TCW Audit Report: Analysis of Internal Controls, Risks & Ratios

VerifiedAdded on 2023/06/04

|16

|3363

|263

Report

AI Summary

This report assesses the effectiveness of internal controls for MYH's audit client, TCW, using a case study approach. It examines business risks from both external and internal factors, utilizing ratio analysis to evaluate associated risks in TCW's accounts, particularly concerning purchase and accounts payable. The report identifies strengths and weaknesses within the accounting system, focusing on areas like investment, accounts receivable, marketing expenses, and property assets. Audit risks are assessed through relevant ratios, and internal control weaknesses in accounts payable and purchase accounts are identified and evaluated. The analysis includes identifying internal controls, tests of control, and risk alleviation strategies, such as computer ordering systems, electronic supplier invoices, online payment approvals, and discrepancy resolution processes.

Running Head: AUDITING

Auditing

Name of the University

Name of the Student

Author Note

Auditing

Name of the University

Name of the Student

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Executive Summary

This report is prepared to evaluate the effectiveness of a system of internal control of the

audit clients of MYH. This analysis is done on the basis of evaluation and the facts of the

given case study. This report also uses the business risks that are faced by TCW. It is also

attributable to both external and internal factors. The funding is generated from the

evaluations of the facts that will help in planning an effective system of audit. Ratio analysis

has been used in analysing the risks that are associated in the mentioned accounts of TCW.

Such analysis will effectively help the management structure in identifying the strenghth and

weakness that are associated with different accounting system. These strengths and weakness

are particular in relation to purchase and accounts payable.

Executive Summary

This report is prepared to evaluate the effectiveness of a system of internal control of the

audit clients of MYH. This analysis is done on the basis of evaluation and the facts of the

given case study. This report also uses the business risks that are faced by TCW. It is also

attributable to both external and internal factors. The funding is generated from the

evaluations of the facts that will help in planning an effective system of audit. Ratio analysis

has been used in analysing the risks that are associated in the mentioned accounts of TCW.

Such analysis will effectively help the management structure in identifying the strenghth and

weakness that are associated with different accounting system. These strengths and weakness

are particular in relation to purchase and accounts payable.

2AUDITING

Table of Contents

Introduction................................................................................................................................3

Answer 1A................................................................................................................................3

Answer 1B..................................................................................................................................7

Answer 2A.................................................................................................................................8

Answer 2b................................................................................................................................10

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Answer 1A................................................................................................................................3

Answer 1B..................................................................................................................................7

Answer 2A.................................................................................................................................8

Answer 2b................................................................................................................................10

Conclusion................................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Introduction

This report is prepared to demonstrate the audit risks in relation to the long standing

and significant audit clients of Miller Yates Howarth(MYH) . The client is Trunkey Creek

wines( TCW). Such risks are normally related to the fraud activities. These risks also include

the efforts that are conducted by the auditors themselves(Barta, 2018). The areas for concern

include investment, accounts receivable , marketing expenses and property assets. The

auditor is required to plan the audit engagement .This can be planned by extracting the

information through reviewing the system notes in the permanent file. Also a new internal

control can be applied to manage the risks associated with it(Vovchenk et al., 2017). The

audit risks have been assessed in relation to the specific accounts . This has been done by the

computation of relevant ratios . The second part of the report represents the analysis of the

internal control systems. Also in this report the weaknesses of internal control system has

been assessed. This is mainly related to accounts payable and purchase account s which have

been identified and evaluated in this report.

Answer 1A

The first questions explains the audit risks that are associated with the TCW. It

analyses the ratios such as gearing ratio, profitability ratio , solvency ratio , efficiency ratios

and liquidity ratio. The financial analysis can be analysed effectively by computing the

ratios(Kraft,2014). This helps in assessing the auditors in understanding the financial position

of an organisation. In this particular case study, the evaluation of the accounts associated

with Turnkey Creek wines is determined by computing the relevant ratios. the accounts

relate to property assets, accounts receivable, marketing expenses and investment. According

to the case study the audit planning indicates that the audit would face numerous material

misstatements while assessing. Due to this the auditors have been burdened by the

Introduction

This report is prepared to demonstrate the audit risks in relation to the long standing

and significant audit clients of Miller Yates Howarth(MYH) . The client is Trunkey Creek

wines( TCW). Such risks are normally related to the fraud activities. These risks also include

the efforts that are conducted by the auditors themselves(Barta, 2018). The areas for concern

include investment, accounts receivable , marketing expenses and property assets. The

auditor is required to plan the audit engagement .This can be planned by extracting the

information through reviewing the system notes in the permanent file. Also a new internal

control can be applied to manage the risks associated with it(Vovchenk et al., 2017). The

audit risks have been assessed in relation to the specific accounts . This has been done by the

computation of relevant ratios . The second part of the report represents the analysis of the

internal control systems. Also in this report the weaknesses of internal control system has

been assessed. This is mainly related to accounts payable and purchase account s which have

been identified and evaluated in this report.

