Internal Control Weaknesses in Sales Process of Buck Phyz

VerifiedAdded on 2024/04/25

|13

|2861

|75

AI Summary

This report analyzes the internal control weaknesses in the sales process of Buck Phyz, suggesting improvements and discussing the implementation of corporate credit cards. Recommendations include enhancing communication channels, tightening security measures, and issuing corporate credit cards to key personnel.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting Information System

Student’s Name:

Student’s ID:

1

Student’s Name:

Student’s ID:

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Executive summary....................................................................................................................3

Introduction................................................................................................................................4

Q1. Overview of the sales process.............................................................................................5

Q2. Internal control weaknesses and their impact on Buck Phyz..............................................6

Q3. Corporate credit card.........................................................................................................10

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

2

Executive summary....................................................................................................................3

Introduction................................................................................................................................4

Q1. Overview of the sales process.............................................................................................5

Q2. Internal control weaknesses and their impact on Buck Phyz..............................................6

Q3. Corporate credit card.........................................................................................................10

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

2

Executive summary:

The following report consists detailed analysis of the internal weaknesses of sales process of

Buck Phyz. Buck Phyz has been facing various structural changes and this report is formed

for investigating the issues in the sales process. The sales process is vital to the organization

as it leads to revenues generation and profits for the organization. Buck Phyz has a hierarchy

which includes CEO, FD and under the FD, there is AR manager, head of sales and financial

accountant. Sales processes mainly include AR, MD specialists, and sales managers. Sales

managers are responsible for making ultimate’s sales and then further reconcile the details of

creditworthiness and payments mechanism with the AR department. Sales managers

formulate legal contracts for clients which are approved by Finance director or head of sales.

The company has faced various internal weaknesses such as improper communication across

different segments, low-security channels/ policies, weak measures for rescuing from credit

losses. This report has made possible suggestions which can be implemented for improving

the weaknesses such as inducing meetings, attachment of client’s personal wealth with the

contracts, clear verification of potential customer before approving for sales. A corporate

credit card is also another important concept discussed over here. Buck Phyz employees face

issue while making business-related expenses such as the purchase of training course. There

are possible solutions such as the issuance of CCC can aid employee to make direct payment

and an effective audit trail can check for possible fraud detection or misleading activities.

3

The following report consists detailed analysis of the internal weaknesses of sales process of

Buck Phyz. Buck Phyz has been facing various structural changes and this report is formed

for investigating the issues in the sales process. The sales process is vital to the organization

as it leads to revenues generation and profits for the organization. Buck Phyz has a hierarchy

which includes CEO, FD and under the FD, there is AR manager, head of sales and financial

accountant. Sales processes mainly include AR, MD specialists, and sales managers. Sales

managers are responsible for making ultimate’s sales and then further reconcile the details of

creditworthiness and payments mechanism with the AR department. Sales managers

formulate legal contracts for clients which are approved by Finance director or head of sales.

The company has faced various internal weaknesses such as improper communication across

different segments, low-security channels/ policies, weak measures for rescuing from credit

losses. This report has made possible suggestions which can be implemented for improving

the weaknesses such as inducing meetings, attachment of client’s personal wealth with the

contracts, clear verification of potential customer before approving for sales. A corporate

credit card is also another important concept discussed over here. Buck Phyz employees face

issue while making business-related expenses such as the purchase of training course. There

are possible solutions such as the issuance of CCC can aid employee to make direct payment

and an effective audit trail can check for possible fraud detection or misleading activities.

3

Introduction:

The sales process of Buck Phyz includes sales managers who sales their offers to potential

customers. Sales managers receive commissions on every customer's invoice (not on credit

notes) generated. Sales contracts are formed, cross-verified for creditworthiness, for database

installation by MD managers and AR managers makes day to day reconciliation of payments.

Internal control systems are integral to the organization for finding any form of fraudulent

accounting activities taking place in the organization. For accounting internal control, the

responsibility lies with finance director and Accounts receivable manager, who head a team

of three AR specialized persons. AR manager, in consultation with FD, overview the ledgers

of, credit customers, whose balance are opened and decides upon immediate actions. Bucks

Phyz is facing issues with payments of small expenditures which are essential and hence,

employees have to make payments by themselves. Corporate credit cards can be an effective

solution to the issue.

4

The sales process of Buck Phyz includes sales managers who sales their offers to potential

customers. Sales managers receive commissions on every customer's invoice (not on credit

notes) generated. Sales contracts are formed, cross-verified for creditworthiness, for database

installation by MD managers and AR managers makes day to day reconciliation of payments.

Internal control systems are integral to the organization for finding any form of fraudulent

accounting activities taking place in the organization. For accounting internal control, the

responsibility lies with finance director and Accounts receivable manager, who head a team

of three AR specialized persons. AR manager, in consultation with FD, overview the ledgers

of, credit customers, whose balance are opened and decides upon immediate actions. Bucks

Phyz is facing issues with payments of small expenditures which are essential and hence,

employees have to make payments by themselves. Corporate credit cards can be an effective

solution to the issue.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Q1. Overview of the sales process:

In Buck Phyz, sales process includes finance director, AR department (MD and AR), and

sales department. Sales are channelized through sales team which includes “Head of sales”

and other five sales managers. The Head of sales reports its team status to finance director of

the company. The five sales manager constitute their offers to their potential customers,

persuade them, consider their request and makes sales. Further, during the contract

negotiation, sales manager sends an email to AR for examining the creditworthiness. It must

be between AAA to C for availing credit otherwise another method of payments is checked

for. They further formulate the legal contract detailing terms and conditions which have to be

signed by either FD or Head of sales. But it is not properly followed due to time constraint.

MD department fills up customer details in ERP system and makes necessary billing system

which are reconciled and contacted by AR managers.

5

In Buck Phyz, sales process includes finance director, AR department (MD and AR), and

sales department. Sales are channelized through sales team which includes “Head of sales”

and other five sales managers. The Head of sales reports its team status to finance director of

the company. The five sales manager constitute their offers to their potential customers,

persuade them, consider their request and makes sales. Further, during the contract

negotiation, sales manager sends an email to AR for examining the creditworthiness. It must

be between AAA to C for availing credit otherwise another method of payments is checked

for. They further formulate the legal contract detailing terms and conditions which have to be

signed by either FD or Head of sales. But it is not properly followed due to time constraint.

