Financial Statement Analysis of a Firm

VerifiedAdded on 2020/04/01

|12

|2192

|138

AI Summary

This assignment presents a detailed analysis of a company's financial statements. It examines various line items such as equity capital, retained earnings, tax assets, reserves, dividends, share capital, investments, net profit after tax, and accounts payable. The analysis aims to provide insights into the firm's financial health, profitability, and overall performance based on its accounting data.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE REPORTING

Corporate Reporting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Reporting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE REPORTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Requirement 1:.............................................................................................................................4

Requirement 2:.............................................................................................................................5

Requirement 3:.............................................................................................................................8

References & Bibliography:..........................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Requirement 1:.............................................................................................................................4

Requirement 2:.............................................................................................................................5

Requirement 3:.............................................................................................................................8

References & Bibliography:..........................................................................................................11

2CORPORATE REPORTING

Answer to Question 1:

The International Accounting Standards Board is an independent body with a private

undertaking that is in charge of development and approval of International Financial Reporting

Standards. In the year of 2001 the International Accounting Standards Committee was replaced

by the International Accounting Standards Board.The International Accounting Standards Board

is the primary body implementingand issuing standards that are generally accepted worldwide

and as mentioned in the question is almost accepted globally with a geographical diversity. The

International Accounting Standards Board (IASB) had amended a lot of accounting principles so

that the preparation of financial statements become proper and they are able to reflect a true and

fair view of the financial or liquidity position of the company. With continued effortson the part

of International Accounting Standards Board, it started making its own accounting standards

named International Financial Reporting Standards (IFRS). The standards of the IFRS are set by

a group of experts that constitute of the IASB with enough practical experience to maintain an

easy to understand and transparent process while setting the standards. In the due process, the

basic points which are taken care of are London office broadcast of the public board meeting,

live; publishing the agenda papers mentioning the future actions that might be implemented by

the board; outcomes of the board meeting are jotted down and circulated (Giner et al. 2016).

While setting the standard the Board is required to maintain certain methods. In every

interval of five years a detailed study is made and after consulting about the priorities the project

plan is designed. Each project begins with a research to know the issue and its probable situation

and decipher the requirement of the standard. Sometimes public comments are also encouraged.

As required the Board amends the standard or brings out something new after a full scope

Answer to Question 1:

The International Accounting Standards Board is an independent body with a private

undertaking that is in charge of development and approval of International Financial Reporting

Standards. In the year of 2001 the International Accounting Standards Committee was replaced

by the International Accounting Standards Board.The International Accounting Standards Board

is the primary body implementingand issuing standards that are generally accepted worldwide

and as mentioned in the question is almost accepted globally with a geographical diversity. The

International Accounting Standards Board (IASB) had amended a lot of accounting principles so

that the preparation of financial statements become proper and they are able to reflect a true and

fair view of the financial or liquidity position of the company. With continued effortson the part

of International Accounting Standards Board, it started making its own accounting standards

named International Financial Reporting Standards (IFRS). The standards of the IFRS are set by

a group of experts that constitute of the IASB with enough practical experience to maintain an

easy to understand and transparent process while setting the standards. In the due process, the

basic points which are taken care of are London office broadcast of the public board meeting,

live; publishing the agenda papers mentioning the future actions that might be implemented by

the board; outcomes of the board meeting are jotted down and circulated (Giner et al. 2016).

While setting the standard the Board is required to maintain certain methods. In every

interval of five years a detailed study is made and after consulting about the priorities the project

plan is designed. Each project begins with a research to know the issue and its probable situation

and decipher the requirement of the standard. Sometimes public comments are also encouraged.

As required the Board amends the standard or brings out something new after a full scope

3CORPORATE REPORTING

research and discussion. Proposals for amendments and new insertions of standards are made

public for consultation (Ames 2013). The Board members and the technical staff of IFRS

Foundation consult with as many as stakeholders all around the globe to get further evidence.

Issuance of standard is not the job actually, but its implementation that matters the most for the

Board otherwise the job may be futile. Thus it is very clear from the above descriptions that

setting up financial reporting standards is not at all an easy task but the International Accounting

Standards Board is in charge of regular monitoring and reviewing the quality of standards

implemented. It is also evident from the above study that it is very natural that due to such care

taken countries worldwide will be very interested in implementing the financial reporting

standards (Christensen et al. 2015).

The reason behind the adoption of financial reporting standards is that it results in better

decision making by the management of the firm, it provides a clear and better understanding of

the financial position of the firm and especially is of use to countries, which make a lot of

international investments.

