Financial Accounting: Intangible Assets Report (IAS 38/AASB 138)

VerifiedAdded on 2022/09/01

|14

|3140

|52

Report

AI Summary

This report critically assesses the accounting standard AASB 138 and its impact on reporting entities, particularly regarding intangible assets. It explores the differences between internally generated and acquired intangible assets, emphasizing the criteria for recognizing intangible assets. The report delves into the accounting treatment of internally generated goodwill and other intangible assets, supported by illustrative examples, including the computation of goodwill and amortization. It also identifies reasons for companies' reluctance to recognize internally generated intangible assets. The report provides a comprehensive analysis of the standard's application, including detailed examples and calculations, and concludes with a summary of the key findings and implications for financial reporting. The report also outlines the conditions for recognizing internally generated intangible assets and the accounting treatment for acquired intangible assets. Furthermore, the report provides an example of goodwill valuation using the super profit method and demonstrates the amortization of internally developed technology.

Running head: INTERNALLY GENERATED INTANGIBLE ASSETS

Internally generated intangible assets

Name of the Student

Name of the University

Author Note

Internally generated intangible assets

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

INTERNALLY GENERATED INTANGIBLE ASSETS

Executive summary:

The report is prepared to evaluate the impact of the accounting standard IAS 138/AASB 138

in the treatment of intangible assets of the company. It also involves the discussion on the

identification of the differences between the intangible assets that is generated internally by

the organization and intangible assets that are acquired. The adoption of the standard for the

treatment of intangible assets by the company has been discussed in terms of their willingness

to adopt. The accounting treatment of the intangible assets are supported by the calculation

that demonstrates how such assets is recorded in the books of account.

INTERNALLY GENERATED INTANGIBLE ASSETS

Executive summary:

The report is prepared to evaluate the impact of the accounting standard IAS 138/AASB 138

in the treatment of intangible assets of the company. It also involves the discussion on the

identification of the differences between the intangible assets that is generated internally by

the organization and intangible assets that are acquired. The adoption of the standard for the

treatment of intangible assets by the company has been discussed in terms of their willingness

to adopt. The accounting treatment of the intangible assets are supported by the calculation

that demonstrates how such assets is recorded in the books of account.

2

INTERNALLY GENERATED INTANGIBLE ASSETS

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Evaluating the impact of AASB 138/IAS 38 for internally generated intangible assets:..........3

Identification of the difference between accounting for internally generated intangible assets

and acquired intangible assets:...................................................................................................4

Example explaining the computation of internally generated goodwill....................................7

Identifying the reasons behind the reluctance of the companies to press:.................................8

Conclusion:................................................................................................................................9

References list:.........................................................................................................................10

INTERNALLY GENERATED INTANGIBLE ASSETS

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Evaluating the impact of AASB 138/IAS 38 for internally generated intangible assets:..........3

Identification of the difference between accounting for internally generated intangible assets

and acquired intangible assets:...................................................................................................4

Example explaining the computation of internally generated goodwill....................................7

Identifying the reasons behind the reluctance of the companies to press:.................................8

Conclusion:................................................................................................................................9

References list:.........................................................................................................................10

3

INTERNALLY GENERATED INTANGIBLE ASSETS

Introduction:

The paper is developed to critically assess the accounting standard AASB 138 and its

impact on the reporting entities. AASB 138 deals with the intangible assets that prescribes

accounting treatment for the same. There are some specified sets of criteria that are required

to be met by reporting entity to recognize intangible assets. Intangible Asset has no physical

existence unlike physical assets like building, land, machinery, equipment, inventory and

much more. It is very challenging to ascertain the value of intangible assets. Both AASB138

and IAS38 provides provision regarding the accounting of the intangible assets.

Intangible assets are of two types- Internally generated and acquired. Intangible

assets that are generated internally refer to the assets that the company generate itself for the

sole purpose of increasing its productivity or giving the firm a competitive edge in the open

market. Intangible assets developed by the firm include brand names, such as goodwill that

are generated which is not openly stated in the financial statement but it is basically the

distinction between the market value of the business and sum total of the total assets (Su et

al. 2018). On the other hand, Acquired Intangible Assets are those intangible assets that a

business purchase either to improve the product quality, production process or acquiring

some new updated technologies to gain a competitive edge in the market. Acquired intangible

Assets includes goodwill, patents, copyrights and many more (Cosmulese et al. 2017).