MD department fills up customer details in ERP system and makes necessary billing system

which are reconciled and contacted by AR managers.

5

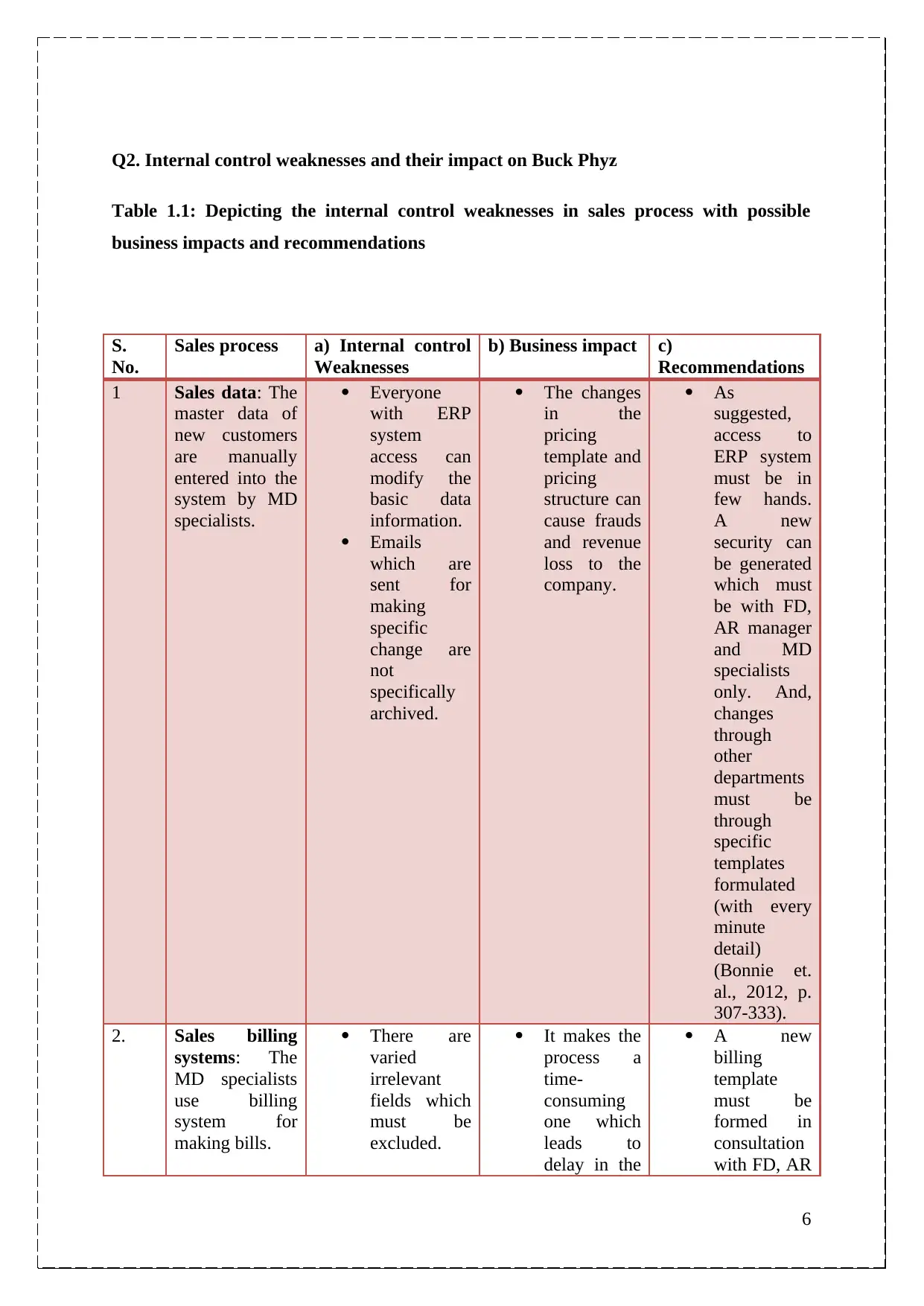

Q2. Internal control weaknesses and their impact on Buck Phyz

Table 1.1: Depicting the internal control weaknesses in sales process with possible

business impacts and recommendations

S.

No.

Sales process a) Internal control

Weaknesses

b) Business impact c)

Recommendations

1 Sales data: The

master data of

new customers

are manually

entered into the

system by MD

specialists.

Everyone

with ERP

system

access can

modify the

basic data

information.

Emails

which are

sent for

making

specific

change are

not

specifically

archived.

The changes

in the

pricing

template and

pricing

structure can

cause frauds

and revenue

loss to the

company.

As

suggested,

access to

ERP system

must be in

few hands.

A new

security can

be generated

which must

be with FD,

AR manager

and MD

specialists

only. And,

changes

through

other

departments

must be

through

specific

templates

formulated

(with every

minute

detail)

(Bonnie et.

al., 2012, p.

307-333).

2. Sales billing

systems: The

MD specialists

use billing

system for

making bills.

There are

varied

irrelevant

fields which

must be

excluded.

It makes the

process a

time-

consuming

one which

leads to

delay in the

A new

billing

template

must be

formed in

consultation

with FD, AR

6

Table 1.1: Depicting the internal control weaknesses in sales process with possible

business impacts and recommendations

S.

No.

Sales process a) Internal control

Weaknesses

b) Business impact c)

Recommendations

1 Sales data: The

master data of

new customers

are manually

entered into the

system by MD

specialists.

Everyone

with ERP

system

access can

modify the

basic data

information.

Emails

which are

sent for

making

specific

change are

not

specifically

archived.

The changes

in the

pricing

template and

pricing

structure can

cause frauds

and revenue

loss to the

company.

As

suggested,

access to

ERP system

must be in

few hands.

A new

security can

be generated

which must

be with FD,

AR manager

and MD

specialists

only. And,

changes

through

other

departments

must be

through

specific

templates

formulated

(with every

minute

detail)

(Bonnie et.

al., 2012, p.

307-333).

2. Sales billing

systems: The

MD specialists

use billing

system for

making bills.

