Analyzing AUD/USD Exchange Rate: Purchasing & Interest Parity Report

VerifiedAdded on 2022/08/27

|13

|2586

|14

Report

AI Summary

This report provides an in-depth analysis of the AUD/USD exchange rate, examining its historical movements through the lens of macroeconomic theories. It begins by exploring Purchasing Power Parity (PPP), differentiating between absolute and relative PPP, and assessing their limitations in explaining the AUD/USD fluctuations over a ten-year period. The analysis then shifts to Interest Rate Parity (IRP), discussing covered and uncovered IRP and their methodologies, while also evaluating the empirical evidence and limitations of these theories. The report further investigates factors influencing the demand and supply of foreign exchange, including relative inflation, interest rates, and growth rates. Additionally, it considers other explanatory factors such as commodity prices, terms of trade, and the relationship between current account balance and exchange rates. Finally, the report delves into qualitative factors like the Global Financial Crisis, Sydney Siege, RBA rate cuts, Brexit, US Presidential Election, and Fed Funds Rate hikes, and concludes with an overall assessment of the factors influencing the AUD/USD exchange rate.

INTERNATIONAL FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Finance

2. Purchasing Power Parity (PPP)

There is a relation between level of price and the exchange rate which is determined by the

famous theory named Purchasing Power Parity (OECD, n.d.). It is often abbreviated as

PPP. There are two versions of theory of purchasing power parity:

1. The Absolute PPP.

2. The Relative PPP.

2.1. Absolute PPP

Absolute Purchasing Power Parity is a theory that works with the same logic as that of

Law of One Price or in other words, the price at which the goods are sold in different

markets are same after providing the adjustment for rate of exchange or exchange rate. It is

a pure theory of price-level which considers the same basket of goods in every country

ignoring any other factors. According to this concept, the currency’s exchange-rate would

gradually change over a period of time until the goods hold an equal value because without

any trade barriers there should be equilibrium in the goods’ prices (IG, n.d.).

As per Absolute PPP, rate of exchange between the currencies of two different nations is

always equal to the ratio of levels of price of basket of goods.

where,

two nations are, (AUD/USD)

foreign price level is, (USA).

Therefore,

1

Domestic Price Level (P) = [Exchange rate between two

nations (S)] x [Foreign (USA) Price Level (P*)]

S=P/P*

2. Purchasing Power Parity (PPP)

There is a relation between level of price and the exchange rate which is determined by the

famous theory named Purchasing Power Parity (OECD, n.d.). It is often abbreviated as

PPP. There are two versions of theory of purchasing power parity:

1. The Absolute PPP.

2. The Relative PPP.

2.1. Absolute PPP

Absolute Purchasing Power Parity is a theory that works with the same logic as that of

Law of One Price or in other words, the price at which the goods are sold in different

markets are same after providing the adjustment for rate of exchange or exchange rate. It is

a pure theory of price-level which considers the same basket of goods in every country

ignoring any other factors. According to this concept, the currency’s exchange-rate would

gradually change over a period of time until the goods hold an equal value because without

any trade barriers there should be equilibrium in the goods’ prices (IG, n.d.).

As per Absolute PPP, rate of exchange between the currencies of two different nations is

always equal to the ratio of levels of price of basket of goods.

where,

two nations are, (AUD/USD)

foreign price level is, (USA).

Therefore,

1

Domestic Price Level (P) = [Exchange rate between two

nations (S)] x [Foreign (USA) Price Level (P*)]

