International Accounting: Analysis of Accounts, IAS 16, IAS 36, IAS 38

VerifiedAdded on 2023/01/16

|10

|1540

|22

AI Summary

This document provides an analysis of accounts, along with explanations of IAS 16, IAS 36, and IAS 38 in the context of international accounting. It covers topics such as chart of accounts, fixed assets, impairment of assets, and intangible assets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

International

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

TASK..................................................................................................................................3

Question 1. Accounting:.................................................................................................3

Question 2. IAS 16- Fixed Assets:.................................................................................5

Question 3. IAS 36. Impairment of assets:....................................................................6

Question 4. IAS 38. Intangible Assets:..........................................................................7

REFERENCES................................................................................................................10

TASK..................................................................................................................................3

Question 1. Accounting:.................................................................................................3

Question 2. IAS 16- Fixed Assets:.................................................................................5

Question 3. IAS 36. Impairment of assets:....................................................................6

Question 4. IAS 38. Intangible Assets:..........................................................................7

REFERENCES................................................................................................................10

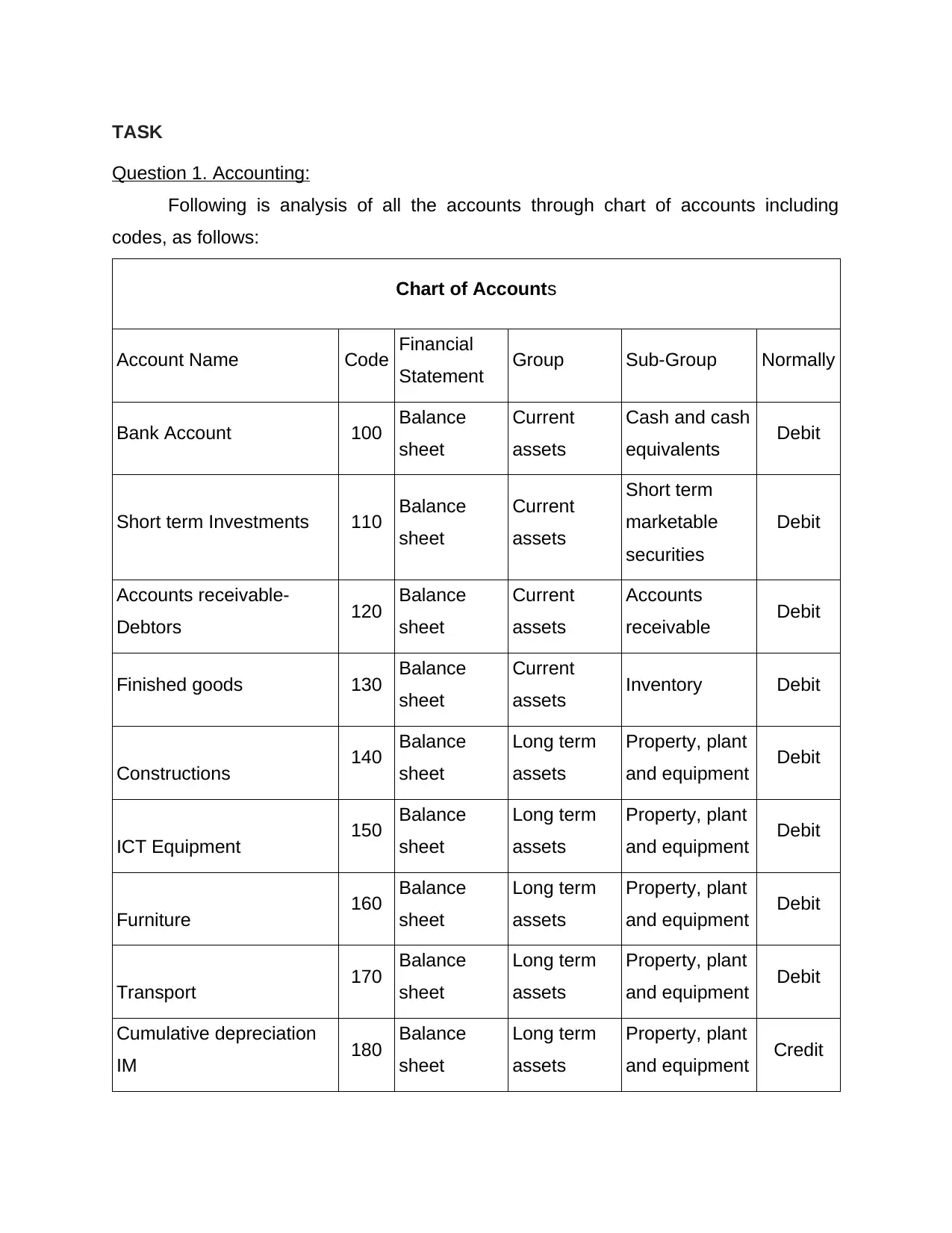

TASK

Question 1. Accounting:

Following is analysis of all the accounts through chart of accounts including

codes, as follows:

Chart of Accounts

Account Name Code Financial

Statement Group Sub-Group Normally

Bank Account 100 Balance

sheet

Current

assets

Cash and cash

equivalents Debit

Short term Investments 110 Balance

sheet

Current

assets

Short term

marketable

securities

Debit

Accounts receivable-

Debtors 120 Balance

sheet

Current

assets

Accounts

receivable Debit

Finished goods 130 Balance

sheet

Current

assets Inventory Debit

Constructions 140 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

ICT Equipment 150 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Furniture 160 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Transport 170 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Cumulative depreciation

