International Finance: Barclays and Royal Bank of Scotland Acquisition

VerifiedAdded on 2020/07/22

|15

|3210

|36

Report

AI Summary

This report analyzes the potential acquisition of the Royal Bank of Scotland (RBS) by Barclays, focusing on the financial viability of the deal. The introduction highlights the importance of financial tools in assessing acquisition plans. Task 1 uses ratio analysis to evaluate RBS's financial performance in 2015 and 2016, including profitability, solvency, and efficiency ratios, concluding that Barclays should avoid the acquisition due to RBS's poor financial health. Task 2 explores the advantages and disadvantages of net asset, price-earnings, and dividend valuation methods, providing computations of intrinsic value based on these methods. The report explains the reasons for valuation differences and identifies various risk exposures faced by RBS, emphasizing the negative impact on market share and investor confidence. Recommendations are provided in Task 3, and the conclusion summarizes the findings, reinforcing the recommendation against the acquisition. The report emphasizes the importance of competent policy frameworks for financial improvement.

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

Assessing whether Barclays should acquire FTSE 100 company or not by using ratio

analysis technique..................................................................................................................1

TASK 2......................................................................................................................................6

a. Advantages and disadvantages of net assets, price earnings and dividend valuation

method....................................................................................................................................6

b. Computation of intrinsic value...........................................................................................7

c. Presenting the reasons due to which net assets, price earnings and dividend valuation

method differs........................................................................................................................9

d. Identifying various risk exposures which are facing by FTSE 100...................................9

e. Stating the extent to which economic environment have an impact on results and

valuation...............................................................................................................................10

TASK 3....................................................................................................................................10

Recommendations................................................................................................................10

CONCUSION..........................................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

Assessing whether Barclays should acquire FTSE 100 company or not by using ratio

analysis technique..................................................................................................................1

TASK 2......................................................................................................................................6

a. Advantages and disadvantages of net assets, price earnings and dividend valuation

method....................................................................................................................................6

b. Computation of intrinsic value...........................................................................................7

c. Presenting the reasons due to which net assets, price earnings and dividend valuation

method differs........................................................................................................................9

d. Identifying various risk exposures which are facing by FTSE 100...................................9

e. Stating the extent to which economic environment have an impact on results and

valuation...............................................................................................................................10

TASK 3....................................................................................................................................10

Recommendations................................................................................................................10

CONCUSION..........................................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION

In the present era, business units are placing high level of emphasis on acquiring other

firms with the motive to explore operations as well as functions. This in turn enables firm to

operate at large level and maximizes both productivity & profitability. In this context,

financial tools and technique are highly significant that assists in identifying whether

proposed acquisition plan would be profitable or not. The present report is based on the case

scenario of Barclays bank which is planning to acquire FTSE 100 company namely Royal

Bank of Scotland. Thus, report will shed light on the extent to which financial position and

performance of Royal Bank is good. Besides this, it will provide deeper insight about how

different types of valuation methods such net asset, price earnings and dividend basis helps in

determining suitable value. It clearly depicts Barclays should acquire Royal bank of Scotland

or not.

TASK 1

Assessing whether Barclays should acquire FTSE 100 company or not by using ratio analysis

technique

Ratio analysis is one of the most effectual tools which summarizes and gives quick

indication pertaining to the financial perform of firm. Hence, by using this technique

investors and other stakeholders can assess the extent to which profitability, liquidity and

solvency position of the company is sound (Görener, Dincer and Hacioglu, 2016).

Ratio analysis of Royal Bank of Scotland for the year of 2015 and 2016 is as follows:

Particulars Formula 2015 2016

Profitability ratios

Shareholders’

equity

53,431

(Annual

report of

RBS

(2016),

2017) 48,609

Net profit -1594 -5258

In the present era, business units are placing high level of emphasis on acquiring other

firms with the motive to explore operations as well as functions. This in turn enables firm to

operate at large level and maximizes both productivity & profitability. In this context,

financial tools and technique are highly significant that assists in identifying whether

proposed acquisition plan would be profitable or not. The present report is based on the case

scenario of Barclays bank which is planning to acquire FTSE 100 company namely Royal

Bank of Scotland. Thus, report will shed light on the extent to which financial position and

performance of Royal Bank is good. Besides this, it will provide deeper insight about how

different types of valuation methods such net asset, price earnings and dividend basis helps in

determining suitable value. It clearly depicts Barclays should acquire Royal bank of Scotland

or not.

TASK 1

Assessing whether Barclays should acquire FTSE 100 company or not by using ratio analysis

technique

Ratio analysis is one of the most effectual tools which summarizes and gives quick

indication pertaining to the financial perform of firm. Hence, by using this technique

investors and other stakeholders can assess the extent to which profitability, liquidity and

solvency position of the company is sound (Görener, Dincer and Hacioglu, 2016).

Ratio analysis of Royal Bank of Scotland for the year of 2015 and 2016 is as follows:

Particulars Formula 2015 2016

Profitability ratios

Shareholders’

