International Financial Management

Added on 2023-01-11

22 Pages4974 Words79 Views

International Financial Management

Name of the Student:

Name of the University:

Authors Note:

Name of the Student:

Name of the University:

Authors Note:

Contents

International financial management............................................................................3

Answer 1..........................................................................................................3

Answer 2............................................................................................................5

Answer 3............................................................................................................9

Answer 4..........................................................................................................10

Answer 5..........................................................................................................11

Answer 6..........................................................................................................18

References........................................................................................................21

International financial management............................................................................3

Answer 1..........................................................................................................3

Answer 2............................................................................................................5

Answer 3............................................................................................................9

Answer 4..........................................................................................................10

Answer 5..........................................................................................................11

Answer 6..........................................................................................................18

References........................................................................................................21

International financial management

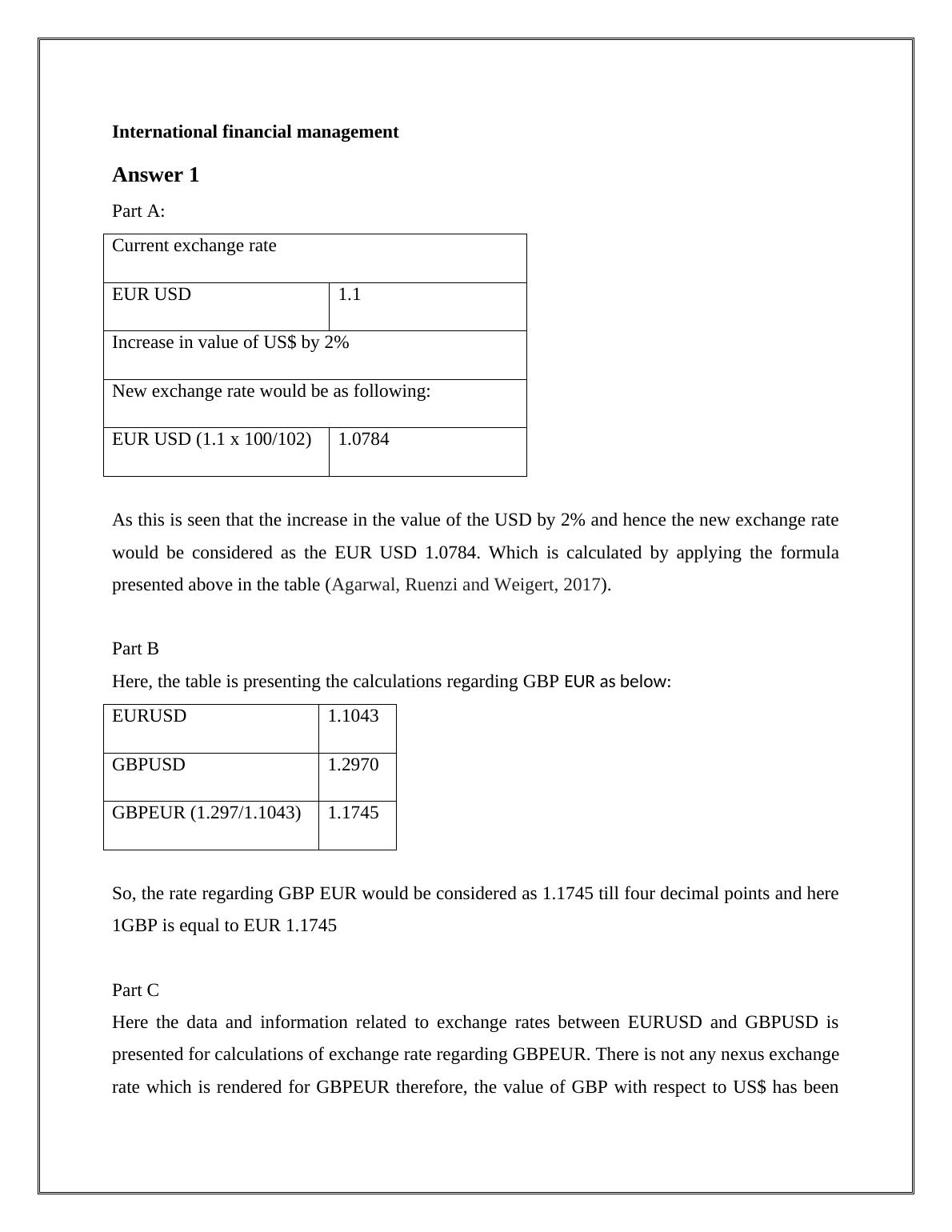

Answer 1

Part A:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

As this is seen that the increase in the value of the USD by 2% and hence the new exchange rate

