International Accounting: Recent Developments, MNE's International Financial, Financial Performance Analysis

VerifiedAdded on 2023/01/06

|12

|3617

|20

AI Summary

This document discusses recent developments in international accounting, including convergence and modernization. It also explores key elements of MNE's international financial and analyzes financial performance using accounting ratios. The focus is on IBM Corporation as a case study. The document provides insights into international accounting principles, trends, and harmonization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

International

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

1. Critically discuss two recent developments in the international financial environment.........2

2. Discuss the following key elements of the MNE’s international financial.............................3

3. Analyse the financial performance by using accounting ratio.................................................4

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

1

MAIN BODY..................................................................................................................................2

1. Critically discuss two recent developments in the international financial environment.........2

2. Discuss the following key elements of the MNE’s international financial.............................3

3. Analyse the financial performance by using accounting ratio.................................................4

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

1

INTRODUCTION

International accounting can be defined as international kinds of transactions, along with

such aspects like accounting principles and monitoring practises countries as well as their

categorization; trends of accounting development; global and domestic harmonisation, exchange

rate transcription; foreign currency risk; descriptive statistics of integration accounting and

inflation accounting (Agostini, 2018). This assessment based on IBM (International Business

Machines) Corporation which is an American multinational innovation and consulting firm

headquarters is located in Armonk, New York, with far more than 350,000 workers assisting

customers in 170 countries. This report covers the several such as two recent developments in the

international market, discuss some elements and analyse the company’s financial performance

with the help of accounting ratio.

MAIN BODY

1. Critically discuss two recent developments in the international financial environment

Recent developments in world financial markets have been the speeding up of convergence

and modernization. This growth, fostered by the deregulation of trade, rapid technological

change and significant developments in technology, has developed numerous strong investment

opportunities for companies and communities around the globe. Due to developments in

financial market is impacting on the IBM for individuals and companies would result in an

effective distribution of capital that will, in effect, foster market prosperity and development.

Besides this increasing convergence and integration, financial markets around the world have

also currently undergoing growing default risk. In particular, this trend has been fuelled by the

increase in mergers and acquisitions and utilized buy-outs that have taken place in late-term

markets, not only in the euro zone countries. One element of this securitization process was

rising in industrial issuing bonds that also correlated IBM with a decreasing supply of treasury

securities in many countries, especially the United States.

Other important recent developments in global financial markets include the ongoing

development and success of derivative instruments. The growth of such markets has been largely

due to the fact that rapid developments in technology, financial innovation and financial

assessment have continued to increase both the supply and demand for more advanced and

complicated derivatives instruments. Enhanced this use commodities to adjust overall risk in

2

International accounting can be defined as international kinds of transactions, along with

such aspects like accounting principles and monitoring practises countries as well as their

categorization; trends of accounting development; global and domestic harmonisation, exchange

rate transcription; foreign currency risk; descriptive statistics of integration accounting and

inflation accounting (Agostini, 2018). This assessment based on IBM (International Business

Machines) Corporation which is an American multinational innovation and consulting firm

headquarters is located in Armonk, New York, with far more than 350,000 workers assisting

customers in 170 countries. This report covers the several such as two recent developments in the

international market, discuss some elements and analyse the company’s financial performance

with the help of accounting ratio.

MAIN BODY

1. Critically discuss two recent developments in the international financial environment

Recent developments in world financial markets have been the speeding up of convergence

and modernization. This growth, fostered by the deregulation of trade, rapid technological

change and significant developments in technology, has developed numerous strong investment

opportunities for companies and communities around the globe. Due to developments in

financial market is impacting on the IBM for individuals and companies would result in an

effective distribution of capital that will, in effect, foster market prosperity and development.

Besides this increasing convergence and integration, financial markets around the world have

also currently undergoing growing default risk. In particular, this trend has been fuelled by the

increase in mergers and acquisitions and utilized buy-outs that have taken place in late-term

markets, not only in the euro zone countries. One element of this securitization process was

rising in industrial issuing bonds that also correlated IBM with a decreasing supply of treasury

securities in many countries, especially the United States.

Other important recent developments in global financial markets include the ongoing

development and success of derivative instruments. The growth of such markets has been largely

due to the fact that rapid developments in technology, financial innovation and financial

assessment have continued to increase both the supply and demand for more advanced and

complicated derivatives instruments. Enhanced this use commodities to adjust overall risk in

2

capital sector has also caused an increase in the unsecured notes of unresolved derivative

products seen in recent years, especially in over-the-counter (OTC) financial institutions with

lending rates and equity markets as traded assets (Al Karaawy and Al Baaj, 2018).

These developments impact on the IBM Company in positive manner. Due to changes in

technology Banks have been leaders in developing consumer-facing applications, but broader

digital reinventions in the finance sector have been slower, constrained by issues which include

data protection and privacy. Currently, many institutions are collaborating with IBM to redesign

their problems and institutions new tech finance frameworks, such as the world’s largest first

cloud-ready financial products. Whenever the international bank BNP Paribas started

implementing its digital technology plan, its aim was to provide outstanding solutions to its

clients and business clients whilst maintaining the protection and anonymity of the respondents.

The bank found that it could not digitize fast enough for its current cloud environment. IBM was

asked to founder-create a public infrastructure that would be robust, stable and secure. In future

changes in technology impact on the profitability due to carry out new technology so increase

cost and reduce profit.

Another development impact on the IBM for 'currency-adjusted' or 'currency-adjusted' in the

Management Discourse do not involve operating effects that could arise from variations in

international exchange rates. As we refer to the rate of growth. Constant currency or changing

certain exchange productivity growth is achieved in such a way that such financial statements

can be seen without the effect of foreign exchange rate volatility, thus allowing time span-to-

period comparison of corporate strategy (Abhayawansa, Guthrie and Bernardi, 2019). This

method is used in countries where the usable money is the national currency. Commonly, as the

dollar either increases or diminishes against the other commodities, growth at constant currency

exchange rates or currency changes would be slightly lower than even the growth recorded at

foreign exchange rates. It impact in future in different variations in regard of Currency-adjusted

financial results are determined by converting current period operation into local currency by

using equivalent exchange rate of the previous year's currency.

