International Finance Management Assignment - Finance [Course Code]

VerifiedAdded on 2022/12/15

|15

|2586

|238

Homework Assignment

AI Summary

This assignment solution delves into international finance management, addressing key aspects of financial decision-making. It begins with an introduction to financial management methods, emphasizing their relevance in investment decisions and wealth management. Question 1 calculates the expected Net Present Value (NPV) and standard deviation of a two-year project, evaluating its profitability. Question 2 analyzes RJW plc's potential investment in lignite mines, calculating NPV under optimistic, pessimistic, and expected scenarios, along with the standard deviation of NPV and the probability of liquidation. Question 3 evaluates four projects using the NPV technique, ranking them based on their NPVs and allocating funds for optimal returns. Additionally, it compares the NPV and Internal Rate of Return (IRR) methods and analyzes a trial license scenario to determine the best investment strategy.

INTERNATIONAL FINANCE

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Question: 1...................................................................................................................................3

Question 2....................................................................................................................................5

Question 3....................................................................................................................................8

a) Calculation of Net Present Value of four projects...................................................................8

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value............................................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Question: 1...................................................................................................................................3

Question 2....................................................................................................................................5

Question 3....................................................................................................................................8

a) Calculation of Net Present Value of four projects...................................................................8

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value............................................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The file is on international finance management. It talks about the financial management

methods which can be of help for the company’s investment decisions and management of

wealth in the right direction. It speaks about the company’s choice of taking the best investment

decision and talks of the business objectives of company and the decision of how the company is

using the financial resources of the company. The relevance of these methods has been shown

with calculation and interpretation has been done.

