Analysis of International Finance: Exchange Rate Volatility Report

VerifiedAdded on 2022/12/22

|10

|2247

|95

Report

AI Summary

This report delves into the realm of international finance, providing a comprehensive analysis of exchange rate volatility, particularly in the context of the Dornbusch overshooting model. It begins by defining and explaining key concepts such as Purchasing Power Parity (PPP) and Uncovered Interest P...

Running Head: INTERNATIONAL FINANCE

INTERNATIONAL FINANCE

Name of the Student

Name of the University

Author Note

INTERNATIONAL FINANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL FINANCE

Table of Contents

Justification of Volatility of Foreign Exchange Rates given PPP and UIP...............................2

Purchasing Power Parity............................................................................................................2

Uncovered Interest Parity...........................................................................................................2

Volatility of Exchange Rates and Relation with PPP or UIP or both........................................3

Devaluation of Pound against other major currencies...............................................................5

Shocks to Other Currencies........................................................................................................5

Econometric approach................................................................................................................7

Reference....................................................................................................................................8

Table of Contents

Justification of Volatility of Foreign Exchange Rates given PPP and UIP...............................2

Purchasing Power Parity............................................................................................................2

Uncovered Interest Parity...........................................................................................................2

Volatility of Exchange Rates and Relation with PPP or UIP or both........................................3

Devaluation of Pound against other major currencies...............................................................5

Shocks to Other Currencies........................................................................................................5

Econometric approach................................................................................................................7

Reference....................................................................................................................................8

2INTERNATIONAL FINANCE

Justification of Volatility of Foreign Exchange Rates given PPP and UIP

The aim of the assignment is the analysis on the international finance. The analysis

will be based on the conditions of the exchange rate equilibrium conditions of Purchasing

Power Parity and Uncovered Interest Parity. In addition, dicussion will also be based on the

justification of the high levels of the volatility in the foreign exchang rates . Volatility of the

exchange rates makes the international trade as well as decisions of investments much more

difficult beacause the volatility increases the risk of exchange rate (Grossmann, Love and

Orlov 2014).

Purchasing Power Parity

It is the theory of economy which compares the currencies of the different countries

through the approach of the “basket of goods”. It is concerned with the concept of the

equilibrium of the two currencies that is at par when the price of the basket of goods is same

for both the countries that takes the account of the exchange rates. Hence, it is the way of the

measurement of the economic variables in the different countries for which the there is

variations of the irrelevant exchange rate does not distort the comparison. This rate is

required in the comparisons of that is equal to the ratio of respective purchasung power of the

currencies (Jolliffe and Prydz 2015).

Uncovered Interest Parity

This theory defines the interest rates differences between the two countries that is

equal to the currency of the foreign exchange rate’s relative change over the same time frame.

It is the form of the interest rate parityh that is used besides the covered interet rate parity.

The conditions of the uncovered interest rate parity is consists with the two streams of return,

one is from the investment’s interest rate of foreign money market as well as other from the

changes in the spot rate of foreign currency(Lothian 2016).

Justification of Volatility of Foreign Exchange Rates given PPP and UIP

The aim of the assignment is the analysis on the international finance. The analysis

will be based on the conditions of the exchange rate equilibrium conditions of Purchasing

Power Parity and Uncovered Interest Parity. In addition, dicussion will also be based on the

justification of the high levels of the volatility in the foreign exchang rates . Volatility of the

exchange rates makes the international trade as well as decisions of investments much more

difficult beacause the volatility increases the risk of exchange rate (Grossmann, Love and

Orlov 2014).

Purchasing Power Parity

It is the theory of economy which compares the currencies of the different countries

through the approach of the “basket of goods”. It is concerned with the concept of the

equilibrium of the two currencies that is at par when the price of the basket of goods is same

for both the countries that takes the account of the exchange rates. Hence, it is the way of the

measurement of the economic variables in the different countries for which the there is

variations of the irrelevant exchange rate does not distort the comparison. This rate is

required in the comparisons of that is equal to the ratio of respective purchasung power of the

currencies (Jolliffe and Prydz 2015).

