International Financial Management: Analysis of Exchange Rates

VerifiedAdded on 2021/11/11

|20

|4488

|61

Homework Assignment

AI Summary

This homework assignment in International Financial Management addresses key concepts such as exchange rate calculations, including the impact of changes in the value of the US dollar, and the calculation of cross-currency rates. It explores the purchasing power parity (PPP) theory, analyzing ...

Running head: INTERNATIONAL FINANCIAL MANAGEMENT

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTERNATIONAL FINANCIAL MANAGEMENT

Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................3

Answer 3:.........................................................................................................................................8

Answer 4:.......................................................................................................................................10

Answer 5:.......................................................................................................................................10

Answer 6:.......................................................................................................................................18

References:....................................................................................................................................22

INTERNATIONAL FINANCIAL MANAGEMENT

Contents

Answer 1:.........................................................................................................................................2

Answer 2:.........................................................................................................................................3

Answer 3:.........................................................................................................................................8

Answer 4:.......................................................................................................................................10

Answer 5:.......................................................................................................................................10

Answer 6:.......................................................................................................................................18

References:....................................................................................................................................22

2

INTERNATIONAL FINANCIAL MANAGEMENT

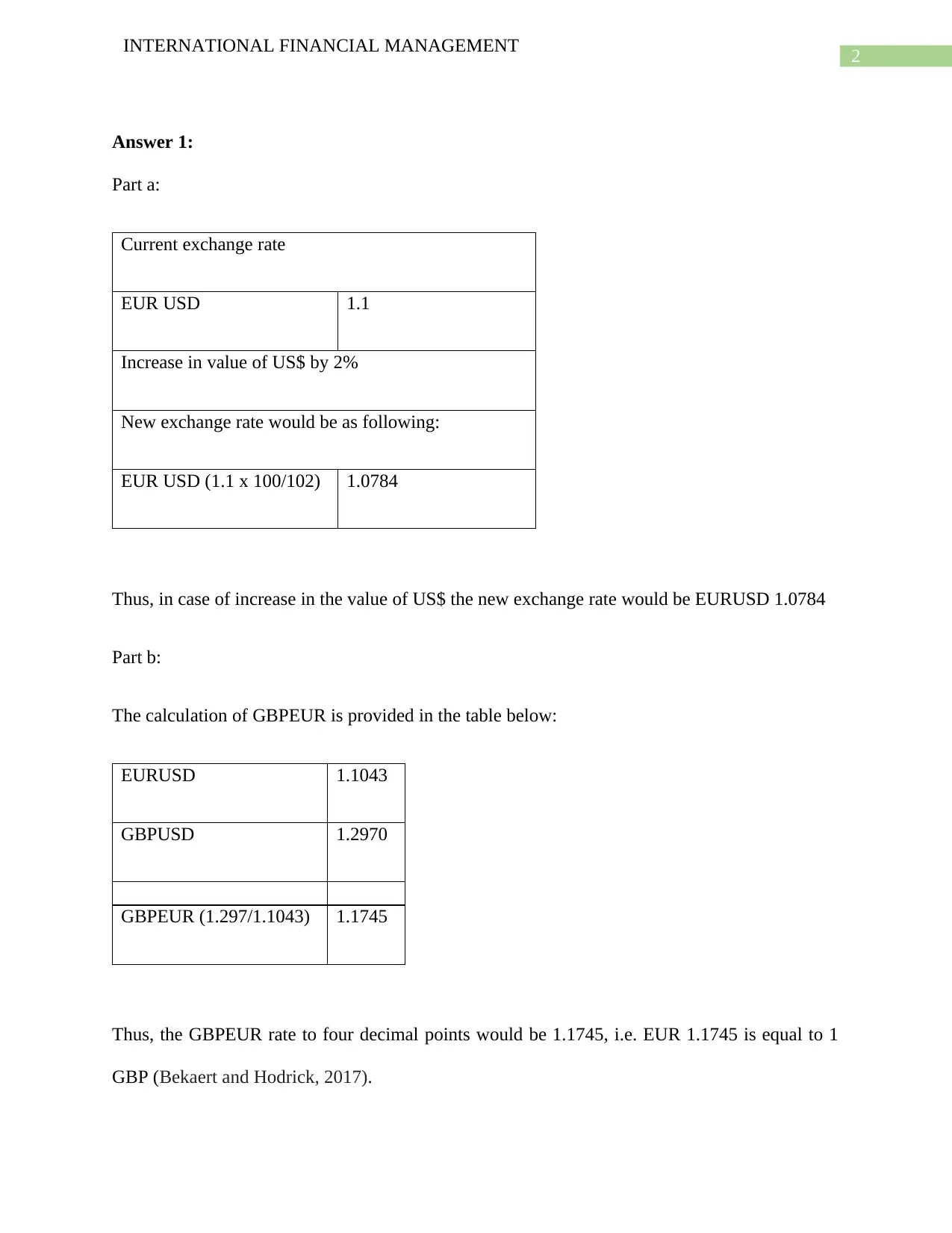

Answer 1:

Part a:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

Thus, in case of increase in the value of US$ the new exchange rate would be EURUSD 1.0784

Part b:

The calculation of GBPEUR is provided in the table below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

Thus, the GBPEUR rate to four decimal points would be 1.1745, i.e. EUR 1.1745 is equal to 1

GBP (Bekaert and Hodrick, 2017).

INTERNATIONAL FINANCIAL MANAGEMENT

Answer 1:

Part a:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

Thus, in case of increase in the value of US$ the new exchange rate would be EURUSD 1.0784

Part b:

The calculation of GBPEUR is provided in the table below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

Thus, the GBPEUR rate to four decimal points would be 1.1745, i.e. EUR 1.1745 is equal to 1

GBP (Bekaert and Hodrick, 2017).

You're viewing a preview

Unlock full access by subscribing today!

3

INTERNATIONAL FINANCIAL MANAGEMENT

Part c:

The exchange rate of GBPEUR is calculated above on the basis of the information provided

about the exchange rate between EURUSD and GBPUSD. Since no direct exchange rate is

provide for GBPEUR thus, the value of GBP with respect to US$ has been taken into

consideration along with the value of US$ in respect to EUR. Accordingly, by comparing the

value US$ against EUR and the value US$ against GBP the exchange rate of GBREUR has been

calculated. This is a very popular technique used by financial experts to calculate the exchange

rate between two currencies when the direct exchange rate between the two currencies are not

available. In this case the exchange rates between US$ and GBP as well as EUR and US$ are

available. However, the exchange rate between GBP and EUR is not available thus, by

comparing the value of US$ against GBP and against EUR the exchange rate of GBPEUR has

been calculated here (Titman and Martin, 2014).

An opportunity to make profit from the arbitration of different currencies due to the fluctuation

in three different currencies called triangular arbitrage. In this case the value of US$ to EUR and

US$ to GBP can be used to earn profit from triangular arbitrage. For example by investing US$

to purchase EUR at present and then to receive GBP in exchange EUR in the future when it will

result in maximum amount of gain to the investor will be called a triangular arbitrage. Proper

understanding about exchange rate differences and ability to forecast the possible fluctuations in

different currencies provide the investors significant opportunities to make profit from arbitration

(Deresky, 2017).

Answer 2:

Part a:

INTERNATIONAL FINANCIAL MANAGEMENT

Part c:

The exchange rate of GBPEUR is calculated above on the basis of the information provided

about the exchange rate between EURUSD and GBPUSD. Since no direct exchange rate is

provide for GBPEUR thus, the value of GBP with respect to US$ has been taken into

consideration along with the value of US$ in respect to EUR. Accordingly, by comparing the

value US$ against EUR and the value US$ against GBP the exchange rate of GBREUR has been

calculated. This is a very popular technique used by financial experts to calculate the exchange

rate between two currencies when the direct exchange rate between the two currencies are not

available. In this case the exchange rates between US$ and GBP as well as EUR and US$ are

available. However, the exchange rate between GBP and EUR is not available thus, by

comparing the value of US$ against GBP and against EUR the exchange rate of GBPEUR has

been calculated here (Titman and Martin, 2014).

An opportunity to make profit from the arbitration of different currencies due to the fluctuation

in three different currencies called triangular arbitrage. In this case the value of US$ to EUR and

US$ to GBP can be used to earn profit from triangular arbitrage. For example by investing US$

to purchase EUR at present and then to receive GBP in exchange EUR in the future when it will

result in maximum amount of gain to the investor will be called a triangular arbitrage. Proper

understanding about exchange rate differences and ability to forecast the possible fluctuations in

different currencies provide the investors significant opportunities to make profit from arbitration

(Deresky, 2017).