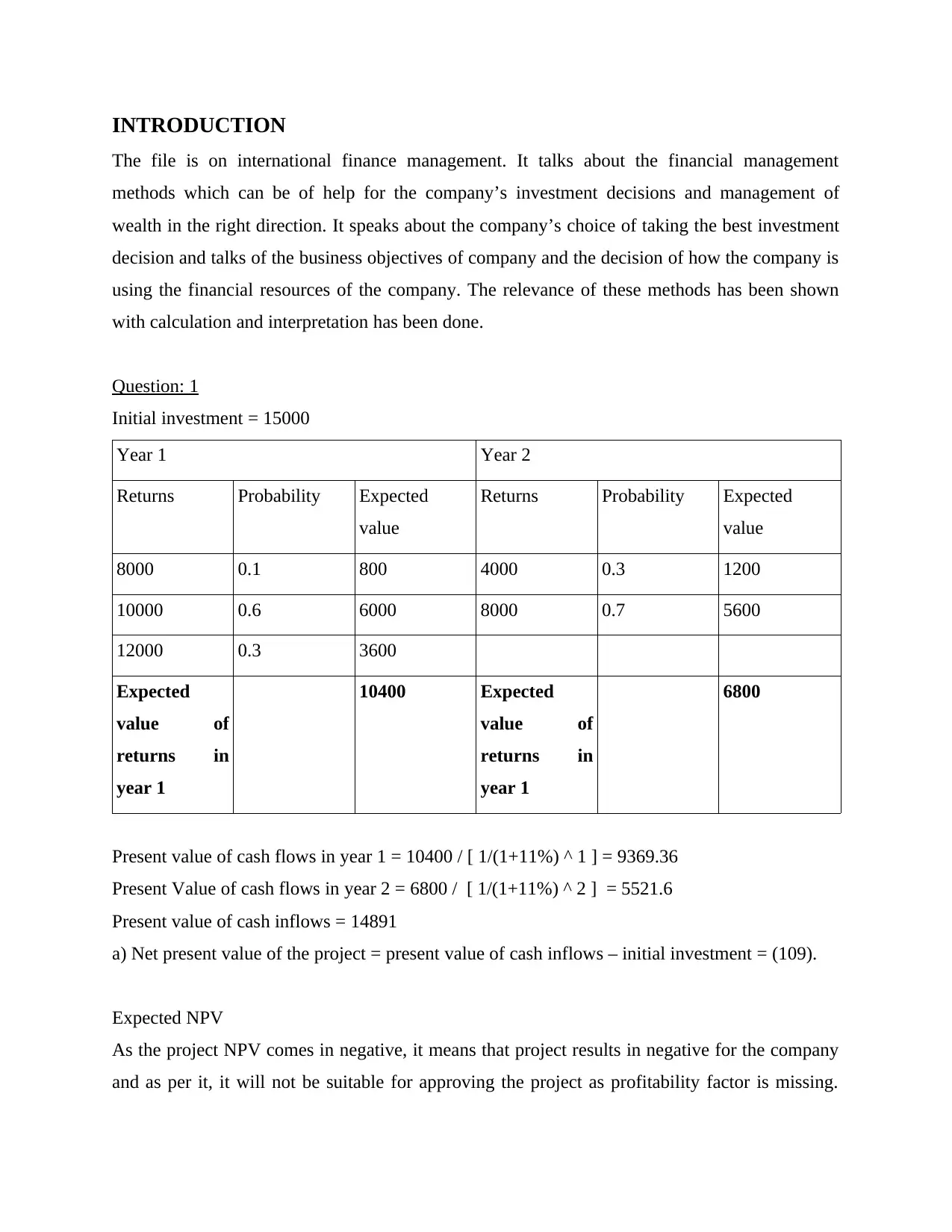

Question: 1

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

Present Value of cash flows in year 2 = 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Present value of cash inflows = 14891

a) Net present value of the project = present value of cash inflows – initial investment = (109).

Expected NPV

As the project NPV comes in negative, it means that project results in negative for the company

and as per it, it will not be suitable for approving the project as profitability factor is missing.

The file is on international finance management. It talks about the financial management

methods which can be of help for the company’s investment decisions and management of

wealth in the right direction. It speaks about the company’s choice of taking the best investment

decision and talks of the business objectives of company and the decision of how the company is

using the financial resources of the company. The relevance of these methods has been shown

with calculation and interpretation has been done.

Question: 1

Initial investment = 15000

Year 1 Year 2

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 1

6800

Present value of cash flows in year 1 = 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

Present Value of cash flows in year 2 = 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Present value of cash inflows = 14891

a) Net present value of the project = present value of cash inflows – initial investment = (109).

Expected NPV

As the project NPV comes in negative, it means that project results in negative for the company

and as per it, it will not be suitable for approving the project as profitability factor is missing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reason behind negative NPV is prominent reduction in value expected of returns which are

derived from project being compared to year 1. The project which is existing does not allow the

business for gaining the capital value as it invests against the project respective. In context of

each project it is necessary that the business gets more value than invested (Zore and et.al.,

2018). The rule which is present and acceptable is that total inflow in future as against the project

should be more than the total investment company is incurring about the project.

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of σ2 = σ = 1200.

By calculation of standard deviation, different scenarios of cash flows possible from project of

year 1, the value is coming out to be 1200, indicating that different events which are related of

cash flow deviate from return expected of project in year 1 by 1200.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

derived from project being compared to year 1. The project which is existing does not allow the

business for gaining the capital value as it invests against the project respective. In context of

each project it is necessary that the business gets more value than invested (Zore and et.al.,

2018). The rule which is present and acceptable is that total inflow in future as against the project

should be more than the total investment company is incurring about the project.

b) The standard deviation of NPV

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2 1440000

Standard deviation of returns in year 1 = square root of σ2 = σ = 1200.

By calculation of standard deviation, different scenarios of cash flows possible from project of

year 1, the value is coming out to be 1200, indicating that different events which are related of

cash flow deviate from return expected of project in year 1 by 1200.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2 3360000

