Assessing Clients' Loan Application and Borrowing Options

46 Pages12076 Words72 Views

Added on 2022-12-23

About This Document

This document discusses the assessment of clients' loan application and borrowing options. It covers topics such as legislative requirements, borrowing capacity, repayment requirements, security, concessions, and potential risks. The document provides data and analysis to support the assessment.

Assessing Clients' Loan Application and Borrowing Options

Added on 2022-12-23

ShareRelated Documents

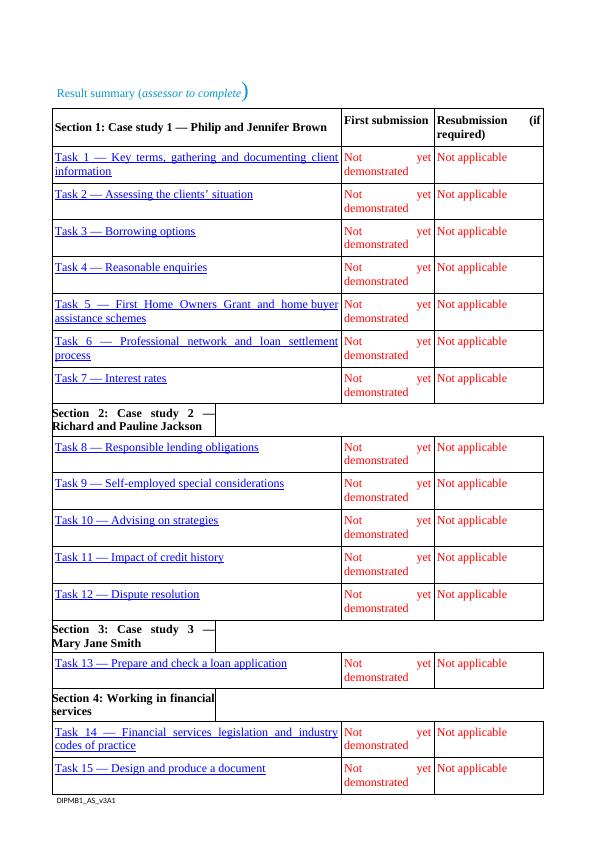

Result summary (assessor to complete)

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if

required)

Task 1 — Key terms, gathering and documenting client

information

Not yet

demonstrated

Not applicable

Task 2 — Assessing the clients’ situation Not yet

demonstrated

Not applicable

Task 3 — Borrowing options Not yet

demonstrated

Not applicable

Task 4 — Reasonable enquiries Not yet

demonstrated

Not applicable

Task 5 — First Home Owners Grant and home buyer

assistance schemes

Not yet

demonstrated

Not applicable

Task 6 — Professional network and loan settlement

process

Not yet

demonstrated

Not applicable

Task 7 — Interest rates Not yet

demonstrated

Not applicable

Section 2: Case study 2 —

Richard and Pauline Jackson

Task 8 — Responsible lending obligations Not yet

demonstrated

Not applicable

Task 9 — Self-employed special considerations Not yet

demonstrated

Not applicable

Task 10 — Advising on strategies Not yet

demonstrated

Not applicable

Task 11 — Impact of credit history Not yet

demonstrated

Not applicable

Task 12 — Dispute resolution Not yet

demonstrated

Not applicable

Section 3: Case study 3 —

Mary Jane Smith

Task 13 — Prepare and check a loan application Not yet

demonstrated

Not applicable

Section 4: Working in financial

services

Task 14 — Financial services legislation and industry

codes of practice

Not yet

demonstrated

Not applicable

Task 15 — Design and produce a document Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if

required)

