International Finance & Decision Making: Kings Bars Analysis

VerifiedAdded on 2023/05/29

|16

|4530

|445

Report

AI Summary

This report evaluates the proposal by the Purchase Manager of Morden Engineering regarding purchasing products instead of manufacturing them, highlighting potential revenue generation. It analyzes arguments from both the Purchase and Production Managers, considering factors like cost reduction, machine value depreciation, and cost of capital. The report identifies key issues for financial analysis, including cash flow reliability, assumption significance, inflation rate impact, qualitative factors, ethical considerations, and short-term incentive influences. A financial appraisal recommends Morden Engineering consider the purchasing option, weighing potential risks and alternatives like warehousing costs and working capital needs. The analysis ultimately favors purchasing due to higher revenue potential and reduced expenses, exceeding income from sales.

Running head: INTERNATIONAL FINANCE AND DECISION MAKING

International Finance and Decision Making

Name of the Student:

Name of the University:

Authors Note:

International Finance and Decision Making

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE AND DECISION MAKING

1

Table of Contents

Introduction:...............................................................................................................................2

i. Evaluating the arguments utilized by the purchasing and the production managers to

support their cases:.....................................................................................................................2

ii. Identifying the factors and important issues that need to be taken into account while doing

financial analysis:.......................................................................................................................5

iii. Providing recommendation with the financial appraisal for detecting the decision that

needs to be made by Morden Engineering:................................................................................7

iv. Identifying the possible risk of adopting the recommendations, while portraying the

alternatives that can be considered by Morden Engineering:..................................................10

Conclusion:..............................................................................................................................12

Reference and Bibliography:....................................................................................................13

1

Table of Contents

Introduction:...............................................................................................................................2

i. Evaluating the arguments utilized by the purchasing and the production managers to

support their cases:.....................................................................................................................2

ii. Identifying the factors and important issues that need to be taken into account while doing

financial analysis:.......................................................................................................................5

iii. Providing recommendation with the financial appraisal for detecting the decision that

needs to be made by Morden Engineering:................................................................................7

iv. Identifying the possible risk of adopting the recommendations, while portraying the

alternatives that can be considered by Morden Engineering:..................................................10

Conclusion:..............................................................................................................................12

Reference and Bibliography:....................................................................................................13

INTERNATIONAL FINANCE AND DECISION MAKING

2

Introduction:

The assessment mainly evaluates the overall Proposal that has been presented by the

Purchase Manager of the organization. The Purchase Manager has directly highlighted that

the organization can purchase the products instead of making it, as it will generate higher the

revenue for the organization. The Purchase Manager has highlighted that the cost that is in

code in producing the products would be reduced, when the company switches to purchase in

the product from other company. This would eventually help in supporting higher levels of

revenue, as it will reduce the expenses of the manufacturing process. Adequate Factors and

issues that need to be taken into consideration are directly highlighted in the assessment.

Moreover, adequate recommendation has been provided with financial appraisal techniques

to identify the appropriate method that can be used by a Morden Engineering. Relevant

analysis has been conducted on the remarks of Purchase Manager and Production Manager

for identifying the benefits that can be presented to the organization.

i. Evaluating the arguments utilized by the purchasing and the production managers to

support their cases:

The study directly provides information regarding the arguments that has been

presented by the purchasing and production managers. Therefore, from the analysis of the

arguments presented by the Purchase Manager, it could be identified that the organization can

benefit from switching to buying phase from the manufacturing phase. The purchasing

manager of the organization who has highlighted the attractive offer of increasing the profits

by £96,000 each year has provided adequate analysis. The purchasing manager has directly

indicated that coaching the parts would eventually help the organization to reduce its overall

cost of sales, which would eventually boost the gross profit and net profit. The new

technology that has been developed by the competitive manufacturer has allowed them to

2

Introduction:

The assessment mainly evaluates the overall Proposal that has been presented by the

Purchase Manager of the organization. The Purchase Manager has directly highlighted that

the organization can purchase the products instead of making it, as it will generate higher the

revenue for the organization. The Purchase Manager has highlighted that the cost that is in

code in producing the products would be reduced, when the company switches to purchase in

the product from other company. This would eventually help in supporting higher levels of

revenue, as it will reduce the expenses of the manufacturing process. Adequate Factors and

issues that need to be taken into consideration are directly highlighted in the assessment.