Standard deviation of returns in year 2 = square root of σ2 = σ 1833

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

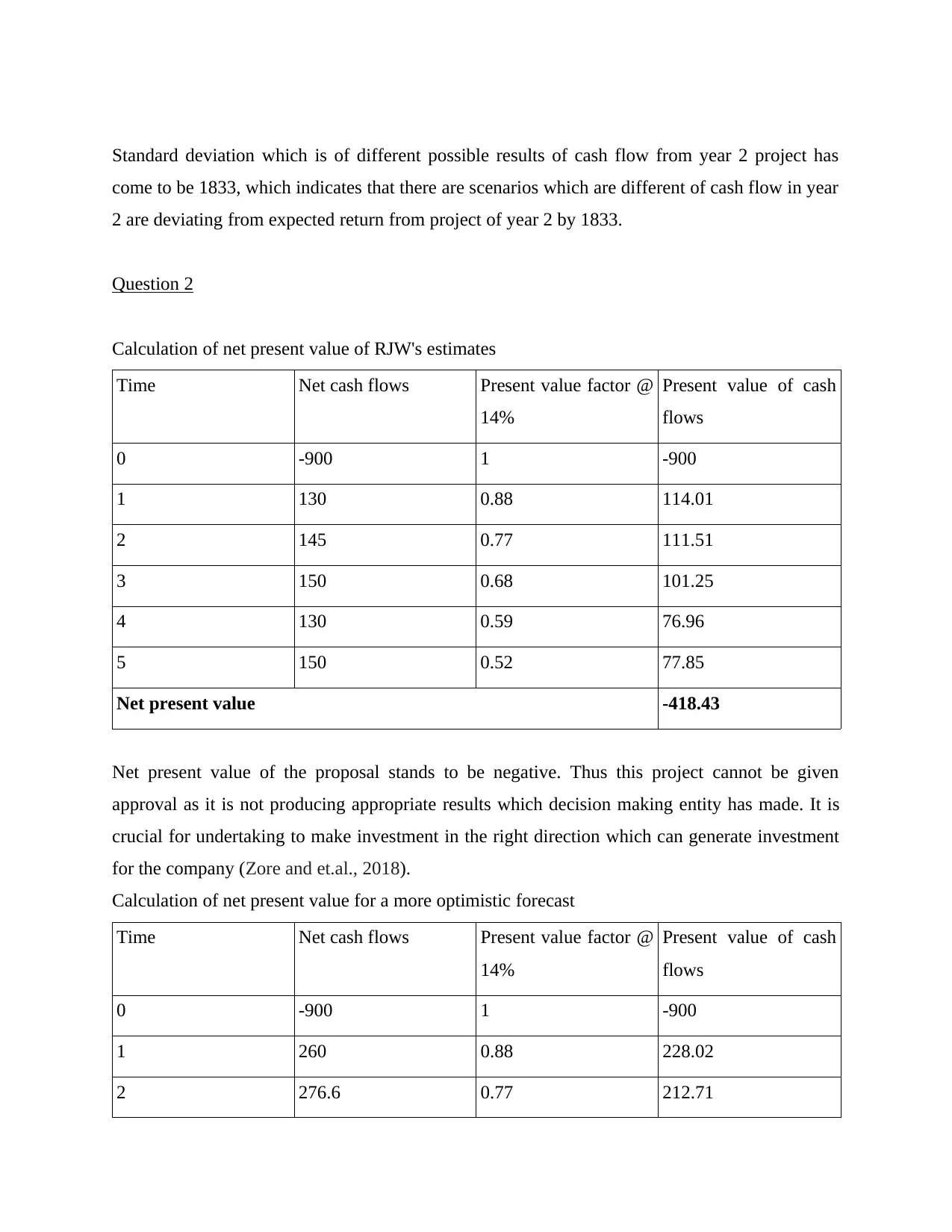

Standard deviation which is of different possible results of cash flow from year 2 project has

come to be 1833, which indicates that there are scenarios which are different of cash flow in year

2 are deviating from expected return from project of year 2 by 1833.

Question 2

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

Net present value of the proposal stands to be negative. Thus this project cannot be given

approval as it is not producing appropriate results which decision making entity has made. It is

crucial for undertaking to make investment in the right direction which can generate investment

for the company (Zore and et.al., 2018).

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

come to be 1833, which indicates that there are scenarios which are different of cash flow in year

2 are deviating from expected return from project of year 2 by 1833.

Question 2

Calculation of net present value of RJW's estimates

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net present value -418.43

Net present value of the proposal stands to be negative. Thus this project cannot be given

approval as it is not producing appropriate results which decision making entity has made. It is

crucial for undertaking to make investment in the right direction which can generate investment

for the company (Zore and et.al., 2018).

Calculation of net present value for a more optimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