Task 1 — Key terms, gathering and documenting client

information

Not yet

demonstrated

Not applicable

Task 2 — Assessing the clients’ situation Not yet

demonstrated

Not applicable

Task 3 — Borrowing options Not yet

demonstrated

Not applicable

Task 4 — Reasonable enquiries Not yet

demonstrated

Not applicable

Task 5 — First Home Owners Grant and home buyer

assistance schemes

Not yet

demonstrated

Not applicable

Task 6 — Professional network and loan settlement

process

Not yet

demonstrated

Not applicable

Task 7 — Interest rates Not yet

demonstrated

Not applicable

Section 2: Case study 2 —

Richard and Pauline Jackson

Task 8 — Responsible lending obligations Not yet

demonstrated

Not applicable

Task 9 — Self-employed special considerations Not yet

demonstrated

Not applicable

Task 10 — Advising on strategies Not yet

demonstrated

Not applicable

Task 11 — Impact of credit history Not yet

demonstrated

Not applicable

Task 12 — Dispute resolution Not yet

demonstrated

Not applicable

Section 3: Case study 3 —

Mary Jane Smith

Task 13 — Prepare and check a loan application Not yet

demonstrated

Not applicable

Section 4: Working in financial

services

Task 14 — Financial services legislation and industry

codes of practice

Not yet

demonstrated

Not applicable

Task 15 — Design and produce a document Not yet

demonstrated

Not applicable

DIPMB1_AS_v3A1

Task 1 — Key terms, gathering and documenting client information

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now

need to assess the clients’ loan application paying particular attention that you have met

legislative requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will

it cost and what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of

the Oral project requirement for this course.

Student response to Task 2: Question 1

The client is meeting all the legislative requirement of NCCP in order to borrow a home loan. It

includes that the borrower is a natural person. The charge is made for providing the credit and credit

provider provides the credit in course of a business. In the given case, the purpose of the borrower

behind borrowing home loan is to purchase and renovate the residential property for household

purpose. The maximum borrowing capacity is indicates the highest amount that the borrower can

pay for the home loan despite having all the changes that affect the borrowers borrowing capacity

such as change in interest rate (Bergmann, 2020).

The maximum borrowing capacity of the Philip and Jennifer is $1,519,000. The total loan amount

of the Philip and Jennifer is $446424 which is 440000 + 1.46% (LMI). The capacity of the client to

meet deposit is 10% which is $50000 and the clients are able to meet the capacity of the deposit.

The capacity of the Philip and Jennifer to meet the deposit amount is less than the total contribution

of $50000 for the loan requirement. It indicates that Philip and Jennifer are able to meet the 10% of

the initial deposit of home loan. The total cash contribution of the client for the loan requirement is

$75000 which includes $50000 of initial deposit and $25000 is the fees and charges of the lender.

The total amount of home loan required by Philips and Jennifer is $446424 at their initial stage.

Repayment requirement of the loan is that the tenure of the home loan is 30 years and the variable

interest rate of the home loan is 4.50% per year (Pawson, Milligan and Yates, 2020). The

requirement of the loan is also that the LMI is capitalized in the principal amount of the home loan.

The fortnightly repayment facility is also available to the client in order to half the repayment. The

lenders require 10% of the home's purchase price as initial deposit and remaining 90% as LVR.

Security in the case of home loan is a property security which guarantees the lenders that the

DIPMB1_AS_v3A1

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now

need to assess the clients’ loan application paying particular attention that you have met

legislative requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will

it cost and what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note: The assessment of the clients’ needs is a critical prelude to you completing Part 4 of

the Oral project requirement for this course.

Student response to Task 2: Question 1

The client is meeting all the legislative requirement of NCCP in order to borrow a home loan. It

includes that the borrower is a natural person. The charge is made for providing the credit and credit

provider provides the credit in course of a business. In the given case, the purpose of the borrower

behind borrowing home loan is to purchase and renovate the residential property for household

purpose. The maximum borrowing capacity is indicates the highest amount that the borrower can

pay for the home loan despite having all the changes that affect the borrowers borrowing capacity

such as change in interest rate (Bergmann, 2020).

The maximum borrowing capacity of the Philip and Jennifer is $1,519,000. The total loan amount

of the Philip and Jennifer is $446424 which is 440000 + 1.46% (LMI). The capacity of the client to

meet deposit is 10% which is $50000 and the clients are able to meet the capacity of the deposit.

The capacity of the Philip and Jennifer to meet the deposit amount is less than the total contribution

of $50000 for the loan requirement. It indicates that Philip and Jennifer are able to meet the 10% of

the initial deposit of home loan. The total cash contribution of the client for the loan requirement is

$75000 which includes $50000 of initial deposit and $25000 is the fees and charges of the lender.

The total amount of home loan required by Philips and Jennifer is $446424 at their initial stage.