Recognition of intangible assets generated internally should not be done as an asset and

assessing the intangible assets as internally generated classifies the generation of asset into

research and development. Acquired intangible assets represents the amalgamation and

accounts the purchase nature according to the accounting standard. However, in spite of

adding any material value to the company, the intangible assets are invaluable to the

company in the way that it increases its competitive strength in the market. For example, the

brand image and goodwill of different MNC’s like Nike, Adidas increases its competitive

INTERNALLY GENERATED INTANGIBLE ASSETS

Introduction:

The paper is developed to critically assess the accounting standard AASB 138 and its

impact on the reporting entities. AASB 138 deals with the intangible assets that prescribes

accounting treatment for the same. There are some specified sets of criteria that are required

to be met by reporting entity to recognize intangible assets. Intangible Asset has no physical

existence unlike physical assets like building, land, machinery, equipment, inventory and

much more. It is very challenging to ascertain the value of intangible assets. Both AASB138

and IAS38 provides provision regarding the accounting of the intangible assets.

Intangible assets are of two types- Internally generated and acquired. Intangible

assets that are generated internally refer to the assets that the company generate itself for the

sole purpose of increasing its productivity or giving the firm a competitive edge in the open

market. Intangible assets developed by the firm include brand names, such as goodwill that

are generated which is not openly stated in the financial statement but it is basically the

distinction between the market value of the business and sum total of the total assets (Su et

al. 2018). On the other hand, Acquired Intangible Assets are those intangible assets that a

business purchase either to improve the product quality, production process or acquiring

some new updated technologies to gain a competitive edge in the market. Acquired intangible

Assets includes goodwill, patents, copyrights and many more (Cosmulese et al. 2017).

Recognition of intangible assets generated internally should not be done as an asset and

assessing the intangible assets as internally generated classifies the generation of asset into

research and development. Acquired intangible assets represents the amalgamation and

accounts the purchase nature according to the accounting standard. However, in spite of

adding any material value to the company, the intangible assets are invaluable to the

company in the way that it increases its competitive strength in the market. For example, the

brand image and goodwill of different MNC’s like Nike, Adidas increases its competitive

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

INTERNALLY GENERATED INTANGIBLE ASSETS

advantage. This report aims at deducing the impacts of AASB 138 and IAS 38 for the

intangible assets that are generated internally.

Discussion:

Evaluating the effect of AASB 138/IAS 38 for internally generated intangible assets:

Intangible assets that are generated internally are the resources advanced by the

company that will yield future benefits; however, these assets are not in physical existence

like land and building, machinery. These Internally generated intangible assets include a

brand name, internally generated goodwill and many more. However, according to the

requirement of AASB 138 and IAS 38, intangible assets generated internally are not recorded

as assets in the Balance Sheet because its source cannot be easily recognized and also that it

is challenging to measure it fairly at cost. Internally generated intangible assets that arising

due to research is not to be recorded and recognized in the books (Aasb.gov.au 2020).

However, the expenses that are incurred in the research process are to be separately registered

as an expense when the cost relating to it is incurred.

An internally generated intangible asset that is either developed or under development

in the company can be registered and recognized if it satisfies the following conditions.

Firstly, recognition of intangible asset is done if the technical viability of developing the asset

can be demonstrated so that the asset could be readily used or sold. Secondly, the asset can be

recognized if the company is able to show its purpose to develop the asset with the sole

intention to either use it or sell it. Thirdly, it can be recognized if the company could be able

to show its willingness to either use sell the asset. Fourthly, asset can be recognized if the

company is able to portray how such will create possible upcoming benefits for the company.

This can either be achieved if the company could identify and show the presence of the

INTERNALLY GENERATED INTANGIBLE ASSETS

advantage. This report aims at deducing the impacts of AASB 138 and IAS 38 for the

intangible assets that are generated internally.

