Finance Report: Hatfield Manufacturing Systems Plc Investment Proposal

VerifiedAdded on 2022/09/10

|11

|2596

|28

Report

AI Summary

This report critically evaluates an investment proposal by Hatfield Manufacturing Systems Plc, an engineering firm specializing in 3D print machines, to establish a new plant in Turkey for manufacturing components for the motor vehicle and aerospace industries. The report employs capital budgeting techniques, including net present value, payback period, and internal rate of return, to assess the project's financial viability, considering sales growth, labor costs, tax rates, and the company's beta. The analysis reveals positive net present value, a payback period of 6.153 years, and an internal rate of return exceeding the cost of capital, supporting the investment. Furthermore, the report identifies and analyzes the foreign exchange risk associated with the international project, acknowledging the potential impact of currency fluctuations on earnings and cash flow. Strategies to mitigate these risks, such as hedging with specialized exchange-traded funds, forward contracts, and currency options, are also discussed. The report concludes that the project is financially sound and provides recommendations for managing foreign exchange risks.

Running head: FINANCE FOR INTERNATIONAL BUSINESS

Finance for international business

Name of the Student

Name of the University

Author Note

Finance for international business

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS

Table of Contents

Introduction:..................................................................................................................2

Discussion:...................................................................................................................2

Evaluating the investment proposal by estimating components and overall capital

costs:.............................................................................................................................2

Identification of the foreign exchange risk on the international investment or project: 5

Conclusion:...................................................................................................................8

References list and Bibliography:.................................................................................9

Table of Contents

Introduction:..................................................................................................................2

Discussion:...................................................................................................................2

Evaluating the investment proposal by estimating components and overall capital

costs:.............................................................................................................................2

Identification of the foreign exchange risk on the international investment or project: 5

Conclusion:...................................................................................................................8

References list and Bibliography:.................................................................................9

FINANCE FOR INTERNATIONAL BUSINESS

Introduction:

The report is prepared to critically evaluate the investment proposal made by

Hatfield manufacturing system Plc which is an engineering firm specializing in the

development, designing, selling and manufacturing of 3D print machines. The

organization has undertaken the trail of supplying the components to the motor

vehicle and aerospace industries that has been successful in terms of the production

cost and durability. Due to the successful of trial, it has been proposed by the

company to manufacture these components by investing in a new plant that is

located in Turkey. The acceptability of the project is determined by evaluating its

feasibility on the financial basis. In addition to this, the report also analyses the

potential impact of the risks of foreign exchange on the proposed investment or the

project undertaken. The financial analysis of the project has been done by the

implementation of the techniques of capital budgeting such as payback period, net

present value and internal rate of return generated by the project (Meyer and Grosse

2018).

Discussion:

Evaluating the investment proposal by estimating components and overall

capital costs:

The financial viability of the project is evaluated by the application of the

techniques of capital budgeting such as net present value, payback period and

internal rate of return (Falkner and Hiebl 2015). The evaluation of the investment

proposal incorporates some assumptions relating to the costs, tax and sales growth.

Such assumptions are listed below:

The rate of sales growth is expected to grow at 12% after the first year of

operation.

Labor cost would be comprised of 35% of the total variable cost.

It is further expected that there will be growth in labor cost every year by 2%

and all the other variable cost will increase by 1.5% per year.

It is also assumed that every year, there will be increment in the fixed cost by

1%.

Introduction:

The report is prepared to critically evaluate the investment proposal made by

Hatfield manufacturing system Plc which is an engineering firm specializing in the

development, designing, selling and manufacturing of 3D print machines. The

organization has undertaken the trail of supplying the components to the motor

vehicle and aerospace industries that has been successful in terms of the production

cost and durability. Due to the successful of trial, it has been proposed by the

company to manufacture these components by investing in a new plant that is

located in Turkey. The acceptability of the project is determined by evaluating its

feasibility on the financial basis. In addition to this, the report also analyses the

potential impact of the risks of foreign exchange on the proposed investment or the

project undertaken. The financial analysis of the project has been done by the

implementation of the techniques of capital budgeting such as payback period, net

present value and internal rate of return generated by the project (Meyer and Grosse

2018).

Discussion:

Evaluating the investment proposal by estimating components and overall

capital costs:

The financial viability of the project is evaluated by the application of the

techniques of capital budgeting such as net present value, payback period and

internal rate of return (Falkner and Hiebl 2015). The evaluation of the investment

proposal incorporates some assumptions relating to the costs, tax and sales growth.