Uncovered Interest Parity

This theory defines the interest rates differences between the two countries that is

equal to the currency of the foreign exchange rate’s relative change over the same time frame.

It is the form of the interest rate parityh that is used besides the covered interet rate parity.

The conditions of the uncovered interest rate parity is consists with the two streams of return,

one is from the investment’s interest rate of foreign money market as well as other from the

changes in the spot rate of foreign currency(Lothian 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL FINANCE

Volatility of Exchange Rates and Relation with PPP or UIP or both

The volatility of the exchange rate is the most important aspects of the international

economies. There is the strong variability of the emerging markets as well as more failure of

the fixed regime. Countries usually commence on the period of the controlled nominal

exchange rates that is in the hope of achieving the stability for both internal and external.

These are the efforts, which rarely lasts and most of such countries are forced for devaluing

(Plakandaras, Papadimitriou and Gogas 2015).

The empirical evidence that explained the volatility of the exchange rate as well as

relation to either UIP or PPP or even both can be done by the Dornbusch’s influential

overshooting model. This model has explains the reason behind the high variance of the

floating exchange rates. This model is highly influential because recently the world has

switched from the system of Bretton Woods to the flexible exchange rates (Moore, and Wang

2014).

The assumption that was made by Dornbusch is as follows:

Uncovered interest rate parity assumes that the differential of the interest rates is

equal to the spot rate’s expected change. This assumes that there is perfect mobility of

the capital, the investors have risk, which is neutral and the perfect substitutes are

assets of domestic and foreign. (Jegajeevan 2015)

Absolutes purchasing power parity assumes that when the basket of goods, expressed

in the common currency, then across the countries, it should have the same cost. The

model assumes that the in the short run, deviation from the PPP is permitted.

However, in the long-run, exchange rate will return to the PPP. The real exchange rate

in the short run can increase which ultimately increase the economy competitiveness

as well as increases the net exports (Jegajeevan 2015).

Volatility of Exchange Rates and Relation with PPP or UIP or both

The volatility of the exchange rate is the most important aspects of the international

economies. There is the strong variability of the emerging markets as well as more failure of

the fixed regime. Countries usually commence on the period of the controlled nominal

exchange rates that is in the hope of achieving the stability for both internal and external.

These are the efforts, which rarely lasts and most of such countries are forced for devaluing

(Plakandaras, Papadimitriou and Gogas 2015).

The empirical evidence that explained the volatility of the exchange rate as well as

relation to either UIP or PPP or even both can be done by the Dornbusch’s influential

overshooting model. This model has explains the reason behind the high variance of the

floating exchange rates. This model is highly influential because recently the world has

switched from the system of Bretton Woods to the flexible exchange rates (Moore, and Wang

2014).

The assumption that was made by Dornbusch is as follows:

Uncovered interest rate parity assumes that the differential of the interest rates is

equal to the spot rate’s expected change. This assumes that there is perfect mobility of

the capital, the investors have risk, which is neutral and the perfect substitutes are

assets of domestic and foreign. (Jegajeevan 2015)

Absolutes purchasing power parity assumes that when the basket of goods, expressed

in the common currency, then across the countries, it should have the same cost. The

model assumes that the in the short run, deviation from the PPP is permitted.

However, in the long-run, exchange rate will return to the PPP. The real exchange rate

in the short run can increase which ultimately increase the economy competitiveness

as well as increases the net exports (Jegajeevan 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL FINANCE

There is equilibrium in the money market when the supply of the real money is equal

to the demand of the real money where the demand of real money is the output’s

rising function as well as interest rate’s falling functions (Hodrick 2014)..

From the curve of the standard IS, output is given that is rising in real exchange rate

as well as falling in interest rate.

Given by Philip curve, inflation rate is the function of output gap.

Under the scrutiny, the economy is the small open economy so as it does not affect

the foreign interest rates, output and its prices (Engel 2014).

There is the beginning of the economy at the stationary state where, the output is at

the potential, PPP holds, prices are constant, there are equal foreign and domestic

interest rates and the equilibrium rate is at level of equilibrium (Jegajeevan 2015).

