Functions and Roles of Internal Audit in Public Sector Risk Management: A Study on Gambia

VerifiedAdded on 2023/06/18

|18

|4395

|186

AI Summary

This research aims to identify the functions and roles of internal audit in risk management within public sector organisations in Gambia. It will also examine the benefits and challenges of internal auditing for public sector organisations. The study will provide insights into the internal audit process of the public sector and identify key areas required for proper functioning. The research will also help the government and other stakeholders to minimize risks involved in internal audit.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Research Method

1.3. Relevant experience:

My job as an assistant internal auditor is to assist the Senior internal Auditor in the National

Assembly to evaluate the adequacy and effectiveness of control in responding to risks within

the organization’s governance, operations and information system regarding the reliability

and integrity of financial and operational information, efficiency and effectiveness of

operations and programmes safe guarding of assets and compliance with laws regulations

policies, procedures and contracts by pre auditing of payments of the National Assembly and

other activities captured in our annual risk base plan since January 2018 to Date.

1.3. Relevant experience:

My job as an assistant internal auditor is to assist the Senior internal Auditor in the National

Assembly to evaluate the adequacy and effectiveness of control in responding to risks within

the organization’s governance, operations and information system regarding the reliability

and integrity of financial and operational information, efficiency and effectiveness of

operations and programmes safe guarding of assets and compliance with laws regulations

policies, procedures and contracts by pre auditing of payments of the National Assembly and

other activities captured in our annual risk base plan since January 2018 to Date.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Internal Audit Functions in the

Public Sector Risk Management

Public Sector Risk Management

Table of Contents

Introduction.........................................................................................................................................4

Literature review.................................................................................................................................7

Explain the function and role that is being played to minimize risk by doing internal audit in the

Gambia..............................................................................................................................................7

Research methodology......................................................................................................................12

Conclusion..........................................................................................................................................16

References..........................................................................................................................................17

Introduction.........................................................................................................................................4

Literature review.................................................................................................................................7

Explain the function and role that is being played to minimize risk by doing internal audit in the

Gambia..............................................................................................................................................7

Research methodology......................................................................................................................12

Conclusion..........................................................................................................................................16

References..........................................................................................................................................17

Introduction

Internal audit is a business process that is used by the organization to increase its

efficiency or to add value. It is an activity of assurance and consulting. This activity helps the

organisation to achieve its goal. Internal audit is a systematic approach that helps in risk

management by improving the effectiveness. This is used by the organisation so that a proper

account can be maintained by the business and the upper body and the government uses this

to make adecision. Public sector businesses are those organisations which is controlled and

run by the national, state or any local legal body of the country. In this sector the major

shareholder of the enterprise is the government body (Kagermann, Kinney and Küting, 2021).

In recent years, the Government of the Gambia has made significant progress in

strengthening fiscal discipline and improving the efficiency of its Public Financial

Management System (PFM). The Government has strengthened the legislative base,

increased the transparency of budget information, improved control over expenditures, and

strengthened budget oversight. At the heart of these initiatives was the establishment of the

Internal Audit Directorate through an Act of Parliament the (Public Financial Act 2014) and

its accompanying Financial Regulations 2016.

Background of the research problem:

Many organisations are hastily presumptuous about the complexity that are arising

while maintaining and managing the internal audit function. Here a wide range of control is

required so that the goals can be achieved effectively.Even with the existence of internal

audit in the public sector, it is still found that the rate of frauds is still rising.In the views of

some they are thinking that internalaudit is creating more problem and making the accounting

complex rather than solving the issues(Alaraji, 2020). The problem that arises in internal

audit of public sector are lack of management responses to internal audit findings, lack of

assigning the proper duties and responsibilities to the auditors, inadequacy in maintaining the

routine audits, lack of internal audit control within the public sector. These are some of the

reasons that are affecting the effectiveness of the audit internally in public sector. So, this

motivated the researcher to undertake a study on this topic so that views can be given to solve

those challenges.

Internal audit is a business process that is used by the organization to increase its

efficiency or to add value. It is an activity of assurance and consulting. This activity helps the

organisation to achieve its goal. Internal audit is a systematic approach that helps in risk

management by improving the effectiveness. This is used by the organisation so that a proper

account can be maintained by the business and the upper body and the government uses this

to make adecision. Public sector businesses are those organisations which is controlled and

run by the national, state or any local legal body of the country. In this sector the major

shareholder of the enterprise is the government body (Kagermann, Kinney and Küting, 2021).

In recent years, the Government of the Gambia has made significant progress in

strengthening fiscal discipline and improving the efficiency of its Public Financial

Management System (PFM). The Government has strengthened the legislative base,

increased the transparency of budget information, improved control over expenditures, and

strengthened budget oversight. At the heart of these initiatives was the establishment of the

Internal Audit Directorate through an Act of Parliament the (Public Financial Act 2014) and

its accompanying Financial Regulations 2016.

Background of the research problem:

Many organisations are hastily presumptuous about the complexity that are arising

while maintaining and managing the internal audit function. Here a wide range of control is

required so that the goals can be achieved effectively.Even with the existence of internal

audit in the public sector, it is still found that the rate of frauds is still rising.In the views of

some they are thinking that internalaudit is creating more problem and making the accounting

complex rather than solving the issues(Alaraji, 2020). The problem that arises in internal

audit of public sector are lack of management responses to internal audit findings, lack of

assigning the proper duties and responsibilities to the auditors, inadequacy in maintaining the

routine audits, lack of internal audit control within the public sector. These are some of the

reasons that are affecting the effectiveness of the audit internally in public sector. So, this

motivated the researcher to undertake a study on this topic so that views can be given to solve

those challenges.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Justify the reason

The objective to choose this topic is that it will help in outlining the task that will

make it possible to achieve the purpose of the researchproblem. Risk management is the

process which is used by the public sector organisation to identify, analyse the risk and

threatmet within public sector. There are so many risks that occurs while preparing the

internal audit. This concept helps the public sector enterprise to maintain a balance, so that

preventive measures can be taken. This helps the organisation to achieve the objective and

aids the managerial decision (Bananuka and et. al, 2018).

