International Financial Management

VerifiedAdded on 2023/01/11

|22

|4974

|79

AI Summary

This document provides answers to various questions related to international financial management. It covers topics such as exchange rates, inflation rates, purchasing power parity, and the impact of these factors on the economy and business environment. The document also discusses the risk associated with international trade and finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

International financial management................................................................................................3

Answer 1..........................................................................................................................................3

Answer 2..........................................................................................................................................5

Answer 3..........................................................................................................................................9

Answer 4........................................................................................................................................10

Answer 5........................................................................................................................................11

Answer 6........................................................................................................................................18

References......................................................................................................................................21

International financial management................................................................................................3

Answer 1..........................................................................................................................................3

Answer 2..........................................................................................................................................5

Answer 3..........................................................................................................................................9

Answer 4........................................................................................................................................10

Answer 5........................................................................................................................................11

Answer 6........................................................................................................................................18

References......................................................................................................................................21

International financial management

Answer 1

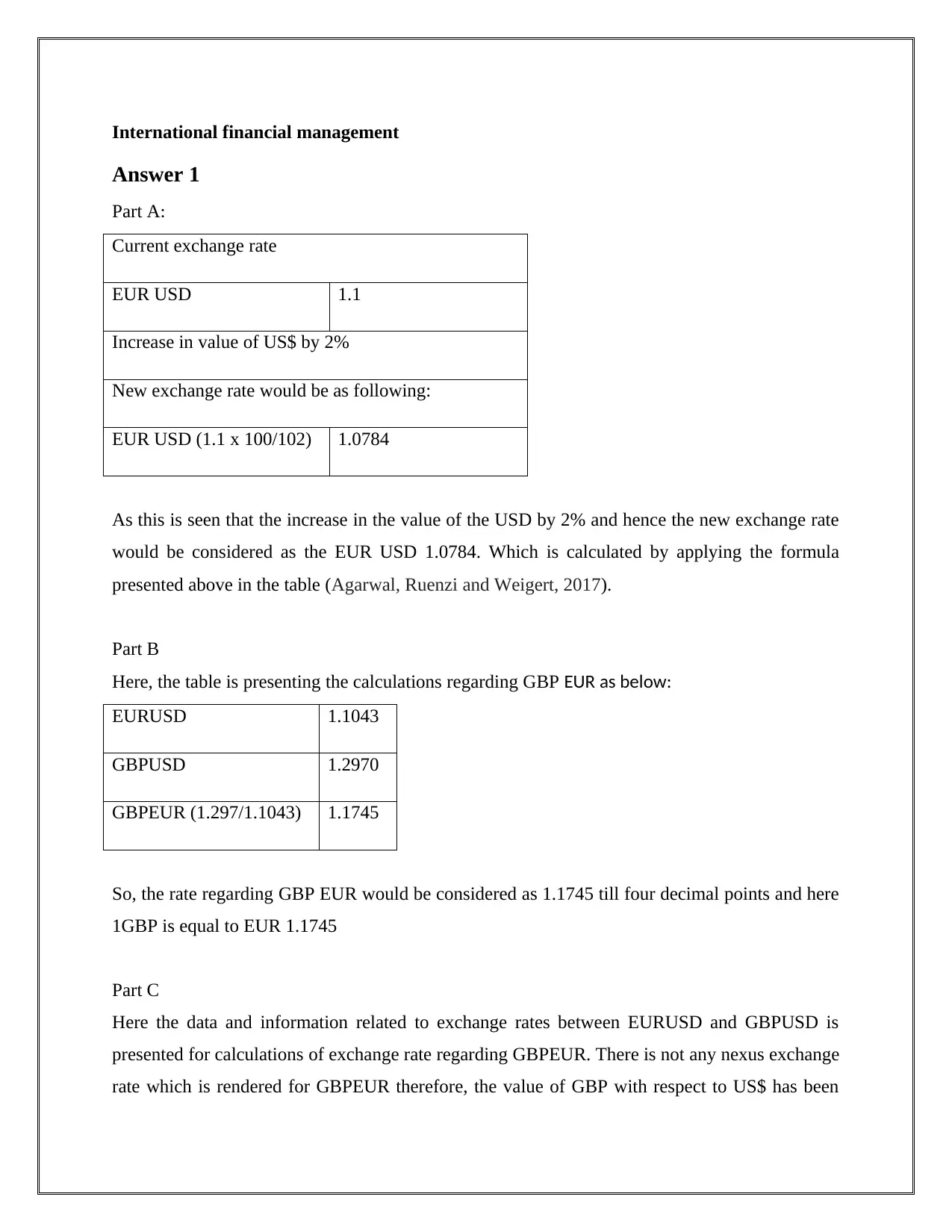

Part A:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

As this is seen that the increase in the value of the USD by 2% and hence the new exchange rate

would be considered as the EUR USD 1.0784. Which is calculated by applying the formula

presented above in the table (Agarwal, Ruenzi and Weigert, 2017).

Part B

Here, the table is presenting the calculations regarding GBP EUR as below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

So, the rate regarding GBP EUR would be considered as 1.1745 till four decimal points and here

1GBP is equal to EUR 1.1745

Part C

Here the data and information related to exchange rates between EURUSD and GBPUSD is

presented for calculations of exchange rate regarding GBPEUR. There is not any nexus exchange

rate which is rendered for GBPEUR therefore, the value of GBP with respect to US$ has been

Answer 1

Part A:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

As this is seen that the increase in the value of the USD by 2% and hence the new exchange rate

would be considered as the EUR USD 1.0784. Which is calculated by applying the formula

presented above in the table (Agarwal, Ruenzi and Weigert, 2017).

Part B

Here, the table is presenting the calculations regarding GBP EUR as below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

So, the rate regarding GBP EUR would be considered as 1.1745 till four decimal points and here

1GBP is equal to EUR 1.1745

Part C

Here the data and information related to exchange rates between EURUSD and GBPUSD is

presented for calculations of exchange rate regarding GBPEUR. There is not any nexus exchange

rate which is rendered for GBPEUR therefore, the value of GBP with respect to US$ has been

considered along with the value of US$ in respect to EUR (Bekaert and Hodrick, 2017). In

accordance with it, the exchange rate of GBREUR can be calculated with the help of value

regarding US$ against EUR and value regarding US$ against GBP with their comparison. Many

experts are using this technique for calculation of exchange rates between two countries and it is

the most popular method for this, helpful when there is no any direct exchange rate is presented

for two currencies. This case is providing as exchange rates between US$ and GBP, EUR and

US$. Even, the exchange rates between GBP and EUR is not rendered so the comparison of

these values regarding US$ against GBP and also against EUR so on the exchange rate of

GBPEUR can be calculated.

Triangular arbitrage is referred as a profit calculated from arbitration of various currencies due to

the variations in three kind of currencies. In the presented case the value regarding US$ to EUR

and US$ to GBP can be applied for determined the earnings from triangular arbitrage. For an

instance if at present US$ to purchase EUR has been invested and after some time received as

GBP in return of EUR. In this situation it rendered a maximum amount of profit to any investor

will be named as triangular arbitrage (Brooke, 2016). There is a complete understanding with

differences of exchange rate and capability of predicting the variations in different currencies

rendered as golden opportunity to investors to make surplus through arbitration.

accordance with it, the exchange rate of GBREUR can be calculated with the help of value

regarding US$ against EUR and value regarding US$ against GBP with their comparison. Many

experts are using this technique for calculation of exchange rates between two countries and it is

the most popular method for this, helpful when there is no any direct exchange rate is presented

for two currencies. This case is providing as exchange rates between US$ and GBP, EUR and

US$. Even, the exchange rates between GBP and EUR is not rendered so the comparison of

these values regarding US$ against GBP and also against EUR so on the exchange rate of

GBPEUR can be calculated.

Triangular arbitrage is referred as a profit calculated from arbitration of various currencies due to

the variations in three kind of currencies. In the presented case the value regarding US$ to EUR

and US$ to GBP can be applied for determined the earnings from triangular arbitrage. For an

instance if at present US$ to purchase EUR has been invested and after some time received as

GBP in return of EUR. In this situation it rendered a maximum amount of profit to any investor

will be named as triangular arbitrage (Brooke, 2016). There is a complete understanding with

differences of exchange rate and capability of predicting the variations in different currencies

rendered as golden opportunity to investors to make surplus through arbitration.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

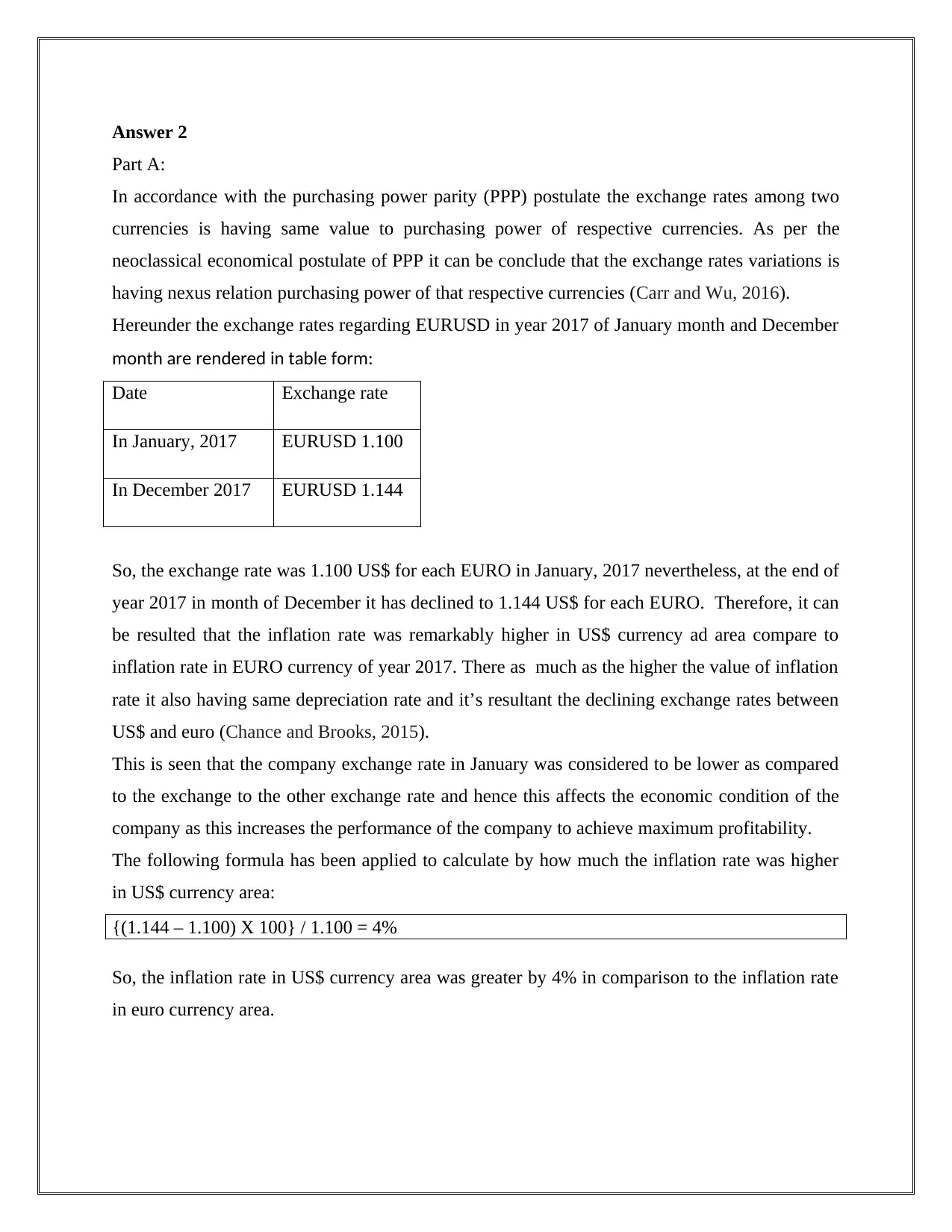

Answer 2

Part A:

In accordance with the purchasing power parity (PPP) postulate the exchange rates among two

currencies is having same value to purchasing power of respective currencies. As per the

neoclassical economical postulate of PPP it can be conclude that the exchange rates variations is

having nexus relation purchasing power of that respective currencies (Carr and Wu, 2016).

Hereunder the exchange rates regarding EURUSD in year 2017 of January month and December

month are rendered in table form:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, the exchange rate was 1.100 US$ for each EURO in January, 2017 nevertheless, at the end of

year 2017 in month of December it has declined to 1.144 US$ for each EURO. Therefore, it can

be resulted that the inflation rate was remarkably higher in US$ currency ad area compare to

inflation rate in EURO currency of year 2017. There as much as the higher the value of inflation

rate it also having same depreciation rate and it’s resultant the declining exchange rates between

US$ and euro (Chance and Brooks, 2015).

This is seen that the company exchange rate in January was considered to be lower as compared

to the exchange to the other exchange rate and hence this affects the economic condition of the

company as this increases the performance of the company to achieve maximum profitability.

The following formula has been applied to calculate by how much the inflation rate was higher

in US$ currency area:

{(1.144 – 1.100) X 100} / 1.100 = 4%

So, the inflation rate in US$ currency area was greater by 4% in comparison to the inflation rate

in euro currency area.

Part A:

In accordance with the purchasing power parity (PPP) postulate the exchange rates among two

currencies is having same value to purchasing power of respective currencies. As per the

neoclassical economical postulate of PPP it can be conclude that the exchange rates variations is

having nexus relation purchasing power of that respective currencies (Carr and Wu, 2016).

Hereunder the exchange rates regarding EURUSD in year 2017 of January month and December

month are rendered in table form:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, the exchange rate was 1.100 US$ for each EURO in January, 2017 nevertheless, at the end of

year 2017 in month of December it has declined to 1.144 US$ for each EURO. Therefore, it can

be resulted that the inflation rate was remarkably higher in US$ currency ad area compare to

inflation rate in EURO currency of year 2017. There as much as the higher the value of inflation

rate it also having same depreciation rate and it’s resultant the declining exchange rates between

US$ and euro (Chance and Brooks, 2015).

This is seen that the company exchange rate in January was considered to be lower as compared

to the exchange to the other exchange rate and hence this affects the economic condition of the

company as this increases the performance of the company to achieve maximum profitability.

The following formula has been applied to calculate by how much the inflation rate was higher

in US$ currency area:

{(1.144 – 1.100) X 100} / 1.100 = 4%

So, the inflation rate in US$ currency area was greater by 4% in comparison to the inflation rate

in euro currency area.

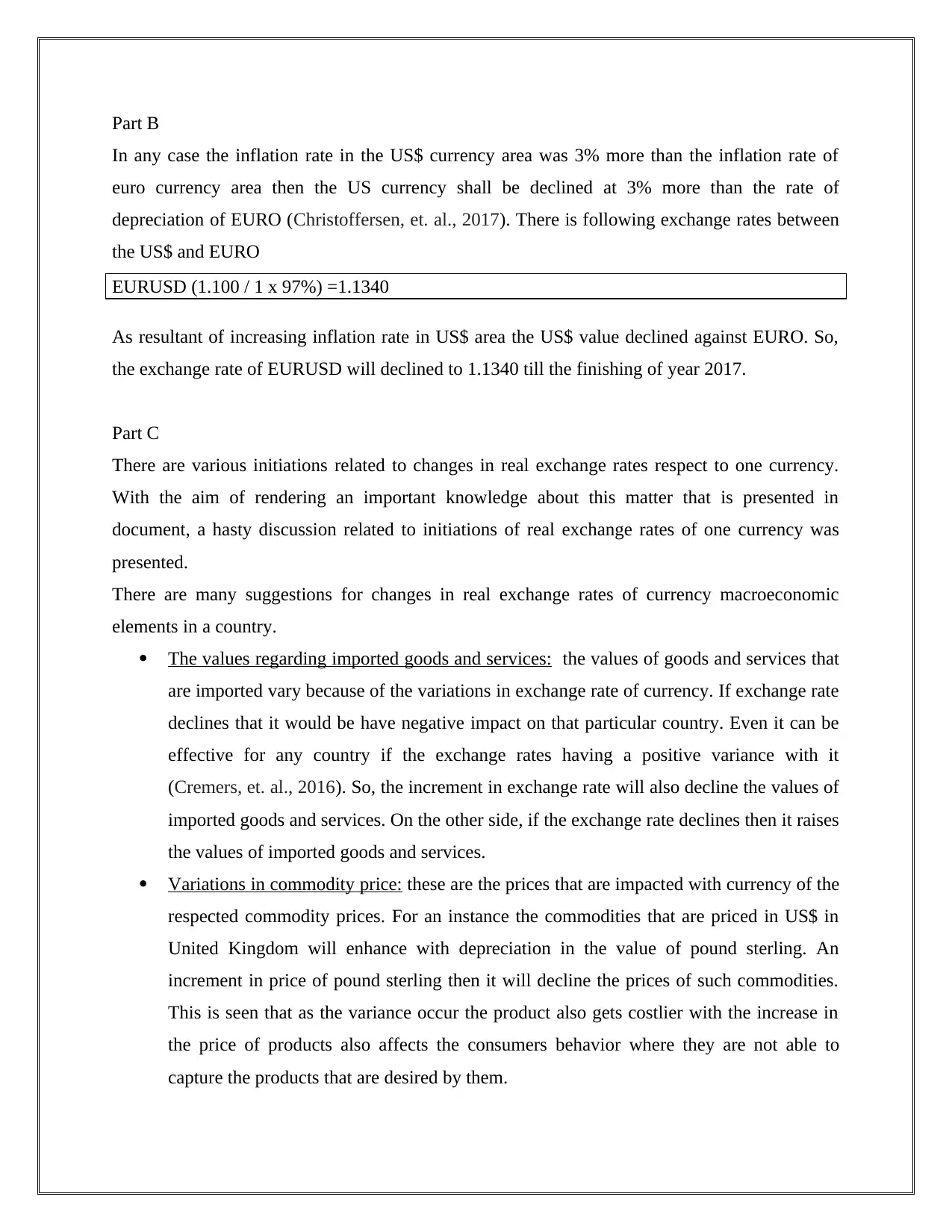

Part B

In any case the inflation rate in the US$ currency area was 3% more than the inflation rate of

euro currency area then the US currency shall be declined at 3% more than the rate of

depreciation of EURO (Christoffersen, et. al., 2017). There is following exchange rates between

the US$ and EURO

EURUSD (1.100 / 1 x 97%) =1.1340

As resultant of increasing inflation rate in US$ area the US$ value declined against EURO. So,

the exchange rate of EURUSD will declined to 1.1340 till the finishing of year 2017.

Part C

There are various initiations related to changes in real exchange rates respect to one currency.

With the aim of rendering an important knowledge about this matter that is presented in

document, a hasty discussion related to initiations of real exchange rates of one currency was

presented.

There are many suggestions for changes in real exchange rates of currency macroeconomic

elements in a country.

The values regarding imported goods and services: the values of goods and services that

are imported vary because of the variations in exchange rate of currency. If exchange rate

declines that it would be have negative impact on that particular country. Even it can be

effective for any country if the exchange rates having a positive variance with it

(Cremers, et. al., 2016). So, the increment in exchange rate will also decline the values of

imported goods and services. On the other side, if the exchange rate declines then it raises

the values of imported goods and services.

Variations in commodity price: these are the prices that are impacted with currency of the

respected commodity prices. For an instance the commodities that are priced in US$ in

United Kingdom will enhance with depreciation in the value of pound sterling. An

increment in price of pound sterling then it will decline the prices of such commodities.

This is seen that as the variance occur the product also gets costlier with the increase in

the price of products also affects the consumers behavior where they are not able to

capture the products that are desired by them.

In any case the inflation rate in the US$ currency area was 3% more than the inflation rate of

euro currency area then the US currency shall be declined at 3% more than the rate of

depreciation of EURO (Christoffersen, et. al., 2017). There is following exchange rates between

the US$ and EURO

EURUSD (1.100 / 1 x 97%) =1.1340

As resultant of increasing inflation rate in US$ area the US$ value declined against EURO. So,

the exchange rate of EURUSD will declined to 1.1340 till the finishing of year 2017.

Part C

There are various initiations related to changes in real exchange rates respect to one currency.

With the aim of rendering an important knowledge about this matter that is presented in

document, a hasty discussion related to initiations of real exchange rates of one currency was

presented.

There are many suggestions for changes in real exchange rates of currency macroeconomic

elements in a country.

The values regarding imported goods and services: the values of goods and services that

are imported vary because of the variations in exchange rate of currency. If exchange rate

declines that it would be have negative impact on that particular country. Even it can be

effective for any country if the exchange rates having a positive variance with it

(Cremers, et. al., 2016). So, the increment in exchange rate will also decline the values of

imported goods and services. On the other side, if the exchange rate declines then it raises

the values of imported goods and services.