would be considered as the EUR USD 1.0784. Which is calculated by applying the formula

presented above in the table (Agarwal, Ruenzi and Weigert, 2017).

Part B

Here, the table is presenting the calculations regarding GBP EUR as below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

So, the rate regarding GBP EUR would be considered as 1.1745 till four decimal points and here

1GBP is equal to EUR 1.1745

Part C

Here the data and information related to exchange rates between EURUSD and GBPUSD is

presented for calculations of exchange rate regarding GBPEUR. There is not any nexus exchange

rate which is rendered for GBPEUR therefore, the value of GBP with respect to US$ has been

Answer 1

Part A:

Current exchange rate

EUR USD 1.1

Increase in value of US$ by 2%

New exchange rate would be as following:

EUR USD (1.1 x 100/102) 1.0784

As this is seen that the increase in the value of the USD by 2% and hence the new exchange rate

would be considered as the EUR USD 1.0784. Which is calculated by applying the formula

presented above in the table (Agarwal, Ruenzi and Weigert, 2017).

Part B

Here, the table is presenting the calculations regarding GBP EUR as below:

EURUSD 1.1043

GBPUSD 1.2970

GBPEUR (1.297/1.1043) 1.1745

So, the rate regarding GBP EUR would be considered as 1.1745 till four decimal points and here

1GBP is equal to EUR 1.1745

Part C

Here the data and information related to exchange rates between EURUSD and GBPUSD is

presented for calculations of exchange rate regarding GBPEUR. There is not any nexus exchange

rate which is rendered for GBPEUR therefore, the value of GBP with respect to US$ has been

considered along with the value of US$ in respect to EUR (Bekaert and Hodrick, 2017). In

accordance with it, the exchange rate of GBREUR can be calculated with the help of value

regarding US$ against EUR and value regarding US$ against GBP with their comparison. Many

experts are using this technique for calculation of exchange rates between two countries and it is

the most popular method for this, helpful when there is no any direct exchange rate is presented

for two currencies. This case is providing as exchange rates between US$ and GBP, EUR and

US$. Even, the exchange rates between GBP and EUR is not rendered so the comparison of

these values regarding US$ against GBP and also against EUR so on the exchange rate of

GBPEUR can be calculated.

Triangular arbitrage is referred as a profit calculated from arbitration of various currencies due to

the variations in three kind of currencies. In the presented case the value regarding US$ to EUR

and US$ to GBP can be applied for determined the earnings from triangular arbitrage. For an

instance if at present US$ to purchase EUR has been invested and after some time received as

GBP in return of EUR. In this situation it rendered a maximum amount of profit to any investor

will be named as triangular arbitrage (Brooke, 2016). There is a complete understanding with

differences of exchange rate and capability of predicting the variations in different currencies

rendered as golden opportunity to investors to make surplus through arbitration.

accordance with it, the exchange rate of GBREUR can be calculated with the help of value

regarding US$ against EUR and value regarding US$ against GBP with their comparison. Many

experts are using this technique for calculation of exchange rates between two countries and it is

the most popular method for this, helpful when there is no any direct exchange rate is presented

for two currencies. This case is providing as exchange rates between US$ and GBP, EUR and

US$. Even, the exchange rates between GBP and EUR is not rendered so the comparison of

these values regarding US$ against GBP and also against EUR so on the exchange rate of

GBPEUR can be calculated.