S=P/P*

International Finance

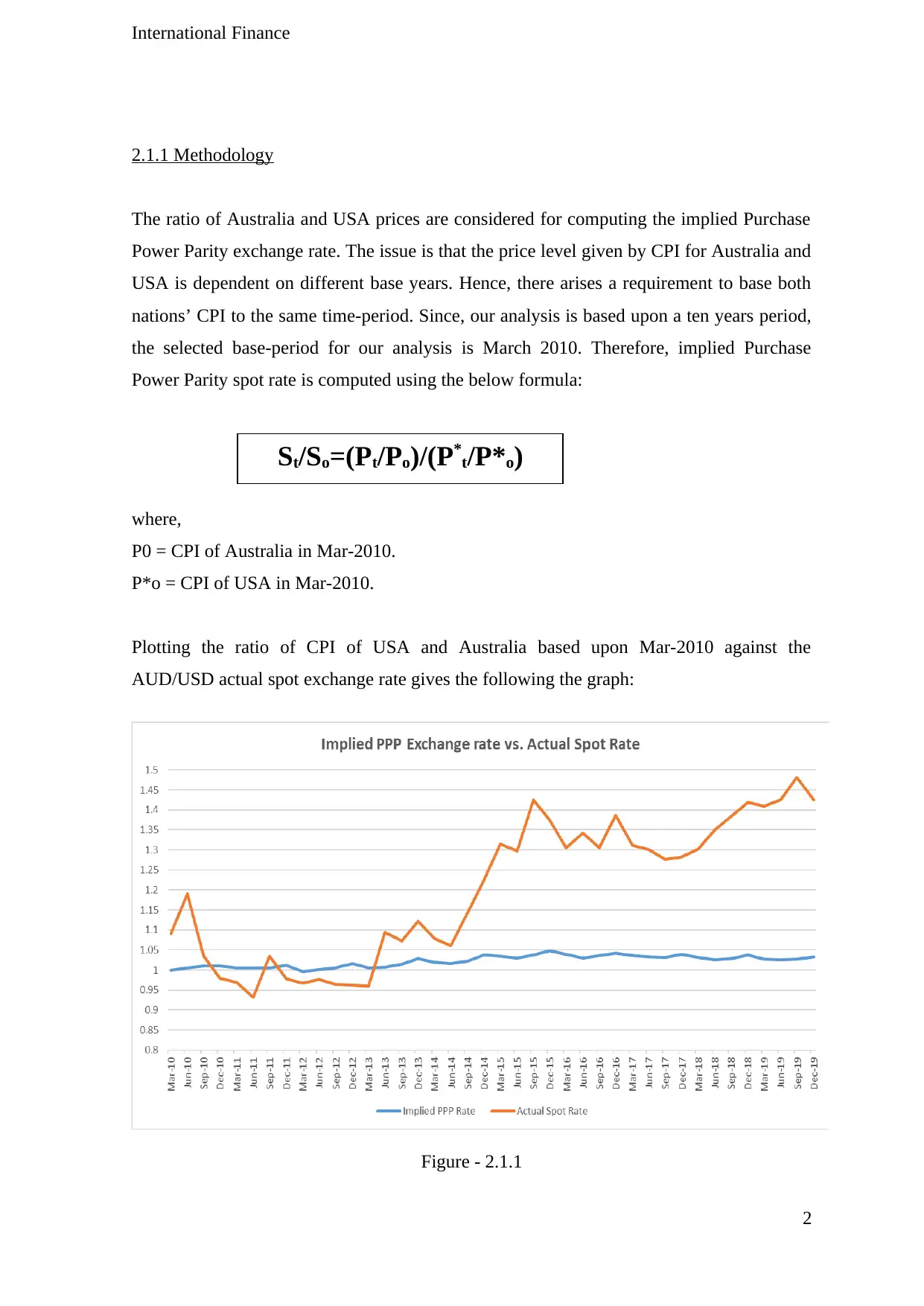

2.1.1 Methodology

The ratio of Australia and USA prices are considered for computing the implied Purchase

Power Parity exchange rate. The issue is that the price level given by CPI for Australia and

USA is dependent on different base years. Hence, there arises a requirement to base both

nations’ CPI to the same time-period. Since, our analysis is based upon a ten years period,

the selected base-period for our analysis is March 2010. Therefore, implied Purchase

Power Parity spot rate is computed using the below formula:

where,

P0 = CPI of Australia in Mar-2010.

P*o = CPI of USA in Mar-2010.

Plotting the ratio of CPI of USA and Australia based upon Mar-2010 against the

AUD/USD actual spot exchange rate gives the following the graph:

Figure - 2.1.1

2

St/So=(Pt/Po)/(P*t/P*o)

2.1.1 Methodology

The ratio of Australia and USA prices are considered for computing the implied Purchase

Power Parity exchange rate. The issue is that the price level given by CPI for Australia and

USA is dependent on different base years. Hence, there arises a requirement to base both

nations’ CPI to the same time-period. Since, our analysis is based upon a ten years period,

the selected base-period for our analysis is March 2010. Therefore, implied Purchase

Power Parity spot rate is computed using the below formula:

where,

P0 = CPI of Australia in Mar-2010.

P*o = CPI of USA in Mar-2010.

Plotting the ratio of CPI of USA and Australia based upon Mar-2010 against the

AUD/USD actual spot exchange rate gives the following the graph:

Figure - 2.1.1

2

St/So=(Pt/Po)/(P*t/P*o)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International Finance

