Ask a question from expert

Intermediate Accounting Assignment PDF

37 Pages4018 Words67 Views

Added on 2021-10-13

Intermediate Accounting Assignment PDF

Added on 2021-10-13

BookmarkShareRelated Documents

Intermediate Accounting

Chapter 7

Cash and Receivables

This slide deck contains animations. Please disable animations if they

cause issues with your device.

Learning Objectives

After studying this chapter, you should be able to:

● Indicate how to report cash and related items.

● Define receivables and explain accounting issues related to their

recognition.

● Explain accounting issues related to valuation of accounts receivable.

● Explain accounting issues related to recognition and valuation of

__notes____ receivable.

Learning Objective 1

Indicate How to Report Cash and Related Items

Cash

● Most liquid asset

● Standard medium of exchange

● Basis for measuring and accounting for all items

● Current asset

● Examples: Coin, currency, available funds on deposit at the bank,

money orders, certified checks, cashier’s checks, personal checks,

bank drafts and __savings_______ accounts

Chapter 7

Cash and Receivables

This slide deck contains animations. Please disable animations if they

cause issues with your device.

Learning Objectives

After studying this chapter, you should be able to:

● Indicate how to report cash and related items.

● Define receivables and explain accounting issues related to their

recognition.

● Explain accounting issues related to valuation of accounts receivable.

● Explain accounting issues related to recognition and valuation of

__notes____ receivable.

Learning Objective 1

Indicate How to Report Cash and Related Items

Cash

● Most liquid asset

● Standard medium of exchange

● Basis for measuring and accounting for all items

● Current asset

● Examples: Coin, currency, available funds on deposit at the bank,

money orders, certified checks, cashier’s checks, personal checks,

bank drafts and __savings_______ accounts

Cash

Reporting Cash

Cash Equivalents

Short-term, highly liquid investments that are both

(a) readily convertible to cash, and

(b) so near their maturity that they present insignificant risk of

changes in value.

Examples: Treasury bills, Commercial paper, and Money market

__funds_____.

Restricted Cash

Companies segregate restricted cash from“regular”cash.

Examples, restricted for:

(1) plant expansion, (2) retirement of long-term debt, and (3)

compensating balances.

Bank Overdrafts

Company writes a check for more than the amount in its cash account.

● Reported as a current ___liability___________

● Offset against other cash accounts only when accounts are with the

same bank

Learning Objective 2

Define Receivables and Explain Accounting Issues Related to Their

Recognition

Reporting Cash

Cash Equivalents

Short-term, highly liquid investments that are both

(a) readily convertible to cash, and

(b) so near their maturity that they present insignificant risk of

changes in value.

Examples: Treasury bills, Commercial paper, and Money market

__funds_____.

Restricted Cash

Companies segregate restricted cash from“regular”cash.

Examples, restricted for:

(1) plant expansion, (2) retirement of long-term debt, and (3)

compensating balances.

Bank Overdrafts

Company writes a check for more than the amount in its cash account.

● Reported as a current ___liability___________

● Offset against other cash accounts only when accounts are with the

same bank

Learning Objective 2

Define Receivables and Explain Accounting Issues Related to Their

Recognition

Receivables

Claims held against customers and others for money, goods, or services.

Classified in the balance sheet as:

● Current or noncurrent

● Trade or nontrade

● Accounts receivable

● Notes receivable

Nontrade Receivables

● Advances to officers and employees.

● Advances to subsidiaries.

● Deposits paid to cover potential damages or losses.

● Deposits paid as a guarantee of performance or _payment________ .

● Dividends and interest receivable.

● Claims against: Insurance companies for casualties sustained;

defendants under suit; governmental bodies for tax refunds; common

carriers for damaged or lost goods; creditors for returned, damaged,

or lost goods; customers for returnable items (crates, containers,

etc.).

Nontrade Receivables

Receivables Balance Sheet Presentations

Claims held against customers and others for money, goods, or services.

Classified in the balance sheet as:

● Current or noncurrent

● Trade or nontrade

● Accounts receivable

● Notes receivable

Nontrade Receivables

● Advances to officers and employees.

● Advances to subsidiaries.

● Deposits paid to cover potential damages or losses.

● Deposits paid as a guarantee of performance or _payment________ .

● Dividends and interest receivable.

● Claims against: Insurance companies for casualties sustained;

defendants under suit; governmental bodies for tax refunds; common

carriers for damaged or lost goods; creditors for returned, damaged,

or lost goods; customers for returnable items (crates, containers,

etc.).