Variations in commodity price: these are the prices that are impacted with currency of the

respected commodity prices. For an instance the commodities that are priced in US$ in

United Kingdom will enhance with depreciation in the value of pound sterling. An

increment in price of pound sterling then it will decline the prices of such commodities.

This is seen that as the variance occur the product also gets costlier with the increase in

the price of products also affects the consumers behavior where they are not able to

capture the products that are desired by them.

Effect on export enhancement: the enhancement in exported commodities would be

remarkably effected to subsequent to variations in real exchange rate of currency. For

instance the more exchange rate will renders more difficulties to sale its products in

foreign market. So, the export enhancement would be negatively affected f exchange rate

having an increment.

Impact on unemployment: In every country the exchange rate is also affected the

unemployment. If the exchange rate is getting higher then it will affect the export

enhancement and due to this the demand will also get declination in country (Davies, Kat

and Lu, 2016). Resultant it declines the production and due to this the unemployment will

increase. Therefore, the unemployment in any country can also be affected with the

variations in real exchange rate related to a currency.

Stimulation of demand: In any country there is a subsequent declination in currency and

its value can be implied to encouraging the demand in economy. As its resultant the

production if increased in economy then it would become higher the employment rate

(Yin, 2016).

So, there are many intimations that are made for real changes in exchange rates of currency that

can be understood from above consultation.

remarkably effected to subsequent to variations in real exchange rate of currency. For

instance the more exchange rate will renders more difficulties to sale its products in

foreign market. So, the export enhancement would be negatively affected f exchange rate

having an increment.

Impact on unemployment: In every country the exchange rate is also affected the

unemployment. If the exchange rate is getting higher then it will affect the export

enhancement and due to this the demand will also get declination in country (Davies, Kat

and Lu, 2016). Resultant it declines the production and due to this the unemployment will

increase. Therefore, the unemployment in any country can also be affected with the

variations in real exchange rate related to a currency.

Stimulation of demand: In any country there is a subsequent declination in currency and

its value can be implied to encouraging the demand in economy. As its resultant the

production if increased in economy then it would become higher the employment rate

(Yin, 2016).

So, there are many intimations that are made for real changes in exchange rates of currency that

can be understood from above consultation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

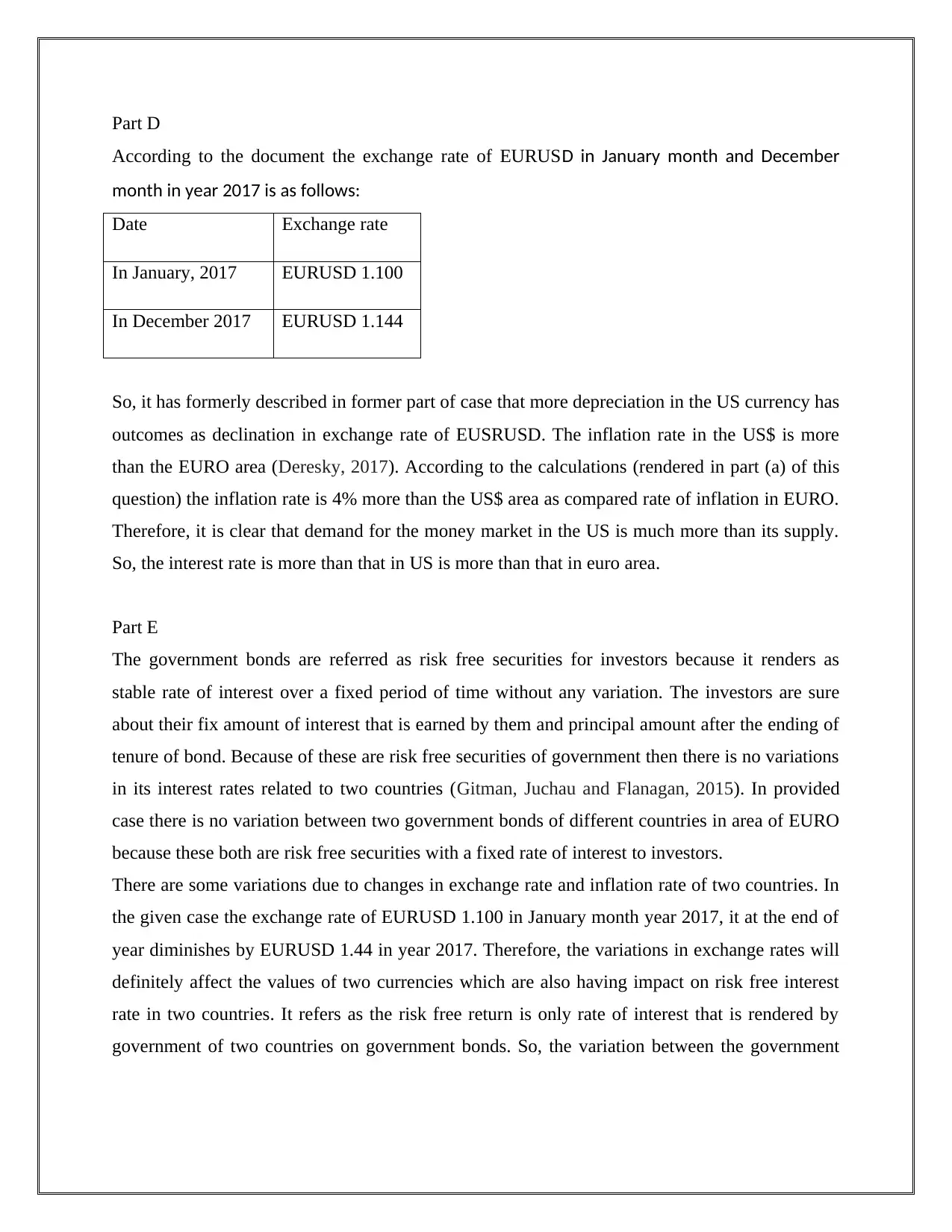

Part D

According to the document the exchange rate of EURUSD in January month and December

month in year 2017 is as follows:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, it has formerly described in former part of case that more depreciation in the US currency has

outcomes as declination in exchange rate of EUSRUSD. The inflation rate in the US$ is more

than the EURO area (Deresky, 2017). According to the calculations (rendered in part (a) of this

question) the inflation rate is 4% more than the US$ area as compared rate of inflation in EURO.

Therefore, it is clear that demand for the money market in the US is much more than its supply.

So, the interest rate is more than that in US is more than that in euro area.

Part E

The government bonds are referred as risk free securities for investors because it renders as

stable rate of interest over a fixed period of time without any variation. The investors are sure

about their fix amount of interest that is earned by them and principal amount after the ending of

tenure of bond. Because of these are risk free securities of government then there is no variations

in its interest rates related to two countries (Gitman, Juchau and Flanagan, 2015). In provided

case there is no variation between two government bonds of different countries in area of EURO

because these both are risk free securities with a fixed rate of interest to investors.

There are some variations due to changes in exchange rate and inflation rate of two countries. In

the given case the exchange rate of EURUSD 1.100 in January month year 2017, it at the end of

year diminishes by EURUSD 1.44 in year 2017. Therefore, the variations in exchange rates will

definitely affect the values of two currencies which are also having impact on risk free interest

rate in two countries. It refers as the risk free return is only rate of interest that is rendered by

government of two countries on government bonds. So, the variation between the government

According to the document the exchange rate of EURUSD in January month and December

month in year 2017 is as follows:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, it has formerly described in former part of case that more depreciation in the US currency has

outcomes as declination in exchange rate of EUSRUSD. The inflation rate in the US$ is more

than the EURO area (Deresky, 2017). According to the calculations (rendered in part (a) of this

question) the inflation rate is 4% more than the US$ area as compared rate of inflation in EURO.

Therefore, it is clear that demand for the money market in the US is much more than its supply.

So, the interest rate is more than that in US is more than that in euro area.

Part E

The government bonds are referred as risk free securities for investors because it renders as

stable rate of interest over a fixed period of time without any variation. The investors are sure

about their fix amount of interest that is earned by them and principal amount after the ending of

tenure of bond. Because of these are risk free securities of government then there is no variations

in its interest rates related to two countries (Gitman, Juchau and Flanagan, 2015). In provided

case there is no variation between two government bonds of different countries in area of EURO

because these both are risk free securities with a fixed rate of interest to investors.

There are some variations due to changes in exchange rate and inflation rate of two countries. In

the given case the exchange rate of EURUSD 1.100 in January month year 2017, it at the end of

year diminishes by EURUSD 1.44 in year 2017. Therefore, the variations in exchange rates will

definitely affect the values of two currencies which are also having impact on risk free interest

rate in two countries. It refers as the risk free return is only rate of interest that is rendered by

government of two countries on government bonds. So, the variation between the government

bonds interest rates which are determined to cost of capital in countries which can also be

considered as inflation rate.

Answer 3

The unpredictability is the most analytical factor in economy and its environment. In every

economy there are various factors that makes it promising for administration of country to

stabilize various factors. There are in economy ad in business world it is not possible to abolish

the uncertainty but with the help of many experts it can be reduce, manage factors of

environment. For conducting activities on international level it is important to determine the risk

associated in it so effective actions can be taken for reduce these uncertainties. There is

variations in exchange rate is very big risk for international trade and business and also for

international finance (Grundy and Verwijmeren, 2018). It is necessary to determine the risk

associated with variations of exchange rate in economy to take elective and proper actions to

diminish the risk and its adverse impact on economy.

Exchange rate variations is the changes in exchange rate that having impact on numerous

macroeconomic elements in economy of country. Variations in exchange rate. Having many

implications on the complete growth and enhancement of an economy. The variations in

exchange rate of domestic currency and other currencies is having noteworthy impact on

economy (Titman and Martin, 2014). The increment in exchange rate will having the adverse

impact on cost of imported goods and services which will better the balance of payment. The

increment in exchange rate is helping the increment in foreign currency reserve. If the

commodities are denominated in foreign currency will be decreasing so demand for that product

will be higher in the economy. On the other side there is an increment in exchange rate and due

to this fact that increment in exchange rate generally reduce the export of country as the prices of

goods increased. As resultants the demand of goods in international market diminishes and it

declines production. As well as the declination in production it also decrease the employment in

country and negatively affect the country (Kelly, Lustig and Van Nieuwerburgh, 2016). But,

sustainable exchange rate leads to a country towards balance of economic enhancement and

progress by taking necessary decisions in right direction. On the other hand the variations in

exchange rate is also having an adverse impact on country and it does not allow a country to

prepare policies and effective actions that can be applied for enhancement and growth of

economy.

considered as inflation rate.

