An Examination of the Influence of Accounting Practices in SMEs

VerifiedAdded on 2022/11/13

|13

|3433

|424

Report

AI Summary

This report investigates the influence of accounting practices on Small and Medium Enterprises (SMEs). The study aims to determine how accounting practices affect SME operations, including cost reduction and overall financial performance. The research employs a descriptive survey design, focusing on a sample of 100 SMEs from various sectors like manufacturing, trading, and services. The research questions address the role of accounting practices and the benefits SMEs expect from professional accountants. The report highlights the importance of accounting in SMEs, especially in developing economies, and acknowledges the challenges these enterprises face due to inadequate accounting practices. The methodology includes a literature review, ethical considerations, and data collection through questionnaires and interviews, with statistical analysis used to interpret the findings. The study also explores the delimitations and limitations, such as the scope of the survey and time constraints. The findings are expected to offer insights into the impact of accounting on SME operations, contributing to a better understanding of financial management in these businesses.

Influence Of Accounting Practices In Small And Medium Enterprises 1

INFLUENCE OF ACCOUNTING PRACTICES IN SMALL AND MEDIUM ENTERPRISES

Name:

Institution:

Course:

Tutor:

Date:

INFLUENCE OF ACCOUNTING PRACTICES IN SMALL AND MEDIUM ENTERPRISES

Name:

Institution:

Course:

Tutor:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Influence Of Accounting Practices In Small And Medium Enterprises 2

Abstract

Small alongside medium enterprises act as the backbone of every business and commerce

by creating several entrepreneurs, involving different stakeholders, creating job opportunities for

a skilled and half skilled workforce. The main purpose of this survey is to determinant how

accounting practices influence operations of small alongside medium enterprises (SMEs) in

different regions around the global community. The primary research inquiry of this examination

includes: What is the role of accountant practices in SME’s? and what kind of benefits, SME’s

expect from professional accountants? The use of descriptive survey design will be embraced for

the survey. Besides, targeted population for units used in this study will include a population of

130 SMEs as respondents and a sample of 100 respondents will be used in this survey. Data

present in the Ministry that deal with trade along with industrialization will be used to include 60

SMEs in the manufacturing sector, 25 SMEs in trading sectors, together with 15 SMEs in the

service centers will be used. The use of stratified sampling technique will be applied as a way of

determining the sample size of one hundred from entire population in the research. For this

examination, vital information will be gathered by well-prepared questionnaires founded on

identified survey questions supplemented by follow up face to face interview. Besides,

descriptive statistics will be used during the analysis process..

Research problem

In most countries such as in Australia, SMEs sectors are considered as major contributors

to financial stability. These enterprises provide income along with employment to a major

portion of people in most nations. The different survey has reported that SMEs contribute to over

seventy per cent of newly created jobs in a single year (Zotorvie 2017). Despite the importance

Abstract

Small alongside medium enterprises act as the backbone of every business and commerce

by creating several entrepreneurs, involving different stakeholders, creating job opportunities for

a skilled and half skilled workforce. The main purpose of this survey is to determinant how

accounting practices influence operations of small alongside medium enterprises (SMEs) in

different regions around the global community. The primary research inquiry of this examination

includes: What is the role of accountant practices in SME’s? and what kind of benefits, SME’s

expect from professional accountants? The use of descriptive survey design will be embraced for

the survey. Besides, targeted population for units used in this study will include a population of

130 SMEs as respondents and a sample of 100 respondents will be used in this survey. Data

present in the Ministry that deal with trade along with industrialization will be used to include 60

SMEs in the manufacturing sector, 25 SMEs in trading sectors, together with 15 SMEs in the

service centers will be used. The use of stratified sampling technique will be applied as a way of

determining the sample size of one hundred from entire population in the research. For this

examination, vital information will be gathered by well-prepared questionnaires founded on

identified survey questions supplemented by follow up face to face interview. Besides,

descriptive statistics will be used during the analysis process..