2. Discuss the following key elements of the MNE’s international financial

Source of Finance: In order to run their operational activities organization required

finance which helps in performing their operations. A firm can manage fund from several

sources and all are different from it (Berger, 2018). It includes equity, debt, debts, retained

3

products seen in recent years, especially in over-the-counter (OTC) financial institutions with

lending rates and equity markets as traded assets (Al Karaawy and Al Baaj, 2018).

These developments impact on the IBM Company in positive manner. Due to changes in

technology Banks have been leaders in developing consumer-facing applications, but broader

digital reinventions in the finance sector have been slower, constrained by issues which include

data protection and privacy. Currently, many institutions are collaborating with IBM to redesign

their problems and institutions new tech finance frameworks, such as the world’s largest first

cloud-ready financial products. Whenever the international bank BNP Paribas started

implementing its digital technology plan, its aim was to provide outstanding solutions to its

clients and business clients whilst maintaining the protection and anonymity of the respondents.

The bank found that it could not digitize fast enough for its current cloud environment. IBM was

asked to founder-create a public infrastructure that would be robust, stable and secure. In future

changes in technology impact on the profitability due to carry out new technology so increase

cost and reduce profit.

Another development impact on the IBM for 'currency-adjusted' or 'currency-adjusted' in the

Management Discourse do not involve operating effects that could arise from variations in

international exchange rates. As we refer to the rate of growth. Constant currency or changing

certain exchange productivity growth is achieved in such a way that such financial statements

can be seen without the effect of foreign exchange rate volatility, thus allowing time span-to-

period comparison of corporate strategy (Abhayawansa, Guthrie and Bernardi, 2019). This

method is used in countries where the usable money is the national currency. Commonly, as the

dollar either increases or diminishes against the other commodities, growth at constant currency

exchange rates or currency changes would be slightly lower than even the growth recorded at

foreign exchange rates. It impact in future in different variations in regard of Currency-adjusted

financial results are determined by converting current period operation into local currency by

using equivalent exchange rate of the previous year's currency.

2. Discuss the following key elements of the MNE’s international financial

Source of Finance: In order to run their operational activities organization required

finance which helps in performing their operations. A firm can manage fund from several

sources and all are different from it (Berger, 2018). It includes equity, debt, debts, retained

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

profits, cash credit, working capital loans, letter of credits, euro problem, venture financing, etc.

Such sources of financing are used in various cases. They are categorised on the basis of time,

ownership rights, and their generational source.

It has been concluded that financial performance is not influenced by the sources of

finance. The study suggests that a mix of financing methods be used to boost the financial

efficiency of organisations instead of focusing on one method of financing. The report also

suggests that government be effective in providing lending facilities to companies, because very

few medium - sized companies have actually used this form of financing. The accessibility of

finance has also been recognised as a major element in the creation, growth and performance of

company. The forms of funding utilised by companies range from original internal factors,

including such proprietor-manager investment accounts and informal income from outside

channels, like financial assistance from family members and friends, commercial credit,

investment funds and angel bankers, and then to structured external sources defined by money

markets such as banks and financial institutions.

Capital structure: The capital structure utilised by the entity to represents the positive

relationship between different long term kinds of capital arrangements like equity, prefernce

shares and retained earnings. As per the IBM's most recent financial statement as reportable on

July 28, 2020, total debt is at $64.74 billion, with $55.45 billion in long-term debt and $9.29

billion in current debt. Modify for $12.04 billion in cash-equivalents, the company has a net debt

of $52.70 billion.

Dividend Policy: It is the policy that a corporation uses to manage its dividend payments

to shareholders. Some scholars say that dividend policy is meaningless, technically, since

investors may sell a part of the stock or portfolios when they need funding in IBM. Dividend

policy is an essential consideration for shareholders to recognize in the inventory-selection

process, since dividends are a significant cash outflow for businesses. However, this might seem

as obvious that even a corporation should still save the money because of its investors rather than

just spending it out.

Financial output is often calculated with the help of net earnings and it can be split into two

types such as dividend and retained earnings (Callao and et.al., 2020). The part of the

firm's retained earnings may also be reinvested although the portion of the dividends is shared to

shareholders who increase their income in IBM. Dividend policies affect the development of

4

Such sources of financing are used in various cases. They are categorised on the basis of time,

ownership rights, and their generational source.

It has been concluded that financial performance is not influenced by the sources of

finance. The study suggests that a mix of financing methods be used to boost the financial

efficiency of organisations instead of focusing on one method of financing. The report also

suggests that government be effective in providing lending facilities to companies, because very

few medium - sized companies have actually used this form of financing. The accessibility of

finance has also been recognised as a major element in the creation, growth and performance of

company. The forms of funding utilised by companies range from original internal factors,

including such proprietor-manager investment accounts and informal income from outside

channels, like financial assistance from family members and friends, commercial credit,

investment funds and angel bankers, and then to structured external sources defined by money

markets such as banks and financial institutions.

Capital structure: The capital structure utilised by the entity to represents the positive

relationship between different long term kinds of capital arrangements like equity, prefernce

shares and retained earnings. As per the IBM's most recent financial statement as reportable on

July 28, 2020, total debt is at $64.74 billion, with $55.45 billion in long-term debt and $9.29

billion in current debt. Modify for $12.04 billion in cash-equivalents, the company has a net debt

of $52.70 billion.

Dividend Policy: It is the policy that a corporation uses to manage its dividend payments

to shareholders. Some scholars say that dividend policy is meaningless, technically, since

investors may sell a part of the stock or portfolios when they need funding in IBM. Dividend

policy is an essential consideration for shareholders to recognize in the inventory-selection

process, since dividends are a significant cash outflow for businesses. However, this might seem

as obvious that even a corporation should still save the money because of its investors rather than

just spending it out.