There are

varied

irrelevant

fields which

must be

excluded.

It makes the

process a

time-

consuming

one which

leads to

delay in the

A new

billing

template

must be

formed in

consultation

with FD, AR

6

processing

system.

manager and

head of sales

with

eliminating

irrelevant

fields.

And,

changes in

the system

can be done

which guide

with regard

to any

irrelevant

field

(Bonnie et.

al., 2012, p.

307-333).

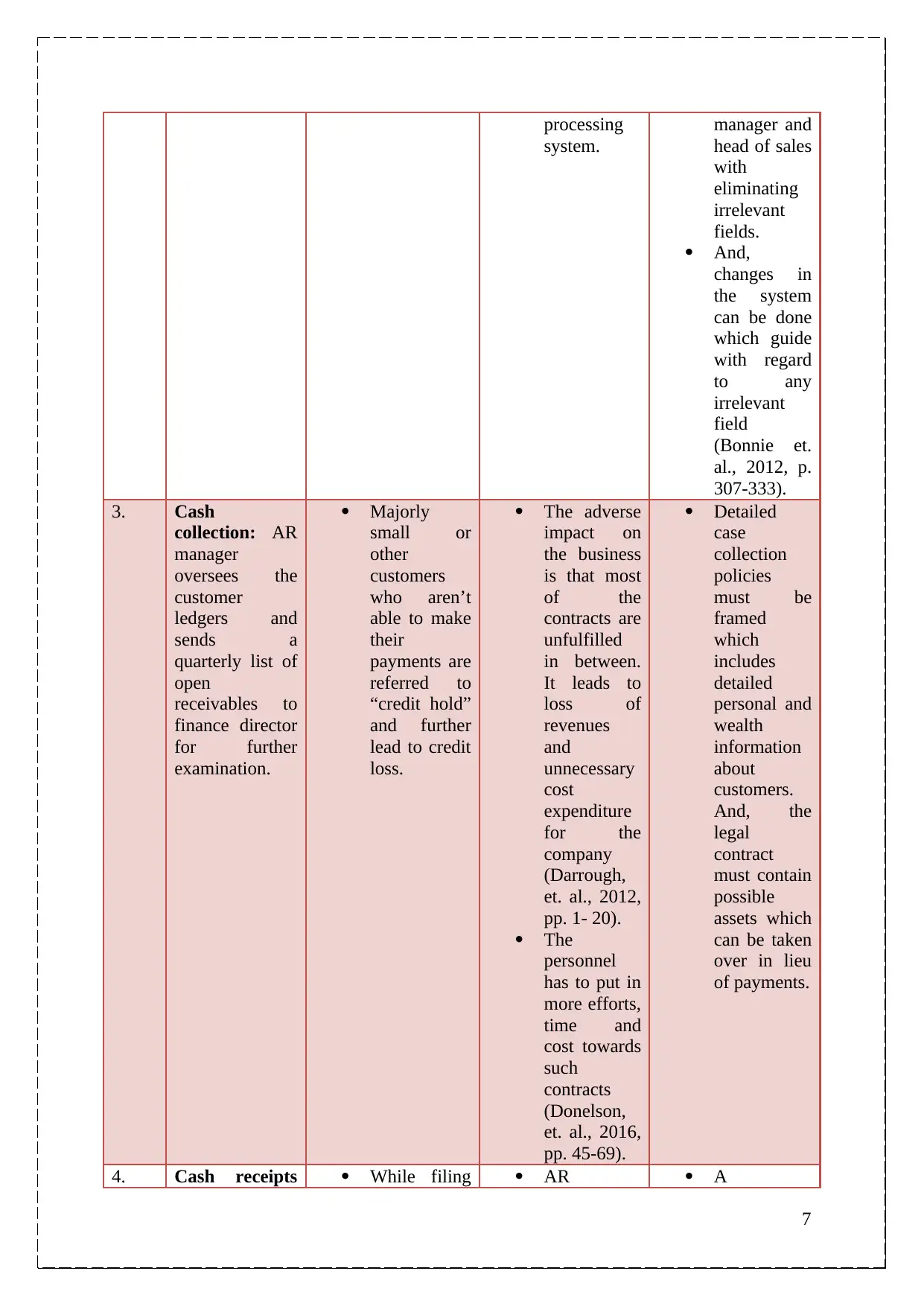

3. Cash

collection: AR

manager

oversees the

customer

ledgers and

sends a

quarterly list of

open

receivables to

finance director

for further

examination.

Majorly

small or

other

customers

who aren’t

able to make

their

payments are

referred to

“credit hold”

and further

lead to credit

loss.

The adverse

impact on

the business

is that most

of the

contracts are

unfulfilled

in between.

It leads to

loss of

revenues

and

unnecessary

cost

expenditure

for the

company

(Darrough,

et. al., 2012,

pp. 1- 20).

The

personnel

has to put in

more efforts,

time and

cost towards

such

contracts

(Donelson,

et. al., 2016,

pp. 45-69).

Detailed

case

collection

policies

must be

framed

which

includes

detailed

personal and

wealth

information

about

customers.

And, the

legal

contract

must contain

possible

assets which

can be taken

over in lieu

of payments.

4. Cash receipts While filing AR A

7

system.

manager and

head of sales

with

eliminating

irrelevant

fields.

And,

changes in

the system

can be done

which guide

with regard

to any

irrelevant

field

(Bonnie et.

al., 2012, p.

307-333).

3. Cash

collection: AR

manager

oversees the

customer

ledgers and

sends a

quarterly list of

open

receivables to

finance director

for further

examination.

Majorly

small or

other

customers

who aren’t

able to make

their

payments are

referred to

“credit hold”

and further

lead to credit

loss.

The adverse

impact on

the business

is that most

of the

contracts are

unfulfilled

in between.

It leads to

loss of

revenues

and

unnecessary

cost

expenditure

for the

company

(Darrough,

et. al., 2012,

pp. 1- 20).

The

personnel

has to put in

more efforts,

time and

cost towards

such

contracts

(Donelson,

et. al., 2016,

pp. 45-69).

Detailed

case

collection

policies

must be

framed

which

includes

detailed

personal and

wealth

information

about

customers.