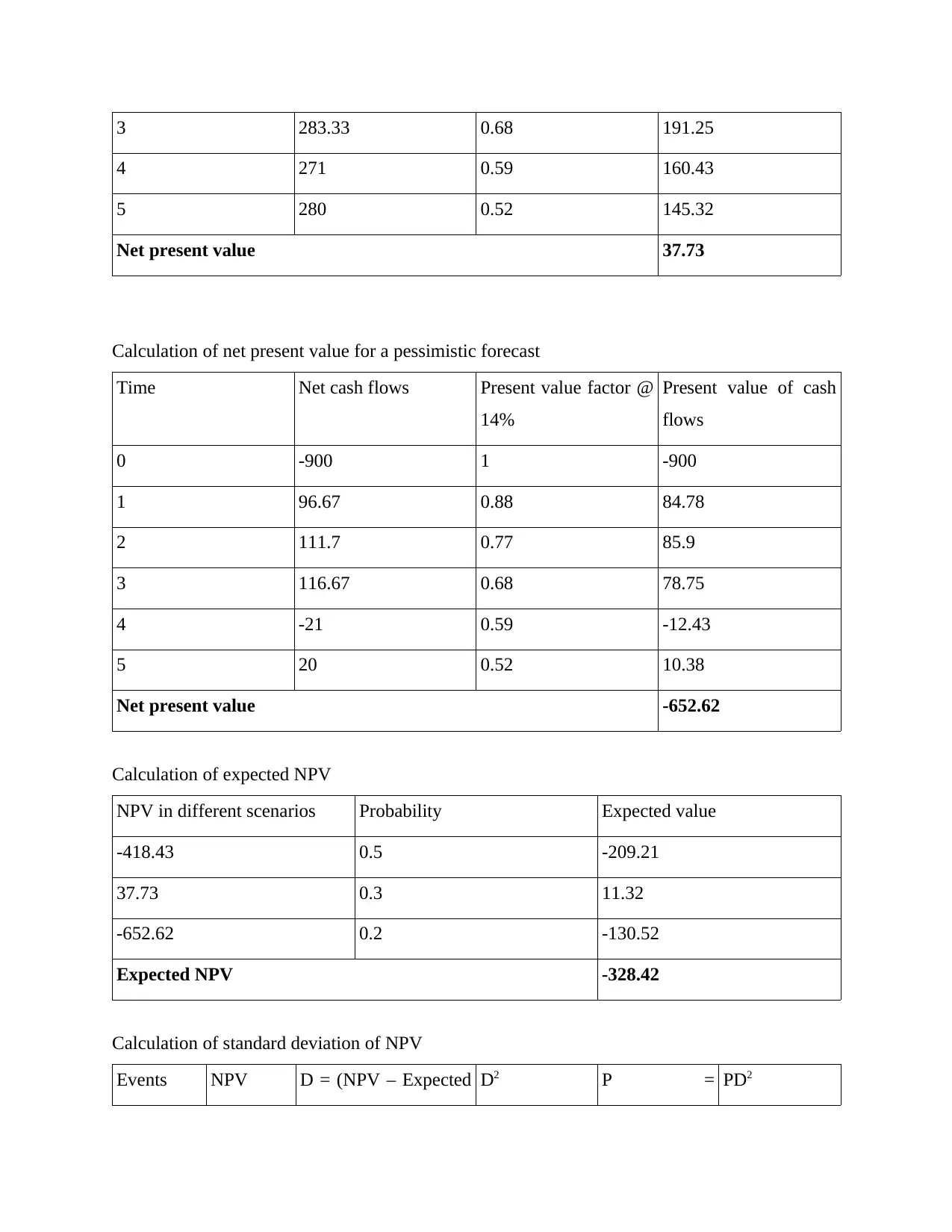

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

Calculation of expected NPV

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected D2 P = PD2

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

Calculation of net present value for a pessimistic forecast

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 96.67 0.88 84.78

2 111.7 0.77 85.9

3 116.67 0.68 78.75

4 -21 0.59 -12.43

5 20 0.52 10.38

Net present value -652.62

Calculation of expected NPV

NPV in different scenarios Probability Expected value

-418.43 0.5 -209.21

37.73 0.3 11.32

-652.62 0.2 -130.52

Expected NPV -328.42

Calculation of standard deviation of NPV

Events NPV D = (NPV – Expected D2 P = PD2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