Financial output is often calculated with the help of net earnings and it can be split into two

types such as dividend and retained earnings (Callao and et.al., 2020). The part of the

firm's retained earnings may also be reinvested although the portion of the dividends is shared to

shareholders who increase their income in IBM. Dividend policies affect the development of

4

small and medium-sized companies, but not large-scale corporations, as shareholders are drawn

to a business which pay-out strategy better fits their investment goals, as investors face various

dividend and capital gain tax treatments and incur costs when selling securities. The positive

relationship is expected between asset returns, dividend policy and revenue growth. Surprisingly,

the study shows that larger GSE firms do less in terms of asset returns. The findings also show

negative correlations among return on assets, dividend pay-out and the leverage ratio in IBM.

3. Analyse the financial performance by using accounting ratio

Profitability ratio:

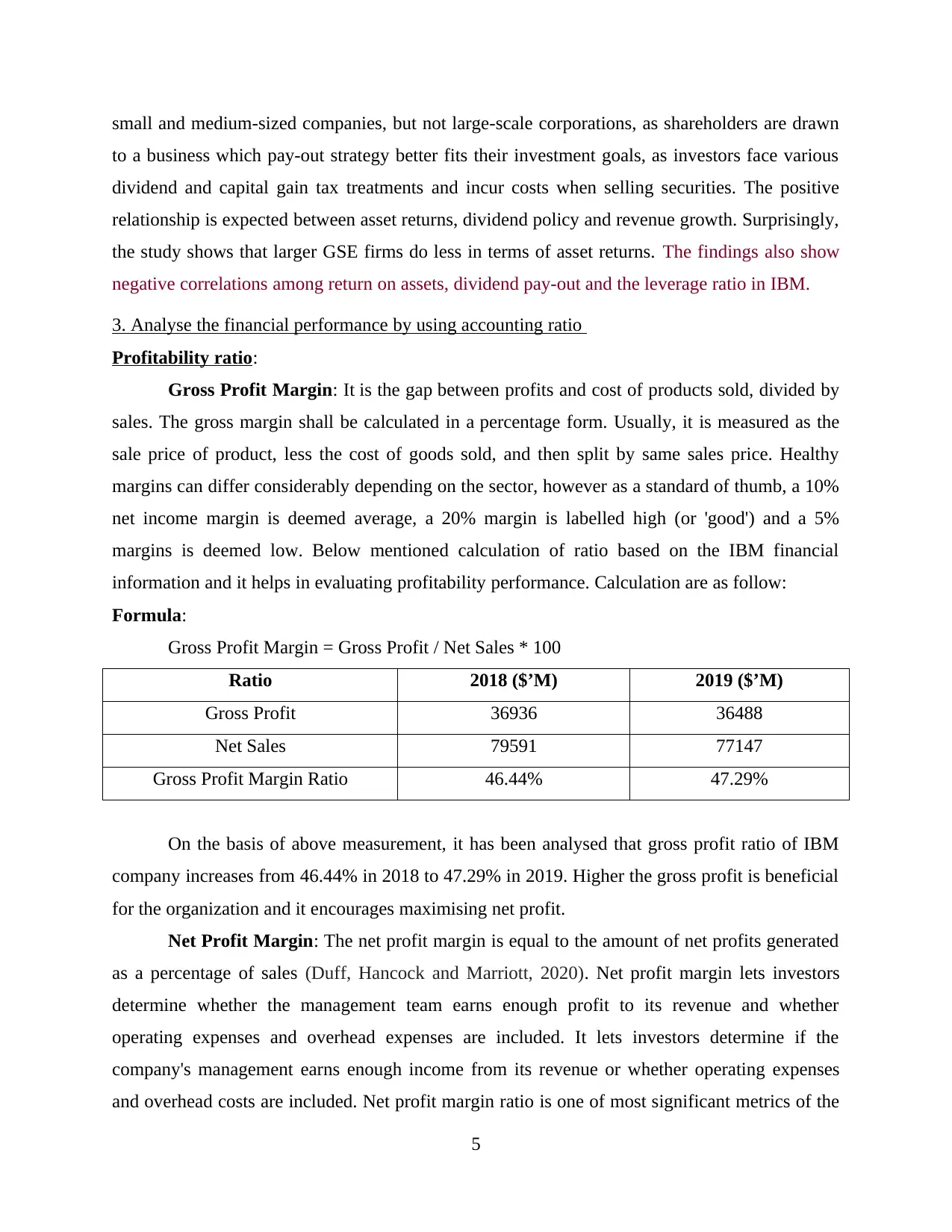

Gross Profit Margin: It is the gap between profits and cost of products sold, divided by

sales. The gross margin shall be calculated in a percentage form. Usually, it is measured as the

sale price of product, less the cost of goods sold, and then split by same sales price. Healthy

margins can differ considerably depending on the sector, however as a standard of thumb, a 10%

net income margin is deemed average, a 20% margin is labelled high (or 'good') and a 5%

margins is deemed low. Below mentioned calculation of ratio based on the IBM financial

information and it helps in evaluating profitability performance. Calculation are as follow:

Formula:

Gross Profit Margin = Gross Profit / Net Sales * 100

Ratio 2018 ($’M) 2019 ($’M)

Gross Profit 36936 36488

Net Sales 79591 77147

Gross Profit Margin Ratio 46.44% 47.29%

On the basis of above measurement, it has been analysed that gross profit ratio of IBM

company increases from 46.44% in 2018 to 47.29% in 2019. Higher the gross profit is beneficial

for the organization and it encourages maximising net profit.

Net Profit Margin: The net profit margin is equal to the amount of net profits generated

as a percentage of sales (Duff, Hancock and Marriott, 2020). Net profit margin lets investors

determine whether the management team earns enough profit to its revenue and whether

operating expenses and overhead expenses are included. It lets investors determine if the

company's management earns enough income from its revenue or whether operating expenses

and overhead costs are included. Net profit margin ratio is one of most significant metrics of the

5

to a business which pay-out strategy better fits their investment goals, as investors face various

dividend and capital gain tax treatments and incur costs when selling securities. The positive

relationship is expected between asset returns, dividend policy and revenue growth. Surprisingly,

the study shows that larger GSE firms do less in terms of asset returns. The findings also show

negative correlations among return on assets, dividend pay-out and the leverage ratio in IBM.