Unfortunately the United States is still reluctant to fully adopt IFRS in its financial

reporting practices. The main reason is the lack of initiative on the part of the IFRS management

team to implement an one in all universal accounting standard that has a strong hold on finance

and is worthy enough to match the highly competitive environment of the United States (Barth et

al. 2014). Another reason for the reluctance of United States is that any kind of mistake in the

recording or any other part of the financial statements will directly pass onto the auditors. Thus it

is very useful to implement such a set financial reporting rules that is absolutely free of errors.

The IFRS fails to convince the United States that it is worthy enough to maintain this role. The

research and discussion. Proposals for amendments and new insertions of standards are made

public for consultation (Ames 2013). The Board members and the technical staff of IFRS

Foundation consult with as many as stakeholders all around the globe to get further evidence.

Issuance of standard is not the job actually, but its implementation that matters the most for the

Board otherwise the job may be futile. Thus it is very clear from the above descriptions that

setting up financial reporting standards is not at all an easy task but the International Accounting

Standards Board is in charge of regular monitoring and reviewing the quality of standards

implemented. It is also evident from the above study that it is very natural that due to such care

taken countries worldwide will be very interested in implementing the financial reporting

standards (Christensen et al. 2015).

The reason behind the adoption of financial reporting standards is that it results in better

decision making by the management of the firm, it provides a clear and better understanding of

the financial position of the firm and especially is of use to countries, which make a lot of

international investments.

Unfortunately the United States is still reluctant to fully adopt IFRS in its financial

reporting practices. The main reason is the lack of initiative on the part of the IFRS management

team to implement an one in all universal accounting standard that has a strong hold on finance

and is worthy enough to match the highly competitive environment of the United States (Barth et

al. 2014). Another reason for the reluctance of United States is that any kind of mistake in the

recording or any other part of the financial statements will directly pass onto the auditors. Thus it

is very useful to implement such a set financial reporting rules that is absolutely free of errors.

The IFRS fails to convince the United States that it is worthy enough to maintain this role. The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE REPORTING

