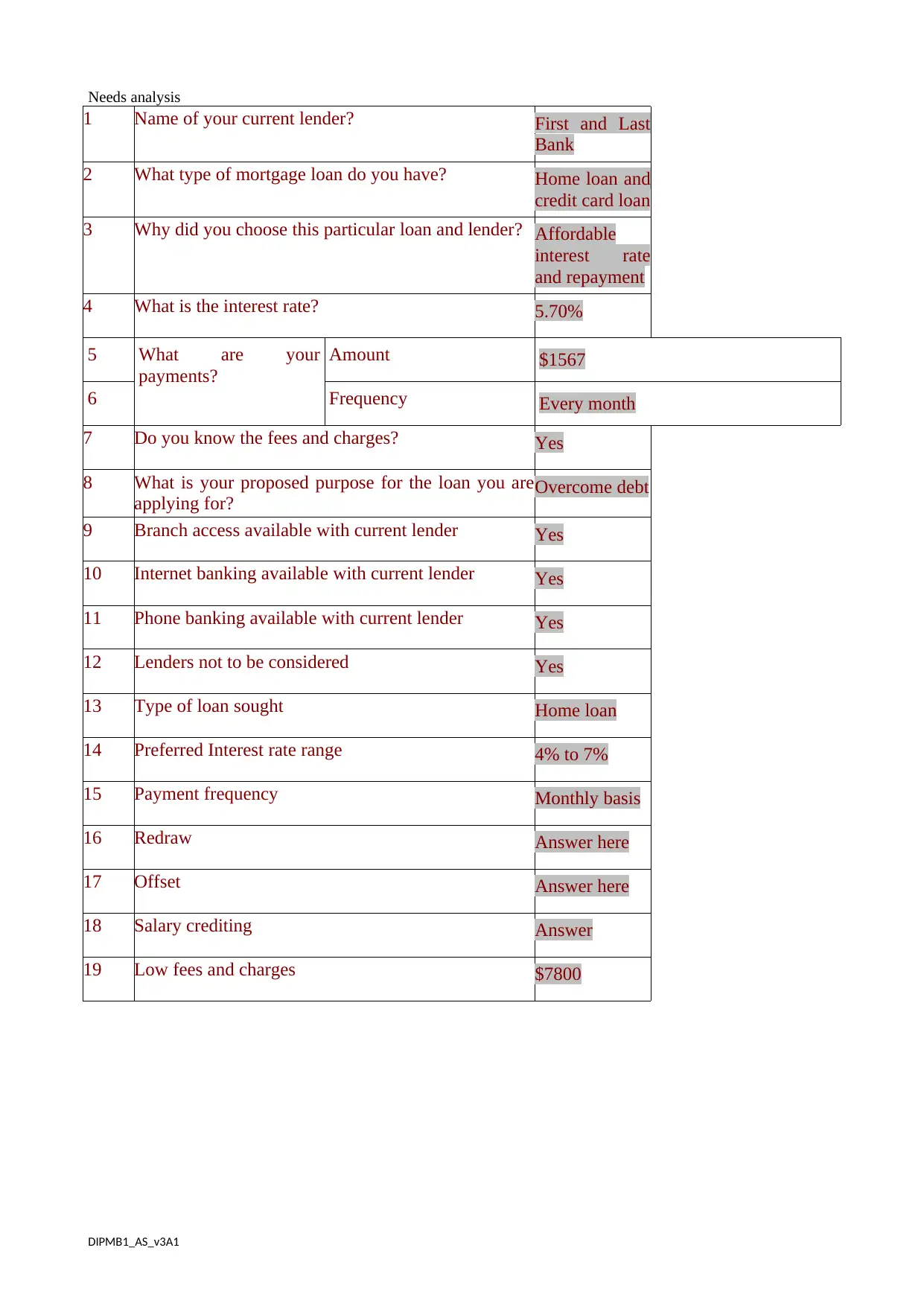

Task 1 — Key terms, gathering and documenting client information

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now

need to assess the clients’ loan application paying particular attention that you have met

legislative requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will

it cost and what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of

the Oral project requirement for this course.

Student response to Task 2: Question 1

The client is meeting all the legislative requirement of NCCP in order to borrow a home loan. It

includes that the borrower is a natural person. The charge is made for providing the credit and credit

provider provides the credit in course of a business. In the given case, the purpose of the borrower

behind borrowing home loan is to purchase and renovate the residential property for household

purpose. The maximum borrowing capacity is indicates the highest amount that the borrower can

pay for the home loan despite having all the changes that affect the borrowers borrowing capacity

such as change in interest rate (Bergmann, 2020).

The maximum borrowing capacity of the Philip and Jennifer is $1,519,000. The total loan amount

of the Philip and Jennifer is $446424 which is 440000 + 1.46% (LMI). The capacity of the client to

meet deposit is 10% which is $50000 and the clients are able to meet the capacity of the deposit.

The capacity of the Philip and Jennifer to meet the deposit amount is less than the total contribution

of $50000 for the loan requirement. It indicates that Philip and Jennifer are able to meet the 10% of

the initial deposit of home loan. The total cash contribution of the client for the loan requirement is

$75000 which includes $50000 of initial deposit and $25000 is the fees and charges of the lender.

The total amount of home loan required by Philips and Jennifer is $446424 at their initial stage.

Repayment requirement of the loan is that the tenure of the home loan is 30 years and the variable

interest rate of the home loan is 4.50% per year (Pawson, Milligan and Yates, 2020). The

requirement of the loan is also that the LMI is capitalized in the principal amount of the home loan.

The fortnightly repayment facility is also available to the client in order to half the repayment. The

lenders require 10% of the home's purchase price as initial deposit and remaining 90% as LVR.

Security in the case of home loan is a property security which guarantees the lenders that the

DIPMB1_AS_v3A1

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now

need to assess the clients’ loan application paying particular attention that you have met

legislative requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will

it cost and what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of

the Oral project requirement for this course.

Student response to Task 2: Question 1

The client is meeting all the legislative requirement of NCCP in order to borrow a home loan. It

includes that the borrower is a natural person. The charge is made for providing the credit and credit

provider provides the credit in course of a business. In the given case, the purpose of the borrower

behind borrowing home loan is to purchase and renovate the residential property for household

purpose. The maximum borrowing capacity is indicates the highest amount that the borrower can

pay for the home loan despite having all the changes that affect the borrowers borrowing capacity

such as change in interest rate (Bergmann, 2020).

The maximum borrowing capacity of the Philip and Jennifer is $1,519,000. The total loan amount

of the Philip and Jennifer is $446424 which is 440000 + 1.46% (LMI). The capacity of the client to

meet deposit is 10% which is $50000 and the clients are able to meet the capacity of the deposit.

The capacity of the Philip and Jennifer to meet the deposit amount is less than the total contribution

of $50000 for the loan requirement. It indicates that Philip and Jennifer are able to meet the 10% of

the initial deposit of home loan. The total cash contribution of the client for the loan requirement is

$75000 which includes $50000 of initial deposit and $25000 is the fees and charges of the lender.

The total amount of home loan required by Philips and Jennifer is $446424 at their initial stage.

Repayment requirement of the loan is that the tenure of the home loan is 30 years and the variable

interest rate of the home loan is 4.50% per year (Pawson, Milligan and Yates, 2020). The

requirement of the loan is also that the LMI is capitalized in the principal amount of the home loan.

The fortnightly repayment facility is also available to the client in order to half the repayment. The

lenders require 10% of the home's purchase price as initial deposit and remaining 90% as LVR.

Security in the case of home loan is a property security which guarantees the lenders that the