And, the

legal

contract

must contain

possible

assets which

can be taken

over in lieu

of payments.

4. Cash receipts While filing AR A

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

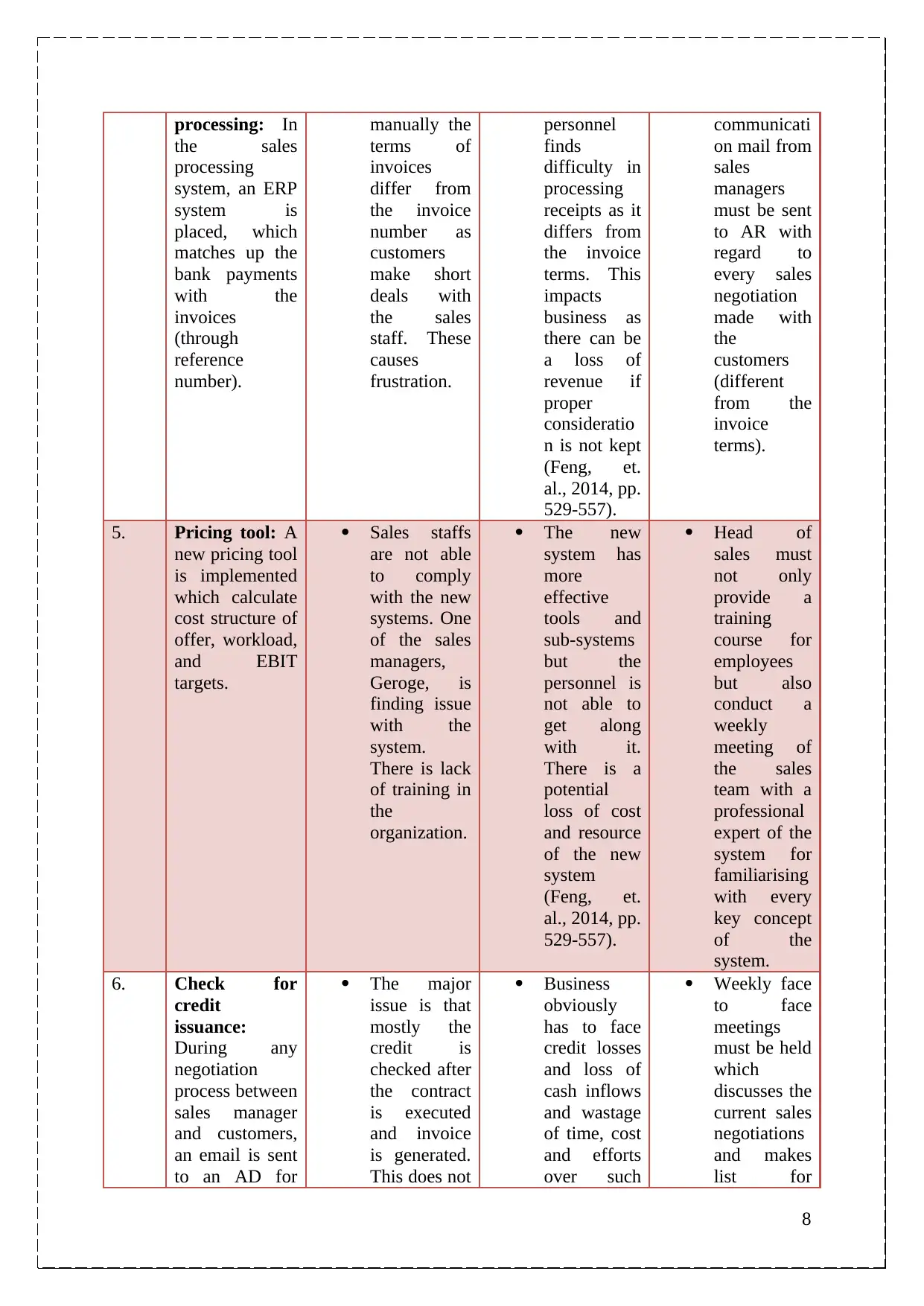

processing: In

the sales

processing

system, an ERP

system is

placed, which

matches up the

bank payments

with the

invoices

(through

reference

number).

manually the

terms of

invoices

differ from

the invoice

number as

customers

make short

deals with

the sales

staff. These

causes

frustration.

personnel

finds

difficulty in

processing

receipts as it

differs from

the invoice

terms. This

impacts

business as

there can be

a loss of

revenue if

proper

consideratio

n is not kept

(Feng, et.

al., 2014, pp.

529-557).

communicati

on mail from

sales

managers

must be sent

to AR with

regard to

every sales

negotiation

made with

the

customers

(different

from the

invoice

terms).

5. Pricing tool: A

new pricing tool

is implemented

which calculate

cost structure of

offer, workload,

and EBIT

targets.

Sales staffs

are not able

to comply

with the new

systems. One

of the sales

managers,

Geroge, is

finding issue

with the

system.

There is lack

of training in

the

organization.

The new

system has

more

effective

tools and

sub-systems

but the

personnel is

not able to

get along

with it.

There is a

potential

loss of cost

and resource

of the new

system

(Feng, et.

al., 2014, pp.

529-557).

Head of

sales must

not only

provide a

training

course for

employees

but also

conduct a

weekly

meeting of

the sales

team with a

professional

expert of the

system for

familiarising

with every

key concept

of the

system.

