International Financial Management

VerifiedAdded on 2022/11/13

|11

|1795

|116

AI Summary

This document covers various topics related to International Financial Management such as transaction, economic and translation exposure, hedging exchange exposures, credit shortage, SIV and CDO. It also provides solved assignments, essays, dissertation and more at Desklib.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INTERNATIONAL FINANCIAL MANAGEMENT

International Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

International Financial Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1INTERNATIONAL FINANCIAL MANAGEMENT

Table of Contents

Question 1:.................................................................................................................................2

Question 2:.................................................................................................................................3

Question 3:.................................................................................................................................5

Question 4:.................................................................................................................................6

Question 5:.................................................................................................................................6

Question 6:.................................................................................................................................7

Question 7:.................................................................................................................................7

References:.................................................................................................................................9

Table of Contents

Question 1:.................................................................................................................................2

Question 2:.................................................................................................................................3

Question 3:.................................................................................................................................5

Question 4:.................................................................................................................................6

Question 5:.................................................................................................................................6

Question 6:.................................................................................................................................7

Question 7:.................................................................................................................................7

References:.................................................................................................................................9

2INTERNATIONAL FINANCIAL MANAGEMENT

Question 1:

Transaction exposure-

It is known as interim "economic exposure”, which is connected to the uncertainties

incorporated with specific agreements ventured into by the companies contributing to

"foreign exchange exposures". A contract observed to discharge or in-pouring of “foreign

currency" would lead to "transaction exposure" (Ahiagbah, et al., 2016). For example,

Company X situated in "Australia" has an agreement for purchasing "raw materials" from

Company Y located in "U.K." at the present "fixed price" for the forthcoming "two years".

The "foreign exchange" remunerator is recognised as Company X and it is opened to

"transaction risk" from the "pound" tariff shifts regarding the "AUD". If there is reduction in

"pound" worth, lesser disbursements would be done in the terminology of "AUD" and in the

other way around, the disbursements would be more contributing to "foreign currency

exposure".

Economic exposure-

When an inevitable "foreign exchange exposure" impacts a company constantly in the

longstanding, it is considered as "economic exposure". The "market" value of the company

would get impacted, as the uncertainty is implicit to the company, this would impact the

"profit level" over the years (Bekaert, & Hodrick, 2017). Suppose, a garment producer in

"Australia" having its "markets" mostly in the "U.K." is open constantly to the "pound" tariff

shifts and therefore, it is "exposed" to "economic exposure".

Translation exposure-

It is of "accounting" "nature" and this exposure is involved with "profit or loss"

occurring from the "translation" or modification of the operating statements of an ancillary

Question 1:

Transaction exposure-

It is known as interim "economic exposure”, which is connected to the uncertainties

incorporated with specific agreements ventured into by the companies contributing to

"foreign exchange exposures". A contract observed to discharge or in-pouring of “foreign

currency" would lead to "transaction exposure" (Ahiagbah, et al., 2016). For example,

Company X situated in "Australia" has an agreement for purchasing "raw materials" from

Company Y located in "U.K." at the present "fixed price" for the forthcoming "two years".

The "foreign exchange" remunerator is recognised as Company X and it is opened to

"transaction risk" from the "pound" tariff shifts regarding the "AUD". If there is reduction in

"pound" worth, lesser disbursements would be done in the terminology of "AUD" and in the

other way around, the disbursements would be more contributing to "foreign currency

exposure".

Economic exposure-

When an inevitable "foreign exchange exposure" impacts a company constantly in the

longstanding, it is considered as "economic exposure". The "market" value of the company

would get impacted, as the uncertainty is implicit to the company, this would impact the

"profit level" over the years (Bekaert, & Hodrick, 2017). Suppose, a garment producer in

"Australia" having its "markets" mostly in the "U.K." is open constantly to the "pound" tariff

shifts and therefore, it is "exposed" to "economic exposure".