In carrying trade, UIP is tied in the speculation of foreign exchange. Hence, it is

suggested, either, there is insufficiency for generating UIP by the volume of the carry trade or

the association of the risk premium with carry trade is quite large. In addition, to this, there is

significant transaction cost and liquidity shortage in carry trade, which leads to the deviations

from the UIP (Jegajeevan 2015).

The evidence of PPP suggests that there is some validity in the long-run as well as it

holds better than what it is in short run. The puzzle PPP is the real exchange rate, which does

not equal to the unity among the countries. The exchange rate is more and highly volatile as

well as rigidity of prices of goods (Twarowska and Kakol, 2014).

Therefore, from the conclusion, it has been find that the model of Dornbusch has the

mixed empirical evidence. Some evidence of the long purchasing power parity has been

accessed. However, in case of unrelated interest rates, most of the academician due to range

of overshooting, undershooting, delayed overshooting as well as no overshooting whatsoever

There is equilibrium in the money market when the supply of the real money is equal

to the demand of the real money where the demand of real money is the output’s

rising function as well as interest rate’s falling functions (Hodrick 2014)..

From the curve of the standard IS, output is given that is rising in real exchange rate

as well as falling in interest rate.

Given by Philip curve, inflation rate is the function of output gap.

Under the scrutiny, the economy is the small open economy so as it does not affect

the foreign interest rates, output and its prices (Engel 2014).

There is the beginning of the economy at the stationary state where, the output is at

the potential, PPP holds, prices are constant, there are equal foreign and domestic

interest rates and the equilibrium rate is at level of equilibrium (Jegajeevan 2015).

In carrying trade, UIP is tied in the speculation of foreign exchange. Hence, it is

suggested, either, there is insufficiency for generating UIP by the volume of the carry trade or

the association of the risk premium with carry trade is quite large. In addition, to this, there is

significant transaction cost and liquidity shortage in carry trade, which leads to the deviations

from the UIP (Jegajeevan 2015).

The evidence of PPP suggests that there is some validity in the long-run as well as it

holds better than what it is in short run. The puzzle PPP is the real exchange rate, which does

not equal to the unity among the countries. The exchange rate is more and highly volatile as

well as rigidity of prices of goods (Twarowska and Kakol, 2014).

Therefore, from the conclusion, it has been find that the model of Dornbusch has the

mixed empirical evidence. Some evidence of the long purchasing power parity has been

accessed. However, in case of unrelated interest rates, most of the academician due to range

of overshooting, undershooting, delayed overshooting as well as no overshooting whatsoever

5INTERNATIONAL FINANCE

rejects parity. Therefore, even though being the most influential model, it has not been able to

give the accuracy of the forecast for the movements of the exchange rates (Adeniran, Yusuf

and Adeyemi 2014).

Devaluation of Pound against other major currencies

The history of pound of British is as unique as the empire of British. It is one of the

oldest reserve currencies; therefore, it is the most reliable to the store wealth. However, there

has been devaluation of the Pound as compare to the other major currencies. It is because

based on short term; there has been immediate devaluation that was driven by the expectation

of the market. Even though, pound was in the market of bear for already more than two years.

It was due to the result of Brexit that came as shock to the financial and political elites that

have forced the positions of long speculative for exit at the level of painful as an evidence by

poor performances of the large number of the hedge funds over the Brexit. It has led to

stabilize of the volatility of pound but it began to spreading of the downward pressure on

currency. Moreover, in the long run, the actions taken by the central banks are to stabilize as

well as immunize the selloff of equity as well as potential crisis have ensured further

depreciation of this currency at lower rates. Therefore, this volatility in the exchange rate

increases the exchange rate risk (Plakandaras, Papadimitriou and Gogas 2015).