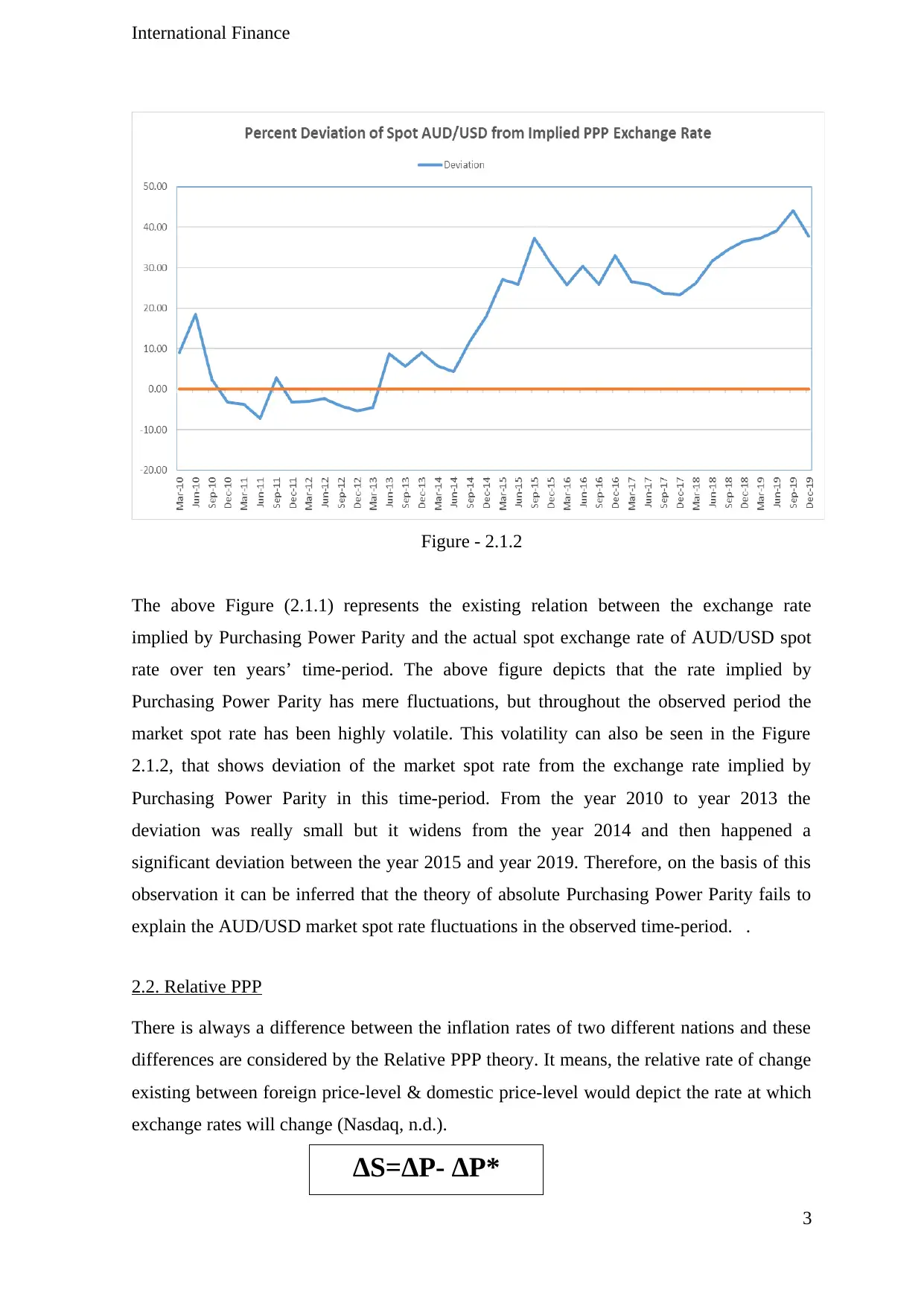

Figure - 2.1.2

The above Figure (2.1.1) represents the existing relation between the exchange rate

implied by Purchasing Power Parity and the actual spot exchange rate of AUD/USD spot

rate over ten years’ time-period. The above figure depicts that the rate implied by

Purchasing Power Parity has mere fluctuations, but throughout the observed period the

market spot rate has been highly volatile. This volatility can also be seen in the Figure

2.1.2, that shows deviation of the market spot rate from the exchange rate implied by

Purchasing Power Parity in this time-period. From the year 2010 to year 2013 the

deviation was really small but it widens from the year 2014 and then happened a

significant deviation between the year 2015 and year 2019. Therefore, on the basis of this

observation it can be inferred that the theory of absolute Purchasing Power Parity fails to

explain the AUD/USD market spot rate fluctuations in the observed time-period. .

2.2. Relative PPP

There is always a difference between the inflation rates of two different nations and these

differences are considered by the Relative PPP theory. It means, the relative rate of change

existing between foreign price-level & domestic price-level would depict the rate at which

exchange rates will change (Nasdaq, n.d.).

3

∆S=∆P- ∆P*

Figure - 2.1.2

The above Figure (2.1.1) represents the existing relation between the exchange rate

implied by Purchasing Power Parity and the actual spot exchange rate of AUD/USD spot

rate over ten years’ time-period. The above figure depicts that the rate implied by

Purchasing Power Parity has mere fluctuations, but throughout the observed period the

market spot rate has been highly volatile. This volatility can also be seen in the Figure

2.1.2, that shows deviation of the market spot rate from the exchange rate implied by

Purchasing Power Parity in this time-period. From the year 2010 to year 2013 the

deviation was really small but it widens from the year 2014 and then happened a

significant deviation between the year 2015 and year 2019. Therefore, on the basis of this

observation it can be inferred that the theory of absolute Purchasing Power Parity fails to

explain the AUD/USD market spot rate fluctuations in the observed time-period. .

2.2. Relative PPP

There is always a difference between the inflation rates of two different nations and these

differences are considered by the Relative PPP theory. It means, the relative rate of change

existing between foreign price-level & domestic price-level would depict the rate at which

exchange rates will change (Nasdaq, n.d.).

3

∆S=∆P- ∆P*

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Finance

where,

∆S = % change in AUD/USD rate.

∆P= % change in Australia Price-Level.

∆P* = % change in USA Price-Level.

As per Relative PPP, the country which has a higher rate of inflation would depreciate.