DIPMB1_AS_v3A1

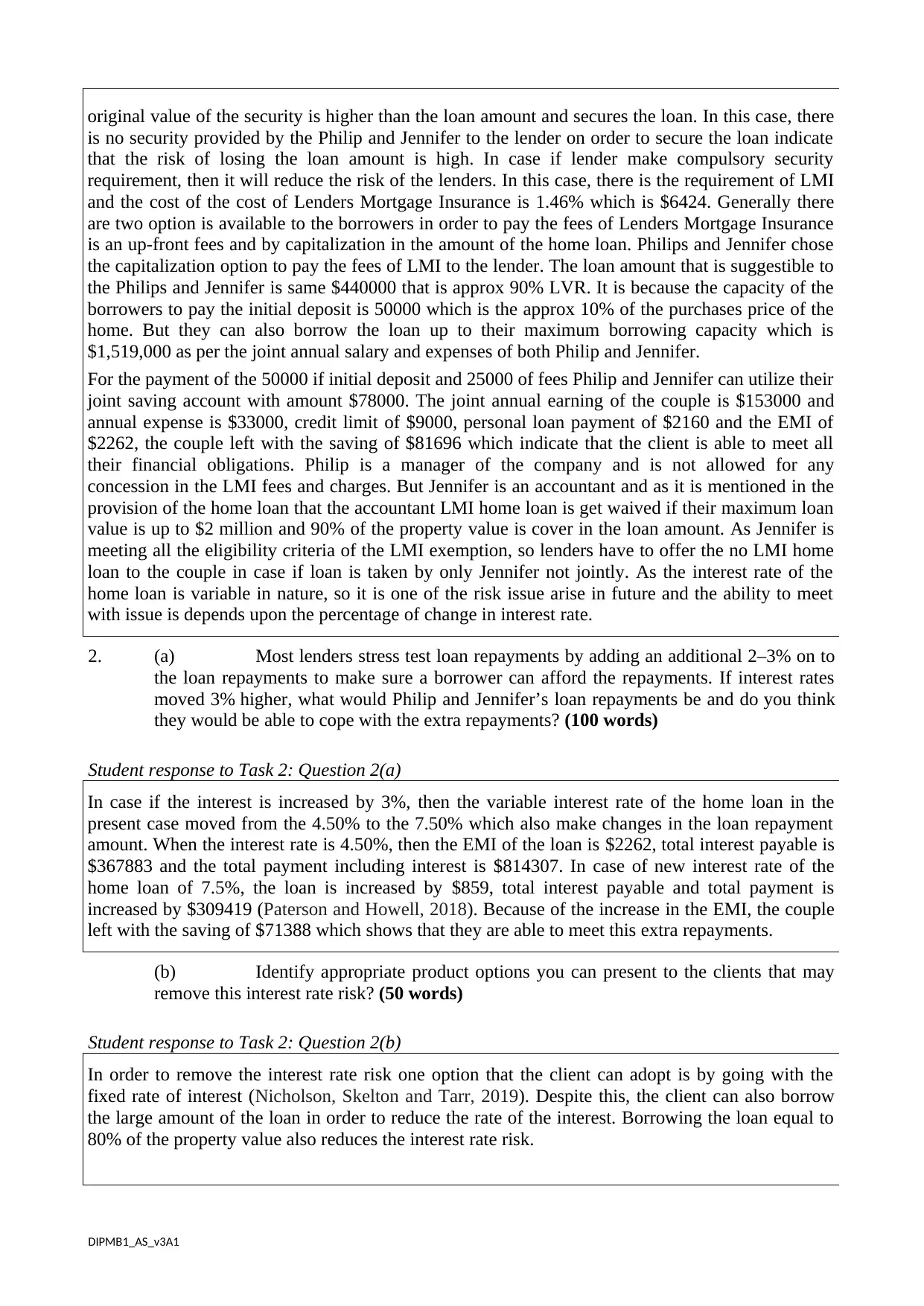

original value of the security is higher than the loan amount and secures the loan. In this case, there

is no security provided by the Philip and Jennifer to the lender on order to secure the loan indicate

that the risk of losing the loan amount is high. In case if lender make compulsory security

requirement, then it will reduce the risk of the lenders. In this case, there is the requirement of LMI

and the cost of the cost of Lenders Mortgage Insurance is 1.46% which is $6424. Generally there

are two option is available to the borrowers in order to pay the fees of Lenders Mortgage Insurance

is an up-front fees and by capitalization in the amount of the home loan. Philips and Jennifer chose

the capitalization option to pay the fees of LMI to the lender. The loan amount that is suggestible to

the Philips and Jennifer is same $440000 that is approx 90% LVR. It is because the capacity of the

borrowers to pay the initial deposit is 50000 which is the approx 10% of the purchases price of the

home. But they can also borrow the loan up to their maximum borrowing capacity which is

$1,519,000 as per the joint annual salary and expenses of both Philip and Jennifer.

For the payment of the 50000 if initial deposit and 25000 of fees Philip and Jennifer can utilize their

joint saving account with amount $78000. The joint annual earning of the couple is $153000 and

annual expense is $33000, credit limit of $9000, personal loan payment of $2160 and the EMI of

$2262, the couple left with the saving of $81696 which indicate that the client is able to meet all

their financial obligations. Philip is a manager of the company and is not allowed for any

concession in the LMI fees and charges. But Jennifer is an accountant and as it is mentioned in the

provision of the home loan that the accountant LMI home loan is get waived if their maximum loan

value is up to $2 million and 90% of the property value is cover in the loan amount. As Jennifer is

meeting all the eligibility criteria of the LMI exemption, so lenders have to offer the no LMI home

loan to the couple in case if loan is taken by only Jennifer not jointly. As the interest rate of the

home loan is variable in nature, so it is one of the risk issue arise in future and the ability to meet

with issue is depends upon the percentage of change in interest rate.

2. (a) Most lenders stress test loan repayments by adding an additional 2–3% on to

the loan repayments to make sure a borrower can afford the repayments. If interest rates

moved 3% higher, what would Philip and Jennifer’s loan repayments be and do you think

they would be able to cope with the extra repayments? (100 words)

Student response to Task 2: Question 2(a)

In case if the interest is increased by 3%, then the variable interest rate of the home loan in the

present case moved from the 4.50% to the 7.50% which also make changes in the loan repayment

amount. When the interest rate is 4.50%, then the EMI of the loan is $2262, total interest payable is

$367883 and the total payment including interest is $814307. In case of new interest rate of the

home loan of 7.5%, the loan is increased by $859, total interest payable and total payment is

increased by $309419 (Paterson and Howell, 2018). Because of the increase in the EMI, the couple

left with the saving of $71388 which shows that they are able to meet this extra repayments.

(b) Identify appropriate product options you can present to the clients that may

remove this interest rate risk? (50 words)

Student response to Task 2: Question 2(b)

In order to remove the interest rate risk one option that the client can adopt is by going with the

fixed rate of interest (Nicholson, Skelton and Tarr, 2019). Despite this, the client can also borrow

the large amount of the loan in order to reduce the rate of the interest. Borrowing the loan equal to

80% of the property value also reduces the interest rate risk.

DIPMB1_AS_v3A1

is no security provided by the Philip and Jennifer to the lender on order to secure the loan indicate

that the risk of losing the loan amount is high. In case if lender make compulsory security

requirement, then it will reduce the risk of the lenders. In this case, there is the requirement of LMI

and the cost of the cost of Lenders Mortgage Insurance is 1.46% which is $6424. Generally there

are two option is available to the borrowers in order to pay the fees of Lenders Mortgage Insurance

is an up-front fees and by capitalization in the amount of the home loan. Philips and Jennifer chose

the capitalization option to pay the fees of LMI to the lender. The loan amount that is suggestible to

the Philips and Jennifer is same $440000 that is approx 90% LVR. It is because the capacity of the

borrowers to pay the initial deposit is 50000 which is the approx 10% of the purchases price of the

home. But they can also borrow the loan up to their maximum borrowing capacity which is

$1,519,000 as per the joint annual salary and expenses of both Philip and Jennifer.

For the payment of the 50000 if initial deposit and 25000 of fees Philip and Jennifer can utilize their

joint saving account with amount $78000. The joint annual earning of the couple is $153000 and

annual expense is $33000, credit limit of $9000, personal loan payment of $2160 and the EMI of

$2262, the couple left with the saving of $81696 which indicate that the client is able to meet all

their financial obligations. Philip is a manager of the company and is not allowed for any

concession in the LMI fees and charges. But Jennifer is an accountant and as it is mentioned in the

provision of the home loan that the accountant LMI home loan is get waived if their maximum loan

value is up to $2 million and 90% of the property value is cover in the loan amount. As Jennifer is

meeting all the eligibility criteria of the LMI exemption, so lenders have to offer the no LMI home

loan to the couple in case if loan is taken by only Jennifer not jointly. As the interest rate of the

home loan is variable in nature, so it is one of the risk issue arise in future and the ability to meet

with issue is depends upon the percentage of change in interest rate.

2. (a) Most lenders stress test loan repayments by adding an additional 2–3% on to

the loan repayments to make sure a borrower can afford the repayments. If interest rates

moved 3% higher, what would Philip and Jennifer’s loan repayments be and do you think

they would be able to cope with the extra repayments? (100 words)

Student response to Task 2: Question 2(a)

In case if the interest is increased by 3%, then the variable interest rate of the home loan in the

present case moved from the 4.50% to the 7.50% which also make changes in the loan repayment

amount. When the interest rate is 4.50%, then the EMI of the loan is $2262, total interest payable is

$367883 and the total payment including interest is $814307. In case of new interest rate of the

home loan of 7.5%, the loan is increased by $859, total interest payable and total payment is

increased by $309419 (Paterson and Howell, 2018). Because of the increase in the EMI, the couple

left with the saving of $71388 which shows that they are able to meet this extra repayments.

(b) Identify appropriate product options you can present to the clients that may

remove this interest rate risk? (50 words)

Student response to Task 2: Question 2(b)

In order to remove the interest rate risk one option that the client can adopt is by going with the

fixed rate of interest (Nicholson, Skelton and Tarr, 2019). Despite this, the client can also borrow

the large amount of the loan in order to reduce the rate of the interest. Borrowing the loan equal to

80% of the property value also reduces the interest rate risk.