Translation exposure-

It is of "accounting" "nature" and this exposure is involved with "profit or loss"

occurring from the "translation" or modification of the operating statements of an ancillary

3INTERNATIONAL FINANCIAL MANAGEMENT

located in foreign country (Brooke, 2016). For instance, a company such as- "General

Motors" could sell vehicles in around "200" countries and those vehicles might be produced

in as many as "50" diverse countries. At the conclusion of the "reporting" time, the company

is required to reveal the unified monetary functionalities in "domestic" money culminating in

"profit or loss" from the various "foreign" monetary shifts.

Question 2:

Requirement 1-

When the stock "market" is ideal, it not vital for a company to "hedge" "exchange"

exposures. Moreover, when "markets" are not ideal, "hedging" contributes worth to the

company. First, if the company administration has a concept of the risks of the business

greater than its investors, the company requires to "hedge" and not their investors (Van

Cauwenberge, et al., 2015). Second, it could be viable for the company to "hedge" at reduced

price. Third, in the event of "default significant" prices, it is feasible to verify "corporate

hedging", because the possibility of "default" is diminished. Lastly, if dynamic "taxes" are

encountered by the company, " hedging" might help in reducing "tax" accountabilities via

balancing of "corporate" incomes.

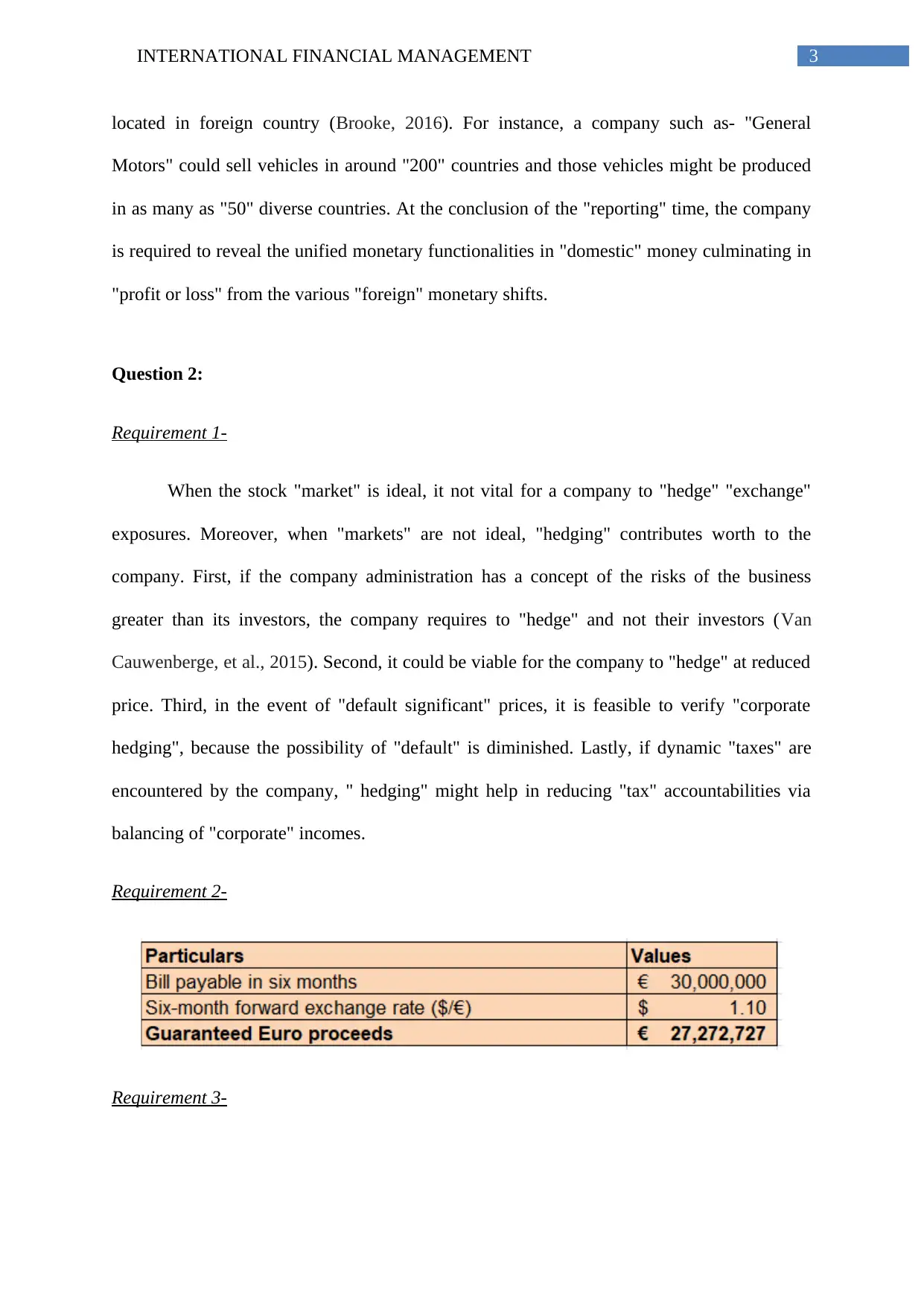

Requirement 2-

Requirement 3-

located in foreign country (Brooke, 2016). For instance, a company such as- "General

Motors" could sell vehicles in around "200" countries and those vehicles might be produced

in as many as "50" diverse countries. At the conclusion of the "reporting" time, the company

is required to reveal the unified monetary functionalities in "domestic" money culminating in

"profit or loss" from the various "foreign" monetary shifts.

Question 2:

Requirement 1-

When the stock "market" is ideal, it not vital for a company to "hedge" "exchange"

exposures. Moreover, when "markets" are not ideal, "hedging" contributes worth to the

company. First, if the company administration has a concept of the risks of the business

greater than its investors, the company requires to "hedge" and not their investors (Van

Cauwenberge, et al., 2015). Second, it could be viable for the company to "hedge" at reduced

price. Third, in the event of "default significant" prices, it is feasible to verify "corporate

hedging", because the possibility of "default" is diminished. Lastly, if dynamic "taxes" are

encountered by the company, " hedging" might help in reducing "tax" accountabilities via

balancing of "corporate" incomes.

Requirement 2-

Requirement 3-

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4INTERNATIONAL FINANCIAL MANAGEMENT