Moreover, adequate recommendation has been provided with financial appraisal techniques

to identify the appropriate method that can be used by a Morden Engineering. Relevant

analysis has been conducted on the remarks of Purchase Manager and Production Manager

for identifying the benefits that can be presented to the organization.

i. Evaluating the arguments utilized by the purchasing and the production managers to

support their cases:

The study directly provides information regarding the arguments that has been

presented by the purchasing and production managers. Therefore, from the analysis of the

arguments presented by the Purchase Manager, it could be identified that the organization can

benefit from switching to buying phase from the manufacturing phase. The purchasing

manager of the organization who has highlighted the attractive offer of increasing the profits

by £96,000 each year has provided adequate analysis. The purchasing manager has directly

indicated that coaching the parts would eventually help the organization to reduce its overall

cost of sales, which would eventually boost the gross profit and net profit. The new

technology that has been developed by the competitive manufacturer has allowed them to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE AND DECISION MAKING

3

reduce the cost of production, which eventually would allow the organization to acquire the

product at 83 pence per unit. On the other hand, the manufacturing cost of the parts has been

calculated to be at the levels of 90 pence. There is a direct benefit of 7 pence, if the

organization switches from manufacturing to buying parts for sale. This benefit would allow

the organization to claim higher revenues and net income over the period of time (Gotze,

Northcott and Schuster 2016).

On the other hand, the production manager provides all the relevant information

regarding the manufacturing process of the organization, which will be halted if purchase is

chosen above manufacturing. The production manager has directly indicated that the machine

is relatively new weight loss of £35,000 will be incurred by the organization if the machine is

sold within one year, as the machine is made to support a specific manufacturing process and

would have no market value. Therefore, the organization will only be able to acquire £5,000

after selling the new machine, which will increase the relevant laws for the organization. The

production manager also highlights that there is only savings of £7,000 every year if the

organizations, which is to buying rather than manufacturing the parts for sale. Moreover, the

manager also highlights that the cost benefit that is produced from purchasing is only

calculated up to 12%, which is not near the estimated cost of capital of the organization.

Thus, the production manager directly indicates that the organization should not adapt to

buying the parts for sale instead, it should continue the manufacturing process (Harris 2017).

There were relevant loopholes in the proposal of the production manager, where no

adequate information has been provided all the future performance of the organization. The

production manager has only highlighted one aspect of the manufacturing process from

which the benefit will be generated by the organization, if the manufacturing process is

discontinued. However, other benefits can be incurred when selecting the Purchase option in

contrary to manufacturing. Therefore, the proposal by the production manager does not

3

reduce the cost of production, which eventually would allow the organization to acquire the

product at 83 pence per unit. On the other hand, the manufacturing cost of the parts has been

calculated to be at the levels of 90 pence. There is a direct benefit of 7 pence, if the

organization switches from manufacturing to buying parts for sale. This benefit would allow

the organization to claim higher revenues and net income over the period of time (Gotze,

Northcott and Schuster 2016).

On the other hand, the production manager provides all the relevant information

regarding the manufacturing process of the organization, which will be halted if purchase is

chosen above manufacturing. The production manager has directly indicated that the machine

is relatively new weight loss of £35,000 will be incurred by the organization if the machine is

sold within one year, as the machine is made to support a specific manufacturing process and

would have no market value. Therefore, the organization will only be able to acquire £5,000

after selling the new machine, which will increase the relevant laws for the organization. The

production manager also highlights that there is only savings of £7,000 every year if the

organizations, which is to buying rather than manufacturing the parts for sale. Moreover, the

manager also highlights that the cost benefit that is produced from purchasing is only

calculated up to 12%, which is not near the estimated cost of capital of the organization.

Thus, the production manager directly indicates that the organization should not adapt to

buying the parts for sale instead, it should continue the manufacturing process (Harris 2017).

There were relevant loopholes in the proposal of the production manager, where no

adequate information has been provided all the future performance of the organization. The

production manager has only highlighted one aspect of the manufacturing process from

which the benefit will be generated by the organization, if the manufacturing process is

discontinued. However, other benefits can be incurred when selecting the Purchase option in

contrary to manufacturing. Therefore, the proposal by the production manager does not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE AND DECISION MAKING

4

provide adequate information regarding the benefits that could be provided from the

manufacturing process. Furthermore, after analyzing the production managers proposal

relevant limitation has been highlighted, which indicates that choosing the manufacturing

process for the organization will not be beneficial. Moreover, the benefits that has been

proposed by the production manager has directly depicted the Additional benefits that can be

generated by the organization after selecting purchase process in contrary to the

manufacturing process (Bader, Al-Nawaiseh and Nawaiseh 2018).

After analyzing, the proposal of Purchase Manager relevant benefits that could be

generated by the organization has been identified. These benefits would eventually allow the

organization to improve its profitability in the long run and increases cash Reserves. The

Purchase Manager has directly provided information regarding the overall benefits and

income that could be generated by using for cheese option for the parts. Moreover, the

additional benefits highlighted by production manager would also be added to the benefits of

purchase in contrary to production of parts. Moreover, the additional cost of machinery has

also been highlighted that needs to be accommodated into the benefits produced by the

Purchase option for the organization. Moreover, expenses on warehousing and working

capital, as adequate inventory needs to be maintained by the organization throughout the

year. This maintenance of high inventory was not needed in manufacturing process, where

the batch purchasing process would eventually increase the inventory stock of the

organization (Brisley et al. 2016). However, the proposal for purchasing the path is more

reliable as the company will generate higher revenues while reducing if expenses and

exceeding the level of income from sales.