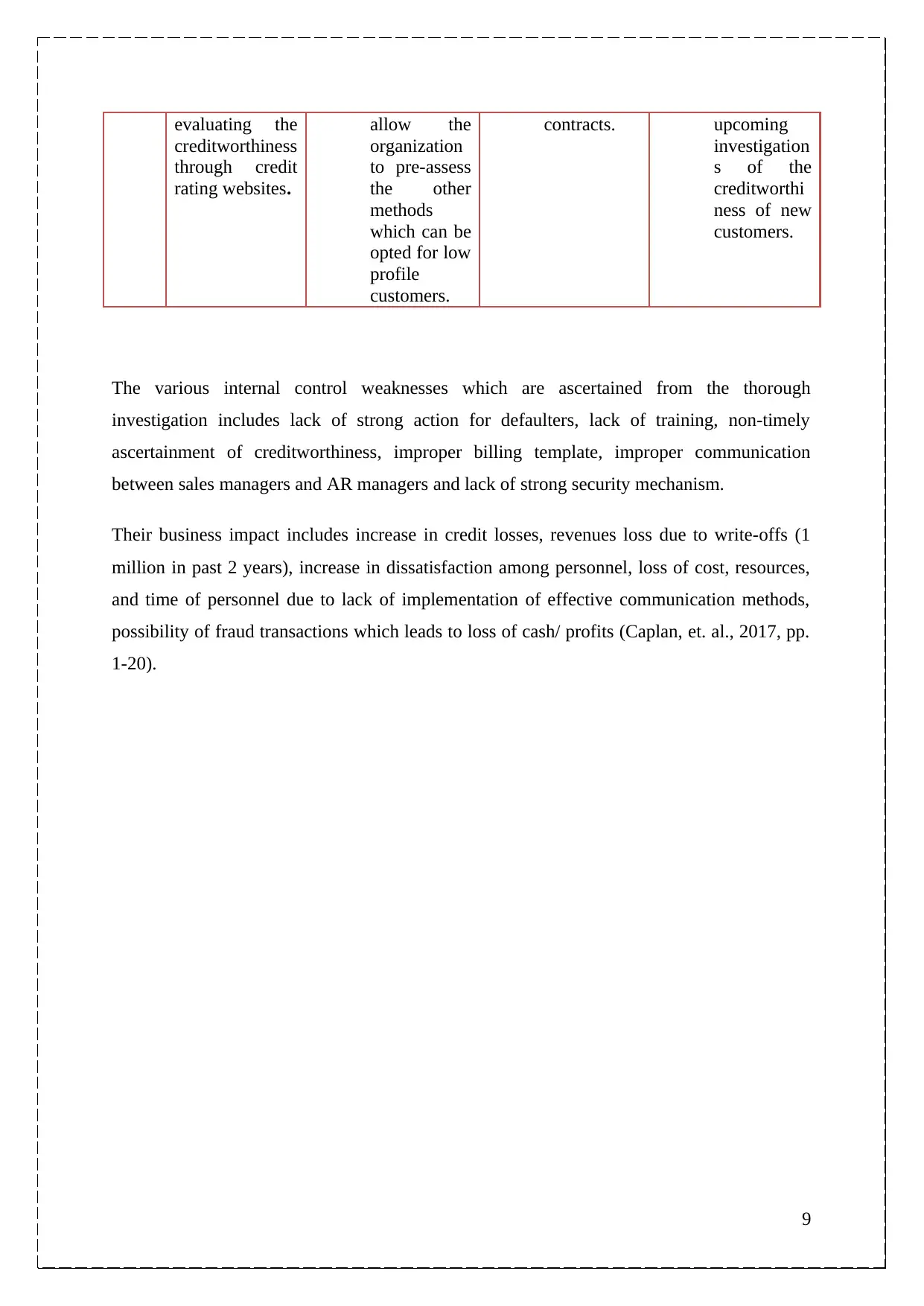

6. Check for

credit

issuance:

During any

negotiation

process between

sales manager

and customers,

an email is sent

to an AD for

The major

issue is that

mostly the

credit is

checked after

the contract

is executed

and invoice

is generated.

This does not

Business

obviously

has to face

credit losses

and loss of

cash inflows

and wastage

of time, cost

and efforts

over such

Weekly face

to face

meetings

must be held

which

discusses the

current sales

negotiations

and makes

list for

8

the sales

processing

system, an ERP

system is

placed, which

matches up the

bank payments

with the

invoices

(through

reference

number).

manually the

terms of

invoices

differ from

the invoice

number as

customers

make short

deals with

the sales

staff. These

causes

frustration.

personnel

finds

difficulty in

processing

receipts as it

differs from

the invoice

terms. This

impacts

business as

there can be

a loss of

revenue if

proper

consideratio

n is not kept

(Feng, et.

al., 2014, pp.

529-557).

communicati

on mail from

sales

managers

must be sent

to AR with

regard to

every sales

negotiation

made with

the

customers

(different

from the

invoice

terms).

5. Pricing tool: A

new pricing tool

is implemented

which calculate

cost structure of

offer, workload,

and EBIT

targets.

Sales staffs

are not able

to comply

with the new

systems. One

of the sales

managers,

Geroge, is

finding issue

with the

system.

There is lack

of training in

the

organization.

The new

system has

more

effective

tools and

sub-systems

but the

personnel is

not able to

get along

with it.

There is a

potential

loss of cost

and resource

of the new

system

(Feng, et.

al., 2014, pp.

529-557).

Head of

sales must

not only

provide a

training

course for

employees

but also

conduct a

weekly

meeting of

the sales

team with a

professional

expert of the

system for

familiarising

with every

key concept

of the

system.

6. Check for

credit

issuance:

During any

negotiation

process between

sales manager

and customers,

an email is sent

to an AD for

The major

issue is that

mostly the

credit is

checked after

the contract

is executed

and invoice

is generated.

This does not

Business

obviously

has to face

credit losses

and loss of

cash inflows

and wastage

of time, cost

and efforts

over such

Weekly face

to face

meetings

must be held

which

discusses the

current sales

negotiations

and makes

list for

8

evaluating the

creditworthiness

through credit

rating websites.

allow the

organization

to pre-assess

the other

methods

which can be

opted for low

profile

customers.

contracts. upcoming

investigation

s of the

creditworthi

ness of new

customers.

The various internal control weaknesses which are ascertained from the thorough

investigation includes lack of strong action for defaulters, lack of training, non-timely

ascertainment of creditworthiness, improper billing template, improper communication

between sales managers and AR managers and lack of strong security mechanism.

Their business impact includes increase in credit losses, revenues loss due to write-offs (1

million in past 2 years), increase in dissatisfaction among personnel, loss of cost, resources,

and time of personnel due to lack of implementation of effective communication methods,

possibility of fraud transactions which leads to loss of cash/ profits (Caplan, et. al., 2017, pp.

1-20).

9

creditworthiness

through credit

rating websites.

allow the

organization

to pre-assess

the other

methods

which can be

opted for low

profile

customers.

contracts. upcoming

investigation

s of the

creditworthi

ness of new

customers.

