Internal Control and Financial Statement Analysis of Buzzard Ltd.

VerifiedAdded on 2021/04/24

|15

|2094

|26

Report

AI Summary

This report provides a comprehensive analysis of the internal controls and financial performance of Buzzard Ltd. It begins with an overview of vertical and horizontal analyses performed on the company's financial statements, highlighting key trends in profitability, assets, and liabilities. The report then delves into the corporate governance practices of Buzzard Ltd., evaluating the board structure, internal policies, and management accountability. It assesses the effectiveness of these practices in relation to financial health and stakeholder needs. Furthermore, the report examines the company's budgetary control procedures, emphasizing the importance of budgetary planning, communication, monitoring, and reconciliation. Finally, the report proposes recommendations for strengthening internal controls, including the implementation of budgetary control to regulate costs and improve financial decision-making, supported by a timeline for budgetary control implementation. The report uses references to support the analysis.

Running head: INTERNAL CONTROL

Internal Control

Name of the Student

Name of the University

Authors Note

Course ID

Internal Control

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNAL CONTROL

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................6

Answer to Question 5:................................................................................................................9

Reference List:.........................................................................................................................13

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to Question 4:................................................................................................................6

Answer to Question 5:................................................................................................................9

Reference List:.........................................................................................................................13

2INTERNAL CONTROL

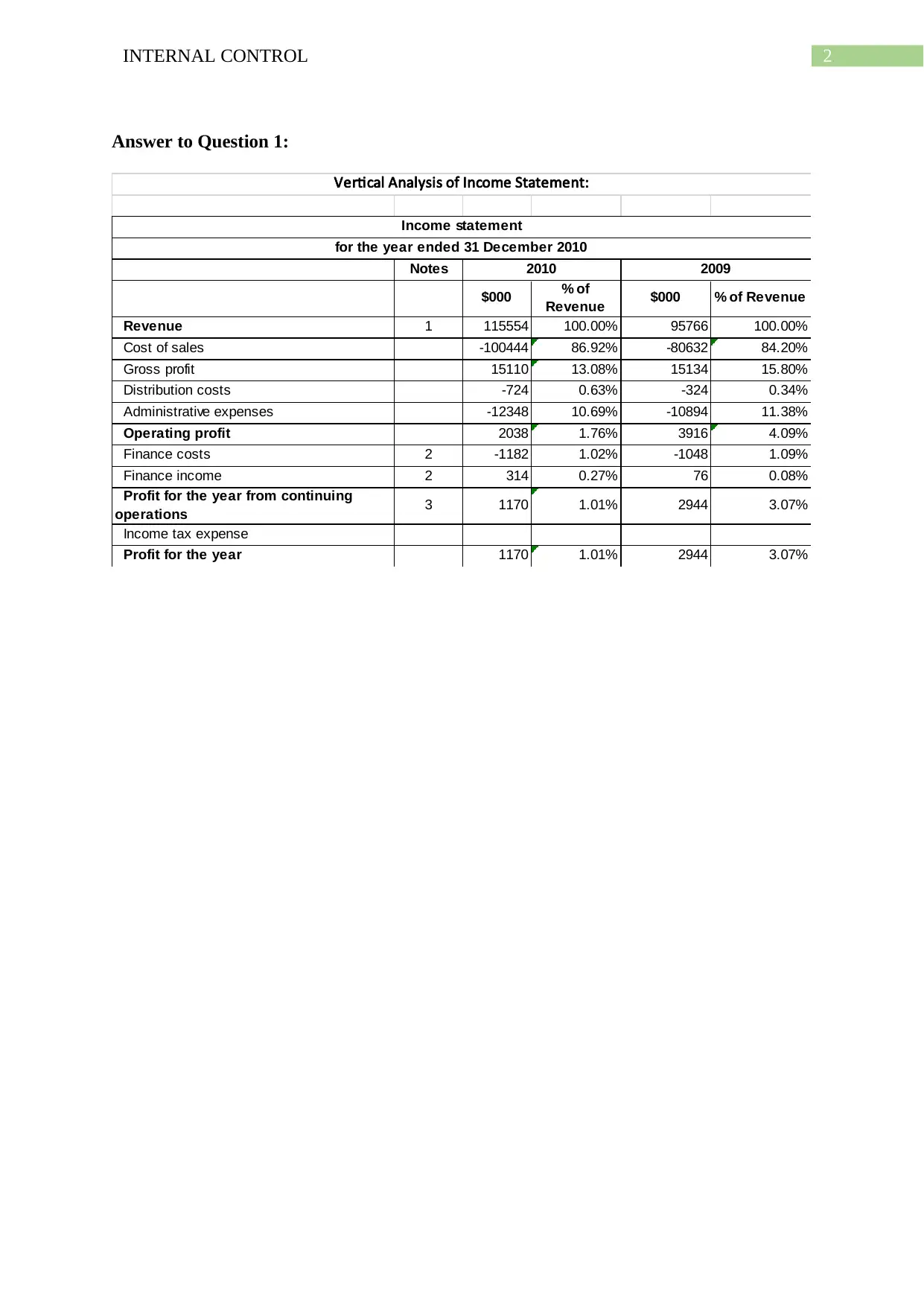

Answer to Question 1:

Notes

$000 % of

Revenue $000 % of Revenue

Revenue 1 115554 100.00% 95766 100.00%

Cost of sales -100444 86.92% -80632 84.20%

Gross profit 15110 13.08% 15134 15.80%

Distribution costs -724 0.63% -324 0.34%

Administrative expenses -12348 10.69% -10894 11.38%

Operating profit 2038 1.76% 3916 4.09%

Finance costs 2 -1182 1.02% -1048 1.09%

Finance income 2 314 0.27% 76 0.08%

Profit for the year from continuing

operations 3 1170 1.01% 2944 3.07%

Income tax expense

Profit for the year 1170 1.01% 2944 3.07%

Vertical Analysis of Income Statement:

Income statement

for the year ended 31 December 2010

2010 2009

Answer to Question 1:

Notes

$000 % of

Revenue $000 % of Revenue

Revenue 1 115554 100.00% 95766 100.00%

Cost of sales -100444 86.92% -80632 84.20%

Gross profit 15110 13.08% 15134 15.80%

Distribution costs -724 0.63% -324 0.34%

Administrative expenses -12348 10.69% -10894 11.38%

Operating profit 2038 1.76% 3916 4.09%

Finance costs 2 -1182 1.02% -1048 1.09%

Finance income 2 314 0.27% 76 0.08%

Profit for the year from continuing

operations 3 1170 1.01% 2944 3.07%

Income tax expense

Profit for the year 1170 1.01% 2944 3.07%

Vertical Analysis of Income Statement:

Income statement

for the year ended 31 December 2010

2010 2009

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNAL CONTROL

Notes

% of

Revenue $000 % of Revenue

Non-current assets

Tangible assets 8 42200 123.34% 29522 89.34%

Total non-current assets 42200 123.34% 29522 89.34%

Current assets

Inventories 9 5702 16.67% 4144 12.54%

Trade and other receivables 10 18202 53.20% 16634 50.34%

Cash and cash equivalents 4 0.01% 12 0.04%

Total current assets 23908 69.88% 20790 62.92%

Total assets 66108 193.22% 50312 152.26%

Current liabilities 11 23274 68.02% 14380 43.52%

Non-current liabilities

Borrowings and finance leases 12 6000 17.54% 0.00%

Provisions 13 1356 3.96% 1508 4.56%

Accruals and deferred income 14 1264 3.69% 1380 4.18%

Total non-current liabilities 8620 25.19% 2888 8.74%

Total liabilities 31894 93.22% 17268 52.26%

Net assets 34214 100.00% 33044 100.00%

Equity

Share capital 15 22714 66.39% 22714 68.74%

Retained earnings 11500 33.61% 10330 31.26%

Total equity 16 34214 100.00% 33044 100.00%

Vertical Analysis of Balance Sheet:

2010 2009

Balance sheet

as at 31 December 2010

Notes

% of

Revenue $000 % of Revenue

Non-current assets

Tangible assets 8 42200 123.34% 29522 89.34%

Total non-current assets 42200 123.34% 29522 89.34%

Current assets

Inventories 9 5702 16.67% 4144 12.54%

Trade and other receivables 10 18202 53.20% 16634 50.34%

Cash and cash equivalents 4 0.01% 12 0.04%

Total current assets 23908 69.88% 20790 62.92%

Total assets 66108 193.22% 50312 152.26%

Current liabilities 11 23274 68.02% 14380 43.52%

Non-current liabilities

Borrowings and finance leases 12 6000 17.54% 0.00%

Provisions 13 1356 3.96% 1508 4.56%

Accruals and deferred income 14 1264 3.69% 1380 4.18%

Total non-current liabilities 8620 25.19% 2888 8.74%

Total liabilities 31894 93.22% 17268 52.26%

Net assets 34214 100.00% 33044 100.00%

Equity

Share capital 15 22714 66.39% 22714 68.74%

Retained earnings 11500 33.61% 10330 31.26%

Total equity 16 34214 100.00% 33044 100.00%

Vertical Analysis of Balance Sheet:

2010 2009

Balance sheet

as at 31 December 2010

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNAL CONTROL

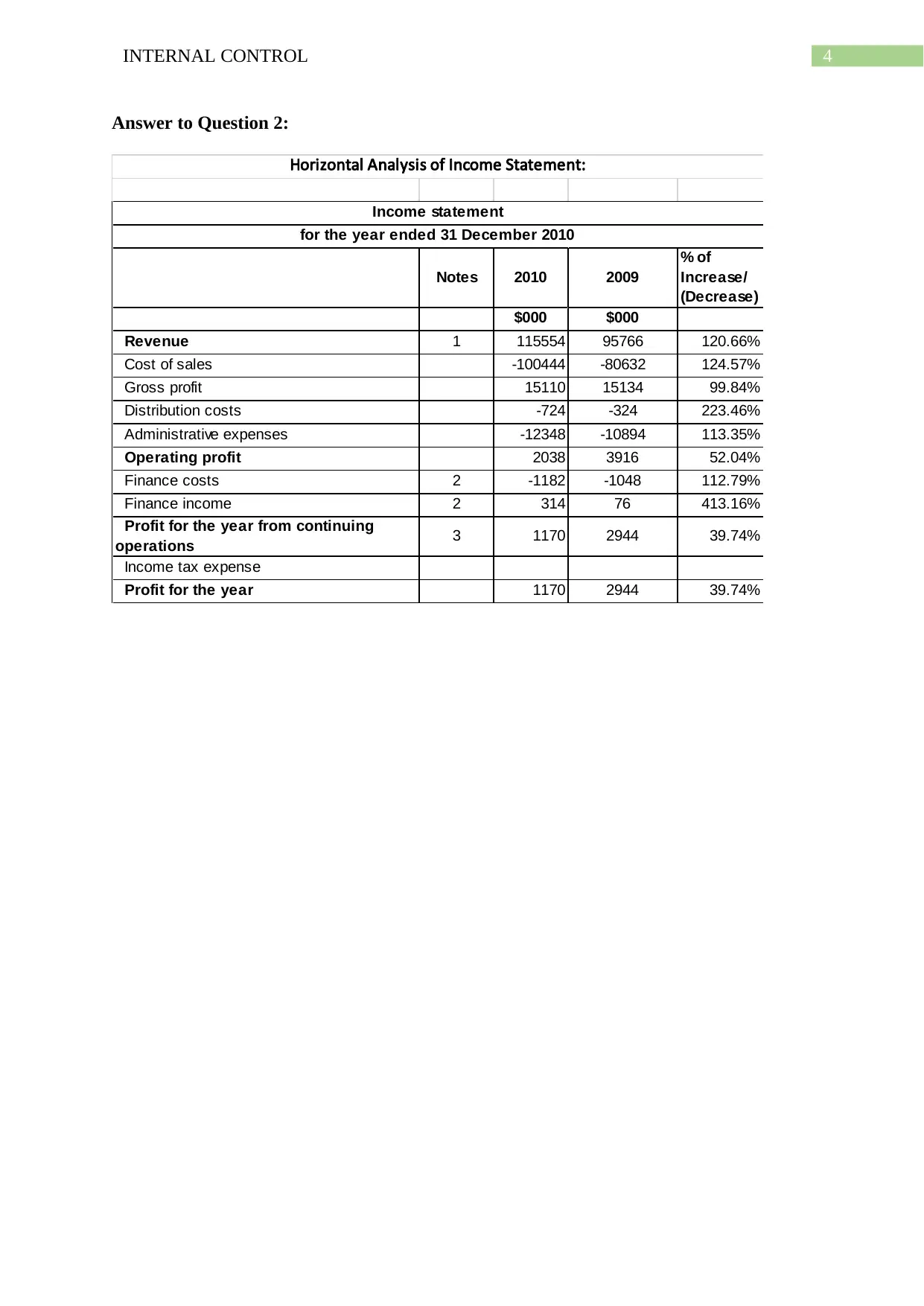

Answer to Question 2:

Notes 2010 2009

% of

Increase/

(Decrease)

$000 $000

Revenue 1 115554 95766 120.66%

Cost of sales -100444 -80632 124.57%

Gross profit 15110 15134 99.84%

Distribution costs -724 -324 223.46%

Administrative expenses -12348 -10894 113.35%

Operating profit 2038 3916 52.04%

Finance costs 2 -1182 -1048 112.79%

Finance income 2 314 76 413.16%

Profit for the year from continuing

operations 3 1170 2944 39.74%

Income tax expense

Profit for the year 1170 2944 39.74%

Horizontal Analysis of Income Statement:

Income statement

for the year ended 31 December 2010

Answer to Question 2:

Notes 2010 2009

% of

Increase/

(Decrease)

$000 $000

Revenue 1 115554 95766 120.66%

Cost of sales -100444 -80632 124.57%

Gross profit 15110 15134 99.84%

Distribution costs -724 -324 223.46%

Administrative expenses -12348 -10894 113.35%

Operating profit 2038 3916 52.04%

Finance costs 2 -1182 -1048 112.79%

Finance income 2 314 76 413.16%

Profit for the year from continuing

operations 3 1170 2944 39.74%

Income tax expense

Profit for the year 1170 2944 39.74%

Horizontal Analysis of Income Statement:

Income statement

for the year ended 31 December 2010

5INTERNAL CONTROL

Notes 2010 2009

% of

Increase/

(Decrease)