DIPMB1_AS_v3A1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assessor feedback for Task 2 — Assessing the clients’ situation

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 3 — Borrowing options

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options

could you present that would avoid the cost of LMI? (100 words)

Student response to Task 3

The way that the Philips and the Jennifer couple can adopt in order to avoid the cost of the Lenders

Mortgage Insurance is by saving the bigger deposits for the purchase of the affordable loan. This

further reduces the amount of loan to low value ratio and help the couple in avoiding the LMI of the

home loan (North and Wilson, 2020). The another way to avoid the LMI of the loan is by arranging

the any family guarantee and property security in order to cover the loan security. Being a doctor,

accountant any professional service also help in avoiding the Lenders Mortgage Insurance of the

home loan.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options

could you present that would avoid the cost of LMI? (100 words)

Student response to Task 3

The way that the Philips and the Jennifer couple can adopt in order to avoid the cost of the Lenders

Mortgage Insurance is by saving the bigger deposits for the purchase of the affordable loan. This

further reduces the amount of loan to low value ratio and help the couple in avoiding the LMI of the

home loan (North and Wilson, 2020). The another way to avoid the LMI of the loan is by arranging

the any family guarantee and property security in order to cover the loan security. Being a doctor,

accountant any professional service also help in avoiding the Lenders Mortgage Insurance of the

home loan.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 4 — Reasonable enquiries

In the course of gathering information about the couple, you are required under the National

Consumer Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s

objectives, requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study

and explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 4

Six reasonable inquiries that the lenders have to make with the clients in order to reduce the risk of

the lender:

What was the impact of the credit contract on the client when they enter into the complex

and unsuitable credit contract.

Whether the client is the new or the existing customer of the credit provider.

Whether the client has the capacity to enter into the credit contract after meeting its fixed

and variable expenses.

The current salary of the client and the nature of the source of the client salary.

The desired credit card limit of the clients and the period for which the credit is required.

Recent income tax return, payroll slip and the statement of their income from their

accountant.

The importance of inquiries about the borrower's objectives, requirements and financial situations

help the lenders to know the clients profitability and the stability (Bhutta and Keys, 2017). This

further help the lenders to know whether the client has any assets to cover the home loans security

or not. It also helps the lenders to know the deposit capacity of the clients and the nature of the

source of the income.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

In the course of gathering information about the couple, you are required under the National

Consumer Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s

objectives, requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study

and explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 4

Six reasonable inquiries that the lenders have to make with the clients in order to reduce the risk of

the lender:

What was the impact of the credit contract on the client when they enter into the complex

and unsuitable credit contract.

Whether the client is the new or the existing customer of the credit provider.

Whether the client has the capacity to enter into the credit contract after meeting its fixed

and variable expenses.

The current salary of the client and the nature of the source of the client salary.

The desired credit card limit of the clients and the period for which the credit is required.

Recent income tax return, payroll slip and the statement of their income from their

accountant.

The importance of inquiries about the borrower's objectives, requirements and financial situations

help the lenders to know the clients profitability and the stability (Bhutta and Keys, 2017). This

further help the lenders to know whether the client has any assets to cover the home loans security

or not. It also helps the lenders to know the deposit capacity of the clients and the nature of the

source of the income.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 5 — First Home Owners Grant and home buyer assistance schemes

Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory, who would be eligible and what would be

their benefit? Are Philip and Jennifer eligible for any assistance?

Note: Please identify which State or Territory you are from in your answer. (150 words)

Student response to Task 5

The state from where the Philips and Jennifer belong is the New South Wales of the Australia. The

eligibility criteria available to the first home buyer assistance under First Home Owner's Grant

scheme is if a client purchase existing home having value less than 650000 then they need not to

pay any transfer duty (Bhutta and Ringo, 2017). And if the value of the property is exists between

the 650000 and the 800000 and apply for concessional transfer rate than the amount of concession

is based upon the value of existing property. In the given case, Philip and Jennifer's purchase

existing home and the property value is 490000, then they are eligible for the full exemption of the

stamp duty.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory, who would be eligible and what would be

their benefit? Are Philip and Jennifer eligible for any assistance?

Note: Please identify which State or Territory you are from in your answer. (150 words)

Student response to Task 5

The state from where the Philips and Jennifer belong is the New South Wales of the Australia. The

eligibility criteria available to the first home buyer assistance under First Home Owner's Grant

scheme is if a client purchase existing home having value less than 650000 then they need not to

pay any transfer duty (Bhutta and Ringo, 2017). And if the value of the property is exists between

the 650000 and the 800000 and apply for concessional transfer rate than the amount of concession

is based upon the value of existing property. In the given case, Philip and Jennifer's purchase

existing home and the property value is 490000, then they are eligible for the full exemption of the

stamp duty.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 6 — Professional network and loan settlement process

1. Name three (3) parties, who are not directly involved in the processing of a loan and what their

role is. Explain how you would communicate with them in an efficient and effective manner so

that they understand pre-settlement conditions and their involvement required. (100 words)

Student response to Task 6: Question 1

The three parties who are not directly involved in the processing of a loan is Glenn Brown brother

of Philip's, Real estate agent and the seller of the property. The role of the Glenn Brown is the pre-

settlement of the property purchase id that he reffer the Philip's and Jennifer's to the lender in order

to borrow the home loan (Koeppl and MacGee, 2017). The role of the Real state agent is to place a

meeting between the Philips and Jennifer's and the seller of the home. The real estate agent role is

intermediary. The role of seller in this case is that they are the owner of the home.

2. Explain how you would develop and maintain relevant networks with professionals such as those

you detailed above or other professionals to ensure you are up to date with the products or

services they provide. (100 words)

Student response to Task 6: Question 2

The first way towards maintaining the professional network is organizing and prioritize the current

connections on the social medias such as Facebook, twitter, Instagram etc. By showing the care

towards the professionals in order to stay in touch such as emails, phone calls etc (Park, 2020). is

also one way to maintain relevant network with the professionals. By offering the professional any

help in case they are in need of any help and by help them in case if the professional deals with any

challenge is the way to develop relevant network.

3. You want to ensure that Philip and Jennifer have all the key insurance protections in place in

case something unfortunate was to happen to one of them. What process would you follow

during your discussion with the clients to ensure you have a good assessment of their needs?

(100 words)

Student response to Task 6: Question 3

The brokers are the professionals who experienced the different ins and outs of the claims process.

They build a strong relationship with the companies by working daily with the insurance companies.

The brokers are able to negotiate with the insurer on behalf of the clients in case if the things are not

straightforward with the claim (Park, 2018). The brokers are the one who truly take care of all the

issues the client faces while selecting the lender and also while taking the loan for the home.

4. Briefly explain why it is important for the broker to remain informed of developments in the

lending process despite not being actively involved at every stage. (100 words)

Student response to Task 6: Question 4

The real estate brokers are not directly involve in the lending process or the buying and selling

agreement of the property, but they help the seller in knowing the market value of the property.

They also help the seller in providing the best client who can offer them the highest price of the

property (Ouazad and Kahn, 2019). Brokers of the real estate are the one who find the buyer for the

seller of the real estate property and they find the seller for the buyer of the real estate property. In

the given case the Philips and Jennifer come across the seller of the home through real estate broker

only.

DIPMB1_AS_v3A1

1. Name three (3) parties, who are not directly involved in the processing of a loan and what their

role is. Explain how you would communicate with them in an efficient and effective manner so

that they understand pre-settlement conditions and their involvement required. (100 words)

Student response to Task 6: Question 1

The three parties who are not directly involved in the processing of a loan is Glenn Brown brother

of Philip's, Real estate agent and the seller of the property. The role of the Glenn Brown is the pre-

settlement of the property purchase id that he reffer the Philip's and Jennifer's to the lender in order

to borrow the home loan (Koeppl and MacGee, 2017). The role of the Real state agent is to place a

meeting between the Philips and Jennifer's and the seller of the home. The real estate agent role is

intermediary. The role of seller in this case is that they are the owner of the home.

2. Explain how you would develop and maintain relevant networks with professionals such as those

you detailed above or other professionals to ensure you are up to date with the products or

services they provide. (100 words)

Student response to Task 6: Question 2

The first way towards maintaining the professional network is organizing and prioritize the current

connections on the social medias such as Facebook, twitter, Instagram etc. By showing the care

towards the professionals in order to stay in touch such as emails, phone calls etc (Park, 2020). is

also one way to maintain relevant network with the professionals. By offering the professional any

help in case they are in need of any help and by help them in case if the professional deals with any

challenge is the way to develop relevant network.

3. You want to ensure that Philip and Jennifer have all the key insurance protections in place in

case something unfortunate was to happen to one of them. What process would you follow

during your discussion with the clients to ensure you have a good assessment of their needs?

(100 words)

Student response to Task 6: Question 3

The brokers are the professionals who experienced the different ins and outs of the claims process.

They build a strong relationship with the companies by working daily with the insurance companies.

The brokers are able to negotiate with the insurer on behalf of the clients in case if the things are not

straightforward with the claim (Park, 2018). The brokers are the one who truly take care of all the

issues the client faces while selecting the lender and also while taking the loan for the home.

4. Briefly explain why it is important for the broker to remain informed of developments in the

lending process despite not being actively involved at every stage. (100 words)

Student response to Task 6: Question 4

The real estate brokers are not directly involve in the lending process or the buying and selling

agreement of the property, but they help the seller in knowing the market value of the property.

They also help the seller in providing the best client who can offer them the highest price of the

property (Ouazad and Kahn, 2019). Brokers of the real estate are the one who find the buyer for the

seller of the real estate property and they find the seller for the buyer of the real estate property. In

the given case the Philips and Jennifer come across the seller of the home through real estate broker

only.

DIPMB1_AS_v3A1

5. Application form and related documents have now been signed and forwarded to the Lender for

approval. Philip and Jennifer have agreed that you will keep their Solicitor informed of progress

if/when the loan is approved.