IM 180 Balance

sheet

Long term

assets

Property, plant

and equipment Credit

Question 1. Accounting:

Following is analysis of all the accounts through chart of accounts including

codes, as follows:

Chart of Accounts

Account Name Code Financial

Statement Group Sub-Group Normally

Bank Account 100 Balance

sheet

Current

assets

Cash and cash

equivalents Debit

Short term Investments 110 Balance

sheet

Current

assets

Short term

marketable

securities

Debit

Accounts receivable-

Debtors 120 Balance

sheet

Current

assets

Accounts

receivable Debit

Finished goods 130 Balance

sheet

Current

assets Inventory Debit

Constructions 140 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

ICT Equipment 150 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Furniture 160 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Transport 170 Balance

sheet

Long term

assets

Property, plant

and equipment Debit

Cumulative depreciation

IM 180 Balance

sheet

Long term

assets

Property, plant

and equipment Credit

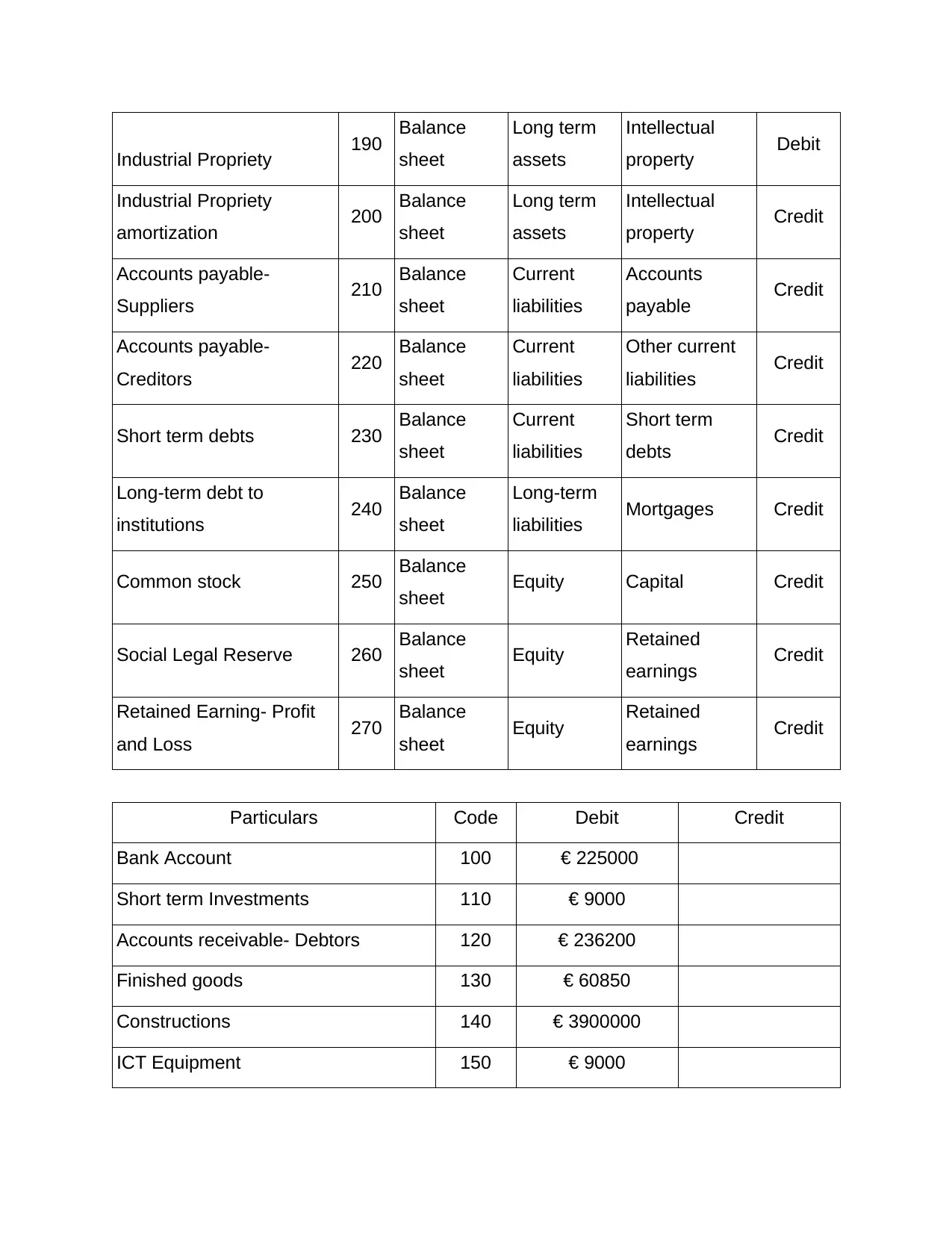

Industrial Propriety 190 Balance

sheet

Long term

assets

Intellectual

property Debit

Industrial Propriety

amortization 200 Balance

sheet

Long term

assets

Intellectual

property Credit

Accounts payable-

Suppliers 210 Balance

sheet

Current

liabilities

Accounts

payable Credit

Accounts payable-

Creditors 220 Balance

sheet

Current

liabilities

Other current

liabilities Credit

Short term debts 230 Balance

sheet

Current

liabilities

Short term

debts Credit

Long-term debt to

institutions 240 Balance

sheet

Long-term

liabilities Mortgages Credit

Common stock 250 Balance

sheet Equity Capital Credit

Social Legal Reserve 260 Balance

sheet Equity Retained

earnings Credit

Retained Earning- Profit

and Loss 270 Balance

sheet Equity Retained

earnings Credit

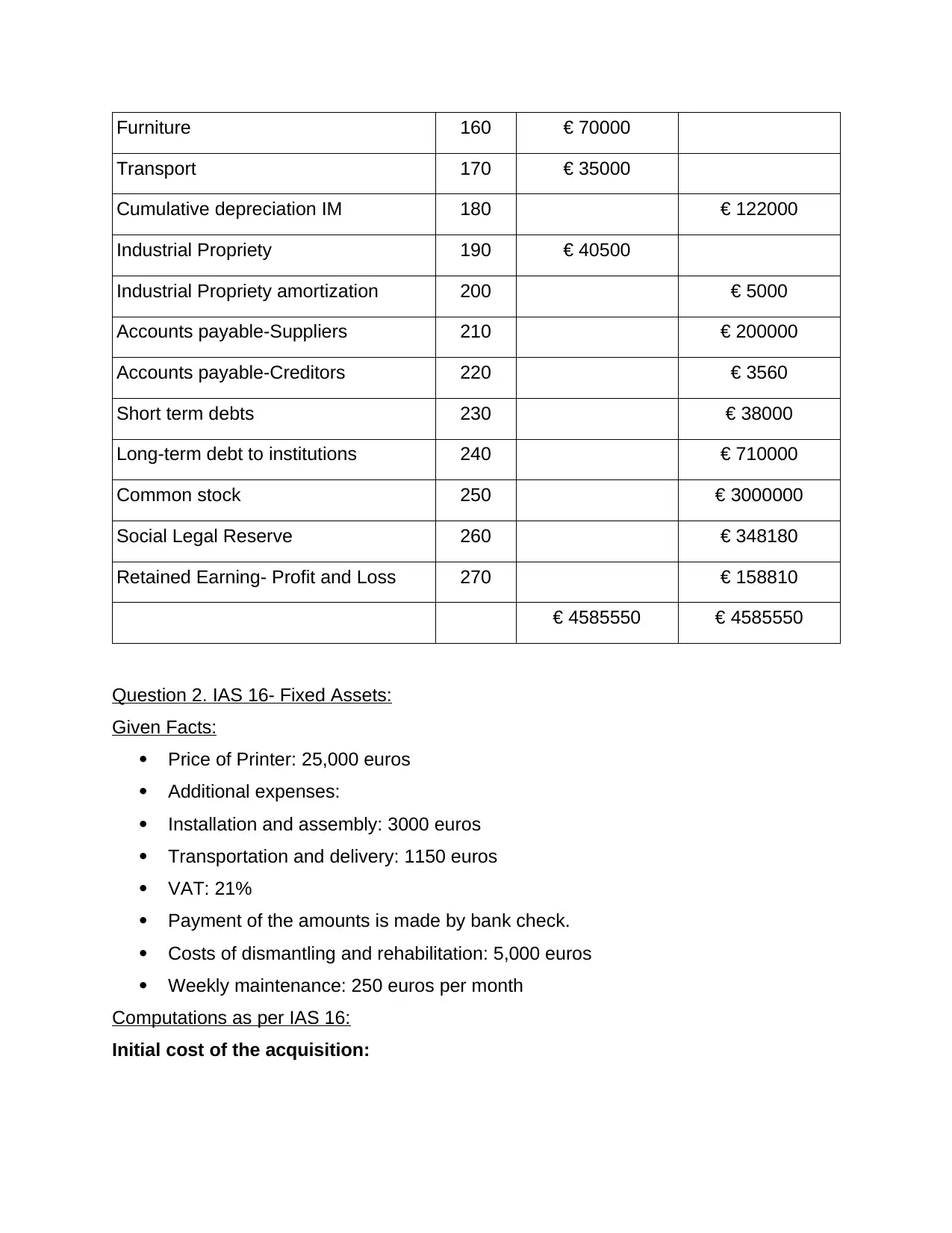