Answer 2:

Part a:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTERNATIONAL FINANCIAL MANAGEMENT

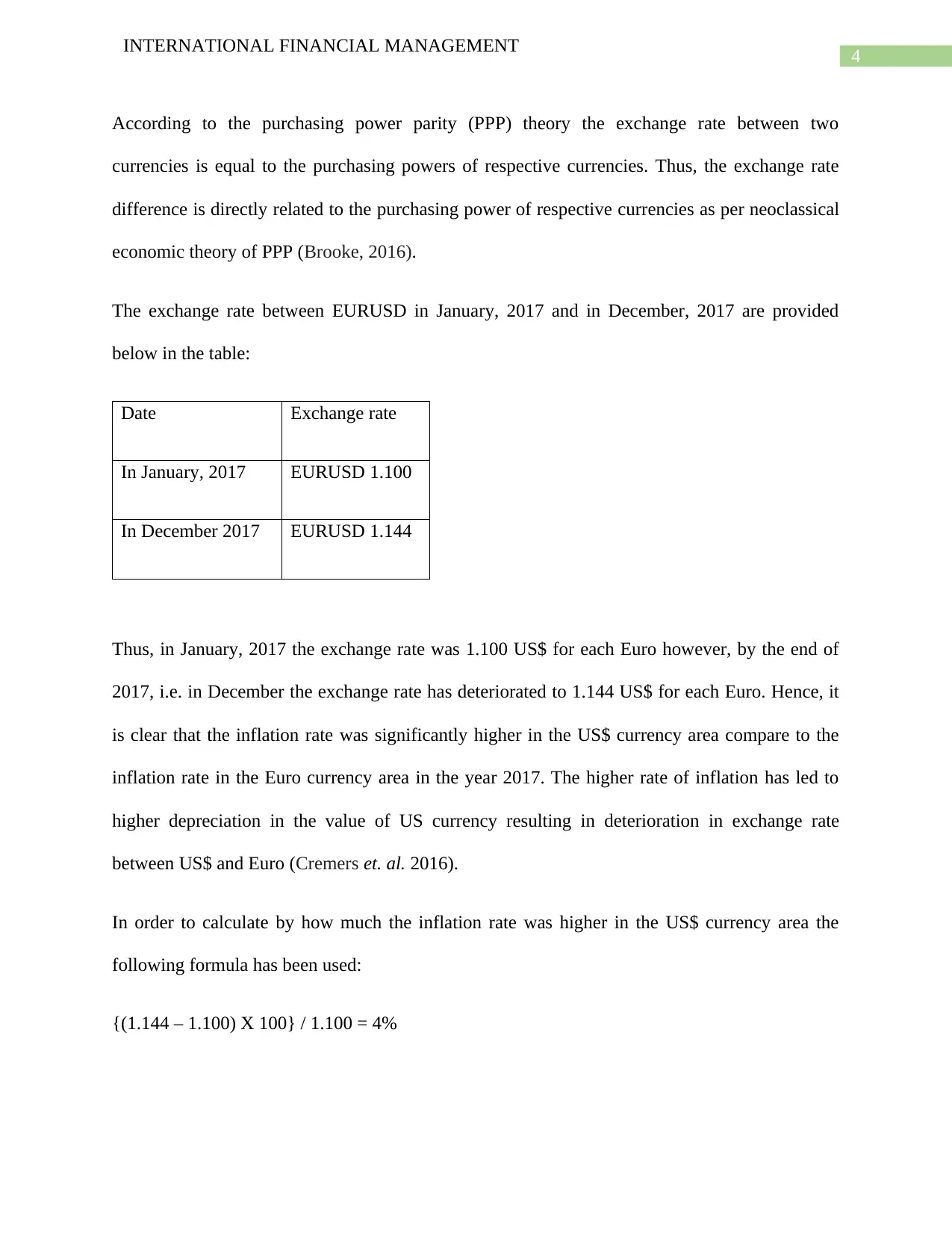

According to the purchasing power parity (PPP) theory the exchange rate between two

currencies is equal to the purchasing powers of respective currencies. Thus, the exchange rate

difference is directly related to the purchasing power of respective currencies as per neoclassical

economic theory of PPP (Brooke, 2016).

The exchange rate between EURUSD in January, 2017 and in December, 2017 are provided

below in the table:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

Thus, in January, 2017 the exchange rate was 1.100 US$ for each Euro however, by the end of

2017, i.e. in December the exchange rate has deteriorated to 1.144 US$ for each Euro. Hence, it

is clear that the inflation rate was significantly higher in the US$ currency area compare to the

inflation rate in the Euro currency area in the year 2017. The higher rate of inflation has led to

higher depreciation in the value of US currency resulting in deterioration in exchange rate

between US$ and Euro (Cremers et. al. 2016).

In order to calculate by how much the inflation rate was higher in the US$ currency area the

following formula has been used:

{(1.144 – 1.100) X 100} / 1.100 = 4%

INTERNATIONAL FINANCIAL MANAGEMENT

According to the purchasing power parity (PPP) theory the exchange rate between two

currencies is equal to the purchasing powers of respective currencies. Thus, the exchange rate

difference is directly related to the purchasing power of respective currencies as per neoclassical

economic theory of PPP (Brooke, 2016).

The exchange rate between EURUSD in January, 2017 and in December, 2017 are provided

below in the table:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

Thus, in January, 2017 the exchange rate was 1.100 US$ for each Euro however, by the end of

2017, i.e. in December the exchange rate has deteriorated to 1.144 US$ for each Euro. Hence, it

is clear that the inflation rate was significantly higher in the US$ currency area compare to the

inflation rate in the Euro currency area in the year 2017. The higher rate of inflation has led to

higher depreciation in the value of US currency resulting in deterioration in exchange rate

between US$ and Euro (Cremers et. al. 2016).

In order to calculate by how much the inflation rate was higher in the US$ currency area the

following formula has been used:

{(1.144 – 1.100) X 100} / 1.100 = 4%

5

INTERNATIONAL FINANCIAL MANAGEMENT

Thus, the inflation rate in US$ currency area was higher by 4% compared to the inflation rate in

the Euro currency area.

Part b:

In case the inflation rate in the US$ currency area was 3% higher than the inflation rate in the

Euro currency area then the US currency shall be depreciated at 3% higher rate than the rate of

depreciation of Euro. The exchange rate between the US$ and Euro will be as following.

Assuming that the exchange rate of EURUSD 1.100 was in January 2017 then with the rate of

inflation in US$ currency area 3% higher than the inflation rate in Euro currency area the

exchange rate at the end of 2017 would be as following:

EURUSD (1.100 / 1 x 97%) =1.1340

Thus, as a result of increased inflation rate in US$ area the value of US$ will reduce against the

Euro. Thus, the exchange rate of EURUSD will deteriorate to 1.1340 by the end of 2017 (Davies,

Kat and Lu, 2016).

Part c:

There are number of implications of changes in real exchange rate of a currency. A brief

discussion about the implications of changes in real exchange rate of a currency is provided in

this document with the objective of imparting significant knowledge about the topic (Klein and

Li, 2015).

Following are the broad implications of changes in real exchange rate of a currency macro-

economic factors in a country:

INTERNATIONAL FINANCIAL MANAGEMENT

Thus, the inflation rate in US$ currency area was higher by 4% compared to the inflation rate in

the Euro currency area.

Part b:

In case the inflation rate in the US$ currency area was 3% higher than the inflation rate in the

Euro currency area then the US currency shall be depreciated at 3% higher rate than the rate of

depreciation of Euro. The exchange rate between the US$ and Euro will be as following.

Assuming that the exchange rate of EURUSD 1.100 was in January 2017 then with the rate of

inflation in US$ currency area 3% higher than the inflation rate in Euro currency area the

exchange rate at the end of 2017 would be as following:

EURUSD (1.100 / 1 x 97%) =1.1340

Thus, as a result of increased inflation rate in US$ area the value of US$ will reduce against the

Euro. Thus, the exchange rate of EURUSD will deteriorate to 1.1340 by the end of 2017 (Davies,

Kat and Lu, 2016).

Part c:

There are number of implications of changes in real exchange rate of a currency. A brief

discussion about the implications of changes in real exchange rate of a currency is provided in

this document with the objective of imparting significant knowledge about the topic (Klein and

Li, 2015).

Following are the broad implications of changes in real exchange rate of a currency macro-

economic factors in a country:

You're viewing a preview

Unlock full access by subscribing today!

6

INTERNATIONAL FINANCIAL MANAGEMENT

The prices of imported goods and services: The prices of imported goods and services changes

due to the change in exchange rate of a currency. The changes will be adverse to the specific

country in case the exchange rate is deteriorated from earlier. However, the change in prices of

goods and services will be positive if the exchange rate improves. Thus appreciation in exchange

rate will decrease the price of imported goods and services. In contrast the prices of imported

goods and services will increase significantly with the depreciation in exchange rate (Agarwal,

Ruenzi and Weigert, 2017).

Changes in commodity prices: The commodity prices will be affected depending on the currency

in which the commodities are prices. For example the commodities which are priced in US$ in

the United Kingdom will increase with depreciation in the value of Pound sterling. Appreciation

in the value of pound sterling on the other hand will decrease the prices of such commodities

(Yin, 2016).

Impact on export growth: The growth of export would be significantly affected to subsequent to

the changes in real exchange rate of a currency. For example higher exchange rate will make it

very hard and difficult for a country to sale its products in foreign market. Thus, the export

growth would be adversely affected if the exchange rate is higher (Grundy and Verwijmeren,

2018).

Impact on unemployment: Exchange rate also affects the unemployment rate in a country. An

appreciation in exchange rate often results in slowdown of exports as a result the demand in the

economy is reduced. This leads to cutting down of production which in turn increased

unemployment. Thus, unemployment rate is also affected with the changes in real exchange rate

of a currency.