Refer to the ‘Example of an Organisation’s Policies and Procedures’ document in toolbox and

explain what the service standards and timelines are up to and including the issue of offer letter

and mortgage documents. (100 words)

Student response to Task 6: Question 5

The mortgage the confirmation of mortgage loan has been checked and approved by person. The

time taken by company to proceed the loan into person account and amount deduction and total

amount revived by the person and interest details and EMI's of person monthly wise will be given in

the time line (Wu and et.al., 2017).

6. Clients have now called to execute loan offer and mortgage documents and are nervous that their

Solicitor is very busy and difficult to contact. They want to know who will be responsible for

what tasks from this point in the lead up to settlement and immediately following settlement.

Explain to Philip and Jennifer who is responsible for completion of what tasks once the loan

documents have been returned to the lender and in the lead up to settlement and once settlement

occurs. Focus on the lending organisation and the client’s solicitor/conveyancer roles in this part

of the lending process. (150 words)

Student response to Task 6: Question 6

Solicitors are the one who gives legal advice to the private and the commercial clients in case if they

enter into any agreement with the others. The solicitor himself responsible for not able to solving the

legal issues related to the clients. In case if the solicitor is busy, they can call the branch and also

email the person who are practicing under the solicitor to solve the issues of the Philips and

Jennifer's (Competition and Consumer Commission, 2020). The client also file complaint against the

solicitor that they are proceeding the lending process and also not forwarding the work to the other

solicitor. The role of the solicitor is to provide all the legal advice to their client in case if they sign

the agreement. If solicitor are busy, then they have to tell this to the clients before entering into the

agreements.

Assessor feedback for Task 6 — Professional network and loan settlement process

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

approval. Philip and Jennifer have agreed that you will keep their Solicitor informed of progress

if/when the loan is approved.

Refer to the ‘Example of an Organisation’s Policies and Procedures’ document in toolbox and

explain what the service standards and timelines are up to and including the issue of offer letter

and mortgage documents. (100 words)

Student response to Task 6: Question 5

The mortgage the confirmation of mortgage loan has been checked and approved by person. The

time taken by company to proceed the loan into person account and amount deduction and total

amount revived by the person and interest details and EMI's of person monthly wise will be given in

the time line (Wu and et.al., 2017).

6. Clients have now called to execute loan offer and mortgage documents and are nervous that their

Solicitor is very busy and difficult to contact. They want to know who will be responsible for

what tasks from this point in the lead up to settlement and immediately following settlement.

Explain to Philip and Jennifer who is responsible for completion of what tasks once the loan

documents have been returned to the lender and in the lead up to settlement and once settlement

occurs. Focus on the lending organisation and the client’s solicitor/conveyancer roles in this part

of the lending process. (150 words)

Student response to Task 6: Question 6

Solicitors are the one who gives legal advice to the private and the commercial clients in case if they

enter into any agreement with the others. The solicitor himself responsible for not able to solving the

legal issues related to the clients. In case if the solicitor is busy, they can call the branch and also

email the person who are practicing under the solicitor to solve the issues of the Philips and

Jennifer's (Competition and Consumer Commission, 2020). The client also file complaint against the

solicitor that they are proceeding the lending process and also not forwarding the work to the other

solicitor. The role of the solicitor is to provide all the legal advice to their client in case if they sign

the agreement. If solicitor are busy, then they have to tell this to the clients before entering into the

agreements.

Assessor feedback for Task 6 — Professional network and loan settlement process

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 7 — Interest rates

1. Conduct your own research and answer the following:

(a) What is the role of the RBA with respect to the movements of interest rates?

(b) Why is it important to have these controls and how do they impact mortgage

loans in Australia?

(c) Are banks obliged to follow the RBA cash rate? Explain the reason for your

answer.

(200 words)

Student response to Task 7: Question 1(a)–(c)

RBA form monetary policy that also involve declaration of the interest rate. It takes decision over

interest rate that further influence over interest charge by other banking and financial institutions.

The policy directly influence the further borrowing transactions in Australia. Banks come under the

RBA which is further influenced the interest rate (Wong and et.al., 2018). Monetary policy is

unanimous of the entire country which further influence every single aspect of the policy making in

country.

2. Philip and Jennifer from Case study 1, have called to discuss whether they should fix the interest

rate on their loan after having received several conflicting viewpoints from family and friends.

(a) Explain the process you would use to research and identify the various

product options available to meet the needs of Philip and Jennifer.

(b) Explain to Philip and Jennifer two (2) advantages and two (2) disadvantages

of fixing a loan over different fixed rate terms.

(150 words)

Student response to Task 7: Question 2(a)–(b)

The research in respect to the interest rate can be done with the support of professionals. They can

further go through internet to search the entire information. As internet disclose the different

product options. The information sources provide different advantages like it clarify the client about

the product. Interest rate also clarifies in this. There are certain disadvantage like many times

information do not modify by these information sources (Wilhelmsson, 2020). Also the

professionals in greed of grating customer spread wrong information that is further mislead the

entire information.

3. What other option/s can you suggest if they remain uncertain about whether to fix the rate on

their loan? (100 words)

Student response to Task 7: Question 3

They can visits to branch location in search of information. This will led them towards the right

information. Interest in loans are rather fix or flexible. The current loan do not offer fixed interest

that indicate as the interest will remain flexible.

Assessor feedback for Task 7 — Interest rates

DIPMB1_AS_v3A1

1. Conduct your own research and answer the following:

(a) What is the role of the RBA with respect to the movements of interest rates?

(b) Why is it important to have these controls and how do they impact mortgage

loans in Australia?

(c) Are banks obliged to follow the RBA cash rate? Explain the reason for your

answer.

(200 words)

Student response to Task 7: Question 1(a)–(c)

RBA form monetary policy that also involve declaration of the interest rate. It takes decision over

interest rate that further influence over interest charge by other banking and financial institutions.

The policy directly influence the further borrowing transactions in Australia. Banks come under the

RBA which is further influenced the interest rate (Wong and et.al., 2018). Monetary policy is

unanimous of the entire country which further influence every single aspect of the policy making in

country.

2. Philip and Jennifer from Case study 1, have called to discuss whether they should fix the interest

rate on their loan after having received several conflicting viewpoints from family and friends.

(a) Explain the process you would use to research and identify the various

product options available to meet the needs of Philip and Jennifer.

(b) Explain to Philip and Jennifer two (2) advantages and two (2) disadvantages

of fixing a loan over different fixed rate terms.

(150 words)

Student response to Task 7: Question 2(a)–(b)

The research in respect to the interest rate can be done with the support of professionals. They can

further go through internet to search the entire information. As internet disclose the different

product options. The information sources provide different advantages like it clarify the client about

the product. Interest rate also clarifies in this. There are certain disadvantage like many times

information do not modify by these information sources (Wilhelmsson, 2020). Also the

professionals in greed of grating customer spread wrong information that is further mislead the

entire information.

3. What other option/s can you suggest if they remain uncertain about whether to fix the rate on

their loan? (100 words)

Student response to Task 7: Question 3

They can visits to branch location in search of information. This will led them towards the right

information. Interest in loans are rather fix or flexible. The current loan do not offer fixed interest

that indicate as the interest will remain flexible.