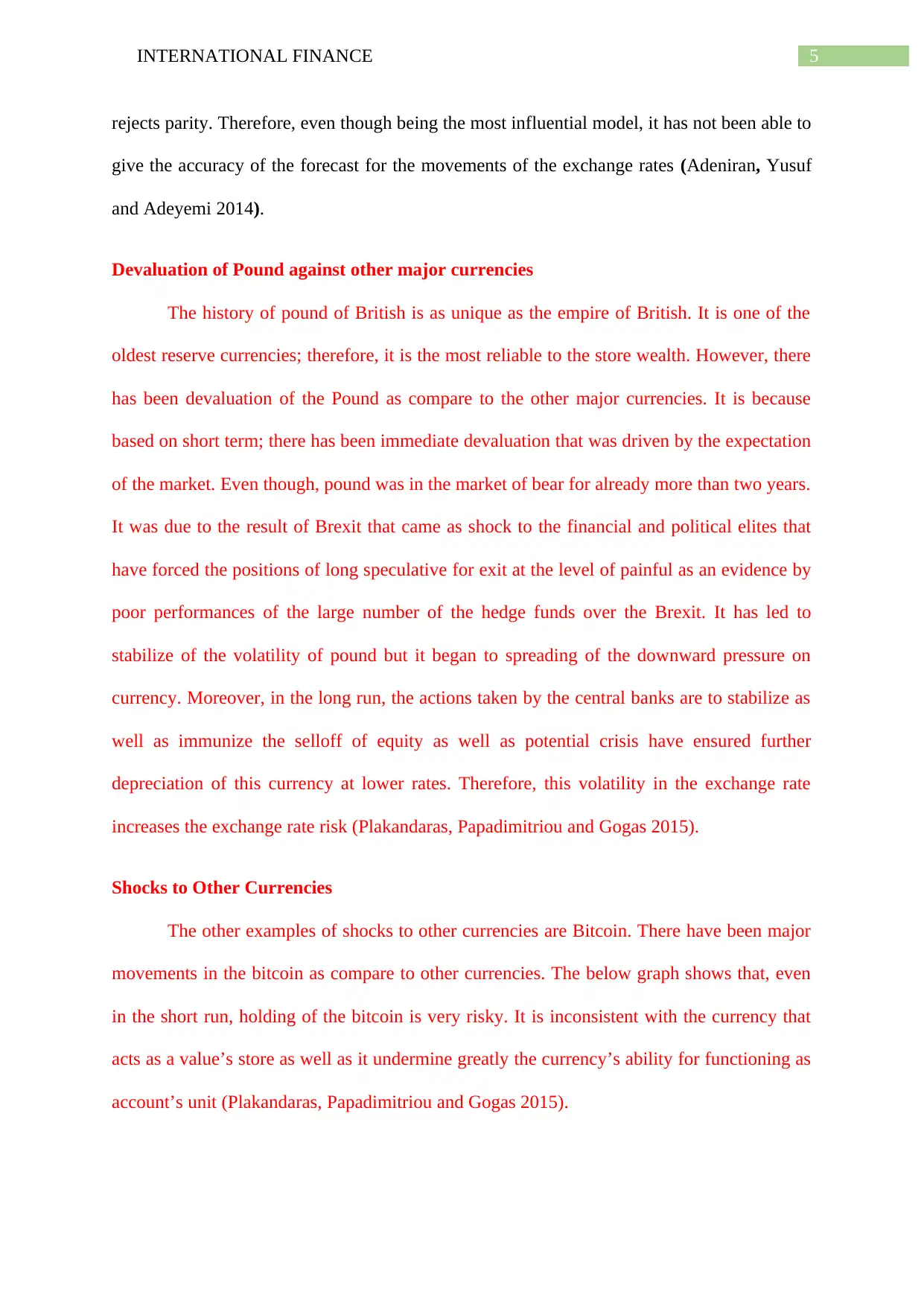

Shocks to Other Currencies

The other examples of shocks to other currencies are Bitcoin. There have been major

movements in the bitcoin as compare to other currencies. The below graph shows that, even

in the short run, holding of the bitcoin is very risky. It is inconsistent with the currency that

acts as a value’s store as well as it undermine greatly the currency’s ability for functioning as

account’s unit (Plakandaras, Papadimitriou and Gogas 2015).

rejects parity. Therefore, even though being the most influential model, it has not been able to

give the accuracy of the forecast for the movements of the exchange rates (Adeniran, Yusuf

and Adeyemi 2014).