4

provide adequate information regarding the benefits that could be provided from the

manufacturing process. Furthermore, after analyzing the production managers proposal

relevant limitation has been highlighted, which indicates that choosing the manufacturing

process for the organization will not be beneficial. Moreover, the benefits that has been

proposed by the production manager has directly depicted the Additional benefits that can be

generated by the organization after selecting purchase process in contrary to the

manufacturing process (Bader, Al-Nawaiseh and Nawaiseh 2018).

After analyzing, the proposal of Purchase Manager relevant benefits that could be

generated by the organization has been identified. These benefits would eventually allow the

organization to improve its profitability in the long run and increases cash Reserves. The

Purchase Manager has directly provided information regarding the overall benefits and

income that could be generated by using for cheese option for the parts. Moreover, the

additional benefits highlighted by production manager would also be added to the benefits of

purchase in contrary to production of parts. Moreover, the additional cost of machinery has

also been highlighted that needs to be accommodated into the benefits produced by the

Purchase option for the organization. Moreover, expenses on warehousing and working

capital, as adequate inventory needs to be maintained by the organization throughout the

year. This maintenance of high inventory was not needed in manufacturing process, where

the batch purchasing process would eventually increase the inventory stock of the

organization (Brisley et al. 2016). However, the proposal for purchasing the path is more

reliable as the company will generate higher revenues while reducing if expenses and

exceeding the level of income from sales.

INTERNATIONAL FINANCE AND DECISION MAKING

5

ii. Identifying the factors and important issues that need to be taken into account while

doing financial analysis:

The relevant issues and factors that need to be addressed by the organization while

conducting adequate financial analysis of a project. The financial analysis is relatively

conducted on the basis of the presumption and assumptions that has been conducted by the

managers. the assumptions made by the organization needs to be accurate while making

analyzing certain project, as it might directly have negative impact on its performance in the

long run (Alkaraan 2016). There are certain issues and factors that need to be addressed by

the organization while conducting capital budgeting process, which are depicted as follows.

Reliability of the estimated cash flow:

The organization needs to identify whether the estimated cash flows that have been

presented by the managers are relatively reliable or an assumption that is made. This analysis

would eventually allow the organization to determine the concrete proof of the benefits that

could be generated from the particular project. This would eventually allow the organization

to identify the financial benefits that could be presented by the project and segregate any kind

of manipulation or exaggeration that might be conducted by the managers while presenting

the proposal (Awojobi and Jenkins 2016).

Significance of the assumptions:

The assumptions that is taken by the managers while presenting the project proposal

needs to be evaluated by the organization during the financial analysis. This evaluation can

directly identify the level of improvements and incomes that could be generated from the new

project, while disclosing any kind of limitations or hindrance that might negatively affect the

current financial position of the organization. The analysis of the assumptions would

eventually allow the organization to understand whether the manager has adequately

5

ii. Identifying the factors and important issues that need to be taken into account while

doing financial analysis:

The relevant issues and factors that need to be addressed by the organization while

conducting adequate financial analysis of a project. The financial analysis is relatively

conducted on the basis of the presumption and assumptions that has been conducted by the

managers. the assumptions made by the organization needs to be accurate while making

analyzing certain project, as it might directly have negative impact on its performance in the

long run (Alkaraan 2016). There are certain issues and factors that need to be addressed by

the organization while conducting capital budgeting process, which are depicted as follows.

Reliability of the estimated cash flow:

The organization needs to identify whether the estimated cash flows that have been

presented by the managers are relatively reliable or an assumption that is made. This analysis

would eventually allow the organization to determine the concrete proof of the benefits that

could be generated from the particular project. This would eventually allow the organization

to identify the financial benefits that could be presented by the project and segregate any kind

of manipulation or exaggeration that might be conducted by the managers while presenting

the proposal (Awojobi and Jenkins 2016).

Significance of the assumptions:

The assumptions that is taken by the managers while presenting the project proposal

needs to be evaluated by the organization during the financial analysis. This evaluation can

directly identify the level of improvements and incomes that could be generated from the new

project, while disclosing any kind of limitations or hindrance that might negatively affect the

current financial position of the organization. The analysis of the assumptions would

eventually allow the organization to understand whether the manager has adequately

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE AND DECISION MAKING

6

conducted the research before presenting the proposed project. This analysis of the

assumptions would also highlight whether the project is a viable option for the organization,

which can generate higher returns in the long run (Jorge-Calderon 2016).

Inflation rate:

Inflation rate information needs to be taken into consideration by the organization

while evaluating the financial performance of the project. Inflation rate directly Erode future

benefits that can be generated by a project. Hence, the organization needs to conduct

adequate financial analysis on the benefits that will be generated by the proposed project with

the inflation rate. This comparison of the inflation rate with the future incomes would

eventually help the organization to determine the actual time value of the investment. This

would eventually allow the organization to make adequate investment decisions on the

project, which could raise the level of revenues in the long run and increase firm value.