The various internal control weaknesses which are ascertained from the thorough

investigation includes lack of strong action for defaulters, lack of training, non-timely

ascertainment of creditworthiness, improper billing template, improper communication

between sales managers and AR managers and lack of strong security mechanism.

Their business impact includes increase in credit losses, revenues loss due to write-offs (1

million in past 2 years), increase in dissatisfaction among personnel, loss of cost, resources,

and time of personnel due to lack of implementation of effective communication methods,

possibility of fraud transactions which leads to loss of cash/ profits (Caplan, et. al., 2017, pp.

1-20).

9

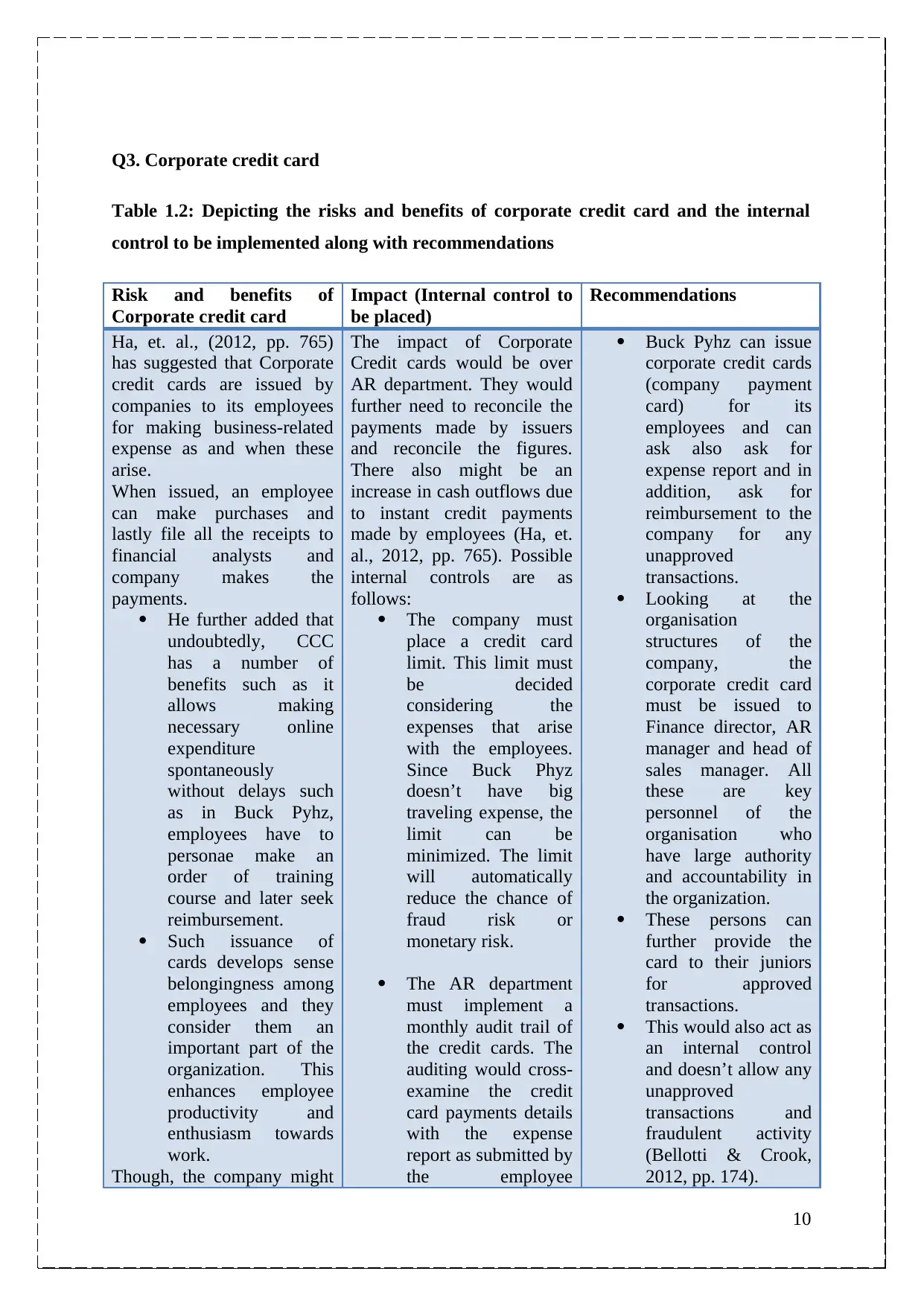

Q3. Corporate credit card

Table 1.2: Depicting the risks and benefits of corporate credit card and the internal

control to be implemented along with recommendations

Risk and benefits of

Corporate credit card

Impact (Internal control to

be placed)

Recommendations

Ha, et. al., (2012, pp. 765)

has suggested that Corporate

credit cards are issued by

companies to its employees

for making business-related

expense as and when these

arise.

When issued, an employee

can make purchases and

lastly file all the receipts to

financial analysts and

company makes the

payments.

He further added that

undoubtedly, CCC

has a number of

benefits such as it

allows making

necessary online

expenditure

spontaneously

without delays such

as in Buck Pyhz,

employees have to

personae make an

order of training

course and later seek

reimbursement.

Such issuance of

cards develops sense

belongingness among

employees and they

consider them an

important part of the

organization. This

enhances employee

productivity and

enthusiasm towards

work.

Though, the company might

The impact of Corporate

Credit cards would be over

AR department. They would

further need to reconcile the

payments made by issuers

and reconcile the figures.

There also might be an

increase in cash outflows due

to instant credit payments

made by employees (Ha, et.

al., 2012, pp. 765). Possible

internal controls are as

follows:

The company must

place a credit card

limit. This limit must

be decided

considering the

expenses that arise

with the employees.

Since Buck Phyz

doesn’t have big

traveling expense, the

limit can be

minimized. The limit

will automatically

reduce the chance of

fraud risk or

monetary risk.

The AR department

must implement a

monthly audit trail of

the credit cards. The

auditing would cross-

examine the credit

card payments details

with the expense

report as submitted by

the employee

Buck Pyhz can issue

corporate credit cards

(company payment

card) for its

employees and can

ask also ask for

expense report and in

addition, ask for

reimbursement to the

company for any

unapproved

transactions.