Value of the research:

This research will help in gaining a proper insight about the internal audit process of

the public sector. This will also help in identifying the key areas which are required for a

proper functioning. This research will also help the government to know what measures that

they will take so that they can minimize those risk which are involved in the internal audit.

They will also help the different stakeholders like local councils, public officials, vote

controllers of government etc. so that proper skills and knowledge can be gained. Public

sector organisation can also get benefit because it will help them in saving their time and

money as they will get to know the solution of the problems that are arising while preparing

the internal audit. This research will also help in gaining the confidence that are developing a

broader way of seeing the things(Ghaleb, Kamardin and Al-Qadasi, 2020).

Research aims and objective:

Research Aim: To identify the functions or roles of internal audit in risk management: A

study on public sector organisations

Research Objectives:

To identify the concept of internal audit in context with public sector

To determine the role of internal audit in risk management within public sector

To examine the benefits of internal auditing for public sector organisation in the

Gambia

To evaluate the challenges confronted by public sector organisation due to poor

internal audit process

The objective to choose this topic is that it will help in outlining the task that will

make it possible to achieve the purpose of the researchproblem. Risk management is the

process which is used by the public sector organisation to identify, analyse the risk and

threatmet within public sector. There are so many risks that occurs while preparing the

internal audit. This concept helps the public sector enterprise to maintain a balance, so that

preventive measures can be taken. This helps the organisation to achieve the objective and

aids the managerial decision (Bananuka and et. al, 2018).

Value of the research:

This research will help in gaining a proper insight about the internal audit process of

the public sector. This will also help in identifying the key areas which are required for a

proper functioning. This research will also help the government to know what measures that

they will take so that they can minimize those risk which are involved in the internal audit.

They will also help the different stakeholders like local councils, public officials, vote

controllers of government etc. so that proper skills and knowledge can be gained. Public

sector organisation can also get benefit because it will help them in saving their time and

money as they will get to know the solution of the problems that are arising while preparing

the internal audit. This research will also help in gaining the confidence that are developing a

broader way of seeing the things(Ghaleb, Kamardin and Al-Qadasi, 2020).

Research aims and objective:

Research Aim: To identify the functions or roles of internal audit in risk management: A

study on public sector organisations

Research Objectives:

To identify the concept of internal audit in context with public sector

To determine the role of internal audit in risk management within public sector

To examine the benefits of internal auditing for public sector organisation in the

Gambia

To evaluate the challenges confronted by public sector organisation due to poor

internal audit process

To identify the ways that would be used by public sector organisations in overcoming

the challenges associated with poor internal audit.

Research Question:

What are the functions and roles of internal auditin public sector risk management for

Gambia?

the challenges associated with poor internal audit.

Research Question:

What are the functions and roles of internal auditin public sector risk management for

Gambia?

Literature review

Literature review is used to see the overview of the past study of the topic internal

audit and risk management. Literature review contains the past published report of the given

topic that is done by many investigators. There are so many secondary sources to study

literature reviews these are books, journal, magazine, articles, online sources, websites etc.

These sources are being detailed in the study so that more understanding and knowledge can

be gained about the problem.

Explain the function and role that is being played to minimize risk by doing internal audit in

the Gambia

According toListon-Heyes and Juillet (2019), Auditing is the process which is done

by the auditors of the organisation so that they can verify the financial statement made by the

accountant. This is on –site verification process that ensure compliance of the requirements.

This is done so that a financial data can be fair and accurate. Audit is done so that a clear

picture can be viewed by the shareholders, government, customer, supplier and partners.

There are two types of auditors: internal and external. An internal auditor is a part of the

business that is responsible for the analysis of the financial data and reviews it. The external

auditor is different from internal audit in each and every way of doing work. The person is a

third party who do audit for the firm.

Auditing is classified in four ways and that are private, statutory, internal and

management audit. Private audit is done because the shareholder of the companies wants it

but statutory audit is carried out because the law wants it to be done. Internal audit is made by

the employee of the company and the management audit is done to check the effectiveness of

management in the organisation(Oladejo and Nwachukwu, 2021).

Internal Auditing is an independent, objective assurance and consulting activity designed to

add value and improve an organisation’s operations. It helps an organisation accomplish its

objectives by bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control and governance processes. (IIA IPPF).

Literature review is used to see the overview of the past study of the topic internal

audit and risk management. Literature review contains the past published report of the given

topic that is done by many investigators. There are so many secondary sources to study

literature reviews these are books, journal, magazine, articles, online sources, websites etc.

These sources are being detailed in the study so that more understanding and knowledge can

be gained about the problem.

Explain the function and role that is being played to minimize risk by doing internal audit in

the Gambia

According toListon-Heyes and Juillet (2019), Auditing is the process which is done

by the auditors of the organisation so that they can verify the financial statement made by the

accountant. This is on –site verification process that ensure compliance of the requirements.

This is done so that a financial data can be fair and accurate. Audit is done so that a clear

picture can be viewed by the shareholders, government, customer, supplier and partners.

There are two types of auditors: internal and external. An internal auditor is a part of the

business that is responsible for the analysis of the financial data and reviews it. The external

auditor is different from internal audit in each and every way of doing work. The person is a

third party who do audit for the firm.

Auditing is classified in four ways and that are private, statutory, internal and

management audit. Private audit is done because the shareholder of the companies wants it

but statutory audit is carried out because the law wants it to be done. Internal audit is made by

the employee of the company and the management audit is done to check the effectiveness of

management in the organisation(Oladejo and Nwachukwu, 2021).

