Financial Management Report: Risk and Investment Analysis

VerifiedAdded on 2022/12/14

|16

|3331

|401

Report

AI Summary

This report delves into the core concepts of International Financial Management, presenting a detailed analysis of financial management practices within enterprises. The report begins with an introduction to financial management, emphasizing its importance in planning, organizing, managing, and reporting financial capital. It then proceeds to address three key questions, primarily involving numerical tasks. The first question focuses on calculating the expected Net Present Value (NPV) and its standard deviation, essential for assessing investment viability under uncertainty. The subsequent questions explore NPV calculations under various scenarios to aid in decision-making, considering factors like cash inflows, probabilities, and discounting rates. The report includes detailed calculations and interpretations, providing insights into project rankings, the comparison of NPV and Internal Rate of Return (IRR), and the probability of achieving specific financial outcomes, such as avoiding liquidation or exceeding certain NPV thresholds. The analysis incorporates concepts of risk assessment, capital budgeting, and financial decision-making, offering a comprehensive overview of the subject.

International Financial Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3......................................................................................................................................10

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3......................................................................................................................................10

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

2

INTRODUCTION

In every enterprise, financial management practice is significant process. This is

t mechanism of preparing, arranging, managing, and reporting financial capital in attempt to

meet the aims and priorities of an entity That's a superior practice for managing an entity 's

financial functions, like fund acquisition, fund allocation, billing, transfers, risk evaluation, and

everything else involving capital. Simply financial management is structured application of

common managerial concepts to an organization's financial assets. Quality gasoline and routine

service are provided by proper financial management in order for a company's operations to run

smoothly. If a company's budgets aren't handled adequately, it can face roadblocks that might

stifle its progress and developments (Ameliawati and Setiyani, 2018).

Typically, companies have a specialized division that handles the enterprise 's financial

affairs. A financial officer is responsible for overseeing an organization's finances and services.

This place is where all financial decisions are made. Dependent on the organization 's

background the finance division might have multiple designations to meet the corporation's

different requirements. The study report comprises three different tasks that covers numerical

tasks based on given information. In first question, expected NPV and standard deviation of NPV

has been computed while in second and third question, NPVs based on different scenarios has

been computed to support decision making,

MAIN BODY

Question 1

a. The expected NPV:

Expected NPV is an investment appraisal strategy that accounts for volatility by measuring net-

present values in various conditions as well as weighting to arrive at most possible NPV. So

rather than depending on single NPV, businesses calculate NPVs for a variety of cases, such as

the base point, worst scenario, and best situation measure the likelihood of each situations

outcome, and measure the NPVs measured as per their respective chances to arrive at the

estimated NPV (Atmadja and Saputra, 2018). Since it acknowledges the complexity involved in

predicting future outcomes, anticipated NPV is more effective interpolation than standard NPV.

The NPV approach is a technique for determining a project's feasibility. This takes time worth of

capital into account. The valuation of potential cash flows would be lower than value of

3

In every enterprise, financial management practice is significant process. This is

t mechanism of preparing, arranging, managing, and reporting financial capital in attempt to

meet the aims and priorities of an entity That's a superior practice for managing an entity 's

financial functions, like fund acquisition, fund allocation, billing, transfers, risk evaluation, and

everything else involving capital. Simply financial management is structured application of

common managerial concepts to an organization's financial assets. Quality gasoline and routine

service are provided by proper financial management in order for a company's operations to run

smoothly. If a company's budgets aren't handled adequately, it can face roadblocks that might

stifle its progress and developments (Ameliawati and Setiyani, 2018).

Typically, companies have a specialized division that handles the enterprise 's financial

affairs. A financial officer is responsible for overseeing an organization's finances and services.

This place is where all financial decisions are made. Dependent on the organization 's

background the finance division might have multiple designations to meet the corporation's

different requirements. The study report comprises three different tasks that covers numerical

tasks based on given information. In first question, expected NPV and standard deviation of NPV

has been computed while in second and third question, NPVs based on different scenarios has

been computed to support decision making,

MAIN BODY

Question 1

a. The expected NPV:

Expected NPV is an investment appraisal strategy that accounts for volatility by measuring net-

present values in various conditions as well as weighting to arrive at most possible NPV. So

rather than depending on single NPV, businesses calculate NPVs for a variety of cases, such as

the base point, worst scenario, and best situation measure the likelihood of each situations

outcome, and measure the NPVs measured as per their respective chances to arrive at the

estimated NPV (Atmadja and Saputra, 2018). Since it acknowledges the complexity involved in

predicting future outcomes, anticipated NPV is more effective interpolation than standard NPV.

The NPV approach is a technique for determining a project's feasibility. This takes time worth of

capital into account. The valuation of potential cash flows would be lower than value of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

present cash flows. As result, the greater the cash balance, the lower the valuation. This is a