Triangular arbitrage is referred as a profit calculated from arbitration of various currencies due to

the variations in three kind of currencies. In the presented case the value regarding US$ to EUR

and US$ to GBP can be applied for determined the earnings from triangular arbitrage. For an

instance if at present US$ to purchase EUR has been invested and after some time received as

GBP in return of EUR. In this situation it rendered a maximum amount of profit to any investor

will be named as triangular arbitrage (Brooke, 2016). There is a complete understanding with

differences of exchange rate and capability of predicting the variations in different currencies

rendered as golden opportunity to investors to make surplus through arbitration.

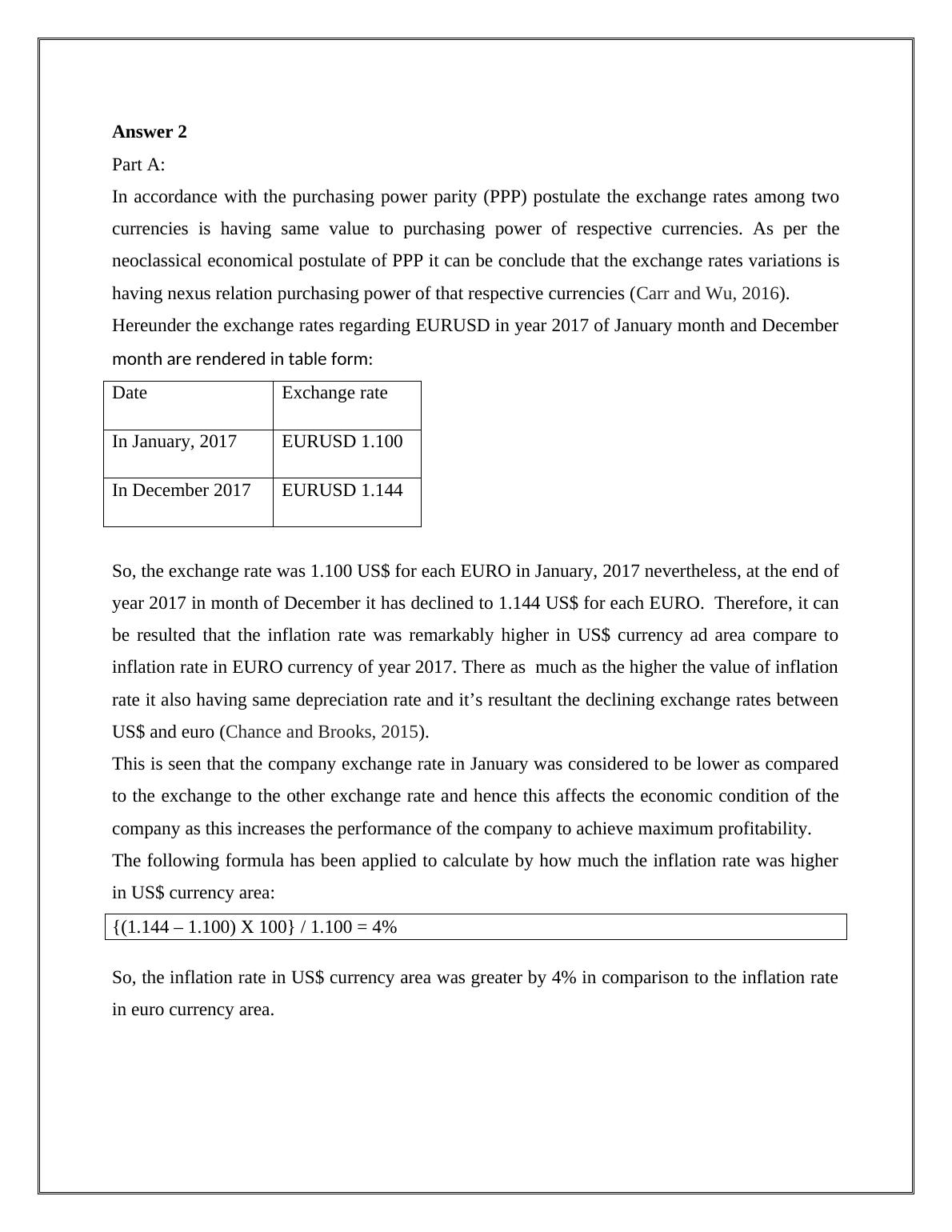

Answer 2

Part A:

In accordance with the purchasing power parity (PPP) postulate the exchange rates among two

currencies is having same value to purchasing power of respective currencies. As per the

neoclassical economical postulate of PPP it can be conclude that the exchange rates variations is

having nexus relation purchasing power of that respective currencies (Carr and Wu, 2016).