3. Analyse the financial performance by using accounting ratio

Profitability ratio:

Gross Profit Margin: It is the gap between profits and cost of products sold, divided by

sales. The gross margin shall be calculated in a percentage form. Usually, it is measured as the

sale price of product, less the cost of goods sold, and then split by same sales price. Healthy

margins can differ considerably depending on the sector, however as a standard of thumb, a 10%

net income margin is deemed average, a 20% margin is labelled high (or 'good') and a 5%

margins is deemed low. Below mentioned calculation of ratio based on the IBM financial

information and it helps in evaluating profitability performance. Calculation are as follow:

Formula:

Gross Profit Margin = Gross Profit / Net Sales * 100

Ratio 2018 ($’M) 2019 ($’M)

Gross Profit 36936 36488

Net Sales 79591 77147

Gross Profit Margin Ratio 46.44% 47.29%

On the basis of above measurement, it has been analysed that gross profit ratio of IBM

company increases from 46.44% in 2018 to 47.29% in 2019. Higher the gross profit is beneficial

for the organization and it encourages maximising net profit.

Net Profit Margin: The net profit margin is equal to the amount of net profits generated

as a percentage of sales (Duff, Hancock and Marriott, 2020). Net profit margin lets investors

determine whether the management team earns enough profit to its revenue and whether

operating expenses and overhead expenses are included. It lets investors determine if the

company's management earns enough income from its revenue or whether operating expenses

and overhead costs are included. Net profit margin ratio is one of most significant metrics of the

5

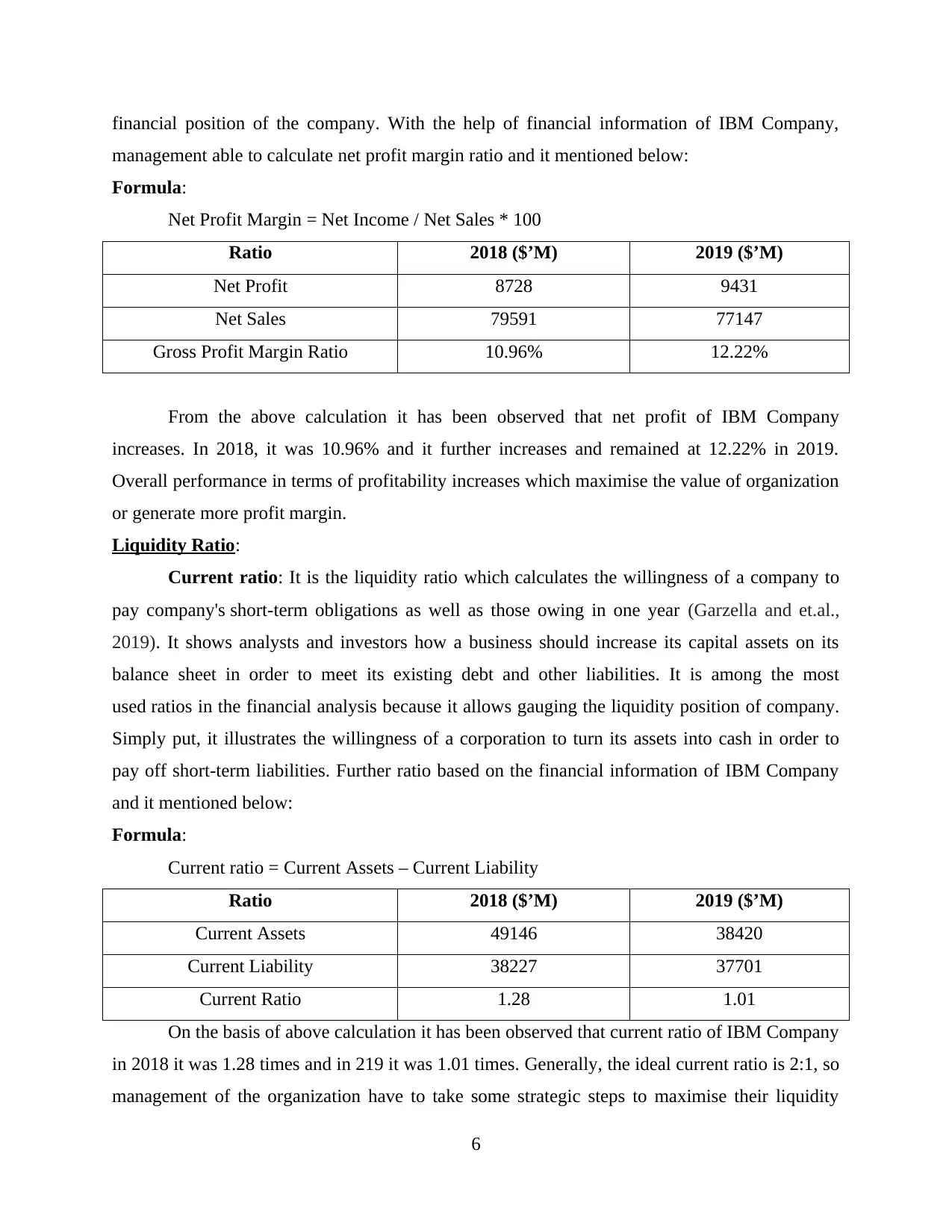

financial position of the company. With the help of financial information of IBM Company,

management able to calculate net profit margin ratio and it mentioned below:

Formula:

Net Profit Margin = Net Income / Net Sales * 100

Ratio 2018 ($’M) 2019 ($’M)

Net Profit 8728 9431

Net Sales 79591 77147

Gross Profit Margin Ratio 10.96% 12.22%

From the above calculation it has been observed that net profit of IBM Company

increases. In 2018, it was 10.96% and it further increases and remained at 12.22% in 2019.