Repayment requirement of the loan is that the tenure of the home loan is 30 years and the variable

interest rate of the home loan is 4.50% per year (Pawson, Milligan and Yates, 2020). The

requirement of the loan is also that the LMI is capitalized in the principal amount of the home loan.

The fortnightly repayment facility is also available to the client in order to half the repayment. The

lenders require 10% of the home's purchase price as initial deposit and remaining 90% as LVR.

Security in the case of home loan is a property security which guarantees the lenders that the

DIPMB1_AS_v3A1

original value of the security is higher than the loan amount and secures the loan. In this case, there

is no security provided by the Philip and Jennifer to the lender on order to secure the loan indicate

that the risk of losing the loan amount is high. In case if lender make compulsory security

requirement, then it will reduce the risk of the lenders. In this case, there is the requirement of LMI

and the cost of the cost of Lenders Mortgage Insurance is 1.46% which is $6424. Generally there

are two option is available to the borrowers in order to pay the fees of Lenders Mortgage Insurance

is an up-front fees and by capitalization in the amount of the home loan. Philips and Jennifer chose

the capitalization option to pay the fees of LMI to the lender. The loan amount that is suggestible to

the Philips and Jennifer is same $440000 that is approx 90% LVR. It is because the capacity of the

borrowers to pay the initial deposit is 50000 which is the approx 10% of the purchases price of the

home. But they can also borrow the loan up to their maximum borrowing capacity which is

$1,519,000 as per the joint annual salary and expenses of both Philip and Jennifer.

For the payment of the 50000 if initial deposit and 25000 of fees Philip and Jennifer can utilize their

joint saving account with amount $78000. The joint annual earning of the couple is $153000 and

annual expense is $33000, credit limit of $9000, personal loan payment of $2160 and the EMI of

$2262, the couple left with the saving of $81696 which indicate that the client is able to meet all

their financial obligations. Philip is a manager of the company and is not allowed for any

concession in the LMI fees and charges. But Jennifer is an accountant and as it is mentioned in the

provision of the home loan that the accountant LMI home loan is get waived if their maximum loan

value is up to $2 million and 90% of the property value is cover in the loan amount. As Jennifer is

meeting all the eligibility criteria of the LMI exemption, so lenders have to offer the no LMI home

loan to the couple in case if loan is taken by only Jennifer not jointly. As the interest rate of the

home loan is variable in nature, so it is one of the risk issue arise in future and the ability to meet

with issue is depends upon the percentage of change in interest rate.

2. (a) Most lenders stress test loan repayments by adding an additional 2–3% on to

the loan repayments to make sure a borrower can afford the repayments. If interest rates

moved 3% higher, what would Philip and Jennifer’s loan repayments be and do you think

they would be able to cope with the extra repayments? (100 words)

Student response to Task 2: Question 2(a)

In case if the interest is increased by 3%, then the variable interest rate of the home loan in the

present case moved from the 4.50% to the 7.50% which also make changes in the loan repayment

amount. When the interest rate is 4.50%, then the EMI of the loan is $2262, total interest payable is

$367883 and the total payment including interest is $814307. In case of new interest rate of the

home loan of 7.5%, the loan is increased by $859, total interest payable and total payment is

increased by $309419 (Paterson and Howell, 2018). Because of the increase in the EMI, the couple

left with the saving of $71388 which shows that they are able to meet this extra repayments.

(b) Identify appropriate product options you can present to the clients that may

remove this interest rate risk? (50 words)

Student response to Task 2: Question 2(b)

In order to remove the interest rate risk one option that the client can adopt is by going with the

fixed rate of interest (Nicholson, Skelton and Tarr, 2019). Despite this, the client can also borrow

the large amount of the loan in order to reduce the rate of the interest. Borrowing the loan equal to

80% of the property value also reduces the interest rate risk.

DIPMB1_AS_v3A1

is no security provided by the Philip and Jennifer to the lender on order to secure the loan indicate

that the risk of losing the loan amount is high. In case if lender make compulsory security

requirement, then it will reduce the risk of the lenders. In this case, there is the requirement of LMI

and the cost of the cost of Lenders Mortgage Insurance is 1.46% which is $6424. Generally there

are two option is available to the borrowers in order to pay the fees of Lenders Mortgage Insurance

is an up-front fees and by capitalization in the amount of the home loan. Philips and Jennifer chose

the capitalization option to pay the fees of LMI to the lender. The loan amount that is suggestible to

the Philips and Jennifer is same $440000 that is approx 90% LVR. It is because the capacity of the

borrowers to pay the initial deposit is 50000 which is the approx 10% of the purchases price of the

home. But they can also borrow the loan up to their maximum borrowing capacity which is

$1,519,000 as per the joint annual salary and expenses of both Philip and Jennifer.