Looking at the

organisation

structures of the

company, the

corporate credit card

must be issued to

Finance director, AR

manager and head of

sales manager. All

these are key

personnel of the

organisation who

have large authority

and accountability in

the organization.

These persons can

further provide the

card to their juniors

for approved

transactions.

This would also act as

an internal control

and doesn’t allow any

unapproved

transactions and

fraudulent activity

(Bellotti & Crook,

2012, pp. 174).

10

Table 1.2: Depicting the risks and benefits of corporate credit card and the internal

control to be implemented along with recommendations

Risk and benefits of

Corporate credit card

Impact (Internal control to

be placed)

Recommendations

Ha, et. al., (2012, pp. 765)

has suggested that Corporate

credit cards are issued by

companies to its employees

for making business-related

expense as and when these

arise.

When issued, an employee

can make purchases and

lastly file all the receipts to

financial analysts and

company makes the

payments.

He further added that

undoubtedly, CCC

has a number of

benefits such as it

allows making

necessary online

expenditure

spontaneously

without delays such

as in Buck Pyhz,

employees have to

personae make an

order of training

course and later seek

reimbursement.

Such issuance of

cards develops sense

belongingness among

employees and they

consider them an

important part of the

organization. This

enhances employee

productivity and

enthusiasm towards

work.

Though, the company might

The impact of Corporate

Credit cards would be over

AR department. They would

further need to reconcile the

payments made by issuers

and reconcile the figures.

There also might be an

increase in cash outflows due

to instant credit payments

made by employees (Ha, et.

al., 2012, pp. 765). Possible

internal controls are as

follows:

The company must

place a credit card

limit. This limit must

be decided

considering the

expenses that arise

with the employees.

Since Buck Phyz

doesn’t have big

traveling expense, the

limit can be

minimized. The limit

will automatically

reduce the chance of

fraud risk or

monetary risk.

The AR department

must implement a

monthly audit trail of

the credit cards. The

auditing would cross-

examine the credit

card payments details

with the expense

report as submitted by

the employee

Buck Pyhz can issue

corporate credit cards

(company payment

card) for its

employees and can

ask also ask for

expense report and in

addition, ask for

reimbursement to the

company for any

unapproved

transactions.

Looking at the

organisation

structures of the

company, the

corporate credit card

must be issued to

Finance director, AR

manager and head of

sales manager. All

these are key

personnel of the

organisation who

have large authority

and accountability in

the organization.

These persons can

further provide the

card to their juniors

for approved

transactions.

This would also act as

an internal control

and doesn’t allow any

unapproved

transactions and

fraudulent activity

(Bellotti & Crook,

2012, pp. 174).

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

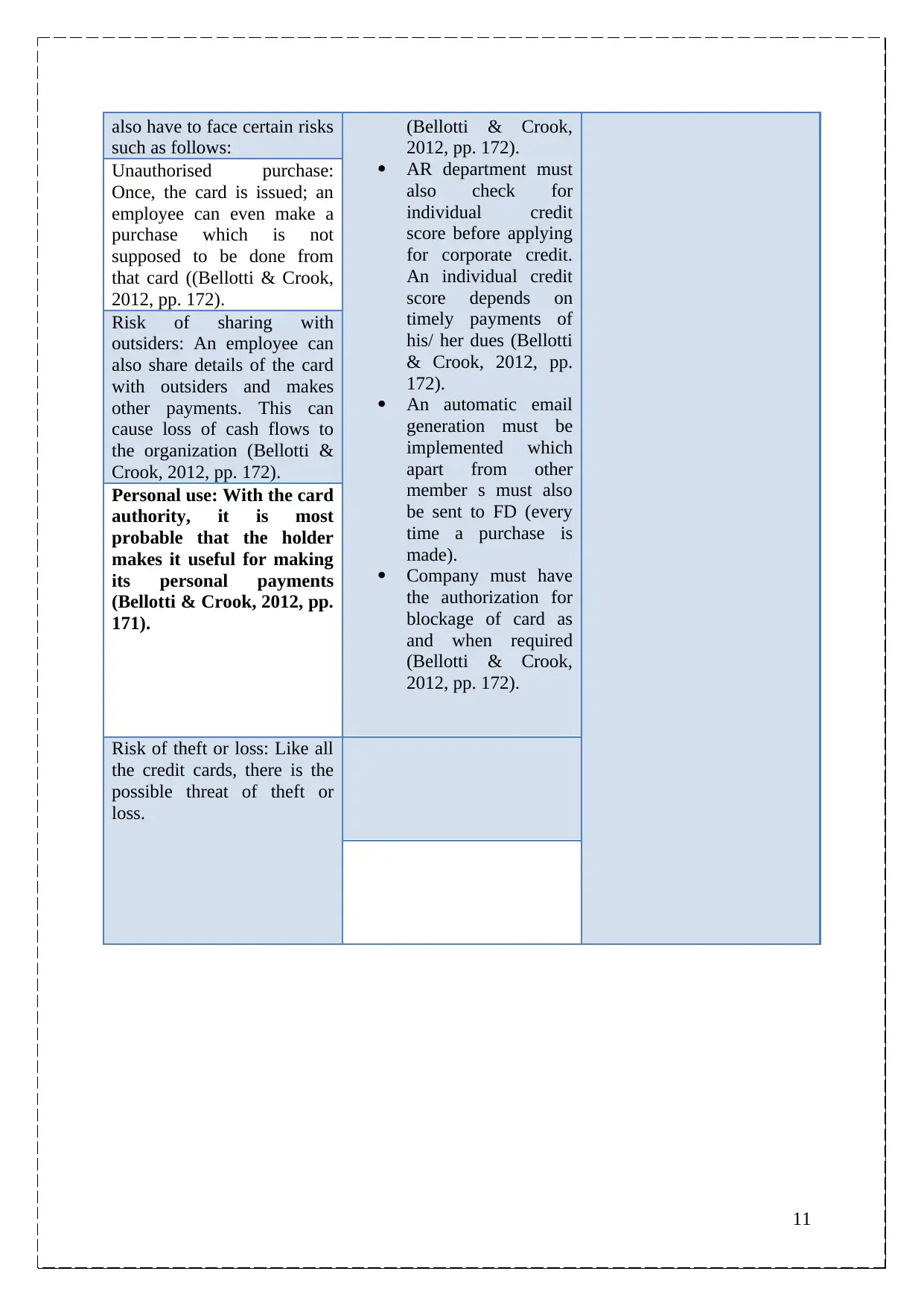

also have to face certain risks

such as follows:

(Bellotti & Crook,

2012, pp. 172).