equity

53,431

(Annual

report of

RBS

(2016),

2017) 48,609

Net profit -1594 -5258

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

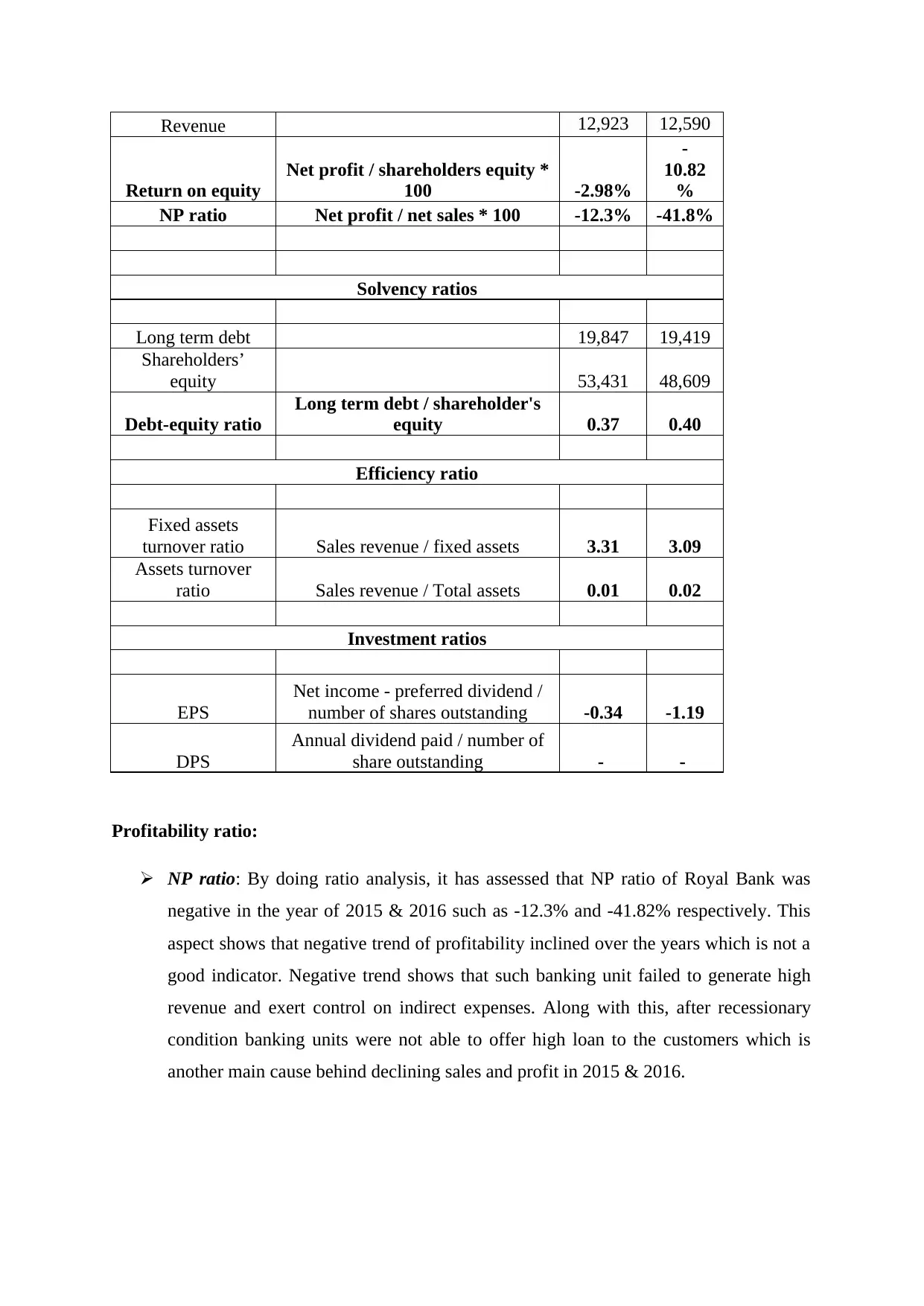

Revenue 12,923 12,590

Return on equity

Net profit / shareholders equity *

100 -2.98%

-

10.82

%

NP ratio Net profit / net sales * 100 -12.3% -41.8%

Solvency ratios

Long term debt 19,847 19,419

Shareholders’

equity 53,431 48,609

Debt-equity ratio

Long term debt / shareholder's

equity 0.37 0.40

Efficiency ratio

Fixed assets

turnover ratio Sales revenue / fixed assets 3.31 3.09

Assets turnover

ratio Sales revenue / Total assets 0.01 0.02

Investment ratios

EPS

Net income - preferred dividend /

number of shares outstanding -0.34 -1.19

DPS

Annual dividend paid / number of

share outstanding - -

Profitability ratio:

NP ratio: By doing ratio analysis, it has assessed that NP ratio of Royal Bank was

negative in the year of 2015 & 2016 such as -12.3% and -41.82% respectively. This

aspect shows that negative trend of profitability inclined over the years which is not a

good indicator. Negative trend shows that such banking unit failed to generate high

revenue and exert control on indirect expenses. Along with this, after recessionary

condition banking units were not able to offer high loan to the customers which is

another main cause behind declining sales and profit in 2015 & 2016.

Return on equity

Net profit / shareholders equity *

100 -2.98%

-

10.82

%

NP ratio Net profit / net sales * 100 -12.3% -41.8%

Solvency ratios

Long term debt 19,847 19,419

Shareholders’

equity 53,431 48,609

Debt-equity ratio

Long term debt / shareholder's

equity 0.37 0.40

Efficiency ratio

Fixed assets

turnover ratio Sales revenue / fixed assets 3.31 3.09

Assets turnover

ratio Sales revenue / Total assets 0.01 0.02

Investment ratios

EPS

Net income - preferred dividend /

number of shares outstanding -0.34 -1.19

DPS

Annual dividend paid / number of

share outstanding - -

Profitability ratio:

NP ratio: By doing ratio analysis, it has assessed that NP ratio of Royal Bank was

negative in the year of 2015 & 2016 such as -12.3% and -41.82% respectively. This

aspect shows that negative trend of profitability inclined over the years which is not a

good indicator. Negative trend shows that such banking unit failed to generate high

revenue and exert control on indirect expenses. Along with this, after recessionary

condition banking units were not able to offer high loan to the customers which is

another main cause behind declining sales and profit in 2015 & 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016