INTERNATIONAL FINANCIAL MANAGEMENT

The prices of imported goods and services: The prices of imported goods and services changes

due to the change in exchange rate of a currency. The changes will be adverse to the specific

country in case the exchange rate is deteriorated from earlier. However, the change in prices of

goods and services will be positive if the exchange rate improves. Thus appreciation in exchange

rate will decrease the price of imported goods and services. In contrast the prices of imported

goods and services will increase significantly with the depreciation in exchange rate (Agarwal,

Ruenzi and Weigert, 2017).

Changes in commodity prices: The commodity prices will be affected depending on the currency

in which the commodities are prices. For example the commodities which are priced in US$ in

the United Kingdom will increase with depreciation in the value of Pound sterling. Appreciation

in the value of pound sterling on the other hand will decrease the prices of such commodities

(Yin, 2016).

Impact on export growth: The growth of export would be significantly affected to subsequent to

the changes in real exchange rate of a currency. For example higher exchange rate will make it

very hard and difficult for a country to sale its products in foreign market. Thus, the export

growth would be adversely affected if the exchange rate is higher (Grundy and Verwijmeren,

2018).

Impact on unemployment: Exchange rate also affects the unemployment rate in a country. An

appreciation in exchange rate often results in slowdown of exports as a result the demand in the

economy is reduced. This leads to cutting down of production which in turn increased

unemployment. Thus, unemployment rate is also affected with the changes in real exchange rate

of a currency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTERNATIONAL FINANCIAL MANAGEMENT

Stimulation of demand: A weaker currency and subsequent fall in exchange rate of the currency

can be used to stimulate demand within the economy. As a result the production would increase

within the economy leading to improvement in employment rate (Kokkonen and Suominen,

2015).

Thus, there are number of implications of real changes in exchange rate of a currency as can be

understood from the above discussion.

Part d:

As per the document the exchange rate of EURUSD in January 2017 and December 2017 is as

following:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

Thus, it has already been established in earlier part that higher depreciation in the US currency

has resulted in deterioration of exchange rate of EURUSD. The inflation rate in the US$ area is

higher than the Euro area. As per the calculation (provided in part (a) of this question) the

inflation rate is 4% higher in US$ area as compared to the rate of inflation in Euro. Thus, it is

clear that the demand for the money market in the US is much higher than the supply. Thus, it is

obvious that the interest rate in the US is higher than that in Euro area (Chance and Brooks,

2015).

INTERNATIONAL FINANCIAL MANAGEMENT

Stimulation of demand: A weaker currency and subsequent fall in exchange rate of the currency

can be used to stimulate demand within the economy. As a result the production would increase

within the economy leading to improvement in employment rate (Kokkonen and Suominen,

2015).

Thus, there are number of implications of real changes in exchange rate of a currency as can be

understood from the above discussion.

Part d:

As per the document the exchange rate of EURUSD in January 2017 and December 2017 is as

following:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

Thus, it has already been established in earlier part that higher depreciation in the US currency

has resulted in deterioration of exchange rate of EURUSD. The inflation rate in the US$ area is

higher than the Euro area. As per the calculation (provided in part (a) of this question) the

inflation rate is 4% higher in US$ area as compared to the rate of inflation in Euro. Thus, it is

clear that the demand for the money market in the US is much higher than the supply. Thus, it is

obvious that the interest rate in the US is higher than that in Euro area (Chance and Brooks,

2015).

8

INTERNATIONAL FINANCIAL MANAGEMENT

Part e:

The government bonds are risk free securities on which stable rate of interests are provided to the

investors over a fixed period of time without any fluctuation. The investors are certain to receive

a fixed amount of interest on the amount of investment over a period of time and receive the

principal amount after the end of tenure of the bond. Since, these are risk free investments hence,

there is generally no difference in the interest rates of government bonds of any two countries. In

this case the interest rates of government bonds two countries in Euro area will not be different

as both are risk free investments providing stable and fixed rate interests to the investors without

any risk (McNeil, Frey and Embrechts, 2015).

In practice, the difference is due to the difference in inflation rate and changes in exchange rate

between the two currencies. In this case compared to the exchange rate of EURUSD 1.100 in

January, 2017 the exchange rate has depreciated to EURUSD 1.144 by the end of 2017. Thus,

the changes in exchange rate will obviously influence the value of two currencies which in turn

will impact the risk free interest rates in two countries. The risk free rate of interests are nothing

but the interest rates provided by the Governments of two countries on government bonds.

Hence, in practice there is the difference between the government bond interest rates which are

considered to determine the cost of capital in countries which can also be taken as the rate of

inflation (Kelly, Lustig and Van Nieuwerburgh, 2016).

Part B:

Answer 3:

The uncertainty is the most critical aspect in an economy and its environment. This is what

makes it challenging for the administration of a country to manage the different elements of an

INTERNATIONAL FINANCIAL MANAGEMENT

Part e:

The government bonds are risk free securities on which stable rate of interests are provided to the

investors over a fixed period of time without any fluctuation. The investors are certain to receive

a fixed amount of interest on the amount of investment over a period of time and receive the

principal amount after the end of tenure of the bond. Since, these are risk free investments hence,

there is generally no difference in the interest rates of government bonds of any two countries. In

this case the interest rates of government bonds two countries in Euro area will not be different

as both are risk free investments providing stable and fixed rate interests to the investors without

any risk (McNeil, Frey and Embrechts, 2015).

In practice, the difference is due to the difference in inflation rate and changes in exchange rate

between the two currencies. In this case compared to the exchange rate of EURUSD 1.100 in

January, 2017 the exchange rate has depreciated to EURUSD 1.144 by the end of 2017. Thus,

the changes in exchange rate will obviously influence the value of two currencies which in turn

will impact the risk free interest rates in two countries. The risk free rate of interests are nothing

but the interest rates provided by the Governments of two countries on government bonds.

Hence, in practice there is the difference between the government bond interest rates which are

considered to determine the cost of capital in countries which can also be taken as the rate of

inflation (Kelly, Lustig and Van Nieuwerburgh, 2016).

Part B:

Answer 3:

The uncertainty is the most critical aspect in an economy and its environment. This is what

makes it challenging for the administration of a country to manage the different elements of an

You're viewing a preview

Unlock full access by subscribing today!

9

INTERNATIONAL FINANCIAL MANAGEMENT

economy. It is impossible to eliminate uncertainty from economic and business environment but

by planning properly the uncertainties in the environment can be managed effectively. For

international trade and business operations it is important to evaluate the country risks to take

appropriate steps to minimize the risk of uncertainties. Exchange rate volatility is one of the most

important elements of overall country risk in international trade as well as international finance.

It is important to understand the impact of exchange rate volatility on the economy of a country

to take appropriate steps to minimize the adverse effects of negative on the economy of a country

(Kim et. al. 2016).

Exchange rate volatility is the fluctuation in exchange rate that affects number of macro-

economic factors in a country. Fluctuation in exchange rate have huge implication on the overall

progress and development of an economy. The changes in exchange rate between the domestic

currency and other currencies will have significant impact on the economy. The appreciation in

exchange rate will reduce the cost of imported goods and services which will improve the

balance of payment. The foreign currency reserve will be increased subsequent to the

appreciation in exchange rate. The commodities denominated in foreign currencies will be

cheaper in the country thus, the demand for such products will be higher in the economy (Carr

and Wu, 2016). There is down side to the appreciation in exchange rate also and it is the fact that

the appreciation in exchange rate often leads to reduction in exports of a country as the prices of

goods increased. As a result the demand for the goods in the international market declines

leading production cuts. The production cuts in the country will adversely impact the

unemployment rate in the country as jobs will be cut with reduction in production. However,

stable exchange rate allows a country to balance its economic growth and progress by taking

necessary decisions in right direction. Exchange rate volatility on the other hand does not allow a

INTERNATIONAL FINANCIAL MANAGEMENT

economy. It is impossible to eliminate uncertainty from economic and business environment but

by planning properly the uncertainties in the environment can be managed effectively. For

international trade and business operations it is important to evaluate the country risks to take

appropriate steps to minimize the risk of uncertainties. Exchange rate volatility is one of the most

important elements of overall country risk in international trade as well as international finance.

It is important to understand the impact of exchange rate volatility on the economy of a country

to take appropriate steps to minimize the adverse effects of negative on the economy of a country

(Kim et. al. 2016).

Exchange rate volatility is the fluctuation in exchange rate that affects number of macro-

economic factors in a country. Fluctuation in exchange rate have huge implication on the overall

progress and development of an economy. The changes in exchange rate between the domestic

currency and other currencies will have significant impact on the economy. The appreciation in

exchange rate will reduce the cost of imported goods and services which will improve the

balance of payment. The foreign currency reserve will be increased subsequent to the

appreciation in exchange rate. The commodities denominated in foreign currencies will be

cheaper in the country thus, the demand for such products will be higher in the economy (Carr

and Wu, 2016). There is down side to the appreciation in exchange rate also and it is the fact that

the appreciation in exchange rate often leads to reduction in exports of a country as the prices of

goods increased. As a result the demand for the goods in the international market declines

leading production cuts. The production cuts in the country will adversely impact the

unemployment rate in the country as jobs will be cut with reduction in production. However,

stable exchange rate allows a country to balance its economic growth and progress by taking

necessary decisions in right direction. Exchange rate volatility on the other hand does not allow a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTERNATIONAL FINANCIAL MANAGEMENT

country that opportunity to formulate an effective strategy and implement it to move in the right

direction towards economic development and prosperity (Christoffersen et. al. 2017).