$000 $000

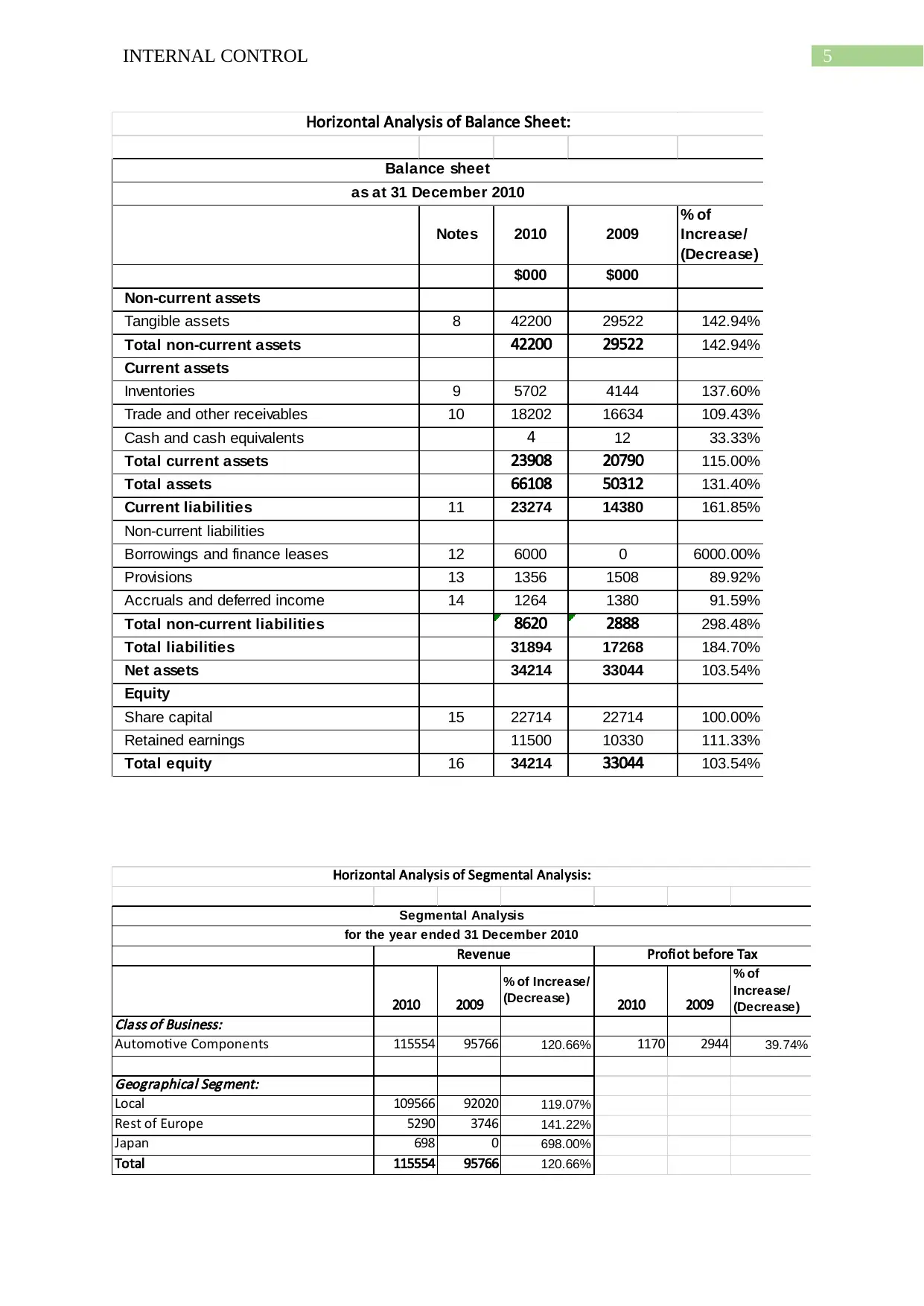

Non-current assets

Tangible assets 8 42200 29522 142.94%

Total non-current assets 42200 29522 142.94%

Current assets

Inventories 9 5702 4144 137.60%

Trade and other receivables 10 18202 16634 109.43%

Cash and cash equivalents 4 12 33.33%

Total current assets 23908 20790 115.00%

Total assets 66108 50312 131.40%

Current liabilities 11 23274 14380 161.85%

Non-current liabilities

Borrowings and finance leases 12 6000 0 6000.00%

Provisions 13 1356 1508 89.92%

Accruals and deferred income 14 1264 1380 91.59%

Total non-current liabilities 8620 2888 298.48%

Total liabilities 31894 17268 184.70%

Net assets 34214 33044 103.54%

Equity

Share capital 15 22714 22714 100.00%

Retained earnings 11500 10330 111.33%

Total equity 16 34214 33044 103.54%

Balance sheet

as at 31 December 2010

Horizontal Analysis of Balance Sheet:

2010 2009

% of Increase/

(Decrease) 2010 2009

% of

Increase/

(Decrease)

Class of Business:

Automotive Components 115554 95766 120.66% 1170 2944 39.74%

Geographical Segment:

Local 109566 92020 119.07%

Rest of Europe 5290 3746 141.22%

Japan 698 0 698.00%

Total 115554 95766 120.66%

Revenue Profiot before Tax

Segmental Analysis

for the year ended 31 December 2010

Horizontal Analysis of Segmental Analysis:

Notes 2010 2009

% of

Increase/

(Decrease)

$000 $000

Non-current assets

Tangible assets 8 42200 29522 142.94%

Total non-current assets 42200 29522 142.94%

Current assets

Inventories 9 5702 4144 137.60%

Trade and other receivables 10 18202 16634 109.43%

Cash and cash equivalents 4 12 33.33%

Total current assets 23908 20790 115.00%

Total assets 66108 50312 131.40%

Current liabilities 11 23274 14380 161.85%

Non-current liabilities

Borrowings and finance leases 12 6000 0 6000.00%

Provisions 13 1356 1508 89.92%

Accruals and deferred income 14 1264 1380 91.59%

Total non-current liabilities 8620 2888 298.48%

Total liabilities 31894 17268 184.70%

Net assets 34214 33044 103.54%

Equity

Share capital 15 22714 22714 100.00%

Retained earnings 11500 10330 111.33%

Total equity 16 34214 33044 103.54%

Balance sheet

as at 31 December 2010

Horizontal Analysis of Balance Sheet:

2010 2009

% of Increase/

(Decrease) 2010 2009

% of

Increase/

(Decrease)

Class of Business:

Automotive Components 115554 95766 120.66% 1170 2944 39.74%

Geographical Segment:

Local 109566 92020 119.07%

Rest of Europe 5290 3746 141.22%

Japan 698 0 698.00%

Total 115554 95766 120.66%

Revenue Profiot before Tax

Segmental Analysis

for the year ended 31 December 2010

Horizontal Analysis of Segmental Analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNAL CONTROL

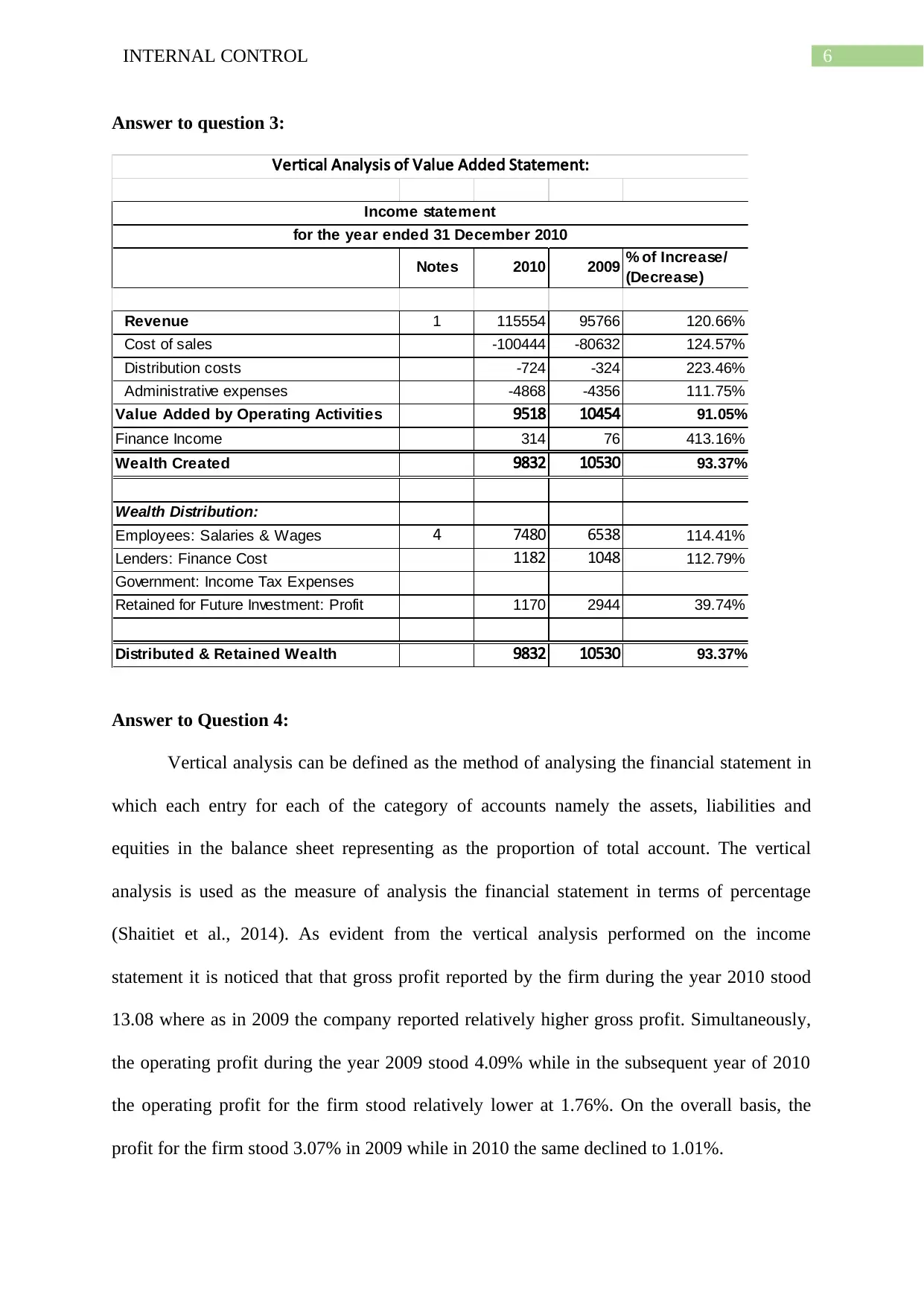

Answer to question 3:

Notes 2010 2009 % of Increase/

(Decrease)

Revenue 1 115554 95766 120.66%

Cost of sales -100444 -80632 124.57%

Distribution costs -724 -324 223.46%

Administrative expenses -4868 -4356 111.75%

Value Added by Operating Activities 9518 10454 91.05%

Finance Income 314 76 413.16%

Wealth Created 9832 10530 93.37%

Wealth Distribution:

Employees: Salaries & Wages 4 7480 6538 114.41%

Lenders: Finance Cost 1182 1048 112.79%

Government: Income Tax Expenses

Retained for Future Investment: Profit 1170 2944 39.74%

Distributed & Retained Wealth 9832 10530 93.37%

Vertical Analysis of Value Added Statement:

Income statement

for the year ended 31 December 2010

Answer to Question 4:

Vertical analysis can be defined as the method of analysing the financial statement in

which each entry for each of the category of accounts namely the assets, liabilities and

equities in the balance sheet representing as the proportion of total account. The vertical

analysis is used as the measure of analysis the financial statement in terms of percentage

(Shaitiet et al., 2014). As evident from the vertical analysis performed on the income

statement it is noticed that that gross profit reported by the firm during the year 2010 stood

13.08 where as in 2009 the company reported relatively higher gross profit. Simultaneously,

the operating profit during the year 2009 stood 4.09% while in the subsequent year of 2010

the operating profit for the firm stood relatively lower at 1.76%. On the overall basis, the

profit for the firm stood 3.07% in 2009 while in 2010 the same declined to 1.01%.

Answer to question 3:

Notes 2010 2009 % of Increase/

(Decrease)

Revenue 1 115554 95766 120.66%

Cost of sales -100444 -80632 124.57%

Distribution costs -724 -324 223.46%

Administrative expenses -4868 -4356 111.75%

Value Added by Operating Activities 9518 10454 91.05%

Finance Income 314 76 413.16%

Wealth Created 9832 10530 93.37%

Wealth Distribution:

Employees: Salaries & Wages 4 7480 6538 114.41%

Lenders: Finance Cost 1182 1048 112.79%

Government: Income Tax Expenses

Retained for Future Investment: Profit 1170 2944 39.74%

Distributed & Retained Wealth 9832 10530 93.37%

Vertical Analysis of Value Added Statement:

Income statement

for the year ended 31 December 2010

Answer to Question 4:

Vertical analysis can be defined as the method of analysing the financial statement in

which each entry for each of the category of accounts namely the assets, liabilities and

equities in the balance sheet representing as the proportion of total account. The vertical

analysis is used as the measure of analysis the financial statement in terms of percentage

(Shaitiet et al., 2014). As evident from the vertical analysis performed on the income

statement it is noticed that that gross profit reported by the firm during the year 2010 stood

13.08 where as in 2009 the company reported relatively higher gross profit. Simultaneously,

the operating profit during the year 2009 stood 4.09% while in the subsequent year of 2010

the operating profit for the firm stood relatively lower at 1.76%. On the overall basis, the

profit for the firm stood 3.07% in 2009 while in 2010 the same declined to 1.01%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNAL CONTROL