-45.0%

-40.0%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

NP ratio

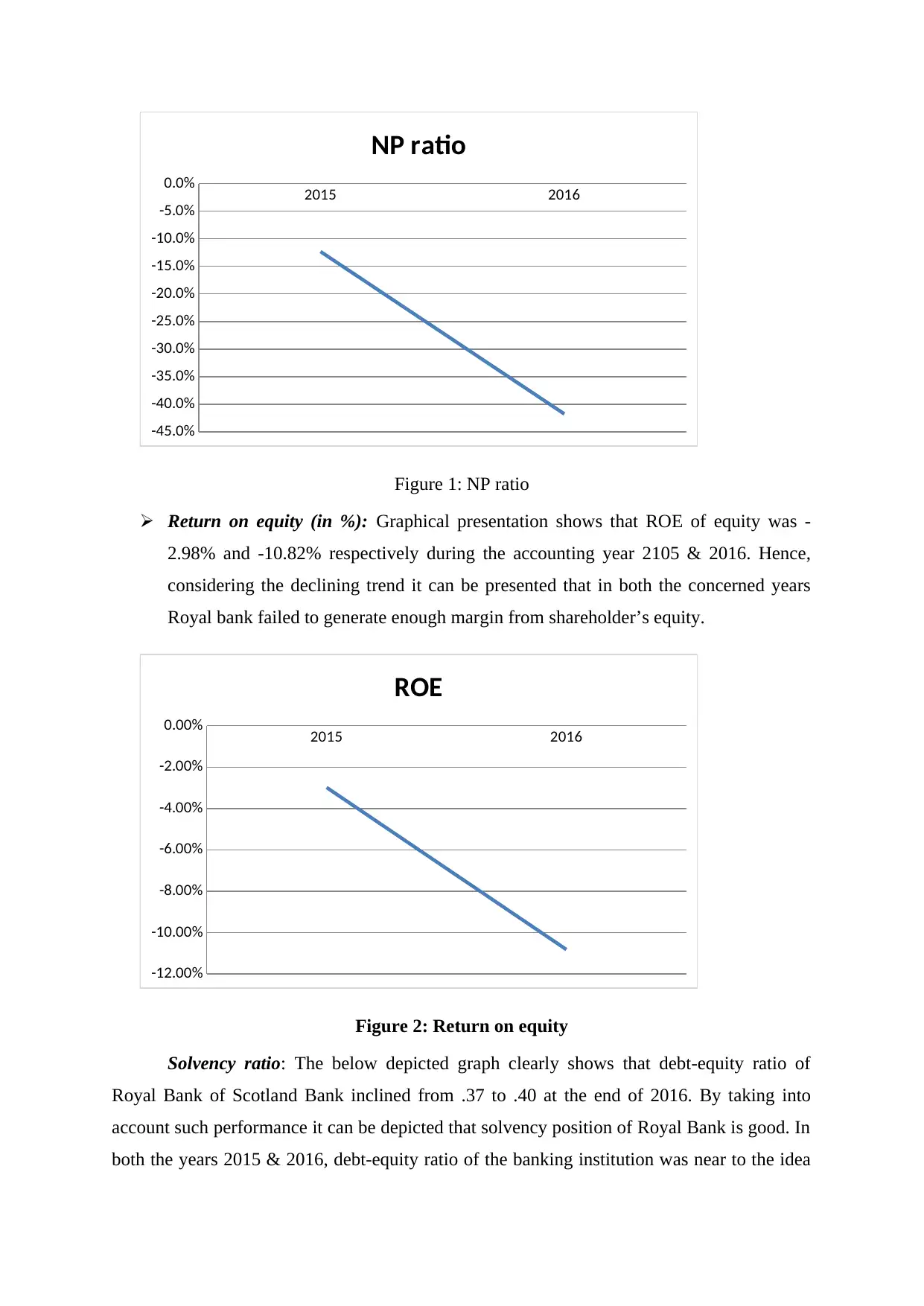

Figure 1: NP ratio

Return on equity (in %): Graphical presentation shows that ROE of equity was -

2.98% and -10.82% respectively during the accounting year 2105 & 2016. Hence,

considering the declining trend it can be presented that in both the concerned years

Royal bank failed to generate enough margin from shareholder’s equity.

2015 2016

-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

ROE

Figure 2: Return on equity

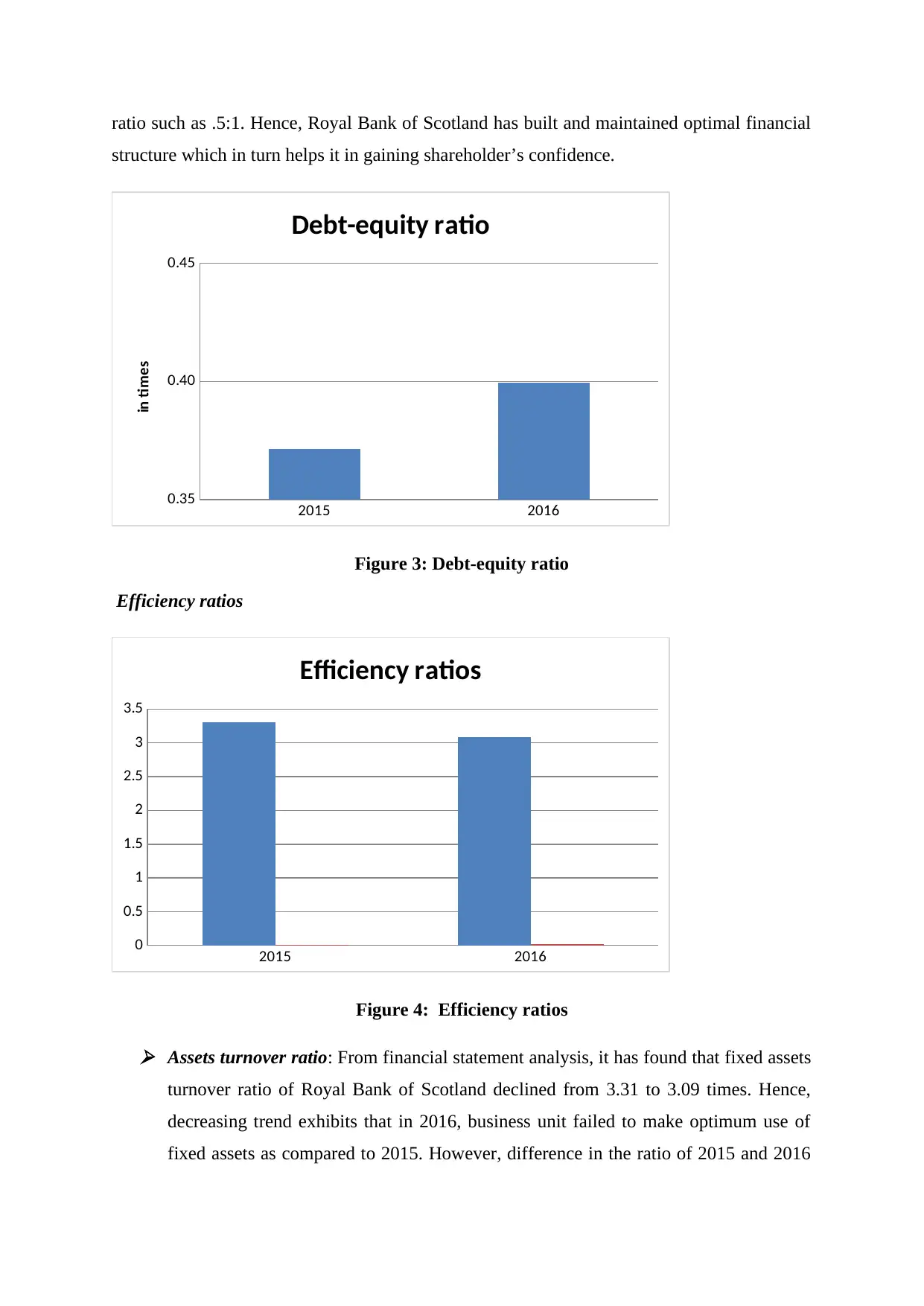

Solvency ratio: The below depicted graph clearly shows that debt-equity ratio of

Royal Bank of Scotland Bank inclined from .37 to .40 at the end of 2016. By taking into

account such performance it can be depicted that solvency position of Royal Bank is good. In

both the years 2015 & 2016, debt-equity ratio of the banking institution was near to the idea