Such assumptions are listed below:

The rate of sales growth is expected to grow at 12% after the first year of

operation.

Labor cost would be comprised of 35% of the total variable cost.

It is further expected that there will be growth in labor cost every year by 2%

and all the other variable cost will increase by 1.5% per year.

It is also assumed that every year, there will be increment in the fixed cost by

1%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR INTERNATIONAL BUSINESS

The corporation tax rate in Turkey is 22%, but a lower rate of taxation is

applied for encouraging the DFI projects. On the other hand, the corporate tax

rate of UK is 19%.

The beta of HMS plc is expected to be at 1.60.

The full cost of 3D machines are depreciated over the time period of ten

years.

Every year, the net cash flow generated by the plant would be expelled to

HMS manufacturing plant as dividend.

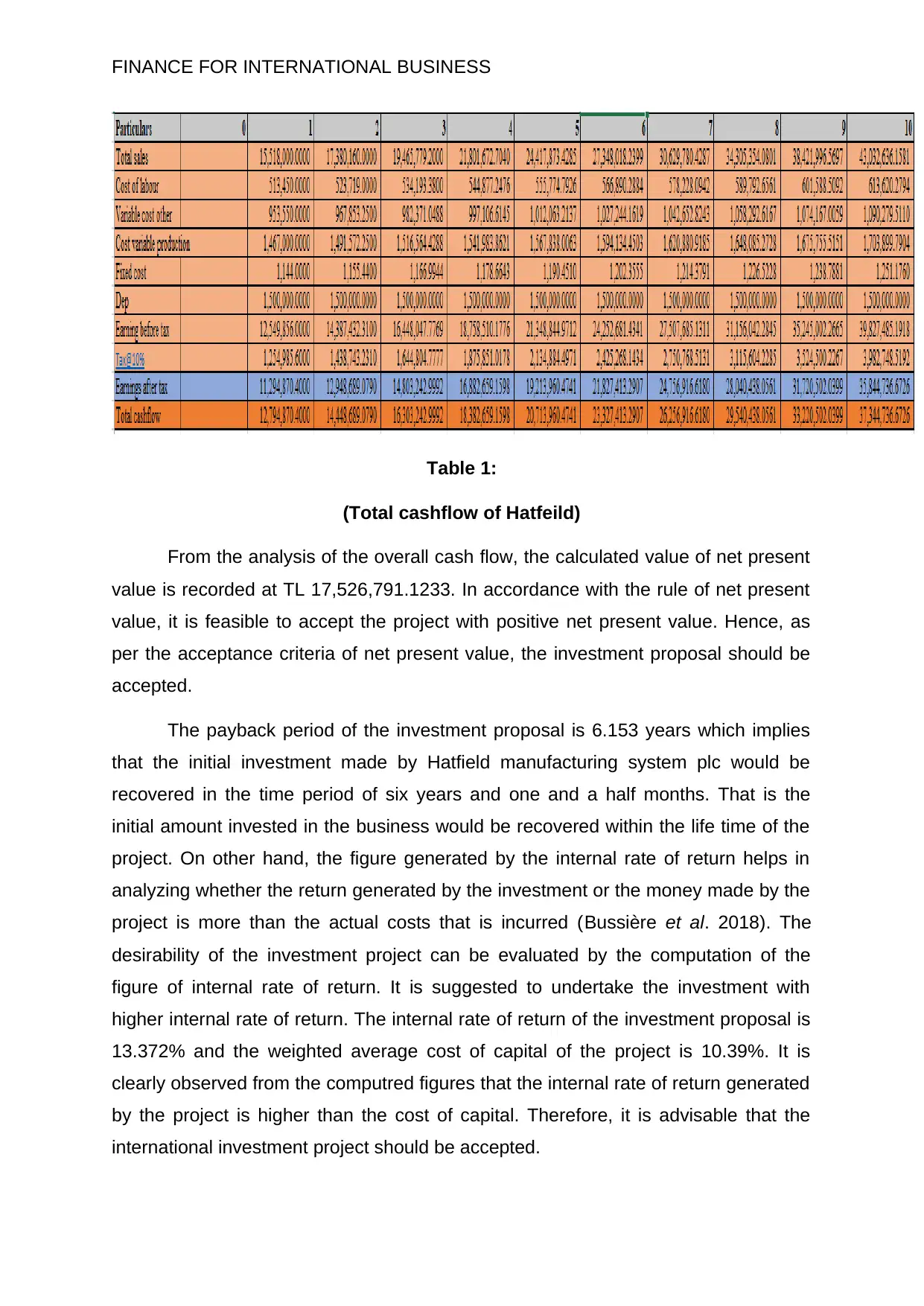

It can be observed that the total sales generated by the international project in