Answer 3

The unpredictability is the most analytical factor in economy and its environment. In every

economy there are various factors that makes it promising for administration of country to

stabilize various factors. There are in economy ad in business world it is not possible to abolish

the uncertainty but with the help of many experts it can be reduce, manage factors of

environment. For conducting activities on international level it is important to determine the risk

associated in it so effective actions can be taken for reduce these uncertainties. There is

variations in exchange rate is very big risk for international trade and business and also for

international finance (Grundy and Verwijmeren, 2018). It is necessary to determine the risk

associated with variations of exchange rate in economy to take elective and proper actions to

diminish the risk and its adverse impact on economy.

Exchange rate variations is the changes in exchange rate that having impact on numerous

macroeconomic elements in economy of country. Variations in exchange rate. Having many

implications on the complete growth and enhancement of an economy. The variations in

exchange rate of domestic currency and other currencies is having noteworthy impact on

economy (Titman and Martin, 2014). The increment in exchange rate will having the adverse

impact on cost of imported goods and services which will better the balance of payment. The

increment in exchange rate is helping the increment in foreign currency reserve. If the

commodities are denominated in foreign currency will be decreasing so demand for that product

will be higher in the economy. On the other side there is an increment in exchange rate and due

to this fact that increment in exchange rate generally reduce the export of country as the prices of

goods increased. As resultants the demand of goods in international market diminishes and it

declines production. As well as the declination in production it also decrease the employment in

country and negatively affect the country (Kelly, Lustig and Van Nieuwerburgh, 2016). But,

sustainable exchange rate leads to a country towards balance of economic enhancement and

progress by taking necessary decisions in right direction. On the other hand the variations in

exchange rate is also having an adverse impact on country and it does not allow a country to

prepare policies and effective actions that can be applied for enhancement and growth of

economy.

Answer 4

There is globalization that allows companies of various countries to establish their operating

units in other countries. Therefore, the term “multi-national companies” has been identified to

companies and entities which are having its operational units in other countries. Multinational

countries (MNCs). This is seen that the economic condition of the company are considered to be

one of the element which made them suggest the exchange rate of the country (Kim, et. al,

2016). This is considered as one of the situation where the country has to find the way to tackle

the market situation and to find the way so that the increasing exchange rate could be handled

and the risk of the decrease in the economic condition of the company can be handled.

There is globalization that allows companies of various countries to establish their operating

units in other countries. Therefore, the term “multi-national companies” has been identified to

companies and entities which are having its operational units in other countries. Multinational

countries (MNCs). This is seen that the economic condition of the company are considered to be

one of the element which made them suggest the exchange rate of the country (Kim, et. al,

2016). This is considered as one of the situation where the country has to find the way to tackle

the market situation and to find the way so that the increasing exchange rate could be handled

and the risk of the decrease in the economic condition of the company can be handled.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

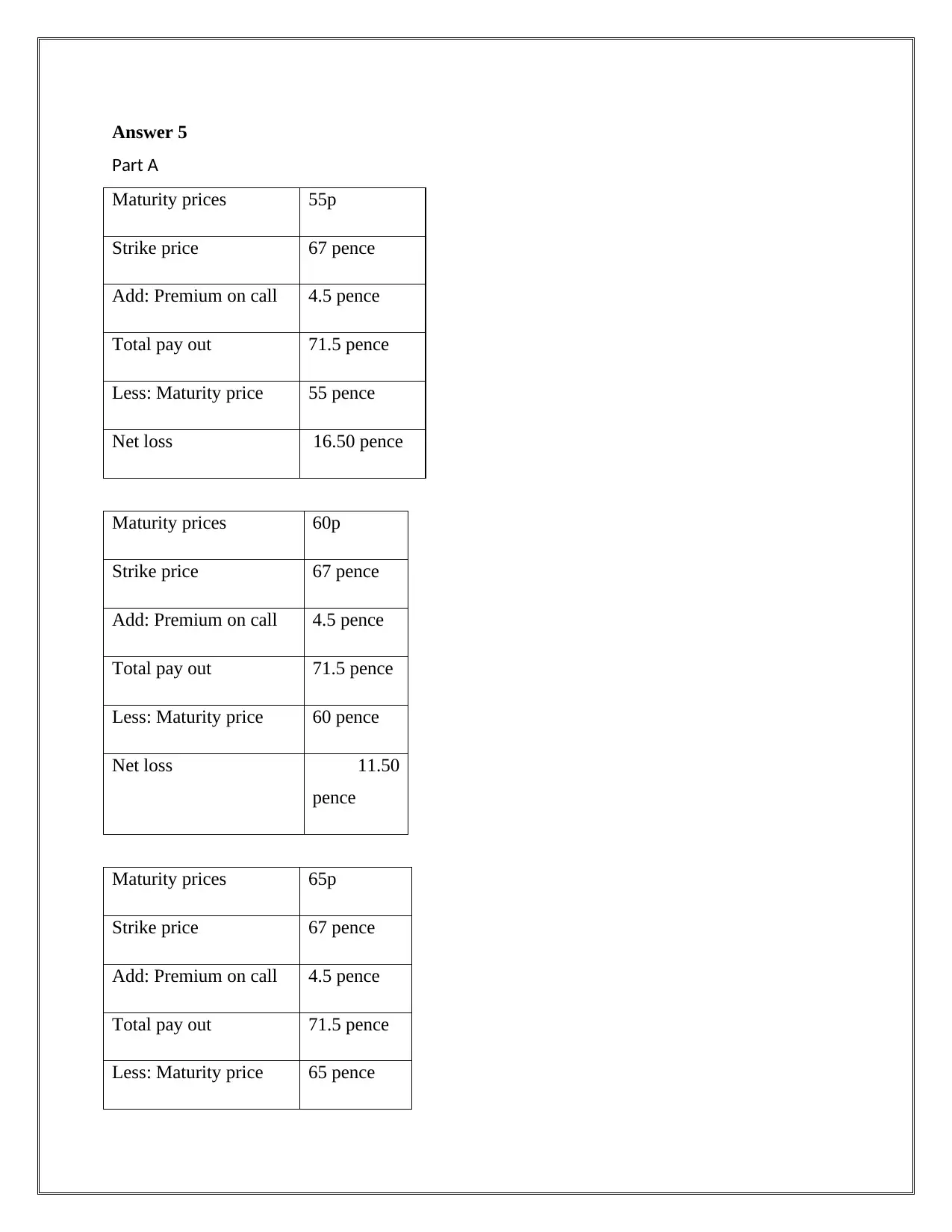

Answer 5

Part A

Maturity prices 55p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 55 pence

Net loss 16.50 pence

Maturity prices 60p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 60 pence

Net loss 11.50

pence

Maturity prices 65p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 65 pence

Part A

Maturity prices 55p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 55 pence

Net loss 16.50 pence

Maturity prices 60p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 60 pence

Net loss 11.50

pence

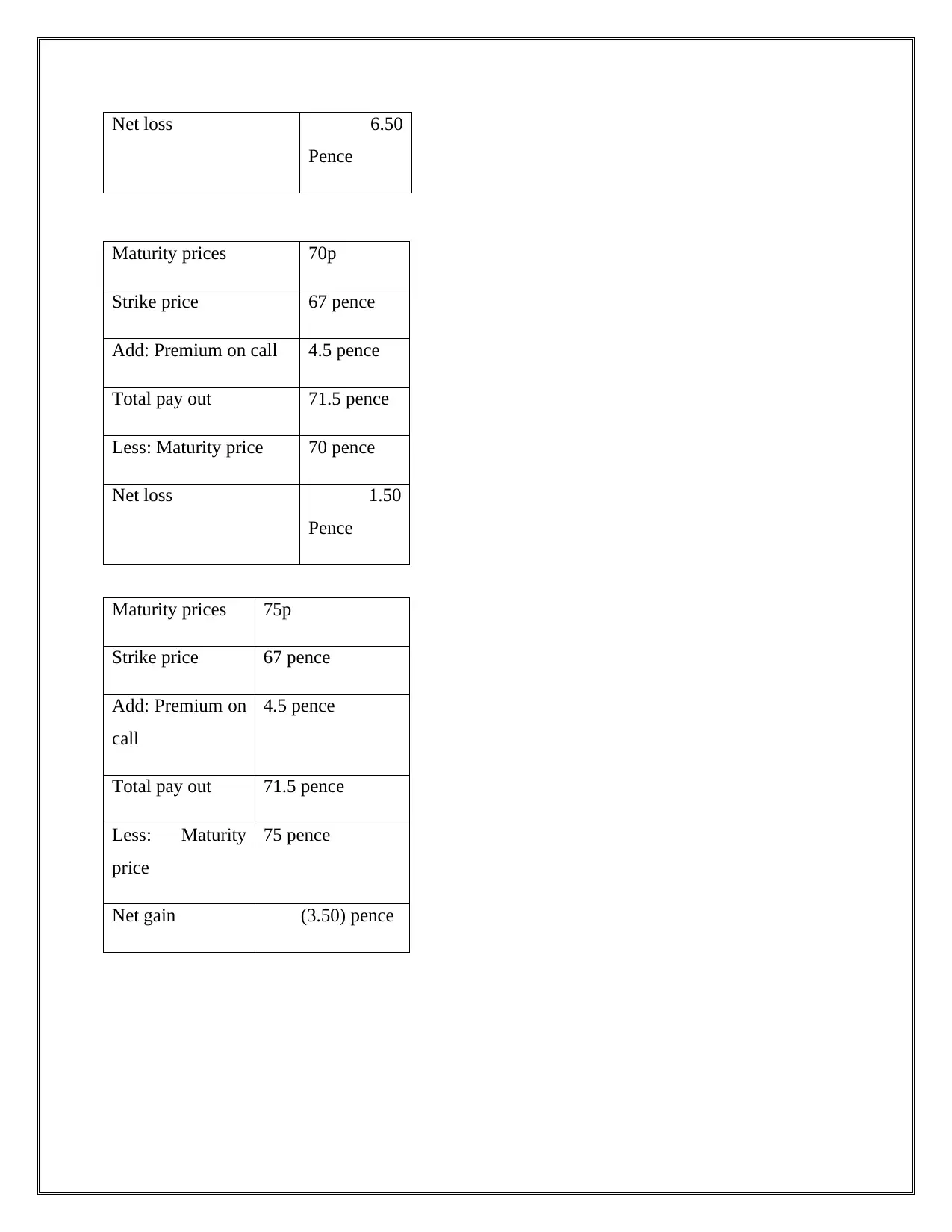

Maturity prices 65p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 65 pence