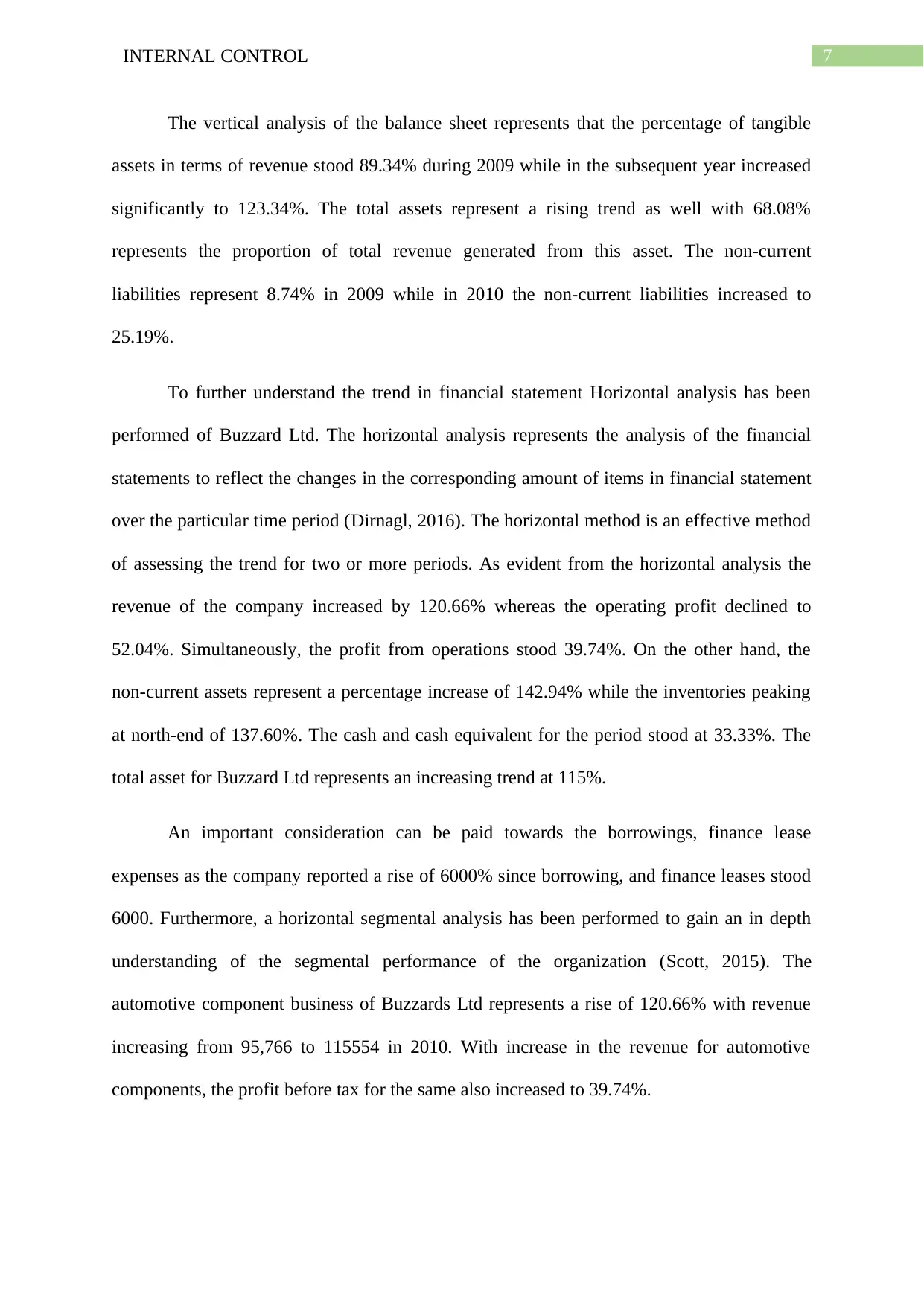

The vertical analysis of the balance sheet represents that the percentage of tangible

assets in terms of revenue stood 89.34% during 2009 while in the subsequent year increased

significantly to 123.34%. The total assets represent a rising trend as well with 68.08%

represents the proportion of total revenue generated from this asset. The non-current

liabilities represent 8.74% in 2009 while in 2010 the non-current liabilities increased to

25.19%.

To further understand the trend in financial statement Horizontal analysis has been

performed of Buzzard Ltd. The horizontal analysis represents the analysis of the financial

statements to reflect the changes in the corresponding amount of items in financial statement

over the particular time period (Dirnagl, 2016). The horizontal method is an effective method

of assessing the trend for two or more periods. As evident from the horizontal analysis the

revenue of the company increased by 120.66% whereas the operating profit declined to

52.04%. Simultaneously, the profit from operations stood 39.74%. On the other hand, the

non-current assets represent a percentage increase of 142.94% while the inventories peaking

at north-end of 137.60%. The cash and cash equivalent for the period stood at 33.33%. The

total asset for Buzzard Ltd represents an increasing trend at 115%.

An important consideration can be paid towards the borrowings, finance lease

expenses as the company reported a rise of 6000% since borrowing, and finance leases stood

6000. Furthermore, a horizontal segmental analysis has been performed to gain an in depth

understanding of the segmental performance of the organization (Scott, 2015). The

automotive component business of Buzzards Ltd represents a rise of 120.66% with revenue

increasing from 95,766 to 115554 in 2010. With increase in the revenue for automotive

components, the profit before tax for the same also increased to 39.74%.

The vertical analysis of the balance sheet represents that the percentage of tangible

assets in terms of revenue stood 89.34% during 2009 while in the subsequent year increased

significantly to 123.34%. The total assets represent a rising trend as well with 68.08%

represents the proportion of total revenue generated from this asset. The non-current

liabilities represent 8.74% in 2009 while in 2010 the non-current liabilities increased to

25.19%.

To further understand the trend in financial statement Horizontal analysis has been

performed of Buzzard Ltd. The horizontal analysis represents the analysis of the financial

statements to reflect the changes in the corresponding amount of items in financial statement

over the particular time period (Dirnagl, 2016). The horizontal method is an effective method

of assessing the trend for two or more periods. As evident from the horizontal analysis the

revenue of the company increased by 120.66% whereas the operating profit declined to

52.04%. Simultaneously, the profit from operations stood 39.74%. On the other hand, the

non-current assets represent a percentage increase of 142.94% while the inventories peaking

at north-end of 137.60%. The cash and cash equivalent for the period stood at 33.33%. The

total asset for Buzzard Ltd represents an increasing trend at 115%.

An important consideration can be paid towards the borrowings, finance lease

expenses as the company reported a rise of 6000% since borrowing, and finance leases stood

6000. Furthermore, a horizontal segmental analysis has been performed to gain an in depth

understanding of the segmental performance of the organization (Scott, 2015). The

automotive component business of Buzzards Ltd represents a rise of 120.66% with revenue

increasing from 95,766 to 115554 in 2010. With increase in the revenue for automotive

components, the profit before tax for the same also increased to 39.74%.