the first year is TL15518000 which is increasing every year by 12%. Total sales

generated in the third year and fifth year of operation is TL19,465,779.2000 and

TL24,417,873.4285 respectively. The total sales figure has increased to

38,421,996.5697 and 43,032,636.1581 in the ninth and tenth year of operation. The

cost of labor is increasing year on year along with other variable cost. Furthermore,

the total fixed cost of the project is also witnessing an increase with the increase in

the year of operation. Total amount of depreciation changed is remaining same

throughout the life of project at TL1500000. The total amount of earnings generated

after tax is increasing every year that is in the first year of operation, earnings

generated is at TL 11,294,870.4000 and this increased to 16,882,659.1598 and

TL19,213,960.4741. The earnings after tax in the ninth and tenth year of operation

has increased to TL 31,720,502.0399 and 35,844,736.6726.

It is clearly observed from the table that the total cash flow generated from the

international project is increasing every year with the first and second year of

operation generating cash flow of TL 12,794,870.4000 and TL 14,448,689.0790. The

later year of operations has also identified an increase in the earnings after tax from

TL 28,040,438.0561 in the eight year of operation to TL 35,844,736.6726 in the tenth

year of operation.

The corporation tax rate in Turkey is 22%, but a lower rate of taxation is

applied for encouraging the DFI projects. On the other hand, the corporate tax

rate of UK is 19%.

The beta of HMS plc is expected to be at 1.60.

The full cost of 3D machines are depreciated over the time period of ten

years.

Every year, the net cash flow generated by the plant would be expelled to

HMS manufacturing plant as dividend.

It can be observed that the total sales generated by the international project in

the first year is TL15518000 which is increasing every year by 12%. Total sales

generated in the third year and fifth year of operation is TL19,465,779.2000 and

TL24,417,873.4285 respectively. The total sales figure has increased to

38,421,996.5697 and 43,032,636.1581 in the ninth and tenth year of operation. The

cost of labor is increasing year on year along with other variable cost. Furthermore,

the total fixed cost of the project is also witnessing an increase with the increase in

the year of operation. Total amount of depreciation changed is remaining same

throughout the life of project at TL1500000. The total amount of earnings generated

after tax is increasing every year that is in the first year of operation, earnings

generated is at TL 11,294,870.4000 and this increased to 16,882,659.1598 and

TL19,213,960.4741. The earnings after tax in the ninth and tenth year of operation

has increased to TL 31,720,502.0399 and 35,844,736.6726.

It is clearly observed from the table that the total cash flow generated from the

international project is increasing every year with the first and second year of

operation generating cash flow of TL 12,794,870.4000 and TL 14,448,689.0790. The

later year of operations has also identified an increase in the earnings after tax from

TL 28,040,438.0561 in the eight year of operation to TL 35,844,736.6726 in the tenth

year of operation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS

Table 1:

(Total cashflow of Hatfeild)