Devaluation of Pound against other major currencies

The history of pound of British is as unique as the empire of British. It is one of the

oldest reserve currencies; therefore, it is the most reliable to the store wealth. However, there

has been devaluation of the Pound as compare to the other major currencies. It is because

based on short term; there has been immediate devaluation that was driven by the expectation

of the market. Even though, pound was in the market of bear for already more than two years.

It was due to the result of Brexit that came as shock to the financial and political elites that

have forced the positions of long speculative for exit at the level of painful as an evidence by

poor performances of the large number of the hedge funds over the Brexit. It has led to

stabilize of the volatility of pound but it began to spreading of the downward pressure on

currency. Moreover, in the long run, the actions taken by the central banks are to stabilize as

well as immunize the selloff of equity as well as potential crisis have ensured further

depreciation of this currency at lower rates. Therefore, this volatility in the exchange rate

increases the exchange rate risk (Plakandaras, Papadimitriou and Gogas 2015).

Shocks to Other Currencies

The other examples of shocks to other currencies are Bitcoin. There have been major

movements in the bitcoin as compare to other currencies. The below graph shows that, even

in the short run, holding of the bitcoin is very risky. It is inconsistent with the currency that

acts as a value’s store as well as it undermine greatly the currency’s ability for functioning as

account’s unit (Plakandaras, Papadimitriou and Gogas 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL FINANCE