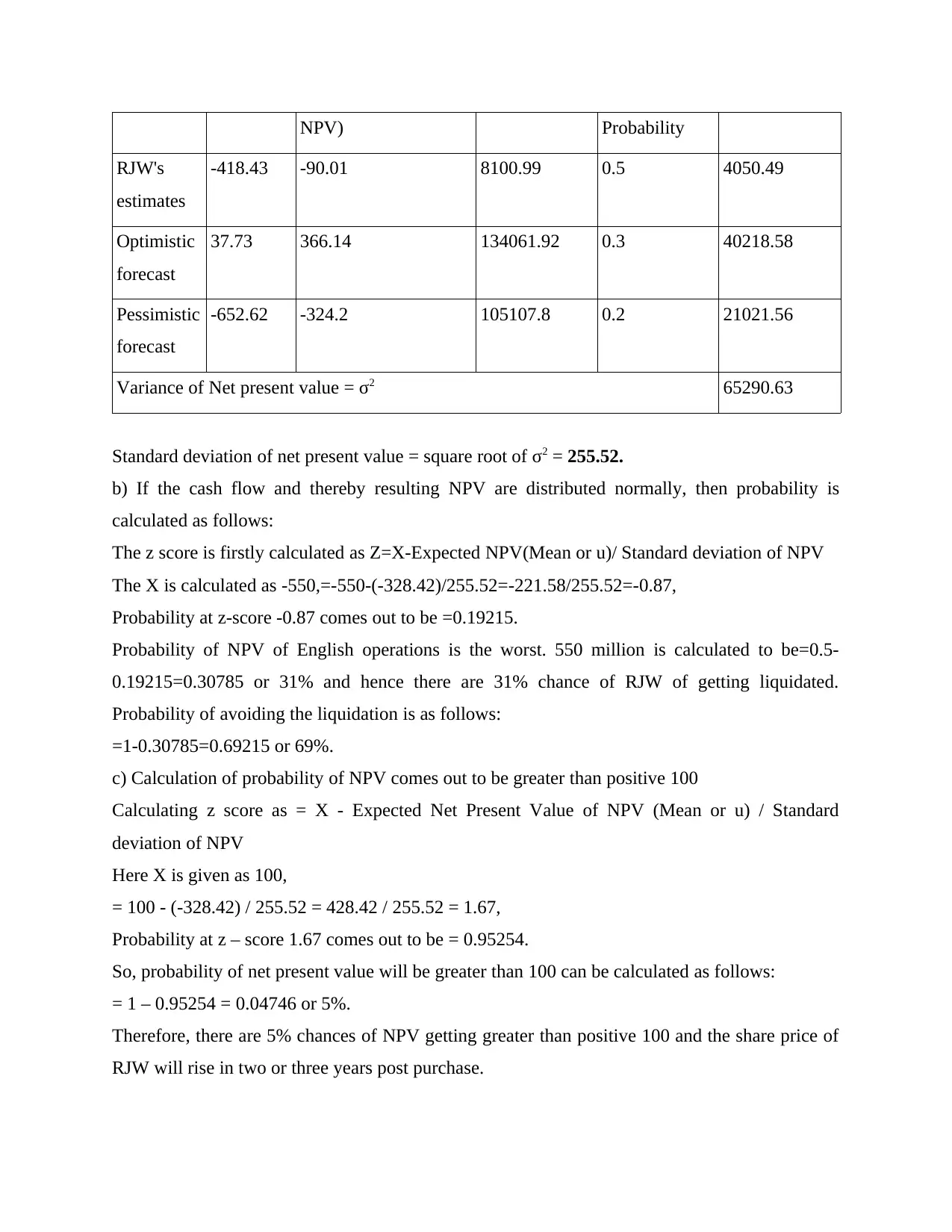

NPV) Probability

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) If the cash flow and thereby resulting NPV are distributed normally, then probability is

calculated as follows:

The z score is firstly calculated as Z=X-Expected NPV(Mean or u)/ Standard deviation of NPV

The X is calculated as -550,=-550-(-328.42)/255.52=-221.58/255.52=-0.87,

Probability at z-score -0.87 comes out to be =0.19215.

Probability of NPV of English operations is the worst. 550 million is calculated to be=0.5-

0.19215=0.30785 or 31% and hence there are 31% chance of RJW of getting liquidated.

Probability of avoiding the liquidation is as follows:

=1-0.30785=0.69215 or 69%.

c) Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, there are 5% chances of NPV getting greater than positive 100 and the share price of

RJW will rise in two or three years post purchase.

RJW's

estimates

-418.43 -90.01 8100.99 0.5 4050.49

Optimistic

forecast

37.73 366.14 134061.92 0.3 40218.58

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2 21021.56

Variance of Net present value = σ2 65290.63

Standard deviation of net present value = square root of σ2 = 255.52.

b) If the cash flow and thereby resulting NPV are distributed normally, then probability is

calculated as follows:

The z score is firstly calculated as Z=X-Expected NPV(Mean or u)/ Standard deviation of NPV

The X is calculated as -550,=-550-(-328.42)/255.52=-221.58/255.52=-0.87,

Probability at z-score -0.87 comes out to be =0.19215.

Probability of NPV of English operations is the worst. 550 million is calculated to be=0.5-

0.19215=0.30785 or 31% and hence there are 31% chance of RJW of getting liquidated.