-45.0%

-40.0%

-35.0%

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

NP ratio

Figure 1: NP ratio

Return on equity (in %): Graphical presentation shows that ROE of equity was -

2.98% and -10.82% respectively during the accounting year 2105 & 2016. Hence,

considering the declining trend it can be presented that in both the concerned years

Royal bank failed to generate enough margin from shareholder’s equity.

2015 2016

-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

ROE

Figure 2: Return on equity

Solvency ratio: The below depicted graph clearly shows that debt-equity ratio of

Royal Bank of Scotland Bank inclined from .37 to .40 at the end of 2016. By taking into

account such performance it can be depicted that solvency position of Royal Bank is good. In

both the years 2015 & 2016, debt-equity ratio of the banking institution was near to the idea

ratio such as .5:1. Hence, Royal Bank of Scotland has built and maintained optimal financial

structure which in turn helps it in gaining shareholder’s confidence.

2015 2016

0.35

0.40

0.45

Debt-equity ratio

in times

Figure 3: Debt-equity ratio

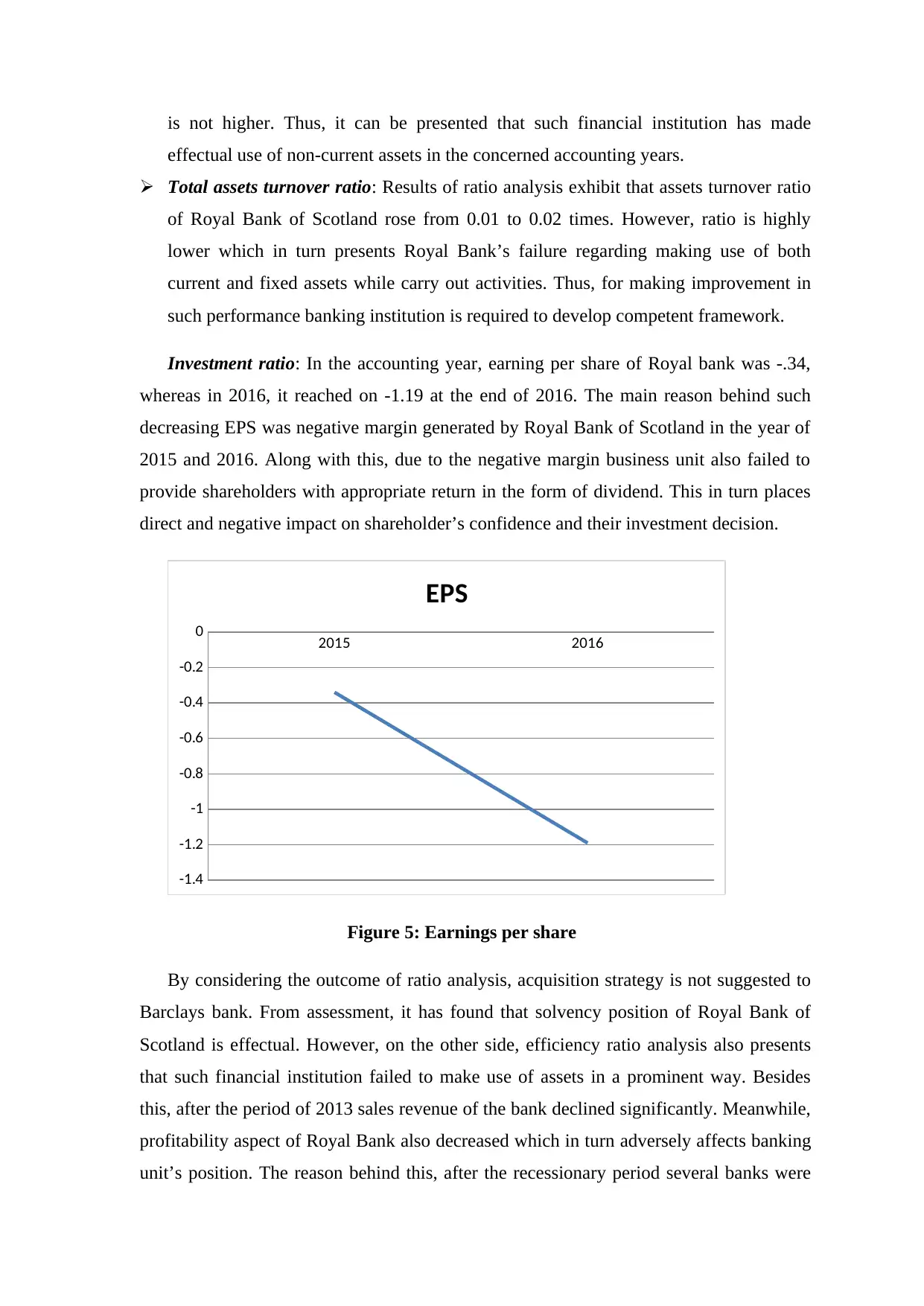

Efficiency ratios

2015 2016

0

0.5

1

1.5

2

2.5

3

3.5

Efficiency ratios

Figure 4: Efficiency ratios

Assets turnover ratio: From financial statement analysis, it has found that fixed assets

turnover ratio of Royal Bank of Scotland declined from 3.31 to 3.09 times. Hence,

decreasing trend exhibits that in 2016, business unit failed to make optimum use of

fixed assets as compared to 2015. However, difference in the ratio of 2015 and 2016

structure which in turn helps it in gaining shareholder’s confidence.