Figure 1: Bitcoin Volatility

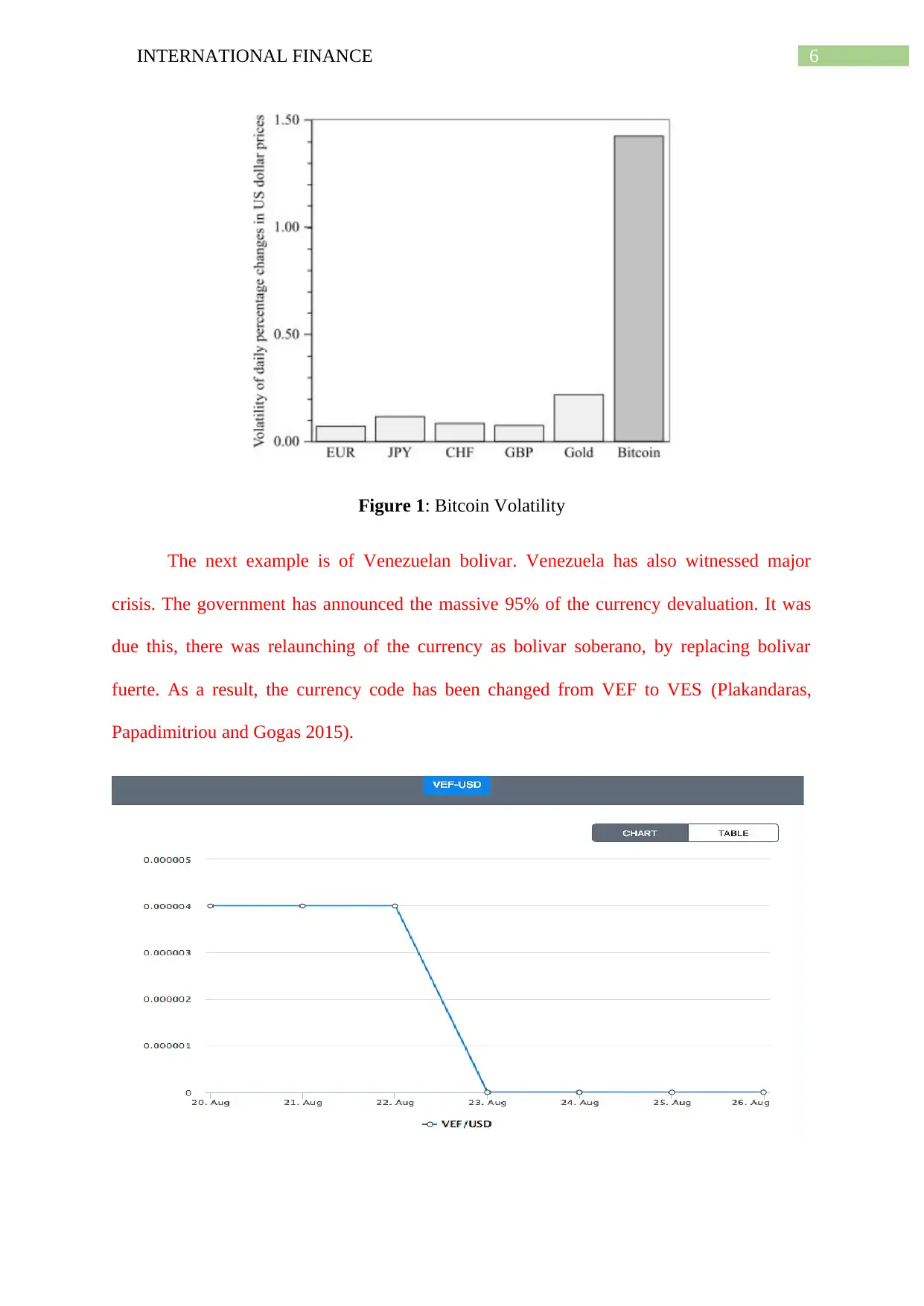

The next example is of Venezuelan bolivar. Venezuela has also witnessed major

crisis. The government has announced the massive 95% of the currency devaluation. It was

due this, there was relaunching of the currency as bolivar soberano, by replacing bolivar

fuerte. As a result, the currency code has been changed from VEF to VES (Plakandaras,

Papadimitriou and Gogas 2015).

Figure 1: Bitcoin Volatility

The next example is of Venezuelan bolivar. Venezuela has also witnessed major

crisis. The government has announced the massive 95% of the currency devaluation. It was

due this, there was relaunching of the currency as bolivar soberano, by replacing bolivar

fuerte. As a result, the currency code has been changed from VEF to VES (Plakandaras,

Papadimitriou and Gogas 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCE

Figure 2: Venezuelan bolivar Volatility

Econometric approach

1. Uncovered interest rate parity:st +k=st + ^it , k

Where s presents the (log) exchange rate, it,k presents the interest rate of maturity k and ^

presents the intercountry difference. Unlike the other specifications, this relation does not

involve estimation in order to make predictions. The study found that the long run maturity

interest rate is not able to predict the changes in long run exchange rate (Zhang et al. 2015).

2. Relative purchasing power parity: st =β0 + ^pt

Where p presents log price level and ^ presents the intercountry difference. The recent

research has shown the usefulness of PPP deviations for predicting exchange rate changes

(Ca’Zorzi, Muck and Rubaszek 2016).

The economic model, purchasing power parity and interest rate parity has importance

and the probable reason is the parsimonious nature of specification where interest rate parity

does not require the estimation of the parameter.

Figure 2: Venezuelan bolivar Volatility

Econometric approach

1. Uncovered interest rate parity:st +k=st + ^it , k

Where s presents the (log) exchange rate, it,k presents the interest rate of maturity k and ^

presents the intercountry difference. Unlike the other specifications, this relation does not

involve estimation in order to make predictions. The study found that the long run maturity

interest rate is not able to predict the changes in long run exchange rate (Zhang et al. 2015).

2. Relative purchasing power parity: st =β0 + ^pt

Where p presents log price level and ^ presents the intercountry difference. The recent

research has shown the usefulness of PPP deviations for predicting exchange rate changes

(Ca’Zorzi, Muck and Rubaszek 2016).

The economic model, purchasing power parity and interest rate parity has importance

and the probable reason is the parsimonious nature of specification where interest rate parity

does not require the estimation of the parameter.

8INTERNATIONAL FINANCE

Reference

Adeniran, J.O., Yusuf, S.A. and Adeyemi, O.A., 2014. The impact of exchange rate

fluctuation on the Nigerian economic growth: An empirical investigation. International

Journal of Academic Research in Business and Social Sciences, 4(8), p.224.

Ca’Zorzi, M., Muck, J. and Rubaszek, M., 2016. Real exchange rate forecasting and PPP:

This time the random walk loses. Open Economies Review, 27(3), pp.585-609.

Engel, C., 2014. Exchange rates and interest parity. In Handbook of international

economics (Vol. 4, pp. 453-522). Elsevier.