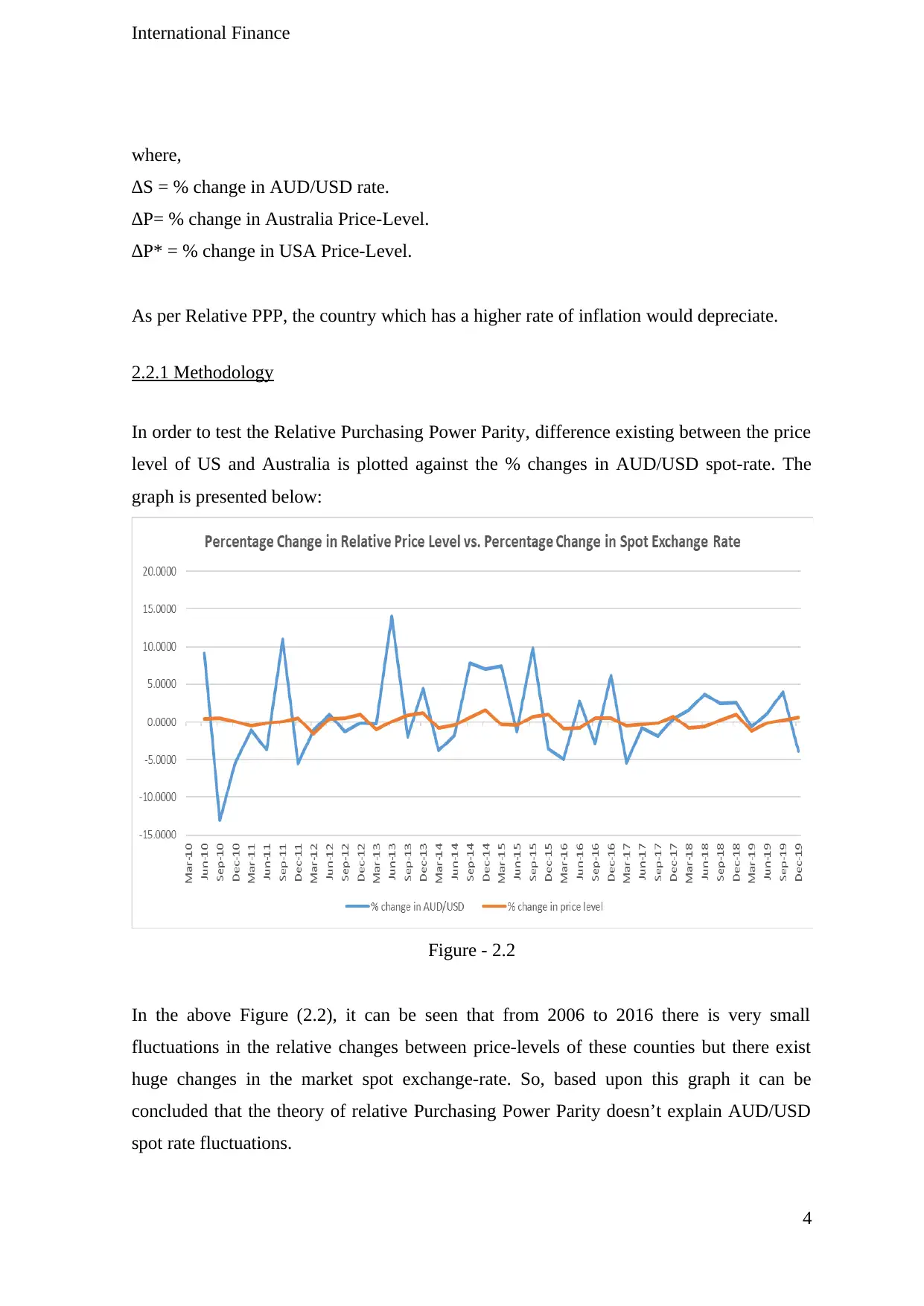

2.2.1 Methodology

In order to test the Relative Purchasing Power Parity, difference existing between the price

level of US and Australia is plotted against the % changes in AUD/USD spot-rate. The

graph is presented below:

Figure - 2.2

In the above Figure (2.2), it can be seen that from 2006 to 2016 there is very small

fluctuations in the relative changes between price-levels of these counties but there exist

huge changes in the market spot exchange-rate. So, based upon this graph it can be

concluded that the theory of relative Purchasing Power Parity doesn’t explain AUD/USD

spot rate fluctuations.

4

where,

∆S = % change in AUD/USD rate.

∆P= % change in Australia Price-Level.

∆P* = % change in USA Price-Level.

As per Relative PPP, the country which has a higher rate of inflation would depreciate.

2.2.1 Methodology

In order to test the Relative Purchasing Power Parity, difference existing between the price

level of US and Australia is plotted against the % changes in AUD/USD spot-rate. The

graph is presented below:

Figure - 2.2

In the above Figure (2.2), it can be seen that from 2006 to 2016 there is very small

fluctuations in the relative changes between price-levels of these counties but there exist

huge changes in the market spot exchange-rate. So, based upon this graph it can be

concluded that the theory of relative Purchasing Power Parity doesn’t explain AUD/USD

spot rate fluctuations.

4

International Finance

2.3. Limitations of PPP

There are certain limitations related to this theory named Purchasing Power Parity (PPP)

which may assist to explain deviations in the movement of actual rate of exchange against

the ones implied through the means of purchasing power parity (PPP).