Overall performance in terms of profitability increases which maximise the value of organization

or generate more profit margin.

Liquidity Ratio:

Current ratio: It is the liquidity ratio which calculates the willingness of a company to

pay company's short-term obligations as well as those owing in one year (Garzella and et.al.,

2019). It shows analysts and investors how a business should increase its capital assets on its

balance sheet in order to meet its existing debt and other liabilities. It is among the most

used ratios in the financial analysis because it allows gauging the liquidity position of company.

Simply put, it illustrates the willingness of a corporation to turn its assets into cash in order to

pay off short-term liabilities. Further ratio based on the financial information of IBM Company

and it mentioned below:

Formula:

Current ratio = Current Assets – Current Liability

Ratio 2018 ($’M) 2019 ($’M)

Current Assets 49146 38420

Current Liability 38227 37701

Current Ratio 1.28 1.01

On the basis of above calculation it has been observed that current ratio of IBM Company

in 2018 it was 1.28 times and in 219 it was 1.01 times. Generally, the ideal current ratio is 2:1, so

management of the organization have to take some strategic steps to maximise their liquidity

6

management able to calculate net profit margin ratio and it mentioned below:

Formula:

Net Profit Margin = Net Income / Net Sales * 100

Ratio 2018 ($’M) 2019 ($’M)

Net Profit 8728 9431

Net Sales 79591 77147

Gross Profit Margin Ratio 10.96% 12.22%

From the above calculation it has been observed that net profit of IBM Company

increases. In 2018, it was 10.96% and it further increases and remained at 12.22% in 2019.

Overall performance in terms of profitability increases which maximise the value of organization

or generate more profit margin.

Liquidity Ratio:

Current ratio: It is the liquidity ratio which calculates the willingness of a company to

pay company's short-term obligations as well as those owing in one year (Garzella and et.al.,

2019). It shows analysts and investors how a business should increase its capital assets on its

balance sheet in order to meet its existing debt and other liabilities. It is among the most

used ratios in the financial analysis because it allows gauging the liquidity position of company.

Simply put, it illustrates the willingness of a corporation to turn its assets into cash in order to

pay off short-term liabilities. Further ratio based on the financial information of IBM Company

and it mentioned below:

Formula:

Current ratio = Current Assets – Current Liability

Ratio 2018 ($’M) 2019 ($’M)

Current Assets 49146 38420

Current Liability 38227 37701

Current Ratio 1.28 1.01

On the basis of above calculation it has been observed that current ratio of IBM Company

in 2018 it was 1.28 times and in 219 it was 1.01 times. Generally, the ideal current ratio is 2:1, so

management of the organization have to take some strategic steps to maximise their liquidity

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

position. It helps in performing their daily basis operational activities or pay off their short term

obligations.

Acid test ratio: It is called quick ratio, measures the firm's mostly short-term assets to

the most short-term liabilities to see whether the company will have enough capital to pay for its

current liabilities, including such short-term debt (Kieso, Weygandt and Warfield, 2020). That

acid test ratio ignores current assets which are risky rapidly, like inventory. The quick ratio

shows the willingness of a firm to cover its existing liabilities before selling its inventory or seek

additional finance. It is known to be a more optimistic indicator than that of the current ratio,

which uses all current assets value as compensation for current liabilities. Below mentioned

calculation based on the IBM Company’s financial performance and ratio calculation is as

follow:

Formula:

Acid test ratio = Quick assets / Current liability

Ratio 2018 ($’M) 2019 ($’M)

Quick Assets 45086 34700

Current Liability 38227 37701

Acid Test Ratio 1.177 0.920

* Quick Assets = Current Assets – Inventory – Prepaid expenses

2018 = 49146 – 1682 – 2378

= 45086

2019 = 38420 – 1619 – 2101

= 34700

On the basis of above ratio calculation, it has been analysed that acid test ratio in 2018

was 1.177 and in 2019 it was 0.920. Overall liquidity position of IBM Company reduces from

2018 to 2019 period. Ideal ratio of this ratio is 1:1 and management should ensure that company

maintain their assets and liability in this portion to meet their current liability in short period.

Efficiency Ratio:

Inventory Turnover: This is the ratio that indicates how many times a business has

sold and replaced inventory over a specified timeframe (Kotsupatriy and et.al., 2020). A business

may then split the days throughout the period by both the inventory turnover equation in order to

7

obligations.

Acid test ratio: It is called quick ratio, measures the firm's mostly short-term assets to

the most short-term liabilities to see whether the company will have enough capital to pay for its

current liabilities, including such short-term debt (Kieso, Weygandt and Warfield, 2020). That

acid test ratio ignores current assets which are risky rapidly, like inventory. The quick ratio

shows the willingness of a firm to cover its existing liabilities before selling its inventory or seek

additional finance. It is known to be a more optimistic indicator than that of the current ratio,

which uses all current assets value as compensation for current liabilities. Below mentioned

calculation based on the IBM Company’s financial performance and ratio calculation is as

follow:

Formula:

Acid test ratio = Quick assets / Current liability

Ratio 2018 ($’M) 2019 ($’M)

Quick Assets 45086 34700

Current Liability 38227 37701

Acid Test Ratio 1.177 0.920

* Quick Assets = Current Assets – Inventory – Prepaid expenses

2018 = 49146 – 1682 – 2378

= 45086

2019 = 38420 – 1619 – 2101

= 34700

On the basis of above ratio calculation, it has been analysed that acid test ratio in 2018

was 1.177 and in 2019 it was 0.920. Overall liquidity position of IBM Company reduces from

2018 to 2019 period. Ideal ratio of this ratio is 1:1 and management should ensure that company

maintain their assets and liability in this portion to meet their current liability in short period.