Internal Auditing is an independent, objective assurance and consulting activity designed to

add value and improve an organisation’s operations. It helps an organisation accomplish its

objectives by bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control and governance processes. (IIA IPPF).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNAL AUDIT is an independent process which many organisations see as a tool for

ensuring the working of internal system. This is done within the company so that evaluation

offinancial activities can be made. Some of the employee of the business is responsible to

perform the auditing.This activity isperformed by the audit department and the employee

whose function is known as internal auditor (García-Meca, Ramón-Llorens and Martínez-

Ferrero, 2021). Internal audit is performed by the company to reduce the risks that are being

identified andanalysed while making the auditing. There are so many roles of internal audit in

risk management within public sector:

The internal auditor is responsible to the account officer for providing a

comprehensive report of an audit of all the activities and operations. He is directly

responsible for monitoring the financial statement so that goals can be achieved

effectively and efficiently.

They are the one who analyse the fraud and misleads so that they can safeguard the

interest of the organisation. Normal safeguard means observing the government

activities and laws so that internal checks can be made(Kahyaoglu and Caliyurt,

2018).

They also control that the revenue is being collected and the money received or paid

are being placed under the correct accounts or sub heads.

The major responsibility that are being played by then is to see that all the issues

made by the government in the company is stored correctly and issued by the right

person.

The issue which are made is also being used for the purpose for which they are

authorized by the government in the public sector.

The internal auditor of the public sector also plays the role in which they keep an eye on the

system of control of expenditure where they see that all the payment are made to the right and

authorised person (ALBAWWAT, AL-HAJAIA and AL FRIJAT, 2021).

Internal auditor plays the role where they properly evaluate the accounting records

and see that if they are accurate and fair. No untraded practice has been made or any

corruption is not involved (Mustafa and Al-Nimer, 2018).

ensuring the working of internal system. This is done within the company so that evaluation

offinancial activities can be made. Some of the employee of the business is responsible to

perform the auditing.This activity isperformed by the audit department and the employee

whose function is known as internal auditor (García-Meca, Ramón-Llorens and Martínez-

Ferrero, 2021). Internal audit is performed by the company to reduce the risks that are being

identified andanalysed while making the auditing. There are so many roles of internal audit in

risk management within public sector:

The internal auditor is responsible to the account officer for providing a

comprehensive report of an audit of all the activities and operations. He is directly

responsible for monitoring the financial statement so that goals can be achieved

effectively and efficiently.

They are the one who analyse the fraud and misleads so that they can safeguard the

interest of the organisation. Normal safeguard means observing the government

activities and laws so that internal checks can be made(Kahyaoglu and Caliyurt,

2018).

They also control that the revenue is being collected and the money received or paid

are being placed under the correct accounts or sub heads.

The major responsibility that are being played by then is to see that all the issues

made by the government in the company is stored correctly and issued by the right

person.

The issue which are made is also being used for the purpose for which they are

authorized by the government in the public sector.

The internal auditor of the public sector also plays the role in which they keep an eye on the

system of control of expenditure where they see that all the payment are made to the right and

authorised person (ALBAWWAT, AL-HAJAIA and AL FRIJAT, 2021).

Internal auditor plays the role where they properly evaluate the accounting records

and see that if they are accurate and fair. No untraded practice has been made or any

corruption is not involved (Mustafa and Al-Nimer, 2018).

Gambia is a country in western Africa which financial condition is not as better as other

countries so here internal audit plays an important role in decreasing the risk for the public

sector enterprise. So here internal audits beneficial so that they can protect their financial

performance. If Gambia public sector adopts the strategy of internal audit, then they can

strongly control their internal finance. Internal audits evaluate the activities and action and

ensure the public sector enterprise to design and implement the auditing in effective manner.

If the public sector enterprise uses their internal auditors, then they can spot the redundancies

that arise in the business practices and on governance procedure (Calvin, 2021). With the

help of these they can save their time and money and come up with better decision for their

organisation. Gambia does not have advanced technology by which they can save their data

from being leak, so with the help of internal auditor they can scrutinize their information and

provide cyber security. This would also help them by examining that the policies which are

made by the government are secured and are efficiently in acquisition of the goal. Internal

audit also helps in identifying the risk that are involved in the organisation and provide helps

so that they can mitigate the risk and work on it to resolve the problems. Internal auditors of

the public sector also help in analysing the financial statement and verify whether they are

accurate and are integrated with each other or not.Internal audits check the laws, regulations,

and industry standards with which your organization needs to comply and determine whether

you are working according to it or not(Newman and Comfort, 2018).

The Government needs to carry out key fundamental roles to achieve economic

transformation andone of which is good governance and strong internal controls. The

accelerating needs for changes of Internal Audit services in public sector are substantial and

must be coordinated by the directorate of Internal Audit in line with international auditing

standards and best practices. The underlying caveat is that individuals singularly or

collectively do not engage in corruption or mismanagement of public funds without

depending on the weaknesses in the systems. Proper governance cannot depend on how

ethical public servants and effective judicial systems are. Thus, the only veritable way of

mitigating mismanagement of public funds is to ensure management adhere to policies,

procedures and internal controls in place within the public sector (Fatah, Hamad and Qader,

2021).

countries so here internal audit plays an important role in decreasing the risk for the public

sector enterprise. So here internal audits beneficial so that they can protect their financial

performance. If Gambia public sector adopts the strategy of internal audit, then they can

strongly control their internal finance. Internal audits evaluate the activities and action and

ensure the public sector enterprise to design and implement the auditing in effective manner.