Research problem

In most countries such as in Australia, SMEs sectors are considered as major contributors

to financial stability. These enterprises provide income along with employment to a major

portion of people in most nations. The different survey has reported that SMEs contribute to over

seventy per cent of newly created jobs in a single year (Zotorvie 2017). Despite the importance

Influence Of Accounting Practices In Small And Medium Enterprises 3

of SME in different regions, different surveys have recorded that three out of five business

operations fail within three years after their establishments (Cuzdriorean 2017). For instance,

failure in operations of SMEs results in loss of occupations and then results to increase in

instances of insecurity, depleted liquidity in market, as well as declined financial progress.

Research question

The study has the expectation of finding appropriate answers to several questions under

investigation. Some of the important research question in this examination comprises of;

i. What is the role of accountant practices in SME’s?

ii. What kind of benefits, SME’s expect from professional accountants?

Hypothesis

In reference to literature work, this examination target at offering deal answers on impact of

accounting operations on operations of SMEs. This proposal of the survey will aim ate checking

the subjected hypotheses with the aim of attaining the best conclusion on the issue under

examination.

First Hypothesis

H0: Accounting practices influence the operations of SMEs.

H1: Accounting practices do not pose any impact on operations of SMEs.

Hypothesis 2

H0: Accounting practices influence the cost reduction in operations of SMEs

of SME in different regions, different surveys have recorded that three out of five business

operations fail within three years after their establishments (Cuzdriorean 2017). For instance,

failure in operations of SMEs results in loss of occupations and then results to increase in

instances of insecurity, depleted liquidity in market, as well as declined financial progress.

Research question

The study has the expectation of finding appropriate answers to several questions under

investigation. Some of the important research question in this examination comprises of;

i. What is the role of accountant practices in SME’s?

ii. What kind of benefits, SME’s expect from professional accountants?

Hypothesis

In reference to literature work, this examination target at offering deal answers on impact of

accounting operations on operations of SMEs. This proposal of the survey will aim ate checking

the subjected hypotheses with the aim of attaining the best conclusion on the issue under

examination.

First Hypothesis

H0: Accounting practices influence the operations of SMEs.

H1: Accounting practices do not pose any impact on operations of SMEs.

Hypothesis 2

H0: Accounting practices influence the cost reduction in operations of SMEs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Influence Of Accounting Practices In Small And Medium Enterprises 4

H1: Accounting practices do not pose any impact on the reduction in cost in operations of

SMEs

Delimitations and limitations

The application of a specified test remains as big restriction in this survey. The study only

focused on a particular number of SMEs while there are various enterprises around the

Australian community. Such ideas might be ineffective in attaining the appropriate solution on

whether accounting activities impact the operations of SMEs. Due to time constraint in

conducting the research in this diverse field that involves many enterprises make it tough for the

surveyor to attain an effective outcome (Haider, Munajat, and Kamarulzaman 2013). The study

requires huge sum of funds in order for plan to attain its completion.

Background

It is clear from most researches that SME plays a fundamental purpose in the economy

especially for countries that are still developing as well as economically emerging states.

Different accounting operations of SMEs do not necessarily provide complete as well as

pertinent financial data required to improve financial choices made by various business operators

(Asirah 2018). It has been noted with a lot of concern that the majority of SMEs around various

markets such as in Australia does not maintain comprehensive accounting reports. The lack of

appropriate documentation of accounting by such enterprise does arise because of lack of

effective knowledge of accounting. Besides, most SMEs fail to prepare financial records at all

during their operations, hence, the financial assessment is not done as a result. Therefore, all

these instances within the operations of SMEs have to lead to the primary target of this research

proposal. The chief target is thus to investigate the impacts of accounting activities within SMEs

H1: Accounting practices do not pose any impact on the reduction in cost in operations of

SMEs

Delimitations and limitations

The application of a specified test remains as big restriction in this survey. The study only

focused on a particular number of SMEs while there are various enterprises around the

Australian community. Such ideas might be ineffective in attaining the appropriate solution on

whether accounting activities impact the operations of SMEs. Due to time constraint in

conducting the research in this diverse field that involves many enterprises make it tough for the

surveyor to attain an effective outcome (Haider, Munajat, and Kamarulzaman 2013). The study

requires huge sum of funds in order for plan to attain its completion.

Background

It is clear from most researches that SME plays a fundamental purpose in the economy

especially for countries that are still developing as well as economically emerging states.