Efficiency Ratio:

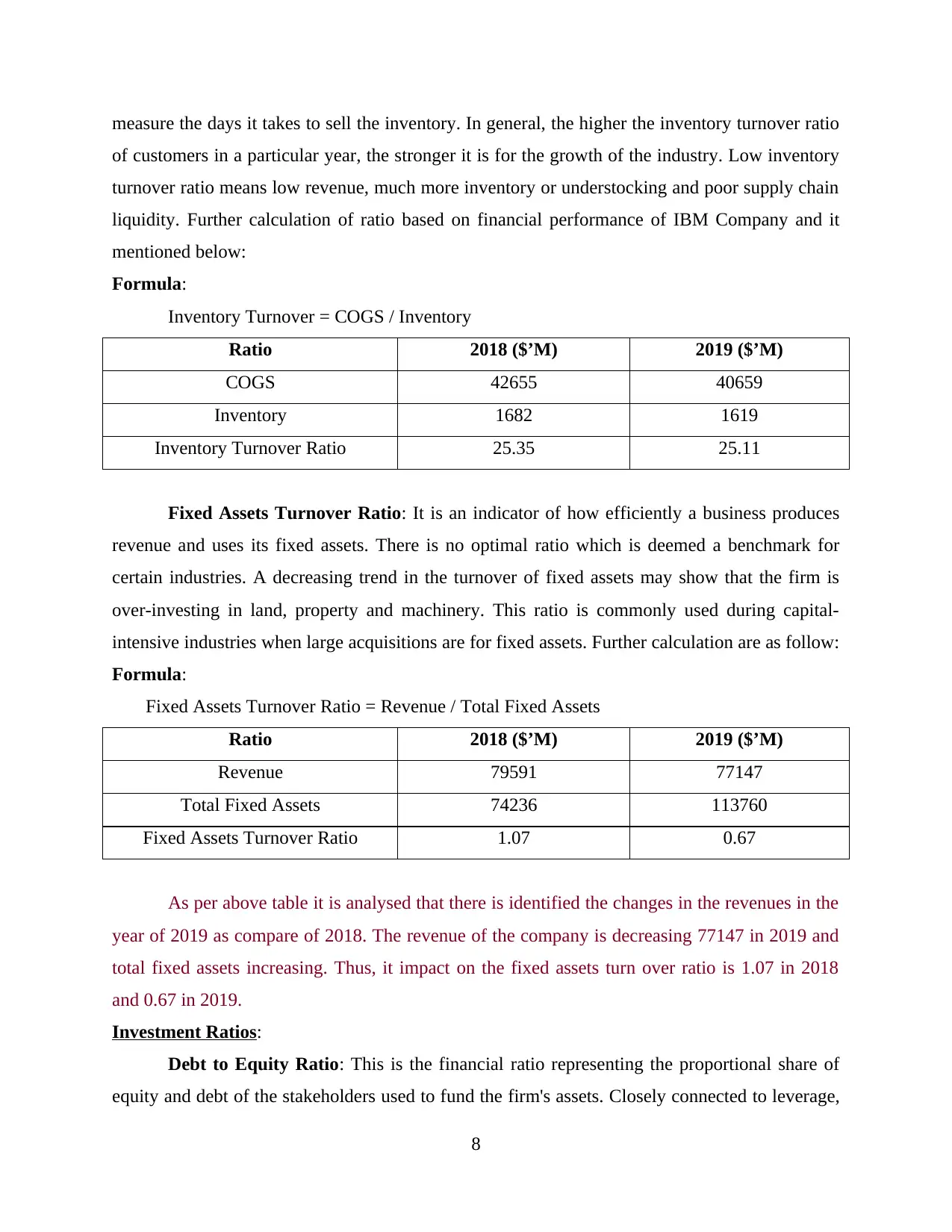

Inventory Turnover: This is the ratio that indicates how many times a business has

sold and replaced inventory over a specified timeframe (Kotsupatriy and et.al., 2020). A business

may then split the days throughout the period by both the inventory turnover equation in order to

7

measure the days it takes to sell the inventory. In general, the higher the inventory turnover ratio

of customers in a particular year, the stronger it is for the growth of the industry. Low inventory

turnover ratio means low revenue, much more inventory or understocking and poor supply chain

liquidity. Further calculation of ratio based on financial performance of IBM Company and it

mentioned below:

Formula:

Inventory Turnover = COGS / Inventory

Ratio 2018 ($’M) 2019 ($’M)

COGS 42655 40659

Inventory 1682 1619

Inventory Turnover Ratio 25.35 25.11

Fixed Assets Turnover Ratio: It is an indicator of how efficiently a business produces

revenue and uses its fixed assets. There is no optimal ratio which is deemed a benchmark for

certain industries. A decreasing trend in the turnover of fixed assets may show that the firm is

over-investing in land, property and machinery. This ratio is commonly used during capital-

intensive industries when large acquisitions are for fixed assets. Further calculation are as follow:

Formula:

Fixed Assets Turnover Ratio = Revenue / Total Fixed Assets

Ratio 2018 ($’M) 2019 ($’M)

Revenue 79591 77147

Total Fixed Assets 74236 113760

Fixed Assets Turnover Ratio 1.07 0.67

As per above table it is analysed that there is identified the changes in the revenues in the

year of 2019 as compare of 2018. The revenue of the company is decreasing 77147 in 2019 and

total fixed assets increasing. Thus, it impact on the fixed assets turn over ratio is 1.07 in 2018

and 0.67 in 2019.