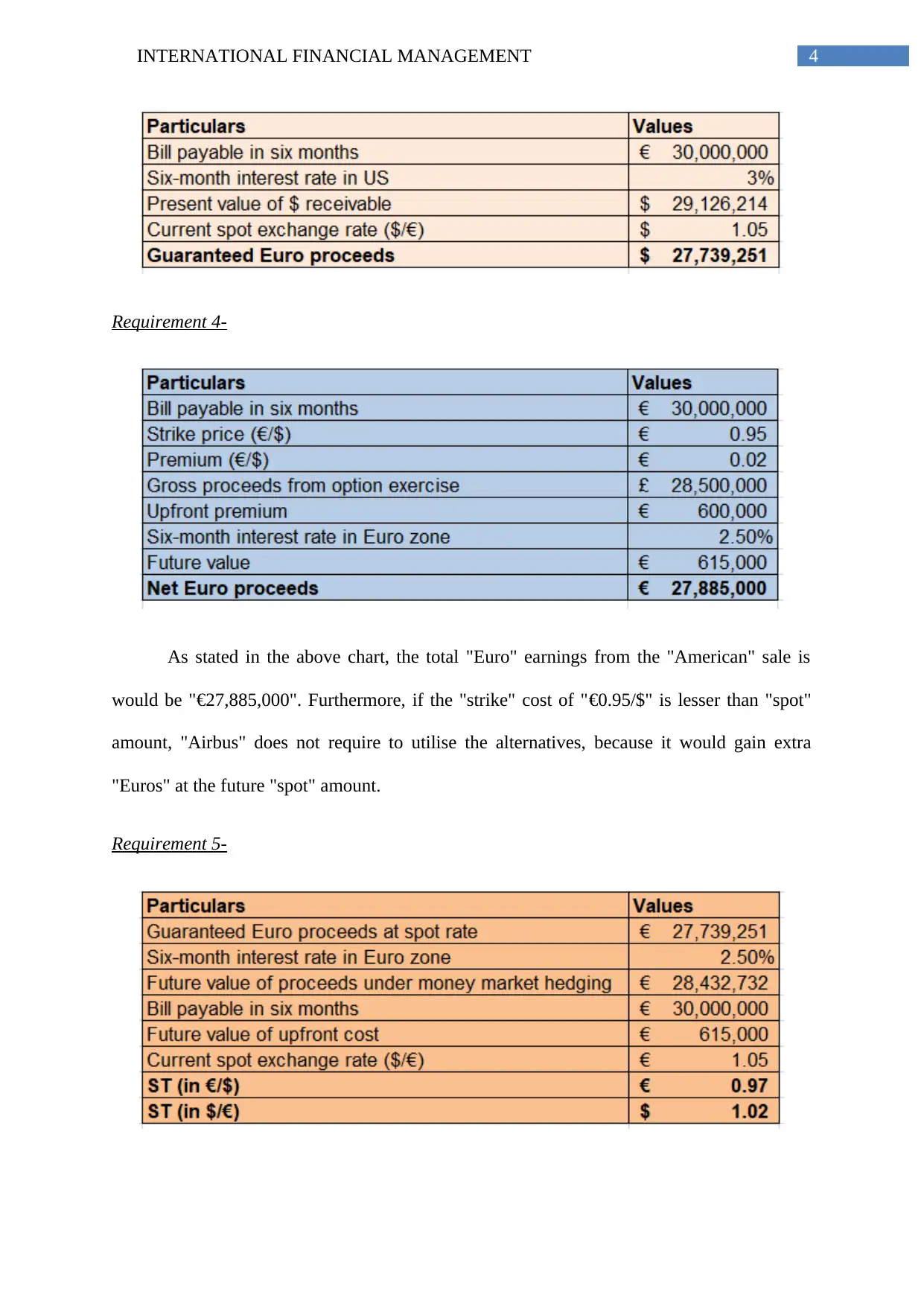

Requirement 4-

As stated in the above chart, the total "Euro" earnings from the "American" sale is

would be "€27,885,000". Furthermore, if the "strike" cost of "€0.95/$" is lesser than "spot"

amount, "Airbus" does not require to utilise the alternatives, because it would gain extra

"Euros" at the future "spot" amount.

Requirement 5-

Requirement 4-

As stated in the above chart, the total "Euro" earnings from the "American" sale is

would be "€27,885,000". Furthermore, if the "strike" cost of "€0.95/$" is lesser than "spot"

amount, "Airbus" does not require to utilise the alternatives, because it would gain extra

"Euros" at the future "spot" amount.