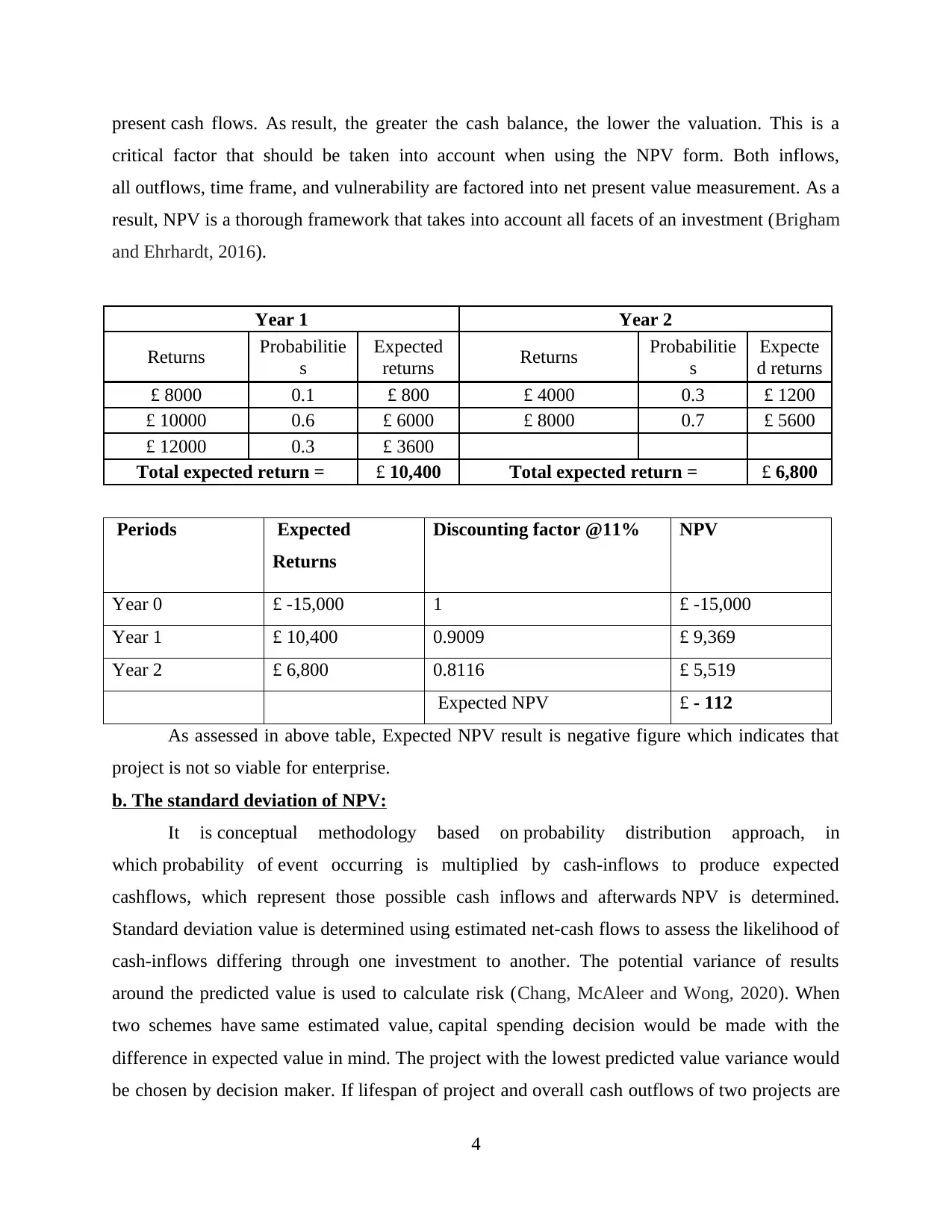

critical factor that should be taken into account when using the NPV form. Both inflows,

all outflows, time frame, and vulnerability are factored into net present value measurement. As a

result, NPV is a thorough framework that takes into account all facets of an investment (Brigham

and Ehrhardt, 2016).

Year 1 Year 2

Returns Probabilitie

s

Expected

returns Returns Probabilitie

s

Expecte

d returns

£ 8000 0.1 £ 800 £ 4000 0.3 £ 1200

£ 10000 0.6 £ 6000 £ 8000 0.7 £ 5600

£ 12000 0.3 £ 3600

Total expected return = £ 10,400 Total expected return = £ 6,800

Periods Expected

Returns

Discounting factor @11% NPV

Year 0 £ -15,000 1 £ -15,000

Year 1 £ 10,400 0.9009 £ 9,369

Year 2 £ 6,800 0.8116 £ 5,519

Expected NPV £ - 112

As assessed in above table, Expected NPV result is negative figure which indicates that

project is not so viable for enterprise.

b. The standard deviation of NPV:

It is conceptual methodology based on probability distribution approach, in

which probability of event occurring is multiplied by cash-inflows to produce expected

cashflows, which represent those possible cash inflows and afterwards NPV is determined.

Standard deviation value is determined using estimated net-cash flows to assess the likelihood of

cash-inflows differing through one investment to another. The potential variance of results

around the predicted value is used to calculate risk (Chang, McAleer and Wong, 2020). When

two schemes have same estimated value, capital spending decision would be made with the

difference in expected value in mind. The project with the lowest predicted value variance would

be chosen by decision maker. If lifespan of project and overall cash outflows of two projects are

4

critical factor that should be taken into account when using the NPV form. Both inflows,

all outflows, time frame, and vulnerability are factored into net present value measurement. As a

result, NPV is a thorough framework that takes into account all facets of an investment (Brigham

and Ehrhardt, 2016).

Year 1 Year 2

Returns Probabilitie

s

Expected

returns Returns Probabilitie

s

Expecte

d returns

£ 8000 0.1 £ 800 £ 4000 0.3 £ 1200

£ 10000 0.6 £ 6000 £ 8000 0.7 £ 5600

£ 12000 0.3 £ 3600

Total expected return = £ 10,400 Total expected return = £ 6,800

Periods Expected

Returns

Discounting factor @11% NPV

Year 0 £ -15,000 1 £ -15,000

Year 1 £ 10,400 0.9009 £ 9,369

Year 2 £ 6,800 0.8116 £ 5,519

Expected NPV £ - 112

As assessed in above table, Expected NPV result is negative figure which indicates that

project is not so viable for enterprise.

b. The standard deviation of NPV:

It is conceptual methodology based on probability distribution approach, in

which probability of event occurring is multiplied by cash-inflows to produce expected

cashflows, which represent those possible cash inflows and afterwards NPV is determined.

Standard deviation value is determined using estimated net-cash flows to assess the likelihood of

cash-inflows differing through one investment to another. The potential variance of results

around the predicted value is used to calculate risk (Chang, McAleer and Wong, 2020). When

two schemes have same estimated value, capital spending decision would be made with the

difference in expected value in mind. The project with the lowest predicted value variance would

be chosen by decision maker. If lifespan of project and overall cash outflows of two projects are