Investment Ratios:

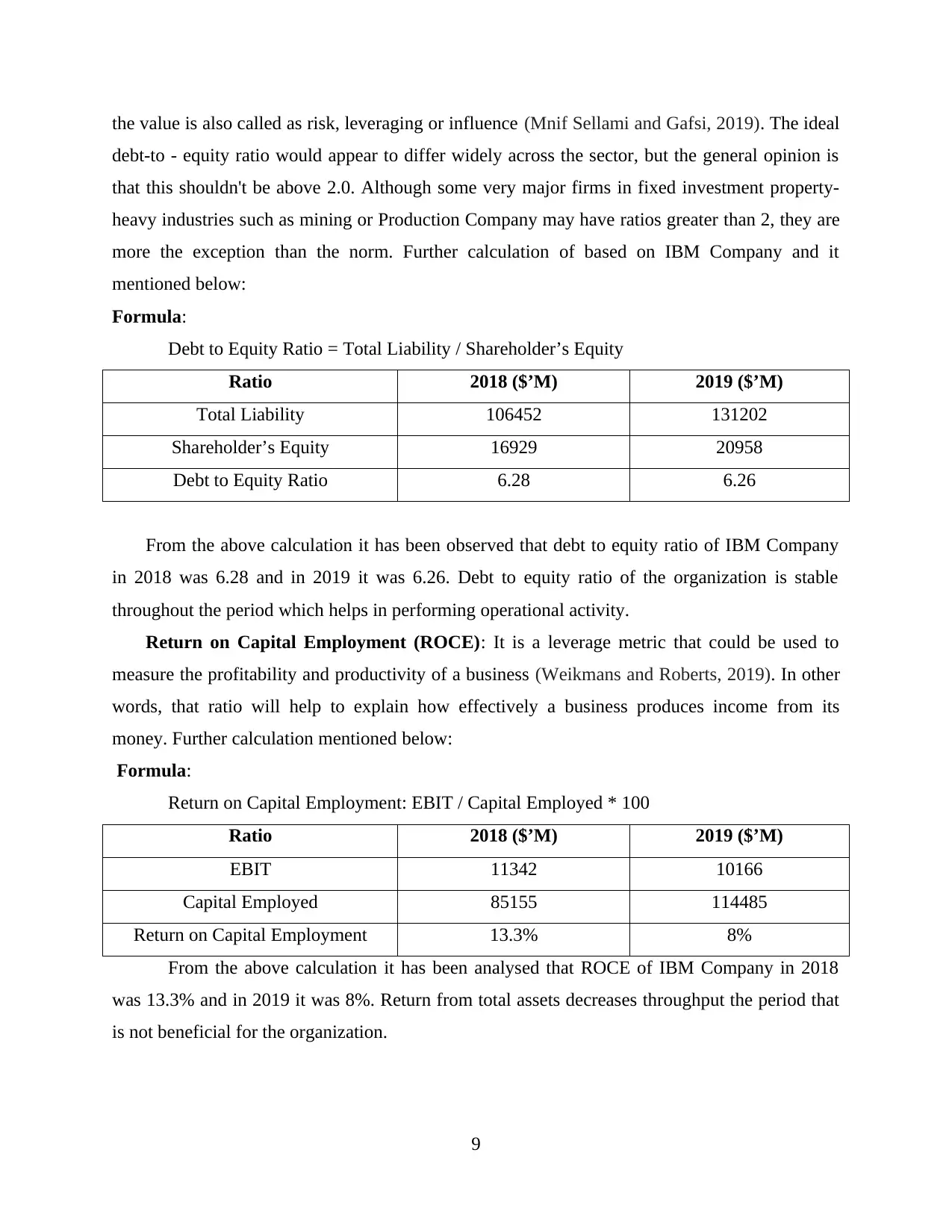

Debt to Equity Ratio: This is the financial ratio representing the proportional share of

equity and debt of the stakeholders used to fund the firm's assets. Closely connected to leverage,

8

of customers in a particular year, the stronger it is for the growth of the industry. Low inventory

turnover ratio means low revenue, much more inventory or understocking and poor supply chain

liquidity. Further calculation of ratio based on financial performance of IBM Company and it

mentioned below:

Formula:

Inventory Turnover = COGS / Inventory

Ratio 2018 ($’M) 2019 ($’M)

COGS 42655 40659

Inventory 1682 1619

Inventory Turnover Ratio 25.35 25.11

Fixed Assets Turnover Ratio: It is an indicator of how efficiently a business produces

revenue and uses its fixed assets. There is no optimal ratio which is deemed a benchmark for

certain industries. A decreasing trend in the turnover of fixed assets may show that the firm is

over-investing in land, property and machinery. This ratio is commonly used during capital-

intensive industries when large acquisitions are for fixed assets. Further calculation are as follow:

Formula:

Fixed Assets Turnover Ratio = Revenue / Total Fixed Assets

Ratio 2018 ($’M) 2019 ($’M)

Revenue 79591 77147

Total Fixed Assets 74236 113760

Fixed Assets Turnover Ratio 1.07 0.67

As per above table it is analysed that there is identified the changes in the revenues in the

year of 2019 as compare of 2018. The revenue of the company is decreasing 77147 in 2019 and

total fixed assets increasing. Thus, it impact on the fixed assets turn over ratio is 1.07 in 2018

and 0.67 in 2019.

Investment Ratios:

Debt to Equity Ratio: This is the financial ratio representing the proportional share of

equity and debt of the stakeholders used to fund the firm's assets. Closely connected to leverage,

8

the value is also called as risk, leveraging or influence (Mnif Sellami and Gafsi, 2019). The ideal

debt-to - equity ratio would appear to differ widely across the sector, but the general opinion is

that this shouldn't be above 2.0. Although some very major firms in fixed investment property-

heavy industries such as mining or Production Company may have ratios greater than 2, they are

more the exception than the norm. Further calculation of based on IBM Company and it

mentioned below:

Formula:

Debt to Equity Ratio = Total Liability / Shareholder’s Equity

Ratio 2018 ($’M) 2019 ($’M)

Total Liability 106452 131202

Shareholder’s Equity 16929 20958

Debt to Equity Ratio 6.28 6.26

From the above calculation it has been observed that debt to equity ratio of IBM Company

in 2018 was 6.28 and in 2019 it was 6.26. Debt to equity ratio of the organization is stable

throughout the period which helps in performing operational activity.

Return on Capital Employment (ROCE): It is a leverage metric that could be used to

measure the profitability and productivity of a business (Weikmans and Roberts, 2019). In other

words, that ratio will help to explain how effectively a business produces income from its

money. Further calculation mentioned below:

Formula:

Return on Capital Employment: EBIT / Capital Employed * 100

Ratio 2018 ($’M) 2019 ($’M)

EBIT 11342 10166

Capital Employed 85155 114485

Return on Capital Employment 13.3% 8%

From the above calculation it has been analysed that ROCE of IBM Company in 2018

was 13.3% and in 2019 it was 8%. Return from total assets decreases throughput the period that

is not beneficial for the organization.