Identifying the qualitative factors:

The organization also needs to identify the qualitative factors that is affecting the

proposed project, which would eventually help in detecting whether the project would have a

positive impact on its performance. The qualitative factors could be the legal cost,

competition and other factors that might negatively affect the organization if the project is

adopted. Moreover, the analysis would eventually help in identifying whether the proposed

project is suitable for the organization. Furthermore, relevant limitations of the project can be

identified from the qualitative factors, which would help the organization with adequate

investment decision (Sims, Powell and Vidgen 2015).

Ethical issue:

The ethical issue also needs to be evaluated by the organization before considering the

project for investment purposes. The investment appraisal technique that has been used on the

6

conducted the research before presenting the proposed project. This analysis of the

assumptions would also highlight whether the project is a viable option for the organization,

which can generate higher returns in the long run (Jorge-Calderon 2016).

Inflation rate:

Inflation rate information needs to be taken into consideration by the organization

while evaluating the financial performance of the project. Inflation rate directly Erode future

benefits that can be generated by a project. Hence, the organization needs to conduct

adequate financial analysis on the benefits that will be generated by the proposed project with

the inflation rate. This comparison of the inflation rate with the future incomes would

eventually help the organization to determine the actual time value of the investment. This

would eventually allow the organization to make adequate investment decisions on the

project, which could raise the level of revenues in the long run and increase firm value.

Identifying the qualitative factors:

The organization also needs to identify the qualitative factors that is affecting the

proposed project, which would eventually help in detecting whether the project would have a

positive impact on its performance. The qualitative factors could be the legal cost,

competition and other factors that might negatively affect the organization if the project is

adopted. Moreover, the analysis would eventually help in identifying whether the proposed

project is suitable for the organization. Furthermore, relevant limitations of the project can be

identified from the qualitative factors, which would help the organization with adequate

investment decision (Sims, Powell and Vidgen 2015).

Ethical issue:

The ethical issue also needs to be evaluated by the organization before considering the

project for investment purposes. The investment appraisal technique that has been used on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE AND DECISION MAKING

7

analysis of the project is a relatively based on the information that is provided by the manager

regarding the future prospects of the investment. Therefore, the ethical consideration needs to

be provided by the manager for analyzing the benefits that could be generated from the

project. This addicted vehicle consideration would eventually allow the organization to

validate the findings that is been provided by the project manager before accepting the

proposal (Kengatharan and Nurullah 2018).

Detecting the impact of short-term incentive on long-term decision:

The relevant analysis needs to be conducted by the organization for detecting the

impact of short-term incentives on the long-term decisions. This analysis would eventually

help in determining whether the proposed project would have would only benefit the

organization for short term, while entering the future continuity of the company. This

analysis would relatively help in determining whether the proposed project would continue to

provide benefits to the organization even in short term and long term. Therefore, the company

would eventually detect whether the proposed project is a viable investment option that can

generate profits and improve the long-term prospect of the organization (Schlegel, Frank and

Britzelmaier 2016).