If the public sector enterprise uses their internal auditors, then they can spot the redundancies

that arise in the business practices and on governance procedure (Calvin, 2021). With the

help of these they can save their time and money and come up with better decision for their

organisation. Gambia does not have advanced technology by which they can save their data

from being leak, so with the help of internal auditor they can scrutinize their information and

provide cyber security. This would also help them by examining that the policies which are

made by the government are secured and are efficiently in acquisition of the goal. Internal

audit also helps in identifying the risk that are involved in the organisation and provide helps

so that they can mitigate the risk and work on it to resolve the problems. Internal auditors of

the public sector also help in analysing the financial statement and verify whether they are

accurate and are integrated with each other or not.Internal audits check the laws, regulations,

and industry standards with which your organization needs to comply and determine whether

you are working according to it or not(Newman and Comfort, 2018).

The Government needs to carry out key fundamental roles to achieve economic

transformation andone of which is good governance and strong internal controls. The

accelerating needs for changes of Internal Audit services in public sector are substantial and

must be coordinated by the directorate of Internal Audit in line with international auditing

standards and best practices. The underlying caveat is that individuals singularly or

collectively do not engage in corruption or mismanagement of public funds without

depending on the weaknesses in the systems. Proper governance cannot depend on how

ethical public servants and effective judicial systems are. Thus, the only veritable way of

mitigating mismanagement of public funds is to ensure management adhere to policies,

procedures and internal controls in place within the public sector (Fatah, Hamad and Qader,

2021).

The Internal Audit regulations establishing internal audit units in MDAs are undergoing

review to capture lessons learnt and incorporate best practices. An organizational review has

proposed changes to internal audit structures and numbers, and Internal Auditors in MDAs

requires enhanced skills development to provide specialized services e.g., consulting services

over internal controls, risk management and public /corporate governance processes, IT,

value for money, review of financial information, system audits and forensic investigations

and scope coverage.

The rolling over of internal audit functions has begun in January 2016. The Internal Audit

Directorate (IAD) in collaboration with the personnel management unit (PMO) and various

Permanent Secretaries has created internal audit units and posted internal auditors at the

following Ministries: Ministry of Health, Ministry of Agriculture, Judiciary, Ministry of

Basic Secondary Education, Ministry of Interior, Office of the President Ministry of Finance

and Economic Affairs, Ministry of Works Transport and Information and the National

Assembly. Although, efforts have been made to recruit qualified personnel in the area of

accounting, economics and other related fields, skills in internal auditing are relatively low.

A high numberof junior auditorsarerecruitedfresh from university. This is because internal

auditing is still new in the Gambia and people with internal audit qualifications are low.

In the Gambia public sector, the internal audit department also faces some challenges

while doing the auditing of their financial data. The problems make it difficult for the

auditor to carry out the auditing in smooth manner. Some of the issues also arrive from

the staff who are not part of internal audit.This research alsowill help to find the

challenges that are arising in Gambia. Some of the challenges that they are facing are:

Lack of accounting system: Some of the audit findingsof public sector enterprise

of the Gambia have shown that the country has unavailability of adequate

accounting system which create problems to the auditor as sometimes it is difficult

for them to categorise the audit according to the current rules and policies.

Non recognition of audit department: the internal audit department of the public

sector feels frustrated and unwanted as the employee or other members does not

recognise them as unit and give no importance. So due to this factor they work

poorly and without willingly and prepare a proper audit(Mubako, 2019).

review to capture lessons learnt and incorporate best practices. An organizational review has

proposed changes to internal audit structures and numbers, and Internal Auditors in MDAs

requires enhanced skills development to provide specialized services e.g., consulting services

over internal controls, risk management and public /corporate governance processes, IT,

value for money, review of financial information, system audits and forensic investigations

and scope coverage.

The rolling over of internal audit functions has begun in January 2016. The Internal Audit

Directorate (IAD) in collaboration with the personnel management unit (PMO) and various

Permanent Secretaries has created internal audit units and posted internal auditors at the

following Ministries: Ministry of Health, Ministry of Agriculture, Judiciary, Ministry of

Basic Secondary Education, Ministry of Interior, Office of the President Ministry of Finance

and Economic Affairs, Ministry of Works Transport and Information and the National

Assembly. Although, efforts have been made to recruit qualified personnel in the area of

accounting, economics and other related fields, skills in internal auditing are relatively low.

A high numberof junior auditorsarerecruitedfresh from university. This is because internal

auditing is still new in the Gambia and people with internal audit qualifications are low.

In the Gambia public sector, the internal audit department also faces some challenges

while doing the auditing of their financial data. The problems make it difficult for the

auditor to carry out the auditing in smooth manner. Some of the issues also arrive from

the staff who are not part of internal audit.This research alsowill help to find the

challenges that are arising in Gambia. Some of the challenges that they are facing are:

Lack of accounting system: Some of the audit findingsof public sector enterprise

of the Gambia have shown that the country has unavailability of adequate

accounting system which create problems to the auditor as sometimes it is difficult

for them to categorise the audit according to the current rules and policies.

Non recognition of audit department: the internal audit department of the public

sector feels frustrated and unwanted as the employee or other members does not

recognise them as unit and give no importance. So due to this factor they work

poorly and without willingly and prepare a proper audit(Mubako, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Lack of proper information: As the public sector of Gambia is not as

professional as other countries so sometime, they do not register the payment or

expenses that are being paid or received and submit it to internal audit without any

recording. This creates problem to the audit team as their accounts does not match

and cannot be able to give clear auditing.

Inadequate observation: some of the internal auditor neglect their roles and

duties that are assigned to them. So, they are not able to observe the accounts and

made mistake which lead to create an unfair auditing.

