Intermediate Financial Accounting Assignment Solution - Rhodes Ltd

VerifiedAdded on 2022/10/12

|11

|1720

|199

Homework Assignment

AI Summary

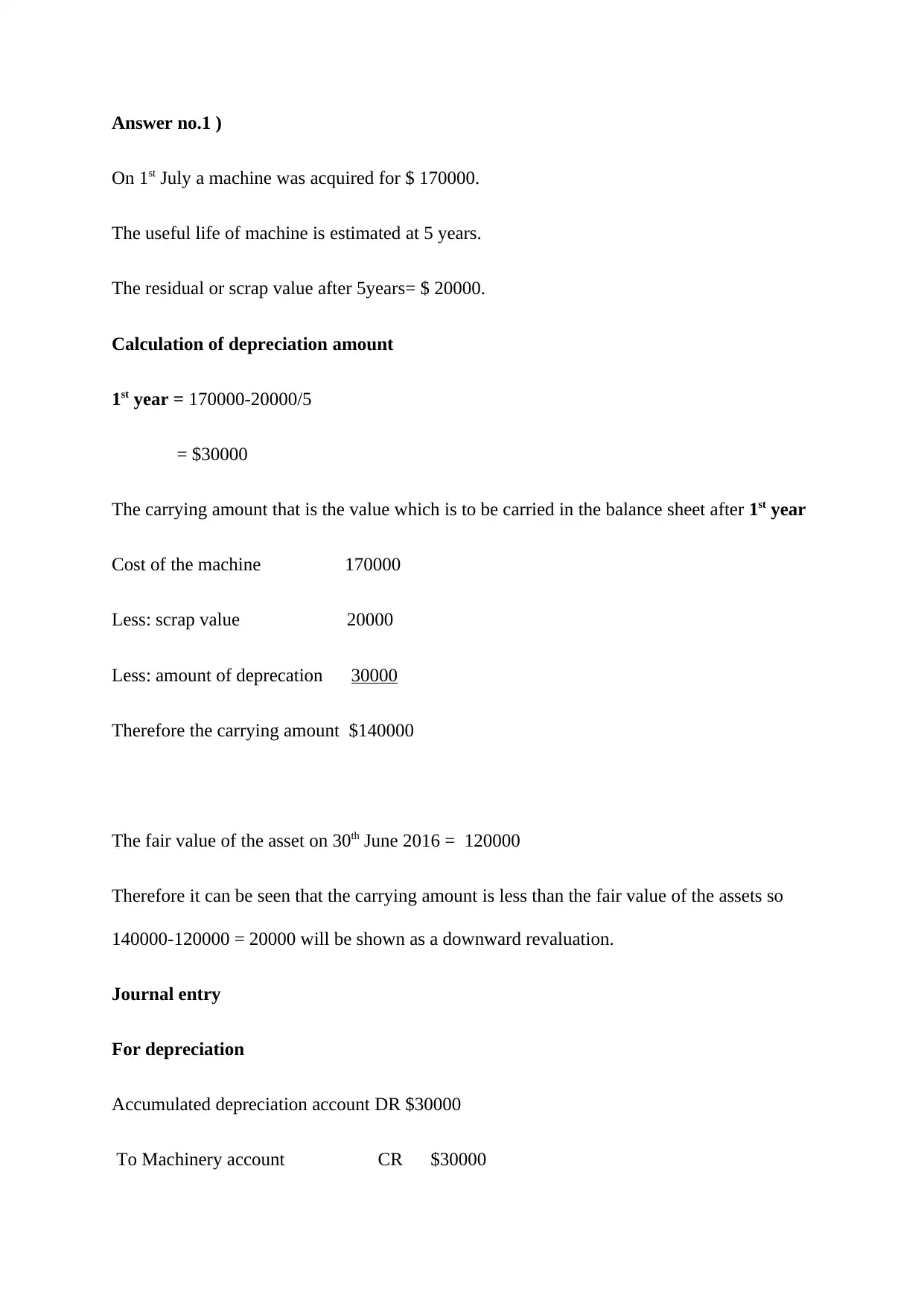

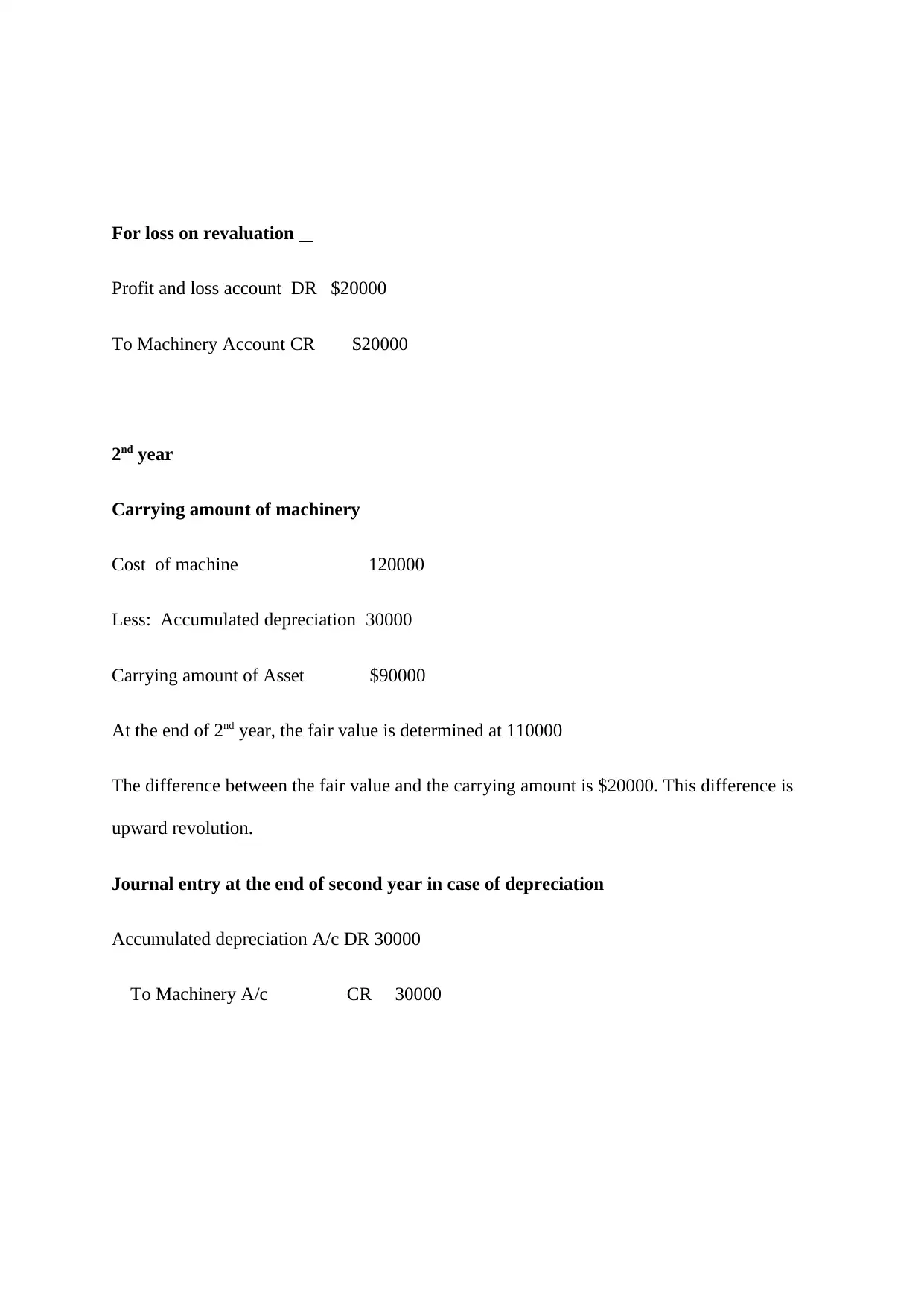

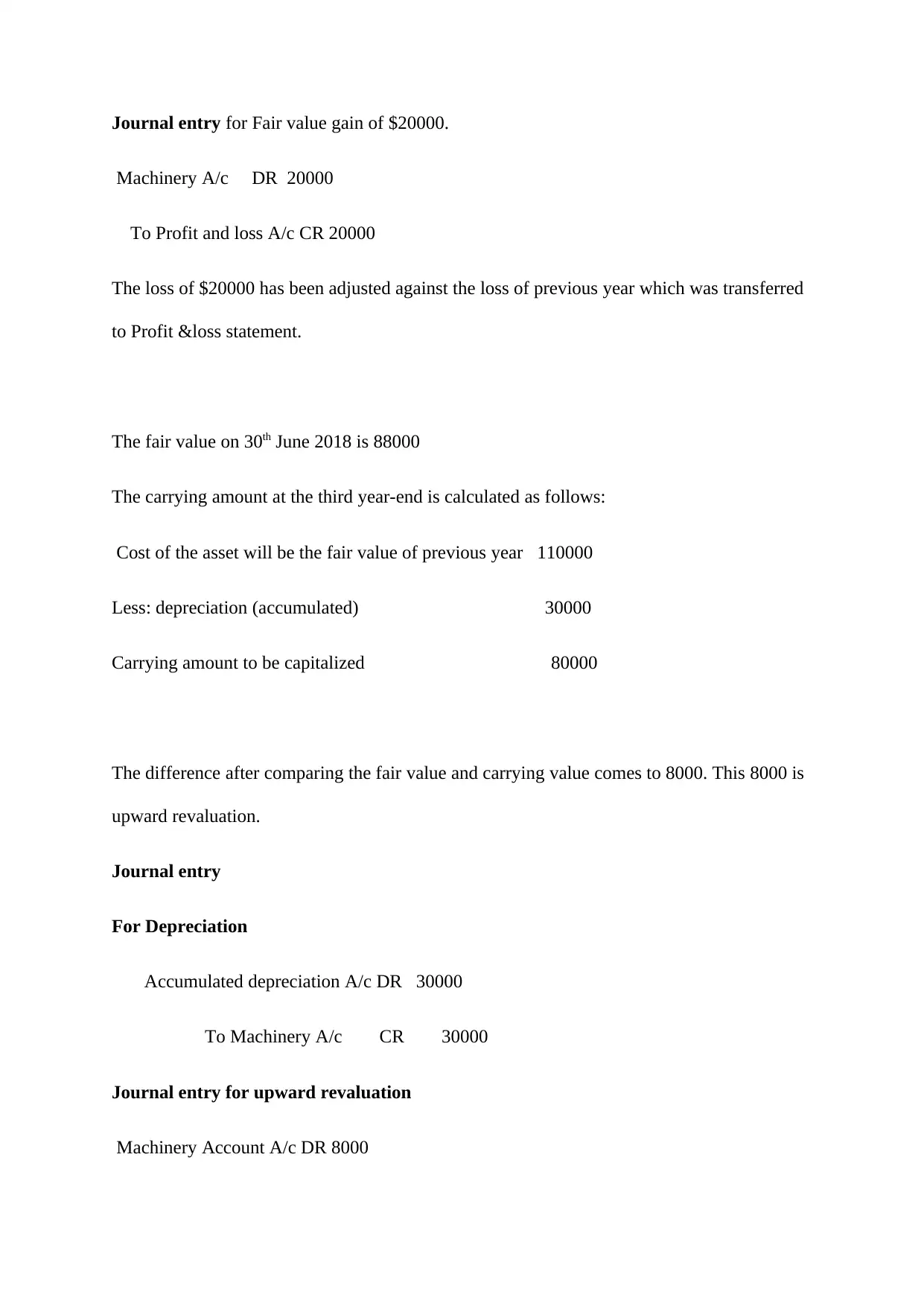

This document presents a comprehensive solution to an intermediate financial accounting assignment. The solution addresses three key questions. The first question focuses on the revaluation model for property, plant, and equipment, specifically a machine acquired by Rhodes Ltd, detailing depreciation calculations, journal entries for revaluation gains and losses, and carrying amounts. The second question defines and explains provisions, illustrating their recognition with an example of Brunswick Limited's environmental liability, including probability analysis and discounting. The final question delves into intangible assets, discussing their characteristics, recognition criteria, and measurement, including the accounting treatment of Bitcoin as an intangible asset, and its compliance with AASB standards. References from academic journals are also included.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.