Assessor feedback for Task 7 — Interest rates

DIPMB1_AS_v3A1

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

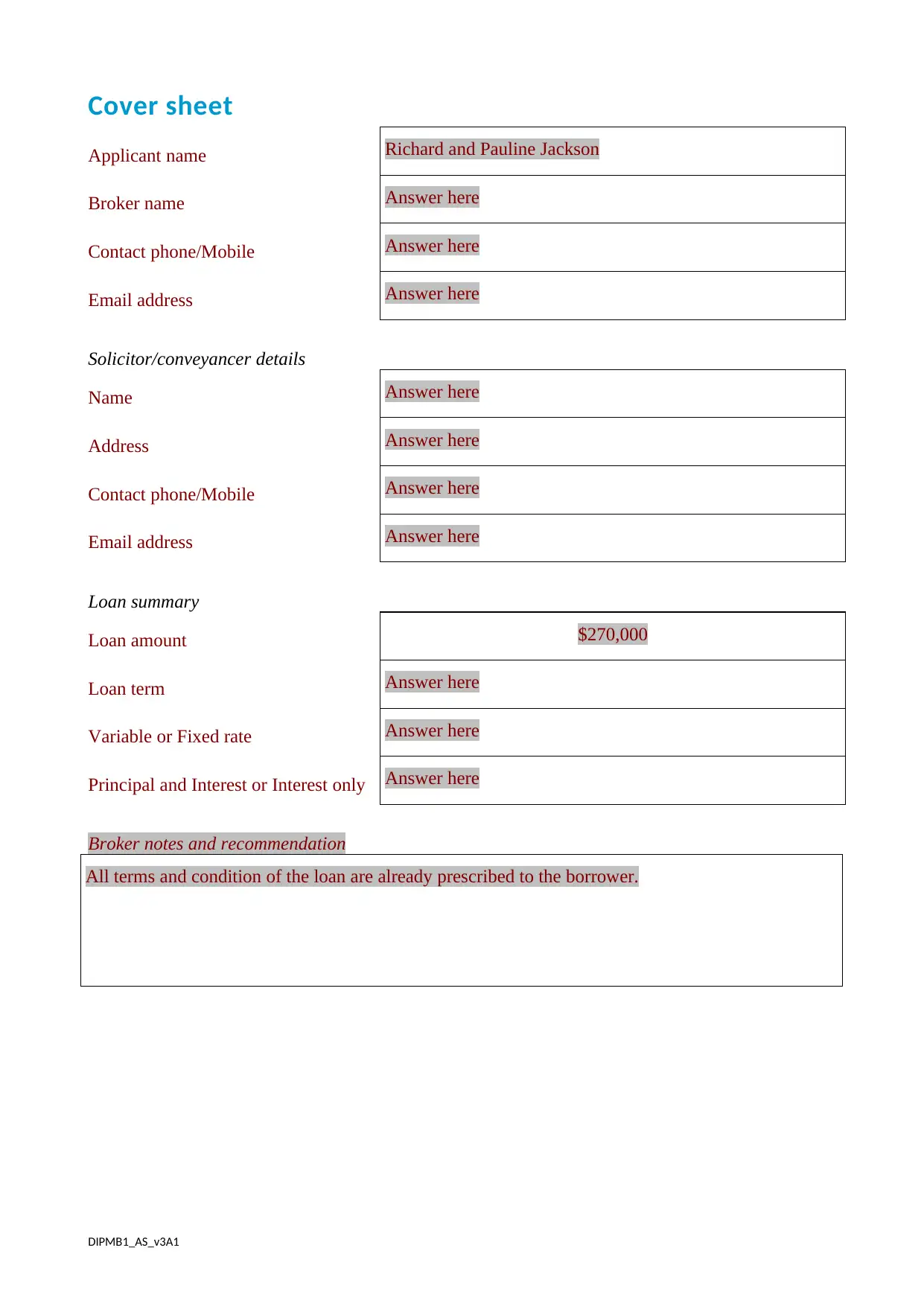

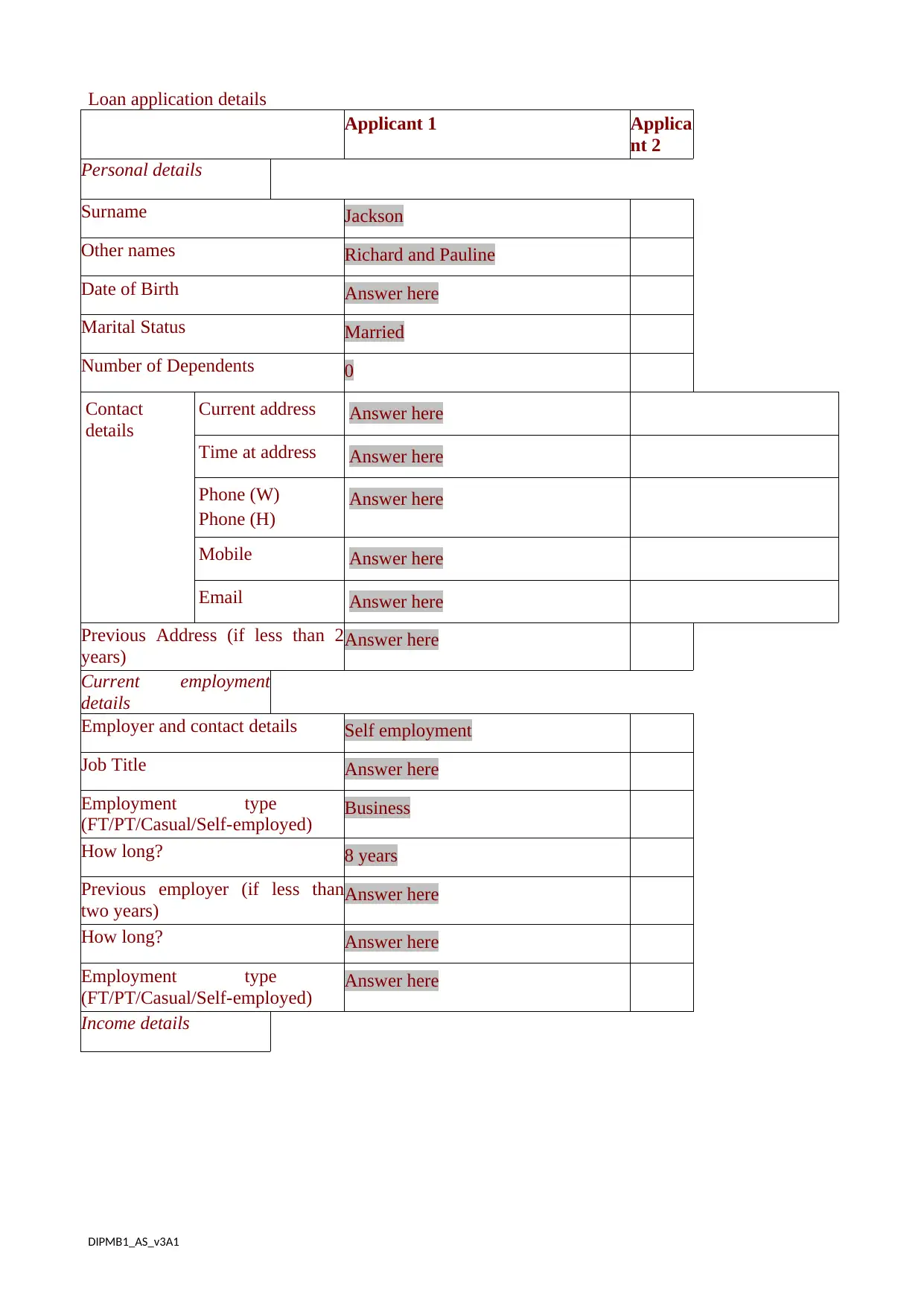

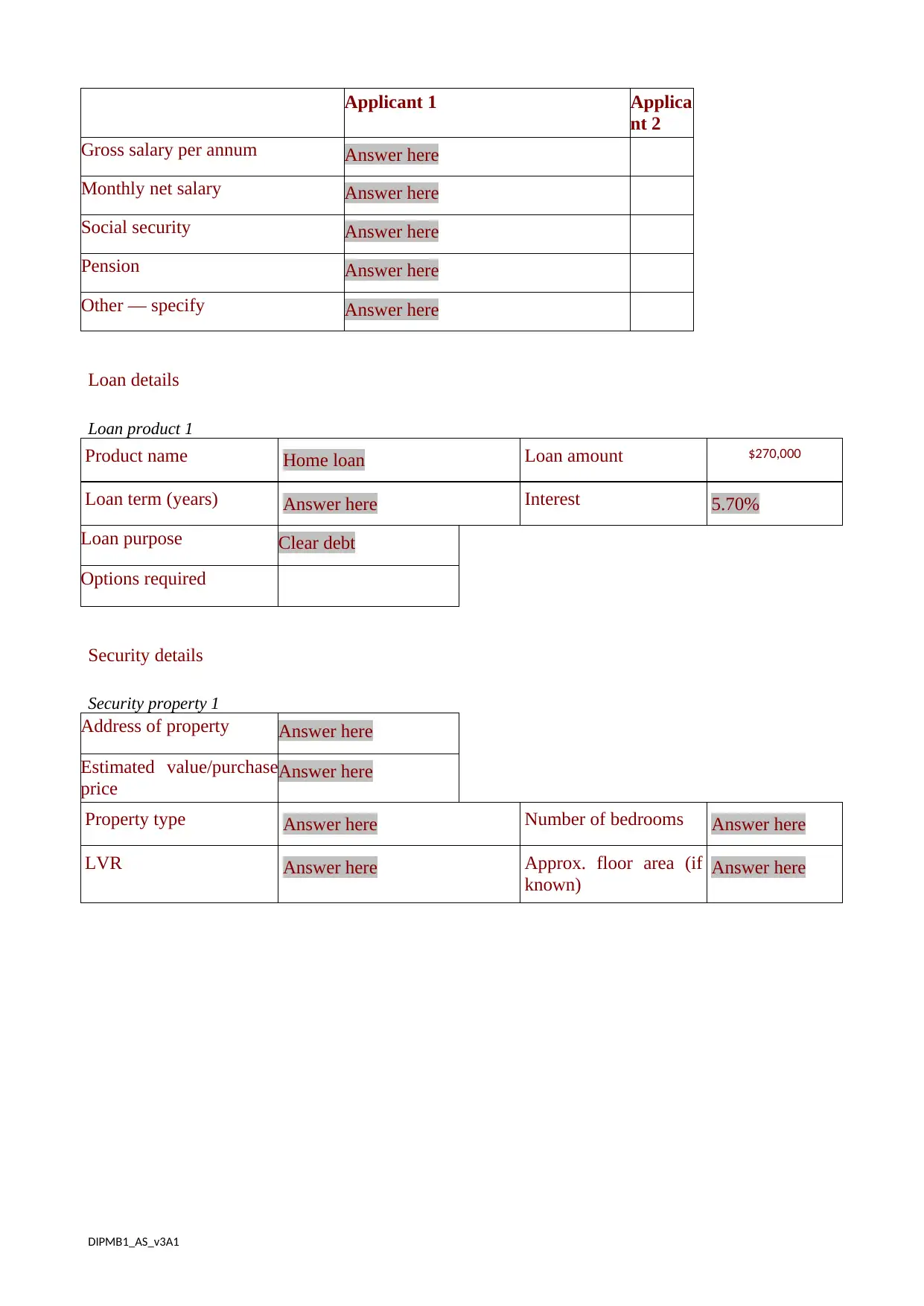

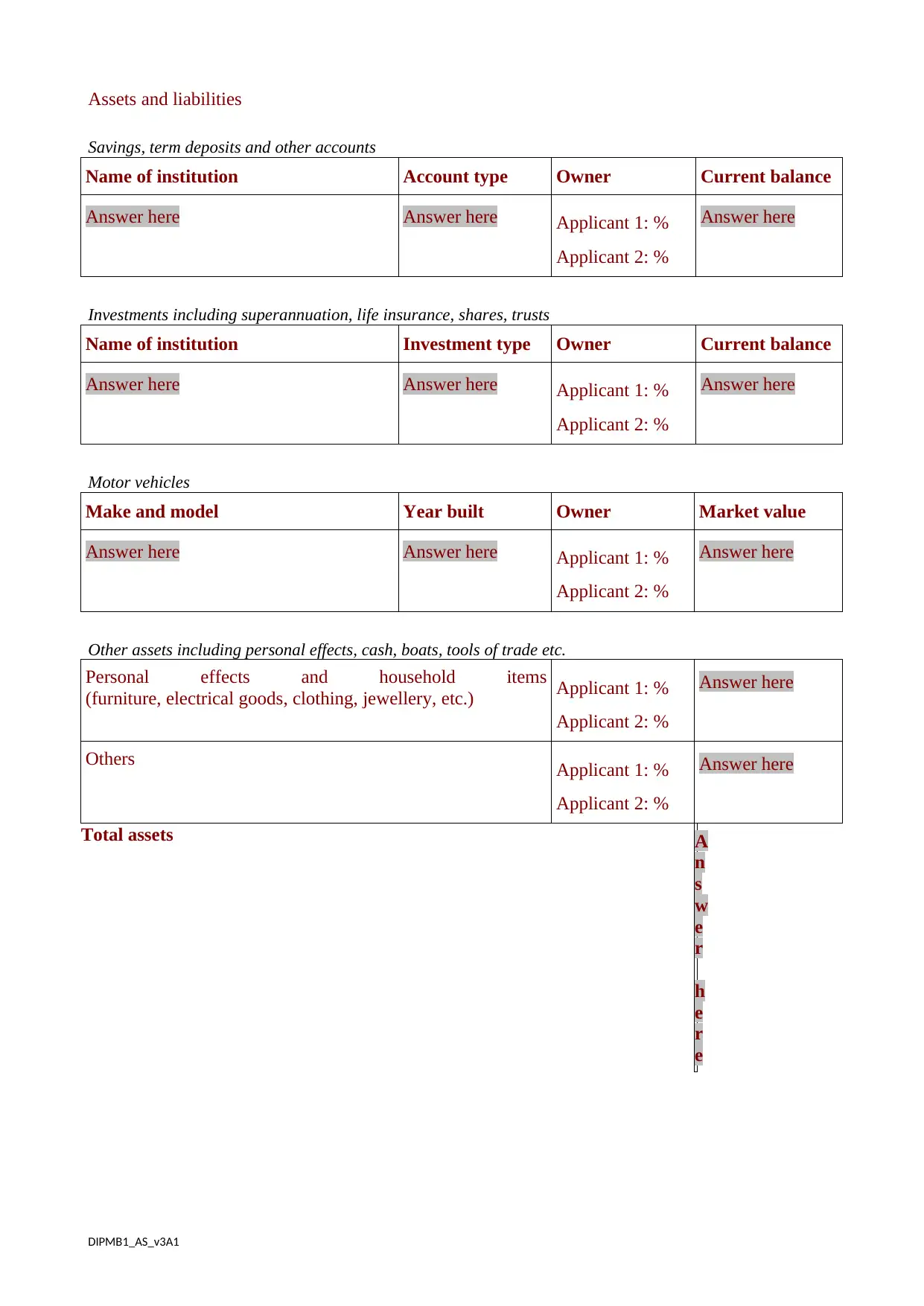

Section 2: Case study 2 — Richard and Pauline Jackson

DIPMB1_AS_v3A1

DIPMB1_AS_v3A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 8 — Responsible lending obligations

The National Consumer Credit Protection Act 2009 imposes ‘responsible lending’ obligations on

brokers that must be satisfied by all people arranging loan applications. The primary objective

under responsible lending guidelines is that the credit facility offered to the borrower is ‘not

unsuitable’ for the borrower, meets their requirements and objectives and will not create substantial

hardship.

1. Refer to ‘What is substantial hardship?’ available in the toolbox. In your own words how would

you define ‘substantial hardship’ (detailed information on this subject is found at RG 209 issued

by ASIC)? (150 words)

Student response to Task 8: Question 1

Substantial hardship is denoted as unanticipated emergency that is caused due to an event outside