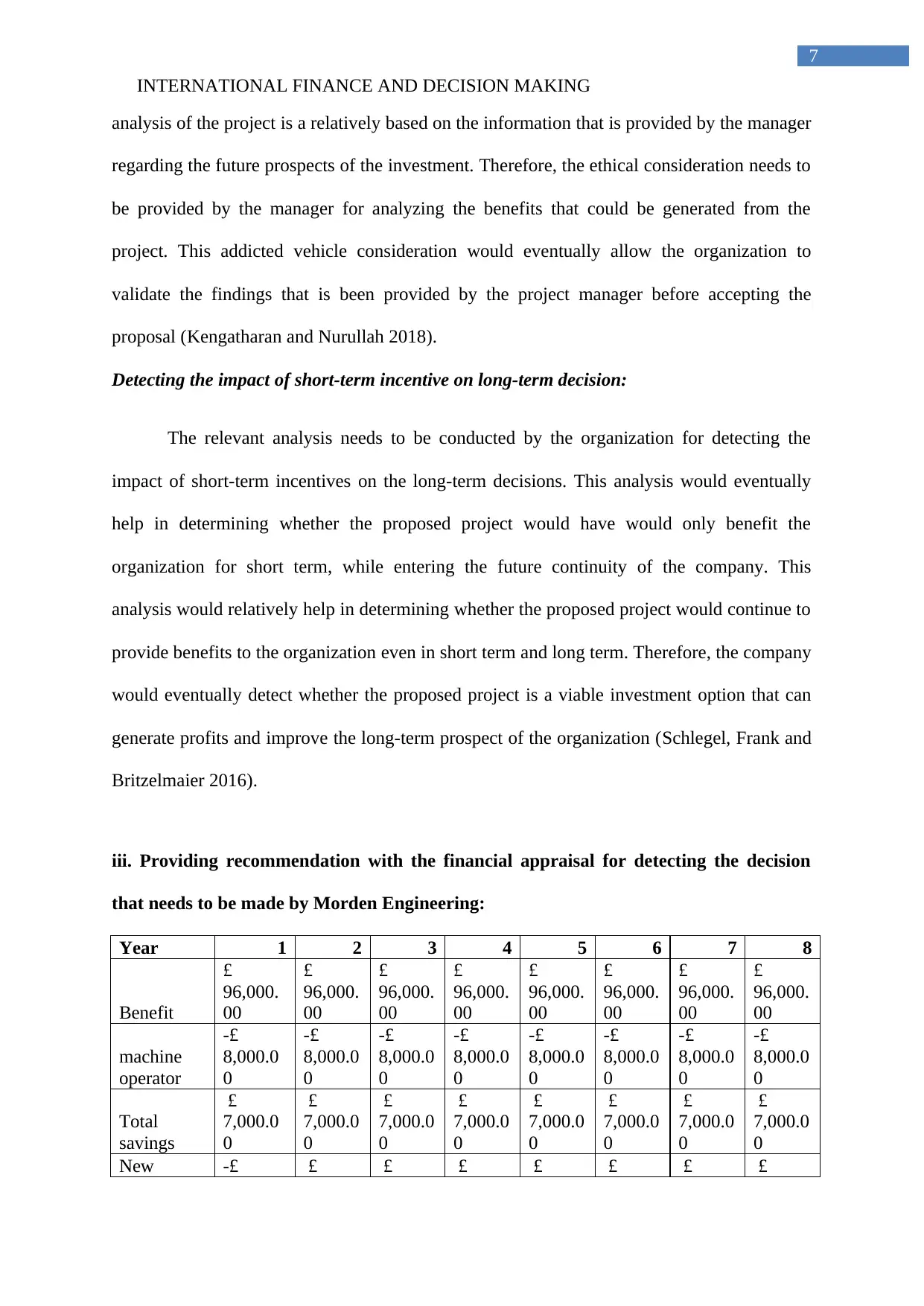

iii. Providing recommendation with the financial appraisal for detecting the decision

that needs to be made by Morden Engineering:

Year 1 2 3 4 5 6 7 8

Benefit

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

machine

operator

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

Total

savings

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

New -£ £ £ £ £ £ £ £

7

analysis of the project is a relatively based on the information that is provided by the manager

regarding the future prospects of the investment. Therefore, the ethical consideration needs to

be provided by the manager for analyzing the benefits that could be generated from the

project. This addicted vehicle consideration would eventually allow the organization to

validate the findings that is been provided by the project manager before accepting the

proposal (Kengatharan and Nurullah 2018).

Detecting the impact of short-term incentive on long-term decision:

The relevant analysis needs to be conducted by the organization for detecting the

impact of short-term incentives on the long-term decisions. This analysis would eventually

help in determining whether the proposed project would have would only benefit the

organization for short term, while entering the future continuity of the company. This

analysis would relatively help in determining whether the proposed project would continue to

provide benefits to the organization even in short term and long term. Therefore, the company

would eventually detect whether the proposed project is a viable investment option that can

generate profits and improve the long-term prospect of the organization (Schlegel, Frank and

Britzelmaier 2016).

iii. Providing recommendation with the financial appraisal for detecting the decision

that needs to be made by Morden Engineering:

Year 1 2 3 4 5 6 7 8

Benefit

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

£

96,000.