Answer 1A

The first questions explains the audit risks that are associated with the TCW. It

analyses the ratios such as gearing ratio, profitability ratio , solvency ratio , efficiency ratios

and liquidity ratio. The financial analysis can be analysed effectively by computing the

ratios(Kraft,2014). This helps in assessing the auditors in understanding the financial position

of an organisation. In this particular case study, the evaluation of the accounts associated

with Turnkey Creek wines is determined by computing the relevant ratios. the accounts

relate to property assets, accounts receivable, marketing expenses and investment. According

to the case study the audit planning indicates that the audit would face numerous material

misstatements while assessing. Due to this the auditors have been burdened by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

responsibility of identifying such risks. These steps help in reducing such risks. The

implementation of effective internal control would help in reducing the fraud related

risk(Tayeh, Al-Jarrah & Tarhini, 2015). The auditor needs to exercise reasonable care and

skill and maintain professional scepticism while conducting the audit. The following table

contains a list of ratios that have been analysed

Ratio Table

Ratio Unaudited (2018) Audited (2017) Audited (2016)

Return on equity 10.80 17.5 15.2

Return on beef

production assets

1.67 -0.82 -3.45

Return on grapes and

wine production

assets

12.2 14.5 16.2

Gross margin 24.5 30 31.76

Net profit margin 14.38 20.27 17.85

Marketing expense 23.67 17.89 15.2

Days in inventory to

wine

367 423 53.24

Current ratio 2.8 2.54 2.66

Quick ratio 1.18 1.15 1.2

Debt to equity ratio 0.54 0.63 0.67

responsibility of identifying such risks. These steps help in reducing such risks. The

implementation of effective internal control would help in reducing the fraud related

risk(Tayeh, Al-Jarrah & Tarhini, 2015). The auditor needs to exercise reasonable care and

skill and maintain professional scepticism while conducting the audit. The following table

contains a list of ratios that have been analysed

Ratio Table

Ratio Unaudited (2018) Audited (2017) Audited (2016)

Return on equity 10.80 17.5 15.2

Return on beef

production assets

1.67 -0.82 -3.45

Return on grapes and

wine production

assets

12.2 14.5 16.2

Gross margin 24.5 30 31.76

Net profit margin 14.38 20.27 17.85

Marketing expense 23.67 17.89 15.2

Days in inventory to

wine

367 423 53.24

Current ratio 2.8 2.54 2.66

Quick ratio 1.18 1.15 1.2

Debt to equity ratio 0.54 0.63 0.67

5AUDITING

Account receivable

Analysis – Accounts receivable is the amount that is due to be paid by thr clients of TCW to

the company. the accounts receivable ratio is evaluated for assessing the financial condition

of the company.( Ngugi, Gakure & Gekara, 2017). From the table it can be seen that the days

in accounts receivables for wine and beef is recorded at 60,65 and 36 respectively. However

in the following year this value has been reduced for beef. This indicates that the time taken

to make the payment by debtors has increased in case of wine as against beef.

Audit risk- On the basis of this case study, the majority of producers by TCW is done on a

credit system. This system attaches a huge amount of risks in the payment made by the

customers. Thus a risk of completeness exists. This represents the risks of firms relating to

the validity. The risk of completeness that exists is the accounts might not file documentation

or file the documents in a correct manner(Barta,2018).

Audit steps to reduce the risk- The accounts receivables days that are increasing should be

viewed and simultaneously discussed with the management. The approval of upper level

management is required to allow the provision of doubtful debts. The process of credit

approval should be reviewed.

Property assets

Analysis- The investment scenario of TCW can be calculated by computing the ratios that

identifies the number of times that the firms are earning compared to the investment made by

the firm. From the table it can be seen that there is an increase in equity return for the audited

financial statements(Long, Chan & Wen-de, 2017). Also it is observed that the return on beef

production of assets has improved. The return on wine and grape production of assets has

improved in the year 2017.