of the control of an individual. Substantial hardship demonstrate as an event causes to some

financial failures over the dependents of borrower. RG 209 issues of ASIC indicated that a

product is not suited if consumer is unable to comply with financial obligation (Herbst, 2018). The

issue is related to evaluation about the individual capacity and potential of customers in respect to

the repaying obligations.

2. What are the benefits of debt consolidation for Richard and Pauline? (100 words)

Student response to Task 8: Question 2

Debt consolidation will allow the Richard and Pauline to easily manage the repayment deadline. It

further lower the interest rate over borrowing. It minimizes risk of collateral repossession. It

further regulates the fixed payment amount in respect to loans and due amount (Amurwon and

et.al., 2017). It also supports in reducing risk value. It reduces the monthly expenditure in respect

to debt repayment. This will further support the Richard and Pauline to improve the credit score.

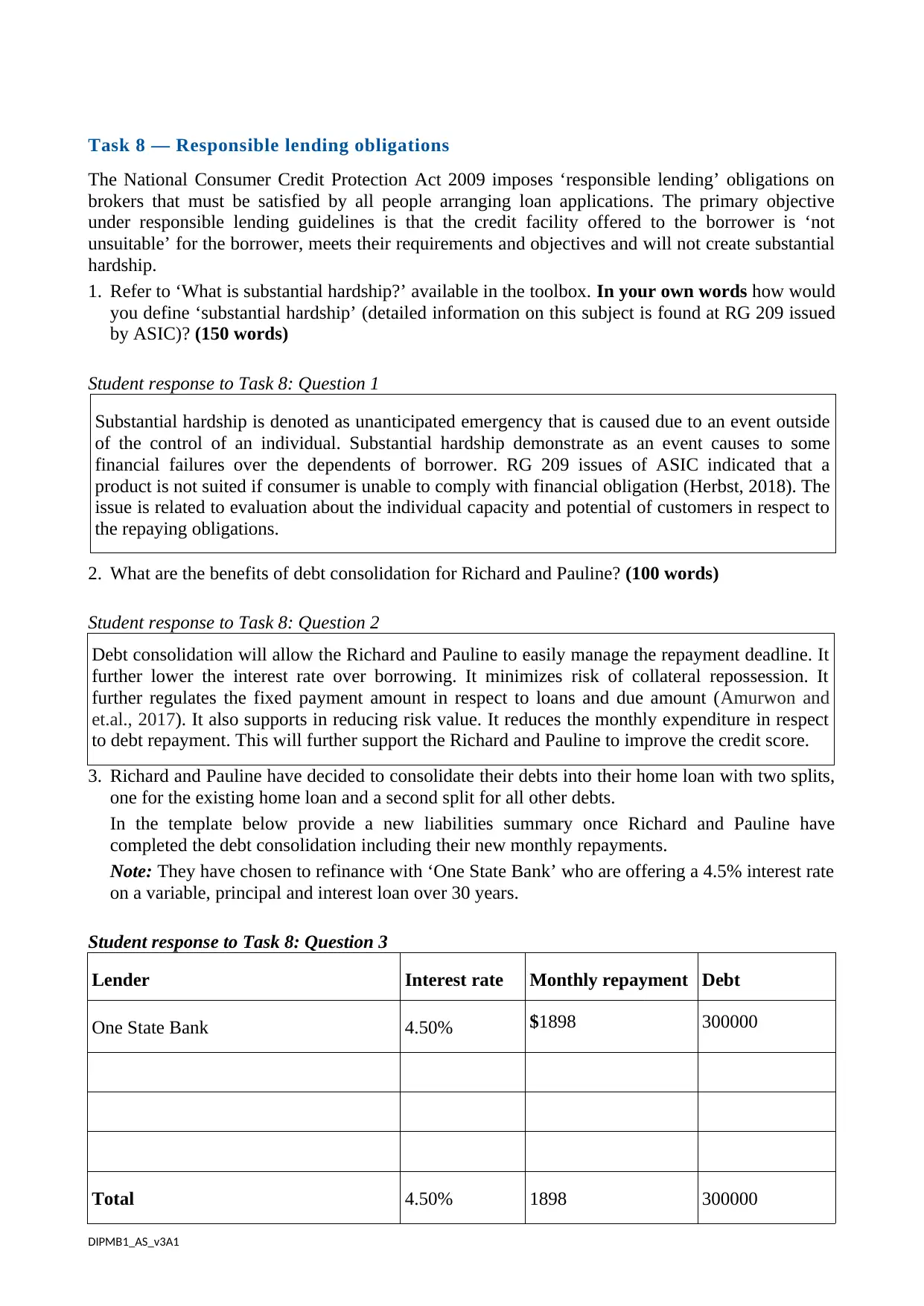

3. Richard and Pauline have decided to consolidate their debts into their home loan with two splits,

one for the existing home loan and a second split for all other debts.