00

machine

operator

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

-£

8,000.0

0

Total

savings

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

£

7,000.0

0

New -£ £ £ £ £ £ £ £

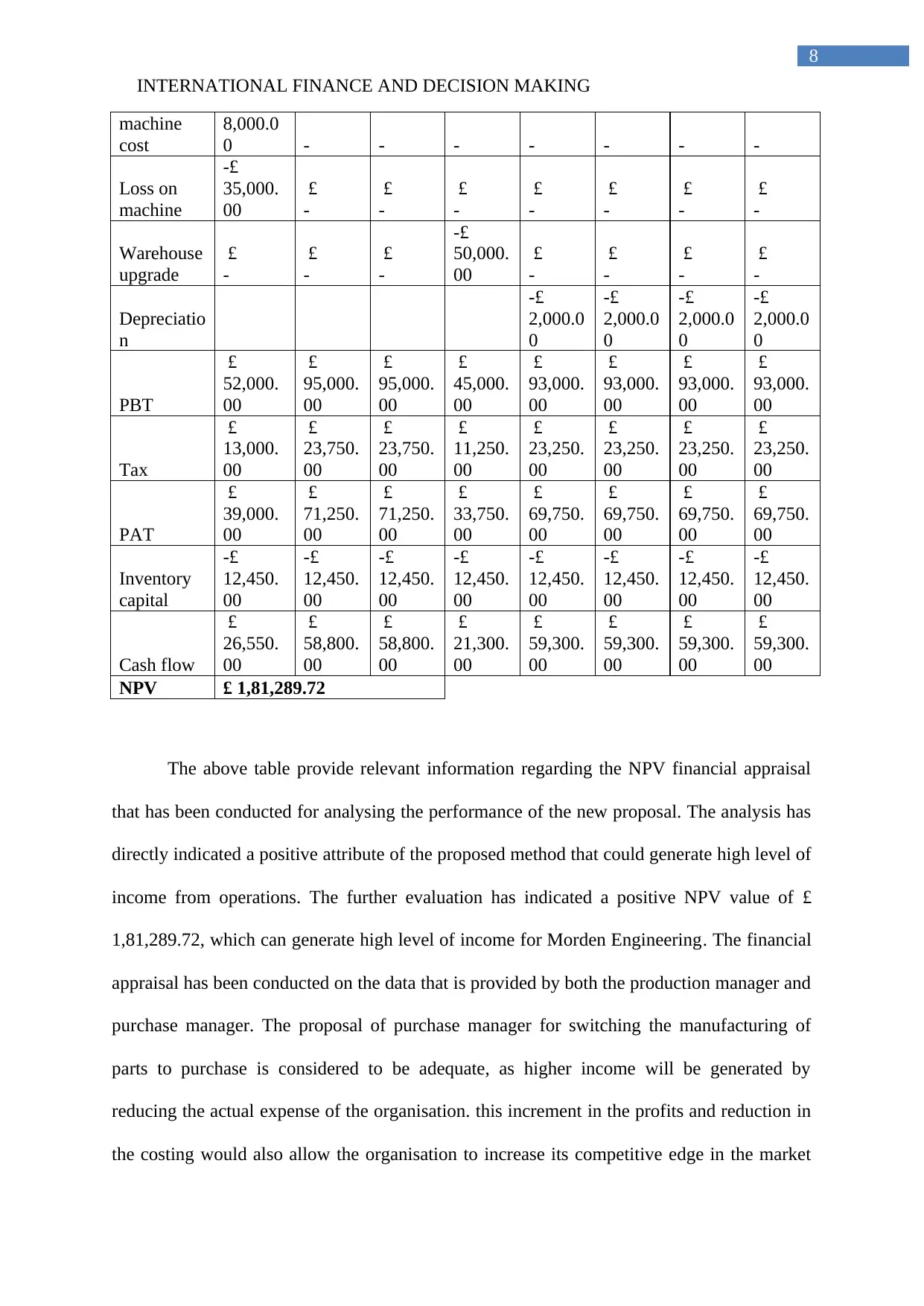

INTERNATIONAL FINANCE AND DECISION MAKING

8

machine

cost

8,000.0

0 - - - - - - -

Loss on

machine

-£

35,000.

00

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Warehouse

upgrade

£

-

£

-

£

-

-£

50,000.

00

£

-

£

-

£

-

£

-

Depreciatio

n

-£

2,000.0

0

-£

2,000.0

0

-£

2,000.0

0

-£

2,000.0

0

PBT

£

52,000.

00

£

95,000.

00

£

95,000.

00

£

45,000.

00

£

93,000.

00

£

93,000.

00

£

93,000.

00

£

93,000.

00

Tax

£

13,000.

00

£

23,750.

00

£

23,750.

00

£

11,250.

00

£

23,250.

00

£

23,250.

00

£

23,250.

00

£

23,250.

00

PAT

£

39,000.

00

£

71,250.

00

£

71,250.

00

£

33,750.

00

£

69,750.

00

£

69,750.

00

£

69,750.

00

£

69,750.

00

Inventory

capital

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

Cash flow

£

26,550.

00

£

58,800.

00

£

58,800.

00

£

21,300.

00

£

59,300.

00

£

59,300.

00

£

59,300.

00

£

59,300.

00

NPV £ 1,81,289.72

The above table provide relevant information regarding the NPV financial appraisal

that has been conducted for analysing the performance of the new proposal. The analysis has

directly indicated a positive attribute of the proposed method that could generate high level of

income from operations. The further evaluation has indicated a positive NPV value of £

1,81,289.72, which can generate high level of income for Morden Engineering. The financial

appraisal has been conducted on the data that is provided by both the production manager and

purchase manager. The proposal of purchase manager for switching the manufacturing of

parts to purchase is considered to be adequate, as higher income will be generated by

reducing the actual expense of the organisation. this increment in the profits and reduction in

the costing would also allow the organisation to increase its competitive edge in the market

8

machine

cost

8,000.0

0 - - - - - - -

Loss on

machine

-£

35,000.

00

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Warehouse

upgrade

£

-

£

-

£

-

-£

50,000.

00

£

-

£

-

£

-

£

-

Depreciatio

n

-£

2,000.0

0

-£

2,000.0

0

-£

2,000.0

0

-£

2,000.0

0

PBT

£

52,000.

00

£

95,000.

00

£

95,000.

00

£

45,000.

00

£

93,000.

00

£

93,000.

00

£

93,000.

00

£

93,000.

00

Tax

£

13,000.

00

£

23,750.

00

£

23,750.

00

£

11,250.

00

£

23,250.

00

£

23,250.

00

£

23,250.

00

£

23,250.

00

PAT

£

39,000.

00

£

71,250.

00

£

71,250.

00

£

33,750.

00

£

69,750.

00

£

69,750.