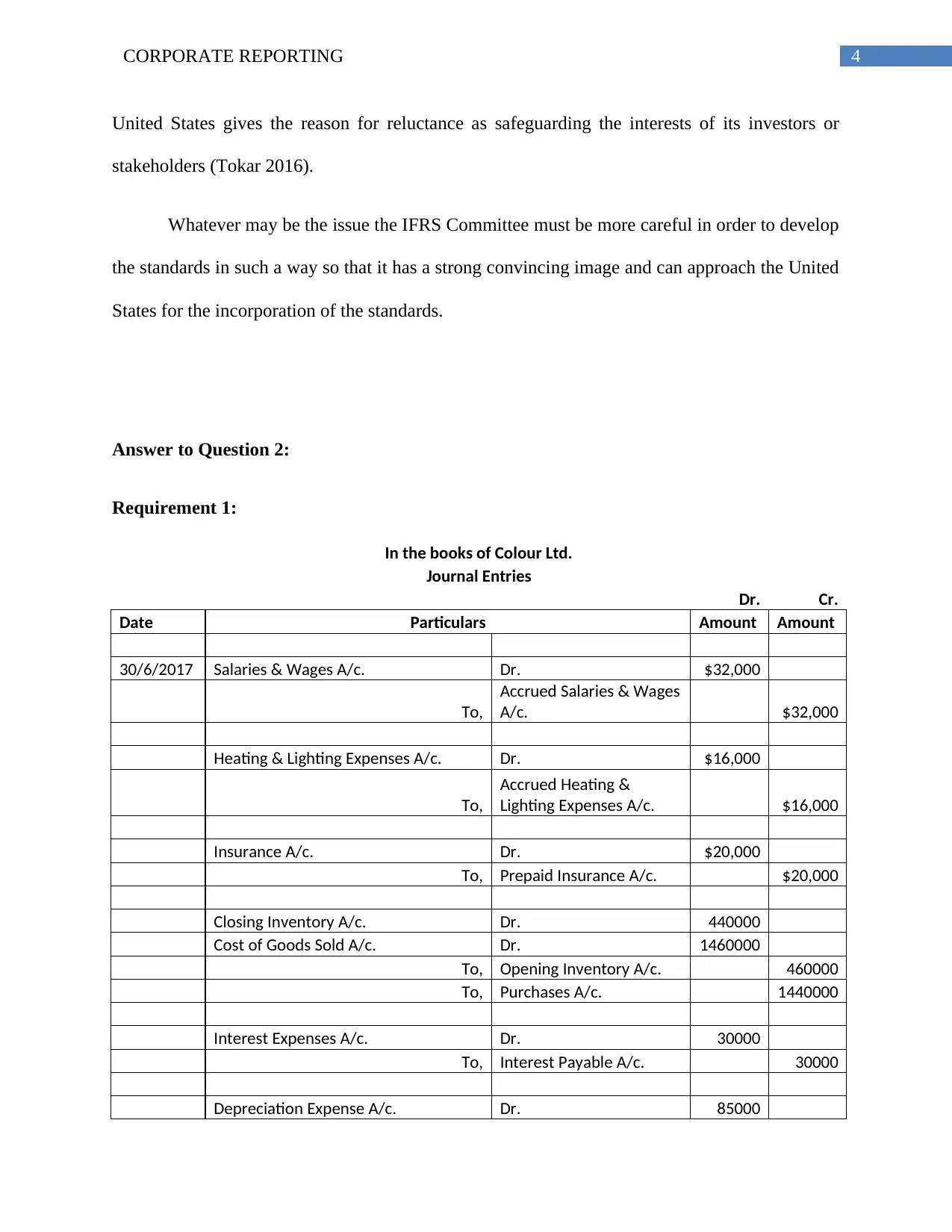

United States gives the reason for reluctance as safeguarding the interests of its investors or

stakeholders (Tokar 2016).

Whatever may be the issue the IFRS Committee must be more careful in order to develop

the standards in such a way so that it has a strong convincing image and can approach the United

States for the incorporation of the standards.

Answer to Question 2:

Requirement 1:

In the books of Colour Ltd.

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

30/6/2017 Salaries & Wages A/c. Dr. $32,000

To,

Accrued Salaries & Wages

A/c. $32,000

Heating & Lighting Expenses A/c. Dr. $16,000

To,

Accrued Heating &

Lighting Expenses A/c. $16,000

Insurance A/c. Dr. $20,000

To, Prepaid Insurance A/c. $20,000

Closing Inventory A/c. Dr. 440000

Cost of Goods Sold A/c. Dr. 1460000

To, Opening Inventory A/c. 460000

To, Purchases A/c. 1440000

Interest Expenses A/c. Dr. 30000

To, Interest Payable A/c. 30000

Depreciation Expense A/c. Dr. 85000

United States gives the reason for reluctance as safeguarding the interests of its investors or

stakeholders (Tokar 2016).

Whatever may be the issue the IFRS Committee must be more careful in order to develop

the standards in such a way so that it has a strong convincing image and can approach the United

States for the incorporation of the standards.

Answer to Question 2:

Requirement 1:

In the books of Colour Ltd.

Journal Entries

Dr. Cr.