In the template below provide a new liabilities summary once Richard and Pauline have

completed the debt consolidation including their new monthly repayments.

Note: They have chosen to refinance with ‘One State Bank’ who are offering a 4.5% interest rate

on a variable, principal and interest loan over 30 years.

Student response to Task 8: Question 3

Lender Interest rate Monthly repayment Debt

One State Bank 4.50% $1898 300000

Total 4.50% 1898 300000

DIPMB1_AS_v3A1

The National Consumer Credit Protection Act 2009 imposes ‘responsible lending’ obligations on

brokers that must be satisfied by all people arranging loan applications. The primary objective

under responsible lending guidelines is that the credit facility offered to the borrower is ‘not

unsuitable’ for the borrower, meets their requirements and objectives and will not create substantial

hardship.

1. Refer to ‘What is substantial hardship?’ available in the toolbox. In your own words how would

you define ‘substantial hardship’ (detailed information on this subject is found at RG 209 issued

by ASIC)? (150 words)

Student response to Task 8: Question 1

Substantial hardship is denoted as unanticipated emergency that is caused due to an event outside

of the control of an individual. Substantial hardship demonstrate as an event causes to some

financial failures over the dependents of borrower. RG 209 issues of ASIC indicated that a

product is not suited if consumer is unable to comply with financial obligation (Herbst, 2018). The

issue is related to evaluation about the individual capacity and potential of customers in respect to

the repaying obligations.

2. What are the benefits of debt consolidation for Richard and Pauline? (100 words)

Student response to Task 8: Question 2

Debt consolidation will allow the Richard and Pauline to easily manage the repayment deadline. It

further lower the interest rate over borrowing. It minimizes risk of collateral repossession. It

further regulates the fixed payment amount in respect to loans and due amount (Amurwon and

et.al., 2017). It also supports in reducing risk value. It reduces the monthly expenditure in respect

to debt repayment. This will further support the Richard and Pauline to improve the credit score.

3. Richard and Pauline have decided to consolidate their debts into their home loan with two splits,

one for the existing home loan and a second split for all other debts.

In the template below provide a new liabilities summary once Richard and Pauline have

completed the debt consolidation including their new monthly repayments.

Note: They have chosen to refinance with ‘One State Bank’ who are offering a 4.5% interest rate

on a variable, principal and interest loan over 30 years.

Student response to Task 8: Question 3

Lender Interest rate Monthly repayment Debt

One State Bank 4.50% $1898 300000

Total 4.50% 1898 300000

DIPMB1_AS_v3A1

4. What savings will Richard and Pauline obtain in monthly repayments?

(Remember to show the calculation of how you determined the savings). (100 words)

Student response to Task 8: Question 4

Richard and Pauline will save $1219 (3117 – 1898). They will get significant advantage in

repaying every monthly installment due to the inclusion of all the debts in housing loan. This

saving will further improve the buying power of the individuals. $1219 is a significant amount

that can further support the Richard and Pauline in repaying all dues and also meet the monthly

expenditure of both the individuals (Moore and Doyon, 2018).

Assessor feedback for Task 8 — Responsible lending obligations

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

(Remember to show the calculation of how you determined the savings). (100 words)

Student response to Task 8: Question 4

Richard and Pauline will save $1219 (3117 – 1898). They will get significant advantage in

repaying every monthly installment due to the inclusion of all the debts in housing loan. This

saving will further improve the buying power of the individuals. $1219 is a significant amount

that can further support the Richard and Pauline in repaying all dues and also meet the monthly

expenditure of both the individuals (Moore and Doyon, 2018).

Assessor feedback for Task 8 — Responsible lending obligations

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 9 — Self-employed special considerations

1. As Richard and Pauline are self-employed, what documents will you need to obtain to verify and

assess their income? (150 words)

Student response to Task 9: Question 1

Richard and Paulie both are business personals. They need to submit the return over the income of

business. In process of taking loan over business income tax returns needs to be submitted. Based

on the income demonstrated under the return filled total income is analysis of both Richard and

Paulie. Total income they earn are presented under the return submitted. This is a conclusive basis

to project the income of both the individuals. Income of self employers are always tough to guess

as it is impossible to predict the existing income based on previous income structure (Shulman,

2018). Income tax return will project the exact income earned by both Richard and Paulie. Eturn

contain all types of income such as salary, business, rental and all other types of sources of

income. This is the only way to identify the income of self-employed individual.

2. If a Low-doc application is an option for the customer, name three (3) extra documents you will

need to obtain and assess. Explain how each of these documents will establish their income. (150

words)

Student response to Task 9: Question 2

In case of Low doc application extra documents like borrower income declaration, ABN and

Business Activity Statement are also the additional documents that needed to be submitted by the

business entity. These documents are the additional requirements associated with the loan

application under low doc application. Borrower income declaration is the self projection of

borrower in respect to its income. This document clearly define the amount of income it earns

every month or year (Loan and et.al., 2018). ABN further demonstrate about the income of an

individual. Activity based statement also disclose all types of activities about the business

organization. Activities demonstrate about the income of the Richard and Pauline. All these

documents demonstrate about the income in different ways. In case of loan income of the borrower

play huge role as it demonstrate about the repaying capacity of the borrower. Based on the income

overall purchasing power of the borrower is identified ad which further reflect the individual

potential ability to meet up its loan liability.

3. Explain how applying for a Low-doc loan could lead the mortgage broker to be accused under

NCCP of recommending an ‘unsuitable’ product. (250 words)

Student response to Task 9: Question 3

DIPMB1_AS_v3A1

1. As Richard and Pauline are self-employed, what documents will you need to obtain to verify and

assess their income? (150 words)

Student response to Task 9: Question 1

Richard and Paulie both are business personals. They need to submit the return over the income of

business. In process of taking loan over business income tax returns needs to be submitted. Based

on the income demonstrated under the return filled total income is analysis of both Richard and

Paulie. Total income they earn are presented under the return submitted. This is a conclusive basis

to project the income of both the individuals. Income of self employers are always tough to guess

as it is impossible to predict the existing income based on previous income structure (Shulman,

2018). Income tax return will project the exact income earned by both Richard and Paulie. Eturn

contain all types of income such as salary, business, rental and all other types of sources of

income. This is the only way to identify the income of self-employed individual.

2. If a Low-doc application is an option for the customer, name three (3) extra documents you will

need to obtain and assess. Explain how each of these documents will establish their income. (150

words)

Student response to Task 9: Question 2

In case of Low doc application extra documents like borrower income declaration, ABN and

Business Activity Statement are also the additional documents that needed to be submitted by the

business entity. These documents are the additional requirements associated with the loan

application under low doc application. Borrower income declaration is the self projection of

borrower in respect to its income. This document clearly define the amount of income it earns

every month or year (Loan and et.al., 2018). ABN further demonstrate about the income of an

individual. Activity based statement also disclose all types of activities about the business

organization. Activities demonstrate about the income of the Richard and Pauline. All these

documents demonstrate about the income in different ways. In case of loan income of the borrower

play huge role as it demonstrate about the repaying capacity of the borrower. Based on the income

overall purchasing power of the borrower is identified ad which further reflect the individual

potential ability to meet up its loan liability.

3. Explain how applying for a Low-doc loan could lead the mortgage broker to be accused under

NCCP of recommending an ‘unsuitable’ product. (250 words)

Student response to Task 9: Question 3

DIPMB1_AS_v3A1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Low doc loan is a process in which lender approve the home loan of the borrower without

availability of income verification. In case of loan income verification play a huge role as it

directly demonstrate the income of the individual taking loan. This process allow the lender to

assess and analysis of the income capacity and potential of the borrower. As this process do not

required income verification that also causes to bad debt in many cases. Many times under this

practice due to the unavailability of the proper income records of the borrower lender allow the

money more than the actual capacity of the borrower. In such a circumstance the product is called

as unsuited. In context to loan suitability of borrower to meet all requirements so that there are no

further issues arises in repayment of respected loan (Wilkinson, Antoniades and Halvitigala,

2018). NCCP clearly disclosed all key requirements associated with loan payment and borrowing

terms. When any unsuited product arises in the mortgage than the broker also get accused. This

further include such loans that are taken out of the fake documentation. In case of loan documents

are essential as all further inquiries are proceeded based on the information submitted. All loans

taken based on fake documentations are disclosed as suited. This is the responsibility of the

Mortgage broker to assess the authenticity of the documents submitted in the whole transaction. If

any casual arises after the loan has been given proper inquiry over the mortgage broker is

established to identify whether the broker is under guilty or not.

Assessor feedback for Task 9 — Self-employed special considerations

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

availability of income verification. In case of loan income verification play a huge role as it

directly demonstrate the income of the individual taking loan. This process allow the lender to

assess and analysis of the income capacity and potential of the borrower. As this process do not

required income verification that also causes to bad debt in many cases. Many times under this

practice due to the unavailability of the proper income records of the borrower lender allow the

money more than the actual capacity of the borrower. In such a circumstance the product is called

as unsuited. In context to loan suitability of borrower to meet all requirements so that there are no

further issues arises in repayment of respected loan (Wilkinson, Antoniades and Halvitigala,

2018). NCCP clearly disclosed all key requirements associated with loan payment and borrowing

terms. When any unsuited product arises in the mortgage than the broker also get accused. This

further include such loans that are taken out of the fake documentation. In case of loan documents

are essential as all further inquiries are proceeded based on the information submitted. All loans

taken based on fake documentations are disclosed as suited. This is the responsibility of the

Mortgage broker to assess the authenticity of the documents submitted in the whole transaction. If

any casual arises after the loan has been given proper inquiry over the mortgage broker is

established to identify whether the broker is under guilty or not.