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

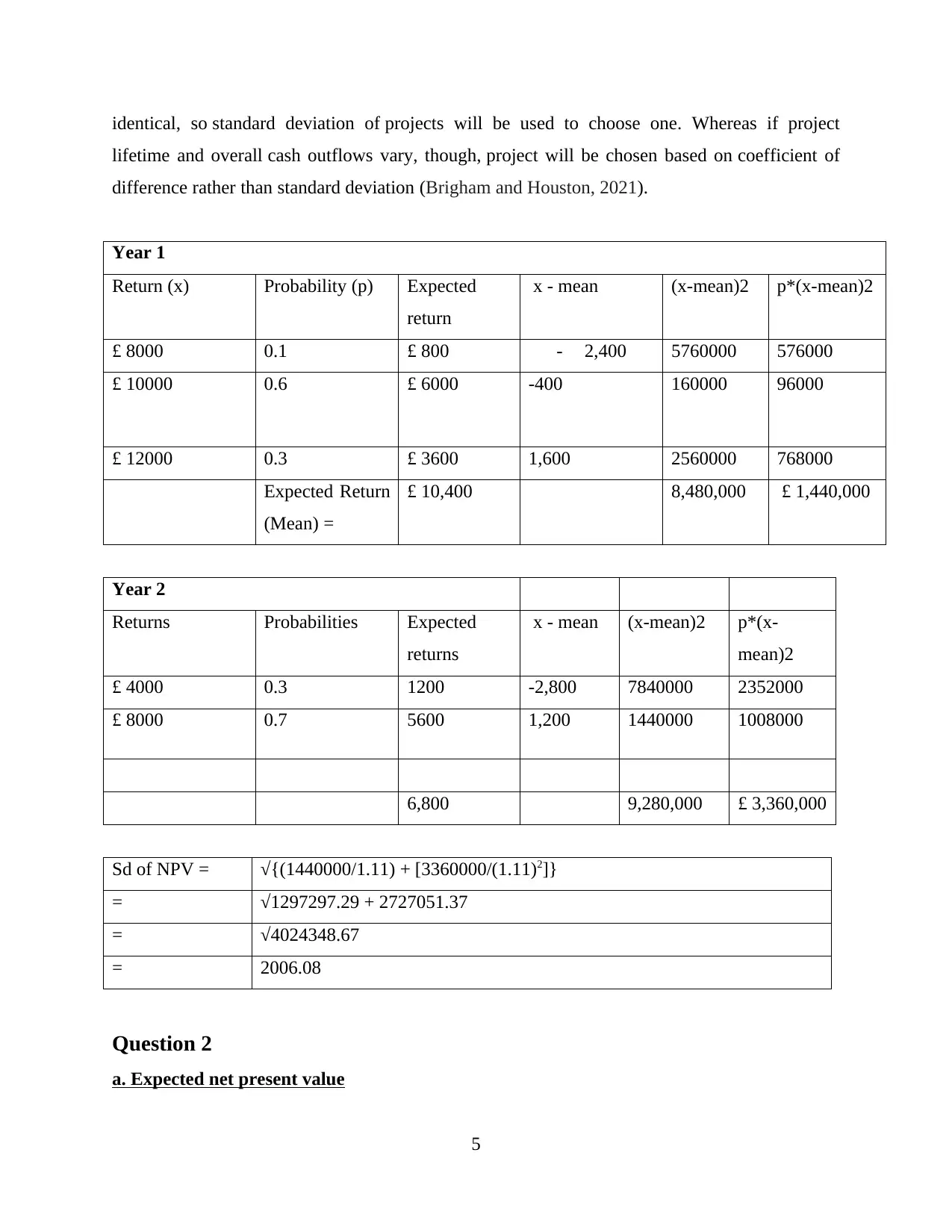

identical, so standard deviation of projects will be used to choose one. Whereas if project

lifetime and overall cash outflows vary, though, project will be chosen based on coefficient of

difference rather than standard deviation (Brigham and Houston, 2021).

Year 1

Return (x) Probability (p) Expected

return

x - mean (x-mean)2 p*(x-mean)2

£ 8000 0.1 £ 800 - 2,400 5760000 576000

£ 10000 0.6 £ 6000 -400 160000 96000

£ 12000 0.3 £ 3600 1,600 2560000 768000

Expected Return

(Mean) =

£ 10,400 8,480,000 £ 1,440,000

Year 2

Returns Probabilities Expected

returns

x - mean (x-mean)2 p*(x-

mean)2

£ 4000 0.3 1200 -2,800 7840000 2352000

£ 8000 0.7 5600 1,200 1440000 1008000

6,800 9,280,000 £ 3,360,000

Sd of NPV = √{(1440000/1.11) + [3360000/(1.11)2]}

= √1297297.29 + 2727051.37

= √4024348.67

= 2006.08

Question 2

a. Expected net present value

5

lifetime and overall cash outflows vary, though, project will be chosen based on coefficient of

difference rather than standard deviation (Brigham and Houston, 2021).