Certain trade related barriers and discrepancies in values of non-traded items

internationally might act as an origin of price differences arising among the nations and

thereby rejects the hypothesis of purchasing power parity (PPP). Imperfect competition can

even lead to price variations because it’s possible that the same item is selling at some

different prices in many other markets with an objective to maximize the profit of firms.

Additionally, difference in weights and statistical differences while computing price

indices would give a different value of price index, leading to deviations from Purchasing

Power Parity (PPP) (Moon, Page, Rodin and Roy, 2010).

Due to commodity arbitrage, prices would be needed to adjust but since the prices are

usually considered sticky in the short-run, it could adjust but little slowly and gradually

over the period of time. In the long-run, exchange-rate can be predicted using the theory of

PPP because arbitrage turn out to be highly efficient and therefore higher goods are traded.

As visible from the graph depicted above, in short-run, the theory of Purchasing Power

Parity (PPP) can hardly describe movement of exchange rate.

5

2.3. Limitations of PPP

There are certain limitations related to this theory named Purchasing Power Parity (PPP)

which may assist to explain deviations in the movement of actual rate of exchange against

the ones implied through the means of purchasing power parity (PPP).

Certain trade related barriers and discrepancies in values of non-traded items

internationally might act as an origin of price differences arising among the nations and

thereby rejects the hypothesis of purchasing power parity (PPP). Imperfect competition can

even lead to price variations because it’s possible that the same item is selling at some

different prices in many other markets with an objective to maximize the profit of firms.

Additionally, difference in weights and statistical differences while computing price

indices would give a different value of price index, leading to deviations from Purchasing

Power Parity (PPP) (Moon, Page, Rodin and Roy, 2010).

Due to commodity arbitrage, prices would be needed to adjust but since the prices are

usually considered sticky in the short-run, it could adjust but little slowly and gradually

over the period of time. In the long-run, exchange-rate can be predicted using the theory of

PPP because arbitrage turn out to be highly efficient and therefore higher goods are traded.

As visible from the graph depicted above, in short-run, the theory of Purchasing Power

Parity (PPP) can hardly describe movement of exchange rate.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International Finance

3. Interest Rate Parity

Interest-rate parity refers to the theory as per which differences in interest-rate between

two nations is equivalent to the differences between the forward and spot-rate of exchange.

Interest rate parity has a significant role to play in foreign exchange rates, connecting

interest rates, foreign exchange markets, and spot exchange rates (Levich, 2013).

IRP has two components namely, Covered Interest Parity and Uncovered Interest Parity.

3.1. Covered Interest Parity (CIP)

As per the idea of CIP, once the risk associated with exchange rate is covered using the

forward market there should not exist any differences in returns of two nations. Any

difference existing in the interest rates of two nations will be converted to the exchange

rate (forward exchange rate and spot exchange rate) movement in the equal proportion

(Efstathiou, 2019). Hence, the chance of arbitrage would be removed or abolished.

It is expected that a country offering higher rate of interest would will sell at a forward

discount and vice-versa.

where

it = domestic rate of interest

it* = foreign rate of interest

Ft = forward exchange rate

St = spot exchange rate

In order to test for Covered Interest Parity (CIP), difference in interest-rate has been

plotted against percentage change in forward exchange-rate. Due to non-availability of

forward exchange-rate data it would not be possible to test the CIP.

3.2. Unbiased Expectation Theory

It is a theory which assumes that the market stands efficient due to which individual would

be neutral to risk. Therefore, conversion of currency using forward-rate today or expected

spot-rate in future would make no difference to an investor (The Motley Fool, 2016).

6

(1+ it) / (1+ it*) = Ft / St

3. Interest Rate Parity

Interest-rate parity refers to the theory as per which differences in interest-rate between

two nations is equivalent to the differences between the forward and spot-rate of exchange.

Interest rate parity has a significant role to play in foreign exchange rates, connecting

interest rates, foreign exchange markets, and spot exchange rates (Levich, 2013).

IRP has two components namely, Covered Interest Parity and Uncovered Interest Parity.

3.1. Covered Interest Parity (CIP)

As per the idea of CIP, once the risk associated with exchange rate is covered using the

forward market there should not exist any differences in returns of two nations. Any

difference existing in the interest rates of two nations will be converted to the exchange

rate (forward exchange rate and spot exchange rate) movement in the equal proportion

(Efstathiou, 2019). Hence, the chance of arbitrage would be removed or abolished.

It is expected that a country offering higher rate of interest would will sell at a forward

discount and vice-versa.

where

it = domestic rate of interest

it* = foreign rate of interest

Ft = forward exchange rate

St = spot exchange rate

In order to test for Covered Interest Parity (CIP), difference in interest-rate has been

plotted against percentage change in forward exchange-rate. Due to non-availability of

forward exchange-rate data it would not be possible to test the CIP.

3.2. Unbiased Expectation Theory

It is a theory which assumes that the market stands efficient due to which individual would

be neutral to risk. Therefore, conversion of currency using forward-rate today or expected

spot-rate in future would make no difference to an investor (The Motley Fool, 2016).