Answer 4:

Globalization has allowed companies from different countries to establish their operating units in

other countries. As a result the term “multi-national companies” has been coined to identify the

companies and entities which are operating in more than one countries. Multi-national

companies (MNCs).

Answer 5:

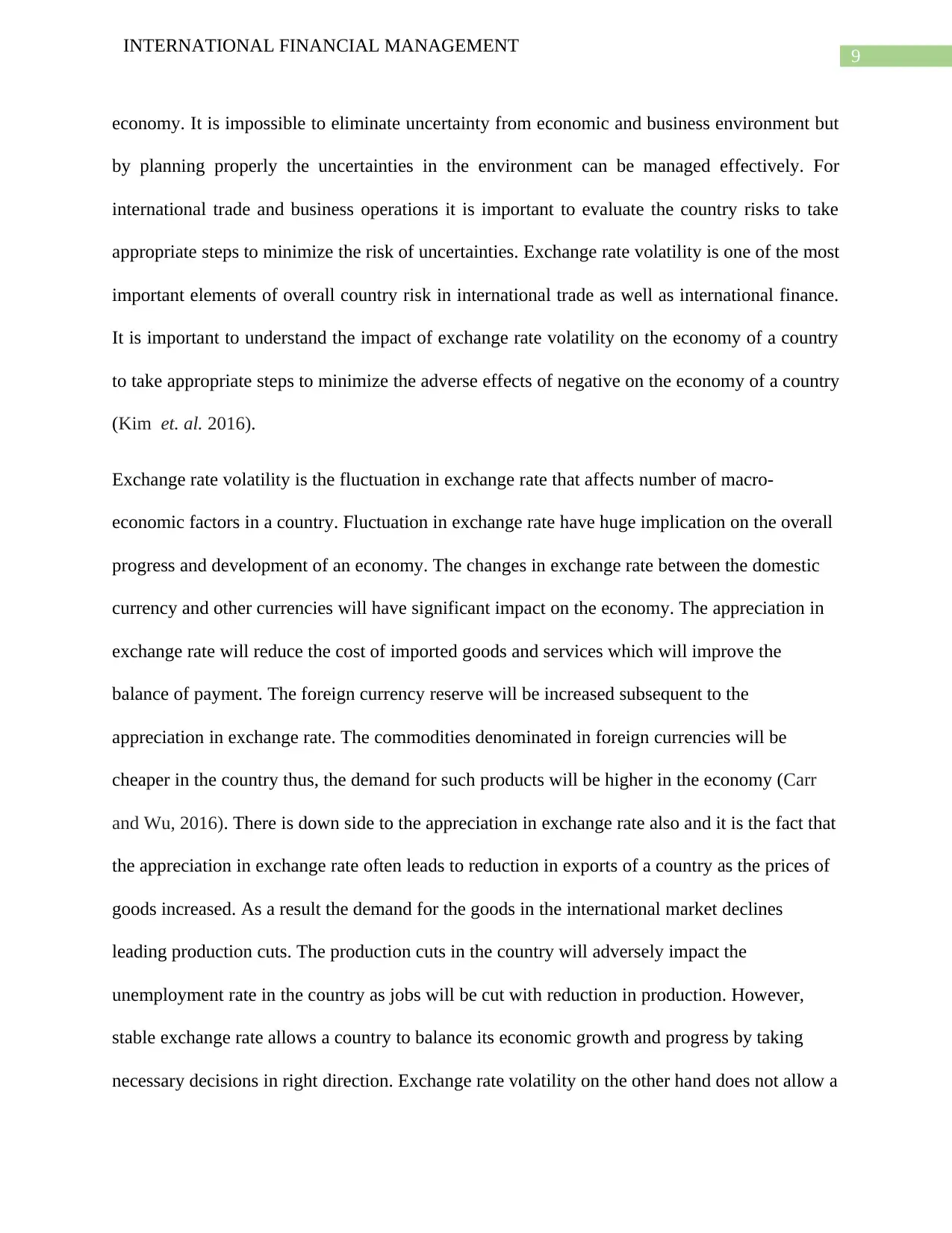

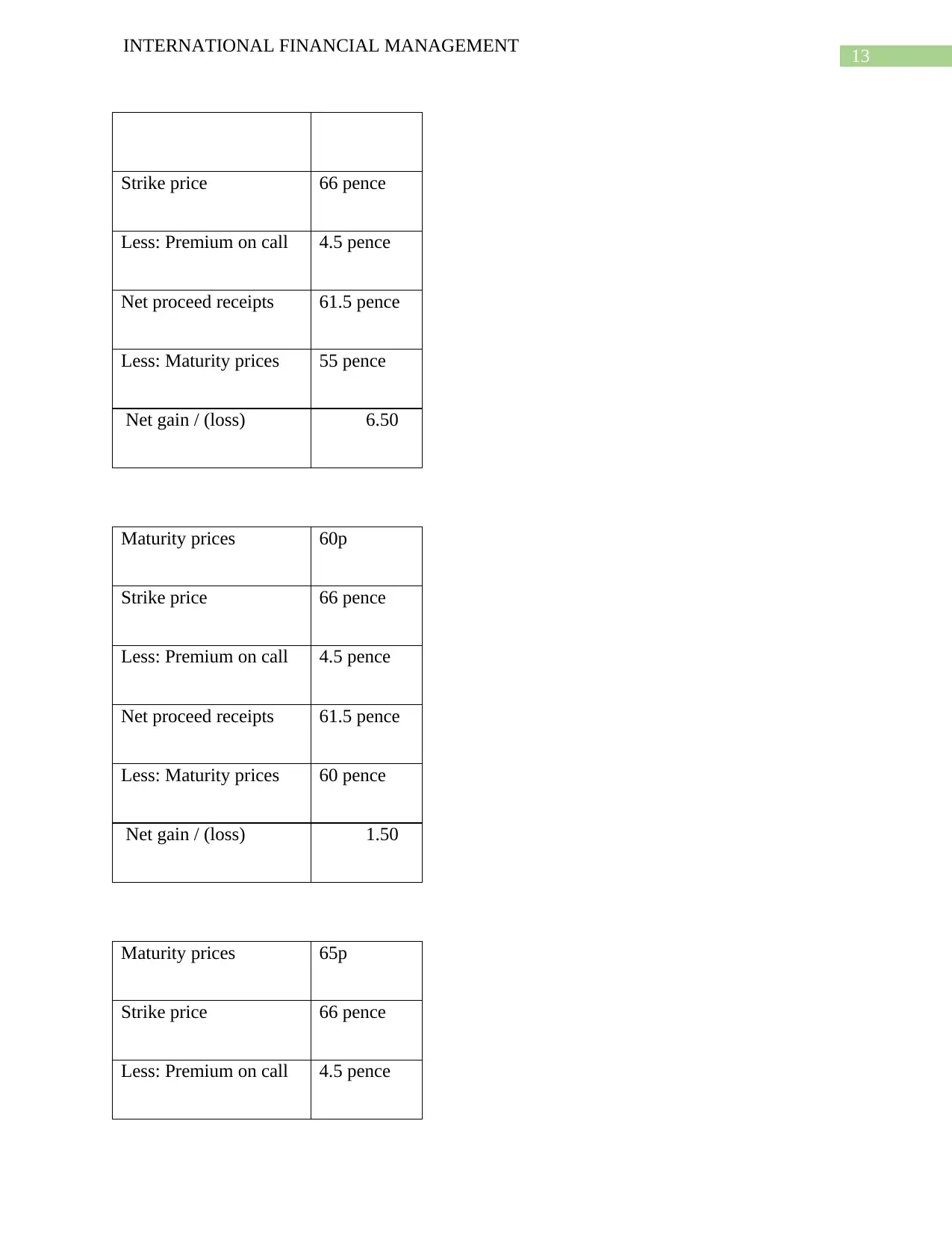

Part a:

Maturity prices 55p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 55 pence

Net loss 16.50 pence

Maturity prices 60p

Strike price 67

INTERNATIONAL FINANCIAL MANAGEMENT

country that opportunity to formulate an effective strategy and implement it to move in the right

direction towards economic development and prosperity (Christoffersen et. al. 2017).

Answer 4:

Globalization has allowed companies from different countries to establish their operating units in

other countries. As a result the term “multi-national companies” has been coined to identify the

companies and entities which are operating in more than one countries. Multi-national

companies (MNCs).