Account receivable

Analysis – Accounts receivable is the amount that is due to be paid by thr clients of TCW to

the company. the accounts receivable ratio is evaluated for assessing the financial condition

of the company.( Ngugi, Gakure & Gekara, 2017). From the table it can be seen that the days

in accounts receivables for wine and beef is recorded at 60,65 and 36 respectively. However

in the following year this value has been reduced for beef. This indicates that the time taken

to make the payment by debtors has increased in case of wine as against beef.

Audit risk- On the basis of this case study, the majority of producers by TCW is done on a

credit system. This system attaches a huge amount of risks in the payment made by the

customers. Thus a risk of completeness exists. This represents the risks of firms relating to

the validity. The risk of completeness that exists is the accounts might not file documentation

or file the documents in a correct manner(Barta,2018).

Audit steps to reduce the risk- The accounts receivables days that are increasing should be

viewed and simultaneously discussed with the management. The approval of upper level

management is required to allow the provision of doubtful debts. The process of credit

approval should be reviewed.

Property assets

Analysis- The investment scenario of TCW can be calculated by computing the ratios that

identifies the number of times that the firms are earning compared to the investment made by

the firm. From the table it can be seen that there is an increase in equity return for the audited

financial statements(Long, Chan & Wen-de, 2017). Also it is observed that the return on beef

production of assets has improved. The return on wine and grape production of assets has

improved in the year 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

Audit risk- There are risks related to recording the asset and registering the property assets .

The audit risks associated with this include depreciation charging method. This is recorded by

the accountant and the documentation might not be appropriate. there also can be an incorrect

valuation of the assets. Further there may be incorrect recording of entries which are hidden

in complex structures(Barta,2018).

Audit steps to reduce the risks- The auditor is required to make an assessment of the

effectiveness of the system of internal control. The depreciation should be analysed for

judging the consistency of the method. The relevant ledgers and journals of property assets

should be monitored. In order to determine the existence of the assets, the auditor should

review the acquisition documents.

Investments

Analysis- The investment effectiveness of an organisation can be measured in relation to the

number of times that the company earns in relation to the particular investment(Lee & Lee,

2015). From the table it can be seen that the time earned interest of TCW has declined. It has

declined from 8.1 in the year 2016 compared to the 2017 year when it was 7.5

Audit risk- The financers is required to spend the investment in a planned manner,

considering the level of risks associated on the investment is high. The working capital

would be impacted by the amount of risks that is associated with the investment made.

Audit steps to reduce risk- The auditor is required to make the assessment in realtion to the

investment made by TCW. He is also required to assess whether there has been an unusual

investment done by the company. It should be carefully monitored by the management.

Marketing expenses

Audit risk- There are risks related to recording the asset and registering the property assets .

The audit risks associated with this include depreciation charging method. This is recorded by

the accountant and the documentation might not be appropriate. there also can be an incorrect

valuation of the assets. Further there may be incorrect recording of entries which are hidden

in complex structures(Barta,2018).

Audit steps to reduce the risks- The auditor is required to make an assessment of the

effectiveness of the system of internal control. The depreciation should be analysed for

judging the consistency of the method. The relevant ledgers and journals of property assets

should be monitored. In order to determine the existence of the assets, the auditor should

review the acquisition documents.

Investments

Analysis- The investment effectiveness of an organisation can be measured in relation to the

number of times that the company earns in relation to the particular investment(Lee & Lee,

2015). From the table it can be seen that the time earned interest of TCW has declined. It has

declined from 8.1 in the year 2016 compared to the 2017 year when it was 7.5

Audit risk- The financers is required to spend the investment in a planned manner,

considering the level of risks associated on the investment is high. The working capital

would be impacted by the amount of risks that is associated with the investment made.

Audit steps to reduce risk- The auditor is required to make the assessment in realtion to the

investment made by TCW. He is also required to assess whether there has been an unusual

investment done by the company. It should be carefully monitored by the management.

Marketing expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

Analysis-The marketing expenses is expressed as a portion of total expenses. Such a ratio

has increased from 15.2 in year 2016 to 17.89 in the year 2017. Such an increase in

percentage indicates the fact that the marketing expenses has increased in the current year.

Audit risk-There was a lack of disclosures of the related third parties transactions and the

data. Such data relates to activities that might change the perception of the stakeholders.

Audit steps to reduce the risk-The auditor is required to evaluate the marketing activities and

then record them. The expenses of all marketing activities need to be properly reviewed in an

analytical fashion(Olefirenko, 2016)..