8INTERNAL CONTROL

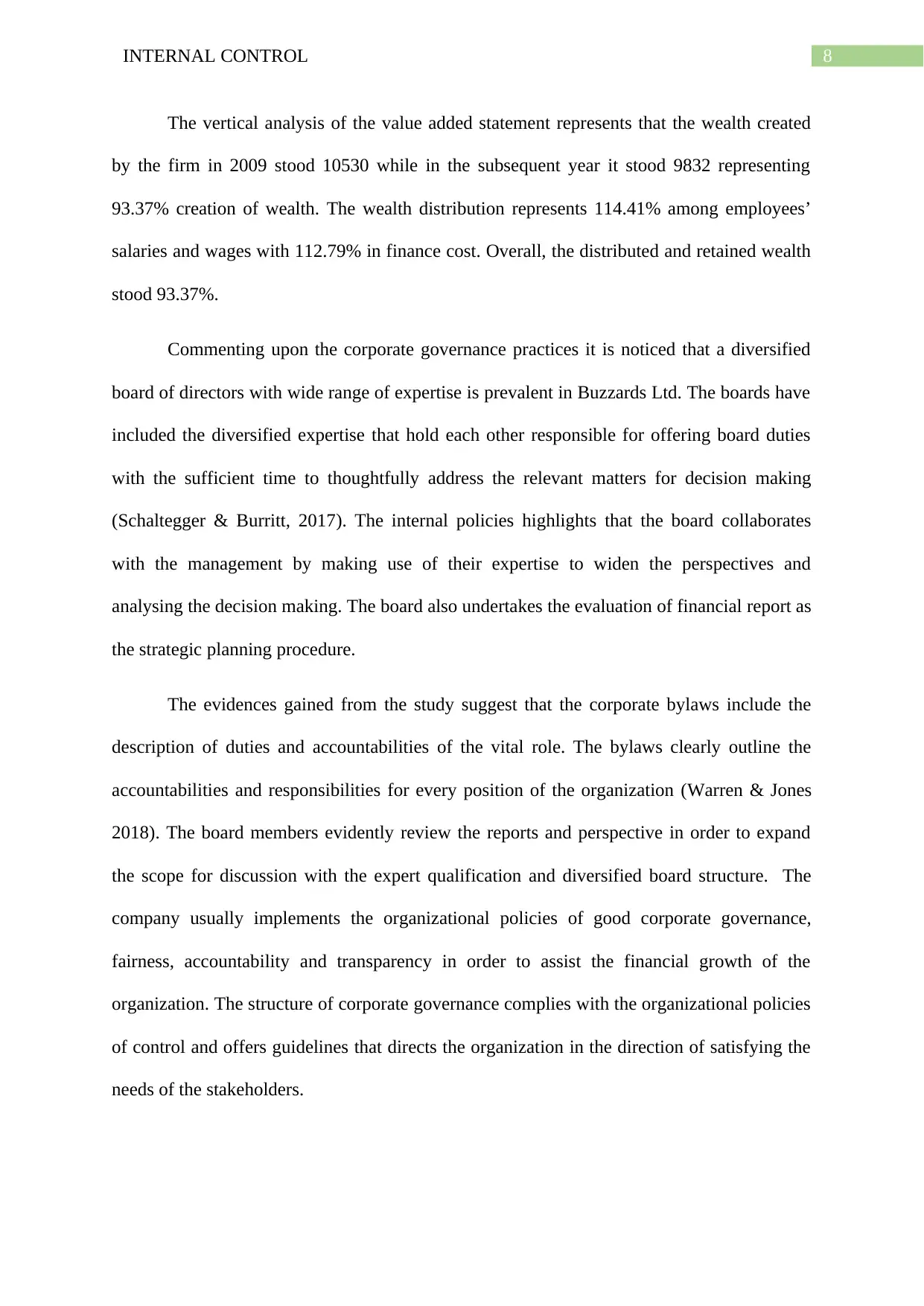

The vertical analysis of the value added statement represents that the wealth created

by the firm in 2009 stood 10530 while in the subsequent year it stood 9832 representing

93.37% creation of wealth. The wealth distribution represents 114.41% among employees’

salaries and wages with 112.79% in finance cost. Overall, the distributed and retained wealth

stood 93.37%.

Commenting upon the corporate governance practices it is noticed that a diversified

board of directors with wide range of expertise is prevalent in Buzzards Ltd. The boards have

included the diversified expertise that hold each other responsible for offering board duties

with the sufficient time to thoughtfully address the relevant matters for decision making

(Schaltegger & Burritt, 2017). The internal policies highlights that the board collaborates

with the management by making use of their expertise to widen the perspectives and

analysing the decision making. The board also undertakes the evaluation of financial report as

the strategic planning procedure.

The evidences gained from the study suggest that the corporate bylaws include the

description of duties and accountabilities of the vital role. The bylaws clearly outline the

accountabilities and responsibilities for every position of the organization (Warren & Jones

2018). The board members evidently review the reports and perspective in order to expand

the scope for discussion with the expert qualification and diversified board structure. The

company usually implements the organizational policies of good corporate governance,

fairness, accountability and transparency in order to assist the financial growth of the

organization. The structure of corporate governance complies with the organizational policies

of control and offers guidelines that directs the organization in the direction of satisfying the

needs of the stakeholders.

The vertical analysis of the value added statement represents that the wealth created

by the firm in 2009 stood 10530 while in the subsequent year it stood 9832 representing

93.37% creation of wealth. The wealth distribution represents 114.41% among employees’

salaries and wages with 112.79% in finance cost. Overall, the distributed and retained wealth

stood 93.37%.

Commenting upon the corporate governance practices it is noticed that a diversified

board of directors with wide range of expertise is prevalent in Buzzards Ltd. The boards have

included the diversified expertise that hold each other responsible for offering board duties

with the sufficient time to thoughtfully address the relevant matters for decision making

(Schaltegger & Burritt, 2017). The internal policies highlights that the board collaborates

with the management by making use of their expertise to widen the perspectives and

analysing the decision making. The board also undertakes the evaluation of financial report as

the strategic planning procedure.

The evidences gained from the study suggest that the corporate bylaws include the

description of duties and accountabilities of the vital role. The bylaws clearly outline the

accountabilities and responsibilities for every position of the organization (Warren & Jones

2018). The board members evidently review the reports and perspective in order to expand

the scope for discussion with the expert qualification and diversified board structure. The

company usually implements the organizational policies of good corporate governance,

fairness, accountability and transparency in order to assist the financial growth of the

organization. The structure of corporate governance complies with the organizational policies

of control and offers guidelines that directs the organization in the direction of satisfying the

needs of the stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNAL CONTROL

As evident from the current situation, it is noticed that management of the

organization are accountable for the each aspect of its financial health. The management

upholds the responsibilities of understanding the unit’s financial situation and does not allows

unintended deficits to take place (Henderson et al., 2015). The evidences obtained from the

study suggest that the resources are entrusted to them that includes funding, facilities and

staffing even though the board have delegated the accountabilities to their staff.

The budgetary funds are required to spend in compliance with the policy of

organization and operating requirements that meet with the available budgets. Evidences has

been obtained suggest that company does not conducts a separate budget to cover the deficits

(Ge et al., 2014). Therefore, there is a need for alternative resources that should be offered

such as departmental budgets. Buzzards Ltd are accountable for internal financial

management and creating a budgeting financial reporting and management practices becomes

necessary. Simultaneously, organizations are encouraged to create an oversight of procedure

that are based on the best practices.