6

(1+ it) / (1+ it*) = Ft / St

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Finance

where,

Ft = Forward exchange rate

St +1

e = expected future spot rate

3.3. Uncovered Interest Parity (UIP)

Like Covered Interest Parity, UIP has the notion that all the return on investments in the

domestic country and foreign countries must be equal or same. Still, UIP does not cover

long currency position and thereby leave it open to exchange rate fluctuations (Saadon and

Sussman, 2018). Uncovered Interest Parity accepts that both unbiased expectation theory

and Covered Interest Parity theory actually holds.

Thus, uncovered interest rate can be defined as change in relative rate of interest between

the two nations is equivalent to the expected change in exchange rate.

where,

it

❑ = Domestic rate of interest

it

¿ = Foreign rate of interest

St +1

e = expected future spot rate

St = spot exchange rate

3.3.1. Methodology

For testing theory of Uncovered Interest Parity, we are required to subtract differences in

rate of interest between two nations from % change in the exchange-rates. However,

regarding future spot rate, data related to forward-rate as well as expected future spot-rate

is unavailable. Since, we did not get the data related to expected future spot rates, we

7

Ft = St +1

e

(1+it) (1+it*) = ¿ ¿) / (St)

where,

Ft = Forward exchange rate

St +1

e = expected future spot rate

3.3. Uncovered Interest Parity (UIP)

Like Covered Interest Parity, UIP has the notion that all the return on investments in the

domestic country and foreign countries must be equal or same. Still, UIP does not cover

long currency position and thereby leave it open to exchange rate fluctuations (Saadon and

Sussman, 2018). Uncovered Interest Parity accepts that both unbiased expectation theory

and Covered Interest Parity theory actually holds.

Thus, uncovered interest rate can be defined as change in relative rate of interest between

the two nations is equivalent to the expected change in exchange rate.

where,

it

❑ = Domestic rate of interest

it

¿ = Foreign rate of interest

St +1

e = expected future spot rate

St = spot exchange rate

3.3.1. Methodology

For testing theory of Uncovered Interest Parity, we are required to subtract differences in

rate of interest between two nations from % change in the exchange-rates. However,

regarding future spot rate, data related to forward-rate as well as expected future spot-rate

is unavailable. Since, we did not get the data related to expected future spot rates, we

7

Ft = St +1

e

(1+it) (1+it*) = ¿ ¿) / (St)

International Finance

would assume that market is efficient as well as rational. Efficient and rational market

means actual spot exchange-rate in time t+1 would be similar to the expected future spot-

rate of an investor.

The above assumption can be represented as follows:

where,

St +1

e = Expected future spot rate

St+1 = Actual future spot rate

Therefore, Uncovered Interest Parity can be computed by:

Where

it = domestic interest rate

it

¿ = foreign interest rate

St+1 = actual future spot rate

St = spot exchange rate

For testing the validity of the theory of UIP, we will use here standard deviation with

confidence interval of 95 per cent. Therefore, we need to use ±2σ and will see whether the

graph would fall within it.

8

St +1

e

= St+1

[it-it*]-[St+1-St/St] = 0

would assume that market is efficient as well as rational. Efficient and rational market

means actual spot exchange-rate in time t+1 would be similar to the expected future spot-

rate of an investor.

The above assumption can be represented as follows:

where,

St +1

e = Expected future spot rate

St+1 = Actual future spot rate

Therefore, Uncovered Interest Parity can be computed by:

Where

it = domestic interest rate

it

¿ = foreign interest rate

St+1 = actual future spot rate

St = spot exchange rate

For testing the validity of the theory of UIP, we will use here standard deviation with

confidence interval of 95 per cent. Therefore, we need to use ±2σ and will see whether the

graph would fall within it.

8

St +1

e

= St+1

[it-it*]-[St+1-St/St] = 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International Finance