9

debt-to - equity ratio would appear to differ widely across the sector, but the general opinion is

that this shouldn't be above 2.0. Although some very major firms in fixed investment property-

heavy industries such as mining or Production Company may have ratios greater than 2, they are

more the exception than the norm. Further calculation of based on IBM Company and it

mentioned below:

Formula:

Debt to Equity Ratio = Total Liability / Shareholder’s Equity

Ratio 2018 ($’M) 2019 ($’M)

Total Liability 106452 131202

Shareholder’s Equity 16929 20958

Debt to Equity Ratio 6.28 6.26

From the above calculation it has been observed that debt to equity ratio of IBM Company

in 2018 was 6.28 and in 2019 it was 6.26. Debt to equity ratio of the organization is stable

throughout the period which helps in performing operational activity.

Return on Capital Employment (ROCE): It is a leverage metric that could be used to

measure the profitability and productivity of a business (Weikmans and Roberts, 2019). In other

words, that ratio will help to explain how effectively a business produces income from its

money. Further calculation mentioned below:

Formula:

Return on Capital Employment: EBIT / Capital Employed * 100

Ratio 2018 ($’M) 2019 ($’M)

EBIT 11342 10166

Capital Employed 85155 114485

Return on Capital Employment 13.3% 8%

From the above calculation it has been analysed that ROCE of IBM Company in 2018

was 13.3% and in 2019 it was 8%. Return from total assets decreases throughput the period that

is not beneficial for the organization.

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above discussion it has been observe that accounting is very important for the

organization, without it organizations unable to evaluate company’s performance in terms of

revenue or expenditures. In addition, in order to evaluate the financial performance of the

organization, management has to use accounting ratios which allow understanding business

performance in terms of profitability, liquidity, efficiency and investment. With the help of it,

business managers and several stakeholders are able to evaluate company’s performance and

make their future decisions accordingly.

10

From the above discussion it has been observe that accounting is very important for the

organization, without it organizations unable to evaluate company’s performance in terms of

revenue or expenditures. In addition, in order to evaluate the financial performance of the

organization, management has to use accounting ratios which allow understanding business

performance in terms of profitability, liquidity, efficiency and investment. With the help of it,

business managers and several stakeholders are able to evaluate company’s performance and

make their future decisions accordingly.

10

REFERENCES

Books & Journals

Abhayawansa, S., Guthrie, J. and Bernardi, C., 2019. Intellectual capital accounting in the age of

integrated reporting: a commentary. Journal of Intellectual Capital.

Agostini, M., 2018. The International Accounting Convergence Promoted by IASB and FASB

Regarding Going Concern Status. In Corporate Financial Distress (pp. 99-118).

Palgrave Pivot, Cham.

Al Karaawy, N. A. A. and Al Baaj, Q. M. A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal. 22(1). pp.1-16.

Berger, T. M. M., 2018. IPSAS explained: A summary of international public sector accounting

standards. John Wiley & Sons.

Callao, S. and et.al., 2020. International Accounting Standards: Transparency, Disclosure and

Valuation for Latin America and the Caribbean. IDB Publications (Books).

Duff, A., Hancock, P. and Marriott, N., 2020. The role and impact of professional accountancy

associations on accounting education research: An international study. The British

Accounting Review, 52(5), p.100829.

Garzella, S. and et.al., 2019. The (in) coherence in accounting for goodwill: Implications for a

revision of international accounting standards. Meditari Accountancy Research, 28(2),

pp.311-325.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2020. Intermediate accounting IFRS. John

Wiley & Sons.

Kotsupatriy, M. and et.al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management, 11(5).

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration, 42(2), pp.119-131.

Weikmans, R. and Roberts, J. T., 2019. The international climate finance accounting muddle: is

there hope on the horizon?. Climate and Development, 11(2), pp.97-111.

Online

Annual Report of IBM. 2019. [Online]. Available Through:

<https://www.ibm.com/annualreport/assets/downloads/IBM_Annual_Report_2019.pdf>

11

Books & Journals

Abhayawansa, S., Guthrie, J. and Bernardi, C., 2019. Intellectual capital accounting in the age of

integrated reporting: a commentary. Journal of Intellectual Capital.

Agostini, M., 2018. The International Accounting Convergence Promoted by IASB and FASB

Regarding Going Concern Status. In Corporate Financial Distress (pp. 99-118).

Palgrave Pivot, Cham.

Al Karaawy, N. A. A. and Al Baaj, Q. M. A., 2018. Taxation of international business

organizations. Academy of Accounting and Financial Studies Journal. 22(1). pp.1-16.

Berger, T. M. M., 2018. IPSAS explained: A summary of international public sector accounting

standards. John Wiley & Sons.

Callao, S. and et.al., 2020. International Accounting Standards: Transparency, Disclosure and

Valuation for Latin America and the Caribbean. IDB Publications (Books).

Duff, A., Hancock, P. and Marriott, N., 2020. The role and impact of professional accountancy

associations on accounting education research: An international study. The British

Accounting Review, 52(5), p.100829.

Garzella, S. and et.al., 2019. The (in) coherence in accounting for goodwill: Implications for a

revision of international accounting standards. Meditari Accountancy Research, 28(2),

pp.311-325.

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2020. Intermediate accounting IFRS. John

Wiley & Sons.

Kotsupatriy, M. and et.al., 2020. Use of international accounting and financial reporting

standards in enterprise management. International Journal of Management, 11(5).

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration, 42(2), pp.119-131.

Weikmans, R. and Roberts, J. T., 2019. The international climate finance accounting muddle: is

there hope on the horizon?. Climate and Development, 11(2), pp.97-111.

Online

Annual Report of IBM. 2019. [Online]. Available Through:

<https://www.ibm.com/annualreport/assets/downloads/IBM_Annual_Report_2019.pdf>

11

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.