As Gambia public sector organisation faces the above challenges so to overcome these

challenges they must adopt those strategies which are beneficial and also help them in

maintaining the proper internal audits. So,there are some of the ways through which they can

cope up with the problems. They can develop or design a proper reporting structure before

finalising the auditing. If they can design a seamless structure, then the level of

communication and transparency will be effective and the chances of omission of error will

be decreased. They should shake their hands with the external auditors (Tamimi, 2021). With

the collaboration of both the internal and external auditing, the risk would be mitigated as

they will work for solving the gaps and provide the work accordingly. If a healthy

relationship will be established between the auditor’s community, this will boost their work

performance and will work according to the IA function. This will also help them in cutting

the costs. The internal auditor also adopts the scope of providing quality rather thanquantity

as this will provide better opportunity to the mangers to take proper decision(Lois, and et.

al ,2020).

professional as other countries so sometime, they do not register the payment or

expenses that are being paid or received and submit it to internal audit without any

recording. This creates problem to the audit team as their accounts does not match

and cannot be able to give clear auditing.

Inadequate observation: some of the internal auditor neglect their roles and

duties that are assigned to them. So, they are not able to observe the accounts and

made mistake which lead to create an unfair auditing.

As Gambia public sector organisation faces the above challenges so to overcome these

challenges they must adopt those strategies which are beneficial and also help them in

maintaining the proper internal audits. So,there are some of the ways through which they can

cope up with the problems. They can develop or design a proper reporting structure before

finalising the auditing. If they can design a seamless structure, then the level of

communication and transparency will be effective and the chances of omission of error will

be decreased. They should shake their hands with the external auditors (Tamimi, 2021). With

the collaboration of both the internal and external auditing, the risk would be mitigated as

they will work for solving the gaps and provide the work accordingly. If a healthy

relationship will be established between the auditor’s community, this will boost their work

performance and will work according to the IA function. This will also help them in cutting

the costs. The internal auditor also adopts the scope of providing quality rather thanquantity

as this will provide better opportunity to the mangers to take proper decision(Lois, and et.

al ,2020).