Net loss 6.50

Pence

Maturity prices 70p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 70 pence

Net loss 1.50

Pence

Maturity prices 75p

Strike price 67 pence

Add: Premium on

call

4.5 pence

Total pay out 71.5 pence

Less: Maturity

price

75 pence

Net gain (3.50) pence

Pence

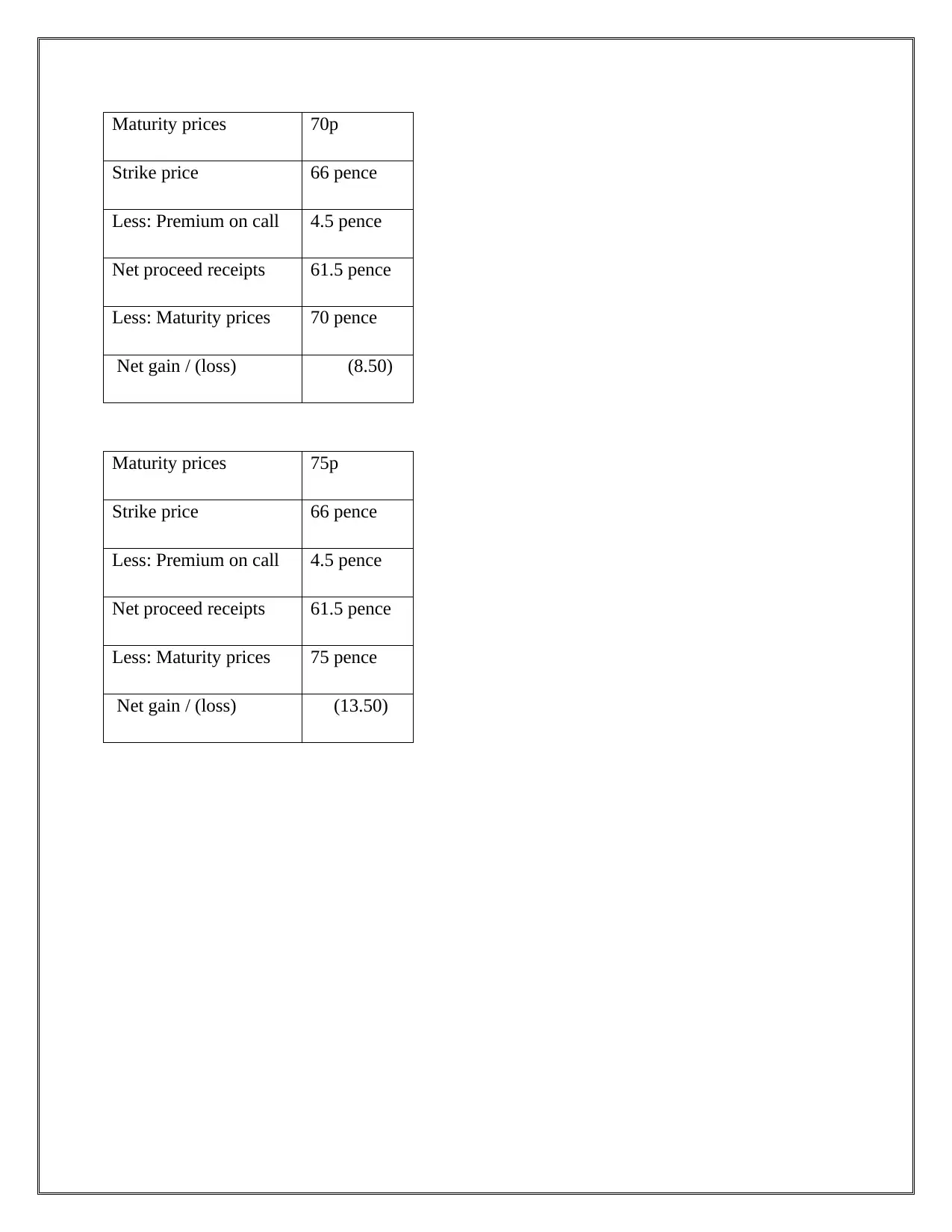

Maturity prices 70p

Strike price 67 pence

Add: Premium on call 4.5 pence

Total pay out 71.5 pence

Less: Maturity price 70 pence

Net loss 1.50

Pence

Maturity prices 75p

Strike price 67 pence

Add: Premium on

call

4.5 pence

Total pay out 71.5 pence

Less: Maturity

price

75 pence

Net gain (3.50) pence

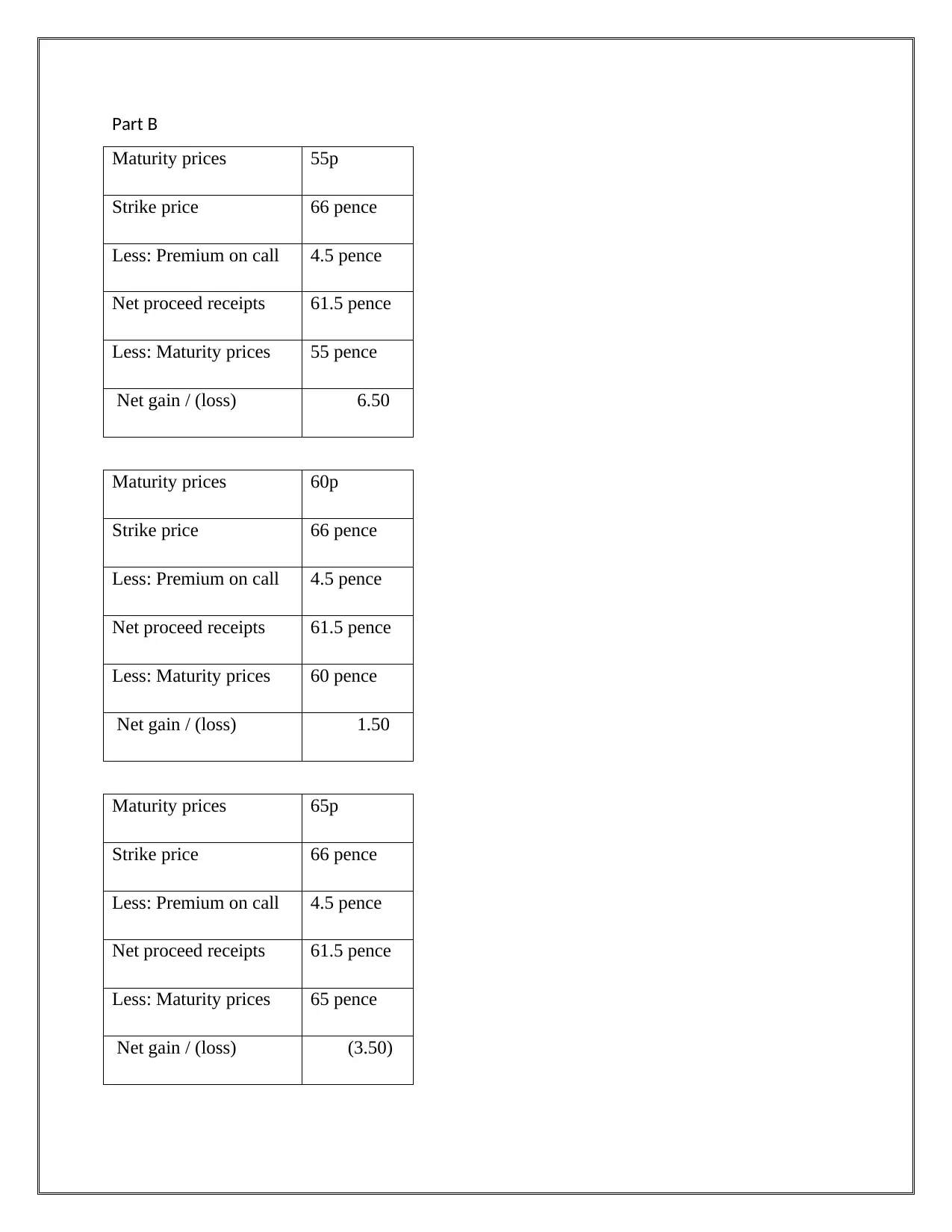

Part B

Maturity prices 55p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 55 pence

Net gain / (loss) 6.50

Maturity prices 60p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 60 pence

Net gain / (loss) 1.50

Maturity prices 65p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 65 pence

Net gain / (loss) (3.50)

Maturity prices 55p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 55 pence

Net gain / (loss) 6.50

Maturity prices 60p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 60 pence

Net gain / (loss) 1.50

Maturity prices 65p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 65 pence

Net gain / (loss) (3.50)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Maturity prices 70p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 70 pence

Net gain / (loss) (8.50)

Maturity prices 75p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 75 pence

Net gain / (loss) (13.50)

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 70 pence

Net gain / (loss) (8.50)

Maturity prices 75p

Strike price 66 pence

Less: Premium on call 4.5 pence

Net proceed receipts 61.5 pence

Less: Maturity prices 75 pence

Net gain / (loss) (13.50)