Different accounting operations of SMEs do not necessarily provide complete as well as

pertinent financial data required to improve financial choices made by various business operators

(Asirah 2018). It has been noted with a lot of concern that the majority of SMEs around various

markets such as in Australia does not maintain comprehensive accounting reports. The lack of

appropriate documentation of accounting by such enterprise does arise because of lack of

effective knowledge of accounting. Besides, most SMEs fail to prepare financial records at all

during their operations, hence, the financial assessment is not done as a result. Therefore, all

these instances within the operations of SMEs have to lead to the primary target of this research

proposal. The chief target is thus to investigate the impacts of accounting activities within SMEs

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Influence Of Accounting Practices In Small And Medium Enterprises 5

(Hawari and Nassar 2018). Moreover, accounting practices and system remain to be the

methodical, well-structured technique for long accurate financial data and controls. The use of

accounting in different operations of SMEs help in sowing the books, statements, files, vouchers,

and other supporting information that result from the use of different processes of accounting.

For instance, in Australia, there are over 100 SMEs (R, Ali, and MS 2017). Among these

enterprises, researchers have shown that a huge number of businesses do not use accounting

practices.

Ethical consideration

Ethics consideration in this research on the influence of accounting on SMEs stays to be

the different collection of guidelines. These regulations govern expectations of different

individual’s together with behaviors of either respondent or interviewer during the exercise of

carrying out the investigation. Ethics in this research work are crucial as it forms the part of the

investigation. Such issues of ethics determine different to do and don't before, during, and after

investigation (Glattke 2017). For instance, there is an important need to respect every

individual’s opinion pertaining to their views on impact of accounting activities on the

operations of SMEs. Therefore, this issue ensures that every respondent is not in any way ready

to receive a subjection to harm in the process of investigation. There is an ethical consideration

of attaining the consent of the respondent. For instance, each and every respondent and

interviewer must have consent before starting the examination. The consent must be obtained

before the investigator can be able to administer a questionnaire to respondents to answer

questions. Besides, the protection of the identity of every respondent is an important ethical

consideration in this study. The protection of identity will ensure that each and every participant

that wishes to take part in the study are unworried about their views that they will air out on how

(Hawari and Nassar 2018). Moreover, accounting practices and system remain to be the

methodical, well-structured technique for long accurate financial data and controls. The use of

accounting in different operations of SMEs help in sowing the books, statements, files, vouchers,

and other supporting information that result from the use of different processes of accounting.

For instance, in Australia, there are over 100 SMEs (R, Ali, and MS 2017). Among these

enterprises, researchers have shown that a huge number of businesses do not use accounting

practices.

Ethical consideration

Ethics consideration in this research on the influence of accounting on SMEs stays to be

the different collection of guidelines. These regulations govern expectations of different

individual’s together with behaviors of either respondent or interviewer during the exercise of

carrying out the investigation. Ethics in this research work are crucial as it forms the part of the

investigation. Such issues of ethics determine different to do and don't before, during, and after

investigation (Glattke 2017). For instance, there is an important need to respect every

individual’s opinion pertaining to their views on impact of accounting activities on the

operations of SMEs. Therefore, this issue ensures that every respondent is not in any way ready

to receive a subjection to harm in the process of investigation. There is an ethical consideration

of attaining the consent of the respondent. For instance, each and every respondent and

interviewer must have consent before starting the examination. The consent must be obtained

before the investigator can be able to administer a questionnaire to respondents to answer

questions. Besides, the protection of the identity of every respondent is an important ethical

consideration in this study. The protection of identity will ensure that each and every participant

that wishes to take part in the study are unworried about their views that they will air out on how

Influence Of Accounting Practices In Small And Medium Enterprises 6

accounting practices affect operations of SMEs in any region of their interest (Glattke 2017).

Through appropriate consideration of above ethics, the surveyor can be able to obtain much-

needed data for the examination.

Literature review

This section of research proposal represents the foregoing reflected studies of the

accounting system from pros as well as cons corner of assessment. It is evident from SMEs

sectors are progressively termed as essential engine useful in the development of employment as

well as advancement in the economy. The issue has been demanded by increasing knowledge

within authority that massive schemes in industrial area are less probable to produce necessary

chances of employment given an enhanced concentration of capital of yield in the sector.

