The Role of Internal Audit in Corporate Governance

25 Pages6963 Words106 Views

Added on 2021-06-17

The Role of Internal Audit in Corporate Governance

Added on 2021-06-17

ShareRelated Documents

Running head: INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCEInternal Audit Function and the Development of Corporate Governance Code in LibyaUniversity NameStudent NameAuthors’ Note

2INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCETable of Contents1. Introduction............................................................................................................................22. Notions of internal audit within a corporation.......................................................................23. Theoretical Perspective of internal audit function and corporate governance.......................73. 1 Agency Theory as a theory of Corporate Governance........................................................73.1.1 Costs of agency model on corporate governance..........................................................93.1.2 Significance of agency model on corporate governance.............................................103.1.3 Effects of agency model on corporate governance.....................................................103.2 Stewardship Theory of Corporate Governance..................................................................103.2.1 Impacts of Stewardship Theory of Corporate Governance on Employees.................123.2.2 Particular Influence of Stewardship Theory of Corporate Governance on Clients....123.2.3 General consequence of Stewardship Theory of Corporate Governance...................124. Developing and implementing well-aligned internal audit strategy....................................135. Role of internal audit function in development of corporate governance code...................14

3INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCELiterature Review1. IntroductionThe current study delivers a comprehensive image of the internal audit purpose. Thisnecessarily views the conceptual evolution of theory of internal audit, and illustrates thenecessity for the same, descriptions of the term, and the way it is inevitable to differententities’ internal audit function operates within. In essence, this runs deeply into the priorstudies that are necessarily directly associated to the topic under consideration and deliverstheir findings. This can aid the process of ascertainment of beginning point of the currentstudy. The present study intends to illustrate and design a conceptual framework and evaluateoverall nature and exercise of the internal audit function within companies in Libya. 2. Notions of internal audit within a corporationConceptual approaches concerning internal auditingGriffiths (2016) indicates that there is a comprehensive image of the internal audit function.The study views the conceptual transformation of the internal audit function and illustratesthe requirement for the same, descriptions of the terms and the way it is necessary to differententities. The activities of internal auditing emerged as well as designed owing to value tospecific recipients and owing to potential of fulfilling specific requirements of different users.Eulerich et al. (2015) assert that the activity of internal auditing is of great importance andthe article recommends specifying significance of the association between specifically sectionof accounting as well as assessment. Internal auditing can be considered to be of strategicsignificance, as managers, along with the Board of Directors of the reporting unit, canunderstand that till there is an appropriate internal structure of control, a few error as well asfailures can be examined and eradicated in a well timed method.