The financial department of Buzzards Ltd responsibly delegates the management of

the organization the cash flow and makes sure that there are sufficient amount of funds are

available to meet the regular payments (Feng et al., 2014). The accounting policies of the

organization encompasses the credit and collection policies for the customers of company to

make sure that the organization collects its accounts receivable on time. In addition to this,

the accounting policies of Buzzards Ltd ensures that payment policies are in line with the

credit terms of the organization suppliers. The accounting policies accompanies the regular

assessment of cash to determine the needs of the working capital and ongoing cash

requirements.

As evident from the current situation, it is noticed that management of the

organization are accountable for the each aspect of its financial health. The management

upholds the responsibilities of understanding the unit’s financial situation and does not allows

unintended deficits to take place (Henderson et al., 2015). The evidences obtained from the

study suggest that the resources are entrusted to them that includes funding, facilities and

staffing even though the board have delegated the accountabilities to their staff.

The budgetary funds are required to spend in compliance with the policy of

organization and operating requirements that meet with the available budgets. Evidences has

been obtained suggest that company does not conducts a separate budget to cover the deficits

(Ge et al., 2014). Therefore, there is a need for alternative resources that should be offered

such as departmental budgets. Buzzards Ltd are accountable for internal financial

management and creating a budgeting financial reporting and management practices becomes

necessary. Simultaneously, organizations are encouraged to create an oversight of procedure

that are based on the best practices.

The financial department of Buzzards Ltd responsibly delegates the management of

the organization the cash flow and makes sure that there are sufficient amount of funds are

available to meet the regular payments (Feng et al., 2014). The accounting policies of the

organization encompasses the credit and collection policies for the customers of company to

make sure that the organization collects its accounts receivable on time. In addition to this,

the accounting policies of Buzzards Ltd ensures that payment policies are in line with the

credit terms of the organization suppliers. The accounting policies accompanies the regular

assessment of cash to determine the needs of the working capital and ongoing cash

requirements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNAL CONTROL

Answer to Question 5:

Internal controls policies and procedure are regarded as the important process in

ensuring that reliability of accounting are maintained. In the current business world, it

requires accuracy and reliability. Without the correct accounting records managers fail to

undertake correct financial decisions (Vovchenko et al., 2017). Considering the current

financial reports evidences can be drawn by stating that the there is a need for Budgetary

control to regulate the increasing costs. The budgetary planning procedures would help in

formalizing the objectives of the firm.

The budgetary planning for Buzzards is stated below;

The budget assist planning: By formalizing the goals and objective through budget the

business will be able make sure that their plans are attainable. It will enable the managers of

each department to make a decision on what is required to generate the output and goods and

to make sure that everything is available at the right time.

Communication of budget and co-ordination: As the budget is agreed by, the business, all

the necessary managers and staff will be working in the direction of the same end. At the time

of setting the budget any form of expected problems must be resolved and eliminating the

confusion (Ogneva et al., 2014). All the department must be in the position of delegating the

part in attaining the overall objectives.

Implementing monitoring and control through budget: One of the important reason for

implementing budgetary procedure is to produce a budget for the managers that are able to

use the budget as the tool for measuring the actual result from the budgeted results to

determine the budget variances (Feng et al., 2014). As a result of this appropriate actions can

be undertaken to modify the business operations with the passage of time to possibly change

the budget when it becomes attainable.

Answer to Question 5:

Internal controls policies and procedure are regarded as the important process in

ensuring that reliability of accounting are maintained. In the current business world, it

requires accuracy and reliability. Without the correct accounting records managers fail to

undertake correct financial decisions (Vovchenko et al., 2017). Considering the current

financial reports evidences can be drawn by stating that the there is a need for Budgetary

control to regulate the increasing costs. The budgetary planning procedures would help in

formalizing the objectives of the firm.

The budgetary planning for Buzzards is stated below;

The budget assist planning: By formalizing the goals and objective through budget the

business will be able make sure that their plans are attainable. It will enable the managers of

each department to make a decision on what is required to generate the output and goods and

to make sure that everything is available at the right time.

Communication of budget and co-ordination: As the budget is agreed by, the business, all

the necessary managers and staff will be working in the direction of the same end. At the time

of setting the budget any form of expected problems must be resolved and eliminating the

confusion (Ogneva et al., 2014). All the department must be in the position of delegating the

part in attaining the overall objectives.

Implementing monitoring and control through budget: One of the important reason for

implementing budgetary procedure is to produce a budget for the managers that are able to

use the budget as the tool for measuring the actual result from the budgeted results to

determine the budget variances (Feng et al., 2014). As a result of this appropriate actions can

be undertaken to modify the business operations with the passage of time to possibly change

the budget when it becomes attainable.

11INTERNAL CONTROL

Budget as the source of motivating managers: The budget forms the part of the techniques

for motivating the managers and other members of staff to attain the objectives of the

business. The degree to which this will take place is reliant on the agreement and criteria set

and determining whether it is fair or attainable.

Periodic reconciliations: Budgets are subjected to periodic reconciliations that helps in

making sure that the balances in the accounting system matches up with the balances in the

accounting system that are held by the suppliers and credit terms of customers (Ge, et al.,

2014). Discrepancies among the complementary accounts can reveal the error or

discrepancies in their accounts.

Obtaining the authority approval: Needing the specific managers to authorize the certain

types of transactions can add a layer of accountability in the budgetary procedure by making

sure that the transactions have been analysed and approved by the proper authorities.

Budget as the source of motivating managers: The budget forms the part of the techniques

for motivating the managers and other members of staff to attain the objectives of the

business. The degree to which this will take place is reliant on the agreement and criteria set

and determining whether it is fair or attainable.

Periodic reconciliations: Budgets are subjected to periodic reconciliations that helps in

making sure that the balances in the accounting system matches up with the balances in the

accounting system that are held by the suppliers and credit terms of customers (Ge, et al.,

2014). Discrepancies among the complementary accounts can reveal the error or

discrepancies in their accounts.

Obtaining the authority approval: Needing the specific managers to authorize the certain

types of transactions can add a layer of accountability in the budgetary procedure by making

sure that the transactions have been analysed and approved by the proper authorities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.