Date Particulars Amount Amount

30/6/2017 Salaries & Wages A/c. Dr. $32,000

To,

Accrued Salaries & Wages

A/c. $32,000

Heating & Lighting Expenses A/c. Dr. $16,000

To,

Accrued Heating &

Lighting Expenses A/c. $16,000

Insurance A/c. Dr. $20,000

To, Prepaid Insurance A/c. $20,000

Closing Inventory A/c. Dr. 440000

Cost of Goods Sold A/c. Dr. 1460000

To, Opening Inventory A/c. 460000

To, Purchases A/c. 1440000

Interest Expenses A/c. Dr. 30000

To, Interest Payable A/c. 30000

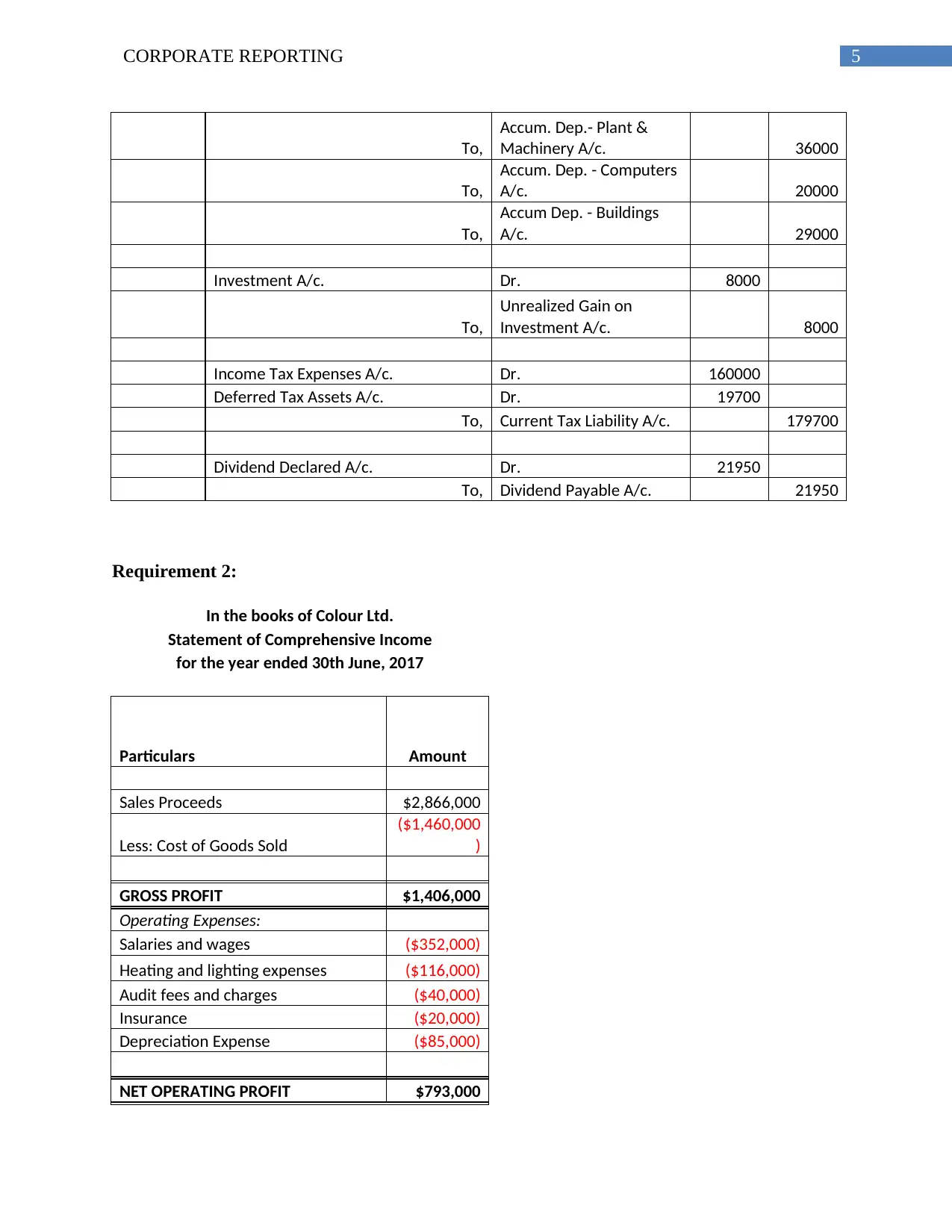

Depreciation Expense A/c. Dr. 85000

5CORPORATE REPORTING

To,

Accum. Dep.- Plant &

Machinery A/c. 36000

To,

Accum. Dep. - Computers

A/c. 20000

To,

Accum Dep. - Buildings

A/c. 29000

Investment A/c. Dr. 8000

To,

Unrealized Gain on

Investment A/c. 8000

Income Tax Expenses A/c. Dr. 160000

Deferred Tax Assets A/c. Dr. 19700

To, Current Tax Liability A/c. 179700

Dividend Declared A/c. Dr. 21950

To, Dividend Payable A/c. 21950

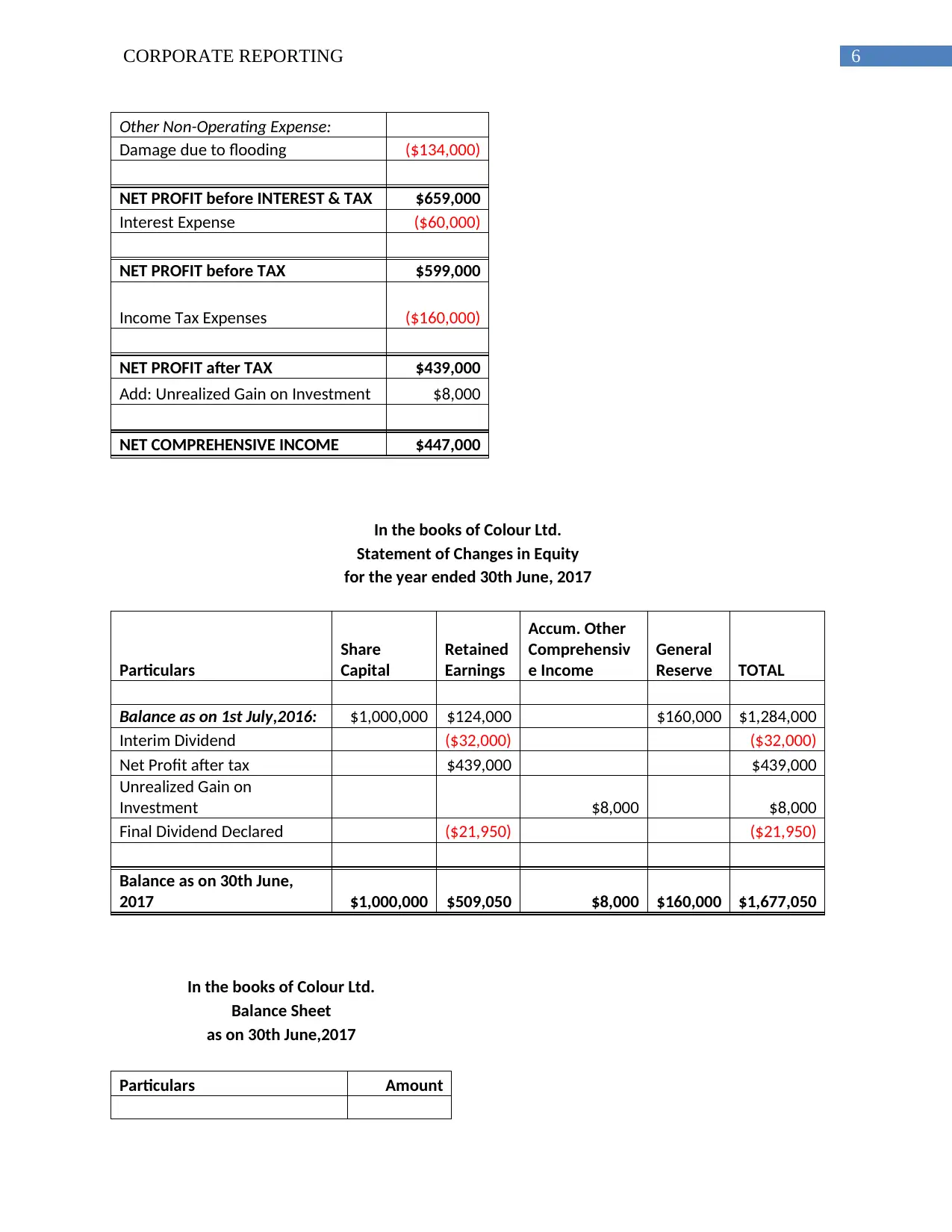

Requirement 2:

In the books of Colour Ltd.

Statement of Comprehensive Income

for the year ended 30th June, 2017

Particulars Amount

Sales Proceeds $2,866,000

Less: Cost of Goods Sold

($1,460,000

)

GROSS PROFIT $1,406,000

Operating Expenses:

Salaries and wages ($352,000)

Heating and lighting expenses ($116,000)

Audit fees and charges ($40,000)

Insurance ($20,000)

Depreciation Expense ($85,000)

NET OPERATING PROFIT $793,000

To,

Accum. Dep.- Plant &

Machinery A/c. 36000

To,

Accum. Dep. - Computers

A/c. 20000

To,

Accum Dep. - Buildings

A/c. 29000