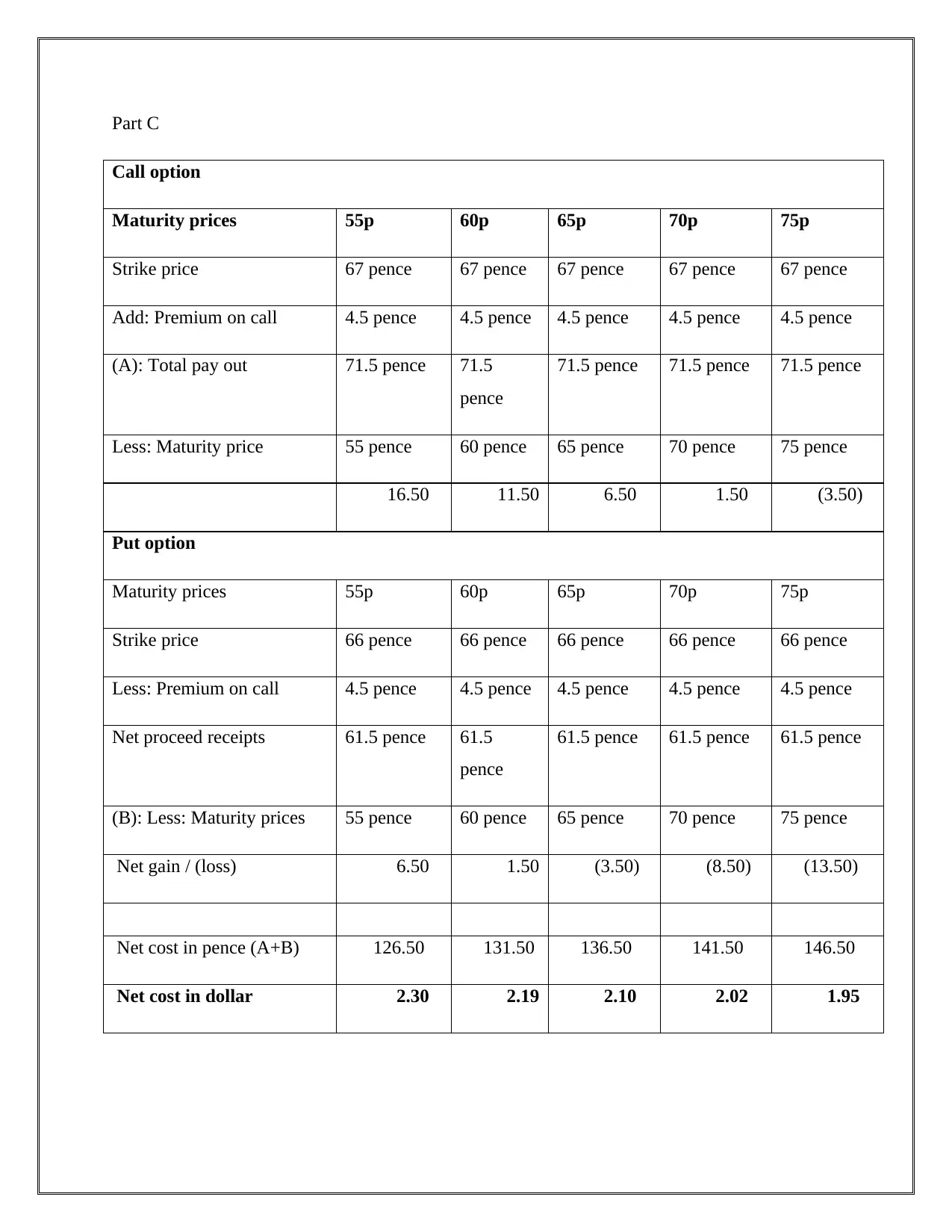

Part C

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5

pence

71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

16.50 11.50 6.50 1.50 (3.50)

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5

pence

61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity prices 55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

Net cost in pence (A+B) 126.50 131.50 136.50 141.50 146.50

Net cost in dollar 2.30 2.19 2.10 2.02 1.95

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5

pence

71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

16.50 11.50 6.50 1.50 (3.50)

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Net proceed receipts 61.5 pence 61.5

pence

61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity prices 55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

Net cost in pence (A+B) 126.50 131.50 136.50 141.50 146.50

Net cost in dollar 2.30 2.19 2.10 2.02 1.95

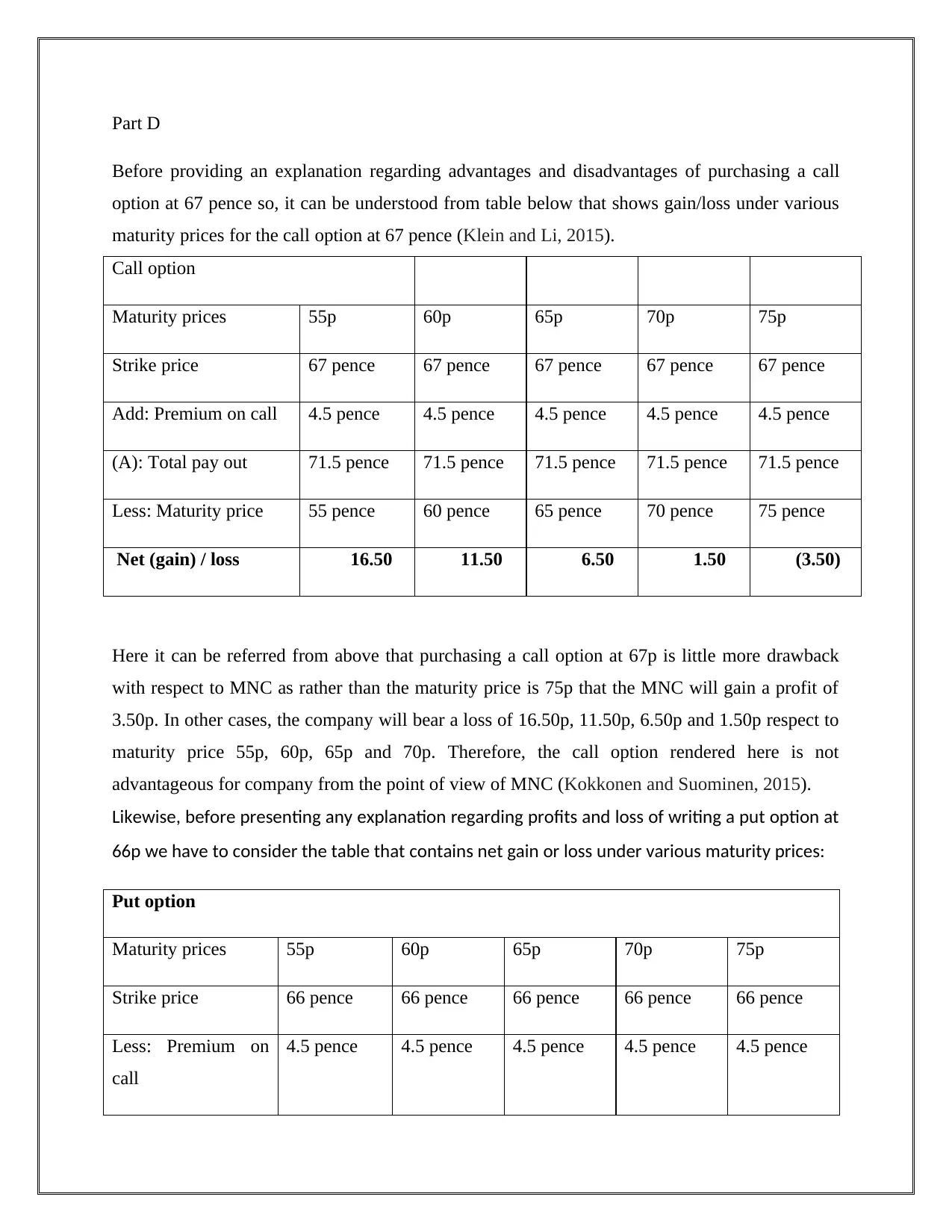

Part D

Before providing an explanation regarding advantages and disadvantages of purchasing a call

option at 67 pence so, it can be understood from table below that shows gain/loss under various

maturity prices for the call option at 67 pence (Klein and Li, 2015).

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5 pence 71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

Net (gain) / loss 16.50 11.50 6.50 1.50 (3.50)

Here it can be referred from above that purchasing a call option at 67p is little more drawback

with respect to MNC as rather than the maturity price is 75p that the MNC will gain a profit of

3.50p. In other cases, the company will bear a loss of 16.50p, 11.50p, 6.50p and 1.50p respect to

maturity price 55p, 60p, 65p and 70p. Therefore, the call option rendered here is not

advantageous for company from the point of view of MNC (Kokkonen and Suominen, 2015).

Likewise, before presenting any explanation regarding profits and loss of writing a put option at

66p we have to consider the table that contains net gain or loss under various maturity prices:

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on

call

4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Before providing an explanation regarding advantages and disadvantages of purchasing a call

option at 67 pence so, it can be understood from table below that shows gain/loss under various

maturity prices for the call option at 67 pence (Klein and Li, 2015).

Call option

Maturity prices 55p 60p 65p 70p 75p

Strike price 67 pence 67 pence 67 pence 67 pence 67 pence

Add: Premium on call 4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

(A): Total pay out 71.5 pence 71.5 pence 71.5 pence 71.5 pence 71.5 pence

Less: Maturity price 55 pence 60 pence 65 pence 70 pence 75 pence

Net (gain) / loss 16.50 11.50 6.50 1.50 (3.50)

Here it can be referred from above that purchasing a call option at 67p is little more drawback

with respect to MNC as rather than the maturity price is 75p that the MNC will gain a profit of

3.50p. In other cases, the company will bear a loss of 16.50p, 11.50p, 6.50p and 1.50p respect to

maturity price 55p, 60p, 65p and 70p. Therefore, the call option rendered here is not

advantageous for company from the point of view of MNC (Kokkonen and Suominen, 2015).

Likewise, before presenting any explanation regarding profits and loss of writing a put option at

66p we have to consider the table that contains net gain or loss under various maturity prices:

Put option

Maturity prices 55p 60p 65p 70p 75p

Strike price 66 pence 66 pence 66 pence 66 pence 66 pence

Less: Premium on

call

4.5 pence 4.5 pence 4.5 pence 4.5 pence 4.5 pence

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

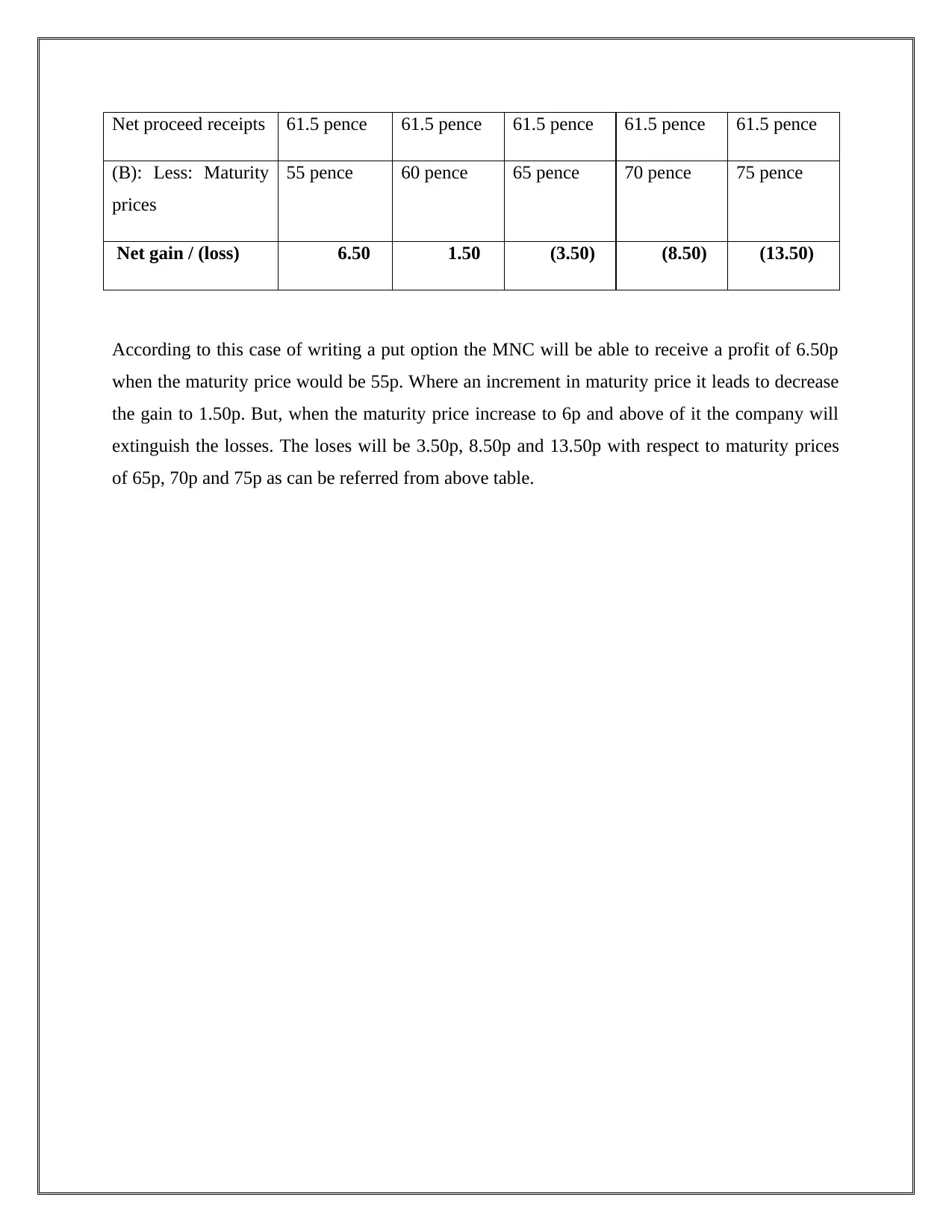

Net proceed receipts 61.5 pence 61.5 pence 61.5 pence 61.5 pence 61.5 pence

(B): Less: Maturity

prices

55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

According to this case of writing a put option the MNC will be able to receive a profit of 6.50p

when the maturity price would be 55p. Where an increment in maturity price it leads to decrease

the gain to 1.50p. But, when the maturity price increase to 6p and above of it the company will

extinguish the losses. The loses will be 3.50p, 8.50p and 13.50p with respect to maturity prices

of 65p, 70p and 75p as can be referred from above table.

(B): Less: Maturity

prices

55 pence 60 pence 65 pence 70 pence 75 pence

Net gain / (loss) 6.50 1.50 (3.50) (8.50) (13.50)

According to this case of writing a put option the MNC will be able to receive a profit of 6.50p

when the maturity price would be 55p. Where an increment in maturity price it leads to decrease

the gain to 1.50p. But, when the maturity price increase to 6p and above of it the company will

extinguish the losses. The loses will be 3.50p, 8.50p and 13.50p with respect to maturity prices

of 65p, 70p and 75p as can be referred from above table.

Answer 6

Part A

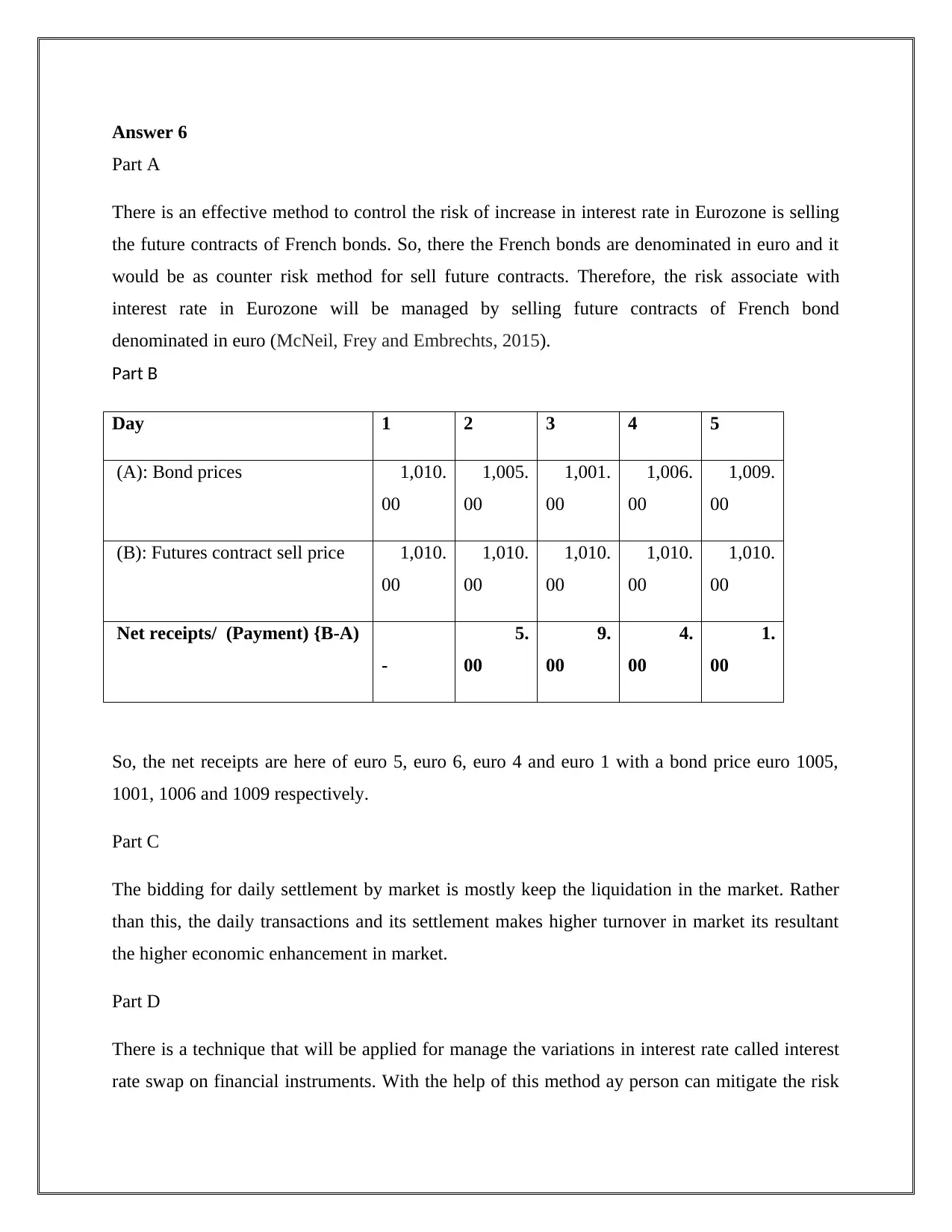

There is an effective method to control the risk of increase in interest rate in Eurozone is selling

the future contracts of French bonds. So, there the French bonds are denominated in euro and it

would be as counter risk method for sell future contracts. Therefore, the risk associate with

interest rate in Eurozone will be managed by selling future contracts of French bond

denominated in euro (McNeil, Frey and Embrechts, 2015).

Part B

Day 1 2 3 4 5

(A): Bond prices 1,010.

00

1,005.

00

1,001.

00

1,006.

00

1,009.

00

(B): Futures contract sell price 1,010.

00

1,010.

00

1,010.

00

1,010.

00

1,010.

00

Net receipts/ (Payment) {B-A)

-

5.

00

9.

00

4.

00

1.

00

So, the net receipts are here of euro 5, euro 6, euro 4 and euro 1 with a bond price euro 1005,

1001, 1006 and 1009 respectively.

Part C

The bidding for daily settlement by market is mostly keep the liquidation in the market. Rather

than this, the daily transactions and its settlement makes higher turnover in market its resultant

the higher economic enhancement in market.

Part D

There is a technique that will be applied for manage the variations in interest rate called interest

rate swap on financial instruments. With the help of this method ay person can mitigate the risk

Part A

There is an effective method to control the risk of increase in interest rate in Eurozone is selling

the future contracts of French bonds. So, there the French bonds are denominated in euro and it

would be as counter risk method for sell future contracts. Therefore, the risk associate with

interest rate in Eurozone will be managed by selling future contracts of French bond

denominated in euro (McNeil, Frey and Embrechts, 2015).

Part B

Day 1 2 3 4 5

(A): Bond prices 1,010.

00

1,005.

00

1,001.

00

1,006.

00

1,009.

00

(B): Futures contract sell price 1,010.

00

1,010.

00

1,010.

00

1,010.

00

1,010.

00

Net receipts/ (Payment) {B-A)

-

5.

00

9.

00

4.

00

1.

00

So, the net receipts are here of euro 5, euro 6, euro 4 and euro 1 with a bond price euro 1005,

1001, 1006 and 1009 respectively.

Part C

The bidding for daily settlement by market is mostly keep the liquidation in the market. Rather

than this, the daily transactions and its settlement makes higher turnover in market its resultant

the higher economic enhancement in market.

Part D

There is a technique that will be applied for manage the variations in interest rate called interest

rate swap on financial instruments. With the help of this method ay person can mitigate the risk

associate with borrowed fund as well as fund providing on loan to others. It is a very Useful and

effective risk management method to diminish the overall risk assimilated with interest rate of

various instrument.