Probability of avoiding the liquidation is as follows:

=1-0.30785=0.69215 or 69%.

c) Calculation of probability of NPV comes out to be greater than positive 100

Calculating z score as = X - Expected Net Present Value of NPV (Mean or u) / Standard

deviation of NPV

Here X is given as 100,

= 100 - (-328.42) / 255.52 = 428.42 / 255.52 = 1.67,

Probability at z – score 1.67 comes out to be = 0.95254.

So, probability of net present value will be greater than 100 can be calculated as follows:

= 1 – 0.95254 = 0.04746 or 5%.

Therefore, there are 5% chances of NPV getting greater than positive 100 and the share price of

RJW will rise in two or three years post purchase.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

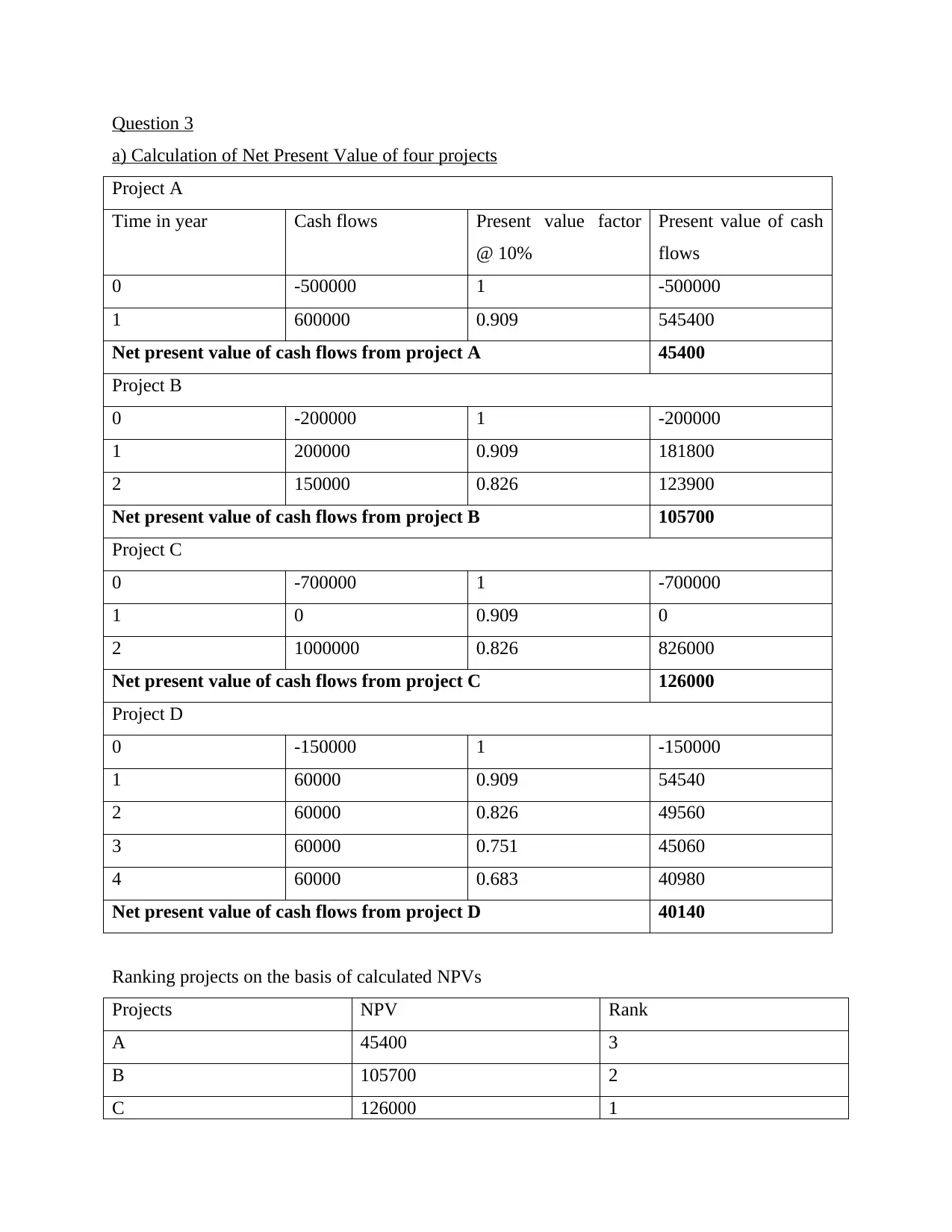

Question 3

a) Calculation of Net Present Value of four projects

Project A

Time in year Cash flows Present value factor

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

Net present value of cash flows from project B 105700

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

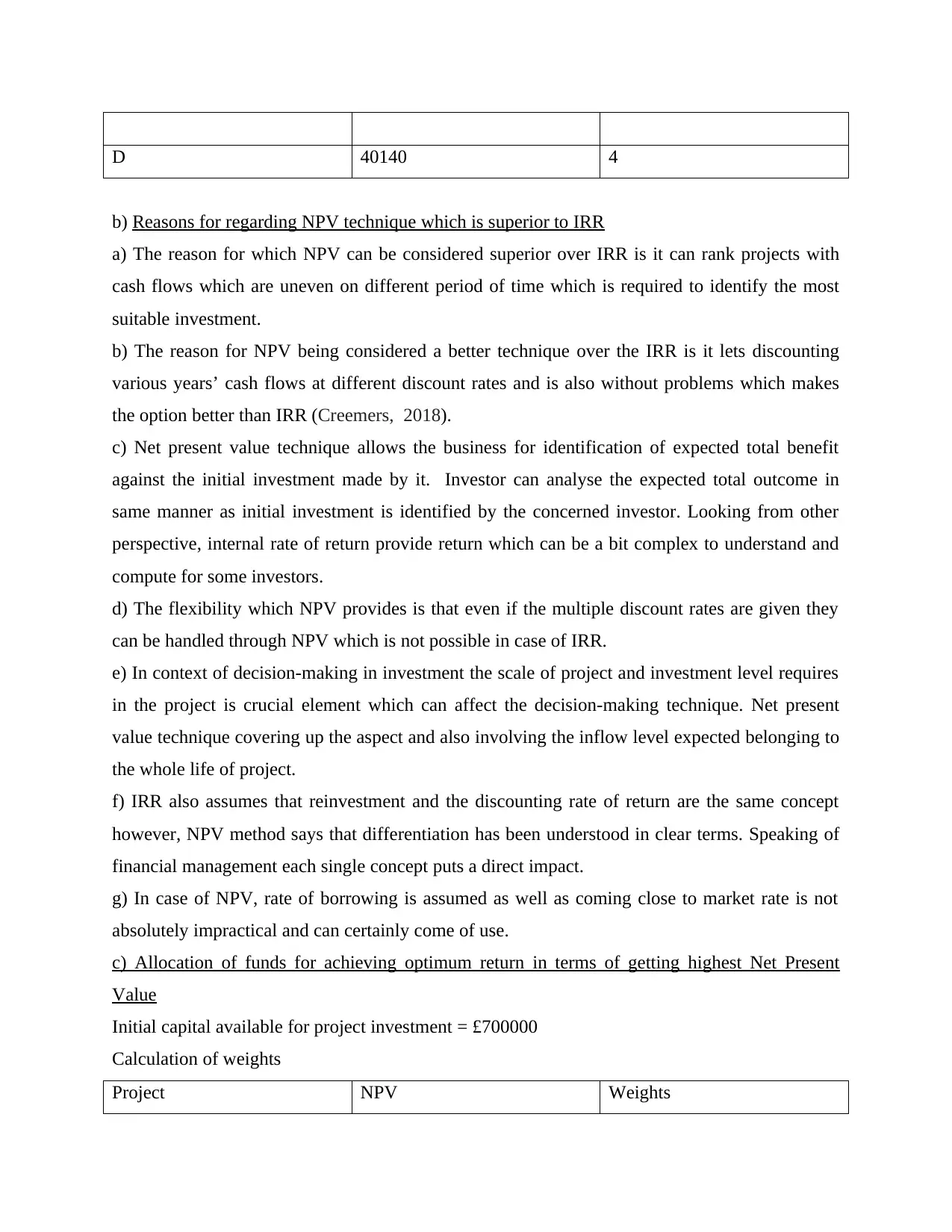

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

a) Calculation of Net Present Value of four projects

Project A

Time in year Cash flows Present value factor

@ 10%

Present value of cash

flows

0 -500000 1 -500000

1 600000 0.909 545400

Net present value of cash flows from project A 45400

Project B

0 -200000 1 -200000

1 200000 0.909 181800

2 150000 0.826 123900

Net present value of cash flows from project B 105700

Project C

0 -700000 1 -700000

1 0 0.909 0

2 1000000 0.826 826000

Net present value of cash flows from project C 126000

Project D

0 -150000 1 -150000

1 60000 0.909 54540

2 60000 0.826 49560

3 60000 0.751 45060

4 60000 0.683 40980

Net present value of cash flows from project D 40140

Ranking projects on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

b) Reasons for regarding NPV technique which is superior to IRR

a) The reason for which NPV can be considered superior over IRR is it can rank projects with

cash flows which are uneven on different period of time which is required to identify the most

suitable investment.