Year 1

Return (x) Probability (p) Expected

return

x - mean (x-mean)2 p*(x-mean)2

£ 8000 0.1 £ 800 - 2,400 5760000 576000

£ 10000 0.6 £ 6000 -400 160000 96000

£ 12000 0.3 £ 3600 1,600 2560000 768000

Expected Return

(Mean) =

£ 10,400 8,480,000 £ 1,440,000

Year 2

Returns Probabilities Expected

returns

x - mean (x-mean)2 p*(x-

mean)2

£ 4000 0.3 1200 -2,800 7840000 2352000

£ 8000 0.7 5600 1,200 1440000 1008000

6,800 9,280,000 £ 3,360,000

Sd of NPV = √{(1440000/1.11) + [3360000/(1.11)2]}

= √1297297.29 + 2727051.37

= √4024348.67

= 2006.08

Question 2

a. Expected net present value

5

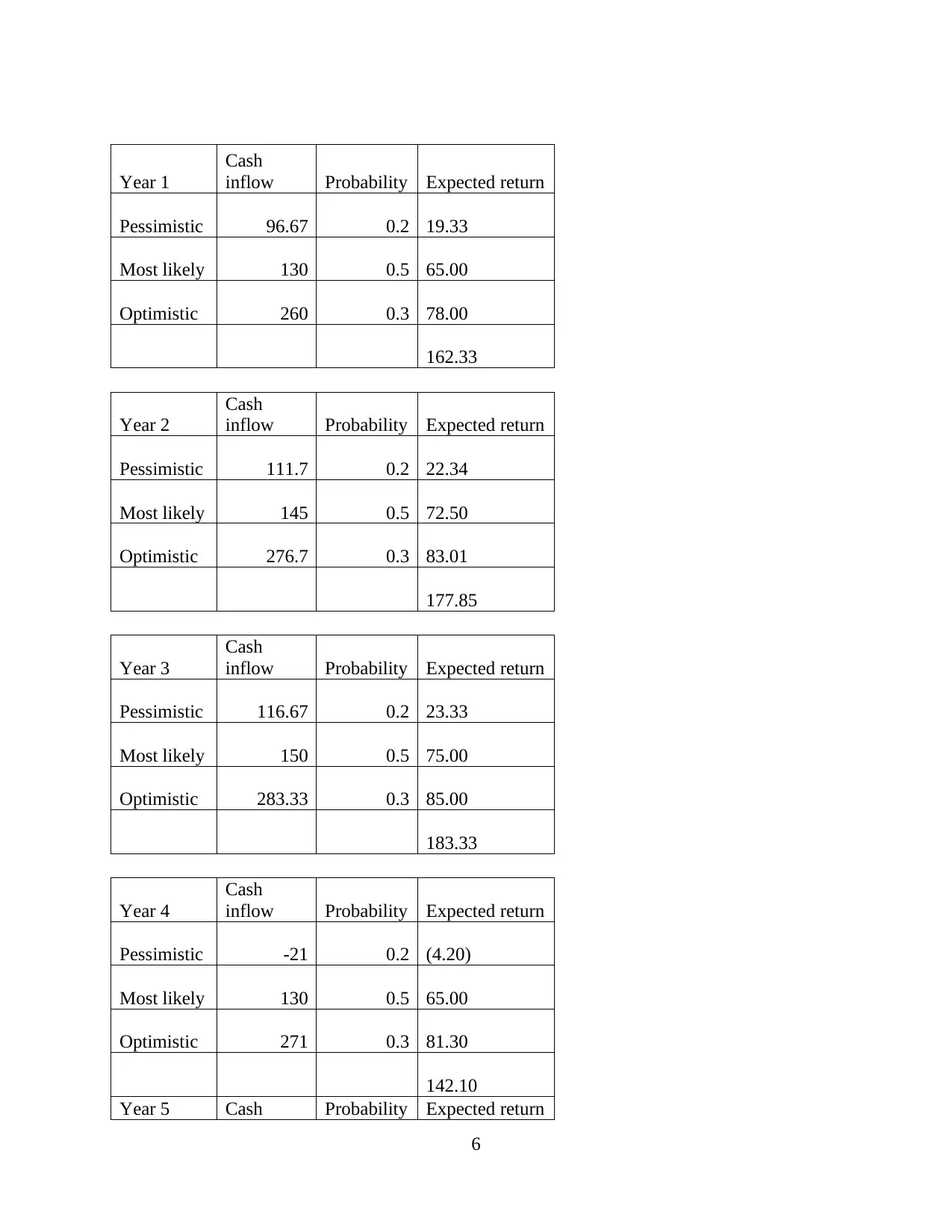

Year 1

Cash

inflow Probability Expected return

Pessimistic 96.67 0.2 19.33

Most likely 130 0.5 65.00

Optimistic 260 0.3 78.00

162.33

Year 2

Cash

inflow Probability Expected return

Pessimistic 111.7 0.2 22.34

Most likely 145 0.5 72.50

Optimistic 276.7 0.3 83.01

177.85

Year 3

Cash

inflow Probability Expected return

Pessimistic 116.67 0.2 23.33

Most likely 150 0.5 75.00

Optimistic 283.33 0.3 85.00

183.33

Year 4

Cash

inflow Probability Expected return

Pessimistic -21 0.2 (4.20)

Most likely 130 0.5 65.00

Optimistic 271 0.3 81.30

142.10

Year 5 Cash Probability Expected return

6

Cash

inflow Probability Expected return

Pessimistic 96.67 0.2 19.33

Most likely 130 0.5 65.00

Optimistic 260 0.3 78.00

162.33

Year 2

Cash

inflow Probability Expected return

Pessimistic 111.7 0.2 22.34

Most likely 145 0.5 72.50

Optimistic 276.7 0.3 83.01

177.85

Year 3

Cash

inflow Probability Expected return

Pessimistic 116.67 0.2 23.33

Most likely 150 0.5 75.00

Optimistic 283.33 0.3 85.00

183.33

Year 4

Cash

inflow Probability Expected return

Pessimistic -21 0.2 (4.20)