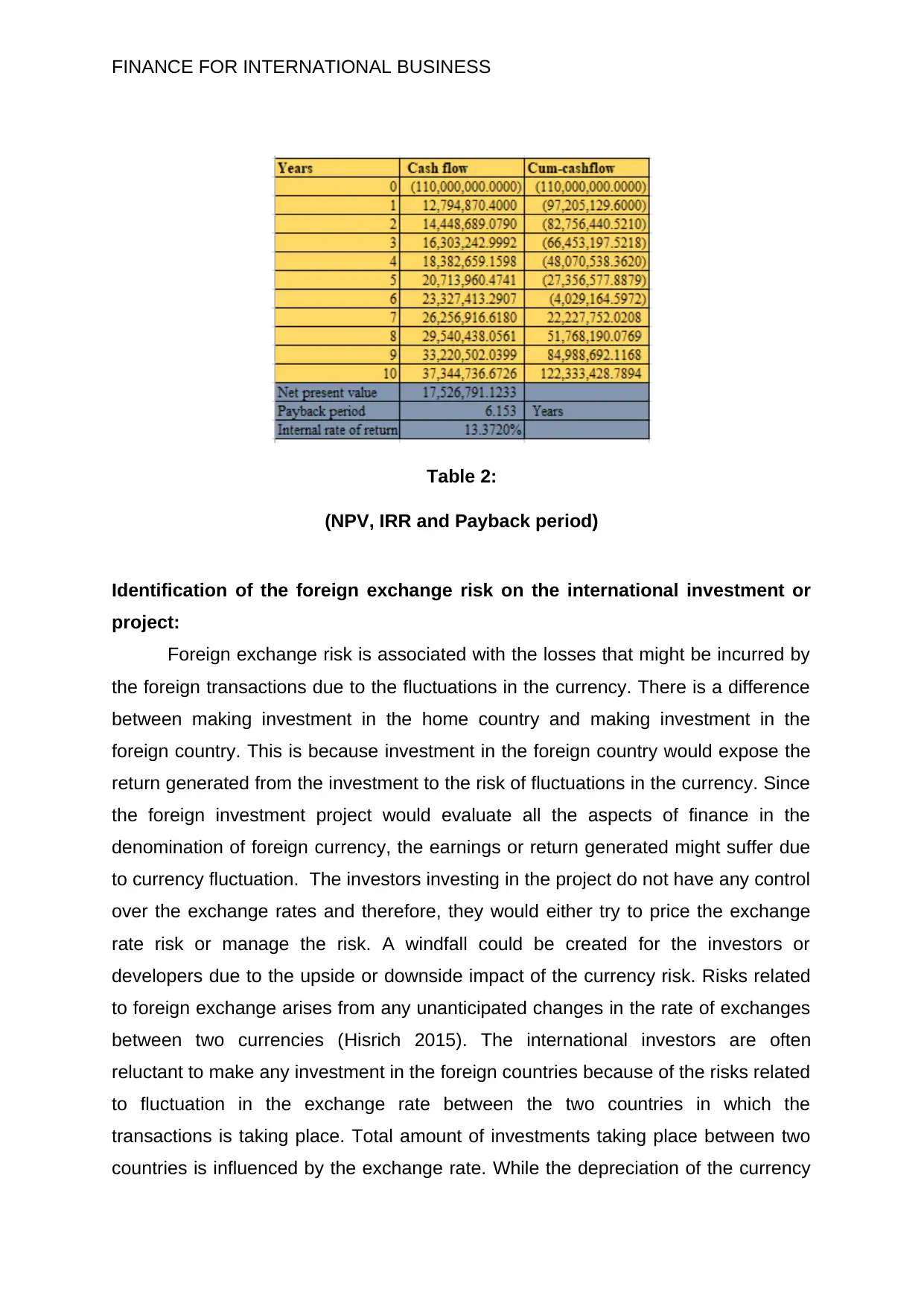

From the analysis of the overall cash flow, the calculated value of net present

value is recorded at TL 17,526,791.1233. In accordance with the rule of net present

value, it is feasible to accept the project with positive net present value. Hence, as

per the acceptance criteria of net present value, the investment proposal should be

accepted.

The payback period of the investment proposal is 6.153 years which implies

that the initial investment made by Hatfield manufacturing system plc would be

recovered in the time period of six years and one and a half months. That is the

initial amount invested in the business would be recovered within the life time of the

project. On other hand, the figure generated by the internal rate of return helps in

analyzing whether the return generated by the investment or the money made by the

project is more than the actual costs that is incurred (Bussière et al. 2018). The

desirability of the investment project can be evaluated by the computation of the

figure of internal rate of return. It is suggested to undertake the investment with

higher internal rate of return. The internal rate of return of the investment proposal is

13.372% and the weighted average cost of capital of the project is 10.39%. It is

clearly observed from the computred figures that the internal rate of return generated

by the project is higher than the cost of capital. Therefore, it is advisable that the

international investment project should be accepted.

Table 1:

(Total cashflow of Hatfeild)

From the analysis of the overall cash flow, the calculated value of net present

value is recorded at TL 17,526,791.1233. In accordance with the rule of net present

value, it is feasible to accept the project with positive net present value. Hence, as

per the acceptance criteria of net present value, the investment proposal should be

accepted.