Moreover, accounting practices have been viewed to be the critical element for the financial

presentation of SMEs (Tabot and Kamala 2016). Limit to accounting practices hinder advance

operational charges than larger ventures in attaining recognition. Additionally, poor management

practices along with accounting practices are also some of the major factors that hinder the

financial performance of these firms. Accounting practices, for instance, hamper the capacity of

SMEs to increase finance. Asymmetries of data linked with loaning to borrowers that borrow on

small portion have a limited stream of finance to smaller corporations. Despite all these assets,

some other examinations have suggested that a huge number of SMEs are unsuccessful because

of non-economical purposes. Du, Jiang, and Ji (2017) noted that poor accounting practices that

result in deprived record maintenance are chief contributors to letdown of SMEs. It was

suggested by Abimbola and Kolawole (2017) that inadequate fundamental business

administration practices with abilities needed for record keeping lead to failure in operations of

SMEs around different nations.

accounting practices affect operations of SMEs in any region of their interest (Glattke 2017).

Through appropriate consideration of above ethics, the surveyor can be able to obtain much-

needed data for the examination.

Literature review

This section of research proposal represents the foregoing reflected studies of the

accounting system from pros as well as cons corner of assessment. It is evident from SMEs

sectors are progressively termed as essential engine useful in the development of employment as

well as advancement in the economy. The issue has been demanded by increasing knowledge

within authority that massive schemes in industrial area are less probable to produce necessary

chances of employment given an enhanced concentration of capital of yield in the sector.

Moreover, accounting practices have been viewed to be the critical element for the financial

presentation of SMEs (Tabot and Kamala 2016). Limit to accounting practices hinder advance

operational charges than larger ventures in attaining recognition. Additionally, poor management

practices along with accounting practices are also some of the major factors that hinder the

financial performance of these firms. Accounting practices, for instance, hamper the capacity of

SMEs to increase finance. Asymmetries of data linked with loaning to borrowers that borrow on

small portion have a limited stream of finance to smaller corporations. Despite all these assets,

some other examinations have suggested that a huge number of SMEs are unsuccessful because

of non-economical purposes. Du, Jiang, and Ji (2017) noted that poor accounting practices that

result in deprived record maintenance are chief contributors to letdown of SMEs. It was

suggested by Abimbola and Kolawole (2017) that inadequate fundamental business

administration practices with abilities needed for record keeping lead to failure in operations of

SMEs around different nations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Influence Of Accounting Practices In Small And Medium Enterprises 7

Practices of accounting along with economic reporting of SMEs

In most fields, regulations require various SMEs to set up different monetary records and

regularly have them reviewed from time to time. In most instances, financial practices are

categorized with authority, positioned on different online sites or prepared ready upon request.

Ahmad (2013), all corporations are needed to maintain appropriate reports of financial

statements in fulfillment with companies act. The organization has the mandate to prepare and

submit tax authority to different governments with an agreement with several pieces of

legislation of tax. Examination by AlKhajeh and Azam (2018) concludes that different

governmental policies are primary drivers as to why different SMEs need to organize economic

records.

Tabot and Kamala (2016) conclude their study by reporting that amount of accounting

exercises in SMEs is reliant on number of working environmental elements that comprise of

business size together with an alliance of industry. It is further reported that most owners, as well

as directors of SMEs, connect with public accountants to organize much-needed data as directors

look for extra data, but to a restricted degree. Research by R, Ali, and MS (2017) ends by

indicating that advancement of resonance accounting data structure within SMEs relies greatly

on quantity of accounting skill of owners of the firm. Glattke (2017) and Mbogo (2017) had a

common view that SMEs use specialized accounting for researching for yearly information and

for different requirements of accounting. Haider, Munajat, and Kamarulzaman (2013) on their

part agreed that expert accountants need to make their operations to comprise of graphics

arrangements and explanation of amount in economical records. It was recorded by Abimbola

and Kolawole (2017)that high charge of hiring accountants leaves SMEs owners or managers

with little or no alternative but to consign accounting administration of data. Zotorvie (2017)

Practices of accounting along with economic reporting of SMEs

In most fields, regulations require various SMEs to set up different monetary records and

regularly have them reviewed from time to time. In most instances, financial practices are

categorized with authority, positioned on different online sites or prepared ready upon request.