Assessor feedback for Task 9 — Self-employed special considerations

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 10 — Advising on strategies

Following the presentation of your proposal, Richard and Pauline say that they would like your

advice on strategies that could help them to repay their home loan as quickly as possible.

• List at least three (3) strategies or methods that will help them achieve their aim.

• Explain how each strategy will result in a home loan being repaid more quickly.

Note to students: You may refer to the MoneySmart website for information on this subject and

your answer may also include, but not be restricted to, available mobile phone apps used for debt

management. (300 words)

Student response to Task 10

Loan repayment is a process in which individual try to clear the liability. Richard and Pauline can

use strategy such as increased repayment with rise of income. They can use investment to repay the

debt value. The changes can also made in lifestyle so that buying power could have been increased.

These are the three different strategies that could have been implemented to repay the total debt

amount in a convenient way possible. These strategies will favor the Richeard and Pauline to

flexibly repay the entire loan amount. In case of long term loan like home loan where the total

tenure is approximately 30 years in time flexibility become very important as a borrower. Igf the

proper flexibility is not maintained in the loan repayment than failures can be faced by the borrower

in against to repay the entire loan value (Porzio, Sampagnaro and Verdoliva, 2020). These strategies

would support the individual to easily manage all dues against the loan repayment. Flexibility is

very important in monthly installment and other expenditure associated with the individual. Loan

repayment needed to be convenient enough especially the loans like home loan which contain the

age of 30 years. These strategies would allow them to flexibly manage all dues. These strategies

would support in restricting loan value in a certain time in process of repaying all dues. The major

emphasis in these strategies over the buying power of the individual when it comes to repaying the

overall dues.

Assessor feedback for Task 10 — Advising on strategies

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Following the presentation of your proposal, Richard and Pauline say that they would like your

advice on strategies that could help them to repay their home loan as quickly as possible.

• List at least three (3) strategies or methods that will help them achieve their aim.

• Explain how each strategy will result in a home loan being repaid more quickly.

Note to students: You may refer to the MoneySmart website for information on this subject and

your answer may also include, but not be restricted to, available mobile phone apps used for debt

management. (300 words)

Student response to Task 10

Loan repayment is a process in which individual try to clear the liability. Richard and Pauline can

use strategy such as increased repayment with rise of income. They can use investment to repay the

debt value. The changes can also made in lifestyle so that buying power could have been increased.

These are the three different strategies that could have been implemented to repay the total debt

amount in a convenient way possible. These strategies will favor the Richeard and Pauline to

flexibly repay the entire loan amount. In case of long term loan like home loan where the total

tenure is approximately 30 years in time flexibility become very important as a borrower. Igf the

proper flexibility is not maintained in the loan repayment than failures can be faced by the borrower

in against to repay the entire loan value (Porzio, Sampagnaro and Verdoliva, 2020). These strategies

would support the individual to easily manage all dues against the loan repayment. Flexibility is

very important in monthly installment and other expenditure associated with the individual. Loan

repayment needed to be convenient enough especially the loans like home loan which contain the

age of 30 years. These strategies would allow them to flexibly manage all dues. These strategies

would support in restricting loan value in a certain time in process of repaying all dues. The major

emphasis in these strategies over the buying power of the individual when it comes to repaying the

overall dues.

Assessor feedback for Task 10 — Advising on strategies

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 11 — Impact of credit history

Richard tells you that his former wife failed to properly meet their unsecured personal loan debt

obligations before they separated. Although he eventually repaid the debt, he is afraid that this

incident may count against him when he applies for a loan. There are a few things Richard can do as

he is concerned about his credit rating. What information would you provide in the following

situations?

1. Provide Richard with the details of two (2) major credit reporting agencies and explain what

information may be recorded on his credit file. Information can be sourced from the websites of

credit reporting agencies and the Office of the Australian Information Commissioner. (200

words)

Student response to Task 11: Question 1

Credit rating are the score of an individual generate out of the loan repayment. Agencies like

Experience, Equifax and Illion are directly involved under the credit rating score. These

organizations allow the banks a financial institution to identify the credit score of an individual. The

credit rating agencies analysis the credit score of the borrower based on the past history of the

individual against taking loans. IN the present case Richard re-payed the loan of his wife. The

failure of the wife in repayment of loan will not effect the Riched as the loan was take by the wife.

Also the Richrd helped his wife in repaying the due (Juru, 2019). There will be not any impact over

the credit score of the Rchrd just because it has helped the wife to repay the due installments. This

becomes essential for the individual to repay all installments on time as it affect the credit score but

in case the individual is repaying loan of its relative it will not impact over the credit score of its

own.

2. Richard has decided he would like to obtain a copy of his credit report from either Equifax or

illion Data Registries (formerly Dun & Bradstreet). Explain what options are available for the

chosen provider, how long it takes to obtain a copy, and the associated costs. (100 words)

Student response to Task 11: Question 2

Time required for the agencies like Equifax and Illion to provide the copy of credit score is 30 to 45

days. This time is the maximum expected time needed for these agencies to provide the copy. There

is a set procedure through which an individual can apply in these agencies in order to get the copy

of the credit score.

3. If there are errors on file, what are the options for Richard to follow in order to have these errors

rectified? To assist you with answering this question, refer to the Equifax website. (150 words)

Student response to Task 11: Question 3

In case of any error in the credit score occurred individual can apply over the help center to rectify

such an error. This will take some time to respond the help center. Instructor will help the individual

in guiding the further process to erase such an error (Namvar and et.al.,, 2018). Help center

executive will listen to the person and based on that it give a instant solution of the problem. This

will favor the individual in solving any query and doubt related to the credit score ratings.

DIPMB1_AS_v3A1

Richard tells you that his former wife failed to properly meet their unsecured personal loan debt

obligations before they separated. Although he eventually repaid the debt, he is afraid that this

incident may count against him when he applies for a loan. There are a few things Richard can do as

he is concerned about his credit rating. What information would you provide in the following

situations?

1. Provide Richard with the details of two (2) major credit reporting agencies and explain what

information may be recorded on his credit file. Information can be sourced from the websites of

credit reporting agencies and the Office of the Australian Information Commissioner. (200

words)

Student response to Task 11: Question 1

Credit rating are the score of an individual generate out of the loan repayment. Agencies like

Experience, Equifax and Illion are directly involved under the credit rating score. These

organizations allow the banks a financial institution to identify the credit score of an individual. The

credit rating agencies analysis the credit score of the borrower based on the past history of the

individual against taking loans. IN the present case Richard re-payed the loan of his wife. The

failure of the wife in repayment of loan will not effect the Riched as the loan was take by the wife.

Also the Richrd helped his wife in repaying the due (Juru, 2019). There will be not any impact over

the credit score of the Rchrd just because it has helped the wife to repay the due installments. This

becomes essential for the individual to repay all installments on time as it affect the credit score but

in case the individual is repaying loan of its relative it will not impact over the credit score of its

own.

2. Richard has decided he would like to obtain a copy of his credit report from either Equifax or

illion Data Registries (formerly Dun & Bradstreet). Explain what options are available for the

chosen provider, how long it takes to obtain a copy, and the associated costs. (100 words)

Student response to Task 11: Question 2

Time required for the agencies like Equifax and Illion to provide the copy of credit score is 30 to 45

days. This time is the maximum expected time needed for these agencies to provide the copy. There

is a set procedure through which an individual can apply in these agencies in order to get the copy

of the credit score.

3. If there are errors on file, what are the options for Richard to follow in order to have these errors

rectified? To assist you with answering this question, refer to the Equifax website. (150 words)

Student response to Task 11: Question 3

In case of any error in the credit score occurred individual can apply over the help center to rectify

such an error. This will take some time to respond the help center. Instructor will help the individual

in guiding the further process to erase such an error (Namvar and et.al.,, 2018). Help center

executive will listen to the person and based on that it give a instant solution of the problem. This

will favor the individual in solving any query and doubt related to the credit score ratings.

DIPMB1_AS_v3A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. What obligation does the Privacy Act imposes on the Lender to supply the client, in terms of

certain information, if they decline an application due to the content of the credit agency file?

(100 words)

Student response to Task 11: Question 4

Information or data protection act is applicable over the financial institutions. They should not be

disclose any personal information of client with anyone. In case of any breach in this legislation the

respected bank and institution will have to bear the legal obligation. Proper compensation will have

to bear to the lender in case of breach of the agreement. Information is very crucial and in case of

any transaction occurred in the banking sector institute carry the responsibility where they can not

share the information of client with any other individual.

5. What alternate options can you suggest to Richard and Pauline in the event that the loan was

rejected by the lender you initially proposed due to a credit report? (150 words)

Student response to Task 11: Question 5

Richard and Pauline can apply in other institutions and banking organizations for the same loan.

This is an instant option available in front of them in case of loan application get rejected due to the

low credit score. Further they contain an option where they can wait form the few months like two

or three to get improve the credit score. There are other options like taking gold loan to improve the

credit score and then to apply back for the home loan (Kraal, Haritos and Cantley-Smith, 2020). All