Particulars Code Debit Credit

Bank Account 100 € 225000

Short term Investments 110 € 9000

Accounts receivable- Debtors 120 € 236200

Finished goods 130 € 60850

Constructions 140 € 3900000

ICT Equipment 150 € 9000

sheet

Long term

assets

Intellectual

property Debit

Industrial Propriety

amortization 200 Balance

sheet

Long term

assets

Intellectual

property Credit

Accounts payable-

Suppliers 210 Balance

sheet

Current

liabilities

Accounts

payable Credit

Accounts payable-

Creditors 220 Balance

sheet

Current

liabilities

Other current

liabilities Credit

Short term debts 230 Balance

sheet

Current

liabilities

Short term

debts Credit

Long-term debt to

institutions 240 Balance

sheet

Long-term

liabilities Mortgages Credit

Common stock 250 Balance

sheet Equity Capital Credit

Social Legal Reserve 260 Balance

sheet Equity Retained

earnings Credit

Retained Earning- Profit

and Loss 270 Balance

sheet Equity Retained

earnings Credit

Particulars Code Debit Credit

Bank Account 100 € 225000

Short term Investments 110 € 9000

Accounts receivable- Debtors 120 € 236200

Finished goods 130 € 60850

Constructions 140 € 3900000

ICT Equipment 150 € 9000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Furniture 160 € 70000

Transport 170 € 35000

Cumulative depreciation IM 180 € 122000

Industrial Propriety 190 € 40500

Industrial Propriety amortization 200 € 5000

Accounts payable-Suppliers 210 € 200000

Accounts payable-Creditors 220 € 3560

Short term debts 230 € 38000

Long-term debt to institutions 240 € 710000

Common stock 250 € 3000000

Social Legal Reserve 260 € 348180

Retained Earning- Profit and Loss 270 € 158810

€ 4585550 € 4585550

Question 2. IAS 16- Fixed Assets:

Given Facts:

Price of Printer: 25,000 euros

Additional expenses:

Installation and assembly: 3000 euros

Transportation and delivery: 1150 euros

VAT: 21%

Payment of the amounts is made by bank check.