The payback period of the investment proposal is 6.153 years which implies

that the initial investment made by Hatfield manufacturing system plc would be

recovered in the time period of six years and one and a half months. That is the

initial amount invested in the business would be recovered within the life time of the

project. On other hand, the figure generated by the internal rate of return helps in

analyzing whether the return generated by the investment or the money made by the

project is more than the actual costs that is incurred (Bussière et al. 2018). The

desirability of the investment project can be evaluated by the computation of the

figure of internal rate of return. It is suggested to undertake the investment with

higher internal rate of return. The internal rate of return of the investment proposal is

13.372% and the weighted average cost of capital of the project is 10.39%. It is

clearly observed from the computred figures that the internal rate of return generated

by the project is higher than the cost of capital. Therefore, it is advisable that the

international investment project should be accepted.

FINANCE FOR INTERNATIONAL BUSINESS

Table 2:

(NPV, IRR and Payback period)

Identification of the foreign exchange risk on the international investment or

project:

Foreign exchange risk is associated with the losses that might be incurred by

the foreign transactions due to the fluctuations in the currency. There is a difference

between making investment in the home country and making investment in the

foreign country. This is because investment in the foreign country would expose the

return generated from the investment to the risk of fluctuations in the currency. Since

the foreign investment project would evaluate all the aspects of finance in the

denomination of foreign currency, the earnings or return generated might suffer due

to currency fluctuation. The investors investing in the project do not have any control

over the exchange rates and therefore, they would either try to price the exchange

rate risk or manage the risk. A windfall could be created for the investors or

developers due to the upside or downside impact of the currency risk. Risks related

to foreign exchange arises from any unanticipated changes in the rate of exchanges

between two currencies (Hisrich 2015). The international investors are often

reluctant to make any investment in the foreign countries because of the risks related

to fluctuation in the exchange rate between the two countries in which the

transactions is taking place. Total amount of investments taking place between two

countries is influenced by the exchange rate. While the depreciation of the currency

Table 2:

(NPV, IRR and Payback period)

Identification of the foreign exchange risk on the international investment or

project:

Foreign exchange risk is associated with the losses that might be incurred by

the foreign transactions due to the fluctuations in the currency. There is a difference

between making investment in the home country and making investment in the

foreign country. This is because investment in the foreign country would expose the

return generated from the investment to the risk of fluctuations in the currency. Since

the foreign investment project would evaluate all the aspects of finance in the

denomination of foreign currency, the earnings or return generated might suffer due

to currency fluctuation. The investors investing in the project do not have any control

over the exchange rates and therefore, they would either try to price the exchange

rate risk or manage the risk. A windfall could be created for the investors or

developers due to the upside or downside impact of the currency risk. Risks related

to foreign exchange arises from any unanticipated changes in the rate of exchanges

between two currencies (Hisrich 2015). The international investors are often

reluctant to make any investment in the foreign countries because of the risks related

to fluctuation in the exchange rate between the two countries in which the

transactions is taking place. Total amount of investments taking place between two

countries is influenced by the exchange rate. While the depreciation of the currency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR INTERNATIONAL BUSINESS

in which the company is investing would make the home currency attractive and

increase the return generated. There are two potential implications of the impact of

the fluctuation in the exchange rate on the international projects. Such implications is

identified in light of appreciating and depreciating currencies. A depreciation of the

currency would cause a reduction in the production cost and wages relating to the

foreign counterparts. The overall return to the foreign country would improve due to

depreciation in the exchange rate and this contemplates them to undertake

investment in the country. It is required to account for a number of factors when

identifying the impact of exchange rate on the international investment project

(Sadgrove 2016). The exchange rate should be linked with the change in the cost of

production and the offsetting of the impact of exchange rate should not be related to

increase in the cost of production and wages of the investment capital in the

destination market. It is also argued that due to the imperfect capital market, the

results of the overseas investments is not known to the lenders that also results in

generation of risks.

The return generated from the investment can either be positively or

negatively impacted by the fluctuations in the currency. The fluctuations in the

currency impacts the return generated from any particular investments made by the

company at the international levels at various levels. The cost that is paid by the

company to the suppliers in the foreign country gets impacted due to change in the

currency (Kang and Mason 2016).