Requirement 5-

5INTERNATIONAL FINANCIAL MANAGEMENT

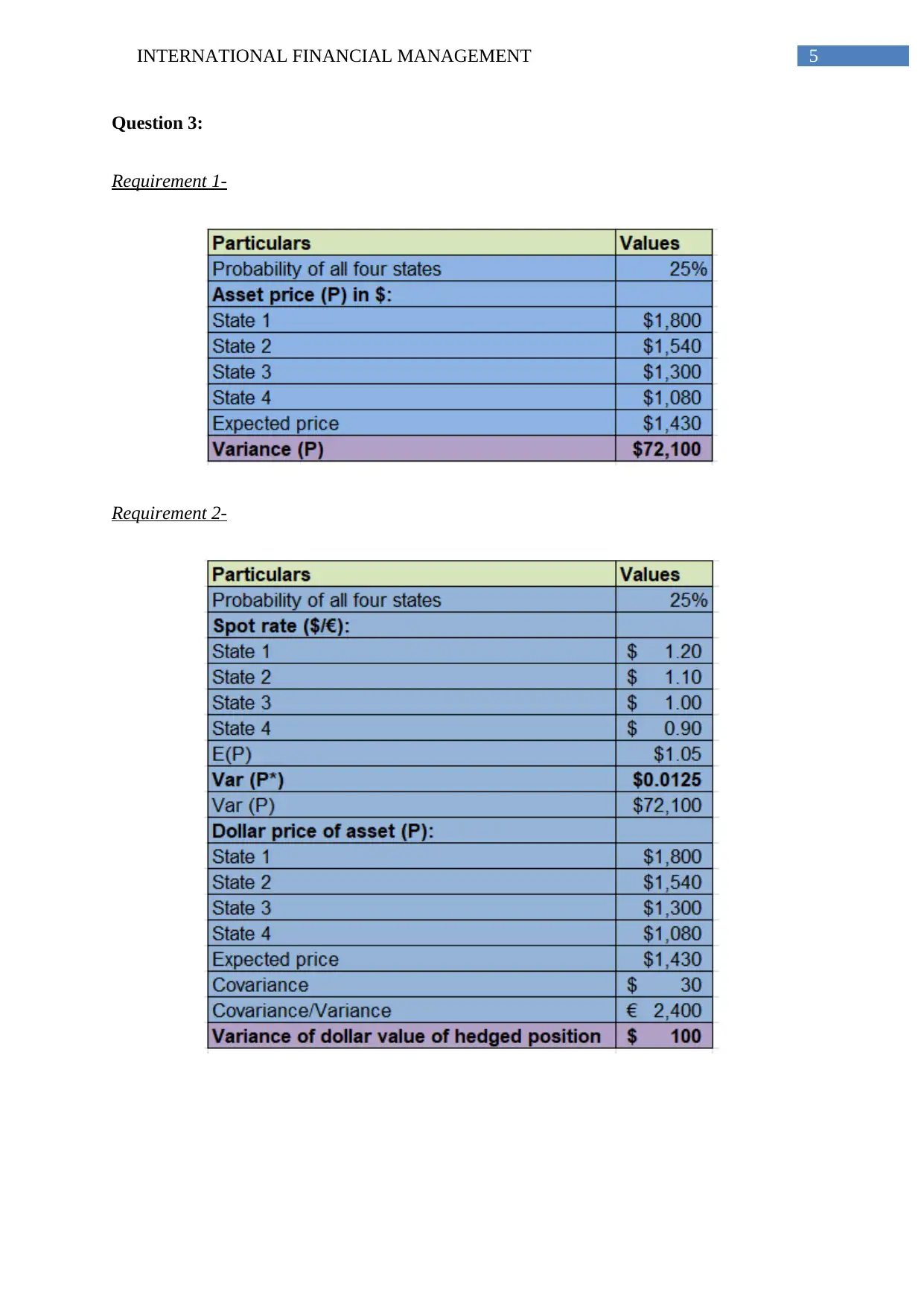

Question 3:

Requirement 1-

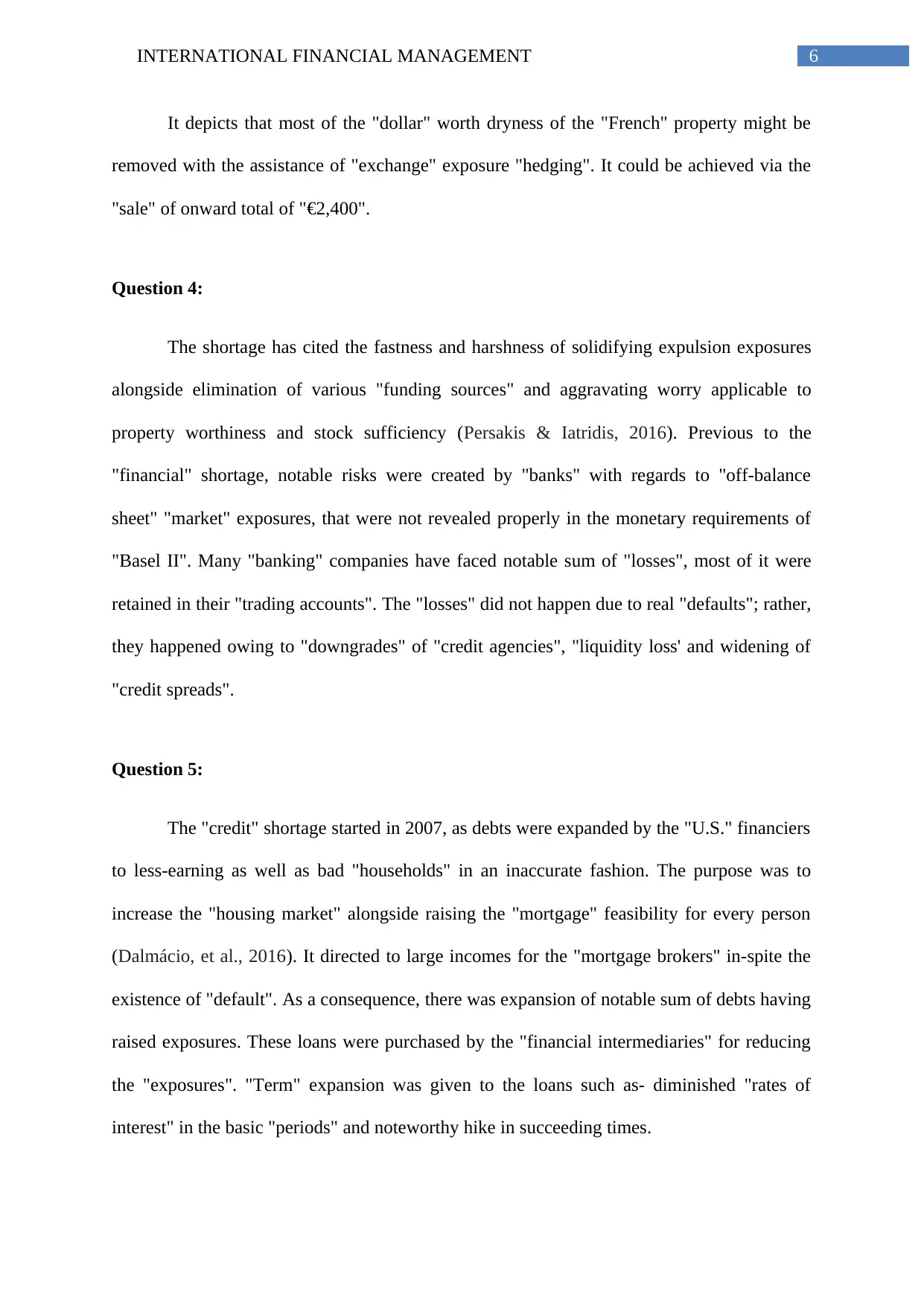

Requirement 2-

Question 3:

Requirement 1-

Requirement 2-

6INTERNATIONAL FINANCIAL MANAGEMENT

It depicts that most of the "dollar" worth dryness of the "French" property might be

removed with the assistance of "exchange" exposure "hedging". It could be achieved via the

"sale" of onward total of "€2,400".

Question 4:

The shortage has cited the fastness and harshness of solidifying expulsion exposures

alongside elimination of various "funding sources" and aggravating worry applicable to

property worthiness and stock sufficiency (Persakis & Iatridis, 2016). Previous to the

"financial" shortage, notable risks were created by "banks" with regards to "off-balance

sheet" "market" exposures, that were not revealed properly in the monetary requirements of

"Basel II". Many "banking" companies have faced notable sum of "losses", most of it were

retained in their "trading accounts". The "losses" did not happen due to real "defaults"; rather,

they happened owing to "downgrades" of "credit agencies", "liquidity loss' and widening of

"credit spreads".