Costs of dismantling and rehabilitation: 5,000 euros

Weekly maintenance: 250 euros per month

Computations as per IAS 16:

Initial cost of the acquisition:

Transport 170 € 35000

Cumulative depreciation IM 180 € 122000

Industrial Propriety 190 € 40500

Industrial Propriety amortization 200 € 5000

Accounts payable-Suppliers 210 € 200000

Accounts payable-Creditors 220 € 3560

Short term debts 230 € 38000

Long-term debt to institutions 240 € 710000

Common stock 250 € 3000000

Social Legal Reserve 260 € 348180

Retained Earning- Profit and Loss 270 € 158810

€ 4585550 € 4585550

Question 2. IAS 16- Fixed Assets:

Given Facts:

Price of Printer: 25,000 euros

Additional expenses:

Installation and assembly: 3000 euros

Transportation and delivery: 1150 euros

VAT: 21%

Payment of the amounts is made by bank check.

Costs of dismantling and rehabilitation: 5,000 euros

Weekly maintenance: 250 euros per month

Computations as per IAS 16:

Initial cost of the acquisition:

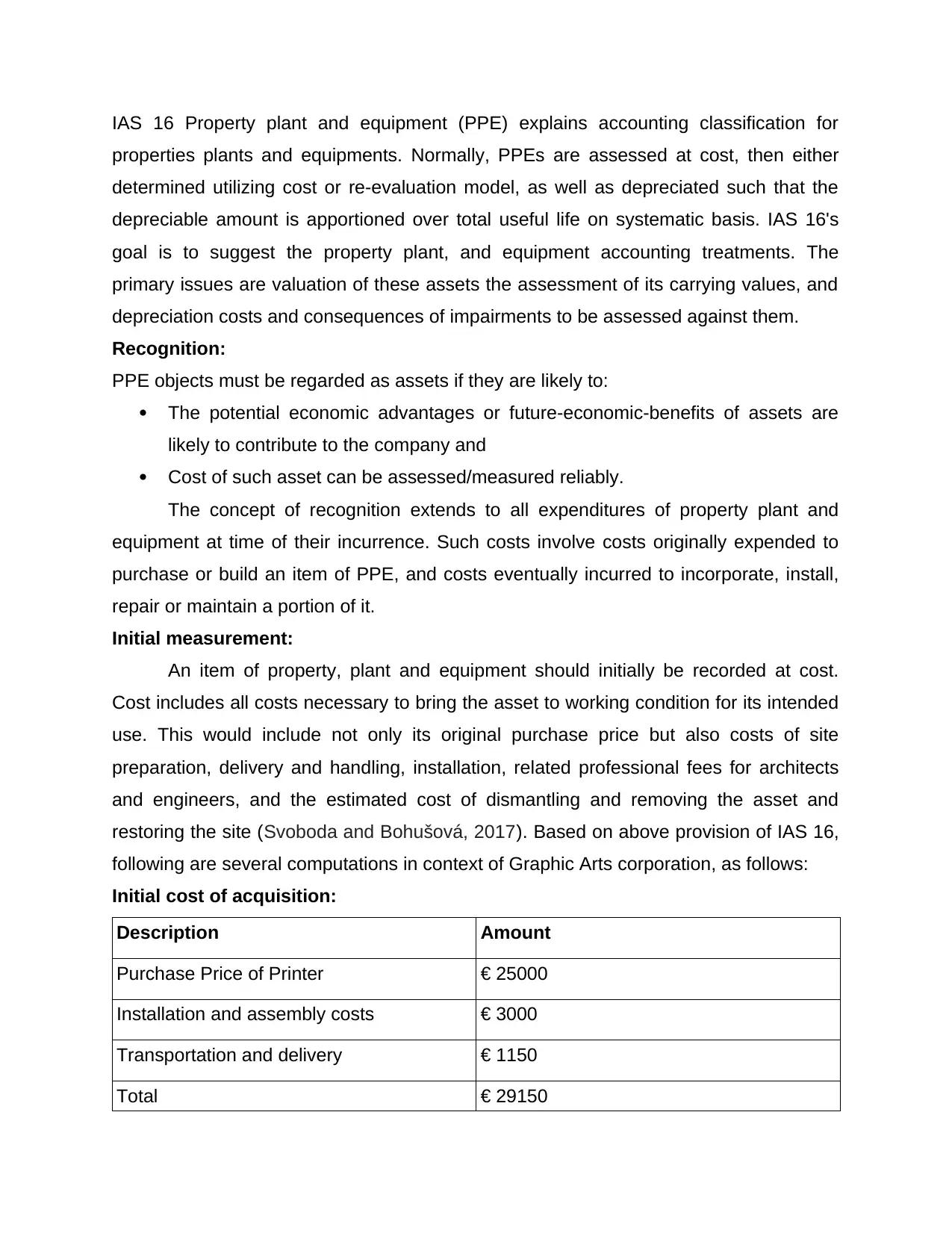

IAS 16 Property plant and equipment (PPE) explains accounting classification for

properties plants and equipments. Normally, PPEs are assessed at cost, then either

determined utilizing cost or re-evaluation model, as well as depreciated such that the

depreciable amount is apportioned over total useful life on systematic basis. IAS 16's

goal is to suggest the property plant, and equipment accounting treatments. The

primary issues are valuation of these assets the assessment of its carrying values, and

depreciation costs and consequences of impairments to be assessed against them.