Ahmad (2013), all corporations are needed to maintain appropriate reports of financial

statements in fulfillment with companies act. The organization has the mandate to prepare and

submit tax authority to different governments with an agreement with several pieces of

legislation of tax. Examination by AlKhajeh and Azam (2018) concludes that different

governmental policies are primary drivers as to why different SMEs need to organize economic

records.

Tabot and Kamala (2016) conclude their study by reporting that amount of accounting

exercises in SMEs is reliant on number of working environmental elements that comprise of

business size together with an alliance of industry. It is further reported that most owners, as well

as directors of SMEs, connect with public accountants to organize much-needed data as directors

look for extra data, but to a restricted degree. Research by R, Ali, and MS (2017) ends by

indicating that advancement of resonance accounting data structure within SMEs relies greatly

on quantity of accounting skill of owners of the firm. Glattke (2017) and Mbogo (2017) had a

common view that SMEs use specialized accounting for researching for yearly information and

for different requirements of accounting. Haider, Munajat, and Kamarulzaman (2013) on their

part agreed that expert accountants need to make their operations to comprise of graphics

arrangements and explanation of amount in economical records. It was recorded by Abimbola

and Kolawole (2017)that high charge of hiring accountants leaves SMEs owners or managers

with little or no alternative but to consign accounting administration of data. Zotorvie (2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Influence Of Accounting Practices In Small And Medium Enterprises 8

proposed that the application of software of bookkeeping by directors in SMEs to enhance

operations of accounting. Such practices are improved but creators of accounting software are

about to create another medium-sized application for SMEs.

The previous investigation of the user of economical records in SMEs exposed that

different proprietors, tax systems, managers, and borrowers are chief consumers. As recorded by

Du, Jiang, and Ji (2018), contemporary assessment is recording that number of different

consumers of accounting practices and data within SMEs is improving. The increase is with the

aim of including venture entrepreneurs alongside clients in different chains of supply. Moreover,

Tabot and Kamala (2016) in their study concluded that accounting practices together with

marketing pose a huge challenge to the management of SMEs. The study further recommends

that the management of SMEs need to learn how to use accounting or hire specialists in order to

improve their competitiveness while using different accounting practices. The conventional

accounting reporting according to Hawari and Nassar (2018) plays a significant purpose in

operations of SMEs. However, it is also reported that operational records need to be altered in

order for them to be used. There is a need for the management of such enterprises of proposes

the proper application of cases basics more willingly than accruals foundation. Some authors

such as Tabot and Kamala (2016) have argued that financial recording ideas within SMEs seem

to fail to be dictated by several external economical recording necessities that are present for

their operations for them.

Aim or objectives of the research

The chief target of this examination is to examine influence of accounting operations in SMEs.

Other precise aims of this research work comprise of the need;

proposed that the application of software of bookkeeping by directors in SMEs to enhance

operations of accounting. Such practices are improved but creators of accounting software are

about to create another medium-sized application for SMEs.

The previous investigation of the user of economical records in SMEs exposed that

different proprietors, tax systems, managers, and borrowers are chief consumers. As recorded by

Du, Jiang, and Ji (2018), contemporary assessment is recording that number of different

consumers of accounting practices and data within SMEs is improving. The increase is with the

aim of including venture entrepreneurs alongside clients in different chains of supply. Moreover,

Tabot and Kamala (2016) in their study concluded that accounting practices together with

marketing pose a huge challenge to the management of SMEs. The study further recommends

that the management of SMEs need to learn how to use accounting or hire specialists in order to

improve their competitiveness while using different accounting practices. The conventional

accounting reporting according to Hawari and Nassar (2018) plays a significant purpose in

operations of SMEs. However, it is also reported that operational records need to be altered in

order for them to be used. There is a need for the management of such enterprises of proposes

the proper application of cases basics more willingly than accruals foundation. Some authors

such as Tabot and Kamala (2016) have argued that financial recording ideas within SMEs seem

to fail to be dictated by several external economical recording necessities that are present for

their operations for them.

Aim or objectives of the research

The chief target of this examination is to examine influence of accounting operations in SMEs.

Other precise aims of this research work comprise of the need;

Influence Of Accounting Practices In Small And Medium Enterprises 9

To investigate the manner in which accounting practices influence operations of

SMEs around different markets

To examine benefits that the accounting practices have on activities that relate to

operations of SMEs.