If the local currency gain value against the foreign currency in the event of

international investment, the company or the project would be benefitted in terms of

total cost savings. It is so because fall in the value of local currency would make

labor less costly in the foreign as the company would be required to pay less for the

labors. In addition to this, the raw materials that is sourced from the suppliers in the

foreign country would also cause require the project to make less payment due to

the appreciation of local currency against foreign country. That is the total cost of the

international investment is expected to fall when there is appreciation of the local

currency against foreign currency. The impact of fluctuation in the currency on the

return generated by project is significant and there is a rapid change in earnings due

to the currency rate difference (Gitman et al. 2015).

in which the company is investing would make the home currency attractive and

increase the return generated. There are two potential implications of the impact of

the fluctuation in the exchange rate on the international projects. Such implications is

identified in light of appreciating and depreciating currencies. A depreciation of the

currency would cause a reduction in the production cost and wages relating to the

foreign counterparts. The overall return to the foreign country would improve due to

depreciation in the exchange rate and this contemplates them to undertake

investment in the country. It is required to account for a number of factors when

identifying the impact of exchange rate on the international investment project

(Sadgrove 2016). The exchange rate should be linked with the change in the cost of

production and the offsetting of the impact of exchange rate should not be related to

increase in the cost of production and wages of the investment capital in the

destination market. It is also argued that due to the imperfect capital market, the

results of the overseas investments is not known to the lenders that also results in

generation of risks.

The return generated from the investment can either be positively or

negatively impacted by the fluctuations in the currency. The fluctuations in the

currency impacts the return generated from any particular investments made by the

company at the international levels at various levels. The cost that is paid by the

company to the suppliers in the foreign country gets impacted due to change in the

currency (Kang and Mason 2016).

If the local currency gain value against the foreign currency in the event of

international investment, the company or the project would be benefitted in terms of

total cost savings. It is so because fall in the value of local currency would make

labor less costly in the foreign as the company would be required to pay less for the

labors. In addition to this, the raw materials that is sourced from the suppliers in the

foreign country would also cause require the project to make less payment due to

the appreciation of local currency against foreign country. That is the total cost of the

international investment is expected to fall when there is appreciation of the local

currency against foreign currency. The impact of fluctuation in the currency on the

return generated by project is significant and there is a rapid change in earnings due

to the currency rate difference (Gitman et al. 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS

The investment made by Hatfield manufacturing system Plc in Turkey for the

manufacturing of the components is exposed to the risks of fluctuations in currency.

In the addition to this, the cash flow of the firm will be denominated into different

currencies such as $ Ca, Won and €. Therefore, the cash flow in terms of the sales

revenue is exposed to the currency fluctuations. Hence, the total earning or the

return generated by the project would be impacted by the change in exchange rate.

Depreciation of the currencies from where the earnings have to be generated would

impact the Hatfield in positive manner because this would increase the inflow of cash

denominated in currencies of different countries.