For the payment of the 50000 if initial deposit and 25000 of fees Philip and Jennifer can utilize their

joint saving account with amount $78000. The joint annual earning of the couple is $153000 and

annual expense is $33000, credit limit of $9000, personal loan payment of $2160 and the EMI of

$2262, the couple left with the saving of $81696 which indicate that the client is able to meet all

their financial obligations. Philip is a manager of the company and is not allowed for any

concession in the LMI fees and charges. But Jennifer is an accountant and as it is mentioned in the

provision of the home loan that the accountant LMI home loan is get waived if their maximum loan

value is up to $2 million and 90% of the property value is cover in the loan amount. As Jennifer is

meeting all the eligibility criteria of the LMI exemption, so lenders have to offer the no LMI home

loan to the couple in case if loan is taken by only Jennifer not jointly. As the interest rate of the

home loan is variable in nature, so it is one of the risk issue arise in future and the ability to meet

with issue is depends upon the percentage of change in interest rate.

2. (a) Most lenders stress test loan repayments by adding an additional 2–3% on to

the loan repayments to make sure a borrower can afford the repayments. If interest rates

moved 3% higher, what would Philip and Jennifer’s loan repayments be and do you think

they would be able to cope with the extra repayments? (100 words)

Student response to Task 2: Question 2(a)

In case if the interest is increased by 3%, then the variable interest rate of the home loan in the

present case moved from the 4.50% to the 7.50% which also make changes in the loan repayment

amount. When the interest rate is 4.50%, then the EMI of the loan is $2262, total interest payable is

$367883 and the total payment including interest is $814307. In case of new interest rate of the

home loan of 7.5%, the loan is increased by $859, total interest payable and total payment is

increased by $309419 (Paterson and Howell, 2018). Because of the increase in the EMI, the couple

left with the saving of $71388 which shows that they are able to meet this extra repayments.

(b) Identify appropriate product options you can present to the clients that may

remove this interest rate risk? (50 words)

Student response to Task 2: Question 2(b)

In order to remove the interest rate risk one option that the client can adopt is by going with the

fixed rate of interest (Nicholson, Skelton and Tarr, 2019). Despite this, the client can also borrow

the large amount of the loan in order to reduce the rate of the interest. Borrowing the loan equal to

80% of the property value also reduces the interest rate risk.

DIPMB1_AS_v3A1

Task 3 — Borrowing options

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options

could you present that would avoid the cost of LMI? (100 words)

Student response to Task 3

The way that the Philips and the Jennifer couple can adopt in order to avoid the cost of the Lenders

Mortgage Insurance is by saving the bigger deposits for the purchase of the affordable loan. This

further reduces the amount of loan to low value ratio and help the couple in avoiding the LMI of the

home loan (North and Wilson, 2020). The another way to avoid the LMI of the loan is by arranging

the any family guarantee and property security in order to cover the loan security. Being a doctor,

accountant any professional service also help in avoiding the Lenders Mortgage Insurance of the

home loan.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Although Philip and Jennifer are looking to borrow at approximately 90% LVR, what other options

could you present that would avoid the cost of LMI? (100 words)

Student response to Task 3

The way that the Philips and the Jennifer couple can adopt in order to avoid the cost of the Lenders

Mortgage Insurance is by saving the bigger deposits for the purchase of the affordable loan. This

further reduces the amount of loan to low value ratio and help the couple in avoiding the LMI of the

home loan (North and Wilson, 2020). The another way to avoid the LMI of the loan is by arranging

the any family guarantee and property security in order to cover the loan security. Being a doctor,

accountant any professional service also help in avoiding the Lenders Mortgage Insurance of the

home loan.