Methodology

This section comprises the description of different procedures and techniques that will be

utilized in conducting this survey. It consists of the report of effective research methodology to

be used, the population of the study. The section also comprises of different sampling

techniques, method of gathering data, as well as techniques of analyzing data.

Design of research

This survey will be managed via descriptive case examination research plan. This plan

will be appropriate as it will permit for the thorough examination of different aspects that impact

financial presentation of SMEs. As stated by Sousa (2014), a case study in research work

consists of a careful as well as an inclusive examination of the societal unit, family, foundation,

entire group, or ethnic association and embraces deep examination. The descriptive case

examination in this work will comprise of the gathering of data through interviewing,

observation, or administering the well-structured questionnaire to the sample of individuals

(Jervis and Drake 2014). This technique will be vital as it will be essential in drilling low, rather

than emit wide. The case examination will be vital as it will provide the surveyors with in-depth

data that aid in attaining different objectives of the assessment.

Sample dimension

To investigate the manner in which accounting practices influence operations of

SMEs around different markets

To examine benefits that the accounting practices have on activities that relate to

operations of SMEs.

Methodology

This section comprises the description of different procedures and techniques that will be

utilized in conducting this survey. It consists of the report of effective research methodology to

be used, the population of the study. The section also comprises of different sampling

techniques, method of gathering data, as well as techniques of analyzing data.

Design of research

This survey will be managed via descriptive case examination research plan. This plan

will be appropriate as it will permit for the thorough examination of different aspects that impact

financial presentation of SMEs. As stated by Sousa (2014), a case study in research work

consists of a careful as well as an inclusive examination of the societal unit, family, foundation,

entire group, or ethnic association and embraces deep examination. The descriptive case

examination in this work will comprise of the gathering of data through interviewing,

observation, or administering the well-structured questionnaire to the sample of individuals

(Jervis and Drake 2014). This technique will be vital as it will be essential in drilling low, rather

than emit wide. The case examination will be vital as it will provide the surveyors with in-depth

data that aid in attaining different objectives of the assessment.

Sample dimension

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Influence Of Accounting Practices In Small And Medium Enterprises 10