Answer 1B

Business risks are those kinds of risks that are associated with the fact that there could

be a negative variation on the expected profit or losses of nay business. There are a variety of

factors that impact the business risks of a company(Kozubíková et al., 2014). Through this

case study t can be analysed that the earnings of TCW have been steady for a number of

years.The capacity of the TCW to fulfil its objectives might be susceptible by both external

and internal factors

Return on wine and grape production assets- the total amount of return that s generated

from the production of wine and beef has been reducing consistently. The return on the

production of such items has declined to 14,5 in 2106 compared to 16.2 in 2015. Such a fall

illustrates that the assets have not been efficiently utilised for production purpose

Debt to equity ratio- this ratio is improving. This means that the proportion of debt that is

held by the company in relation to the assets has reduced in 2017 compared to 2016. The

ratio has reduced from 0.67 to 0.63. This indicates that the financial leverage as declined and

hence the business risk has also lowered(Enekwe, Agu & Eziedo,2014).

Analysis-The marketing expenses is expressed as a portion of total expenses. Such a ratio

has increased from 15.2 in year 2016 to 17.89 in the year 2017. Such an increase in

percentage indicates the fact that the marketing expenses has increased in the current year.

Audit risk-There was a lack of disclosures of the related third parties transactions and the

data. Such data relates to activities that might change the perception of the stakeholders.

Audit steps to reduce the risk-The auditor is required to evaluate the marketing activities and

then record them. The expenses of all marketing activities need to be properly reviewed in an

analytical fashion(Olefirenko, 2016)..

Answer 1B

Business risks are those kinds of risks that are associated with the fact that there could

be a negative variation on the expected profit or losses of nay business. There are a variety of

factors that impact the business risks of a company(Kozubíková et al., 2014). Through this

case study t can be analysed that the earnings of TCW have been steady for a number of

years.The capacity of the TCW to fulfil its objectives might be susceptible by both external

and internal factors

Return on wine and grape production assets- the total amount of return that s generated

from the production of wine and beef has been reducing consistently. The return on the

production of such items has declined to 14,5 in 2106 compared to 16.2 in 2015. Such a fall

illustrates that the assets have not been efficiently utilised for production purpose

Debt to equity ratio- this ratio is improving. This means that the proportion of debt that is

held by the company in relation to the assets has reduced in 2017 compared to 2016. The

ratio has reduced from 0.67 to 0.63. This indicates that the financial leverage as declined and

hence the business risk has also lowered(Enekwe, Agu & Eziedo,2014).

8AUDITING

Days in accounts receivables beef- From the table it can be seen that there has been an

increase in the accounts receivable days of beef. The days has increased from 24 in year

2016 to 36 in year 2017 with a further increase in year 2018 to 57. This suggests that the time

taken by TCW to recover money from customers has increased significantly.

Gross margin- the gross margin of TCW declined in 2017 from 2016. It declined from 31.76

to 30. Such a fall would make the firm very difficult in retaining a higher percent of sales.

Time interest earned- The interest coverage ratio illustrates the total amount of times that it

takes for the firm to repay its assets.From the table, it can be seen that the interest coverage

ratio is less than one. This indicates that the operating profit cannot generate sufficient cash

so that it can make payments or carry out other operating activities(Tucker, et al., 2016).

Answer 2A

In this section, the internal controls have been identified along with the test o control

for each identified control systems . The following paragraphs makes a list of the

identification of internal control system , test of control and risk alleviated

Risk alleviated

Effective control Risk alleviated Test of control

Computer ordering system This would help in

generating complete records

without any data missing. To

access the program, there

needs to be a password. All

these would help in

mitigating fraud risks(Chan

& Vasarhelyi, 2018)

Auditors must take notice of

the prepaartoin of deposits

and the mail openings of

employees. There should be

sample of resistance that

should be selected. This

sample should be selected for

tracing the recording of

Days in accounts receivables beef- From the table it can be seen that there has been an

increase in the accounts receivable days of beef. The days has increased from 24 in year

2016 to 36 in year 2017 with a further increase in year 2018 to 57. This suggests that the time

taken by TCW to recover money from customers has increased significantly.

Gross margin- the gross margin of TCW declined in 2017 from 2016. It declined from 31.76

to 30. Such a fall would make the firm very difficult in retaining a higher percent of sales.

Time interest earned- The interest coverage ratio illustrates the total amount of times that it

takes for the firm to repay its assets.From the table, it can be seen that the interest coverage

ratio is less than one. This indicates that the operating profit cannot generate sufficient cash

so that it can make payments or carry out other operating activities(Tucker, et al., 2016).