Assessor feedback for Task 3 — Borrowing options

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 4 — Reasonable enquiries

In the course of gathering information about the couple, you are required under the National

Consumer Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s

objectives, requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study

and explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 4

Six reasonable inquiries that the lenders have to make with the clients in order to reduce the risk of

the lender:

What was the impact of the credit contract on the client when they enter into the complex

and unsuitable credit contract.

Whether the client is the new or the existing customer of the credit provider.

Whether the client has the capacity to enter into the credit contract after meeting its fixed

and variable expenses.

The current salary of the client and the nature of the source of the client salary.

The desired credit card limit of the clients and the period for which the credit is required.

Recent income tax return, payroll slip and the statement of their income from their

accountant.

The importance of inquiries about the borrower's objectives, requirements and financial situations

help the lenders to know the clients profitability and the stability (Bhutta and Keys, 2017). This

further help the lenders to know whether the client has any assets to cover the home loans security

or not. It also helps the lenders to know the deposit capacity of the clients and the nature of the

source of the income.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

In the course of gathering information about the couple, you are required under the National

Consumer Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s

objectives, requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study

and explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 4

Six reasonable inquiries that the lenders have to make with the clients in order to reduce the risk of

the lender:

What was the impact of the credit contract on the client when they enter into the complex

and unsuitable credit contract.

Whether the client is the new or the existing customer of the credit provider.

Whether the client has the capacity to enter into the credit contract after meeting its fixed

and variable expenses.

The current salary of the client and the nature of the source of the client salary.

The desired credit card limit of the clients and the period for which the credit is required.

Recent income tax return, payroll slip and the statement of their income from their

accountant.

The importance of inquiries about the borrower's objectives, requirements and financial situations

help the lenders to know the clients profitability and the stability (Bhutta and Keys, 2017). This

further help the lenders to know whether the client has any assets to cover the home loans security

or not. It also helps the lenders to know the deposit capacity of the clients and the nature of the

source of the income.

Assessor feedback for Task 4 — Reasonable enquiries

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Task 5 — First Home Owners Grant and home buyer assistance schemes

Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory, who would be eligible and what would be

their benefit? Are Philip and Jennifer eligible for any assistance?

Note: Please identify which State or Territory you are from in your answer. (150 words)

Student response to Task 5

The state from where the Philips and Jennifer belong is the New South Wales of the Australia. The

eligibility criteria available to the first home buyer assistance under First Home Owner's Grant

scheme is if a client purchase existing home having value less than 650000 then they need not to

pay any transfer duty (Bhutta and Ringo, 2017). And if the value of the property is exists between

the 650000 and the 800000 and apply for concessional transfer rate than the amount of concession

is based upon the value of existing property. In the given case, Philip and Jennifer's purchase

existing home and the property value is 490000, then they are eligible for the full exemption of the

stamp duty.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

Describe the First Home Owner’s Grant or home buyer assistance scheme benefits and stamp duty

concessions that are available in your State or Territory, who would be eligible and what would be

their benefit? Are Philip and Jennifer eligible for any assistance?

Note: Please identify which State or Territory you are from in your answer. (150 words)

Student response to Task 5

The state from where the Philips and Jennifer belong is the New South Wales of the Australia. The

eligibility criteria available to the first home buyer assistance under First Home Owner's Grant

scheme is if a client purchase existing home having value less than 650000 then they need not to

pay any transfer duty (Bhutta and Ringo, 2017). And if the value of the property is exists between

the 650000 and the 800000 and apply for concessional transfer rate than the amount of concession

is based upon the value of existing property. In the given case, Philip and Jennifer's purchase

existing home and the property value is 490000, then they are eligible for the full exemption of the

stamp duty.

Assessor feedback for Task 5 — First Home Owners Grant and home buyer assistance schemes

(Insert Feedback)

Question(s) that need to be resubmitted

(if required)

(List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

DIPMB1_AS_v3A1

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

FNS40815 FNSCRD301 Assessment 2 - Performancelg...

|5

|1965

|486

Industry Knowledge and the Lending Processlg...

|55

|10804

|47

Case Study 1: Philip and Jennifer Brownlg...

|91

|19289

|44

Case Study 1: Philip and Jennifer Brownlg...

|69

|19259

|1

Case Study 1: Philip and Jennifer Brownlg...

|68

|18816

|493

Industry Knowledge and the Lending Processlg...

|51

|16017

|1