Recognition:

PPE objects must be regarded as assets if they are likely to:

The potential economic advantages or future-economic-benefits of assets are

likely to contribute to the company and

Cost of such asset can be assessed/measured reliably.

The concept of recognition extends to all expenditures of property plant and

equipment at time of their incurrence. Such costs involve costs originally expended to

purchase or build an item of PPE, and costs eventually incurred to incorporate, install,

repair or maintain a portion of it.

Initial measurement:

An item of property, plant and equipment should initially be recorded at cost.

Cost includes all costs necessary to bring the asset to working condition for its intended

use. This would include not only its original purchase price but also costs of site

preparation, delivery and handling, installation, related professional fees for architects

and engineers, and the estimated cost of dismantling and removing the asset and

restoring the site (Svoboda and Bohušová, 2017). Based on above provision of IAS 16,

following are several computations in context of Graphic Arts corporation, as follows:

Initial cost of acquisition:

Description Amount

Purchase Price of Printer € 25000

Installation and assembly costs € 3000

Transportation and delivery € 1150

Total € 29150

properties plants and equipments. Normally, PPEs are assessed at cost, then either

determined utilizing cost or re-evaluation model, as well as depreciated such that the

depreciable amount is apportioned over total useful life on systematic basis. IAS 16's

goal is to suggest the property plant, and equipment accounting treatments. The

primary issues are valuation of these assets the assessment of its carrying values, and

depreciation costs and consequences of impairments to be assessed against them.

Recognition:

PPE objects must be regarded as assets if they are likely to:

The potential economic advantages or future-economic-benefits of assets are

likely to contribute to the company and

Cost of such asset can be assessed/measured reliably.

The concept of recognition extends to all expenditures of property plant and

equipment at time of their incurrence. Such costs involve costs originally expended to

purchase or build an item of PPE, and costs eventually incurred to incorporate, install,

repair or maintain a portion of it.

Initial measurement:

An item of property, plant and equipment should initially be recorded at cost.

Cost includes all costs necessary to bring the asset to working condition for its intended

use. This would include not only its original purchase price but also costs of site

preparation, delivery and handling, installation, related professional fees for architects

and engineers, and the estimated cost of dismantling and removing the asset and

restoring the site (Svoboda and Bohušová, 2017). Based on above provision of IAS 16,

following are several computations in context of Graphic Arts corporation, as follows:

Initial cost of acquisition:

Description Amount

Purchase Price of Printer € 25000

Installation and assembly costs € 3000

Transportation and delivery € 1150

Total € 29150

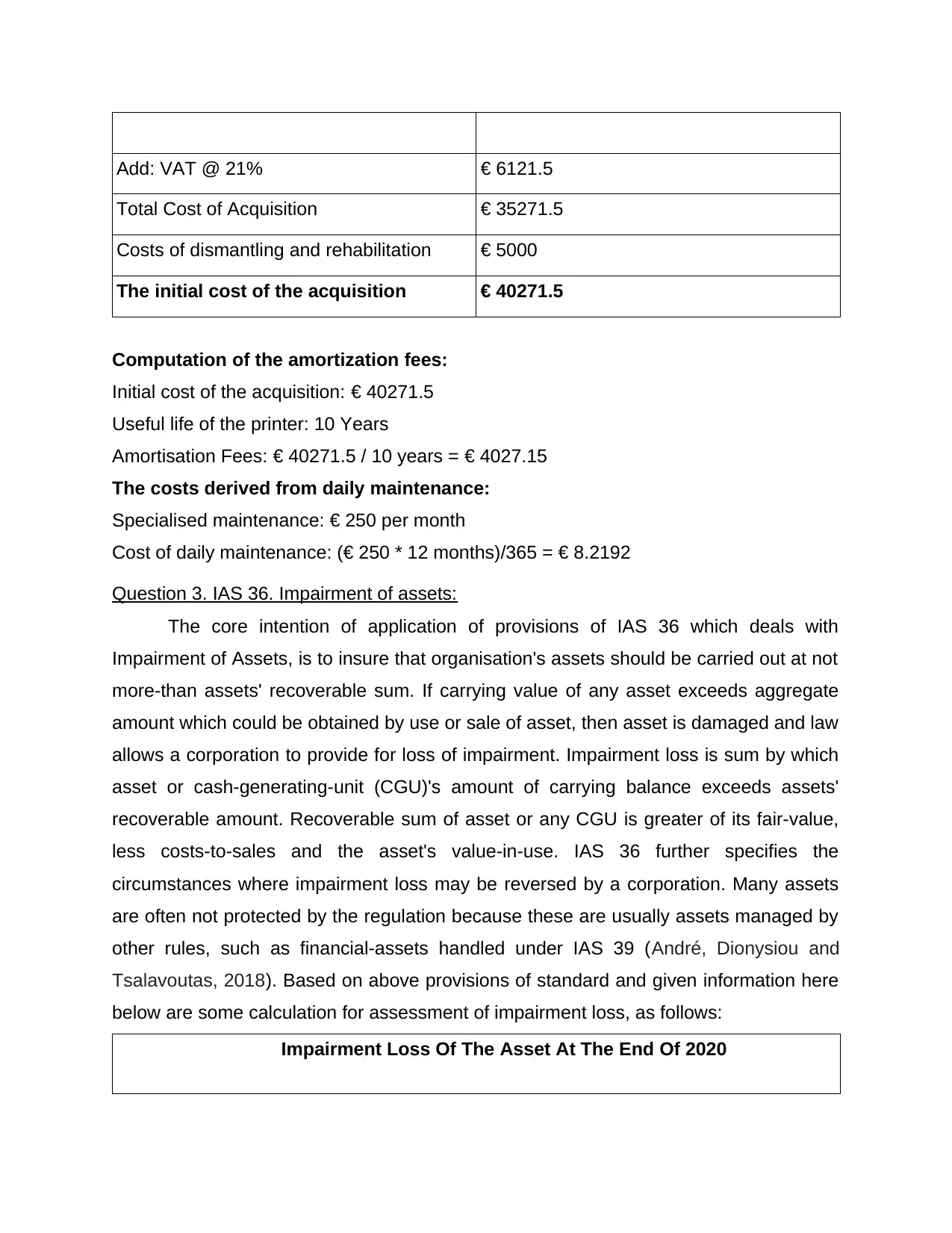

Add: VAT @ 21% € 6121.5

Total Cost of Acquisition € 35271.5

Costs of dismantling and rehabilitation € 5000

The initial cost of the acquisition € 40271.5

Computation of the amortization fees:

Initial cost of the acquisition: € 40271.5

Useful life of the printer: 10 Years

Amortisation Fees: € 40271.5 / 10 years = € 4027.15

The costs derived from daily maintenance:

Specialised maintenance: € 250 per month

Cost of daily maintenance: (€ 250 * 12 months)/365 = € 8.2192

Question 3. IAS 36. Impairment of assets:

The core intention of application of provisions of IAS 36 which deals with

Impairment of Assets, is to insure that organisation's assets should be carried out at not

more-than assets' recoverable sum. If carrying value of any asset exceeds aggregate

amount which could be obtained by use or sale of asset, then asset is damaged and law

allows a corporation to provide for loss of impairment. Impairment loss is sum by which

asset or cash-generating-unit (CGU)'s amount of carrying balance exceeds assets'

recoverable amount. Recoverable sum of asset or any CGU is greater of its fair-value,

less costs-to-sales and the asset's value-in-use. IAS 36 further specifies the

circumstances where impairment loss may be reversed by a corporation. Many assets

are often not protected by the regulation because these are usually assets managed by

other rules, such as financial-assets handled under IAS 39 (André, Dionysiou and

Tsalavoutas, 2018). Based on above provisions of standard and given information here

below are some calculation for assessment of impairment loss, as follows:

Impairment Loss Of The Asset At The End Of 2020

Total Cost of Acquisition € 35271.5

Costs of dismantling and rehabilitation € 5000

The initial cost of the acquisition € 40271.5

Computation of the amortization fees:

Initial cost of the acquisition: € 40271.5

Useful life of the printer: 10 Years

Amortisation Fees: € 40271.5 / 10 years = € 4027.15

The costs derived from daily maintenance:

Specialised maintenance: € 250 per month

Cost of daily maintenance: (€ 250 * 12 months)/365 = € 8.2192

Question 3. IAS 36. Impairment of assets:

The core intention of application of provisions of IAS 36 which deals with

Impairment of Assets, is to insure that organisation's assets should be carried out at not

more-than assets' recoverable sum. If carrying value of any asset exceeds aggregate

amount which could be obtained by use or sale of asset, then asset is damaged and law

allows a corporation to provide for loss of impairment. Impairment loss is sum by which

asset or cash-generating-unit (CGU)'s amount of carrying balance exceeds assets'

recoverable amount. Recoverable sum of asset or any CGU is greater of its fair-value,

less costs-to-sales and the asset's value-in-use. IAS 36 further specifies the

circumstances where impairment loss may be reversed by a corporation. Many assets

are often not protected by the regulation because these are usually assets managed by

other rules, such as financial-assets handled under IAS 39 (André, Dionysiou and

Tsalavoutas, 2018). Based on above provisions of standard and given information here

below are some calculation for assessment of impairment loss, as follows:

Impairment Loss Of The Asset At The End Of 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