Discussion:

Evaluating the effect of AASB 138/IAS 38 for internally generated intangible assets:

Intangible assets that are generated internally are the resources advanced by the

company that will yield future benefits; however, these assets are not in physical existence

like land and building, machinery. These Internally generated intangible assets include a

brand name, internally generated goodwill and many more. However, according to the

requirement of AASB 138 and IAS 38, intangible assets generated internally are not recorded

as assets in the Balance Sheet because its source cannot be easily recognized and also that it

is challenging to measure it fairly at cost. Internally generated intangible assets that arising

due to research is not to be recorded and recognized in the books (Aasb.gov.au 2020).

However, the expenses that are incurred in the research process are to be separately registered

as an expense when the cost relating to it is incurred.

An internally generated intangible asset that is either developed or under development

in the company can be registered and recognized if it satisfies the following conditions.

Firstly, recognition of intangible asset is done if the technical viability of developing the asset

can be demonstrated so that the asset could be readily used or sold. Secondly, the asset can be

recognized if the company is able to show its purpose to develop the asset with the sole

intention to either use it or sell it. Thirdly, it can be recognized if the company could be able

to show its willingness to either use sell the asset. Fourthly, asset can be recognized if the

company is able to portray how such will create possible upcoming benefits for the company.

This can either be achieved if the company could identify and show the presence of the

5

INTERNALLY GENERATED INTANGIBLE ASSETS

market for the developed asset or could portray the effectiveness of the developed asset.

Fifthly, asset could be recognized if there is adequate technical and financial knowledge other

resources for the generating the intangible asset internally which could be used either use the

asset or to sale it (Cosmulese et al. 2017). Lastly, recognition of the internally generated

intangible asset could be done if there is a dependability in the measurement of expenses for

the asset development. On other hand, recording and recognizing of acquired intangible are

done in the books because its cost can always be separately ascertained. The initial cost at

which the Acquired intangible asset is to be recorded should be its initial price, including all

refundable and non-refundable taxes and after discounts and rebates deduction. The initial

purchase price should also include the cost of and installing the asset for using it in the

production. It should also be remembered that if the acquired intangible asset results out of

any business combination, then the fair value of the intangible asset should be its cost price

and should be recorded on its acquisition date (Russell 2017).

Identification of the difference between accounting for internally generated intangible

assets and acquired intangible assets:

The accounting of the intangible assets acquired in the business combination requires

the entity to adopt AASB 138. In accordance with the AASB 3 of business combination, the

intangible assets fair value at the date of acquisition represents its cost. The expectation of

market participants is reflected in the assets about the prospect of the expected future

economic benefits. A group of the complimentary intangible assets by the acquirer is

recognized as the single asset. If the measurement of the acquired assets is not at the fair

value, then the carrying amount of the asset is used for measuring the cost. It is required by

the entity to make a disclosure of the intangible assets acquired by government grant and

recognizing it initially at the fair value (Wen and Moehrle 2016).

INTERNALLY GENERATED INTANGIBLE ASSETS

market for the developed asset or could portray the effectiveness of the developed asset.

Fifthly, asset could be recognized if there is adequate technical and financial knowledge other

resources for the generating the intangible asset internally which could be used either use the

asset or to sale it (Cosmulese et al. 2017). Lastly, recognition of the internally generated

intangible asset could be done if there is a dependability in the measurement of expenses for

the asset development. On other hand, recording and recognizing of acquired intangible are

done in the books because its cost can always be separately ascertained. The initial cost at

which the Acquired intangible asset is to be recorded should be its initial price, including all

refundable and non-refundable taxes and after discounts and rebates deduction. The initial

purchase price should also include the cost of and installing the asset for using it in the

production. It should also be remembered that if the acquired intangible asset results out of

any business combination, then the fair value of the intangible asset should be its cost price

and should be recorded on its acquisition date (Russell 2017).

Identification of the difference between accounting for internally generated intangible

assets and acquired intangible assets:

The accounting of the intangible assets acquired in the business combination requires

the entity to adopt AASB 138. In accordance with the AASB 3 of business combination, the

intangible assets fair value at the date of acquisition represents its cost. The expectation of

market participants is reflected in the assets about the prospect of the expected future

economic benefits. A group of the complimentary intangible assets by the acquirer is

recognized as the single asset. If the measurement of the acquired assets is not at the fair

value, then the carrying amount of the asset is used for measuring the cost. It is required by

the entity to make a disclosure of the intangible assets acquired by government grant and

recognizing it initially at the fair value (Wen and Moehrle 2016).