Answer 2A

In this section, the internal controls have been identified along with the test o control

for each identified control systems . The following paragraphs makes a list of the

identification of internal control system , test of control and risk alleviated

Risk alleviated

Effective control Risk alleviated Test of control

Computer ordering system This would help in

generating complete records

without any data missing. To

access the program, there

needs to be a password. All

these would help in

mitigating fraud risks(Chan

& Vasarhelyi, 2018)

Auditors must take notice of

the prepaartoin of deposits

and the mail openings of

employees. There should be

sample of resistance that

should be selected. This

sample should be selected for

tracing the recording of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

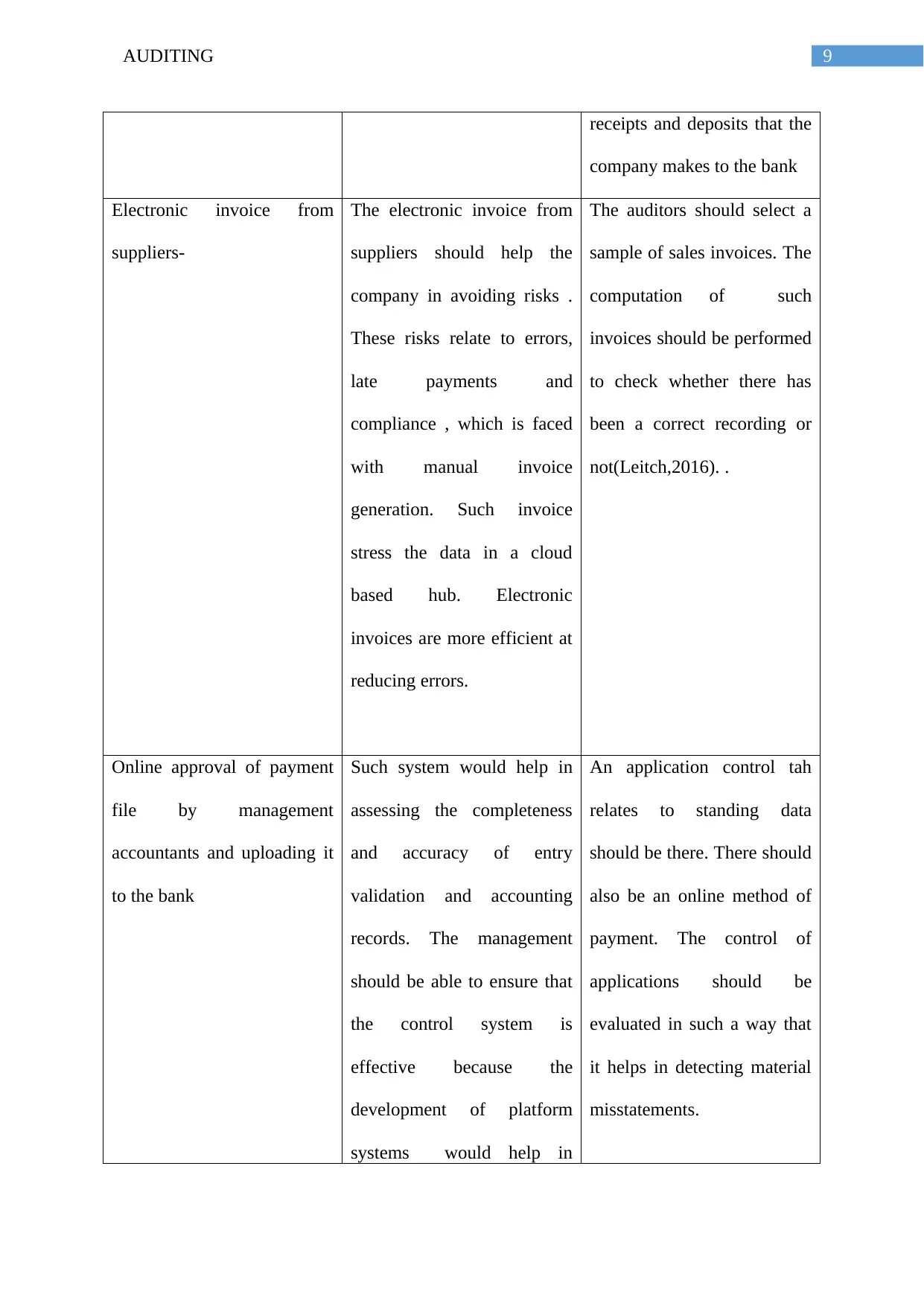

9AUDITING

receipts and deposits that the

company makes to the bank

Electronic invoice from

suppliers-

The electronic invoice from

suppliers should help the

company in avoiding risks .