Part E

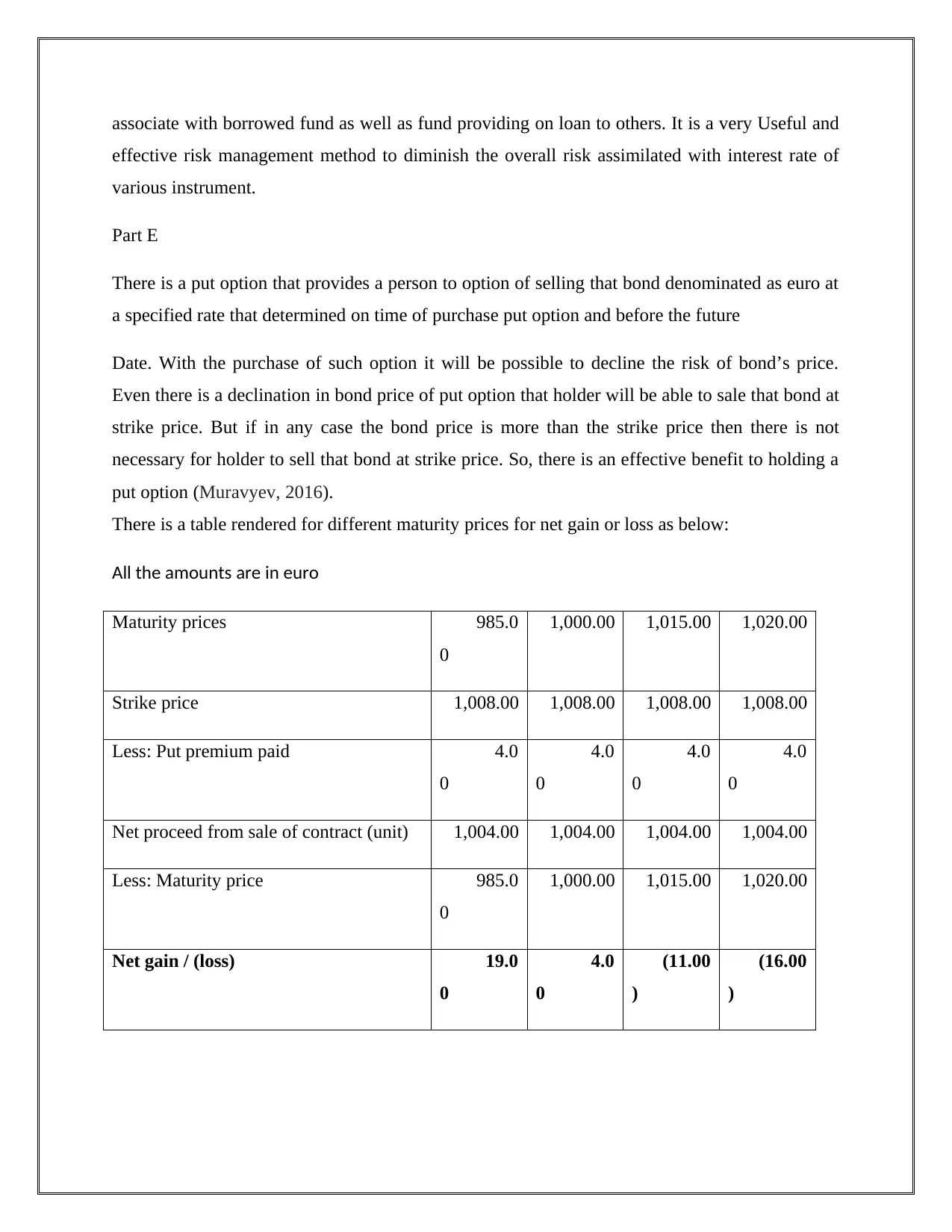

There is a put option that provides a person to option of selling that bond denominated as euro at

a specified rate that determined on time of purchase put option and before the future

Date. With the purchase of such option it will be possible to decline the risk of bond’s price.

Even there is a declination in bond price of put option that holder will be able to sale that bond at

strike price. But if in any case the bond price is more than the strike price then there is not

necessary for holder to sell that bond at strike price. So, there is an effective benefit to holding a

put option (Muravyev, 2016).

There is a table rendered for different maturity prices for net gain or loss as below:

All the amounts are in euro

Maturity prices 985.0

0

1,000.00 1,015.00 1,020.00

Strike price 1,008.00 1,008.00 1,008.00 1,008.00

Less: Put premium paid 4.0

0

4.0

0

4.0

0

4.0

0

Net proceed from sale of contract (unit) 1,004.00 1,004.00 1,004.00 1,004.00

Less: Maturity price 985.0

0

1,000.00 1,015.00 1,020.00

Net gain / (loss) 19.0

0

4.0

0

(11.00

)

(16.00

)

effective risk management method to diminish the overall risk assimilated with interest rate of

various instrument.

Part E

There is a put option that provides a person to option of selling that bond denominated as euro at

a specified rate that determined on time of purchase put option and before the future

Date. With the purchase of such option it will be possible to decline the risk of bond’s price.

Even there is a declination in bond price of put option that holder will be able to sale that bond at

strike price. But if in any case the bond price is more than the strike price then there is not

necessary for holder to sell that bond at strike price. So, there is an effective benefit to holding a

put option (Muravyev, 2016).

There is a table rendered for different maturity prices for net gain or loss as below:

All the amounts are in euro

Maturity prices 985.0

0

1,000.00 1,015.00 1,020.00

Strike price 1,008.00 1,008.00 1,008.00 1,008.00

Less: Put premium paid 4.0

0

4.0

0

4.0

0

4.0

0

Net proceed from sale of contract (unit) 1,004.00 1,004.00 1,004.00 1,004.00

Less: Maturity price 985.0

0

1,000.00 1,015.00 1,020.00

Net gain / (loss) 19.0

0

4.0

0

(11.00

)

(16.00

)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If the maturity prices would be 1015 and 1020 then the holder of put option shall not exercise the

option as it provides a huge loss but if there is no option is Using the loss will be occurred up to

the premium amount paid to purchase that option that is 4.00.

Part F

From above table it can be conclude that the holder of put option will be capable to apply the

arbitrage opportunity with the Using of put option if the price is below than the strike price.

Even, it is consider as right not an obligation there would be the estimated loss amount becomes

more than the premium paid for purchase that option so there Is not any chance to exercise the

option.

option as it provides a huge loss but if there is no option is Using the loss will be occurred up to

the premium amount paid to purchase that option that is 4.00.

Part F

From above table it can be conclude that the holder of put option will be capable to apply the

arbitrage opportunity with the Using of put option if the price is below than the strike price.

Even, it is consider as right not an obligation there would be the estimated loss amount becomes

more than the premium paid for purchase that option so there Is not any chance to exercise the

option.

References

Agarwal, V., Ruenzi, S. and Weigert, F., 2017. Tail risk in hedge funds: A unique view from

portfolio holdings. Journal of financial economics, 125(3), pp.610-636.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Brooke, M.Z., 2016. Handbook of international financial management. Springer.

Carr, P. and Wu, L., 2016. Analyzing volatility risk and risk premium in option contracts: A new

theory. Journal of Financial Economics, 120(1), pp.1-20.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management. Cengage

Learning.

Christoffersen, P., Goyenko, R., Jacobs, K. and Karoui, M., 2017. Illiquidity premia in the equity

options market. The Review of Financial Studies, 31(3), pp.811-851.

Cremers, M., Ferreira, M.A., Matos, P. and Starks, L., 2016. Indexing and active fund

management: International evidence. Journal of Financial Economics, 120(3), pp.539-560.

Davies, R.J., Kat, H.M. and Lu, S., 2016. Fund of hedge funds portfolio selection: A multiple-

objective approach. In Derivatives and Hedge Funds (pp. 45-71). Palgrave Macmillan, London.

Deresky, H., 2017. International management: Managing across borders and cultures. Pearson

Education India.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Grundy, B.D. and Verwijmeren, P., 2018. The buyers’ perspective on security design: Hedge

funds and convertible bond call provisions. Journal of Financial Economics, 127(1), pp.77-93.

Kelly, B., Lustig, H. and Van Nieuwerburgh, S., 2016. Too-systemic-to-fail: What option

markets imply about sector-wide government guarantees. American Economic Review, 106(6),

pp.1278-1319. Kelly, B., Lustig, H. and Van Nieuwerburgh, S., 2016. Too-systemic-to-fail:

What option markets imply about sector-wide government guarantees. American Economic

Review, 106(6), pp.1278-1319.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Klein, A. and Li, T., 2015. Acquiring and trading on complex information: How hedge funds use

the Freedom of Information Act.

Agarwal, V., Ruenzi, S. and Weigert, F., 2017. Tail risk in hedge funds: A unique view from

portfolio holdings. Journal of financial economics, 125(3), pp.610-636.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Brooke, M.Z., 2016. Handbook of international financial management. Springer.

Carr, P. and Wu, L., 2016. Analyzing volatility risk and risk premium in option contracts: A new

theory. Journal of Financial Economics, 120(1), pp.1-20.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management. Cengage

Learning.

Christoffersen, P., Goyenko, R., Jacobs, K. and Karoui, M., 2017. Illiquidity premia in the equity

options market. The Review of Financial Studies, 31(3), pp.811-851.

Cremers, M., Ferreira, M.A., Matos, P. and Starks, L., 2016. Indexing and active fund

management: International evidence. Journal of Financial Economics, 120(3), pp.539-560.

Davies, R.J., Kat, H.M. and Lu, S., 2016. Fund of hedge funds portfolio selection: A multiple-

objective approach. In Derivatives and Hedge Funds (pp. 45-71). Palgrave Macmillan, London.

Deresky, H., 2017. International management: Managing across borders and cultures. Pearson

Education India.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Grundy, B.D. and Verwijmeren, P., 2018. The buyers’ perspective on security design: Hedge

funds and convertible bond call provisions. Journal of Financial Economics, 127(1), pp.77-93.

Kelly, B., Lustig, H. and Van Nieuwerburgh, S., 2016. Too-systemic-to-fail: What option

markets imply about sector-wide government guarantees. American Economic Review, 106(6),

pp.1278-1319. Kelly, B., Lustig, H. and Van Nieuwerburgh, S., 2016. Too-systemic-to-fail:

What option markets imply about sector-wide government guarantees. American Economic

Review, 106(6), pp.1278-1319.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Klein, A. and Li, T., 2015. Acquiring and trading on complex information: How hedge funds use

the Freedom of Information Act.

Kokkonen, J. and Suominen, M., 2015. Hedge funds and stock market efficiency. Management

Science, 61(12), pp.2890-2904.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management.

Muravyev, D., 2016. Order flow and expected option returns. The Journal of Finance, 71(2),

pp.673-708.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Yin, C., 2016. The optimal size of hedge funds: conflict between investors and fund

managers. The Journal of Finance, 71(4), pp.1857-1894. Yin, C., 2016. The optimal size of hedge

funds: conflict between investors and fund managers. The Journal of Finance, 71(4), pp.1857-

1894.

Science, 61(12), pp.2890-2904.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management.

Muravyev, D., 2016. Order flow and expected option returns. The Journal of Finance, 71(2),

pp.673-708.

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

Yin, C., 2016. The optimal size of hedge funds: conflict between investors and fund

managers. The Journal of Finance, 71(4), pp.1857-1894. Yin, C., 2016. The optimal size of hedge

funds: conflict between investors and fund managers. The Journal of Finance, 71(4), pp.1857-

1894.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.