6

INTERNALLY GENERATED INTANGIBLE ASSETS

The accounting treatment for assessing the useful lives of the intangible assets

acquired as per AASB 138 can be explained with the help of an example of an acquired

patent expiring in fifteen years. A source of net cash flow is expected to be generated by the

patented technology protecting the product over the next fifteen years. The third party has

committed the entity to purchase the 60% of the fair value of patent in five years and the

selling off the patent in five years is intended by the entity. Over the five year assets life,

amortization of the patent would be done. On the acquired date, the present value of the 60%

of the fair value of patent is equal to the residual value (Cheung and Lau 2016).

The accounting for the intangible assets generated internally, it is required by the

entity to apply the guidance and requirements according to paragraph 52-67 of AASB 138

apart from aligning the requirements for the initial measurement and recognition of an

intangible assets. The costs incurred by the entity in internally generating the intangible assets

can be reliably measured using the costing system of entity. There should not be any

distinction between the business development cost as a whole and expenditure incurred on

the intangible assets generated internally. Recognition of goodwill should not be done as

assets as it do not represent identifiable resource that is measured reliably at cost provided

such assets has been generated internally. In some cases, the cost of maintaining and

enhancing the internally generated goodwill c from the cost of generating intangible assets

internally is not distinctive (Iasplus.com 2020).

An entity is required to classify the assets generation into phase of research and

development for assessing the recognition criteria of internally generated intangible assets.

Recognition of the intangible assets arising from the development phase is done when

the following facts is demonstrated by the entity. These includes

The intention of completing, using or selling the intangible assets

INTERNALLY GENERATED INTANGIBLE ASSETS

The accounting treatment for assessing the useful lives of the intangible assets

acquired as per AASB 138 can be explained with the help of an example of an acquired

patent expiring in fifteen years. A source of net cash flow is expected to be generated by the

patented technology protecting the product over the next fifteen years. The third party has

committed the entity to purchase the 60% of the fair value of patent in five years and the

selling off the patent in five years is intended by the entity. Over the five year assets life,

amortization of the patent would be done. On the acquired date, the present value of the 60%

of the fair value of patent is equal to the residual value (Cheung and Lau 2016).

The accounting for the intangible assets generated internally, it is required by the

entity to apply the guidance and requirements according to paragraph 52-67 of AASB 138

apart from aligning the requirements for the initial measurement and recognition of an

intangible assets. The costs incurred by the entity in internally generating the intangible assets

can be reliably measured using the costing system of entity. There should not be any

distinction between the business development cost as a whole and expenditure incurred on

the intangible assets generated internally. Recognition of goodwill should not be done as

assets as it do not represent identifiable resource that is measured reliably at cost provided

such assets has been generated internally. In some cases, the cost of maintaining and

enhancing the internally generated goodwill c from the cost of generating intangible assets

internally is not distinctive (Iasplus.com 2020).

An entity is required to classify the assets generation into phase of research and

development for assessing the recognition criteria of internally generated intangible assets.

Recognition of the intangible assets arising from the development phase is done when

the following facts is demonstrated by the entity. These includes

The intention of completing, using or selling the intangible assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTERNALLY GENERATED INTANGIBLE ASSETS

Evaluating the availability or the use of intangible assets by identifying the technical

feasibility.

Entity has acceptable resources for completing the development of using or vending

the intangible assets.

The expenditure relating to the development of such assets can be measured reliably

(Yaremko et al. 2017).

For distinguishing between other intangible assets and internally generated intangible

assets, entity is supposed to make disclosure for each class of intangible assets. The

accumulated amortization and gross carrying amount at the end and beginning of the period

should be disclosed. It is also required to disclose whether the intangible assets lives are finite

or infinite along with the method of amortization used (Christensen et al. 2019).

Some guidance are offered by the board on how the intangible assets should be

accounted in the reporting entity financial statement as per AASB 138. In general, entity is

not required to recognize the internally generated legal intangibles as against recognition of

intangibles purchased from the third parties. Amortization of the intangible assets for which

useful lives can be identified is done on the straight line method. Furthermore, it is important

to recognize the profit or loss generated from the impairment of such assets. Determination of

impairment loss should be done by deducting the assets fair value from its carrying value

(Trent and Mohr 2017).