00

£

69,750.

00

£

69,750.

00

Inventory

capital

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

-£

12,450.

00

Cash flow

£

26,550.

00

£

58,800.

00

£

58,800.

00

£

21,300.

00

£

59,300.

00

£

59,300.

00

£

59,300.

00

£

59,300.

00

NPV £ 1,81,289.72

The above table provide relevant information regarding the NPV financial appraisal

that has been conducted for analysing the performance of the new proposal. The analysis has

directly indicated a positive attribute of the proposed method that could generate high level of

income from operations. The further evaluation has indicated a positive NPV value of £

1,81,289.72, which can generate high level of income for Morden Engineering. The financial

appraisal has been conducted on the data that is provided by both the production manager and

purchase manager. The proposal of purchase manager for switching the manufacturing of

parts to purchase is considered to be adequate, as higher income will be generated by

reducing the actual expense of the organisation. this increment in the profits and reduction in

the costing would also allow the organisation to increase its competitive edge in the market

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTERNATIONAL FINANCE AND DECISION MAKING

9

and generate high level of income from investment. for investments. Abdel-Kader, Dugdale

and Taylor (2018) mentioned hat with the help of investment appraisals techniques the time

value of money is detected, which allow the organisation to detect the most viable investment

option that can increase its profitability in the long run.

The calculations have been provided on the benefits, and expenses that has been

incurred, while making relevant change in the current financial performance. The relevant

income of the project has been accounted under the time value of money, which can

eventually help in detecting the actual income that will be generated from the change in the

operations of the organisation. This change in the operations can eventually help in

determining the level of extra income that can be generated from the new scheme. However,

certain expenses have also been involved in the calculation such as the sale of the new

machine in loss, purchase of new machine for packaging, expansion of the warehouse, and

increment in the salary of the operator. Therefore, the This evaluation has been conducted by

the company for determining the level of income that can be generated from the investment

over the time. However, certain benefits and income that will be generated from the

operations is also incurred in the calculation, which has mainly allowed the organisation to

acquire positive cash flow from operations.

Thus, it could be understood that the proposal made by the purchase manager for

purchasing the parts for sale is viable. In addition, the viability of the proposal is also

supported by the financial analysis and investment appraisal, which indicated a positive

income for the organisation. The company will eventually raise the level of income from

operations if they switch from the traditional manufacturing process to purchasing process.

This move will eventually help the organisation to substantially reduce its cost over time and

improve the level of income that can be generated from operations. Hence, the use of

purchasing method can allow Morden Engineering to generate high level of income, while

9

and generate high level of income from investment. for investments. Abdel-Kader, Dugdale

and Taylor (2018) mentioned hat with the help of investment appraisals techniques the time

value of money is detected, which allow the organisation to detect the most viable investment

option that can increase its profitability in the long run.

The calculations have been provided on the benefits, and expenses that has been

incurred, while making relevant change in the current financial performance. The relevant

income of the project has been accounted under the time value of money, which can

eventually help in detecting the actual income that will be generated from the change in the

operations of the organisation. This change in the operations can eventually help in

determining the level of extra income that can be generated from the new scheme. However,

certain expenses have also been involved in the calculation such as the sale of the new

machine in loss, purchase of new machine for packaging, expansion of the warehouse, and

increment in the salary of the operator. Therefore, the This evaluation has been conducted by

the company for determining the level of income that can be generated from the investment

over the time. However, certain benefits and income that will be generated from the

operations is also incurred in the calculation, which has mainly allowed the organisation to

acquire positive cash flow from operations.

Thus, it could be understood that the proposal made by the purchase manager for

purchasing the parts for sale is viable. In addition, the viability of the proposal is also

supported by the financial analysis and investment appraisal, which indicated a positive

income for the organisation. The company will eventually raise the level of income from

operations if they switch from the traditional manufacturing process to purchasing process.

This move will eventually help the organisation to substantially reduce its cost over time and

improve the level of income that can be generated from operations. Hence, the use of

purchasing method can allow Morden Engineering to generate high level of income, while

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL FINANCE AND DECISION MAKING

10

reducing the expenditure, which is currently being incurred in the manufacturing process

(Elmassri, Harris and Carter 2016).

iv. Identifying the possible risk of adopting the recommendations, while portraying the

alternatives that can be considered by Morden Engineering:

The recommendation provided to Morden Engineering directly indicates that the

organisation can improve its revenue generation capability by reducing the total cost incurred

in its manufacturing process. However, there are certain risk involved in the

recommendation, which can hamper the operations of the organisation in the long run. These

risks are not evaluated on the financial perspective rather from qualitative viewpoint, as the

organisation will face problems from competition. The purchase manager of Morden

engineering has collected a price quotation from the competitor, who has improved the

manufacturing process and reduced the actual cost of making the parts. The risk from rising

competition can be a major concern for the organisation, as the purchase will be conducted

from the competitor. Therefore, accepting the recommendation can reduce the competitive

edge of the organisation, where it will have to fully rely on the competitor for providing the

products for its sales.