Answer 5:

Part a:

Maturity prices 55p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 55 pence

Net loss 16.50 pence

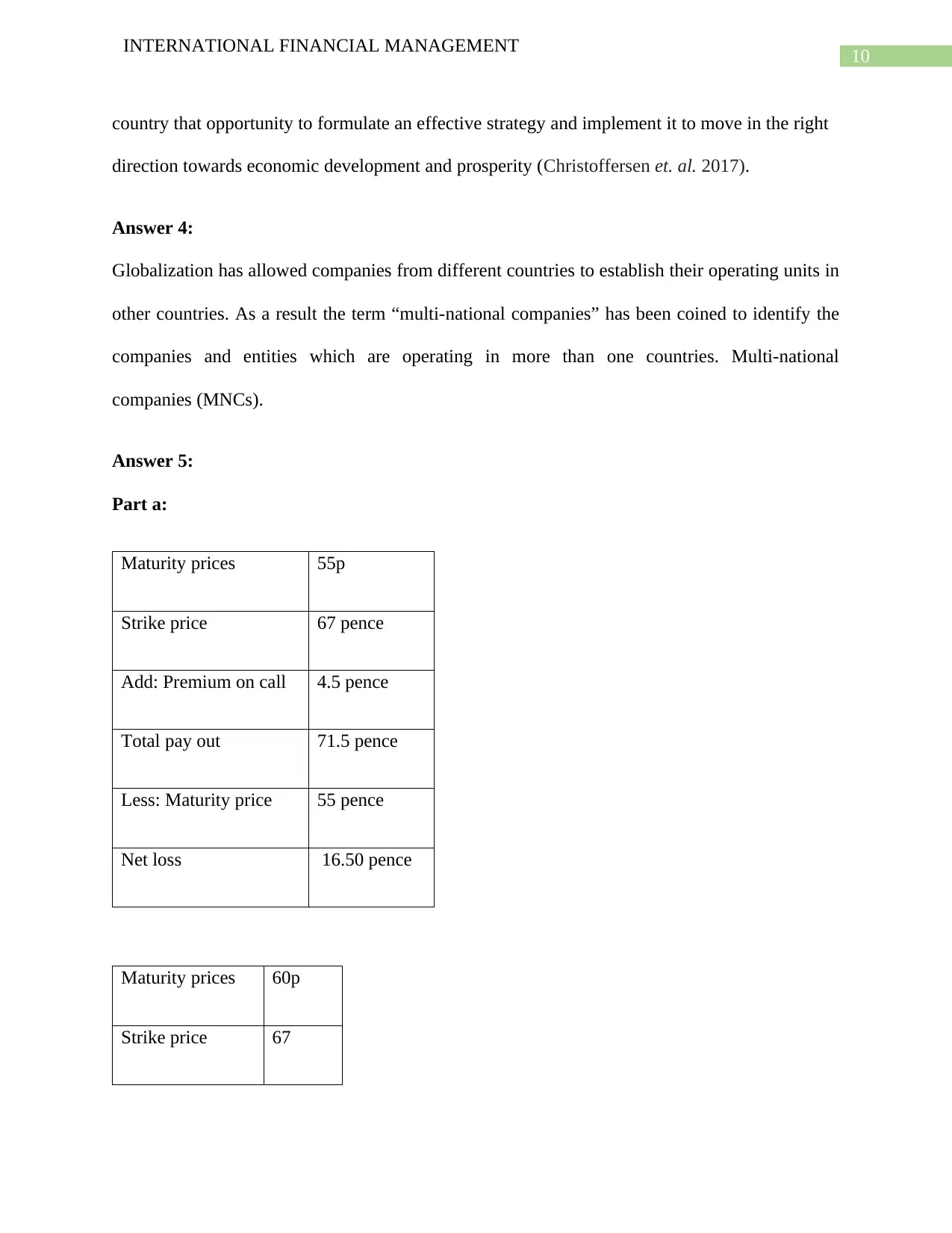

Maturity prices 60p

Strike price 67

11

INTERNATIONAL FINANCIAL MANAGEMENT

pence

Add: Premium on

call

4.5

pence

Total pay out 71.5

pence

Less: Maturity

price

60

pence

Net loss 11

.50

pence

Maturity prices 65p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 65 pence

Net loss 6.50

Pence

INTERNATIONAL FINANCIAL MANAGEMENT

pence

Add: Premium on

call

4.5

pence

Total pay out 71.5

pence

Less: Maturity

price

60

pence

Net loss 11

.50

pence

Maturity prices 65p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 65 pence

Net loss 6.50

Pence

You're viewing a preview

Unlock full access by subscribing today!

12

INTERNATIONAL FINANCIAL MANAGEMENT

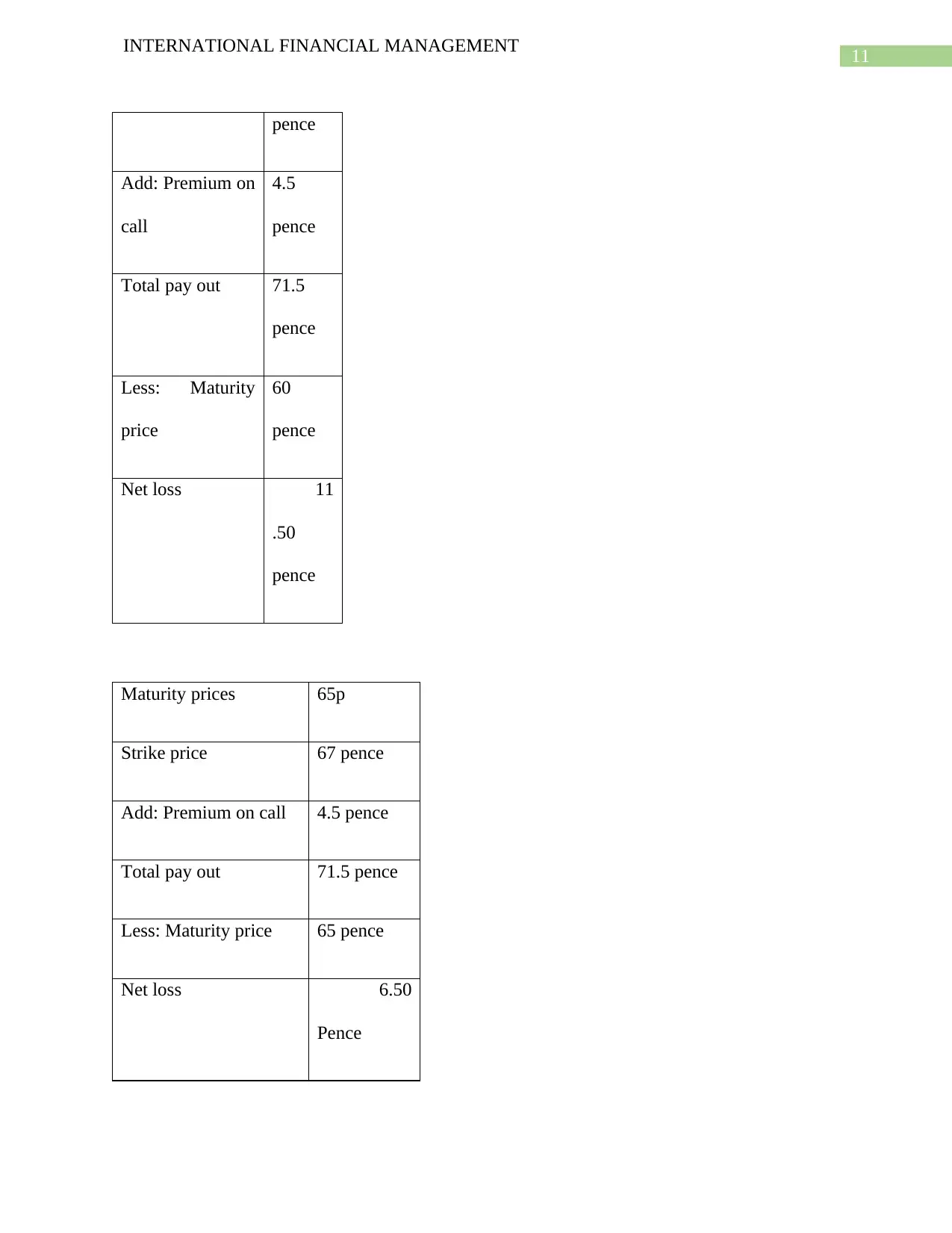

Maturity prices 70p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 70 pence

Net loss 1.50 Pence

Maturity prices 75p

Strike price 67 pence

Add: Premium on

call

4.5 pence

Total pay out 71.5 pence

Less: Maturity

price

75 pence

Net gain (3.50) pence

Part b:

Maturity prices 55p

INTERNATIONAL FINANCIAL MANAGEMENT

Maturity prices 70p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 70 pence

Net loss 1.50 Pence

Maturity prices 75p

Strike price 67 pence

Add: Premium on

call

4.5 pence

Total pay out 71.5 pence

Less: Maturity

price

75 pence

Net gain (3.50) pence

Part b:

Maturity prices 55p

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

INTERNATIONAL FINANCIAL MANAGEMENT

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 55 pence

Net gain / (loss) 6.50

Maturity prices 60p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 60 pence

Net gain / (loss) 1.50

Maturity prices 65p

Strike price 66 pence

Less: Premium on call 4.5 pence

INTERNATIONAL FINANCIAL MANAGEMENT

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 55 pence

Net gain / (loss) 6.50

Maturity prices 60p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 60 pence