2015 2016

0.35

0.40

0.45

Debt-equity ratio

in times

Figure 3: Debt-equity ratio

Efficiency ratios

2015 2016

0

0.5

1

1.5

2

2.5

3

3.5

Efficiency ratios

Figure 4: Efficiency ratios

Assets turnover ratio: From financial statement analysis, it has found that fixed assets

turnover ratio of Royal Bank of Scotland declined from 3.31 to 3.09 times. Hence,

decreasing trend exhibits that in 2016, business unit failed to make optimum use of

fixed assets as compared to 2015. However, difference in the ratio of 2015 and 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is not higher. Thus, it can be presented that such financial institution has made

effectual use of non-current assets in the concerned accounting years.

Total assets turnover ratio: Results of ratio analysis exhibit that assets turnover ratio

of Royal Bank of Scotland rose from 0.01 to 0.02 times. However, ratio is highly

lower which in turn presents Royal Bank’s failure regarding making use of both

current and fixed assets while carry out activities. Thus, for making improvement in

such performance banking institution is required to develop competent framework.

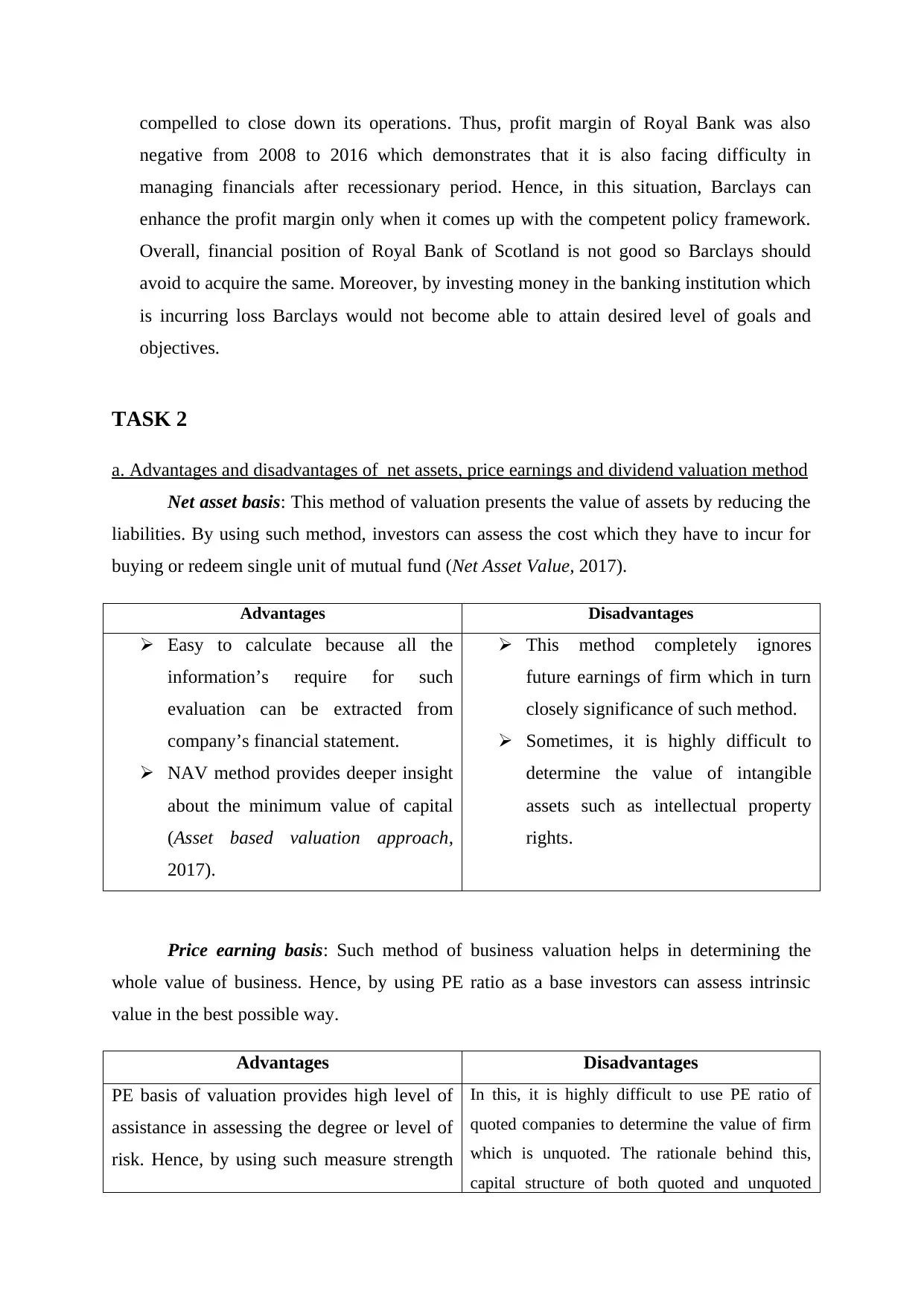

Investment ratio: In the accounting year, earning per share of Royal bank was -.34,

whereas in 2016, it reached on -1.19 at the end of 2016. The main reason behind such

decreasing EPS was negative margin generated by Royal Bank of Scotland in the year of

2015 and 2016. Along with this, due to the negative margin business unit also failed to

provide shareholders with appropriate return in the form of dividend. This in turn places

direct and negative impact on shareholder’s confidence and their investment decision.

2015 2016

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

EPS

Figure 5: Earnings per share

By considering the outcome of ratio analysis, acquisition strategy is not suggested to

Barclays bank. From assessment, it has found that solvency position of Royal Bank of

Scotland is effectual. However, on the other side, efficiency ratio analysis also presents

that such financial institution failed to make use of assets in a prominent way. Besides

this, after the period of 2013 sales revenue of the bank declined significantly. Meanwhile,

profitability aspect of Royal Bank also decreased which in turn adversely affects banking

unit’s position. The reason behind this, after the recessionary period several banks were

effectual use of non-current assets in the concerned accounting years.

Total assets turnover ratio: Results of ratio analysis exhibit that assets turnover ratio

of Royal Bank of Scotland rose from 0.01 to 0.02 times. However, ratio is highly

lower which in turn presents Royal Bank’s failure regarding making use of both

current and fixed assets while carry out activities. Thus, for making improvement in

such performance banking institution is required to develop competent framework.

Investment ratio: In the accounting year, earning per share of Royal bank was -.34,

whereas in 2016, it reached on -1.19 at the end of 2016. The main reason behind such

decreasing EPS was negative margin generated by Royal Bank of Scotland in the year of

2015 and 2016. Along with this, due to the negative margin business unit also failed to

provide shareholders with appropriate return in the form of dividend. This in turn places

direct and negative impact on shareholder’s confidence and their investment decision.