Example explaining the computation of internally generated goodwill

Valuation of goodwill can be done by many methods, one of the widely accepted

technique is the valuation of goodwill through Super Profit method.

Particulars Amount ($)

INTERNALLY GENERATED INTANGIBLE ASSETS

Evaluating the availability or the use of intangible assets by identifying the technical

feasibility.

Entity has acceptable resources for completing the development of using or vending

the intangible assets.

The expenditure relating to the development of such assets can be measured reliably

(Yaremko et al. 2017).

For distinguishing between other intangible assets and internally generated intangible

assets, entity is supposed to make disclosure for each class of intangible assets. The

accumulated amortization and gross carrying amount at the end and beginning of the period

should be disclosed. It is also required to disclose whether the intangible assets lives are finite

or infinite along with the method of amortization used (Christensen et al. 2019).

Some guidance are offered by the board on how the intangible assets should be

accounted in the reporting entity financial statement as per AASB 138. In general, entity is

not required to recognize the internally generated legal intangibles as against recognition of

intangibles purchased from the third parties. Amortization of the intangible assets for which

useful lives can be identified is done on the straight line method. Furthermore, it is important

to recognize the profit or loss generated from the impairment of such assets. Determination of

impairment loss should be done by deducting the assets fair value from its carrying value

(Trent and Mohr 2017).

Example explaining the computation of internally generated goodwill

Valuation of goodwill can be done by many methods, one of the widely accepted

technique is the valuation of goodwill through Super Profit method.

Particulars Amount ($)

8

INTERNALLY GENERATED INTANGIBLE ASSETS

Total investment 1.00,000

Net profit for the year 25,000

Normal rate of return 20%

Number of years of purchase 5 years

Solution: Calculation of goodwill on the basis of 5 years purchase of super profits.

Normal profit = $ (1,00,000 x 20%) = $ 20,000

Therefore, Super profits = $ (25,000 – 20,000) = $ 5,000

Therefore, Goodwill = Super profits x Number of years of Purchase.

= $ (5,000 x 5)

= $ 25,000

Treatment of goodwill

Intangible assets are treated as an expense and hence it is written off (Amortized)

from the books through a straight-line method. If a company generates any assets internally

like developing any software or generating goodwill internally is amortized or written off

from the books subsequently.

A company develops certain technology internally at the cost of $ 1, 00,000, which

will improve its production and will provide a competitive edge to the company. The

company estimates that the developed technology will have an effective life of three years

keeping the continuous innovation in the field of production in mind.

INTERNALLY GENERATED INTANGIBLE ASSETS

Total investment 1.00,000

Net profit for the year 25,000

Normal rate of return 20%

Number of years of purchase 5 years

Solution: Calculation of goodwill on the basis of 5 years purchase of super profits.

Normal profit = $ (1,00,000 x 20%) = $ 20,000

Therefore, Super profits = $ (25,000 – 20,000) = $ 5,000

Therefore, Goodwill = Super profits x Number of years of Purchase.

= $ (5,000 x 5)

= $ 25,000

Treatment of goodwill

Intangible assets are treated as an expense and hence it is written off (Amortized)

from the books through a straight-line method. If a company generates any assets internally

like developing any software or generating goodwill internally is amortized or written off

from the books subsequently.

A company develops certain technology internally at the cost of $ 1, 00,000, which

will improve its production and will provide a competitive edge to the company. The

company estimates that the developed technology will have an effective life of three years

keeping the continuous innovation in the field of production in mind.