Hereunder the exchange rates regarding EURUSD in year 2017 of January month and December

month are rendered in table form:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, the exchange rate was 1.100 US$ for each EURO in January, 2017 nevertheless, at the end of

year 2017 in month of December it has declined to 1.144 US$ for each EURO. Therefore, it can

be resulted that the inflation rate was remarkably higher in US$ currency ad area compare to

inflation rate in EURO currency of year 2017. There as much as the higher the value of inflation

rate it also having same depreciation rate and it’s resultant the declining exchange rates between

US$ and euro (Chance and Brooks, 2015).

This is seen that the company exchange rate in January was considered to be lower as compared

to the exchange to the other exchange rate and hence this affects the economic condition of the

company as this increases the performance of the company to achieve maximum profitability.

The following formula has been applied to calculate by how much the inflation rate was higher

in US$ currency area:

{(1.144 – 1.100) X 100} / 1.100 = 4%

So, the inflation rate in US$ currency area was greater by 4% in comparison to the inflation rate

in euro currency area.

Part A:

In accordance with the purchasing power parity (PPP) postulate the exchange rates among two

currencies is having same value to purchasing power of respective currencies. As per the

neoclassical economical postulate of PPP it can be conclude that the exchange rates variations is

having nexus relation purchasing power of that respective currencies (Carr and Wu, 2016).

Hereunder the exchange rates regarding EURUSD in year 2017 of January month and December

month are rendered in table form:

Date Exchange rate

In January, 2017 EURUSD 1.100

In December 2017 EURUSD 1.144

So, the exchange rate was 1.100 US$ for each EURO in January, 2017 nevertheless, at the end of

year 2017 in month of December it has declined to 1.144 US$ for each EURO. Therefore, it can

be resulted that the inflation rate was remarkably higher in US$ currency ad area compare to

inflation rate in EURO currency of year 2017. There as much as the higher the value of inflation

rate it also having same depreciation rate and it’s resultant the declining exchange rates between

US$ and euro (Chance and Brooks, 2015).

This is seen that the company exchange rate in January was considered to be lower as compared

to the exchange to the other exchange rate and hence this affects the economic condition of the

company as this increases the performance of the company to achieve maximum profitability.

The following formula has been applied to calculate by how much the inflation rate was higher

in US$ currency area:

{(1.144 – 1.100) X 100} / 1.100 = 4%

So, the inflation rate in US$ currency area was greater by 4% in comparison to the inflation rate

in euro currency area.

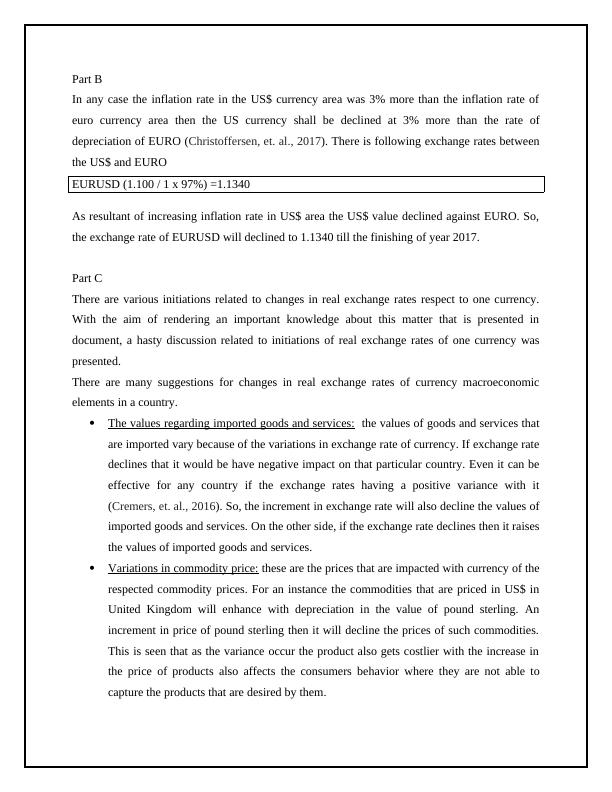

Part B

In any case the inflation rate in the US$ currency area was 3% more than the inflation rate of