Net gain / (loss) 1.50

Maturity prices 65p

Strike price 66 pence

Less: Premium on call 4.5 pence

14

INTERNATIONAL FINANCIAL MANAGEMENT

Net proceed receipts 61.5 pence

Less: Maturity prices 65 pence

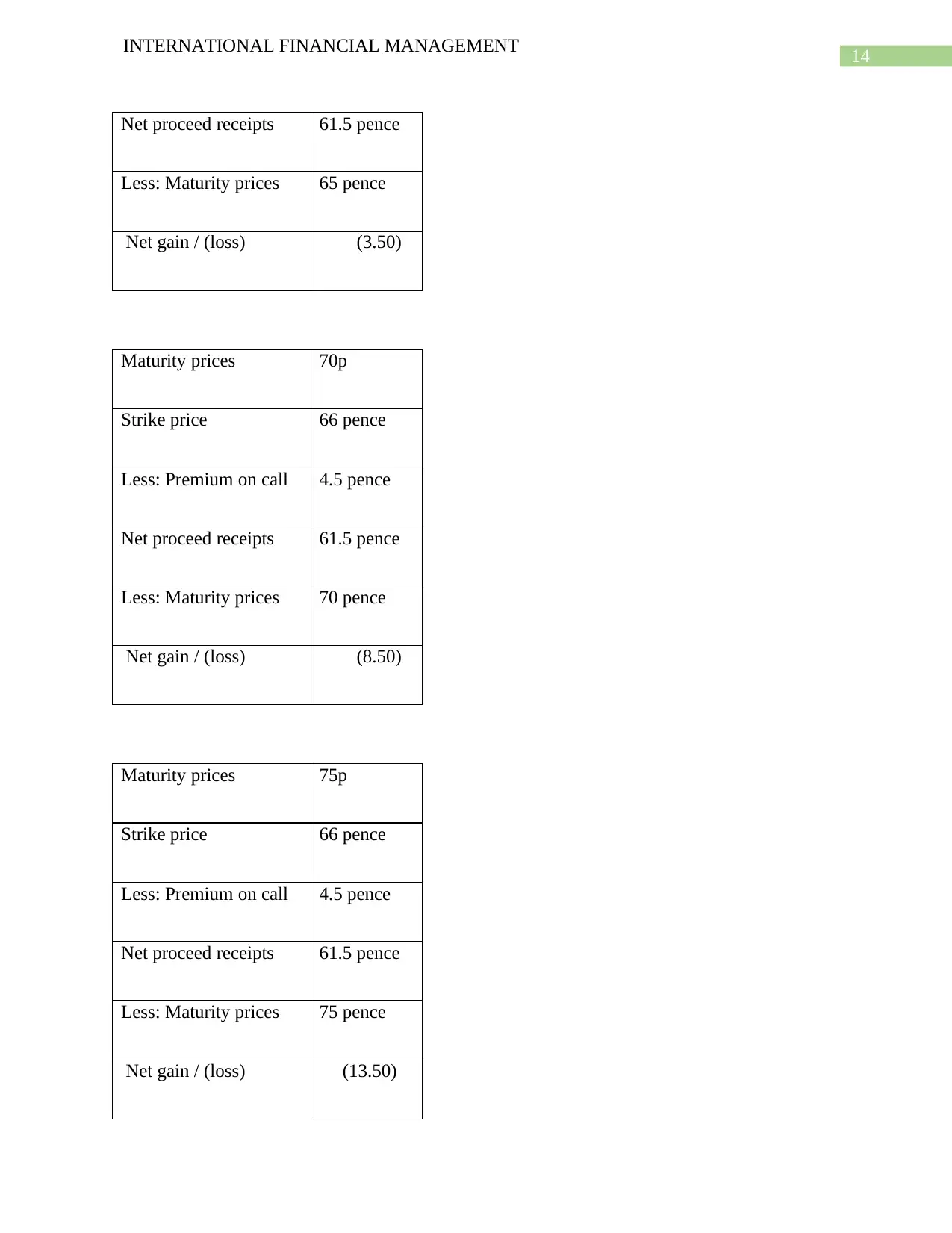

Net gain / (loss) (3.50)

Maturity prices 70p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 70 pence

Net gain / (loss) (8.50)

Maturity prices 75p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 75 pence

Net gain / (loss) (13.50)

INTERNATIONAL FINANCIAL MANAGEMENT

Net proceed receipts 61.5 pence

Less: Maturity prices 65 pence

Net gain / (loss) (3.50)

Maturity prices 70p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 70 pence

Net gain / (loss) (8.50)

Maturity prices 75p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 75 pence

Net gain / (loss) (13.50)

You're viewing a preview

Unlock full access by subscribing today!

15

INTERNATIONAL FINANCIAL MANAGEMENT

Part c:

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5

pence

71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

16.50 11.50 6.50 1.50 (3.50)

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5

pence

61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity prices 55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

INTERNATIONAL FINANCIAL MANAGEMENT

Part c:

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5

pence

71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

16.50 11.50 6.50 1.50 (3.50)

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5

pence

61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity prices 55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16

INTERNATIONAL FINANCIAL MANAGEMENT

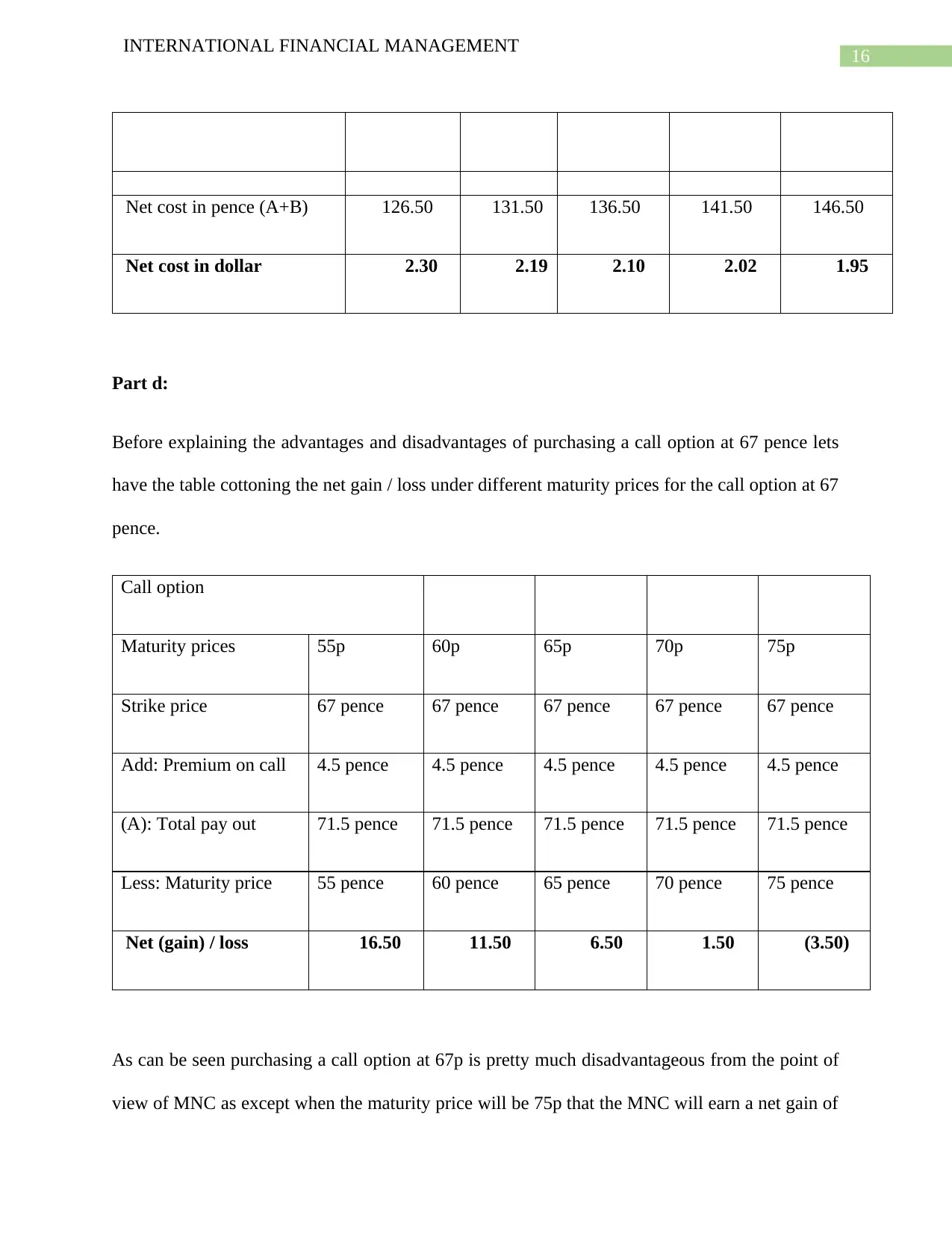

Net cost in pence (A+B) 126.50 131.50 136.50 141.50 146.50

Net cost in dollar 2.30 2.19 2.10 2.02 1.95

Part d:

Before explaining the advantages and disadvantages of purchasing a call option at 67 pence lets

have the table cottoning the net gain / loss under different maturity prices for the call option at 67

pence.