9

INTERNALLY GENERATED INTANGIBLE ASSETS

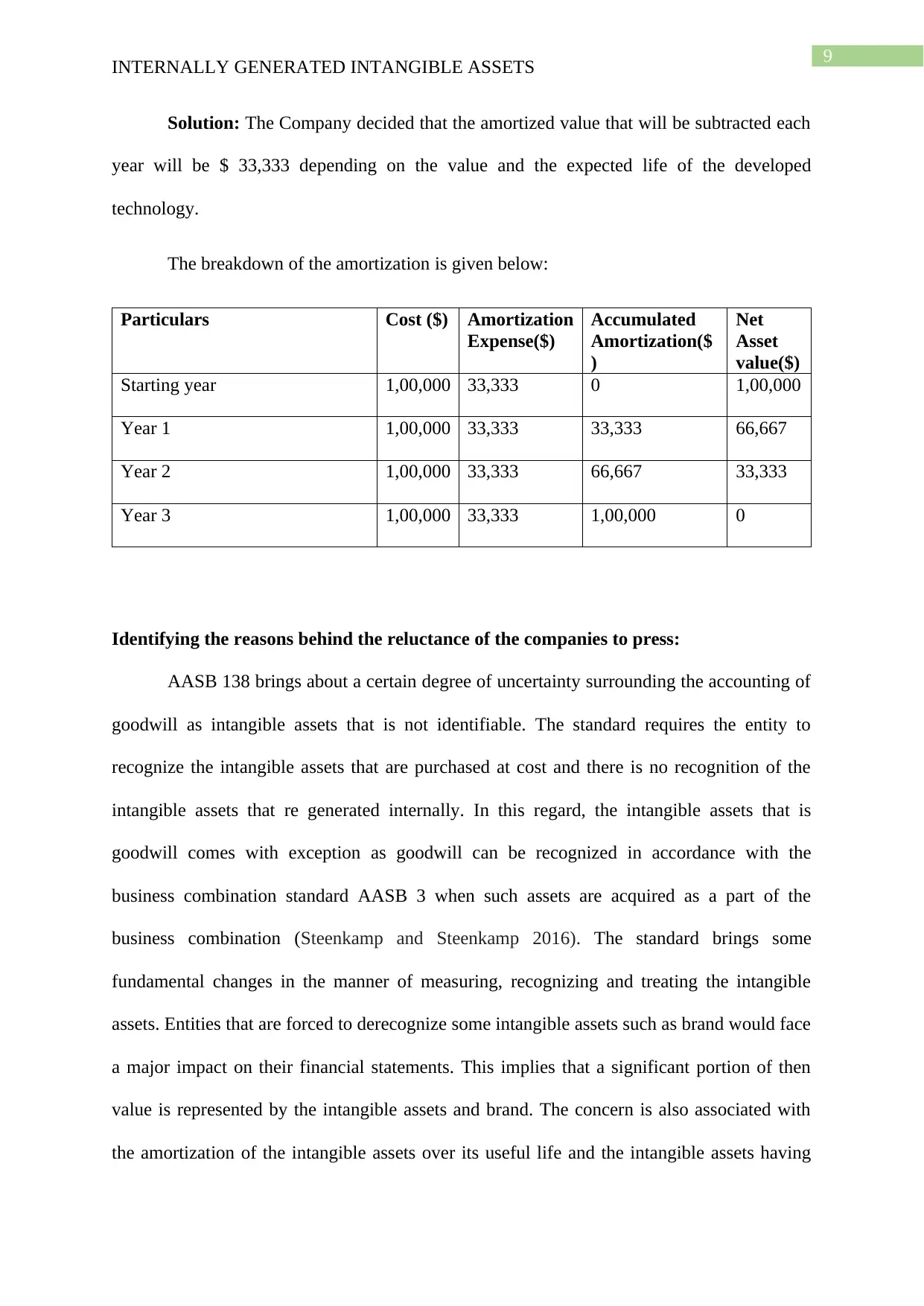

Solution: The Company decided that the amortized value that will be subtracted each

year will be $ 33,333 depending on the value and the expected life of the developed

technology.

The breakdown of the amortization is given below:

Particulars Cost ($) Amortization

Expense($)

Accumulated

Amortization($

)

Net

Asset

value($)

Starting year 1,00,000 33,333 0 1,00,000

Year 1 1,00,000 33,333 33,333 66,667

Year 2 1,00,000 33,333 66,667 33,333

Year 3 1,00,000 33,333 1,00,000 0

Identifying the reasons behind the reluctance of the companies to press:

AASB 138 brings about a certain degree of uncertainty surrounding the accounting of

goodwill as intangible assets that is not identifiable. The standard requires the entity to

recognize the intangible assets that are purchased at cost and there is no recognition of the

intangible assets that re generated internally. In this regard, the intangible assets that is

goodwill comes with exception as goodwill can be recognized in accordance with the

business combination standard AASB 3 when such assets are acquired as a part of the

business combination (Steenkamp and Steenkamp 2016). The standard brings some

fundamental changes in the manner of measuring, recognizing and treating the intangible

assets. Entities that are forced to derecognize some intangible assets such as brand would face

a major impact on their financial statements. This implies that a significant portion of then

value is represented by the intangible assets and brand. The concern is also associated with

the amortization of the intangible assets over its useful life and the intangible assets having

INTERNALLY GENERATED INTANGIBLE ASSETS

Solution: The Company decided that the amortized value that will be subtracted each

year will be $ 33,333 depending on the value and the expected life of the developed

technology.