Question 5:

The "credit" shortage started in 2007, as debts were expanded by the "U.S." financiers

to less-earning as well as bad "households" in an inaccurate fashion. The purpose was to

increase the "housing market" alongside raising the "mortgage" feasibility for every person

(Dalmácio, et al., 2016). It directed to large incomes for the "mortgage brokers" in-spite the

existence of "default". As a consequence, there was expansion of notable sum of debts having

raised exposures. These loans were purchased by the "financial intermediaries" for reducing

the "exposures". "Term" expansion was given to the loans such as- diminished "rates of

interest" in the basic "periods" and noteworthy hike in succeeding times.

It depicts that most of the "dollar" worth dryness of the "French" property might be

removed with the assistance of "exchange" exposure "hedging". It could be achieved via the

"sale" of onward total of "€2,400".

Question 4:

The shortage has cited the fastness and harshness of solidifying expulsion exposures

alongside elimination of various "funding sources" and aggravating worry applicable to

property worthiness and stock sufficiency (Persakis & Iatridis, 2016). Previous to the

"financial" shortage, notable risks were created by "banks" with regards to "off-balance

sheet" "market" exposures, that were not revealed properly in the monetary requirements of

"Basel II". Many "banking" companies have faced notable sum of "losses", most of it were

retained in their "trading accounts". The "losses" did not happen due to real "defaults"; rather,

they happened owing to "downgrades" of "credit agencies", "liquidity loss' and widening of

"credit spreads".

Question 5:

The "credit" shortage started in 2007, as debts were expanded by the "U.S." financiers

to less-earning as well as bad "households" in an inaccurate fashion. The purpose was to

increase the "housing market" alongside raising the "mortgage" feasibility for every person

(Dalmácio, et al., 2016). It directed to large incomes for the "mortgage brokers" in-spite the

existence of "default". As a consequence, there was expansion of notable sum of debts having

raised exposures. These loans were purchased by the "financial intermediaries" for reducing

the "exposures". "Term" expansion was given to the loans such as- diminished "rates of

interest" in the basic "periods" and noteworthy hike in succeeding times.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCIAL MANAGEMENT

Due to the hike in "inflation", the "banks" raised the "lending rates" notably, this

hiked the "defaults" from the "homeowners". The ultimate result was the reduction in the

"housing" cots which boosted the "mortgage" issues. As a consequence, the "lending"

businesses went into solvency, as they backslide to reclaim the expanded debts that resulted

in dramatic hike in exposure. This became a "global" problem, as it was impossible to

increase "funds" or even "borrow" them due to the "market" downslide and the effect was on

the companies which gave debts. As an outcome, the "U.S." "economy" lagged, which

initially was the outcome in the "global financial crisis".

Question 6:

The "structured investment vehicle (SIV)" might be explained in the term of a "non-

banking institution", that is included in extending of "short-term" debts from properties which

are clasped in their list. They produce incomes from the property variations and expanded

debts (Deresky, 2017).

During the period "credit" shortage, "SIVs" were forced for expulsion of its

longstanding properties in order to reimburse the "maturing commercial" documents. It

happened because at that period, they faced notable monetary "losses" due to the expulsion

crisis. As a result, it affected the "SIVs" to rebuild due to the "global financial crisis".

Question 7:

A secured "debt" commitment (CDO) is associated "pooling funds" produced from

properties generating "profits" after this it is reconditioned in little portions for "selling" the

identical thing to the shareholders. These properties work in the terms of a guarantee to the

bundles, that are "sold" to the shareholders (Starks, et al., 2016).

Due to the hike in "inflation", the "banks" raised the "lending rates" notably, this

hiked the "defaults" from the "homeowners". The ultimate result was the reduction in the

"housing" cots which boosted the "mortgage" issues. As a consequence, the "lending"

businesses went into solvency, as they backslide to reclaim the expanded debts that resulted

in dramatic hike in exposure. This became a "global" problem, as it was impossible to

increase "funds" or even "borrow" them due to the "market" downslide and the effect was on

the companies which gave debts. As an outcome, the "U.S." "economy" lagged, which

initially was the outcome in the "global financial crisis".

Question 6:

The "structured investment vehicle (SIV)" might be explained in the term of a "non-

banking institution", that is included in extending of "short-term" debts from properties which

are clasped in their list. They produce incomes from the property variations and expanded

debts (Deresky, 2017).