Most likely 130 0.5 65.00

Optimistic 271 0.3 81.30

142.10

Year 5 Cash Probability Expected return

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

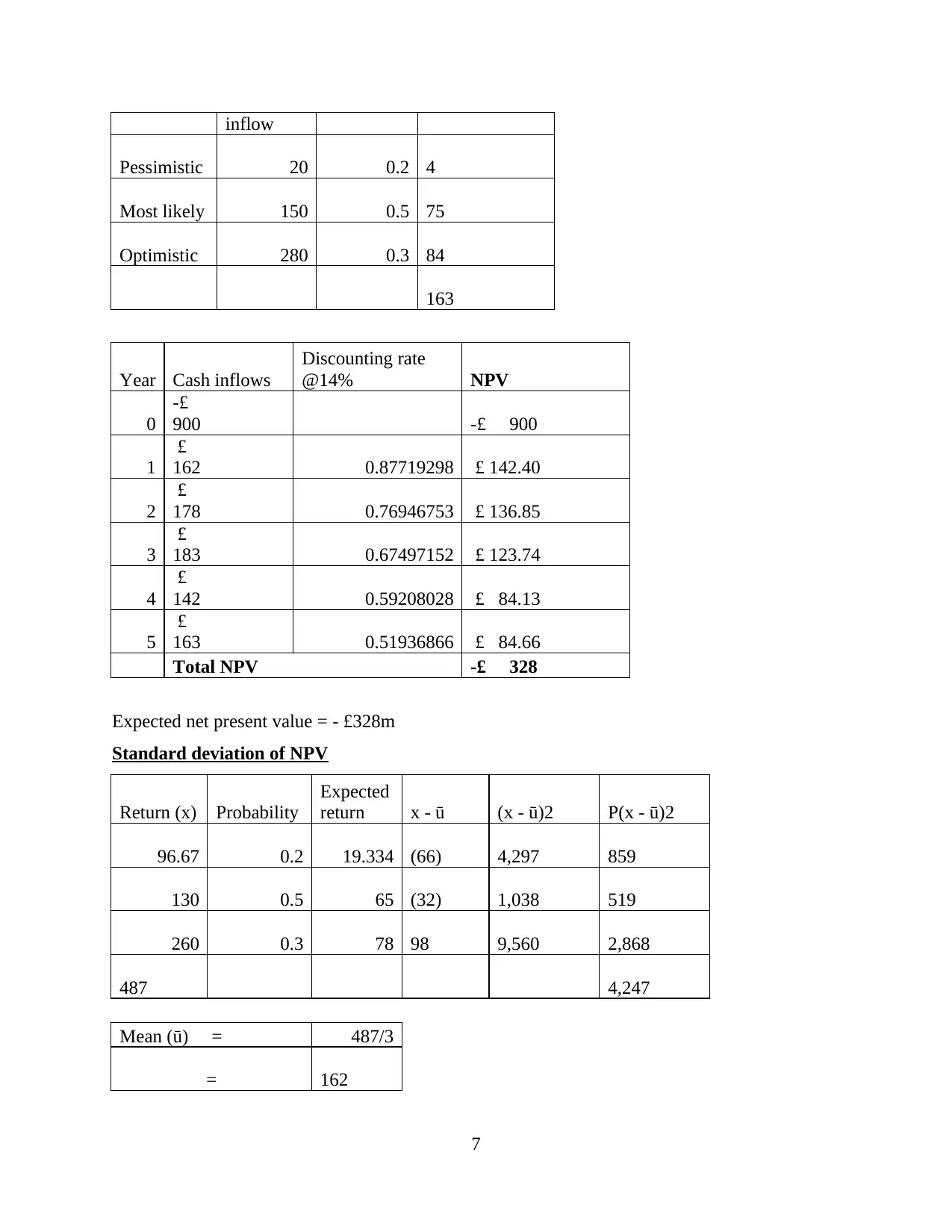

inflow

Pessimistic 20 0.2 4

Most likely 150 0.5 75

Optimistic 280 0.3 84

163

Year Cash inflows

Discounting rate

@14% NPV

0

-£

900 -£ 900

1

£

162 0.87719298 £ 142.40

2

£

178 0.76946753 £ 136.85

3

£

183 0.67497152 £ 123.74

4

£

142 0.59208028 £ 84.13

5

£

163 0.51936866 £ 84.66

Total NPV -£ 328

Expected net present value = - £328m

Standard deviation of NPV

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

Mean (ū) = 487/3

= 162

7

Pessimistic 20 0.2 4

Most likely 150 0.5 75

Optimistic 280 0.3 84

163

Year Cash inflows

Discounting rate

@14% NPV

0

-£

900 -£ 900

1

£

162 0.87719298 £ 142.40

2

£

178 0.76946753 £ 136.85

3

£

183 0.67497152 £ 123.74

4

£

142 0.59208028 £ 84.13

5

£

163 0.51936866 £ 84.66

Total NPV -£ 328

Expected net present value = - £328m

Standard deviation of NPV

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

96.67 0.2 19.334 (66) 4,297 859

130 0.5 65 (32) 1,038 519

260 0.3 78 98 9,560 2,868

487 4,247

Mean (ū) = 487/3

= 162

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

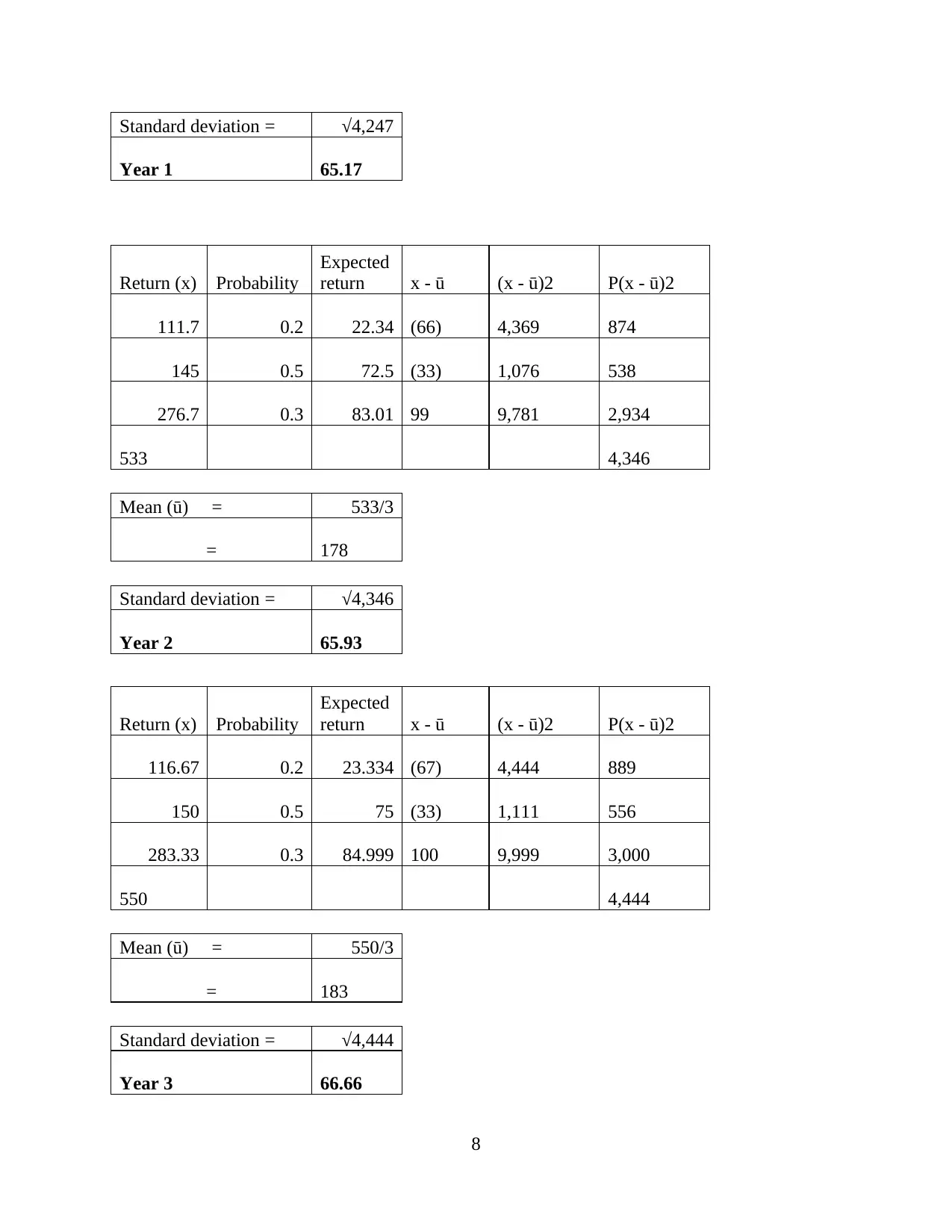

Standard deviation = √4,247

Year 1 65.17

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

Standard deviation = √4,444

Year 3 66.66

8

Year 1 65.17

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