The breakdown of the amortization is given below:

Particulars Cost ($) Amortization

Expense($)

Accumulated

Amortization($

)

Net

Asset

value($)

Starting year 1,00,000 33,333 0 1,00,000

Year 1 1,00,000 33,333 33,333 66,667

Year 2 1,00,000 33,333 66,667 33,333

Year 3 1,00,000 33,333 1,00,000 0

Identifying the reasons behind the reluctance of the companies to press:

AASB 138 brings about a certain degree of uncertainty surrounding the accounting of

goodwill as intangible assets that is not identifiable. The standard requires the entity to

recognize the intangible assets that are purchased at cost and there is no recognition of the

intangible assets that re generated internally. In this regard, the intangible assets that is

goodwill comes with exception as goodwill can be recognized in accordance with the

business combination standard AASB 3 when such assets are acquired as a part of the

business combination (Steenkamp and Steenkamp 2016). The standard brings some

fundamental changes in the manner of measuring, recognizing and treating the intangible

assets. Entities that are forced to derecognize some intangible assets such as brand would face

a major impact on their financial statements. This implies that a significant portion of then

value is represented by the intangible assets and brand. The concern is also associated with

the amortization of the intangible assets over its useful life and the intangible assets having

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

INTERNALLY GENERATED INTANGIBLE ASSETS

indefinite life is subjected to the impairment test is expected that AASB 138 would create a

substantial impact on the entities due to the issues related to the difference in accounting

policy (Nichita 2019).

Assessment of the accounting standard AASB 138 can be done in terms of the

changes made to the reported intangible assets. The standard requires the recognition criteria

of intangible assets is deemed to be met by the expenditure resulting from the transactions

relating to the external exchange. The expenditure rules on the internally generated in

tangibles is contrasted sharply by this deeming provision and such expenditure are defined as

research and development and are subjected to set of additional recognition rules. The

acquisition mode of intangible assets is not regarded as the economic feature of intangible

assets and they lack some systematic basis of accounting (Glova et al. 2018).

Conclusion:

The report demonstrating the analysis of the impact of AASB 138 for the internally

generated assets has ascertained that this particular accounting standard lays down certain

specific criteria for recognizing and measuring the good that is generated internally. In

addition to this, the standard also outlines the recognition and measurement of the intangible

assets that is acquired. From the analysis of different measures used for both the sets of

assets, it has been found that there exist differences between the accounting for the acquired

and internally generated intangible assets. In addition to this, it has been also ascertained that

the criteria for recognizing the intangible assets as per this accounting standard make the

firms or the entity reluctant to adopt because of the uncertainty associated with the

recognition of the goodwill as intangible assets. Moreover, the fundamental changes brought

in recognition, measurement and other accounting treatment of the intangible assets has

impacted the company in terms of the accounting policies difference.

INTERNALLY GENERATED INTANGIBLE ASSETS

indefinite life is subjected to the impairment test is expected that AASB 138 would create a

substantial impact on the entities due to the issues related to the difference in accounting

policy (Nichita 2019).

Assessment of the accounting standard AASB 138 can be done in terms of the

changes made to the reported intangible assets. The standard requires the recognition criteria

of intangible assets is deemed to be met by the expenditure resulting from the transactions

relating to the external exchange. The expenditure rules on the internally generated in

tangibles is contrasted sharply by this deeming provision and such expenditure are defined as

research and development and are subjected to set of additional recognition rules. The

acquisition mode of intangible assets is not regarded as the economic feature of intangible

assets and they lack some systematic basis of accounting (Glova et al. 2018).