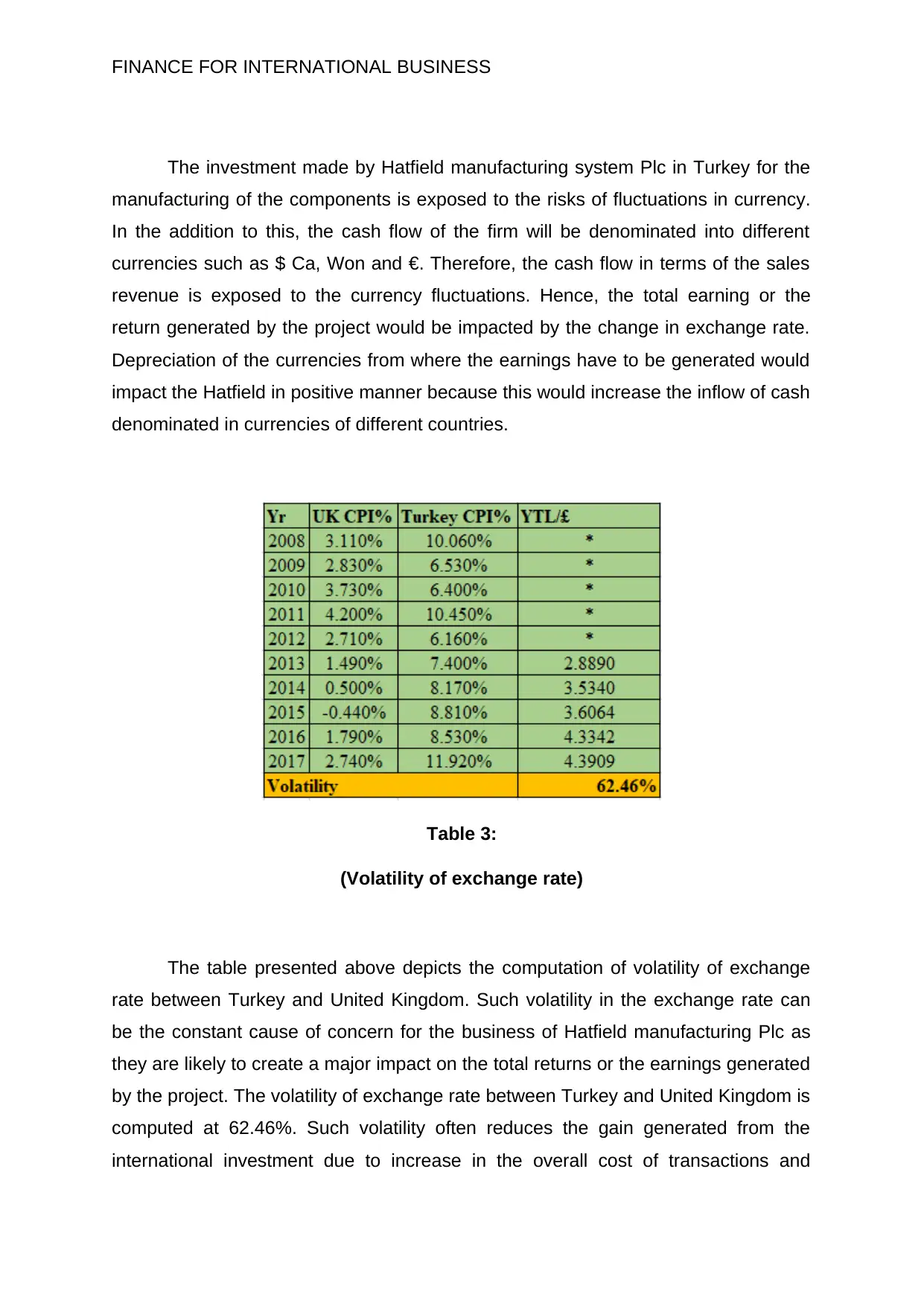

Table 3:

(Volatility of exchange rate)

The table presented above depicts the computation of volatility of exchange

rate between Turkey and United Kingdom. Such volatility in the exchange rate can

be the constant cause of concern for the business of Hatfield manufacturing Plc as

they are likely to create a major impact on the total returns or the earnings generated

by the project. The volatility of exchange rate between Turkey and United Kingdom is

computed at 62.46%. Such volatility often reduces the gain generated from the

international investment due to increase in the overall cost of transactions and

The investment made by Hatfield manufacturing system Plc in Turkey for the

manufacturing of the components is exposed to the risks of fluctuations in currency.

In the addition to this, the cash flow of the firm will be denominated into different

currencies such as $ Ca, Won and €. Therefore, the cash flow in terms of the sales

revenue is exposed to the currency fluctuations. Hence, the total earning or the

return generated by the project would be impacted by the change in exchange rate.

Depreciation of the currencies from where the earnings have to be generated would

impact the Hatfield in positive manner because this would increase the inflow of cash

denominated in currencies of different countries.

Table 3:

(Volatility of exchange rate)

The table presented above depicts the computation of volatility of exchange

rate between Turkey and United Kingdom. Such volatility in the exchange rate can

be the constant cause of concern for the business of Hatfield manufacturing Plc as

they are likely to create a major impact on the total returns or the earnings generated

by the project. The volatility of exchange rate between Turkey and United Kingdom is

computed at 62.46%. Such volatility often reduces the gain generated from the

international investment due to increase in the overall cost of transactions and

FINANCE FOR INTERNATIONAL BUSINESS

thereby making the total earnings of the project uncertain. Nevertheless, the

company can mitigate the risks associated with the foreign exchange by adopting

different strategies. Risks can be hedged by using the specialized exchange traded

funds that helps in offering long and short term exposures to different country’s

currencies. In addition to this, the company can also enter into the forward contracts

that can be used for hedging as the rate of currency can be locked in at a particular

rate. Lastly, currency options can also be used for the mitigation of risks related to

the exchange rate. With such option, the company has the right to sell or buy the

currency of different countries at a particular rate before or on the specific date

(Bekaert and Hodrick 2017).