111.7 0.2 22.34 (66) 4,369 874

145 0.5 72.5 (33) 1,076 538

276.7 0.3 83.01 99 9,781 2,934

533 4,346

Mean (ū) = 533/3

= 178

Standard deviation = √4,346

Year 2 65.93

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

116.67 0.2 23.334 (67) 4,444 889

150 0.5 75 (33) 1,111 556

283.33 0.3 84.999 100 9,999 3,000

550 4,444

Mean (ū) = 550/3

= 183

Standard deviation = √4,444

Year 3 66.66

8

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

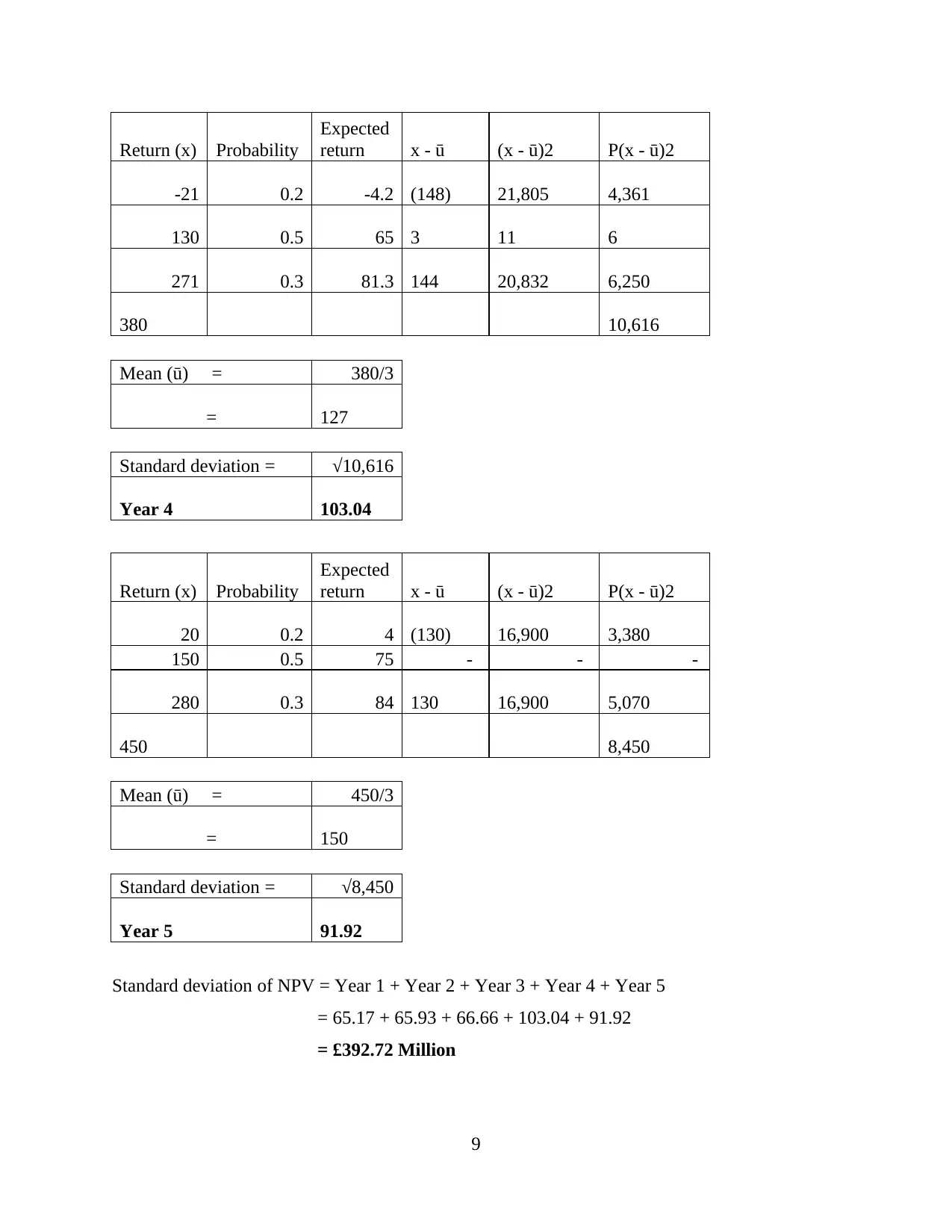

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

Standard deviation of NPV = Year 1 + Year 2 + Year 3 + Year 4 + Year 5

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

9

Expected

return x - ū (x - ū)2 P(x - ū)2

-21 0.2 -4.2 (148) 21,805 4,361

130 0.5 65 3 11 6

271 0.3 81.3 144 20,832 6,250

380 10,616

Mean (ū) = 380/3

= 127

Standard deviation = √10,616

Year 4 103.04

Return (x) Probability

Expected

return x - ū (x - ū)2 P(x - ū)2

20 0.2 4 (130) 16,900 3,380

150 0.5 75 - - -

280 0.3 84 130 16,900 5,070

450 8,450

Mean (ū) = 450/3

= 150

Standard deviation = √8,450

Year 5 91.92

Standard deviation of NPV = Year 1 + Year 2 + Year 3 + Year 4 + Year 5

= 65.17 + 65.93 + 66.66 + 103.04 + 91.92

= £392.72 Million

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

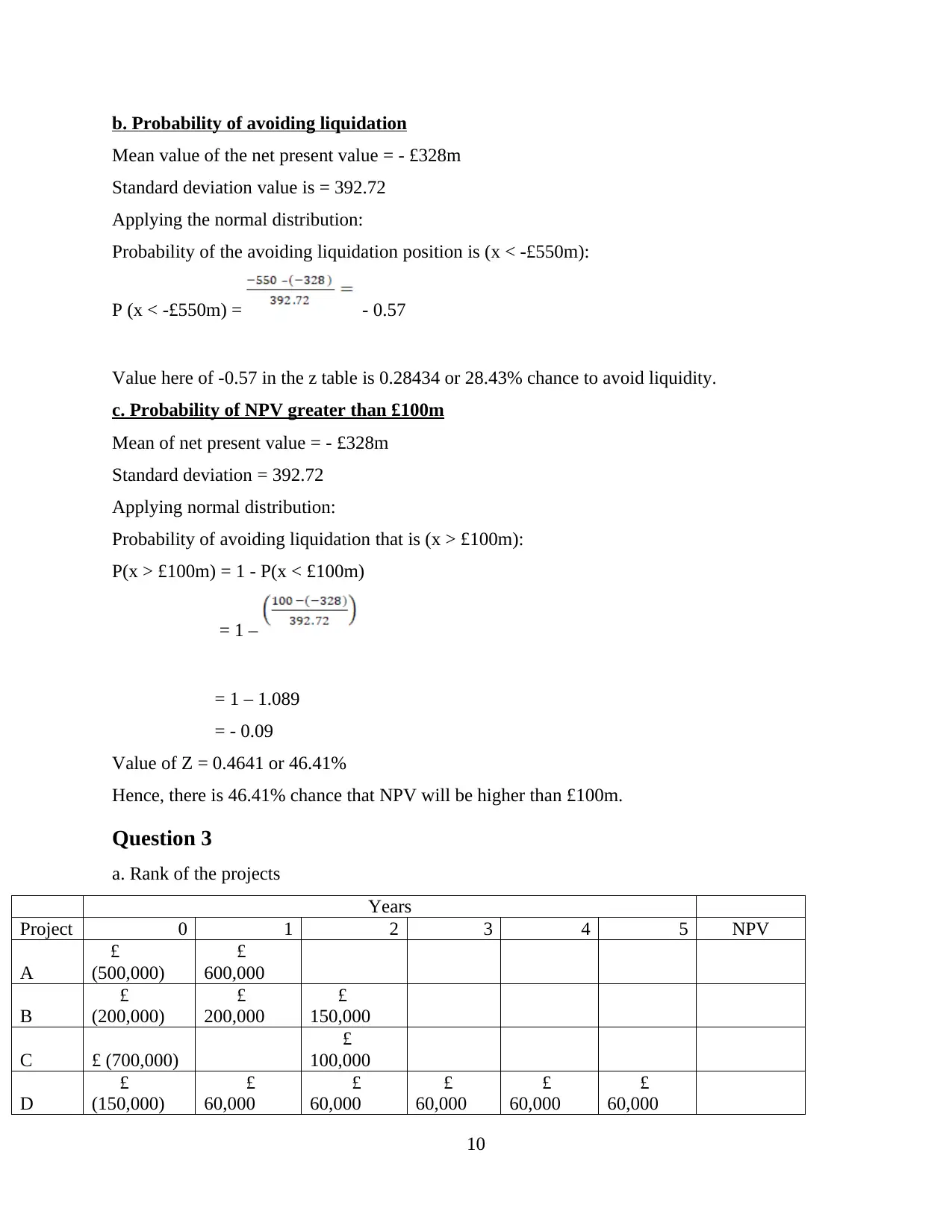

b. Probability of avoiding liquidation

Mean value of the net present value = - £328m

Standard deviation value is = 392.72

Applying the normal distribution:

Probability of the avoiding liquidation position is (x < -£550m):

P (x < -£550m) = - 0.57

Value here of -0.57 in the z table is 0.28434 or 28.43% chance to avoid liquidity.

c. Probability of NPV greater than £100m

Mean of net present value = - £328m

Standard deviation = 392.72

Applying normal distribution:

Probability of avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 –

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Hence, there is 46.41% chance that NPV will be higher than £100m.

Question 3

a. Rank of the projects

Years

Project 0 1 2 3 4 5 NPV

A

£

(500,000)

£

600,000

B

£

(200,000)

£

200,000

£

150,000

C £ (700,000)

£

100,000

D

£

(150,000)

£

60,000

£

60,000

£

60,000

£

60,000

£

60,000

10

Mean value of the net present value = - £328m

Standard deviation value is = 392.72

Applying the normal distribution:

Probability of the avoiding liquidation position is (x < -£550m):

P (x < -£550m) = - 0.57

Value here of -0.57 in the z table is 0.28434 or 28.43% chance to avoid liquidity.

c. Probability of NPV greater than £100m

Mean of net present value = - £328m

Standard deviation = 392.72

Applying normal distribution:

Probability of avoiding liquidation that is (x > £100m):

P(x > £100m) = 1 - P(x < £100m)

= 1 –

= 1 – 1.089

= - 0.09

Value of Z = 0.4641 or 46.41%

Hence, there is 46.41% chance that NPV will be higher than £100m.

Question 3

a. Rank of the projects

Years

Project 0 1 2 3 4 5 NPV

A

£

(500,000)

£

600,000

B

£

(200,000)

£

200,000

£

150,000

C £ (700,000)

£

100,000

D

£

(150,000)

£

60,000

£

60,000

£

60,000

£

60,000

£

60,000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Discou

nt

factor

@10% 0.90909091 0.82644628

0.751314

8 0.6830135 0.6209213

A

£

(500,000)

£

545,454.55

£

45,455

B

£

(200,000)

£

181,818.18

£

123,966.94

£

105,785

C

£

(700,000)

£

82,644.63

£

(617,355)

D

£

(150,000)

£

54,545.45

£

49,586.78

£

45,078.89

£

40,980.81

£

37,255.28

£

77,447

Ranks Project NPV

1 B £ 105,785

2 D £ 77,447

3 A £ 45,455

4 C £ (617,355)

b. Net present value vs. internal rate of return

Reasons: IRR and NPV approaches conflict in capital budgeting corresponds to a condition

wherein the NPV approach rates projects differently than the IRR method. When there is a

disparity, the organization should consider the project(s) with the greater NPV. Two of most

commonly used investment valuation as well as capital budgeting methods are NPV and intrinsic

rate-of-return (IRR). They're close in that they're both discounted cash-flows models, which

means they take time value of capital into account (Dwiastanti, 2017). They do, though, vary in

terms of their core strategy as well as their strengths and limitations. The pound amount of value

generated or missed by performing project is NPV, which is absolute indicator. The IRR,

on other side, is relative indicator of project's rate of return throughout its life cycle. Independent

proposals are those in which approval of one proposal has no bearing on acceptance of another.

We will approve all individual ventures as they add value, so there is no disagreement between

NPV as well as IRR. Any ventures with positive net present value (NPV) will be accepted by

the organization (Eschenbach and Lewis, 2019).

11

nt

factor

@10% 0.90909091 0.82644628

0.751314

8 0.6830135 0.6209213

A

£

(500,000)

£

545,454.55

£

45,455

B

£

(200,000)

£

181,818.18

£

123,966.94

£

105,785

C

£

(700,000)

£

82,644.63

£

(617,355)

D

£

(150,000)

£

54,545.45

£

49,586.78

£

45,078.89

£

40,980.81

£

37,255.28

£

77,447

Ranks Project NPV

1 B £ 105,785

2 D £ 77,447

3 A £ 45,455

4 C £ (617,355)

b. Net present value vs. internal rate of return

Reasons: IRR and NPV approaches conflict in capital budgeting corresponds to a condition

wherein the NPV approach rates projects differently than the IRR method. When there is a

disparity, the organization should consider the project(s) with the greater NPV. Two of most

commonly used investment valuation as well as capital budgeting methods are NPV and intrinsic

rate-of-return (IRR). They're close in that they're both discounted cash-flows models, which

means they take time value of capital into account (Dwiastanti, 2017). They do, though, vary in

terms of their core strategy as well as their strengths and limitations. The pound amount of value

generated or missed by performing project is NPV, which is absolute indicator. The IRR,

on other side, is relative indicator of project's rate of return throughout its life cycle. Independent

proposals are those in which approval of one proposal has no bearing on acceptance of another.

We will approve all individual ventures as they add value, so there is no disagreement between

NPV as well as IRR. Any ventures with positive net present value (NPV) will be accepted by

the organization (Eschenbach and Lewis, 2019).

11

In scenario of mutually exclusive ventures, although, NPV and IRR dispute can occur,

where one proposal has greater NPV but higher IRR. Projects that are mutually exclusive are

those in which approval of one proposal precludes consideration of others. The disagreement

occurs either as result of project's relative scale or as result of projects' varying cash flow

allocation. As NPV is objective metric, a project that adds more pound value would be ranked

higher, irrespective of initial investment involved (Haydarov, 2020). IRR is relative metric, but

programs with the highest investment yield will be ranked better regardless of overall value

added. Accept project with higher NPV if an NPV and IRR dispute occurs. That's

because intrinsic rate of return means that all cash flows should be reinvested at same rate. This

theory is flawed since there's no certainty that similarly lucrative opportunities will become open

as quickly as cash flows become available. Reinvestment threat is risk of acquiring cash flows

but not getting adequate time to reinvest them. NPV, on other side, does not have this issue

because it expects reinvestment at cost of money, that is conservative and rational presumption

(Loke, 2017).