Conclusion:

The report demonstrating the analysis of the impact of AASB 138 for the internally

generated assets has ascertained that this particular accounting standard lays down certain

specific criteria for recognizing and measuring the good that is generated internally. In

addition to this, the standard also outlines the recognition and measurement of the intangible

assets that is acquired. From the analysis of different measures used for both the sets of

assets, it has been found that there exist differences between the accounting for the acquired

and internally generated intangible assets. In addition to this, it has been also ascertained that

the criteria for recognizing the intangible assets as per this accounting standard make the

firms or the entity reluctant to adopt because of the uncertainty associated with the

recognition of the goodwill as intangible assets. Moreover, the fundamental changes brought

in recognition, measurement and other accounting treatment of the intangible assets has

impacted the company in terms of the accounting policies difference.

11

INTERNALLY GENERATED INTANGIBLE ASSETS

INTERNALLY GENERATED INTANGIBLE ASSETS

12

INTERNALLY GENERATED INTANGIBLE ASSETS

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 3 Jan. 2020].

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Christensen, M., Newberry, S. and Potter, B.N., 2019. Enabling global accounting change:

Epistemic communities and the creation of a ‘more business-like’public sector. Critical

Perspectives on Accounting, 58, pp.53-76.

Cosmulese, C.G.L., Grosu, V. and HLACIUC, E., 2017. Intangible assets with a high degree

of difficulty in estimating their value. Ecoforum Journal, 6(3).

Glova, J., Dancaková, D. and Suleimenova, S., 2018. Managerial aspect of intangibles: own

development or external purchased intangible assets: what does really count?. Polish Journal

of Management Studies, 18.

Iasplus.com., 2020. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 3 Jan. 2020].

Nichita, M.E., 2019. Intangible assets–insights from a literature review. Journal of

Accounting and Management Information Systems, 18(2), pp.224-261.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

INTERNALLY GENERATED INTANGIBLE ASSETS

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-18.pdf

[Accessed 3 Jan. 2020].

Cheung, E. and Lau, J., 2016. Readability of Notes to the Financial Statements and the

Adoption of IFRS. Australian Accounting Review, 26(2), pp.162-176.

Christensen, M., Newberry, S. and Potter, B.N., 2019. Enabling global accounting change:

Epistemic communities and the creation of a ‘more business-like’public sector. Critical

Perspectives on Accounting, 58, pp.53-76.

Cosmulese, C.G.L., Grosu, V. and HLACIUC, E., 2017. Intangible assets with a high degree

of difficulty in estimating their value. Ecoforum Journal, 6(3).

Glova, J., Dancaková, D. and Suleimenova, S., 2018. Managerial aspect of intangibles: own

development or external purchased intangible assets: what does really count?. Polish Journal

of Management Studies, 18.

Iasplus.com., 2020. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 3 Jan. 2020].

Nichita, M.E., 2019. Intangible assets–insights from a literature review. Journal of

Accounting and Management Information Systems, 18(2), pp.224-261.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

INTERNALLY GENERATED INTANGIBLE ASSETS

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions

reducing R&D spending?. Journal of Financial Reporting and Accounting, 14(1), pp.116-

130.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal, 31(2), pp.135-156.

Trent, L. and Mohr, J., 2017. Marketers' Methodologies for Valuing Brand Equity: Insights

into Accounting for Intangible Assets. The CPA Journal, 87(7), pp.58-61.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review

and analysis to inform the debate. Research in Accounting Regulation, 28(1), pp.11-21.

Yaremko, I.J., Pylypenko, L.M. and Tyvonchuk, O.I., 2017. The paradigms of accounting

and financial reporting. International Journal of Synergy and Research, 5, p.135.

INTERNALLY GENERATED INTANGIBLE ASSETS

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions

reducing R&D spending?. Journal of Financial Reporting and Accounting, 14(1), pp.116-

130.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal, 31(2), pp.135-156.

Trent, L. and Mohr, J., 2017. Marketers' Methodologies for Valuing Brand Equity: Insights

into Accounting for Intangible Assets. The CPA Journal, 87(7), pp.58-61.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review

and analysis to inform the debate. Research in Accounting Regulation, 28(1), pp.11-21.

Yaremko, I.J., Pylypenko, L.M. and Tyvonchuk, O.I., 2017. The paradigms of accounting

and financial reporting. International Journal of Synergy and Research, 5, p.135.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.