This is a major concern for the organisation, which can reduce its competitive edge in

the market and hamper its financial growth. Babatunde (2016) mentioned that the company

can increase their current financial performance by reducing the level of risk involved in its

operations. Hence, the major anticipation of the proposal made by the purchasing manager is

the reduction on cost, which will allow the organisation to increase its profits. However, no

anticipation has been conducted for detecting problems that might increase from the

competitors. There is relevantly high risk involved in discounting the manufacturing process,

as it will make the organisation dependent on its competitors for the parts.

10

reducing the expenditure, which is currently being incurred in the manufacturing process

(Elmassri, Harris and Carter 2016).

iv. Identifying the possible risk of adopting the recommendations, while portraying the

alternatives that can be considered by Morden Engineering:

The recommendation provided to Morden Engineering directly indicates that the

organisation can improve its revenue generation capability by reducing the total cost incurred

in its manufacturing process. However, there are certain risk involved in the

recommendation, which can hamper the operations of the organisation in the long run. These

risks are not evaluated on the financial perspective rather from qualitative viewpoint, as the

organisation will face problems from competition. The purchase manager of Morden

engineering has collected a price quotation from the competitor, who has improved the

manufacturing process and reduced the actual cost of making the parts. The risk from rising

competition can be a major concern for the organisation, as the purchase will be conducted

from the competitor. Therefore, accepting the recommendation can reduce the competitive

edge of the organisation, where it will have to fully rely on the competitor for providing the

products for its sales.

This is a major concern for the organisation, which can reduce its competitive edge in

the market and hamper its financial growth. Babatunde (2016) mentioned that the company

can increase their current financial performance by reducing the level of risk involved in its

operations. Hence, the major anticipation of the proposal made by the purchasing manager is

the reduction on cost, which will allow the organisation to increase its profits. However, no

anticipation has been conducted for detecting problems that might increase from the

competitors. There is relevantly high risk involved in discounting the manufacturing process,

as it will make the organisation dependent on its competitors for the parts.

INTERNATIONAL FINANCE AND DECISION MAKING

11

However, certain alternative can be adopted by the organisation instead of the

recommendations that is been provided by the purchasing manager. The improvements in the

current manufacturing process can be conducted by the organisation for reducing the level of

cost involved in producing the parts for sale. The competitors have used new technology for

improving the production level and reduce the cost involved in operations. The same method

or technology can be can be used by Morden Engendering for improving the level income

production reduce the actual cost of production. This reduction in cost would eventually help

in organisation to improve its competitive edge in the market and reduce any kind of risk

involved in investment. Furthermore, the organisation can use the zero-budgeting method for

controlling the relevant cost involved in the manufacturing process. This method can help in

determining the different level of expenses, which has been incurred by the company to

complete its production process. The zero-budgeting method will substantially reduce the

excessive expenses incurred by the company, which in turn can raise its profitability and

competitive edge. In addition, the adopting of new technology can be evaluated on the basis

of the investment appraisal technique for determining the accurate level of income that can be

generated from an operation (Pivoriene 2017).

Therefore, the alternative method can be used by the organisation for maintaining the

manufacturing process and reduce the actual cost involved in operations. This would allow

Morden Engineering to reduce the level of expenses, which can be generated from

operations. The organisation can eventually improve its current financial performance by

reading the level of expenses incurred in the production process. However, the alternative

method can increase the expense and investment of the organisation, as it will raise their

competition level in the market. The overall performance of the organisation can eventually

improve over the period when choosing the alternative option. The increment in

11

However, certain alternative can be adopted by the organisation instead of the

recommendations that is been provided by the purchasing manager. The improvements in the

current manufacturing process can be conducted by the organisation for reducing the level of

cost involved in producing the parts for sale. The competitors have used new technology for

improving the production level and reduce the cost involved in operations. The same method

or technology can be can be used by Morden Engendering for improving the level income

production reduce the actual cost of production. This reduction in cost would eventually help

in organisation to improve its competitive edge in the market and reduce any kind of risk

involved in investment. Furthermore, the organisation can use the zero-budgeting method for

controlling the relevant cost involved in the manufacturing process. This method can help in

determining the different level of expenses, which has been incurred by the company to

complete its production process. The zero-budgeting method will substantially reduce the

excessive expenses incurred by the company, which in turn can raise its profitability and

competitive edge. In addition, the adopting of new technology can be evaluated on the basis

of the investment appraisal technique for determining the accurate level of income that can be

generated from an operation (Pivoriene 2017).

Therefore, the alternative method can be used by the organisation for maintaining the

manufacturing process and reduce the actual cost involved in operations. This would allow

Morden Engineering to reduce the level of expenses, which can be generated from

operations. The organisation can eventually improve its current financial performance by

reading the level of expenses incurred in the production process. However, the alternative

method can increase the expense and investment of the organisation, as it will raise their

competition level in the market. The overall performance of the organisation can eventually

improve over the period when choosing the alternative option. The increment in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16