Nontrade Receivables

Receivables Balance Sheet Presentations

Recognition of Accounts Receivables

● Accounts receivable generally arise as part of a revenue arrangement

● Revenue recognition principle indicates that a company should

recognize revenue when it satisfies its performance obligation by

transferring the good or service to the customer.

Recognition of Accounts Receivables

Illustration

If Lululemon sells a yoga outfit to Jennifer Burian for $100 on account, the

yoga outfit is transferred when Jennifer obtains control of this outfit. When

this change in control occurs, Lululemon should recognize an account

receivable and sales revenue. Lululemon makes the following entry:

Accounts Receivable

100

Sales Revenue

100

Recognition of Accounts Receivables

Key indicators control has been _____transferred_________

● Lululemon has the right to payment from the customer.

● Lululemon has passed legal title to the customer.

● Lululemon has transferred physical possession of the goods.

● Lululemon no longer has significant risks and rewards of ownership of

the goods.

● Jennifer has accepted the asset.

● Accounts receivable generally arise as part of a revenue arrangement

● Revenue recognition principle indicates that a company should

recognize revenue when it satisfies its performance obligation by

transferring the good or service to the customer.

Recognition of Accounts Receivables

Illustration

If Lululemon sells a yoga outfit to Jennifer Burian for $100 on account, the

yoga outfit is transferred when Jennifer obtains control of this outfit. When

this change in control occurs, Lululemon should recognize an account

receivable and sales revenue. Lululemon makes the following entry:

Accounts Receivable

100

Sales Revenue

100

Recognition of Accounts Receivables

Key indicators control has been _____transferred_________

● Lululemon has the right to payment from the customer.

● Lululemon has passed legal title to the customer.

● Lululemon has transferred physical possession of the goods.

● Lululemon no longer has significant risks and rewards of ownership of

the goods.

● Jennifer has accepted the asset.

Receivables

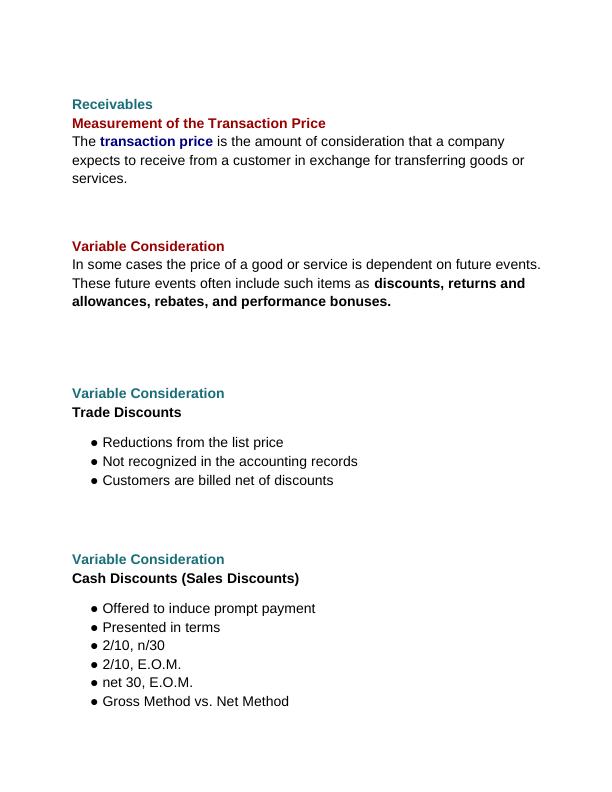

Measurement of the Transaction Price

The transaction price is the amount of consideration that a company

expects to receive from a customer in exchange for transferring goods or

services.

Variable Consideration

In some cases the price of a good or service is dependent on future events.

These future events often include such items as discounts, returns and

allowances, rebates, and performance bonuses.

Variable Consideration

Trade Discounts

● Reductions from the list price

● Not recognized in the accounting records

● Customers are billed net of discounts

Variable Consideration

Cash Discounts (Sales Discounts)

● Offered to induce prompt payment

● Presented in terms

● 2/10, n/30

● 2/10, E.O.M.

● net 30, E.O.M.

● Gross Method vs. Net Method

Measurement of the Transaction Price

The transaction price is the amount of consideration that a company

expects to receive from a customer in exchange for transferring goods or

services.

Variable Consideration

In some cases the price of a good or service is dependent on future events.

These future events often include such items as discounts, returns and

allowances, rebates, and performance bonuses.