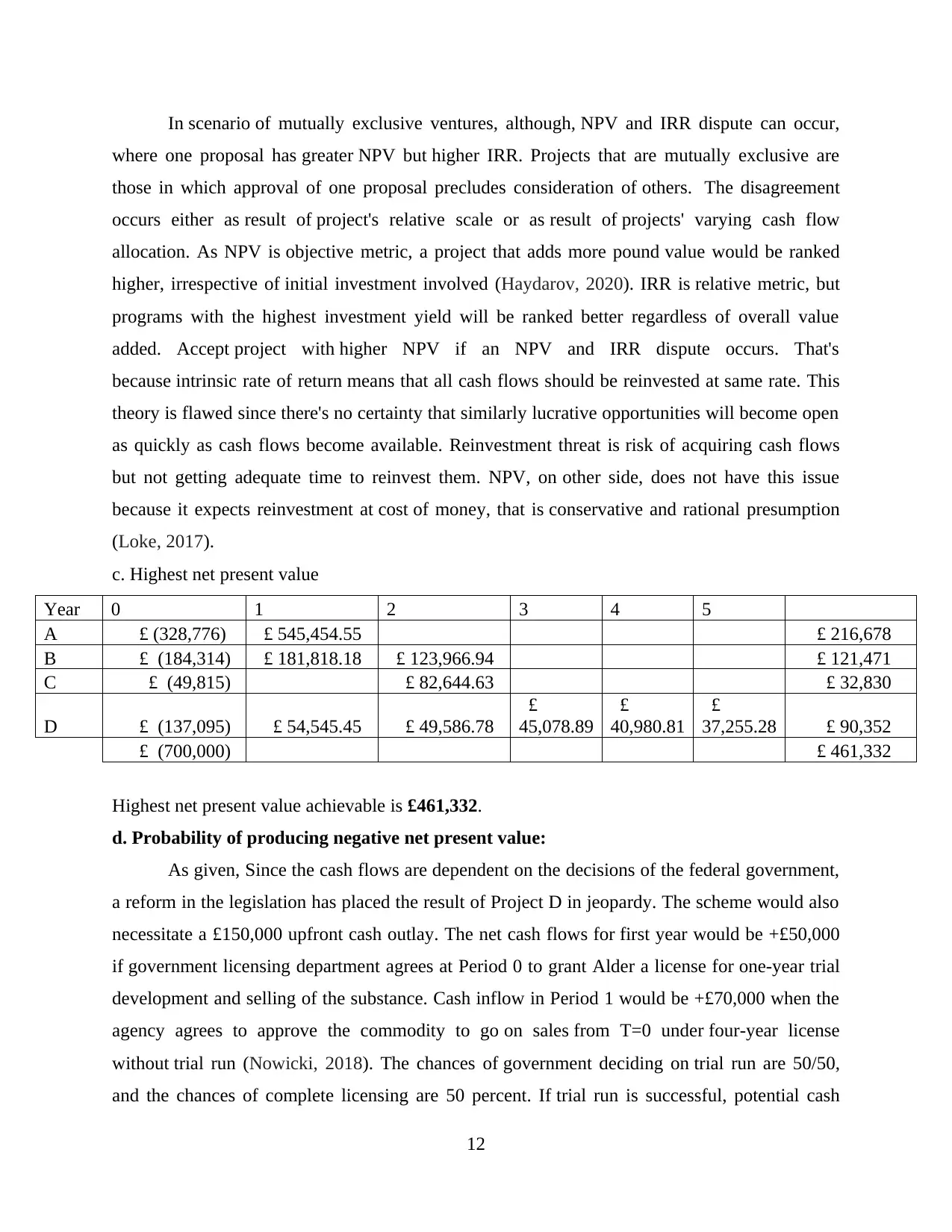

c. Highest net present value

Year 0 1 2 3 4 5

A £ (328,776) £ 545,454.55 £ 216,678

B £ (184,314) £ 181,818.18 £ 123,966.94 £ 121,471

C £ (49,815) £ 82,644.63 £ 32,830

D £ (137,095) £ 54,545.45 £ 49,586.78

£

45,078.89

£

40,980.81

£

37,255.28 £ 90,352

£ (700,000) £ 461,332

Highest net present value achievable is £461,332.

d. Probability of producing negative net present value:

As given, Since the cash flows are dependent on the decisions of the federal government,

a reform in the legislation has placed the result of Project D in jeopardy. The scheme would also

necessitate a £150,000 upfront cash outlay. The net cash flows for first year would be +£50,000

if government licensing department agrees at Period 0 to grant Alder a license for one-year trial

development and selling of the substance. Cash inflow in Period 1 would be +£70,000 when the

agency agrees to approve the commodity to go on sales from T=0 under four-year license

without trial run (Nowicki, 2018). The chances of government deciding on trial run are 50/50,

and the chances of complete licensing are 50 percent. If trial run is successful, potential cash

12

where one proposal has greater NPV but higher IRR. Projects that are mutually exclusive are

those in which approval of one proposal precludes consideration of others. The disagreement

occurs either as result of project's relative scale or as result of projects' varying cash flow

allocation. As NPV is objective metric, a project that adds more pound value would be ranked

higher, irrespective of initial investment involved (Haydarov, 2020). IRR is relative metric, but

programs with the highest investment yield will be ranked better regardless of overall value

added. Accept project with higher NPV if an NPV and IRR dispute occurs. That's

because intrinsic rate of return means that all cash flows should be reinvested at same rate. This

theory is flawed since there's no certainty that similarly lucrative opportunities will become open

as quickly as cash flows become available. Reinvestment threat is risk of acquiring cash flows

but not getting adequate time to reinvest them. NPV, on other side, does not have this issue

because it expects reinvestment at cost of money, that is conservative and rational presumption

(Loke, 2017).

c. Highest net present value

Year 0 1 2 3 4 5

A £ (328,776) £ 545,454.55 £ 216,678

B £ (184,314) £ 181,818.18 £ 123,966.94 £ 121,471

C £ (49,815) £ 82,644.63 £ 32,830

D £ (137,095) £ 54,545.45 £ 49,586.78

£

45,078.89

£

40,980.81

£

37,255.28 £ 90,352

£ (700,000) £ 461,332

Highest net present value achievable is £461,332.

d. Probability of producing negative net present value:

As given, Since the cash flows are dependent on the decisions of the federal government,

a reform in the legislation has placed the result of Project D in jeopardy. The scheme would also

necessitate a £150,000 upfront cash outlay. The net cash flows for first year would be +£50,000

if government licensing department agrees at Period 0 to grant Alder a license for one-year trial

development and selling of the substance. Cash inflow in Period 1 would be +£70,000 when the

agency agrees to approve the commodity to go on sales from T=0 under four-year license

without trial run (Nowicki, 2018). The chances of government deciding on trial run are 50/50,

and the chances of complete licensing are 50 percent. If trial run is successful, potential cash

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16