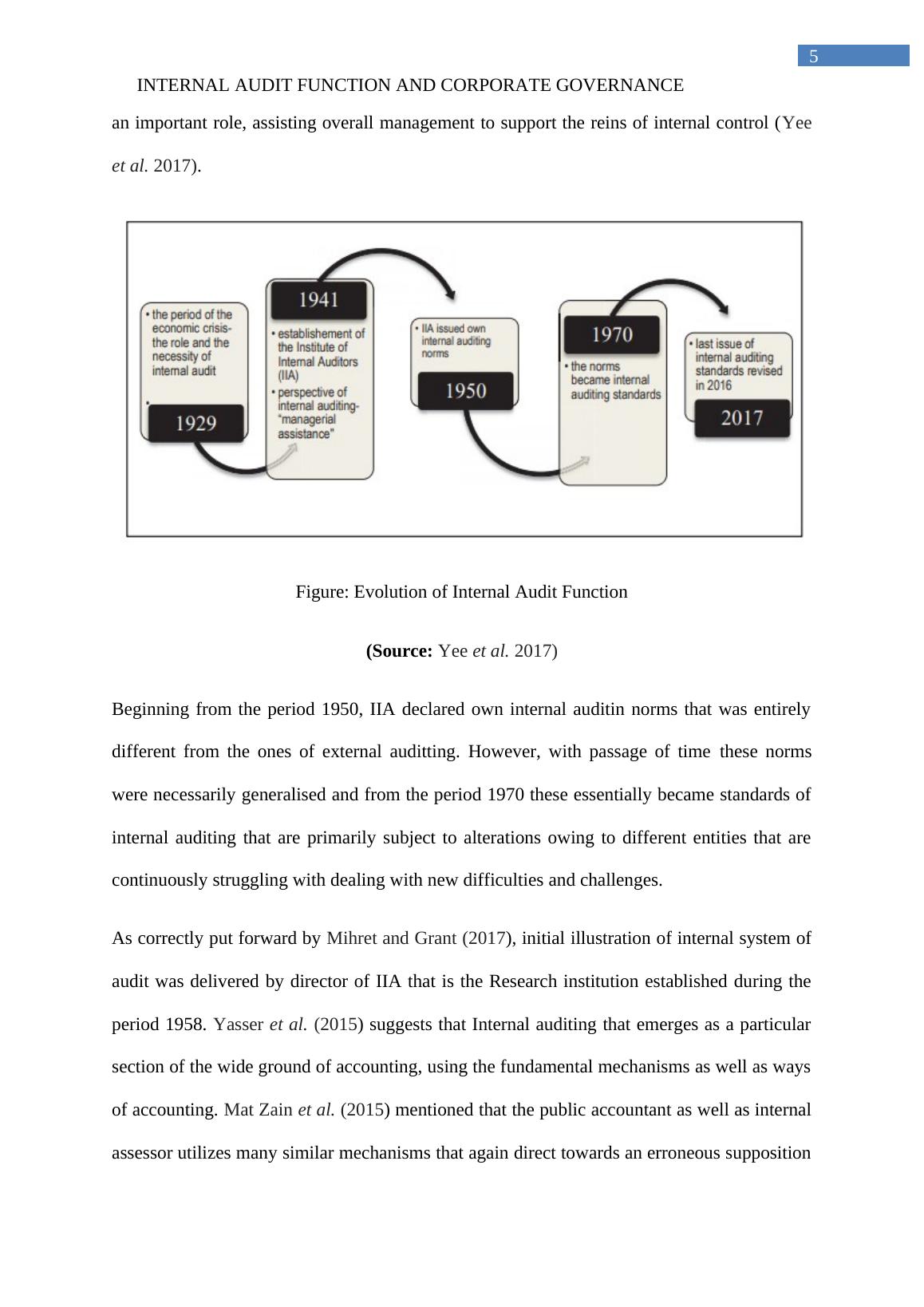

4INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCEThe Board of Directors of the company necessarily give the impression auditing that isinternal in nature as an act for enhancing the action, in addition to an act of searching for aswell as detecting faults as well as wrongdoing. Therefore, amplification of auditing conceptthat is internal in nature, and over and above than that, elucidation of the role that internalauditing essentially plays today, is crucial. As suggested by Salvioni and Astori (2015), thereare several scholars from the specific ground have analysed the advancement of internalauditing at the global level as well as nationwide level. A more strong utilization of theexpression audit is discovered during period of economic crisis from the period 1929, giventhat then role as well as requirement of internal auditing endlessly augmented, a fact thatdirected to the corporation along with standardisation of exercises of internal auditing by wayof institution in the year 1941 in Orlando, USA, of principally the Institute of InternalAuditors (abbreviated as IIA), to which, at the instant, in excess of 120 nations are associated.As recommended by Alzeban and Gwilliam (2014), internal audit necessarily had asignificant role within corporate governance ever since the period 1940. It certainly becamemore imperative with passage of time. Ever since the period of 1940, several transformationshave taken place as regards internal auditing that was regulated by means of diverse norms aswell as corporate governance codes. McAlister and Ferrell (2016) takes into account the factthat there are diverse basic actions of internal auditing are registered include analysis of risk,making certain organization within the entity as well as ensuring conformity.During the year 1942, Lenz and Hahn (2015) asserts that the first president of the entityInternational Institute of Internal Auditors, announced an surprising forecast that majority ofexcellent standpoint of internal auditing shall be the “managerial backing”. During the year1991, Joseph J. Mossis that is the president of the “Institute of Internal Auditors” of Britain,started again the same comment, however in a more a precise manner. In essence, it is quiteclear for the ones that operate within “Internal Auditing function” that this necessarily plays

5INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCEan important role, assisting overall management to support the reins of internal control (Yeeet al. 2017). Figure: Evolution of Internal Audit Function(Source:Yee et al. 2017)Beginning from the period 1950, IIA declared own internal auditin norms that was entirelydifferent from the ones of external auditting. However, with passage of time these normswere necessarily generalised and from the period 1970 these essentially became standards ofinternal auditing that are primarily subject to alterations owing to different entities that arecontinuously struggling with dealing with new difficulties and challenges. As correctly put forward by Mihret and Grant (2017), initial illustration of internal system ofaudit was delivered by director of IIA that is the Research institution established during theperiod 1958. Yasser et al. (2015) suggests that Internal auditing that emerges as a particularsection of the wide ground of accounting, using the fundamental mechanisms as well as waysof accounting. Mat Zain et al. (2015) mentioned that the public accountant as well as internalassessor utilizes many similar mechanisms that again direct towards an erroneous supposition

6INTERNAL AUDIT FUNCTION AND CORPORATE GOVERNANCEthat there subsists minute inconsistency in firm’s operation. Essentially, firm’s internalassessor, similar to any evaluator, is worried regarding evaluation of legitimacy of depiction.However, as regards the current case under consideration, the illustration with whichparticular evaluator is disturbed takes into account fairly broader choice. Also, there isrequirement to accomplish different themes in which the association to particular accountingitems is frequently to some extent isolated. Also, the internal assessor is relatively moreintensely concerned in assisting to carrying out the operations profitably (Christopher 2015). As recommended by El-Kassar et al. (2014), internal auditing can be referred to asProfessional rules declared by the “Institute of Audit and Internal Control”. This rule refers toa specific purpose along with independent activities that confer to a business concern ancover concerning the stage of specific controls regarding different functions. This shows theway to the business concern and helps in enhancement of business functions that in turn canadd plus value. In addition to this, this has the requirement to be state that internal audit alsoassists the business concern to attain its aims since the same evaluates the administrativeprocess, controls in addition to processes of governance. However, there exists a risk towhich the business concern is exposed. In addition to this, internal audit presentsexplanations and solutions for enhancement of effectiveness of these procedures, or else tomask drawbacks (Ruud 2013).As mentioned by Alzeban (2015), internal auditing action appreciates and directs thecorporate governance procedure, in a bid to achieve particular aims associated to ethics,accountability as well as effectiveness in management. Fundamentally, in this regard, it canbe said that for the purpose of tracking and making certain compliance to the pertinent codeof corporate governance. Essentially, it is crucial to illustrate the notion of corporategovernance. In particular, corporate governance as per OECD, reflects different proceduresaccording to which a corporation is directed and at the same time controlled (Drogalas et al.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Internal Audit Function & the Development of Corporate Governance Codelg...

|23

|5866

|211

Seminal Theories of Governance and Stewardship in Organizationslg...

|13

|2884

|73

Contemporary Issues in Accounting Studylg...

|19

|2625

|113

Importance of Conceptual Framework for Financial Reportinglg...

|18

|4601

|482

Corporate Governance Ethics and Governance EThics and Governance Executive Summarylg...

|14

|4158

|194

The Effect of the Internal Audit and Firm Performance: A Proposed Research Frameworklg...

|8

|5326

|366