2015 2016

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

EPS

Figure 5: Earnings per share

By considering the outcome of ratio analysis, acquisition strategy is not suggested to

Barclays bank. From assessment, it has found that solvency position of Royal Bank of

Scotland is effectual. However, on the other side, efficiency ratio analysis also presents

that such financial institution failed to make use of assets in a prominent way. Besides

this, after the period of 2013 sales revenue of the bank declined significantly. Meanwhile,

profitability aspect of Royal Bank also decreased which in turn adversely affects banking

unit’s position. The reason behind this, after the recessionary period several banks were

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

compelled to close down its operations. Thus, profit margin of Royal Bank was also

negative from 2008 to 2016 which demonstrates that it is also facing difficulty in

managing financials after recessionary period. Hence, in this situation, Barclays can

enhance the profit margin only when it comes up with the competent policy framework.

Overall, financial position of Royal Bank of Scotland is not good so Barclays should

avoid to acquire the same. Moreover, by investing money in the banking institution which

is incurring loss Barclays would not become able to attain desired level of goals and

objectives.

TASK 2

a. Advantages and disadvantages of net assets, price earnings and dividend valuation method

Net asset basis: This method of valuation presents the value of assets by reducing the

liabilities. By using such method, investors can assess the cost which they have to incur for

buying or redeem single unit of mutual fund (Net Asset Value, 2017).

Advantages Disadvantages

Easy to calculate because all the

information’s require for such

evaluation can be extracted from

company’s financial statement.

NAV method provides deeper insight

about the minimum value of capital

(Asset based valuation approach,

2017).

This method completely ignores

future earnings of firm which in turn

closely significance of such method.

Sometimes, it is highly difficult to

determine the value of intangible

assets such as intellectual property

rights.

Price earning basis: Such method of business valuation helps in determining the

whole value of business. Hence, by using PE ratio as a base investors can assess intrinsic

value in the best possible way.

Advantages Disadvantages

PE basis of valuation provides high level of

assistance in assessing the degree or level of

risk. Hence, by using such measure strength

In this, it is highly difficult to use PE ratio of

quoted companies to determine the value of firm

which is unquoted. The rationale behind this,

capital structure of both quoted and unquoted

negative from 2008 to 2016 which demonstrates that it is also facing difficulty in

managing financials after recessionary period. Hence, in this situation, Barclays can

enhance the profit margin only when it comes up with the competent policy framework.

Overall, financial position of Royal Bank of Scotland is not good so Barclays should

avoid to acquire the same. Moreover, by investing money in the banking institution which

is incurring loss Barclays would not become able to attain desired level of goals and

objectives.

TASK 2

a. Advantages and disadvantages of net assets, price earnings and dividend valuation method

Net asset basis: This method of valuation presents the value of assets by reducing the

liabilities. By using such method, investors can assess the cost which they have to incur for

buying or redeem single unit of mutual fund (Net Asset Value, 2017).

Advantages Disadvantages

Easy to calculate because all the

information’s require for such

evaluation can be extracted from

company’s financial statement.

NAV method provides deeper insight

about the minimum value of capital

(Asset based valuation approach,

2017).

This method completely ignores

future earnings of firm which in turn

closely significance of such method.

Sometimes, it is highly difficult to

determine the value of intangible

assets such as intellectual property

rights.

Price earning basis: Such method of business valuation helps in determining the

whole value of business. Hence, by using PE ratio as a base investors can assess intrinsic

value in the best possible way.

Advantages Disadvantages

PE basis of valuation provides high level of

assistance in assessing the degree or level of

risk. Hence, by using such measure strength

In this, it is highly difficult to use PE ratio of

quoted companies to determine the value of firm

which is unquoted. The rationale behind this,

capital structure of both quoted and unquoted

of expected future earnings can be assessed

by firm (Business Valuation, 2017).

companies differ to a great extent.

Dividend valuation basis: This model of share valuation is based on dividend and

assumes stagnant growth (Duncan and et.al., 2017). Hence, by using the following formula

investors can assess intrinsic value:

D1 ÷ (k – g)

Advantages Disadvantages

This measure assists financial firms in

determining and evaluating the value

of assets.

Dividend basis of valuation is more

stable than EPS. Thus, by using this,

investors can assess suitable intrinsic

value (Calculating Intrinsic Value

With the Dividend Growth Model,

2017).

It is highly appropriate for valuing

non-controlling interest.

It does not consider non-physical

assets as image, employees etc which

in turn also has significant impact on

valuation.

Further, it provides mislead results

when level of assets vary.

It assumes that dividend growth is

constant. Whereas, it is not possible

in the case of most of the companies

because dividend decision varies as

per the income level.

Dividend model of valuation fails to

consider expectations of shareholders

while making assessment. Moreover,

some investors demand for dividend,

whereas other lays emphasis on future

appreciation.

b. Computation of intrinsic value

1. Net assets basis

NAV = (Fund assets - Fund Liabilities) / Total Fund Shares Outstanding

by firm (Business Valuation, 2017).

companies differ to a great extent.

Dividend valuation basis: This model of share valuation is based on dividend and

assumes stagnant growth (Duncan and et.al., 2017). Hence, by using the following formula

investors can assess intrinsic value:

D1 ÷ (k – g)

Advantages Disadvantages

This measure assists financial firms in

determining and evaluating the value

of assets.

Dividend basis of valuation is more

stable than EPS. Thus, by using this,

investors can assess suitable intrinsic

value (Calculating Intrinsic Value

With the Dividend Growth Model,

2017).

It is highly appropriate for valuing

non-controlling interest.

It does not consider non-physical

assets as image, employees etc which

in turn also has significant impact on

valuation.

Further, it provides mislead results

when level of assets vary.

It assumes that dividend growth is

constant. Whereas, it is not possible

in the case of most of the companies

because dividend decision varies as

per the income level.