Variable Consideration

Trade Discounts

● Reductions from the list price

● Not recognized in the accounting records

● Customers are billed net of discounts

Variable Consideration

Cash Discounts (Sales Discounts)

● Offered to induce prompt payment

● Presented in terms

● 2/10, n/30

● 2/10, E.O.M.

● net 30, E.O.M.

● Gross Method vs. Net Method

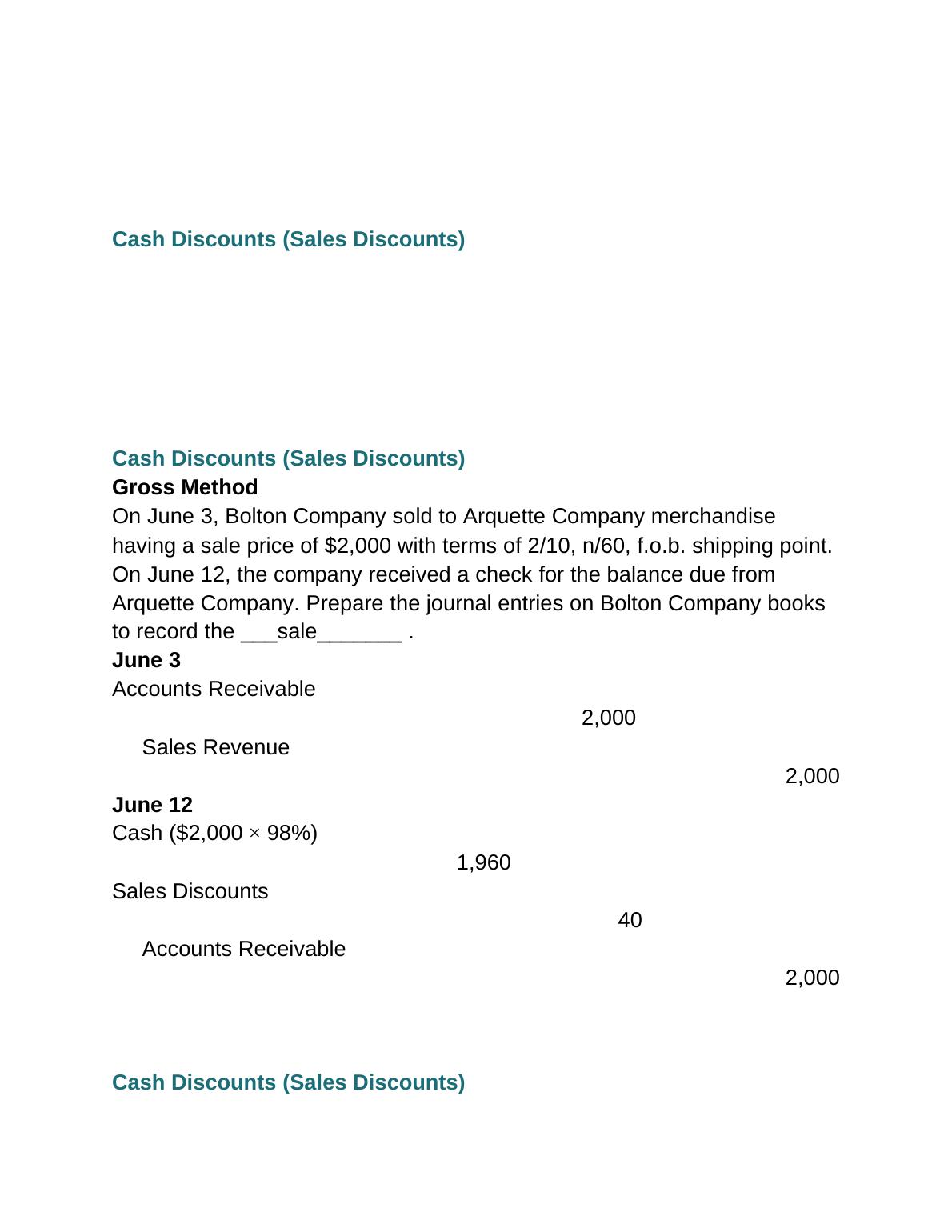

Cash Discounts (Sales Discounts)

Cash Discounts (Sales Discounts)

Gross Method

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On June 12, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the ___sale_______ .

June 3

Accounts Receivable

2,000

Sales Revenue

2,000

June 12

Cash ($2,000 ×98%)

1,960

Sales Discounts

40

Accounts Receivable

2,000

Cash Discounts (Sales Discounts)

Cash Discounts (Sales Discounts)

Gross Method

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On June 12, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the ___sale_______ .