Investment A/c. Dr. 8000

To,

Unrealized Gain on

Investment A/c. 8000

Income Tax Expenses A/c. Dr. 160000

Deferred Tax Assets A/c. Dr. 19700

To, Current Tax Liability A/c. 179700

Dividend Declared A/c. Dr. 21950

To, Dividend Payable A/c. 21950

Requirement 2:

In the books of Colour Ltd.

Statement of Comprehensive Income

for the year ended 30th June, 2017

Particulars Amount

Sales Proceeds $2,866,000

Less: Cost of Goods Sold

($1,460,000

)

GROSS PROFIT $1,406,000

Operating Expenses:

Salaries and wages ($352,000)

Heating and lighting expenses ($116,000)

Audit fees and charges ($40,000)

Insurance ($20,000)

Depreciation Expense ($85,000)

NET OPERATING PROFIT $793,000

6CORPORATE REPORTING

Other Non-Operating Expense:

Damage due to flooding ($134,000)

NET PROFIT before INTEREST & TAX $659,000

Interest Expense ($60,000)

NET PROFIT before TAX $599,000

Income Tax Expenses ($160,000)

NET PROFIT after TAX $439,000

Add: Unrealized Gain on Investment $8,000

NET COMPREHENSIVE INCOME $447,000

In the books of Colour Ltd.

Statement of Changes in Equity

for the year ended 30th June, 2017

Particulars

Share

Capital

Retained

Earnings

Accum. Other

Comprehensiv

e Income

General

Reserve TOTAL

Balance as on 1st July,2016: $1,000,000 $124,000 $160,000 $1,284,000

Interim Dividend ($32,000) ($32,000)

Net Profit after tax $439,000 $439,000

Unrealized Gain on

Investment $8,000 $8,000

Final Dividend Declared ($21,950) ($21,950)

Balance as on 30th June,

2017 $1,000,000 $509,050 $8,000 $160,000 $1,677,050

In the books of Colour Ltd.