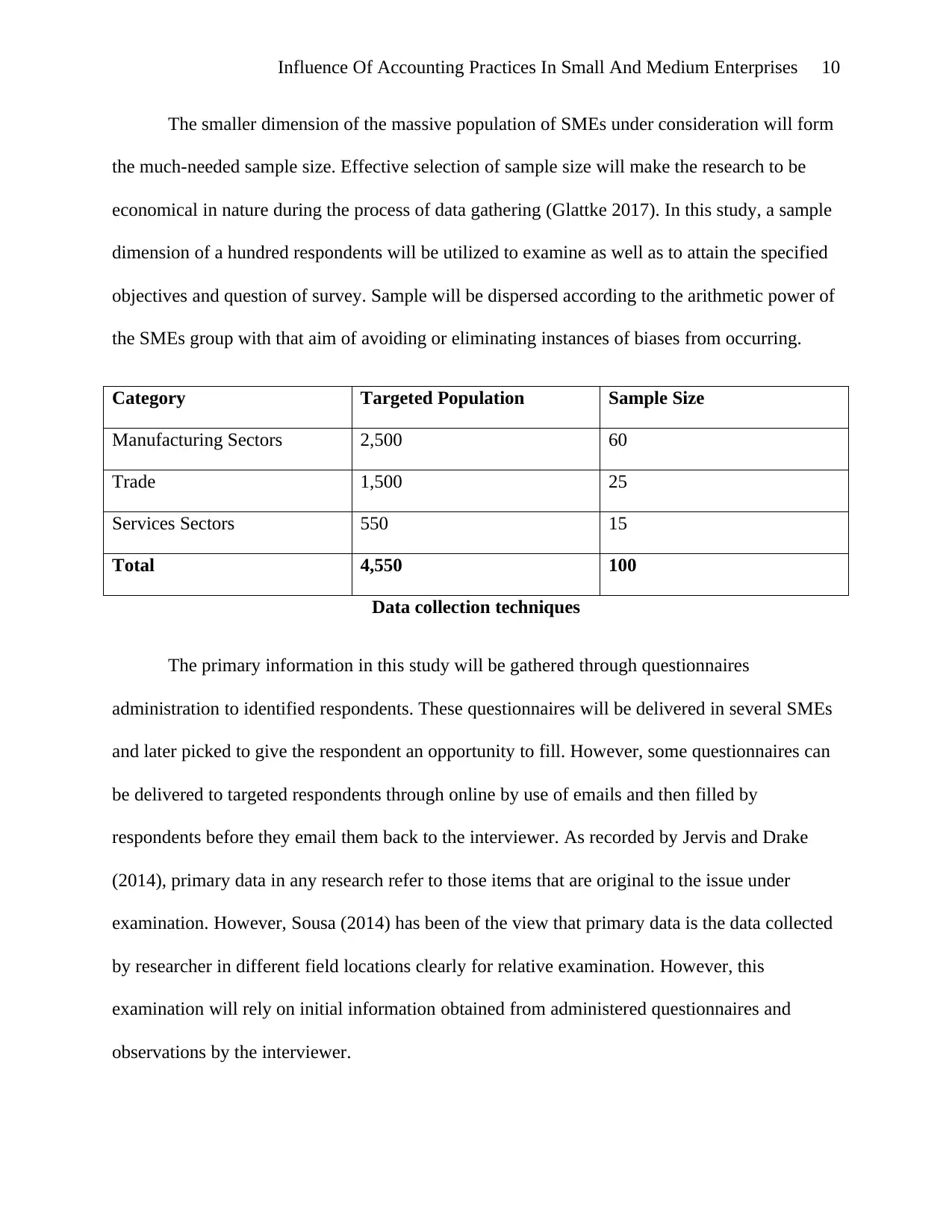

The smaller dimension of the massive population of SMEs under consideration will form

the much-needed sample size. Effective selection of sample size will make the research to be

economical in nature during the process of data gathering (Glattke 2017). In this study, a sample

dimension of a hundred respondents will be utilized to examine as well as to attain the specified

objectives and question of survey. Sample will be dispersed according to the arithmetic power of

the SMEs group with that aim of avoiding or eliminating instances of biases from occurring.

Category Targeted Population Sample Size

Manufacturing Sectors 2,500 60

Trade 1,500 25

Services Sectors 550 15

Total 4,550 100

Data collection techniques

The primary information in this study will be gathered through questionnaires

administration to identified respondents. These questionnaires will be delivered in several SMEs

and later picked to give the respondent an opportunity to fill. However, some questionnaires can

be delivered to targeted respondents through online by use of emails and then filled by

respondents before they email them back to the interviewer. As recorded by Jervis and Drake

(2014), primary data in any research refer to those items that are original to the issue under

examination. However, Sousa (2014) has been of the view that primary data is the data collected

by researcher in different field locations clearly for relative examination. However, this

examination will rely on initial information obtained from administered questionnaires and

observations by the interviewer.

The smaller dimension of the massive population of SMEs under consideration will form

the much-needed sample size. Effective selection of sample size will make the research to be

economical in nature during the process of data gathering (Glattke 2017). In this study, a sample

dimension of a hundred respondents will be utilized to examine as well as to attain the specified

objectives and question of survey. Sample will be dispersed according to the arithmetic power of

the SMEs group with that aim of avoiding or eliminating instances of biases from occurring.

Category Targeted Population Sample Size

Manufacturing Sectors 2,500 60

Trade 1,500 25

Services Sectors 550 15

Total 4,550 100

Data collection techniques

The primary information in this study will be gathered through questionnaires

administration to identified respondents. These questionnaires will be delivered in several SMEs

and later picked to give the respondent an opportunity to fill. However, some questionnaires can

be delivered to targeted respondents through online by use of emails and then filled by

respondents before they email them back to the interviewer. As recorded by Jervis and Drake

(2014), primary data in any research refer to those items that are original to the issue under

examination. However, Sousa (2014) has been of the view that primary data is the data collected

by researcher in different field locations clearly for relative examination. However, this

examination will rely on initial information obtained from administered questionnaires and

observations by the interviewer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Influence Of Accounting Practices In Small And Medium Enterprises 11