During the period "credit" shortage, "SIVs" were forced for expulsion of its

longstanding properties in order to reimburse the "maturing commercial" documents. It

happened because at that period, they faced notable monetary "losses" due to the expulsion

crisis. As a result, it affected the "SIVs" to rebuild due to the "global financial crisis".

Question 7:

A secured "debt" commitment (CDO) is associated "pooling funds" produced from

properties generating "profits" after this it is reconditioned in little portions for "selling" the

identical thing to the shareholders. These properties work in the terms of a guarantee to the

bundles, that are "sold" to the shareholders (Starks, et al., 2016).

8INTERNATIONAL FINANCIAL MANAGEMENT

"CDOs" are considered to be tricky and this could be a factor behind "global financial

crisis". The factor is that during the time, there was decline in the worth "underlying"

properties culminating in "loss" for the publishing companies.

"CDOs" are considered to be tricky and this could be a factor behind "global financial

crisis". The factor is that during the time, there was decline in the worth "underlying"

properties culminating in "loss" for the publishing companies.

9INTERNATIONAL FINANCIAL MANAGEMENT

References:

Appiah, K. O., Awunyo-Vitor, D., Mireku, K., & Ahiagbah, C. (2016). Compliance with

international financial reporting standards: the case of listed firms in Ghana. Journal

of Financial Reporting and Accounting, 14(1), 131-156.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Brooke, M. Z. (2016). Handbook of international financial management. Springer.

Christiaens, J., Vanhee, C., Manes-Rossi, F., Aversano, N., & Van Cauwenberge, P. (2015).

The effect of IPSAS on reforming governmental financial reporting: An international

comparison. International Review of Administrative Sciences, 81(1), 158-177.

Cremers, M., Ferreira, M. A., Matos, P., & Starks, L. (2016). Indexing and active fund

management: International evidence. Journal of Financial Economics, 120(3), 539-

560.

Deresky, H. (2017). International management: Managing across borders and cultures.

Pearson Education India.

Persakis, A., & Iatridis, G. E. (2016). Audit quality, investor protection and earnings

management during the financial crisis of 2008: An international perspective. Journal

of International Financial Markets, Institutions and Money, 41, 73-101.

Rathke, A. A. T., Santana, V. D. F., Lourenço, I. M. E. C., & Dalmácio, F. Z. (2016).

International financial reporting standards and earnings management in latin

america. Revista de administração contemporânea, 20(3), 368-388.

References:

Appiah, K. O., Awunyo-Vitor, D., Mireku, K., & Ahiagbah, C. (2016). Compliance with

international financial reporting standards: the case of listed firms in Ghana. Journal

of Financial Reporting and Accounting, 14(1), 131-156.

Bekaert, G., & Hodrick, R. (2017). International financial management. Cambridge

University Press.

Brooke, M. Z. (2016). Handbook of international financial management. Springer.

Christiaens, J., Vanhee, C., Manes-Rossi, F., Aversano, N., & Van Cauwenberge, P. (2015).

The effect of IPSAS on reforming governmental financial reporting: An international

comparison. International Review of Administrative Sciences, 81(1), 158-177.

Cremers, M., Ferreira, M. A., Matos, P., & Starks, L. (2016). Indexing and active fund

management: International evidence. Journal of Financial Economics, 120(3), 539-

560.

Deresky, H. (2017). International management: Managing across borders and cultures.

Pearson Education India.

Persakis, A., & Iatridis, G. E. (2016). Audit quality, investor protection and earnings

management during the financial crisis of 2008: An international perspective. Journal

of International Financial Markets, Institutions and Money, 41, 73-101.

Rathke, A. A. T., Santana, V. D. F., Lourenço, I. M. E. C., & Dalmácio, F. Z. (2016).

International financial reporting standards and earnings management in latin

america. Revista de administração contemporânea, 20(3), 368-388.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10INTERNATIONAL FINANCIAL MANAGEMENT

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.