Bond and Option Valuation: Problems, Calculations, and Analysis

VerifiedAdded on 2021/06/17

|7

|2027

|122

Homework Assignment

AI Summary

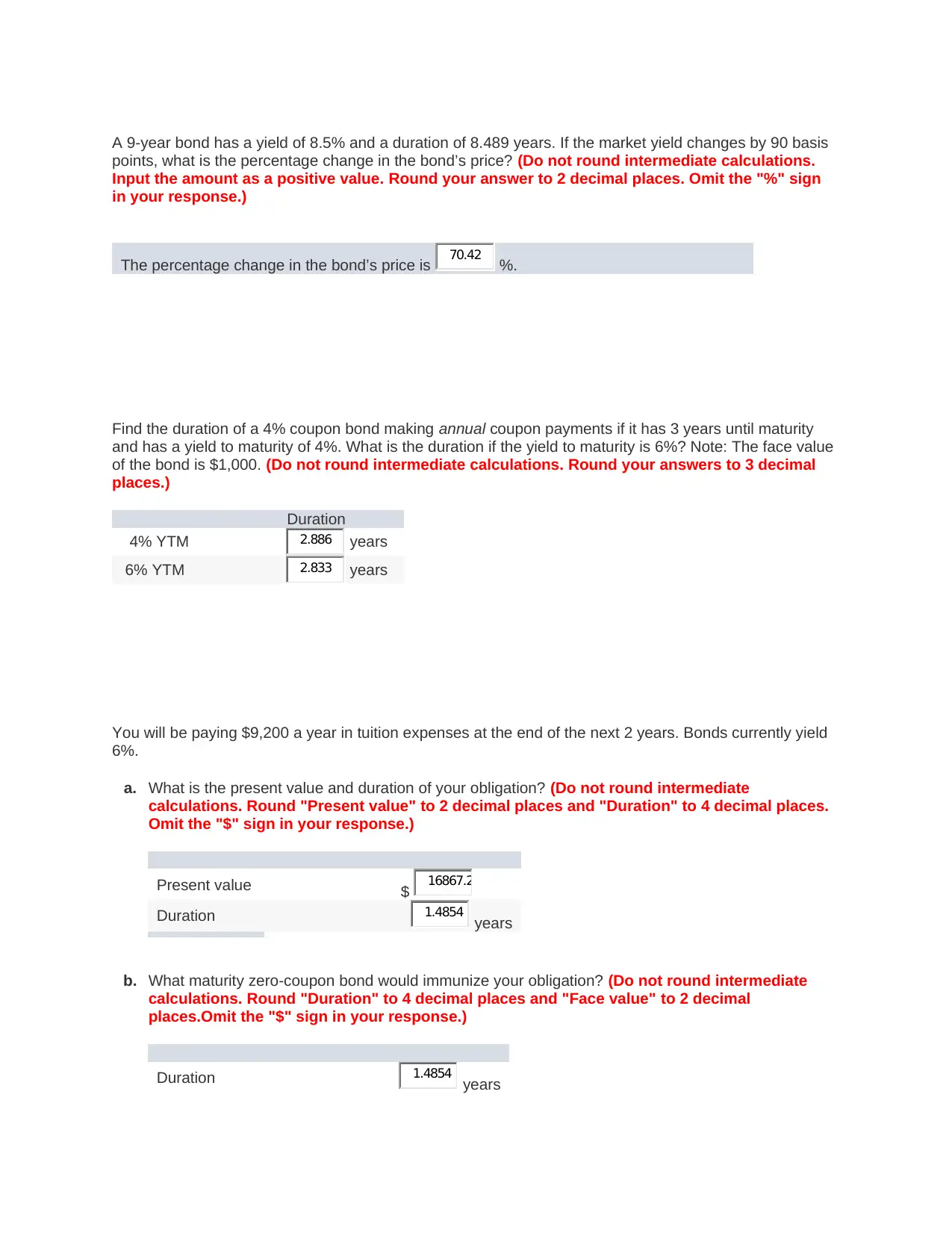

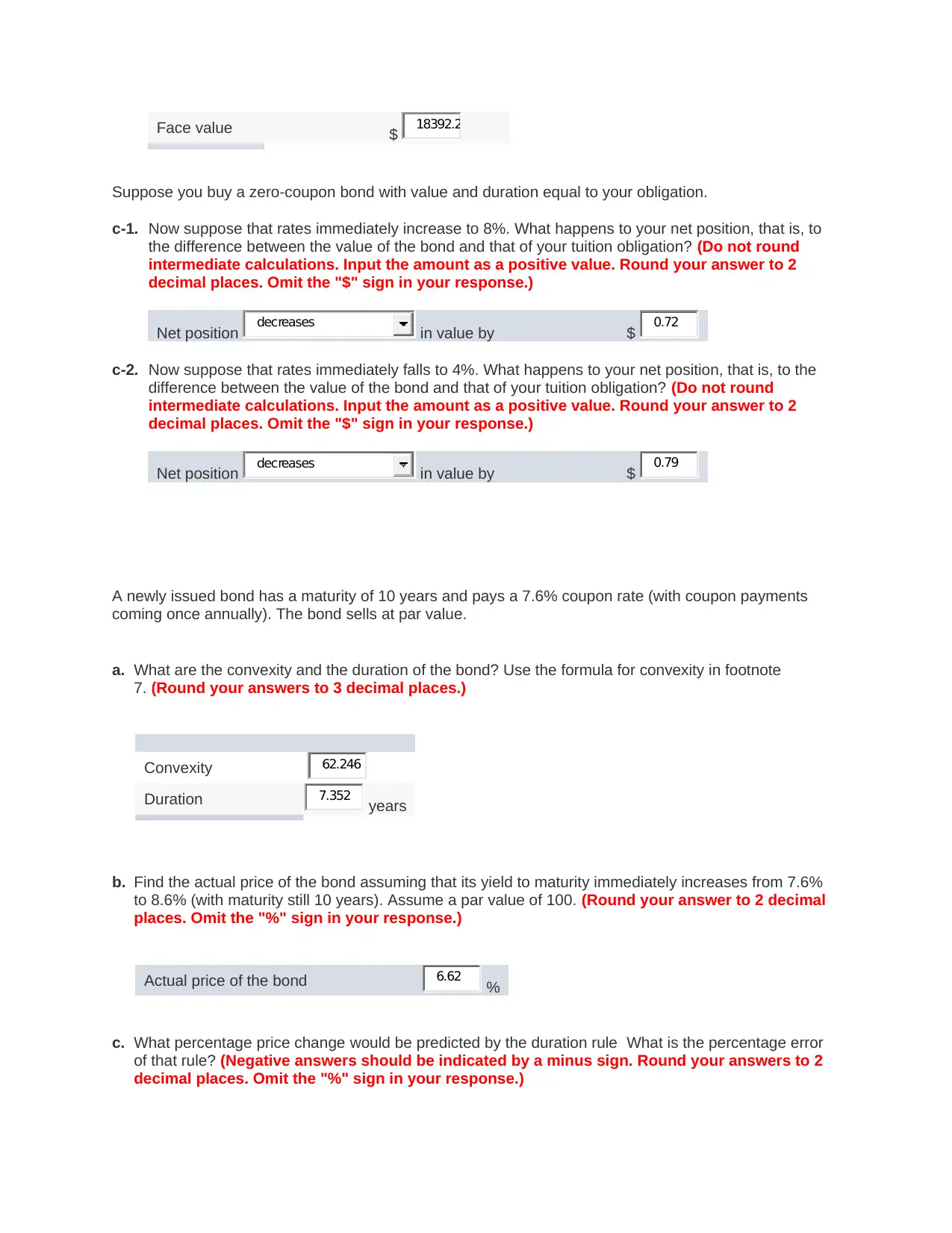

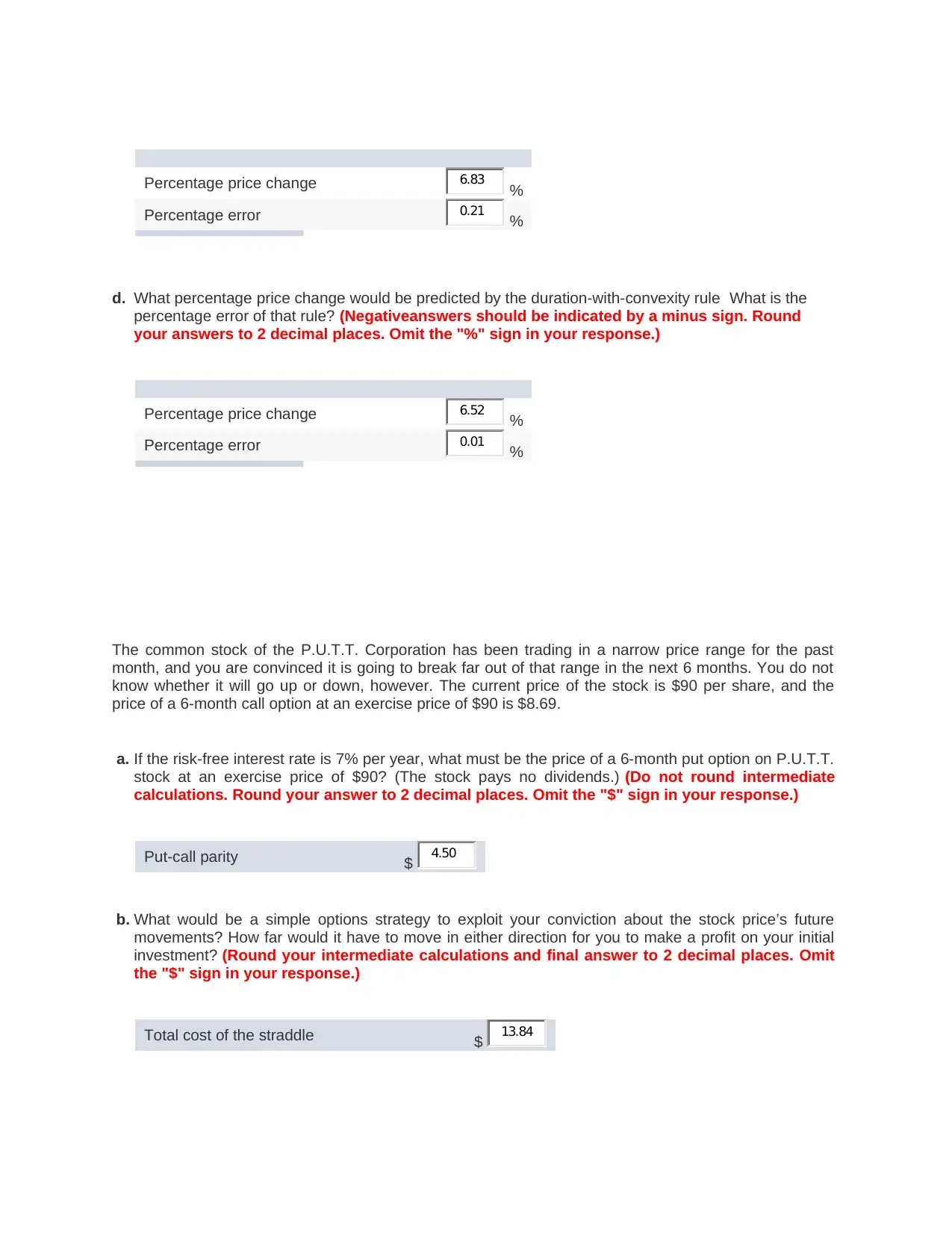

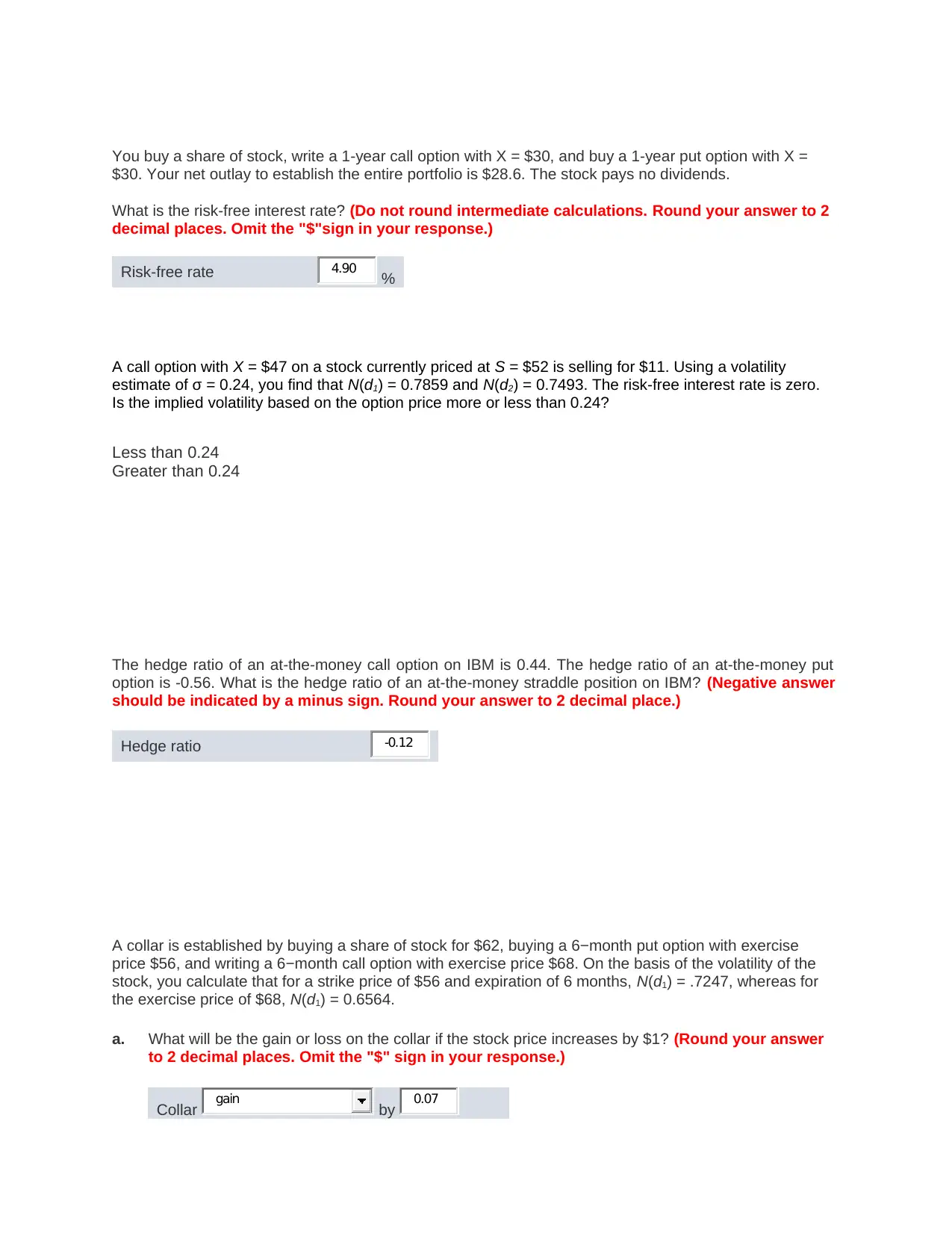

This assignment delves into various aspects of bond and option valuation. It starts with calculations involving bond duration and its impact on price changes due to yield fluctuations. The assignment then explores duration calculations for coupon bonds and the concept of immunizing obligations using zero-coupon bonds. Furthermore, it covers convexity calculations, percentage price changes predicted by the duration rule, and the accuracy of the duration-with-convexity rule. Option valuation problems, including put-call parity, straddle strategies, and the Black-Scholes model are analyzed. The assignment also examines hedging strategies using options and the valuation of callable and convertible bonds. Finally, it addresses the calculation of expected and promised returns on bonds, along with the probability of default and the implementation of trading strategies involving convertible bonds.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.