Conclusion:

The report discussed above outlines the evaluation of the financial viability of

the investment proposal made by Hatfield manufacturing system Plc. It has been

ascertained from the overall analysis of the investment proposal using different

techniques of capital budgeting that it would be worthy to undertake the project. This

has been justified from the positive figure of net present value, higher rate of internal

return and lower payback period. Therefore, it is advisable to the firm to accept the

project on the financial basis. In addition to this, it has been found that the returns or

the earnings of the project can be impacted by the exchange rate volatility. For this

purpose, the organization can mitigate the risks by the implementation of different

currency hedging strategies such as options contracts and exchange traded funds.

thereby making the total earnings of the project uncertain. Nevertheless, the

company can mitigate the risks associated with the foreign exchange by adopting

different strategies. Risks can be hedged by using the specialized exchange traded

funds that helps in offering long and short term exposures to different country’s

currencies. In addition to this, the company can also enter into the forward contracts

that can be used for hedging as the rate of currency can be locked in at a particular

rate. Lastly, currency options can also be used for the mitigation of risks related to

the exchange rate. With such option, the company has the right to sell or buy the

currency of different countries at a particular rate before or on the specific date

(Bekaert and Hodrick 2017).

Conclusion:

The report discussed above outlines the evaluation of the financial viability of

the investment proposal made by Hatfield manufacturing system Plc. It has been

ascertained from the overall analysis of the investment proposal using different

techniques of capital budgeting that it would be worthy to undertake the project. This

has been justified from the positive figure of net present value, higher rate of internal

return and lower payback period. Therefore, it is advisable to the firm to accept the

project on the financial basis. In addition to this, it has been found that the returns or

the earnings of the project can be impacted by the exchange rate volatility. For this

purpose, the organization can mitigate the risks by the implementation of different

currency hedging strategies such as options contracts and exchange traded funds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR INTERNATIONAL BUSINESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR INTERNATIONAL BUSINESS

References list and Bibliography:

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge

University Press.

Bussière, M., Schmidt, J. and Valla, N., 2018. International financial flows in the new

normal: Key patterns (and why we should care). In International Macroeconomics in

the Wake of the Global Financial Crisis (pp. 249-269). Springer, Cham.

Falkner, E.M. and Hiebl, M.R., 2015. Risk management in SMEs: a systematic

review of available evidence. The Journal of Risk Finance, 16(2), pp.122-144.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Hisrich, R.D., 2015. International entrepreneurship: starting, developing, and

managing a global venture. SAGE publications.

Kaltenbrunner, A., 2015. A post Keynesian framework of exchange rate

determination: a Minskyan approach. Journal of Post Keynesian Economics, 38(3),

pp.426-448.

Kang, D. and Mason, A. eds., 2016. Macroprudential Regulation of International

Finance: Managing Capital Flows and Exchange Rates. Edward Elgar Publishing.

Kinsey, S., 2017. Managing risk. In The International Business Archives

Handbook (pp. 356-381). Routledge.

Meyer, K.E. and Grosse, R., 2018. Introduction to managing in emerging

markets. Oxford handbook of managing in emerging markets, pp.3-34.

Picciotto, S., 2017. Rights, responsibilities and regulation of international business.

In Globalization and International Investment (pp. 177-198). Routledge.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

Terjesen, S., Hessels, J. and Li, D., 2016. Comparative international

entrepreneurship: A review and research agenda. Journal of Management, 42(1),

pp.299-344.

References list and Bibliography:

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge

University Press.

Bussière, M., Schmidt, J. and Valla, N., 2018. International financial flows in the new

normal: Key patterns (and why we should care). In International Macroeconomics in

the Wake of the Global Financial Crisis (pp. 249-269). Springer, Cham.

Falkner, E.M. and Hiebl, M.R., 2015. Risk management in SMEs: a systematic

review of available evidence. The Journal of Risk Finance, 16(2), pp.122-144.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

Hisrich, R.D., 2015. International entrepreneurship: starting, developing, and

managing a global venture. SAGE publications.

Kaltenbrunner, A., 2015. A post Keynesian framework of exchange rate

determination: a Minskyan approach. Journal of Post Keynesian Economics, 38(3),

pp.426-448.

Kang, D. and Mason, A. eds., 2016. Macroprudential Regulation of International

Finance: Managing Capital Flows and Exchange Rates. Edward Elgar Publishing.

Kinsey, S., 2017. Managing risk. In The International Business Archives

Handbook (pp. 356-381). Routledge.

Meyer, K.E. and Grosse, R., 2018. Introduction to managing in emerging

markets. Oxford handbook of managing in emerging markets, pp.3-34.

Picciotto, S., 2017. Rights, responsibilities and regulation of international business.

In Globalization and International Investment (pp. 177-198). Routledge.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

Terjesen, S., Hessels, J. and Li, D., 2016. Comparative international

entrepreneurship: A review and research agenda. Journal of Management, 42(1),

pp.299-344.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.