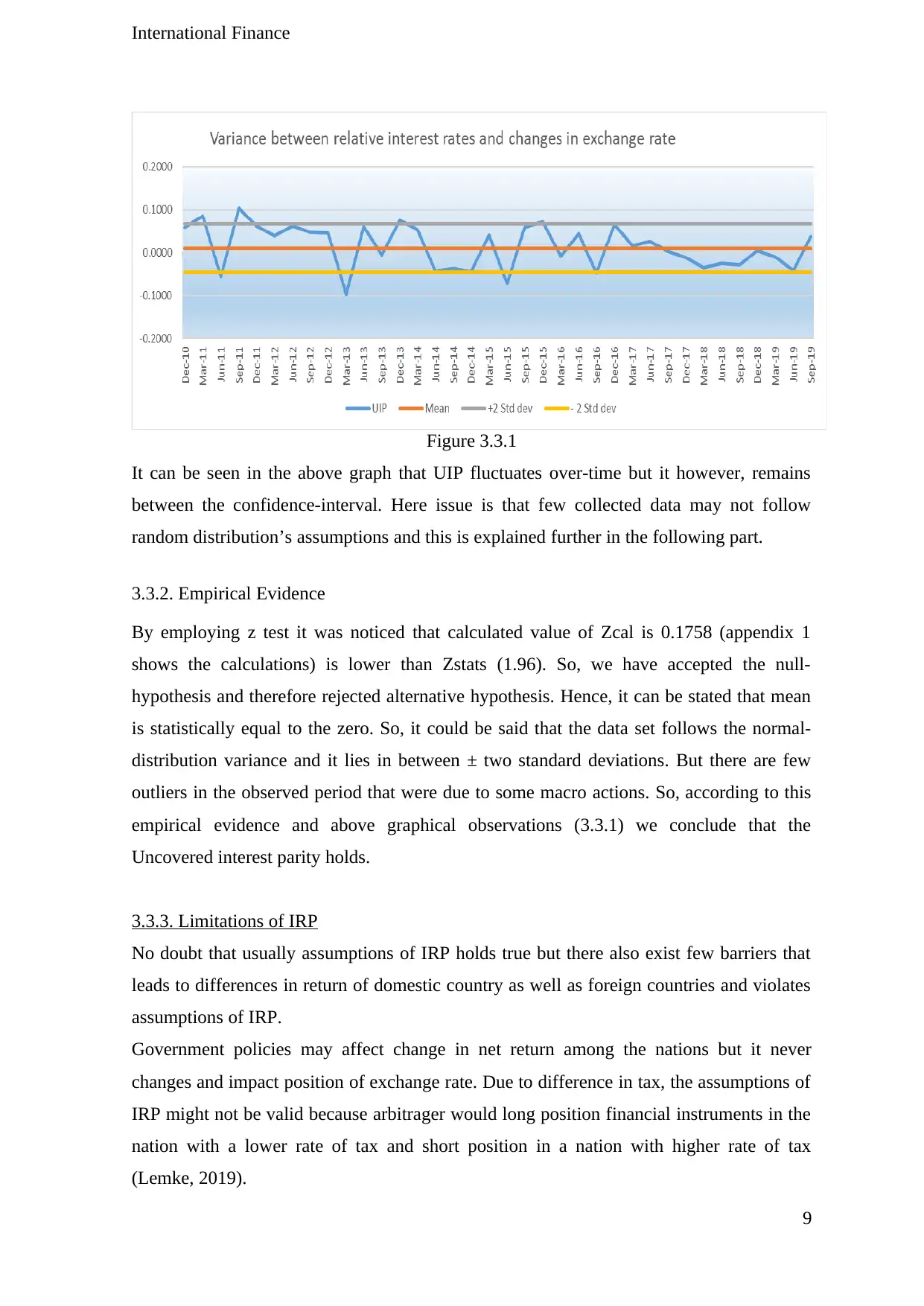

Figure 3.3.1

It can be seen in the above graph that UIP fluctuates over-time but it however, remains

between the confidence-interval. Here issue is that few collected data may not follow

random distribution’s assumptions and this is explained further in the following part.

3.3.2. Empirical Evidence

By employing z test it was noticed that calculated value of Zcal is 0.1758 (appendix 1

shows the calculations) is lower than Zstats (1.96). So, we have accepted the null-

hypothesis and therefore rejected alternative hypothesis. Hence, it can be stated that mean

is statistically equal to the zero. So, it could be said that the data set follows the normal-

distribution variance and it lies in between ± two standard deviations. But there are few

outliers in the observed period that were due to some macro actions. So, according to this

empirical evidence and above graphical observations (3.3.1) we conclude that the

Uncovered interest parity holds.

3.3.3. Limitations of IRP

No doubt that usually assumptions of IRP holds true but there also exist few barriers that

leads to differences in return of domestic country as well as foreign countries and violates

assumptions of IRP.

Government policies may affect change in net return among the nations but it never

changes and impact position of exchange rate. Due to difference in tax, the assumptions of

IRP might not be valid because arbitrager would long position financial instruments in the

nation with a lower rate of tax and short position in a nation with higher rate of tax

(Lemke, 2019).

9

Figure 3.3.1

It can be seen in the above graph that UIP fluctuates over-time but it however, remains

between the confidence-interval. Here issue is that few collected data may not follow

random distribution’s assumptions and this is explained further in the following part.

3.3.2. Empirical Evidence

By employing z test it was noticed that calculated value of Zcal is 0.1758 (appendix 1

shows the calculations) is lower than Zstats (1.96). So, we have accepted the null-

hypothesis and therefore rejected alternative hypothesis. Hence, it can be stated that mean

is statistically equal to the zero. So, it could be said that the data set follows the normal-

distribution variance and it lies in between ± two standard deviations. But there are few

outliers in the observed period that were due to some macro actions. So, according to this

empirical evidence and above graphical observations (3.3.1) we conclude that the

Uncovered interest parity holds.

3.3.3. Limitations of IRP

No doubt that usually assumptions of IRP holds true but there also exist few barriers that

leads to differences in return of domestic country as well as foreign countries and violates

assumptions of IRP.

Government policies may affect change in net return among the nations but it never

changes and impact position of exchange rate. Due to difference in tax, the assumptions of

IRP might not be valid because arbitrager would long position financial instruments in the

nation with a lower rate of tax and short position in a nation with higher rate of tax

(Lemke, 2019).

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

International Finance

IRP assumes that there exists an infinite fund for currency arbitrage which cannot be held

realistic. When future contracts and forward contracts are not available for the hedging

means, uncovered interest-rate parity cannot be held in the actual world.

References

1. Efstathiou, K. (2019). The breakdown of the covered interest rate parity condition.

[online] Available at: https://www.bruegel.org/2019/07/the-breakdown-of-the-

covered-interest-rate-parity-condition/ [Accessed 23 Mar. 2020].