euro currency area then the US currency shall be declined at 3% more than the rate of

depreciation of EURO (Christoffersen, et. al., 2017). There is following exchange rates between

the US$ and EURO

EURUSD (1.100 / 1 x 97%) =1.1340

As resultant of increasing inflation rate in US$ area the US$ value declined against EURO. So,

the exchange rate of EURUSD will declined to 1.1340 till the finishing of year 2017.

Part C

There are various initiations related to changes in real exchange rates respect to one currency.

With the aim of rendering an important knowledge about this matter that is presented in

document, a hasty discussion related to initiations of real exchange rates of one currency was

presented.

There are many suggestions for changes in real exchange rates of currency macroeconomic

elements in a country.

The values regarding imported goods and services: the values of goods and services that

are imported vary because of the variations in exchange rate of currency. If exchange rate

declines that it would be have negative impact on that particular country. Even it can be

effective for any country if the exchange rates having a positive variance with it

(Cremers, et. al., 2016). So, the increment in exchange rate will also decline the values of

imported goods and services. On the other side, if the exchange rate declines then it raises

the values of imported goods and services.

Variations in commodity price: these are the prices that are impacted with currency of the

respected commodity prices. For an instance the commodities that are priced in US$ in

United Kingdom will enhance with depreciation in the value of pound sterling. An

increment in price of pound sterling then it will decline the prices of such commodities.

This is seen that as the variance occur the product also gets costlier with the increase in

the price of products also affects the consumers behavior where they are not able to

capture the products that are desired by them.

In any case the inflation rate in the US$ currency area was 3% more than the inflation rate of

euro currency area then the US currency shall be declined at 3% more than the rate of

depreciation of EURO (Christoffersen, et. al., 2017). There is following exchange rates between

the US$ and EURO

EURUSD (1.100 / 1 x 97%) =1.1340

As resultant of increasing inflation rate in US$ area the US$ value declined against EURO. So,

the exchange rate of EURUSD will declined to 1.1340 till the finishing of year 2017.

Part C

There are various initiations related to changes in real exchange rates respect to one currency.

With the aim of rendering an important knowledge about this matter that is presented in

document, a hasty discussion related to initiations of real exchange rates of one currency was

presented.

There are many suggestions for changes in real exchange rates of currency macroeconomic

elements in a country.

The values regarding imported goods and services: the values of goods and services that

are imported vary because of the variations in exchange rate of currency. If exchange rate

declines that it would be have negative impact on that particular country. Even it can be

effective for any country if the exchange rates having a positive variance with it

(Cremers, et. al., 2016). So, the increment in exchange rate will also decline the values of

imported goods and services. On the other side, if the exchange rate declines then it raises

the values of imported goods and services.

Variations in commodity price: these are the prices that are impacted with currency of the

respected commodity prices. For an instance the commodities that are priced in US$ in

United Kingdom will enhance with depreciation in the value of pound sterling. An

increment in price of pound sterling then it will decline the prices of such commodities.

This is seen that as the variance occur the product also gets costlier with the increase in

the price of products also affects the consumers behavior where they are not able to

capture the products that are desired by them.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

International Financial Management PDFlg...

|20

|4488

|61

International Finance Problems with Solutions 2022lg...

|17

|4372

|23

Reports Of International Financial Managementlg...

|13

|2972

|22

International Financial Management: Exchange Rates, Triangular Arbitrage, Purchasing Power Parity, and Country Risk Analysislg...

|15

|3822

|316

International Financial Management .lg...

|14

|3403

|161

International Financial Managementlg...

|13

|3863

|81