These risks relate to errors,

late payments and

compliance , which is faced

with manual invoice

generation. Such invoice

stress the data in a cloud

based hub. Electronic

invoices are more efficient at

reducing errors.

The auditors should select a

sample of sales invoices. The

computation of such

invoices should be performed

to check whether there has

been a correct recording or

not(Leitch,2016). .

Online approval of payment

file by management

accountants and uploading it

to the bank

Such system would help in

assessing the completeness

and accuracy of entry

validation and accounting

records. The management

should be able to ensure that

the control system is

effective because the

development of platform

systems would help in

An application control tah

relates to standing data

should be there. There should

also be an online method of

payment. The control of

applications should be

evaluated in such a way that

it helps in detecting material

misstatements.

receipts and deposits that the

company makes to the bank

Electronic invoice from

suppliers-

The electronic invoice from

suppliers should help the

company in avoiding risks .

These risks relate to errors,

late payments and

compliance , which is faced

with manual invoice

generation. Such invoice

stress the data in a cloud

based hub. Electronic

invoices are more efficient at

reducing errors.

The auditors should select a

sample of sales invoices. The

computation of such

invoices should be performed

to check whether there has

been a correct recording or

not(Leitch,2016). .

Online approval of payment

file by management

accountants and uploading it

to the bank

Such system would help in

assessing the completeness

and accuracy of entry

validation and accounting

records. The management

should be able to ensure that

the control system is

effective because the

development of platform

systems would help in

An application control tah

relates to standing data

should be there. There should

also be an online method of

payment. The control of

applications should be

evaluated in such a way that

it helps in detecting material

misstatements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