2. IG. (n.d.). What is purchasing power parity (PPP)?. [online] Available at:

https://www.ig.com/en/trading-strategies/what-is-purchasing-power-parity--ppp---

191106. [Accessed 23 Mar. 2020].

3. Lemke, T. (2019). What Is Interest Rate Parity?. [online] Available at:

https://www.thebalance.com/what-is-interest-rate-parity-4164249 [Accessed 23

Mar. 2020].

4. Levich, R.M. (2013). Interest Rate Parity. [online] Available at:

https://www.sciencedirect.com/topics/economics-econometrics-and-finance/

interest-rate-parity [Accessed 23 Mar. 2020].

5. Moon, S. Page, S. Rodin, B. and Roy, D. (2010). Purchasing Power Parity

measures: advantages and limitations. [online] Available at:

https://www.odi.org/sites/odi.org.uk/files/odi-assets/publications-opinion-files/

6018.pdf [Accessed 23 Mar. 2020].

6. Nasdaq. (n.d.). Glossary of Stock Market Terms. [online] Available at:

https://www.nasdaq.com/glossary/r/relative-purchasing-power-parity. [Accessed 23

Mar. 2020].

10

IRP assumes that there exists an infinite fund for currency arbitrage which cannot be held

realistic. When future contracts and forward contracts are not available for the hedging

means, uncovered interest-rate parity cannot be held in the actual world.

References

1. Efstathiou, K. (2019). The breakdown of the covered interest rate parity condition.

[online] Available at: https://www.bruegel.org/2019/07/the-breakdown-of-the-

covered-interest-rate-parity-condition/ [Accessed 23 Mar. 2020].

2. IG. (n.d.). What is purchasing power parity (PPP)?. [online] Available at:

https://www.ig.com/en/trading-strategies/what-is-purchasing-power-parity--ppp---

191106. [Accessed 23 Mar. 2020].

3. Lemke, T. (2019). What Is Interest Rate Parity?. [online] Available at:

https://www.thebalance.com/what-is-interest-rate-parity-4164249 [Accessed 23

Mar. 2020].

4. Levich, R.M. (2013). Interest Rate Parity. [online] Available at:

https://www.sciencedirect.com/topics/economics-econometrics-and-finance/

interest-rate-parity [Accessed 23 Mar. 2020].

5. Moon, S. Page, S. Rodin, B. and Roy, D. (2010). Purchasing Power Parity

measures: advantages and limitations. [online] Available at:

https://www.odi.org/sites/odi.org.uk/files/odi-assets/publications-opinion-files/

6018.pdf [Accessed 23 Mar. 2020].

6. Nasdaq. (n.d.). Glossary of Stock Market Terms. [online] Available at:

https://www.nasdaq.com/glossary/r/relative-purchasing-power-parity. [Accessed 23

Mar. 2020].

10

International Finance

7. OECD. (n.d.). Purchasing power parities (PPP). [online] Available at:

https://data.oecd.org/conversion/purchasing-power-parities-ppp.htm [Accessed 23

Mar. 2020].

8. Saadon, Y. and Sussman, N. (2018). Nominal exchange rate dynamics and

monetary policy: Uncovered interest rate parity and purchasing power parity

revisited. [online] Available at: https://voxeu.org/article/uncovered-interest-rate-

parity-and-purchasing-power-parity-revisited [Accessed 23 Mar. 2020].

9. The Motley Fool. (2016). How to Calculate Unbiased Expectations Theory.

[online] Available at: https://www.fool.com/knowledge-center/how-to-calculate-

unbiased-expectations-theory.aspx [Accessed 23 Mar. 2020].

Appendix

To ensure UIP validity, we have performed hypothesis testing:

1st step

H0: μ = 0

H1: μ ≠ 0

2nd step

X = 0.01

σ = 0.0569

3rd step

Z0.05/2 = 1.96

If Calculated Z > Zstat, we reject H0

If calculated Z < Zstat, we do not reject H0

4th step

Zcal = 0.1758

5th step

11

7. OECD. (n.d.). Purchasing power parities (PPP). [online] Available at:

https://data.oecd.org/conversion/purchasing-power-parities-ppp.htm [Accessed 23

Mar. 2020].

8. Saadon, Y. and Sussman, N. (2018). Nominal exchange rate dynamics and

monetary policy: Uncovered interest rate parity and purchasing power parity

revisited. [online] Available at: https://voxeu.org/article/uncovered-interest-rate-

parity-and-purchasing-power-parity-revisited [Accessed 23 Mar. 2020].

9. The Motley Fool. (2016). How to Calculate Unbiased Expectations Theory.

[online] Available at: https://www.fool.com/knowledge-center/how-to-calculate-

unbiased-expectations-theory.aspx [Accessed 23 Mar. 2020].

Appendix

To ensure UIP validity, we have performed hypothesis testing:

1st step

H0: μ = 0

H1: μ ≠ 0

2nd step

X = 0.01

σ = 0.0569

3rd step

Z0.05/2 = 1.96

If Calculated Z > Zstat, we reject H0

If calculated Z < Zstat, we do not reject H0

4th step

Zcal = 0.1758

5th step

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.