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5 pence 71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

Net (gain) / loss 16.50 11.50 6.50 1.50 (3.50)

As can be seen purchasing a call option at 67p is pretty much disadvantageous from the point of

view of MNC as except when the maturity price will be 75p that the MNC will earn a net gain of

INTERNATIONAL FINANCIAL MANAGEMENT

Net cost in pence (A+B) 126.50 131.50 136.50 141.50 146.50

Net cost in dollar 2.30 2.19 2.10 2.02 1.95

Part d:

Before explaining the advantages and disadvantages of purchasing a call option at 67 pence lets

have the table cottoning the net gain / loss under different maturity prices for the call option at 67

pence.

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5 pence 71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

Net (gain) / loss 16.50 11.50 6.50 1.50 (3.50)

As can be seen purchasing a call option at 67p is pretty much disadvantageous from the point of

view of MNC as except when the maturity price will be 75p that the MNC will earn a net gain of

17

INTERNATIONAL FINANCIAL MANAGEMENT

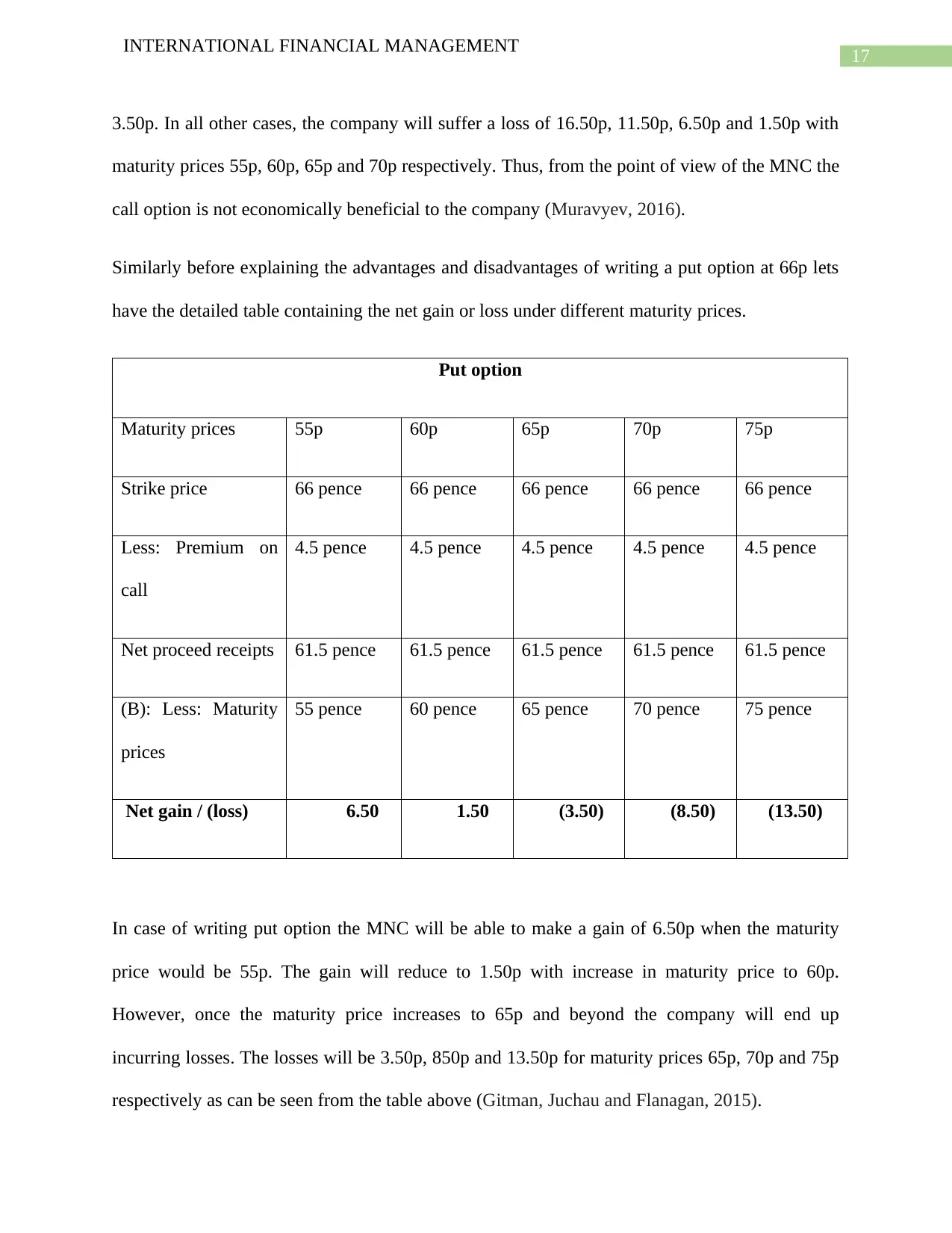

3.50p. In all other cases, the company will suffer a loss of 16.50p, 11.50p, 6.50p and 1.50p with

maturity prices 55p, 60p, 65p and 70p respectively. Thus, from the point of view of the MNC the

call option is not economically beneficial to the company (Muravyev, 2016).

Similarly before explaining the advantages and disadvantages of writing a put option at 66p lets

have the detailed table containing the net gain or loss under different maturity prices.

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on

call

4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5 pence 61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity

prices

55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

In case of writing put option the MNC will be able to make a gain of 6.50p when the maturity

price would be 55p. The gain will reduce to 1.50p with increase in maturity price to 60p.

However, once the maturity price increases to 65p and beyond the company will end up

incurring losses. The losses will be 3.50p, 850p and 13.50p for maturity prices 65p, 70p and 75p

respectively as can be seen from the table above (Gitman, Juchau and Flanagan, 2015).

INTERNATIONAL FINANCIAL MANAGEMENT

3.50p. In all other cases, the company will suffer a loss of 16.50p, 11.50p, 6.50p and 1.50p with

maturity prices 55p, 60p, 65p and 70p respectively. Thus, from the point of view of the MNC the

call option is not economically beneficial to the company (Muravyev, 2016).

Similarly before explaining the advantages and disadvantages of writing a put option at 66p lets

have the detailed table containing the net gain or loss under different maturity prices.

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on

call

4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5 pence 61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity

prices

55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

In case of writing put option the MNC will be able to make a gain of 6.50p when the maturity

price would be 55p. The gain will reduce to 1.50p with increase in maturity price to 60p.

However, once the maturity price increases to 65p and beyond the company will end up

incurring losses. The losses will be 3.50p, 850p and 13.50p for maturity prices 65p, 70p and 75p

respectively as can be seen from the table above (Gitman, Juchau and Flanagan, 2015).

You're viewing a preview

Unlock full access by subscribing today!

18

INTERNATIONAL FINANCIAL MANAGEMENT

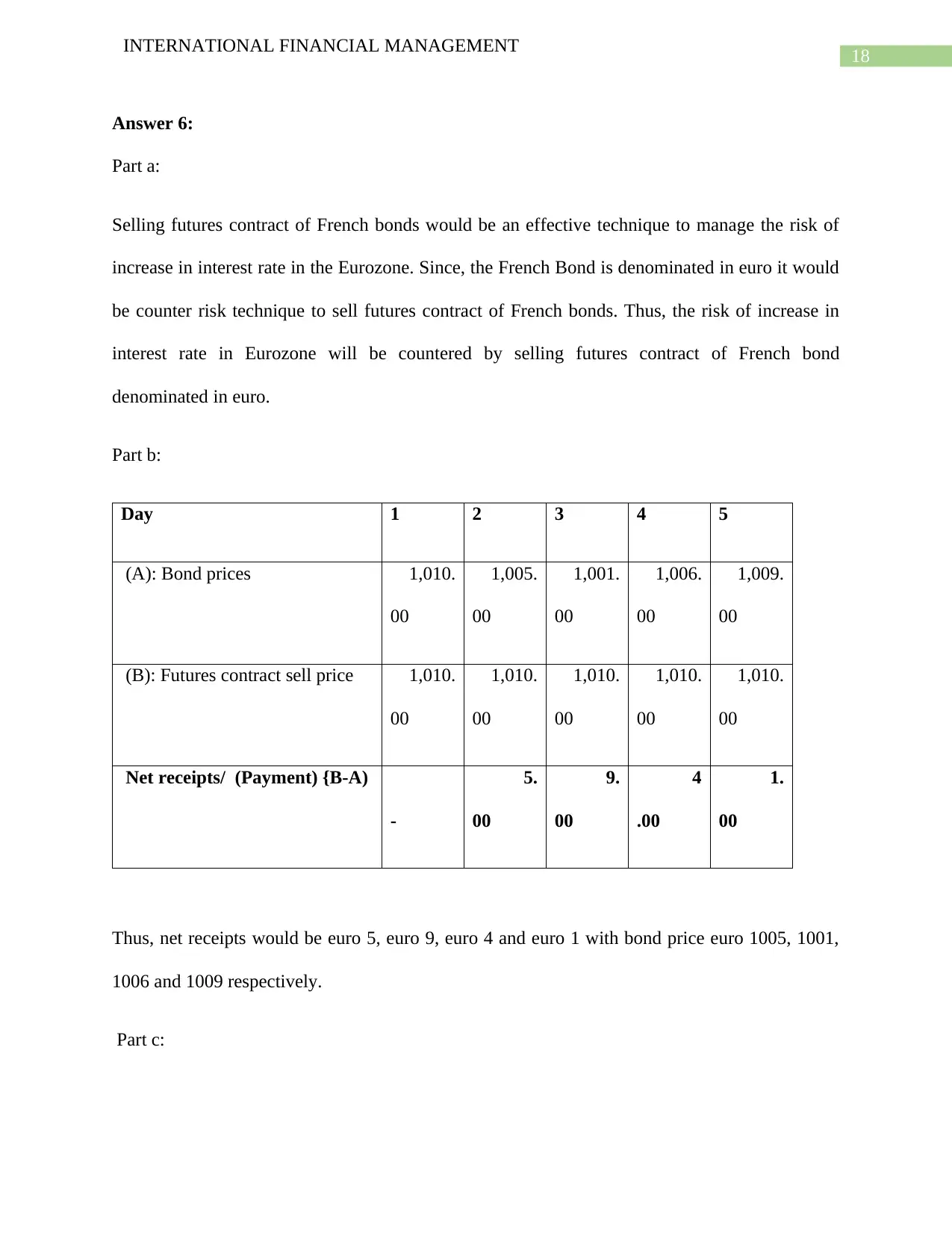

Answer 6:

Part a:

Selling futures contract of French bonds would be an effective technique to manage the risk of

increase in interest rate in the Eurozone. Since, the French Bond is denominated in euro it would

be counter risk technique to sell futures contract of French bonds. Thus, the risk of increase in

interest rate in Eurozone will be countered by selling futures contract of French bond

denominated in euro.

Part b:

Day 1 2 3 4 5

(A): Bond prices 1,010.

00

1,005.

00

1,001.

00

1,006.

00

1,009.

00

(B): Futures contract sell price 1,010.

00

1,010.

00

1,010.

00

1,010.

00

1,010.

00

Net receipts/ (Payment) {B-A)

-

5.

00

9.

00

4

.00

1.

00

Thus, net receipts would be euro 5, euro 9, euro 4 and euro 1 with bond price euro 1005, 1001,

1006 and 1009 respectively.

Part c:

INTERNATIONAL FINANCIAL MANAGEMENT

Answer 6:

Part a:

Selling futures contract of French bonds would be an effective technique to manage the risk of

increase in interest rate in the Eurozone. Since, the French Bond is denominated in euro it would

be counter risk technique to sell futures contract of French bonds. Thus, the risk of increase in

interest rate in Eurozone will be countered by selling futures contract of French bond

denominated in euro.

Part b:

Day 1 2 3 4 5

(A): Bond prices 1,010.

00

1,005.

00

1,001.

00

1,006.

00

1,009.

00

(B): Futures contract sell price 1,010.

00

1,010.

00

1,010.

00

1,010.

00

1,010.

00

Net receipts/ (Payment) {B-A)

-

5.

00

9.

00

4

.00

1.

00

Thus, net receipts would be euro 5, euro 9, euro 4 and euro 1 with bond price euro 1005, 1001,

1006 and 1009 respectively.

Part c:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

INTERNATIONAL FINANCIAL MANAGEMENT

The insistence of for daily settlement by the market is mainly to keep the liquidation in the

market. Apart from that daily trading through settlement will increase the total turnover in the

market resulting in economic growth in the market.

Part d:

Interest rate swap is a technique used to manage the fluctuation in interest rates on financial

instruments. By interest rate swap one can manage the risk of loss on borrowed funds as well as

funds given on loan to other parties. It is an effective risk management strategy to reduce the

overall risk associated with interest rates on different instruments.

Part e:

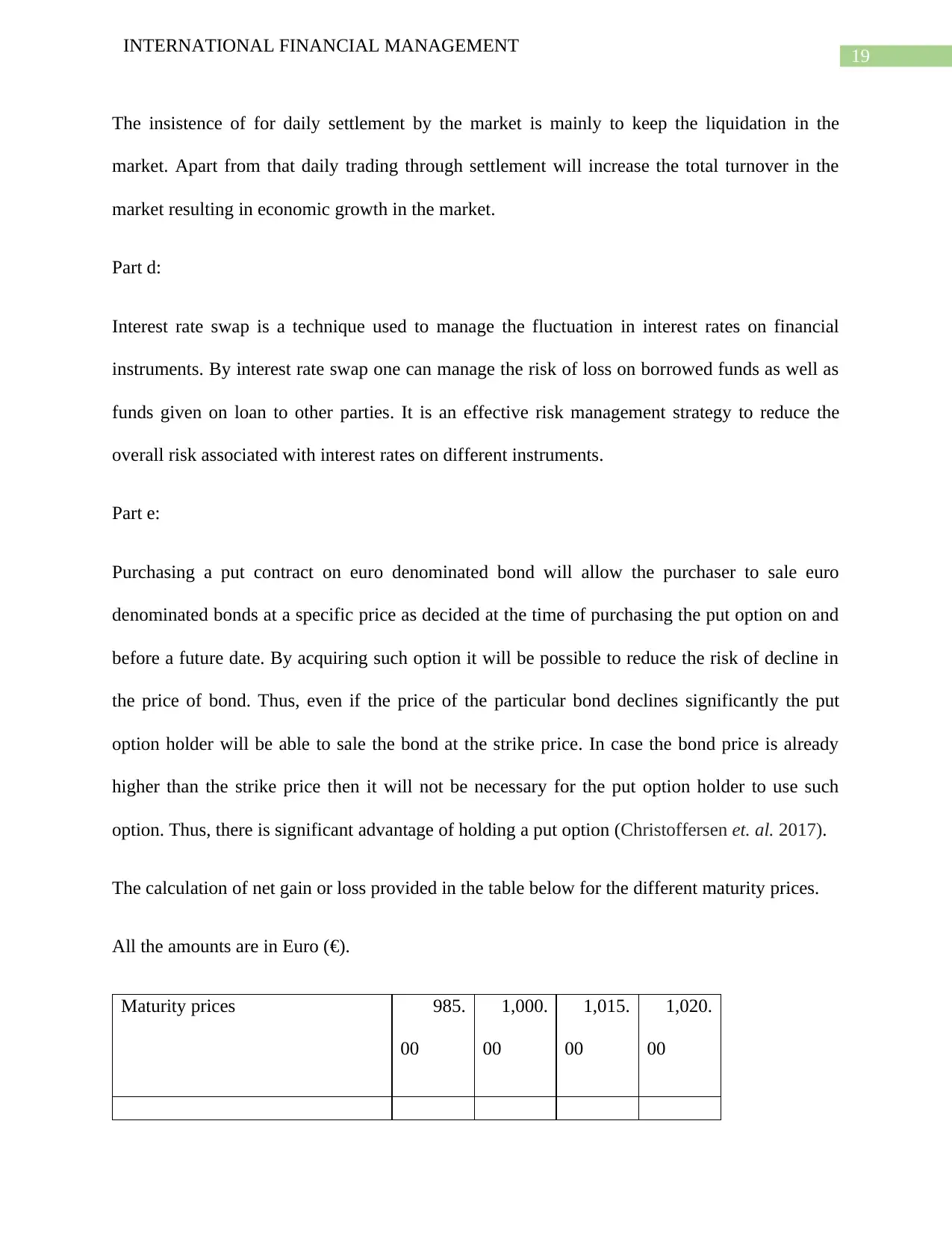

Purchasing a put contract on euro denominated bond will allow the purchaser to sale euro

denominated bonds at a specific price as decided at the time of purchasing the put option on and

before a future date. By acquiring such option it will be possible to reduce the risk of decline in

the price of bond. Thus, even if the price of the particular bond declines significantly the put

option holder will be able to sale the bond at the strike price. In case the bond price is already

higher than the strike price then it will not be necessary for the put option holder to use such

option. Thus, there is significant advantage of holding a put option (Christoffersen et. al. 2017).

The calculation of net gain or loss provided in the table below for the different maturity prices.

All the amounts are in Euro (€).

Maturity prices 985.

00

1,000.

00

1,015.

00

1,020.

00

INTERNATIONAL FINANCIAL MANAGEMENT

The insistence of for daily settlement by the market is mainly to keep the liquidation in the

market. Apart from that daily trading through settlement will increase the total turnover in the

market resulting in economic growth in the market.

Part d:

Interest rate swap is a technique used to manage the fluctuation in interest rates on financial

instruments. By interest rate swap one can manage the risk of loss on borrowed funds as well as

funds given on loan to other parties. It is an effective risk management strategy to reduce the

overall risk associated with interest rates on different instruments.

Part e:

Purchasing a put contract on euro denominated bond will allow the purchaser to sale euro

denominated bonds at a specific price as decided at the time of purchasing the put option on and

before a future date. By acquiring such option it will be possible to reduce the risk of decline in

the price of bond. Thus, even if the price of the particular bond declines significantly the put

option holder will be able to sale the bond at the strike price. In case the bond price is already

higher than the strike price then it will not be necessary for the put option holder to use such

option. Thus, there is significant advantage of holding a put option (Christoffersen et. al. 2017).

The calculation of net gain or loss provided in the table below for the different maturity prices.

All the amounts are in Euro (€).

Maturity prices 985.

00

1,000.

00

1,015.

00

1,020.

00

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.