Balance Sheet

as on 30th June,2017

Particulars Amount

Other Non-Operating Expense:

Damage due to flooding ($134,000)

NET PROFIT before INTEREST & TAX $659,000

Interest Expense ($60,000)

NET PROFIT before TAX $599,000

Income Tax Expenses ($160,000)

NET PROFIT after TAX $439,000

Add: Unrealized Gain on Investment $8,000

NET COMPREHENSIVE INCOME $447,000

In the books of Colour Ltd.

Statement of Changes in Equity

for the year ended 30th June, 2017

Particulars

Share

Capital

Retained

Earnings

Accum. Other

Comprehensiv

e Income

General

Reserve TOTAL

Balance as on 1st July,2016: $1,000,000 $124,000 $160,000 $1,284,000

Interim Dividend ($32,000) ($32,000)

Net Profit after tax $439,000 $439,000

Unrealized Gain on

Investment $8,000 $8,000

Final Dividend Declared ($21,950) ($21,950)

Balance as on 30th June,

2017 $1,000,000 $509,050 $8,000 $160,000 $1,677,050

In the books of Colour Ltd.

Balance Sheet

as on 30th June,2017

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE REPORTING

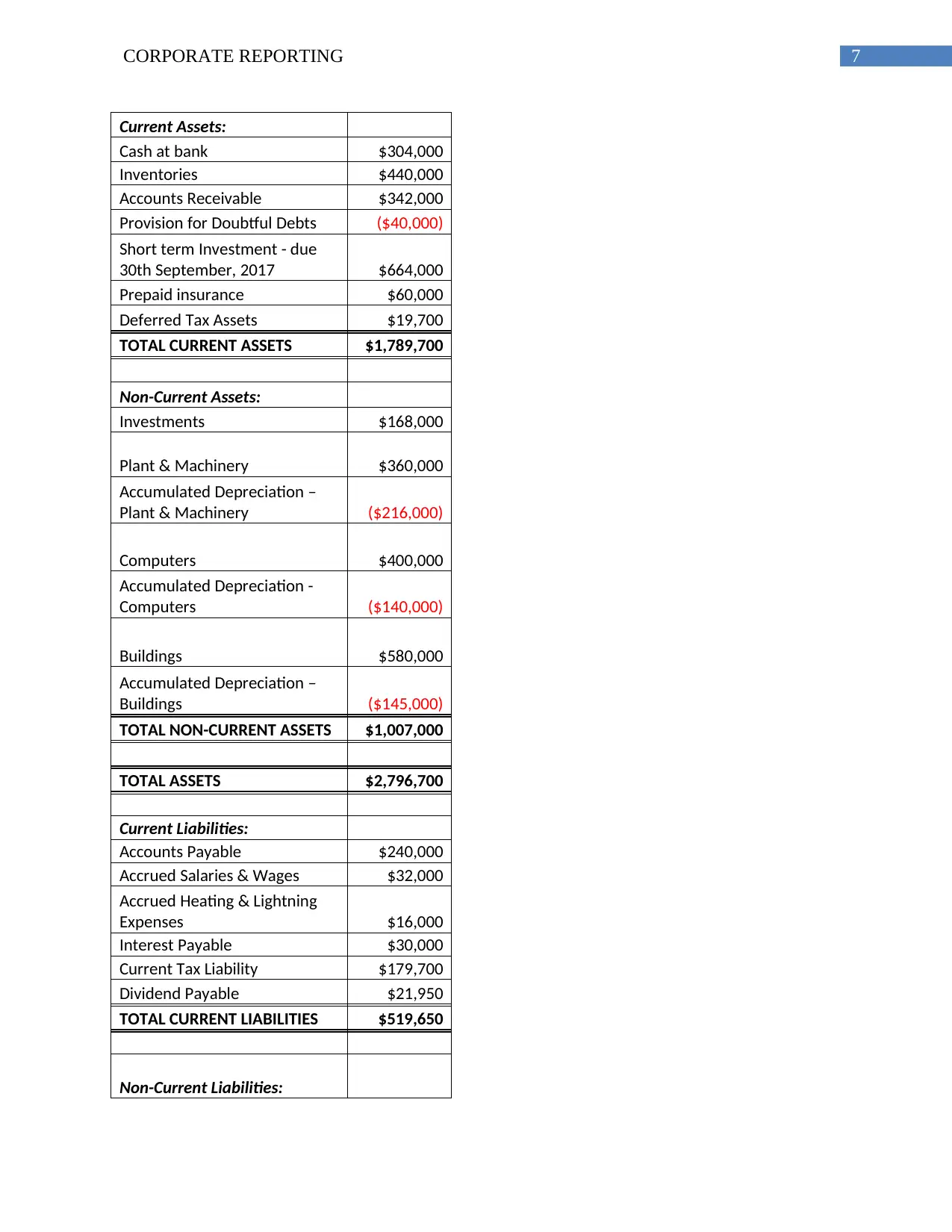

Current Assets:

Cash at bank $304,000

Inventories $440,000

Accounts Receivable $342,000

Provision for Doubtful Debts ($40,000)

Short term Investment - due

30th September, 2017 $664,000

Prepaid insurance $60,000

Deferred Tax Assets $19,700

TOTAL CURRENT ASSETS $1,789,700

Non-Current Assets:

Investments $168,000

Plant & Machinery $360,000

Accumulated Depreciation –

Plant & Machinery ($216,000)

Computers $400,000

Accumulated Depreciation -

Computers ($140,000)

Buildings $580,000

Accumulated Depreciation –

Buildings ($145,000)

TOTAL NON-CURRENT ASSETS $1,007,000

TOTAL ASSETS $2,796,700

Current Liabilities:

Accounts Payable $240,000

Accrued Salaries & Wages $32,000

Accrued Heating & Lightning

Expenses $16,000

Interest Payable $30,000

Current Tax Liability $179,700

Dividend Payable $21,950

TOTAL CURRENT LIABILITIES $519,650

Non-Current Liabilities:

Current Assets:

Cash at bank $304,000

Inventories $440,000

Accounts Receivable $342,000

Provision for Doubtful Debts ($40,000)

Short term Investment - due

30th September, 2017 $664,000

Prepaid insurance $60,000

Deferred Tax Assets $19,700

TOTAL CURRENT ASSETS $1,789,700

Non-Current Assets:

Investments $168,000

Plant & Machinery $360,000

Accumulated Depreciation –

Plant & Machinery ($216,000)

Computers $400,000

Accumulated Depreciation -

Computers ($140,000)

Buildings $580,000

Accumulated Depreciation –

Buildings ($145,000)

TOTAL NON-CURRENT ASSETS $1,007,000

TOTAL ASSETS $2,796,700

Current Liabilities:

Accounts Payable $240,000

Accrued Salaries & Wages $32,000

Accrued Heating & Lightning

Expenses $16,000

Interest Payable $30,000

Current Tax Liability $179,700

Dividend Payable $21,950

TOTAL CURRENT LIABILITIES $519,650

Non-Current Liabilities:

8CORPORATE REPORTING

Bank Loan secured over

buildings, due 1st May, 2019 $600,000

TOTAL NON-CURRENT

LIABILITIES $600,000

TOTAL LIABILITIES $1,119,650

NET ASSETS $1,677,050

Equity Capital:

Share Capital $1,000,000

General Reserve $160,000

Retained Earnings $509,050

Accum. Other Comprehensive

Income $8,000

TOTAL EQUITY CAPITAL $1,677,050

Requirement 3:

The fifteen notes to financial statements are as following:

The net comprehensive income of the company is of the value of $447,000. This means

that this is the sum of net income and other unrealized gains or losses that have been

previously omitted due to some issues.

The net operating profit is of the value $793,000, this means that this amount is excluding

the costs and tax benefits of debt financing.

The total current asset of the firm is $1789700 and the total current liability of the firm is

$519650. Therefore the working capital of the firm is $1270050.

The net asset of the firm is $1677050 which is alright and indicates that the firm is

presently in a good position.

Bank Loan secured over

buildings, due 1st May, 2019 $600,000

TOTAL NON-CURRENT

LIABILITIES $600,000

TOTAL LIABILITIES $1,119,650

NET ASSETS $1,677,050

Equity Capital:

Share Capital $1,000,000

General Reserve $160,000

Retained Earnings $509,050

Accum. Other Comprehensive

Income $8,000

TOTAL EQUITY CAPITAL $1,677,050

Requirement 3:

The fifteen notes to financial statements are as following:

The net comprehensive income of the company is of the value of $447,000. This means

that this is the sum of net income and other unrealized gains or losses that have been

previously omitted due to some issues.

The net operating profit is of the value $793,000, this means that this amount is excluding

the costs and tax benefits of debt financing.

The total current asset of the firm is $1789700 and the total current liability of the firm is

$519650. Therefore the working capital of the firm is $1270050.

The net asset of the firm is $1677050 which is alright and indicates that the firm is

presently in a good position.