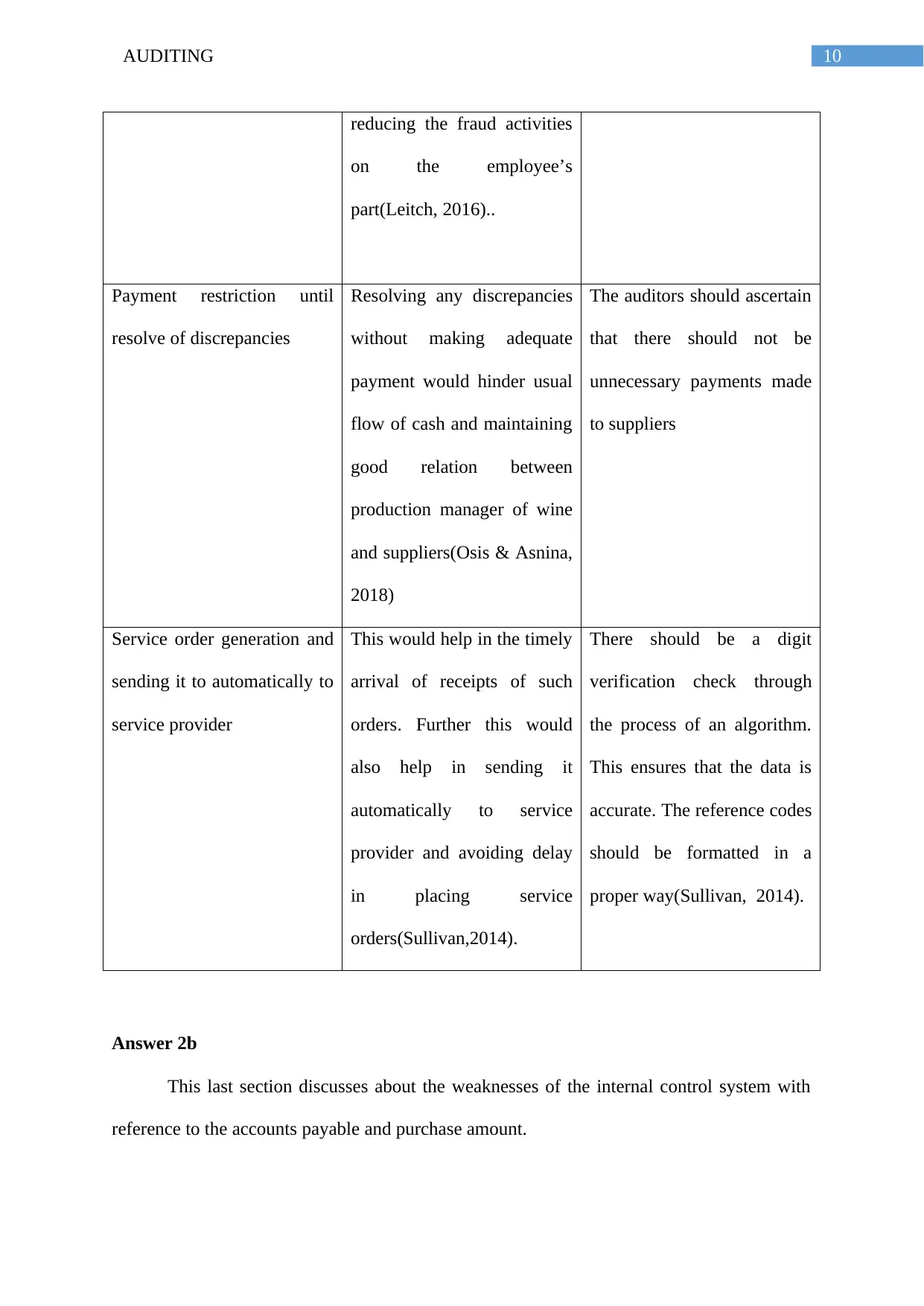

10AUDITING

reducing the fraud activities

on the employee’s

part(Leitch, 2016)..

Payment restriction until

resolve of discrepancies

Resolving any discrepancies

without making adequate

payment would hinder usual

flow of cash and maintaining

good relation between

production manager of wine

and suppliers(Osis & Asnina,

2018)

The auditors should ascertain

that there should not be

unnecessary payments made

to suppliers

Service order generation and

sending it to automatically to

service provider

This would help in the timely

arrival of receipts of such

orders. Further this would

also help in sending it

automatically to service

provider and avoiding delay

in placing service

orders(Sullivan,2014).

There should be a digit

verification check through

the process of an algorithm.

This ensures that the data is

accurate. The reference codes

should be formatted in a

proper way(Sullivan, 2014).

Answer 2b

This last section discusses about the weaknesses of the internal control system with

reference to the accounts payable and purchase amount.

reducing the fraud activities

on the employee’s

part(Leitch, 2016)..

Payment restriction until

resolve of discrepancies

Resolving any discrepancies

without making adequate

payment would hinder usual

flow of cash and maintaining

good relation between

production manager of wine

and suppliers(Osis & Asnina,

2018)

The auditors should ascertain

that there should not be

unnecessary payments made

to suppliers

Service order generation and

sending it to automatically to

service provider

This would help in the timely

arrival of receipts of such

orders. Further this would

also help in sending it

automatically to service

provider and avoiding delay

in placing service

orders(Sullivan,2014).

There should be a digit

verification check through

the process of an algorithm.

This ensures that the data is

accurate. The reference codes

should be formatted in a

proper way(Sullivan, 2014).

Answer 2b

This last section discusses about the weaknesses of the internal control system with

reference to the accounts payable and purchase amount.