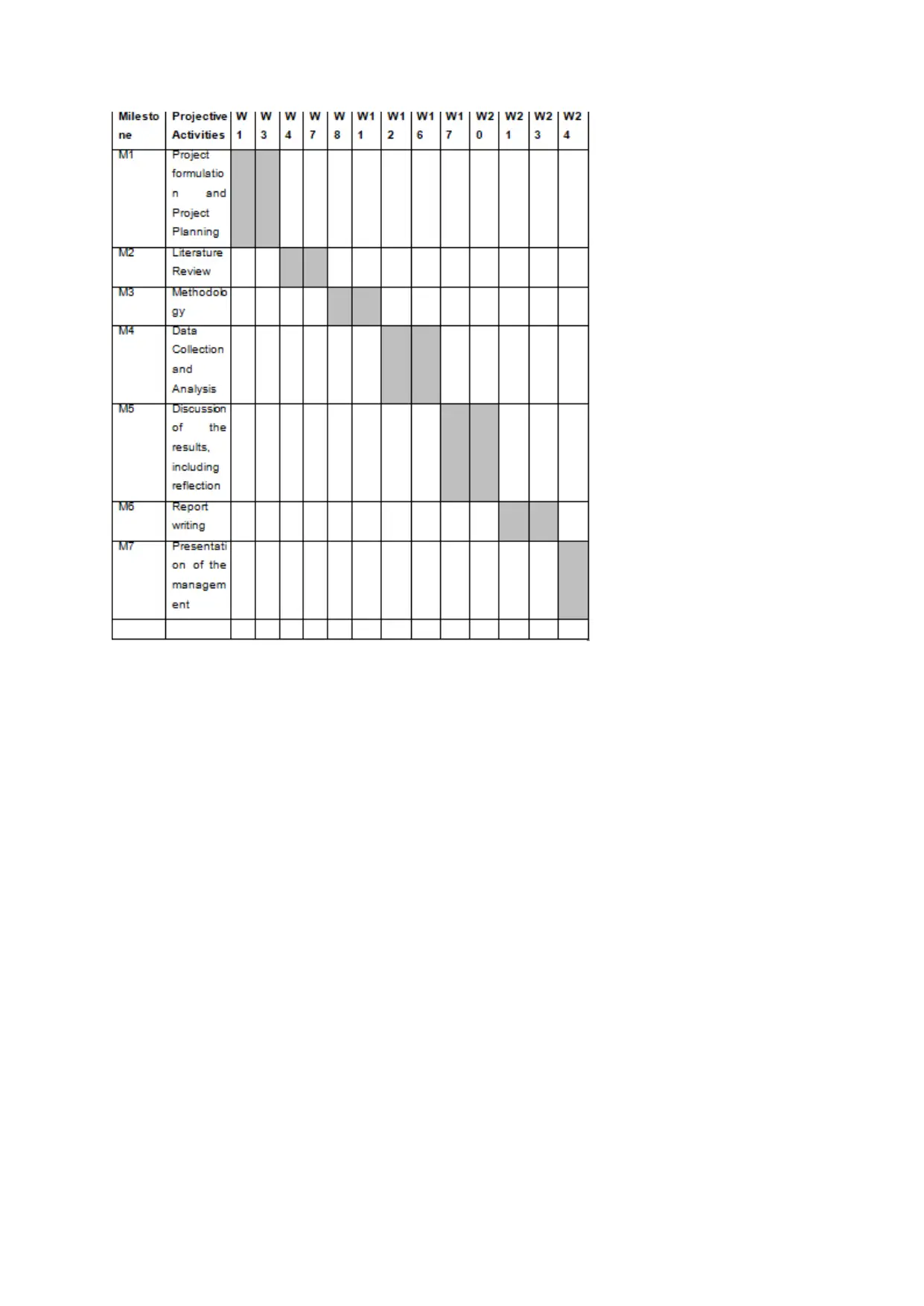

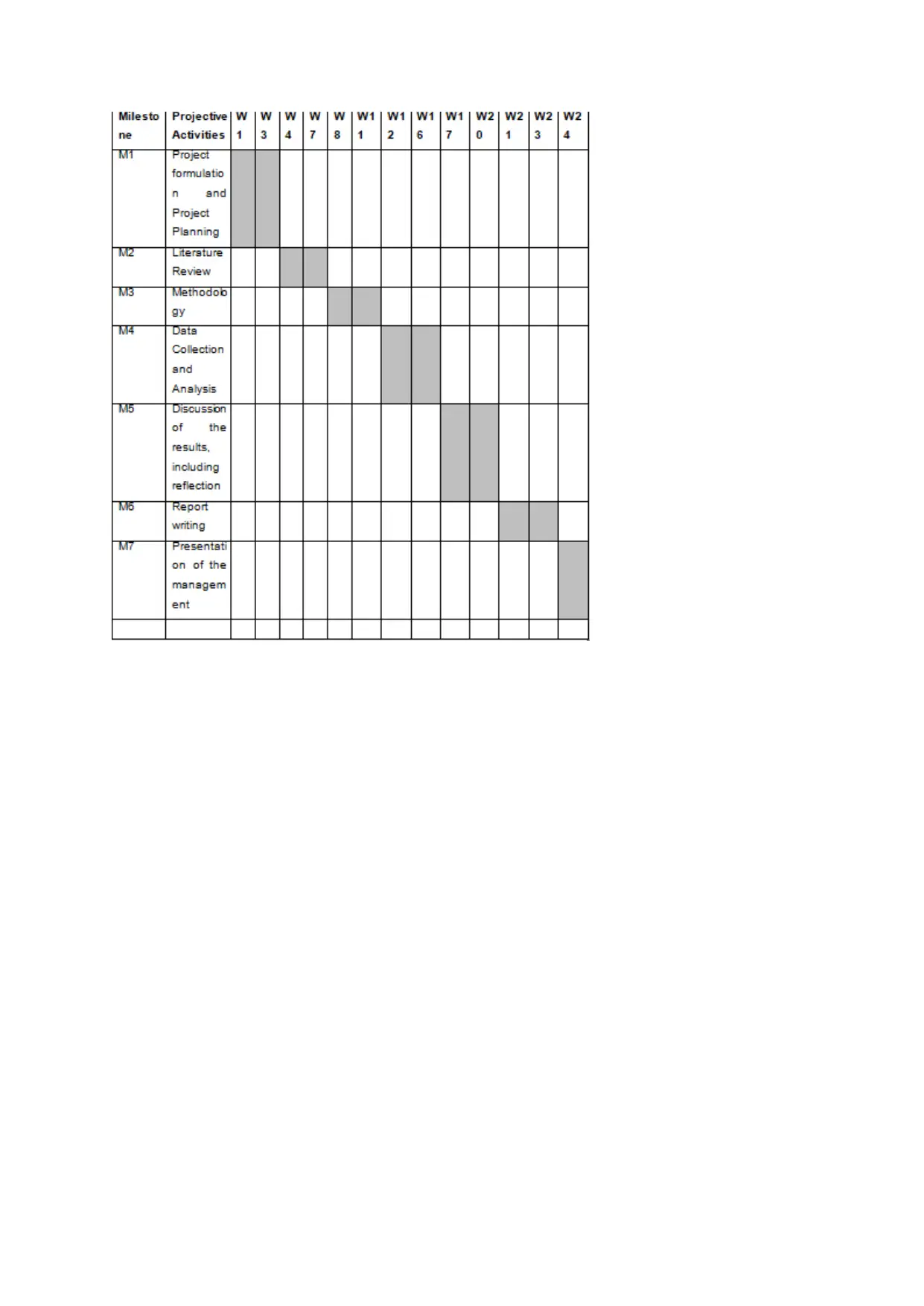

Research methodology

Research methodology is the process which is used to identify, analyse, collect and

interpret the information of the study of internal audit functions in the public sector risk

management. Quantitative and Qualitative are the two type of research methodology. In the

present research topic Quantitative methodology will be selected because the data that will be

collected is in the form of numbers or numeric (Snyder, 2019).

Research philosophy: It is a set of belief regarding the way within which information

about a topic or subject should be collected. There are three types of research philosophy that

is Ontology, Epistemology, Axiology. Iwill select Epistemology philosophy.In this

positivism will be chosen so that quantitative data in the form of primary source can be

gathered.

Research approach: This is the procedure followed for evaluating gathered

information through the of use of effective approach. There are two types of research

approaches such as inductive and deductive. In the near future if data will be gathered then

Deductive approachwill be chosen. This is the essential approach that assists in analysing

numerical information about the topic(Hansmeier, Schiller and Rogge, 2021).

Research strategy: This is that part of onion framework which is used in assisting to

collect the accurate information regarding the different research approach. There are so many

types of strategy that is used to gather information these are survey, case study, action

research, observation and many more. In the current research topic,I will choose survey

strategy to collect data as this will help in gathering appropriate number of samples.

Research choice: it is used to choose the methodology to be adopted to gather the

quantitative and qualitative data. Mono method, Mixed method and Multi-mixed method are

the three-choice available to the investigator to choose among them. In the current scenario

Mono method will be chosen to collect data. This will be selected as only one methodology is

to be selected out of two and in this whole report only single data that is numeric data is to be

collected for further analysis(Iovino and Tsitsianis, 2020).

Research methodology is the process which is used to identify, analyse, collect and

interpret the information of the study of internal audit functions in the public sector risk

management. Quantitative and Qualitative are the two type of research methodology. In the

present research topic Quantitative methodology will be selected because the data that will be

collected is in the form of numbers or numeric (Snyder, 2019).

Research philosophy: It is a set of belief regarding the way within which information

about a topic or subject should be collected. There are three types of research philosophy that

is Ontology, Epistemology, Axiology. Iwill select Epistemology philosophy.In this

positivism will be chosen so that quantitative data in the form of primary source can be

gathered.