Dividend model of valuation fails to

consider expectations of shareholders

while making assessment. Moreover,

some investors demand for dividend,

whereas other lays emphasis on future

appreciation.

b. Computation of intrinsic value

1. Net assets basis

NAV = (Fund assets - Fund Liabilities) / Total Fund Shares Outstanding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

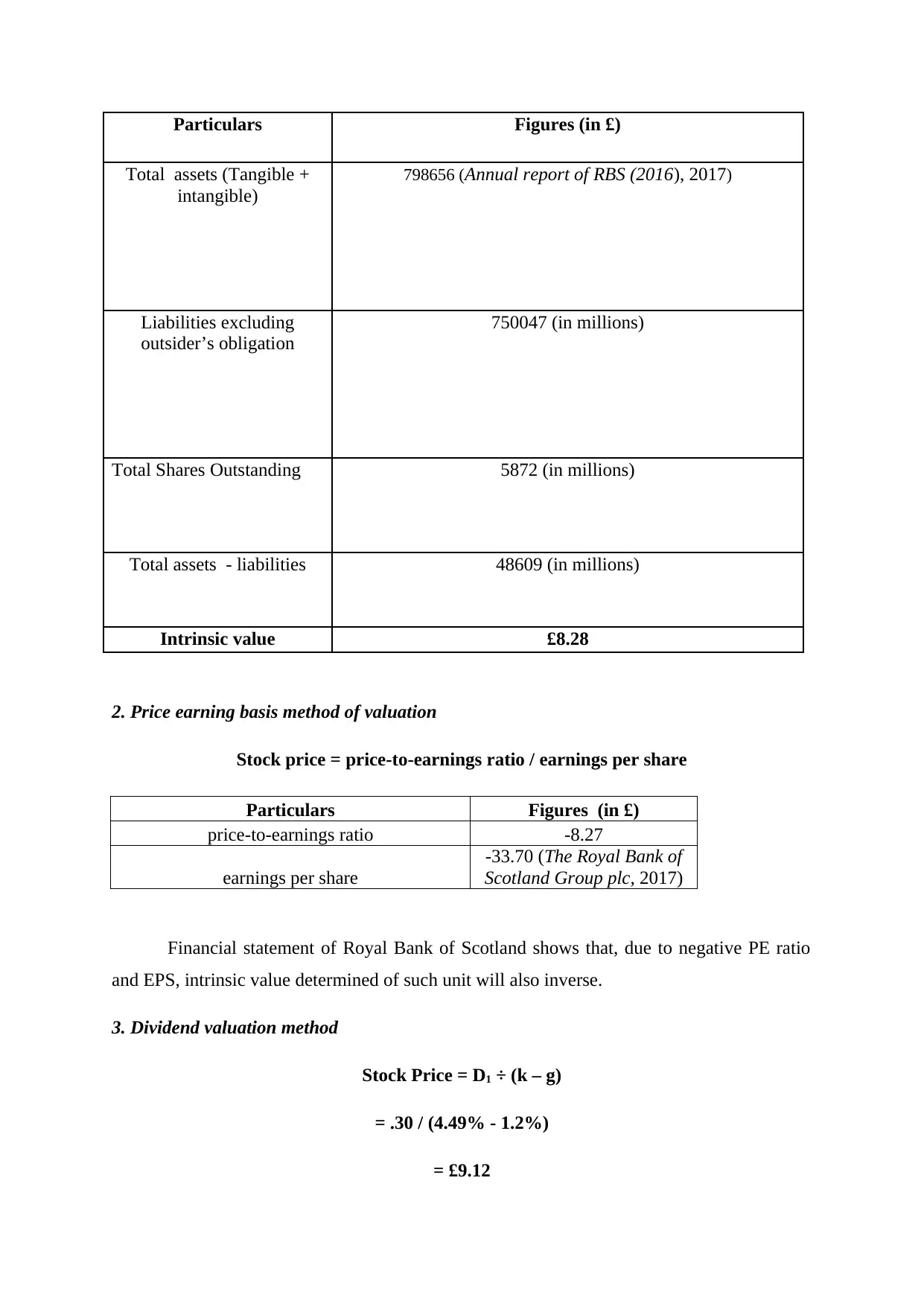

Particulars Figures (in £)

Total assets (Tangible +

intangible)

798656 (Annual report of RBS (2016), 2017)

Liabilities excluding

outsider’s obligation

750047 (in millions)

Total Shares Outstanding 5872 (in millions)

Total assets - liabilities 48609 (in millions)

Intrinsic value £8.28

2. Price earning basis method of valuation

Stock price = price-to-earnings ratio / earnings per share

Particulars Figures (in £)

price-to-earnings ratio -8.27

earnings per share

-33.70 (The Royal Bank of

Scotland Group plc, 2017)

Financial statement of Royal Bank of Scotland shows that, due to negative PE ratio

and EPS, intrinsic value determined of such unit will also inverse.

3. Dividend valuation method

Stock Price = D1 ÷ (k – g)

= .30 / (4.49% - 1.2%)

= £9.12

Total assets (Tangible +

intangible)

798656 (Annual report of RBS (2016), 2017)

Liabilities excluding

outsider’s obligation

750047 (in millions)

Total Shares Outstanding 5872 (in millions)

Total assets - liabilities 48609 (in millions)

Intrinsic value £8.28

2. Price earning basis method of valuation

Stock price = price-to-earnings ratio / earnings per share

Particulars Figures (in £)

price-to-earnings ratio -8.27

earnings per share

-33.70 (The Royal Bank of

Scotland Group plc, 2017)

Financial statement of Royal Bank of Scotland shows that, due to negative PE ratio

and EPS, intrinsic value determined of such unit will also inverse.

3. Dividend valuation method

Stock Price = D1 ÷ (k – g)

= .30 / (4.49% - 1.2%)

= £9.12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Required rate of return for equity = risk-free rate + (market risk premium × beta for equity)

= 2% + (2.8% * 0.89)

= 4.49%

c. Presenting the reasons due to which net assets, price earnings and dividend valuation

method differs

There are several reasons due to which outcome of valuation differs to the significant

level such as assumptions etc. For instance: dividend growth model assumes that returns

which will be offered by the company grow with constant rate. On the other side, price

earning basis lays emphasis on considering EPS and PE ratio while determining intrinsic

value. In contrast to this, NAV method focuses on undertaking value of total assets and

liabilities for assessing intrinsic value. Hence, this method focuses on dividing remaining

balance of assets by number of shares outstanding for calculating intrinsic value. Thus,

different assumptions which are considered by analyst is one of the main reason due to which

outcome of such business valuation methods vary to some extent.

d. Identifying various risk exposures which are facing by FTSE 100

On the basis of current financial position and performance several risks are

facing by Royal Bank of Scotland. Moreover, EPS of the firm is negative, whereas due to

the attainment of negative profit margin firm failed to offer dividend to the shareholders.

