Comprehensive Report on Internal Control in Accounting Systems

VerifiedAdded on 2021/06/14

|8

|1169

|213

Report

AI Summary

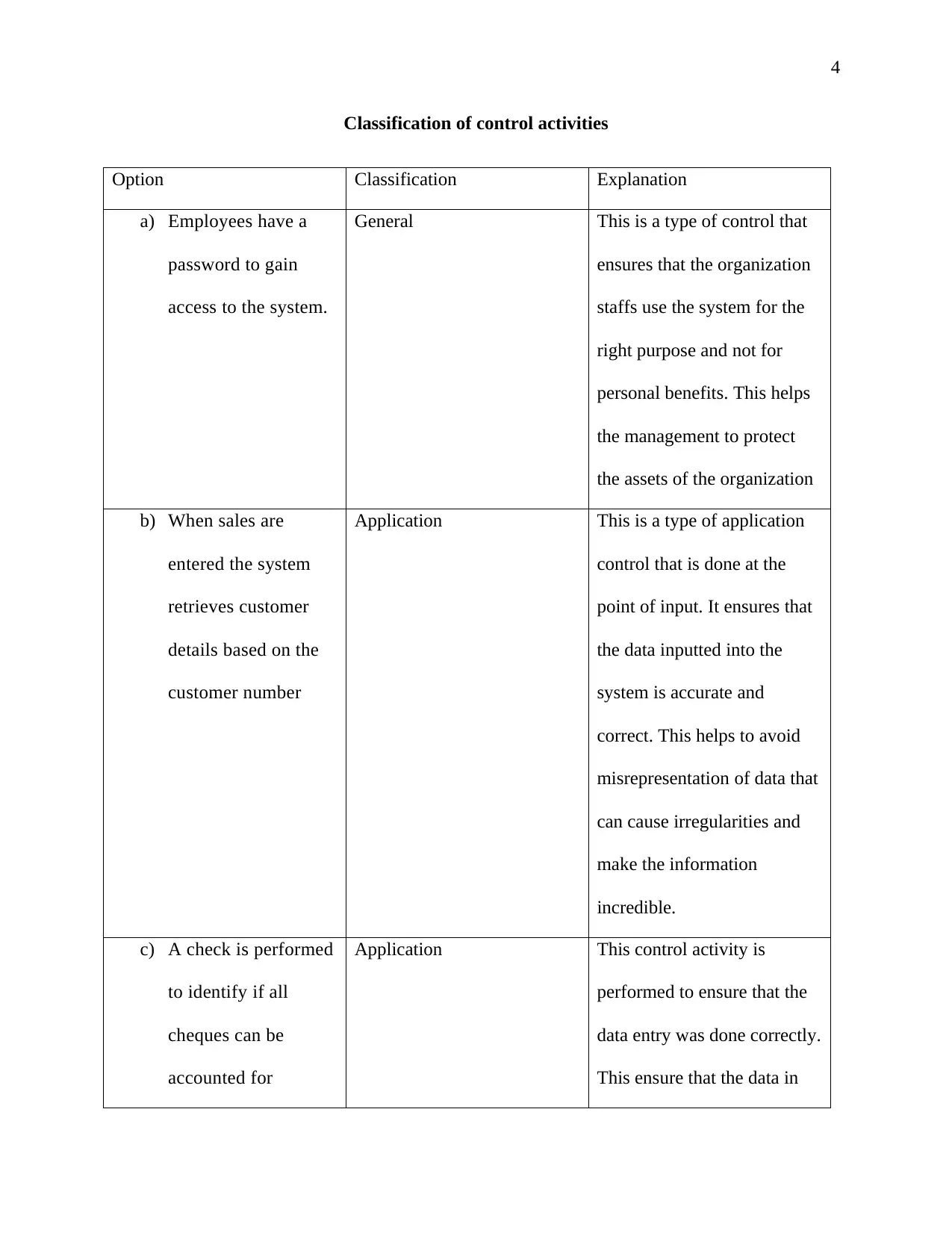

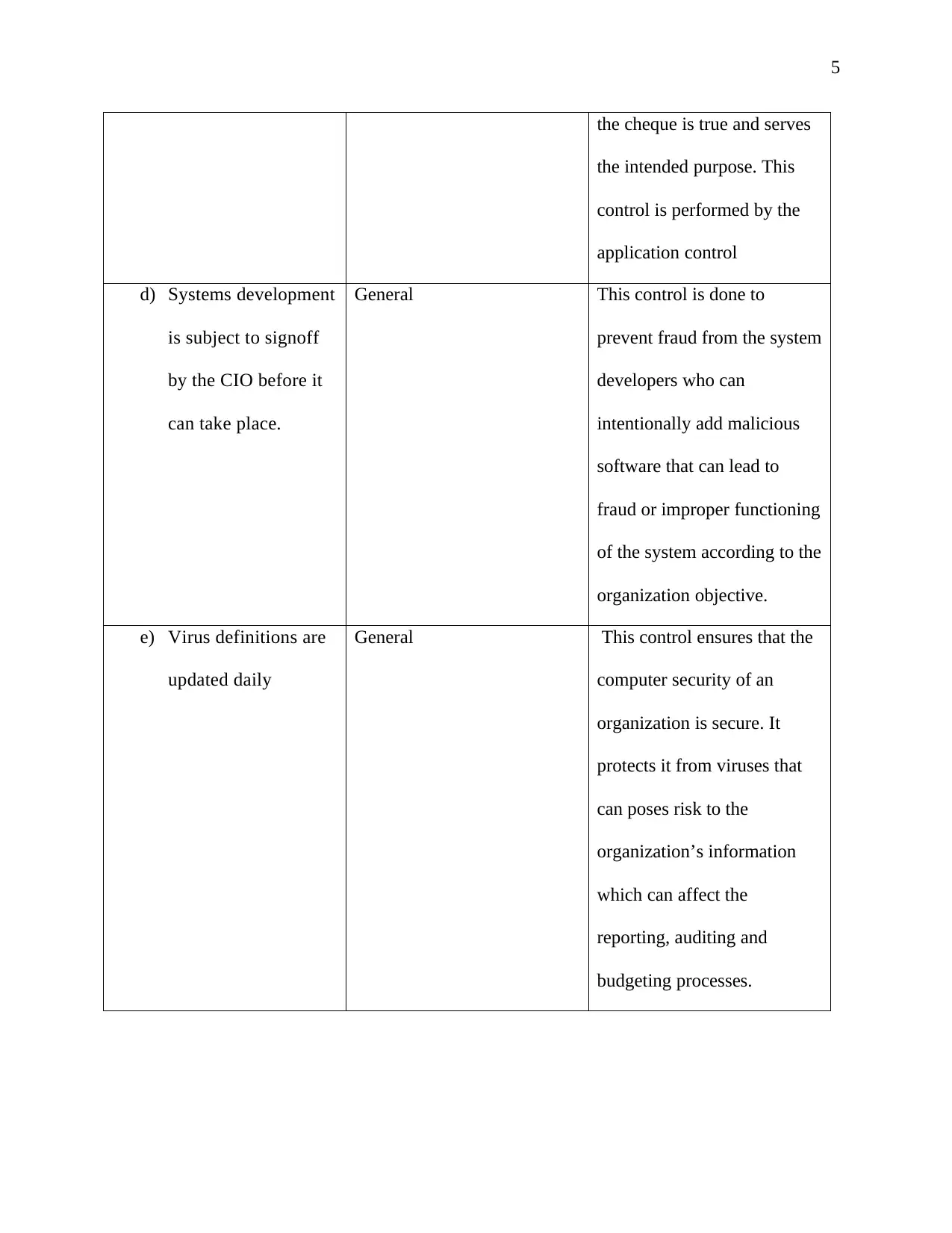

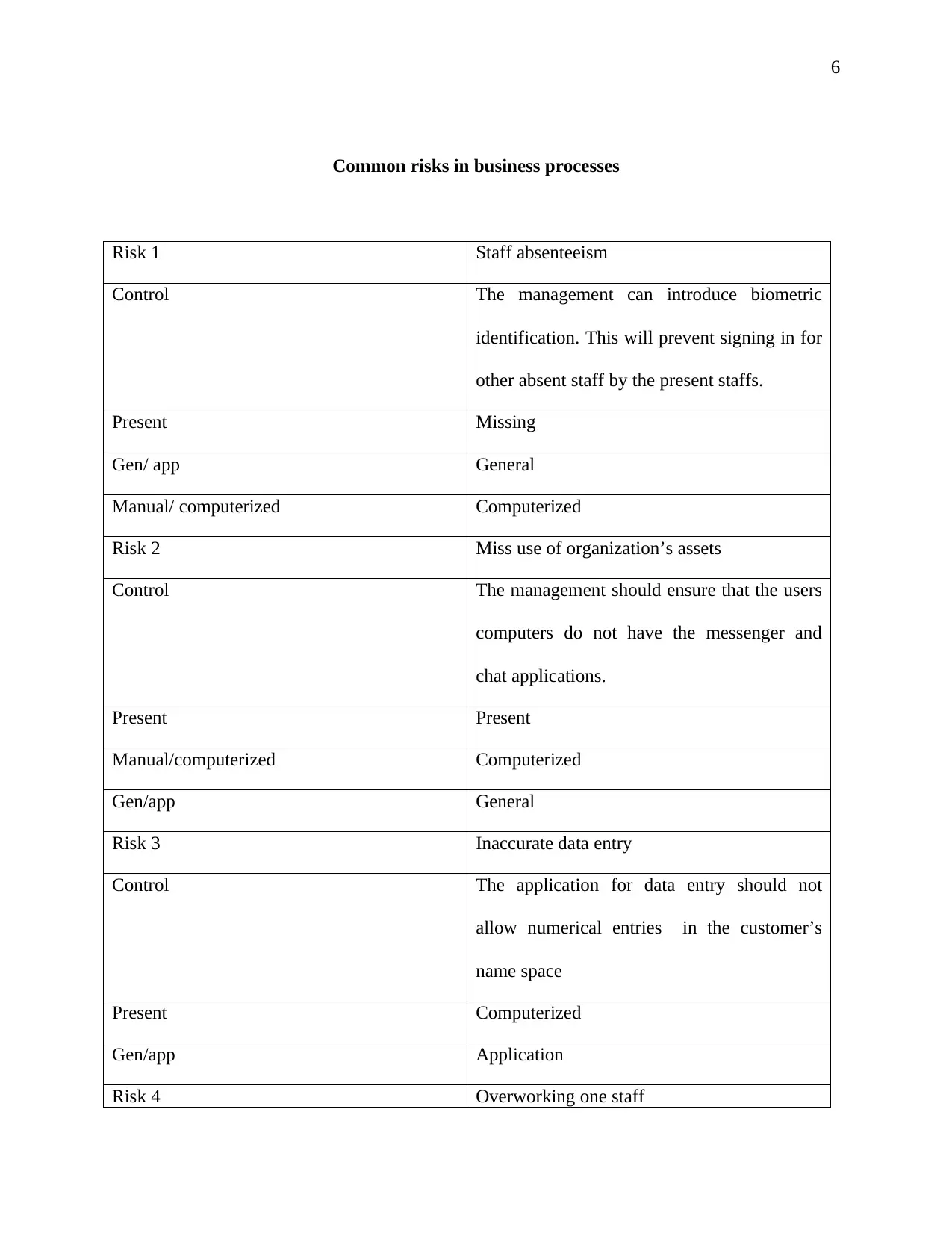

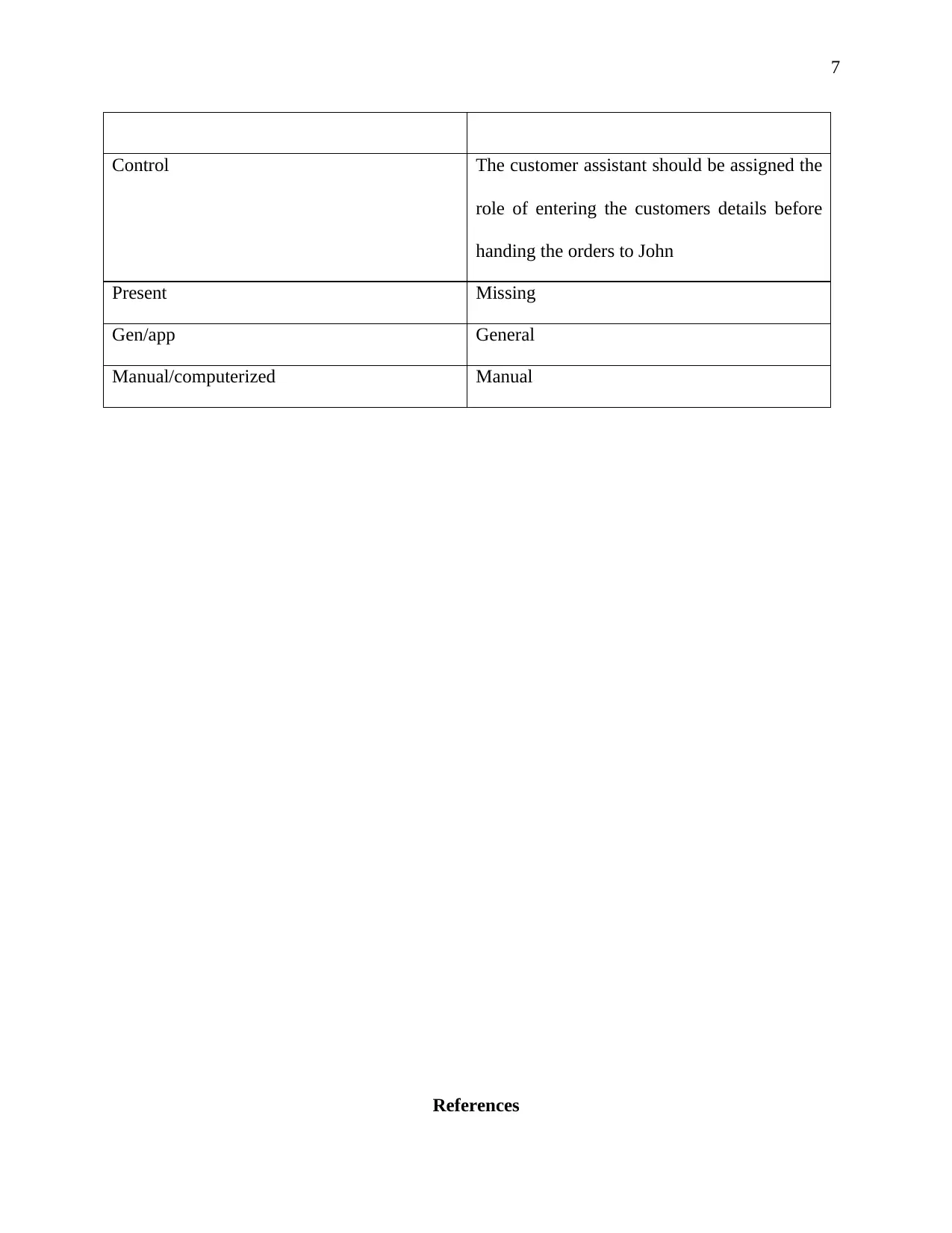

This report examines internal control within organizations, focusing on accounting information systems and their importance in ensuring accurate financial data storage, as highlighted by Hall (2012). It defines internal control as a process ensuring operational efficiency, reliable financial reporting, and compliance with regulations, as described by Brett et al. (2012). The report details the five components of internal control: control environment, risk assessment, information and communication, control activities, and monitoring. It explores how these components, as discussed by Hilton and Plitt (2013), contribute to achieving organizational objectives and mitigating risks, as noted by Malmi and Brown (2008). The report also classifies various control activities, such as general and application controls, using examples like password protection and data validation. It identifies common business process risks, including staff absenteeism, asset misuse, and inaccurate data entry, along with potential control measures. The report references key academic sources, including Doyle and McVay (2007) and Sajady et al. (2012), to support its analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.