9CORPORATE REPORTING

The net liabilities of the firm is $ 1119650 which is not very close to the asset amount

that again indicates a healthy condition of the firm.

The income tax expense is of the value of $160000 that indicates that the firm is a regular

payer of tax and does not generally evade it.

The total equity capital is of the value of $1677050 that indicates the part to be

distributed among the investors or stakeholders.

The retained earnings is of the value $509050 and indicates to the revenue amount not to

be paid out as dividends.

The deferred tax assets is of the value $19700 that means this asset has been used in the

balance sheet in order to reduce the taxable income.

The general reserve is of the value $16000, this means the firm has enough funds for

back up.

The final dividend declared is $21950 that is this dividend is declared at the annual

general meeting after the recommendation by the Board of Directors.

The share capital is of the amount $1000000 this indicates that the company has enough

shares invested in the market.

The investment of the firm is $168000 deciphering the same that the firm has enough

liability in investment.

The net profit after tax is $439000 that is the revenue remaining after all the operating

expenses and interests and other deductible components are subtracted.

The money owned by the firm to its creditors that is accounts payable is high enough to

be $240000.

The net liabilities of the firm is $ 1119650 which is not very close to the asset amount

that again indicates a healthy condition of the firm.

The income tax expense is of the value of $160000 that indicates that the firm is a regular

payer of tax and does not generally evade it.

The total equity capital is of the value of $1677050 that indicates the part to be

distributed among the investors or stakeholders.

The retained earnings is of the value $509050 and indicates to the revenue amount not to

be paid out as dividends.

The deferred tax assets is of the value $19700 that means this asset has been used in the

balance sheet in order to reduce the taxable income.

The general reserve is of the value $16000, this means the firm has enough funds for

back up.

The final dividend declared is $21950 that is this dividend is declared at the annual

general meeting after the recommendation by the Board of Directors.

The share capital is of the amount $1000000 this indicates that the company has enough

shares invested in the market.

The investment of the firm is $168000 deciphering the same that the firm has enough

liability in investment.

The net profit after tax is $439000 that is the revenue remaining after all the operating

expenses and interests and other deductible components are subtracted.

The money owned by the firm to its creditors that is accounts payable is high enough to

be $240000.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE REPORTING

References & Bibliography:

Ames, D., 2013. IFRS adoption and accounting quality: The case of South Africa. Journal of

Applied Economics and Business Research, 3(3), pp.154-165.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business Research,

67(3), pp.332-338.

Barth, M.E., Landsman, W.R., Young, D. and Zhuang, Z., 2014. Relevance of differences

between net income based on IFRS and domestic standards for European firms. Journal of

Business Finance & Accounting, 41(3-4), pp.297-327.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and the

cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Giner, B., Hellman, N., Jorissen, A., Quagli, A. and Taleb, A., 2016. On the ‘Review of

Structure and Effectiveness of the IFRS Foundation’: the EAA’s Financial Reporting Standards

Committee’s View. Accounting in Europe, 13(2), pp.285-294.

Šodan, S. and Aljinović Barać, Ž., 2017. The Role and Current Status of IFRS in the Completion

of National Accounting Rules–Evidence from Croatia. Accounting in Europe, pp.1-9.

References & Bibliography:

Ames, D., 2013. IFRS adoption and accounting quality: The case of South Africa. Journal of

Applied Economics and Business Research, 3(3), pp.154-165.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital

management, corporate performance, and financial constraints. Journal of Business Research,

67(3), pp.332-338.

Barth, M.E., Landsman, W.R., Young, D. and Zhuang, Z., 2014. Relevance of differences

between net income based on IFRS and domestic standards for European firms. Journal of

Business Finance & Accounting, 41(3-4), pp.297-327.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and the

cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Giner, B., Hellman, N., Jorissen, A., Quagli, A. and Taleb, A., 2016. On the ‘Review of

Structure and Effectiveness of the IFRS Foundation’: the EAA’s Financial Reporting Standards

Committee’s View. Accounting in Europe, 13(2), pp.285-294.

Šodan, S. and Aljinović Barać, Ž., 2017. The Role and Current Status of IFRS in the Completion

of National Accounting Rules–Evidence from Croatia. Accounting in Europe, pp.1-9.

11CORPORATE REPORTING

Tokar, M.B., 2016. ‘IFRS–ten years later’: a standard-setter’s view. Accounting and Business

Research, 46(5), pp.572-576.

Tokar, M.B., 2016. ‘IFRS–ten years later’: a standard-setter’s view. Accounting and Business

Research, 46(5), pp.572-576.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.