This in turn adversely impacts market share and brand image of firm. Moreover, the main

motive of investors behind making investment is to earn higher returns. Hence, when

shareholders are not provided with suitable or enough return then they lose their

confidence from concerned business operations (Borio, Gambacorta and Hofmann, 2017).

Thus, there is a risk that in the near future shareholders hesitate or do not prefer to invest

money in the shares of Royal Bank of Scotland. Along with this, after 2008, such banking

unit continuously incurred loss which in turn shows that company is facing difficulty in

managing the operations. However, as compared to before times, net loss of Royal Bank

decreased in the recent years. Thus, risk pertaining to loss can be mitigated by acquiring

company, Barclays bank, through the means of contingency plan. Thus, for maximizing

both revenue and profitability such banking unit is required to develop strategic

framework by evaluating the macro factors.

= 2% + (2.8% * 0.89)

= 4.49%

c. Presenting the reasons due to which net assets, price earnings and dividend valuation

method differs

There are several reasons due to which outcome of valuation differs to the significant

level such as assumptions etc. For instance: dividend growth model assumes that returns

which will be offered by the company grow with constant rate. On the other side, price

earning basis lays emphasis on considering EPS and PE ratio while determining intrinsic

value. In contrast to this, NAV method focuses on undertaking value of total assets and

liabilities for assessing intrinsic value. Hence, this method focuses on dividing remaining

balance of assets by number of shares outstanding for calculating intrinsic value. Thus,

different assumptions which are considered by analyst is one of the main reason due to which

outcome of such business valuation methods vary to some extent.

d. Identifying various risk exposures which are facing by FTSE 100

On the basis of current financial position and performance several risks are

facing by Royal Bank of Scotland. Moreover, EPS of the firm is negative, whereas due to

the attainment of negative profit margin firm failed to offer dividend to the shareholders.

This in turn adversely impacts market share and brand image of firm. Moreover, the main

motive of investors behind making investment is to earn higher returns. Hence, when

shareholders are not provided with suitable or enough return then they lose their

confidence from concerned business operations (Borio, Gambacorta and Hofmann, 2017).

Thus, there is a risk that in the near future shareholders hesitate or do not prefer to invest

money in the shares of Royal Bank of Scotland. Along with this, after 2008, such banking

unit continuously incurred loss which in turn shows that company is facing difficulty in

managing the operations. However, as compared to before times, net loss of Royal Bank

decreased in the recent years. Thus, risk pertaining to loss can be mitigated by acquiring

company, Barclays bank, through the means of contingency plan. Thus, for maximizing

both revenue and profitability such banking unit is required to develop strategic

framework by evaluating the macro factors.

e. Stating the extent to which economic environment have an impact on results and valuation

By taking into consideration business valuation methods it can be said that economic

environment has significant impact on results and evaluation. Moreover, economic

environment or condition such as inflation, deflation etc closely influences financial position

of firm. In the period of 2008, situation of recession occurs that affects all the banking units

and other firm globally. Due to recessionary condition profitability aspect of the company

influenced significantly and thereby EPS. Besides this, decision making aspect of the

company is also highly based on the net profit margin generated by it during the accounting

year. Thus, it is one of the main reasons due to which variation occur in the results. In 2008,

when condition of global recession occurred, then majority of the banks were not in position

to run their operations effectually (Avdjiev, McCauley and Shin, 2016). Thus, both Barclays

and Royal Bank of Scotland should develop contingent risk management plan to cope up with

the difficult situation.

TASK 3

Recommendations

Financial statement evaluation shows that debt-equity position of Royal Bank of

Scotland is good. Nevertheless, due to the condition of global recession profitability aspect of

the banking unit was decreased. Hence, by developing risk management policies and

frameworks profitability aspect of the firm can be improved. Thus, on the basis of such

aspect acquisition of Royal Bank of Scotland is not recommended to Barclays. Further,

outcome of asset valuation method presents that shares of Royal Bank of Scotland is

undervalued. Thus, Barclays bank should acquire such FTSE 100 company because its shares

are relatively cheap in against to its peers. Besides this, undervalued stocks also have some

prospect for future growth.

Along with this, the rationale behind such changing level of recommendation is that

undervalued stocks offer high value of money to investors. From assessment, it has been

identified that when price level of stock goes below to the level which is considered by

financial experts as fair then chances in relation to value enhancement increases significantly

(The Advantages of Buying Undervalued Stock, 2017). By keeping all such aspects in mind

acquisition strategy is advised to Barclays bank.

By taking into consideration business valuation methods it can be said that economic

environment has significant impact on results and evaluation. Moreover, economic

environment or condition such as inflation, deflation etc closely influences financial position

of firm. In the period of 2008, situation of recession occurs that affects all the banking units

and other firm globally. Due to recessionary condition profitability aspect of the company

influenced significantly and thereby EPS. Besides this, decision making aspect of the

company is also highly based on the net profit margin generated by it during the accounting

year. Thus, it is one of the main reasons due to which variation occur in the results. In 2008,

when condition of global recession occurred, then majority of the banks were not in position

to run their operations effectually (Avdjiev, McCauley and Shin, 2016). Thus, both Barclays

and Royal Bank of Scotland should develop contingent risk management plan to cope up with

the difficult situation.

TASK 3

Recommendations

Financial statement evaluation shows that debt-equity position of Royal Bank of

Scotland is good. Nevertheless, due to the condition of global recession profitability aspect of

the banking unit was decreased. Hence, by developing risk management policies and

frameworks profitability aspect of the firm can be improved. Thus, on the basis of such

aspect acquisition of Royal Bank of Scotland is not recommended to Barclays. Further,

outcome of asset valuation method presents that shares of Royal Bank of Scotland is

undervalued. Thus, Barclays bank should acquire such FTSE 100 company because its shares

are relatively cheap in against to its peers. Besides this, undervalued stocks also have some

prospect for future growth.

Along with this, the rationale behind such changing level of recommendation is that

undervalued stocks offer high value of money to investors. From assessment, it has been

identified that when price level of stock goes below to the level which is considered by

financial experts as fair then chances in relation to value enhancement increases significantly

(The Advantages of Buying Undervalued Stock, 2017). By keeping all such aspects in mind

acquisition strategy is advised to Barclays bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.