Methods of data analysis

Data analysis techniques in this research will comprise of several approaches that

comprise of quantitative approach. For instance, the use of quantitative research technique of

analyzing gathered data will focus on attaining efficient use of different online forums and

survey with the different advisory of accounting practices on their influence on operations of

SMEs (Jervis and Drake 2014). However, the application of the quantitative approach of survey

analysis targeted at creating significant use of diverse figures, charts, mathematical models, and

excels sheets, alongside diverse statistical approaches present on online sites will be used. The

technique utilized to analyze quantitative data will be descriptive (Sousa 2014). For instance, the

use of descriptive approach will comprise of ideas of getting different statistical means, media,

and variances for the already gathered data.

Methods of data analysis

Data analysis techniques in this research will comprise of several approaches that

comprise of quantitative approach. For instance, the use of quantitative research technique of

analyzing gathered data will focus on attaining efficient use of different online forums and

survey with the different advisory of accounting practices on their influence on operations of

SMEs (Jervis and Drake 2014). However, the application of the quantitative approach of survey

analysis targeted at creating significant use of diverse figures, charts, mathematical models, and

excels sheets, alongside diverse statistical approaches present on online sites will be used. The

technique utilized to analyze quantitative data will be descriptive (Sousa 2014). For instance, the

use of descriptive approach will comprise of ideas of getting different statistical means, media,

and variances for the already gathered data.

Influence Of Accounting Practices In Small And Medium Enterprises 12

List of References

Abimbola, O. and Kolawole, O. (2017). Effect of Working Capital Management Practices on the

Performance of Small and Medium Enterprises in Oyo State, Nigeria. Asian Journal of

Economics, Business and Accounting, 3(4), pp.1-8.

Ahmad, K. (2013). The Adoption of Management Accounting Practices in Malaysian Small and

Medium-Sized Enterprises. Asian Social Science, 10(2).

AlKhajeh, M. and Azam, A. (2018). The Relationship of Implementing Management Accounting

Practices (MAPs) with Performance in Small and Medium Size Enterprises. Journal of

Accounting and Auditing: Research & Practice, 2018, pp.1-7.

Asirah, A. (2018). Analysis Of Accounting Application On Micro Small And Medium

Enterprises. Patria Artha Journal of Accounting & Financial Reporting, 2(1).

Cuzdriorean, D. (2017). The Use of Management Accounting Practices by Romanian Small and

Medium-Sized Enterprises: A Field Study. Journal of Accounting and Management Information

Systems, 16(2), pp.291-312.

Du, B., Jiang, J. and Ji, X. (2018). Research on the Development of Management Accounting in

Small and Medium-Sized Enterprises in China. Open Journal of Accounting, 07(01), pp.19-24.

Glattke, T. (2017). International Research Collaborations: Ethical and Regulatory

Considerations. The ASHA Leader, 12(17), pp.19-21.

List of References

Abimbola, O. and Kolawole, O. (2017). Effect of Working Capital Management Practices on the

Performance of Small and Medium Enterprises in Oyo State, Nigeria. Asian Journal of

Economics, Business and Accounting, 3(4), pp.1-8.

Ahmad, K. (2013). The Adoption of Management Accounting Practices in Malaysian Small and

Medium-Sized Enterprises. Asian Social Science, 10(2).

AlKhajeh, M. and Azam, A. (2018). The Relationship of Implementing Management Accounting

Practices (MAPs) with Performance in Small and Medium Size Enterprises. Journal of

Accounting and Auditing: Research & Practice, 2018, pp.1-7.

Asirah, A. (2018). Analysis Of Accounting Application On Micro Small And Medium

Enterprises. Patria Artha Journal of Accounting & Financial Reporting, 2(1).

Cuzdriorean, D. (2017). The Use of Management Accounting Practices by Romanian Small and

Medium-Sized Enterprises: A Field Study. Journal of Accounting and Management Information

Systems, 16(2), pp.291-312.

Du, B., Jiang, J. and Ji, X. (2018). Research on the Development of Management Accounting in

Small and Medium-Sized Enterprises in China. Open Journal of Accounting, 07(01), pp.19-24.

Glattke, T. (2017). International Research Collaborations: Ethical and Regulatory

Considerations. The ASHA Leader, 12(17), pp.19-21.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.