AR department must

also check for

individual credit

score before applying

for corporate credit.

An individual credit

score depends on

timely payments of

his/ her dues (Bellotti

& Crook, 2012, pp.

172).

An automatic email

generation must be

implemented which

apart from other

member s must also

be sent to FD (every

time a purchase is

made).

Company must have

the authorization for

blockage of card as

and when required

(Bellotti & Crook,

2012, pp. 172).

Unauthorised purchase:

Once, the card is issued; an

employee can even make a

purchase which is not

supposed to be done from

that card ((Bellotti & Crook,

2012, pp. 172).

Risk of sharing with

outsiders: An employee can

also share details of the card

with outsiders and makes

other payments. This can

cause loss of cash flows to

the organization (Bellotti &

Crook, 2012, pp. 172).

Personal use: With the card

authority, it is most

probable that the holder

makes it useful for making

its personal payments

(Bellotti & Crook, 2012, pp.

171).

Risk of theft or loss: Like all

the credit cards, there is the

possible threat of theft or

loss.

11

such as follows:

(Bellotti & Crook,

2012, pp. 172).

AR department must

also check for

individual credit

score before applying

for corporate credit.

An individual credit

score depends on

timely payments of

his/ her dues (Bellotti

& Crook, 2012, pp.

172).

An automatic email

generation must be

implemented which

apart from other

member s must also

be sent to FD (every

time a purchase is

made).

Company must have

the authorization for

blockage of card as

and when required

(Bellotti & Crook,

2012, pp. 172).

Unauthorised purchase:

Once, the card is issued; an

employee can even make a

purchase which is not

supposed to be done from

that card ((Bellotti & Crook,

2012, pp. 172).

Risk of sharing with

outsiders: An employee can

also share details of the card

with outsiders and makes

other payments. This can

cause loss of cash flows to

the organization (Bellotti &

Crook, 2012, pp. 172).

Personal use: With the card

authority, it is most

probable that the holder

makes it useful for making

its personal payments

(Bellotti & Crook, 2012, pp.

171).

Risk of theft or loss: Like all

the credit cards, there is the

possible threat of theft or

loss.

11

Conclusion:

With this report, it can be concluded that Buck Phyz is currently facing a number of internal

control weaknesses in its sales process. The company has also been facing difficulties such as

credit loss, loss of revenues, improper investigation of customer’s creditworthiness and lack

of tight security to providing access of ERP system to a large number of personnel. With this

overview, it is suggested the organisation need to improve its communication channels (for

effective customer verification, detailed modification of term and reduction in credit hold/

credit loss), lesser access of ERP system for true customer database etc. lastly, company must

also corporate credit cards to its key persons for non-delay for payments and no personal

expenses to be made by employees for business-related expenses.

12

With this report, it can be concluded that Buck Phyz is currently facing a number of internal

control weaknesses in its sales process. The company has also been facing difficulties such as

credit loss, loss of revenues, improper investigation of customer’s creditworthiness and lack

of tight security to providing access of ERP system to a large number of personnel. With this

overview, it is suggested the organisation need to improve its communication channels (for

effective customer verification, detailed modification of term and reduction in credit hold/

credit loss), lesser access of ERP system for true customer database etc. lastly, company must

also corporate credit cards to its key persons for non-delay for payments and no personal

expenses to be made by employees for business-related expenses.

12

Reference:

Bellotti, T., & Crook, J. (2012). Loss given default models incorporating

macroeconomic variables for credit cards. International Journal of Forecasting, 28(1),

171-182.

Bonnie K. Klamm, Kevin W. Kobelsky, and Marcia Weidenmier Watson (2012)

Determinants of the Persistence of Internal Control Weaknesses. Accounting

Horizons: June 2012, Vol. 26, No. 2, pp. 307-333.

Caplan, D., Dutta, S. K., & Liu, A. Z. (2017). Are Material Weaknesses in Internal

Controls Associated with Poor M&A Decisions? Evidence from Goodwill

Impairment. Auditing: A Journal of Practice and Theory, pp. 1-20.

Darrough, M., Huang, R., Zur, E., (2012). Internal control weaknesses in the market

for corporate control, Disclosure vs. Propensity. Branch college, city university of

New york, pp. 1-20.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses

and financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), pp.

45-69.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control

over financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), pp. 529-557.

Ha, S. H., & Krishnan, R. (2012). Predicting repayment of the credit card debt.

Computers & Operations Research, 39(4), 765-773.

13

Bellotti, T., & Crook, J. (2012). Loss given default models incorporating

macroeconomic variables for credit cards. International Journal of Forecasting, 28(1),

171-182.

Bonnie K. Klamm, Kevin W. Kobelsky, and Marcia Weidenmier Watson (2012)

Determinants of the Persistence of Internal Control Weaknesses. Accounting

Horizons: June 2012, Vol. 26, No. 2, pp. 307-333.

Caplan, D., Dutta, S. K., & Liu, A. Z. (2017). Are Material Weaknesses in Internal

Controls Associated with Poor M&A Decisions? Evidence from Goodwill

Impairment. Auditing: A Journal of Practice and Theory, pp. 1-20.

Darrough, M., Huang, R., Zur, E., (2012). Internal control weaknesses in the market

for corporate control, Disclosure vs. Propensity. Branch college, city university of

New york, pp. 1-20.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses

and financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), pp.

45-69.

Feng, M., Li, C., McVay, S. E., & Skaife, H. (2014). Does ineffective internal control

over financial reporting affect a firm's operations? Evidence from firms' inventory

management. The Accounting Review, 90(2), pp. 529-557.

Ha, S. H., & Krishnan, R. (2012). Predicting repayment of the credit card debt.

Computers & Operations Research, 39(4), 765-773.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.