Research approach: This is the procedure followed for evaluating gathered

information through the of use of effective approach. There are two types of research

approaches such as inductive and deductive. In the near future if data will be gathered then

Deductive approachwill be chosen. This is the essential approach that assists in analysing

numerical information about the topic(Hansmeier, Schiller and Rogge, 2021).

Research strategy: This is that part of onion framework which is used in assisting to

collect the accurate information regarding the different research approach. There are so many

types of strategy that is used to gather information these are survey, case study, action

research, observation and many more. In the current research topic,I will choose survey

strategy to collect data as this will help in gathering appropriate number of samples.

Research choice: it is used to choose the methodology to be adopted to gather the

quantitative and qualitative data. Mono method, Mixed method and Multi-mixed method are

the three-choice available to the investigator to choose among them. In the current scenario

Mono method will be chosen to collect data. This will be selected as only one methodology is

to be selected out of two and in this whole report only single data that is numeric data is to be

collected for further analysis(Iovino and Tsitsianis, 2020).

Research design:This is used to know the impact that will be made after the data is

being collected and evaluated. The research design has three types that are experimental,

descriptive and exploratory. In the present research report Descriptive design will be selected.

This type of research design is significant in gathering, analysing and using numerical

information regarding any subject or topic.

Data collection: it is that technique which helps in collecting the appropriate piece of

information which is useful in obtaining the aims and objectives. Data collection is divided

into two parts that are: primary and secondary data collection. In this topic the data that will

be collected is in primary source. This is selected by me because I want to gather the

firsthand data for their experiment.

Time horizon: it is that part which is used to know the exact time that will be needed to

complete the research. Cross-sectional and longitudinal time horizon is the two types. In this

report cross-sectional time horizon is being chosen to so that research can be completed in

shorter time period(Davidavičienė, 2018).

Data Analysis:Data analysis is a part of the research methodology that helps in

analysing the information in systematic way. The data analysis is divided into two parts:

frequency distribution analysis and thematic analysis. Investigator has selected the frequency

distribution analysis to evaluate the numerical information in effective and efficient manner.

This method helps in evaluating and analysing the reliability and validity of the gathered

numerical piece of information.

being collected and evaluated. The research design has three types that are experimental,

descriptive and exploratory. In the present research report Descriptive design will be selected.

This type of research design is significant in gathering, analysing and using numerical

information regarding any subject or topic.

Data collection: it is that technique which helps in collecting the appropriate piece of

information which is useful in obtaining the aims and objectives. Data collection is divided

into two parts that are: primary and secondary data collection. In this topic the data that will

be collected is in primary source. This is selected by me because I want to gather the

firsthand data for their experiment.

Time horizon: it is that part which is used to know the exact time that will be needed to

complete the research. Cross-sectional and longitudinal time horizon is the two types. In this

report cross-sectional time horizon is being chosen to so that research can be completed in

shorter time period(Davidavičienė, 2018).

Data Analysis:Data analysis is a part of the research methodology that helps in

analysing the information in systematic way. The data analysis is divided into two parts:

frequency distribution analysis and thematic analysis. Investigator has selected the frequency

distribution analysis to evaluate the numerical information in effective and efficient manner.

This method helps in evaluating and analysing the reliability and validity of the gathered

numerical piece of information.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

From the above research proposal, it is being concluded that internal audit is important to

minimise the risk that is involved in the public sector by the government rules and regulation.

It is also concluded that a proper auditing helps the organisation to achieve the goals and

make proper decision by seeing the audit report that have been made by the internal auditors

within the organisation.Internal audit will only fully achieve its objectives if the weaknesses

identified are addressed and risk becomes effectively managed. (ACCA website, brief guide

to internal audit).

From the above research proposal, it is being concluded that internal audit is important to

minimise the risk that is involved in the public sector by the government rules and regulation.

It is also concluded that a proper auditing helps the organisation to achieve the goals and

make proper decision by seeing the audit report that have been made by the internal auditors

within the organisation.Internal audit will only fully achieve its objectives if the weaknesses

identified are addressed and risk becomes effectively managed. (ACCA website, brief guide

to internal audit).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Books and journal

Alaraji, F.A.A.S., 2020. Corporate Governance and its Impact on the quality of internal

audit. Calitatea. 21(175). pp.85-90.

Bananuka and et. al, 2018. Internal audit function, audit committee effectiveness and

accountability in the Ugandan statutory corporations. Journal of Financial Reporting and

Accounting.

Davidavičienė, V., 2018. Research Methodology: An Introduction. In Modernizing the

Academic Teaching and Research Environment (pp. 1-23). Springer, Cham.

Ghaleb, B.A.A., Kamardin, H. and Al-Qadasi, A.A., 2020. Internal audit function and real

earnings management practices in an emerging market. Meditari Accountancy Research.

Hansmeier, H., Schiller, K. and Rogge, K.S., 2021. Towards methodological diversity in

sustainability transitions research? Comparing recent developments (2016-2019) with the

past (before 2016). Environmental Innovation and Societal Transitions. 38. pp.169-174.

Iovino, F. and Tsitsianis, N., 2020. The Methodology of the Research. In Changes in

European Energy Markets. Emerald Publishing Limited.

Kahyaoglu, S.B. and Caliyurt, K., 2018. Cyber security assurance process from the

internal audit perspective. Managerial Auditing Journal.

Liston-Heyes, C. and Juillet, L., 2019. Employee isolation and support for change in the

public sector: a study of the internal audit profession. Public Management Review. 21(3).

pp.423-445.

Lois, P., Drogalas, G., Karagiorgos, A. and Tsikalakis, K., 2020. Internal audits in the

digital era: opportunities risks and challenges. EuroMed Journal of Business.

Mubako, G., 2019. Internal audit outsourcing: A literature synthesis and future

directions. Australian Accounting Review. 29(3). pp.532-545.