June 3

Accounts Receivable

2,000

Sales Revenue

2,000

June 12

Cash ($2,000 ×98%)

1,960

Sales Discounts

40

Accounts Receivable

2,000

Cash Discounts (Sales Discounts)

Net Method

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On June 12, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the sale.

June 3

Accounts Receivable

1,960

Sales Revenue

1,960

June 12

Cash ($2,000 ×98%)

1,960

Accounts Receivable

1,960

Cash Discounts (Sales Discounts)

Net Method, payment made on July 29

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On July 29, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the sale.

June 3

Accounts Receivable

1,960

Sales

1,960

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On June 12, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the sale.

June 3

Accounts Receivable

1,960

Sales Revenue

1,960

June 12

Cash ($2,000 ×98%)

1,960

Accounts Receivable

1,960

Cash Discounts (Sales Discounts)

Net Method, payment made on July 29

On June 3, Bolton Company sold to Arquette Company merchandise

having a sale price of $2,000 with terms of 2/10, n/60, f.o.b. shipping point.

On July 29, the company received a check for the balance due from

Arquette Company. Prepare the journal entries on Bolton Company books

to record the sale.

June 3

Accounts Receivable

1,960

Sales

1,960

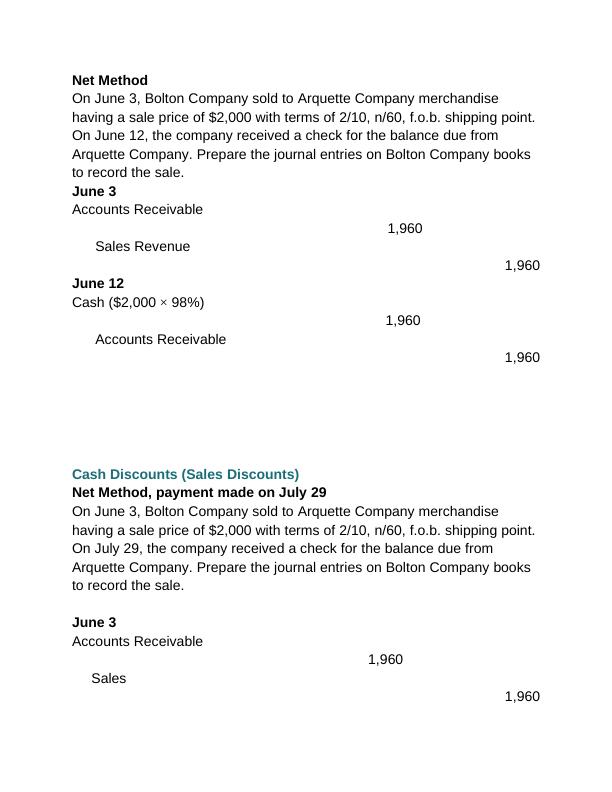

July 29

Cash

2,000

Accounts Receivable

1,960

Sales Discounts Forfeited

40

Variable Consideration

Sales Returns and Allowances

● Contra revenue account to Sales Revenue

● Allowance for Sales Returns and Allowances is a contra asset

account to Accounts Receivable

● Use of both Sales Returns and Allowances, and Allowance for Sales

Return and Allowances accounts is helpful to identify potential

problems associated with inferior merchandise, inefficiencies in filling

orders, or delivery or shipment _____mistakes________________ .

Sales Returns and Allowances

Illustration

Assume on January 4, 2020, Max sells $5,000 of hurricane glass to Oliver

on __account______. Max records the sale on account as follows.

On January 16, 2020, Max grants an allowance of $300 to Oliver because

some of the hurricane glass is defective. The entry to record this

transaction is as follows.

Cash

2,000

Accounts Receivable

1,960

Sales Discounts Forfeited

40

Variable Consideration

Sales Returns and Allowances

● Contra revenue account to Sales Revenue

● Allowance for Sales Returns and Allowances is a contra asset

account to Accounts Receivable

● Use of both Sales Returns and Allowances, and Allowance for Sales

Return and Allowances accounts is helpful to identify potential

problems associated with inferior merchandise, inefficiencies in filling

orders, or delivery or shipment _____mistakes________________ .

Sales Returns and Allowances

Illustration

Assume on January 4, 2020, Max sells $5,000 of hurricane glass to Oliver

on __account______. Max records the sale on account as follows.

On January 16, 2020, Max grants an allowance of $300 to Oliver because

some of the hurricane glass is defective. The entry to record this

transaction is as follows.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting Information System (AIS) Reportlg...

|9

|1549

|93