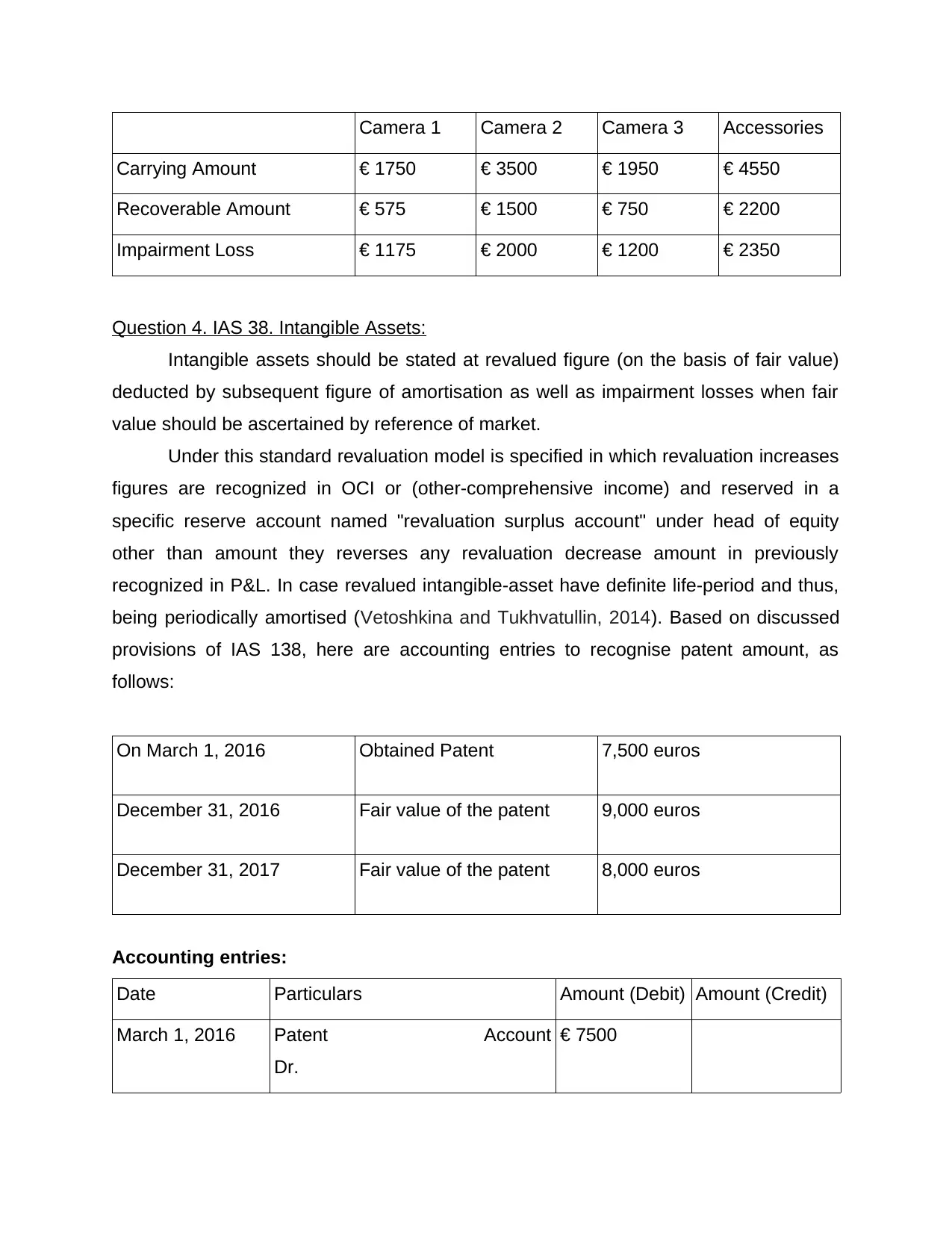

Camera 1 Camera 2 Camera 3 Accessories

Carrying Amount € 1750 € 3500 € 1950 € 4550

Recoverable Amount € 575 € 1500 € 750 € 2200

Impairment Loss € 1175 € 2000 € 1200 € 2350

Question 4. IAS 38. Intangible Assets:

Intangible assets should be stated at revalued figure (on the basis of fair value)

deducted by subsequent figure of amortisation as well as impairment losses when fair

value should be ascertained by reference of market.

Under this standard revaluation model is specified in which revaluation increases

figures are recognized in OCI or (other-comprehensive income) and reserved in a

specific reserve account named "revaluation surplus account" under head of equity

other than amount they reverses any revaluation decrease amount in previously

recognized in P&L. In case revalued intangible-asset have definite life-period and thus,

being periodically amortised (Vetoshkina and Tukhvatullin, 2014). Based on discussed

provisions of IAS 138, here are accounting entries to recognise patent amount, as

follows:

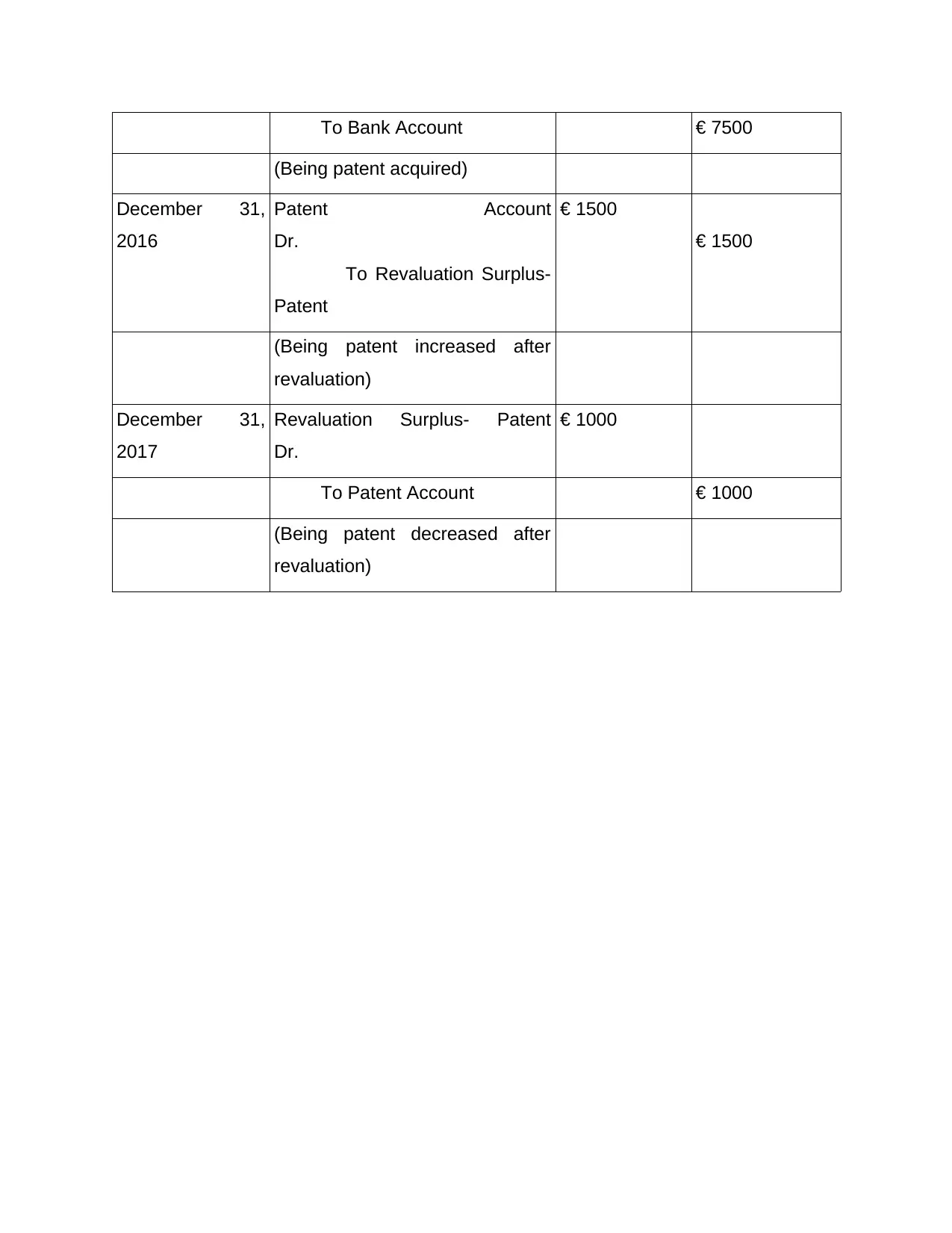

On March 1, 2016 Obtained Patent 7,500 euros

December 31, 2016 Fair value of the patent 9,000 euros

December 31, 2017 Fair value of the patent 8,000 euros

Accounting entries:

Date Particulars Amount (Debit) Amount (Credit)

March 1, 2016 Patent Account

Dr.

€ 7500

Carrying Amount € 1750 € 3500 € 1950 € 4550

Recoverable Amount € 575 € 1500 € 750 € 2200

Impairment Loss € 1175 € 2000 € 1200 € 2350

Question 4. IAS 38. Intangible Assets:

Intangible assets should be stated at revalued figure (on the basis of fair value)

deducted by subsequent figure of amortisation as well as impairment losses when fair

value should be ascertained by reference of market.

Under this standard revaluation model is specified in which revaluation increases

figures are recognized in OCI or (other-comprehensive income) and reserved in a

specific reserve account named "revaluation surplus account" under head of equity

other than amount they reverses any revaluation decrease amount in previously

recognized in P&L. In case revalued intangible-asset have definite life-period and thus,

being periodically amortised (Vetoshkina and Tukhvatullin, 2014). Based on discussed

provisions of IAS 138, here are accounting entries to recognise patent amount, as

follows:

On March 1, 2016 Obtained Patent 7,500 euros

December 31, 2016 Fair value of the patent 9,000 euros

December 31, 2017 Fair value of the patent 8,000 euros

Accounting entries:

Date Particulars Amount (Debit) Amount (Credit)

March 1, 2016 Patent Account

Dr.

€ 7500

To Bank Account € 7500

(Being patent acquired)

December 31,

2016

Patent Account

Dr.

To Revaluation Surplus-

Patent

€ 1500

€ 1500

(Being patent increased after

revaluation)

December 31,

2017

Revaluation Surplus- Patent

Dr.

€ 1000

To Patent Account € 1000

(Being patent decreased after

revaluation)

(Being patent acquired)

December 31,

2016

Patent Account

Dr.

To Revaluation Surplus-

Patent

€ 1500

€ 1500

(Being patent increased after

revaluation)

December 31,

2017

Revaluation Surplus- Patent

Dr.

€ 1000

To Patent Account € 1000

(Being patent decreased after

revaluation)

REFERENCES

Books and Journals:

Svoboda, P. and Bohušová, H., 2017. Amendments to IAS 16 and IAS 41: Are there

any differences between plant and animal from a financial reporting point of

view?. Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis, 65(1), pp.327-337.

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact

on analysts’ forecasts. Applied Economics, 50(7), pp.707-725.

Vetoshkina, E.Y. and Tukhvatullin, R.S., 2014. The problem of accounting for the costs

incurred after the initial recognition of an intangible asset. Mediterranean

Journal of Social Sciences, 5(24), p.52.

Books and Journals:

Svoboda, P. and Bohušová, H., 2017. Amendments to IAS 16 and IAS 41: Are there

any differences between plant and animal from a financial reporting point of

view?. Acta Universitatis Agriculturae et Silviculturae Mendelianae

Brunensis, 65(1), pp.327-337.

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact

on analysts’ forecasts. Applied Economics, 50(7), pp.707-725.

Vetoshkina, E.Y. and Tukhvatullin, R.S., 2014. The problem of accounting for the costs

incurred after the initial recognition of an intangible asset. Mediterranean

Journal of Social Sciences, 5(24), p.52.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.