Grossmann, A., Love, I. and Orlov, A.G., 2014. The dynamics of exchange rate volatility: A

panel VAR approach. Journal of International Financial Markets, Institutions and

Money, 33, pp.1-27.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign

exchange markets. Routledge.

Jegajeevan, S., 2015. Validity of the Monetary Model of the Exchange Rate: Empirical

Evidence from Sri Lanka. Staff Studies, 42(1).

Jolliffe, D. and Prydz, E.B., 2015. Global poverty goals and prices: how purchasing power

parity matters. The World Bank.

Lothian, J.R., 2016. Uncovered interest parity: The long and the short of it. Journal of

Empirical Finance, 36, pp.1-7.

Moore, T. and Wang, P., 2014. Dynamic linkage between real exchange rates and stock

prices: Evidence from developed and emerging Asian markets. International Review of

Economics & Finance, 29, pp.1-11.

Reference

Adeniran, J.O., Yusuf, S.A. and Adeyemi, O.A., 2014. The impact of exchange rate

fluctuation on the Nigerian economic growth: An empirical investigation. International

Journal of Academic Research in Business and Social Sciences, 4(8), p.224.

Ca’Zorzi, M., Muck, J. and Rubaszek, M., 2016. Real exchange rate forecasting and PPP:

This time the random walk loses. Open Economies Review, 27(3), pp.585-609.

Engel, C., 2014. Exchange rates and interest parity. In Handbook of international

economics (Vol. 4, pp. 453-522). Elsevier.

Grossmann, A., Love, I. and Orlov, A.G., 2014. The dynamics of exchange rate volatility: A

panel VAR approach. Journal of International Financial Markets, Institutions and

Money, 33, pp.1-27.

Hodrick, R., 2014. The empirical evidence on the efficiency of forward and futures foreign

exchange markets. Routledge.

Jegajeevan, S., 2015. Validity of the Monetary Model of the Exchange Rate: Empirical

Evidence from Sri Lanka. Staff Studies, 42(1).

Jolliffe, D. and Prydz, E.B., 2015. Global poverty goals and prices: how purchasing power

parity matters. The World Bank.

Lothian, J.R., 2016. Uncovered interest parity: The long and the short of it. Journal of

Empirical Finance, 36, pp.1-7.

Moore, T. and Wang, P., 2014. Dynamic linkage between real exchange rates and stock

prices: Evidence from developed and emerging Asian markets. International Review of

Economics & Finance, 29, pp.1-11.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL FINANCE

Plakandaras, V., Papadimitriou, T. and Gogas, P., 2015. Forecasting daily and monthly

exchange rates with machine learning techniques. Journal of Forecasting, 34(7), pp.560-573.

Twarowska, K. and Kakol, M., 2014. Analysis of Factors Affecting Fluctuations in the

Exchange Rate of Polish Zloty against Euro. In Human Capital without Borders: Knowledge

and Learning for Quality of Life; Proceedings of the Management, Knowledge and Learning

International Conference 2014 (pp. 889-896). ToKnowPress.

Zhang, Z., Perez, E.C.V., Chinn, A. and Davies, J., 2015. Tree Diversity has Limited Effects

on Beech Bark Disease Incidence in American Beech Population of Mont St-Hilaire. McGill

Science Undergraduate Research Journal, 10(1).

Plakandaras, V., Papadimitriou, T. and Gogas, P., 2015. Forecasting daily and monthly

exchange rates with machine learning techniques. Journal of Forecasting, 34(7), pp.560-573.

Twarowska, K. and Kakol, M., 2014. Analysis of Factors Affecting Fluctuations in the

Exchange Rate of Polish Zloty against Euro. In Human Capital without Borders: Knowledge

and Learning for Quality of Life; Proceedings of the Management, Knowledge and Learning

International Conference 2014 (pp. 889-896). ToKnowPress.

Zhang, Z., Perez, E.C.V., Chinn, A. and Davies, J., 2015. Tree Diversity has Limited Effects

on Beech Bark Disease Incidence in American Beech Population of Mont St-Hilaire. McGill

Science Undergraduate Research Journal, 10(1).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.