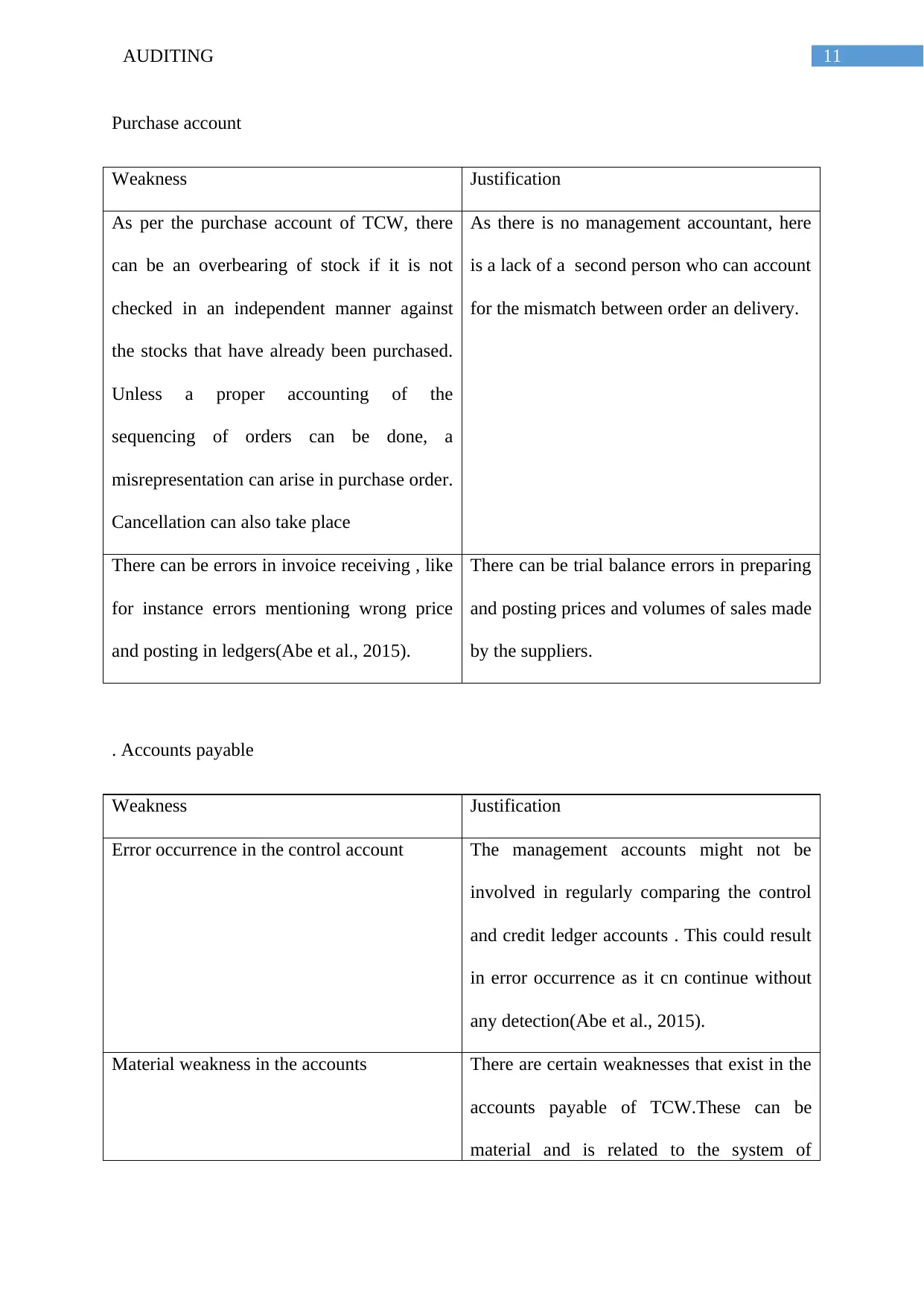

11AUDITING

Purchase account

Weakness Justification

As per the purchase account of TCW, there

can be an overbearing of stock if it is not

checked in an independent manner against

the stocks that have already been purchased.

Unless a proper accounting of the

sequencing of orders can be done, a

misrepresentation can arise in purchase order.

Cancellation can also take place

As there is no management accountant, here

is a lack of a second person who can account

for the mismatch between order an delivery.

There can be errors in invoice receiving , like

for instance errors mentioning wrong price

and posting in ledgers(Abe et al., 2015).

There can be trial balance errors in preparing

and posting prices and volumes of sales made

by the suppliers.

. Accounts payable

Weakness Justification

Error occurrence in the control account The management accounts might not be

involved in regularly comparing the control

and credit ledger accounts . This could result

in error occurrence as it cn continue without

any detection(Abe et al., 2015).

Material weakness in the accounts There are certain weaknesses that exist in the

accounts payable of TCW.These can be

material and is related to the system of

Purchase account

Weakness Justification

As per the purchase account of TCW, there

can be an overbearing of stock if it is not

checked in an independent manner against

the stocks that have already been purchased.

Unless a proper accounting of the

sequencing of orders can be done, a

misrepresentation can arise in purchase order.

Cancellation can also take place

As there is no management accountant, here

is a lack of a second person who can account

for the mismatch between order an delivery.

There can be errors in invoice receiving , like

for instance errors mentioning wrong price

and posting in ledgers(Abe et al., 2015).

There can be trial balance errors in preparing

and posting prices and volumes of sales made

by the suppliers.

. Accounts payable

Weakness Justification

Error occurrence in the control account The management accounts might not be

involved in regularly comparing the control

and credit ledger accounts . This could result

in error occurrence as it cn continue without

any detection(Abe et al., 2015).

Material weakness in the accounts There are certain weaknesses that exist in the

accounts payable of TCW.These can be

material and is related to the system of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.