Mustafa, F.M. and Al-Nimer, M.B., 2018. The association between enterprise risk

management and corporate governance quality: The mediating role of internal audit

performance. J. Advanced Res. L. & Econ.. 9. p.1387.

Newman, W. and Comfort, M., 2018. Investigating the value creation of internal audit

and its impact on company performance. Academy of Entrepreneurship Journal. 24(3).

pp.1-21.

Oladejo, A. and Nwachukwu, C., 2021. Assessing internal audit function and public

sector performance in Nigeria. International Journal of Economics and

Accounting. 10(1). pp.97-111.

Snyder, H., 2019. Literature review as a research methodology: An overview and

guidelines. Journal of business research.104. pp.333-339.

Books and journal

Alaraji, F.A.A.S., 2020. Corporate Governance and its Impact on the quality of internal

audit. Calitatea. 21(175). pp.85-90.

Bananuka and et. al, 2018. Internal audit function, audit committee effectiveness and

accountability in the Ugandan statutory corporations. Journal of Financial Reporting and

Accounting.

Davidavičienė, V., 2018. Research Methodology: An Introduction. In Modernizing the

Academic Teaching and Research Environment (pp. 1-23). Springer, Cham.

Ghaleb, B.A.A., Kamardin, H. and Al-Qadasi, A.A., 2020. Internal audit function and real

earnings management practices in an emerging market. Meditari Accountancy Research.

Hansmeier, H., Schiller, K. and Rogge, K.S., 2021. Towards methodological diversity in

sustainability transitions research? Comparing recent developments (2016-2019) with the

past (before 2016). Environmental Innovation and Societal Transitions. 38. pp.169-174.

Iovino, F. and Tsitsianis, N., 2020. The Methodology of the Research. In Changes in

European Energy Markets. Emerald Publishing Limited.

Kahyaoglu, S.B. and Caliyurt, K., 2018. Cyber security assurance process from the

internal audit perspective. Managerial Auditing Journal.

Liston-Heyes, C. and Juillet, L., 2019. Employee isolation and support for change in the

public sector: a study of the internal audit profession. Public Management Review. 21(3).

pp.423-445.

Lois, P., Drogalas, G., Karagiorgos, A. and Tsikalakis, K., 2020. Internal audits in the

digital era: opportunities risks and challenges. EuroMed Journal of Business.

Mubako, G., 2019. Internal audit outsourcing: A literature synthesis and future

directions. Australian Accounting Review. 29(3). pp.532-545.

Mustafa, F.M. and Al-Nimer, M.B., 2018. The association between enterprise risk

management and corporate governance quality: The mediating role of internal audit

performance. J. Advanced Res. L. & Econ.. 9. p.1387.

Newman, W. and Comfort, M., 2018. Investigating the value creation of internal audit

and its impact on company performance. Academy of Entrepreneurship Journal. 24(3).

pp.1-21.

Oladejo, A. and Nwachukwu, C., 2021. Assessing internal audit function and public

sector performance in Nigeria. International Journal of Economics and

Accounting. 10(1). pp.97-111.

Snyder, H., 2019. Literature review as a research methodology: An overview and

guidelines. Journal of business research.104. pp.333-339.

Kagermann, H., Kinney, W. and Küting, K., 2021. Internal Audit Handbook Management

with the SAP®-Audit Roadmap. Springer.

García-Meca, E., Ramón-Llorens, M.C. and Martínez-Ferrero, J., 2021. Are narcissistic

CEOs more tax aggressive? The moderating role of internal audit committees. Journal of

Business Research, 129, pp.223-235.

ALBAWWAT, I.E., AL-HAJAIA, M.E. and AL FRIJAT, Y.S., 2021. The Relationship

Between Internal Auditors' Personality Traits, Internal Audit Effectiveness, and Financial

Reporting Quality: Empirical Evidence from Jordan. The Journal of Asian Finance,

Economics and Business, 8(4), pp.797-808.

Fatah, N.A., Hamad, H.A. and Qader, K.S., 2021. The Role of Internal Audit on Financial

Performance Under IIA Standards: A Survey Study of Selected Iraqi Banks. QALAAI

ZANIST SCIENTIFIC JOURNAL, 6(2), pp.1028-1048.

Tamimi, O., 2021. The Role of Internal Audit in Risk Management from the Perspective

of Risk Managers in the Banking Sector. Australasian Accounting, Business and Finance

Journal, 15(2), pp.114-129.

Calvin, C.G., 2021. Adherence to the Internal Audit Core Principles and Threats to

Internal Audit Function Effectiveness. AUDITING: A Journal of Practice & Theory.

with the SAP®-Audit Roadmap. Springer.

García-Meca, E., Ramón-Llorens, M.C. and Martínez-Ferrero, J., 2021. Are narcissistic

CEOs more tax aggressive? The moderating role of internal audit committees. Journal of

Business Research, 129, pp.223-235.

ALBAWWAT, I.E., AL-HAJAIA, M.E. and AL FRIJAT, Y.S., 2021. The Relationship

Between Internal Auditors' Personality Traits, Internal Audit Effectiveness, and Financial

Reporting Quality: Empirical Evidence from Jordan. The Journal of Asian Finance,

Economics and Business, 8(4), pp.797-808.

Fatah, N.A., Hamad, H.A. and Qader, K.S., 2021. The Role of Internal Audit on Financial

Performance Under IIA Standards: A Survey Study of Selected Iraqi Banks. QALAAI

ZANIST SCIENTIFIC JOURNAL, 6(2), pp.1028-1048.

Tamimi, O., 2021. The Role of Internal Audit in Risk Management from the Perspective

of Risk Managers in the Banking Sector. Australasian Accounting, Business and Finance

Journal, 15(2), pp.114-129.

Calvin, C.G., 2021. Adherence to the Internal Audit Core Principles and Threats to

Internal Audit Function Effectiveness. AUDITING: A Journal of Practice & Theory.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.