b) The reason for NPV being considered a better technique over the IRR is it lets discounting

various years’ cash flows at different discount rates and is also without problems which makes

the option better than IRR (Creemers, 2018).

c) Net present value technique allows the business for identification of expected total benefit

against the initial investment made by it. Investor can analyse the expected total outcome in

same manner as initial investment is identified by the concerned investor. Looking from other

perspective, internal rate of return provide return which can be a bit complex to understand and

compute for some investors.

d) The flexibility which NPV provides is that even if the multiple discount rates are given they

can be handled through NPV which is not possible in case of IRR.

e) In context of decision-making in investment the scale of project and investment level requires

in the project is crucial element which can affect the decision-making technique. Net present

value technique covering up the aspect and also involving the inflow level expected belonging to

the whole life of project.

f) IRR also assumes that reinvestment and the discounting rate of return are the same concept

however, NPV method says that differentiation has been understood in clear terms. Speaking of

financial management each single concept puts a direct impact.

g) In case of NPV, rate of borrowing is assumed as well as coming close to market rate is not

absolutely impractical and can certainly come of use.

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital available for project investment = £700000

Calculation of weights

Project NPV Weights

b) Reasons for regarding NPV technique which is superior to IRR

a) The reason for which NPV can be considered superior over IRR is it can rank projects with

cash flows which are uneven on different period of time which is required to identify the most

suitable investment.

b) The reason for NPV being considered a better technique over the IRR is it lets discounting

various years’ cash flows at different discount rates and is also without problems which makes

the option better than IRR (Creemers, 2018).

c) Net present value technique allows the business for identification of expected total benefit

against the initial investment made by it. Investor can analyse the expected total outcome in

same manner as initial investment is identified by the concerned investor. Looking from other

perspective, internal rate of return provide return which can be a bit complex to understand and

compute for some investors.

d) The flexibility which NPV provides is that even if the multiple discount rates are given they

can be handled through NPV which is not possible in case of IRR.

e) In context of decision-making in investment the scale of project and investment level requires

in the project is crucial element which can affect the decision-making technique. Net present

value technique covering up the aspect and also involving the inflow level expected belonging to

the whole life of project.

f) IRR also assumes that reinvestment and the discounting rate of return are the same concept

however, NPV method says that differentiation has been understood in clear terms. Speaking of

financial management each single concept puts a direct impact.

g) In case of NPV, rate of borrowing is assumed as well as coming close to market rate is not

absolutely impractical and can certainly come of use.

c) Allocation of funds for achieving optimum return in terms of getting highest Net Present

Value

Initial capital available for project investment = £700000

Calculation of weights

Project NPV Weights

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

The highest achievable NPV after allocation of initial capital to four projects on calculated

weights basis is 96855.

d)

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

0.3

B 105700 0.33

C 126000 0.40

D 40140 0.13

TOTAL 317240 1

Allocation of capital amount for investment in different projects on the basis of weights

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

The highest achievable NPV after allocation of initial capital to four projects on calculated

weights basis is 96855.

d)

One year Trial (0.5)

Year Cash

flows

Present

value

factor

@13%

Present value of cash flows

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

Expected present value of cash flows from One year trial license

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

0.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net present value of one year trial license = 81861 – 150000 = (68139).

The project does not look favourable as the NPV is in a negative figure and thus cannot be

approved.

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

Expected present value of cash flows from four year license without a trial run

= [61950 + 56383 + 49903 + 44158] = 212394

Net present value of four year license = 212394 – 150000 = 62394.

The project is capable to generate positive value of the NPV and thus is favourable for the

business.

Expected NPV

NPVs Probability Expected Value

(68139) 0.5 -34070

62394 0.5 31197

Expected NPV -2873

Standard deviation of NPV

The project does not look favourable as the NPV is in a negative figure and thus cannot be

approved.

Four year license without a trial run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

Expected present value of cash flows from four year license without a trial run

= [61950 + 56383 + 49903 + 44158] = 212394

Net present value of four year license = 212394 – 150000 = 62394.

The project is capable to generate positive value of the NPV and thus is favourable for the

business.

Expected NPV

NPVs Probability Expected Value

(68139) 0.5 -34070

62394 0.5 31197

Expected NPV -2873

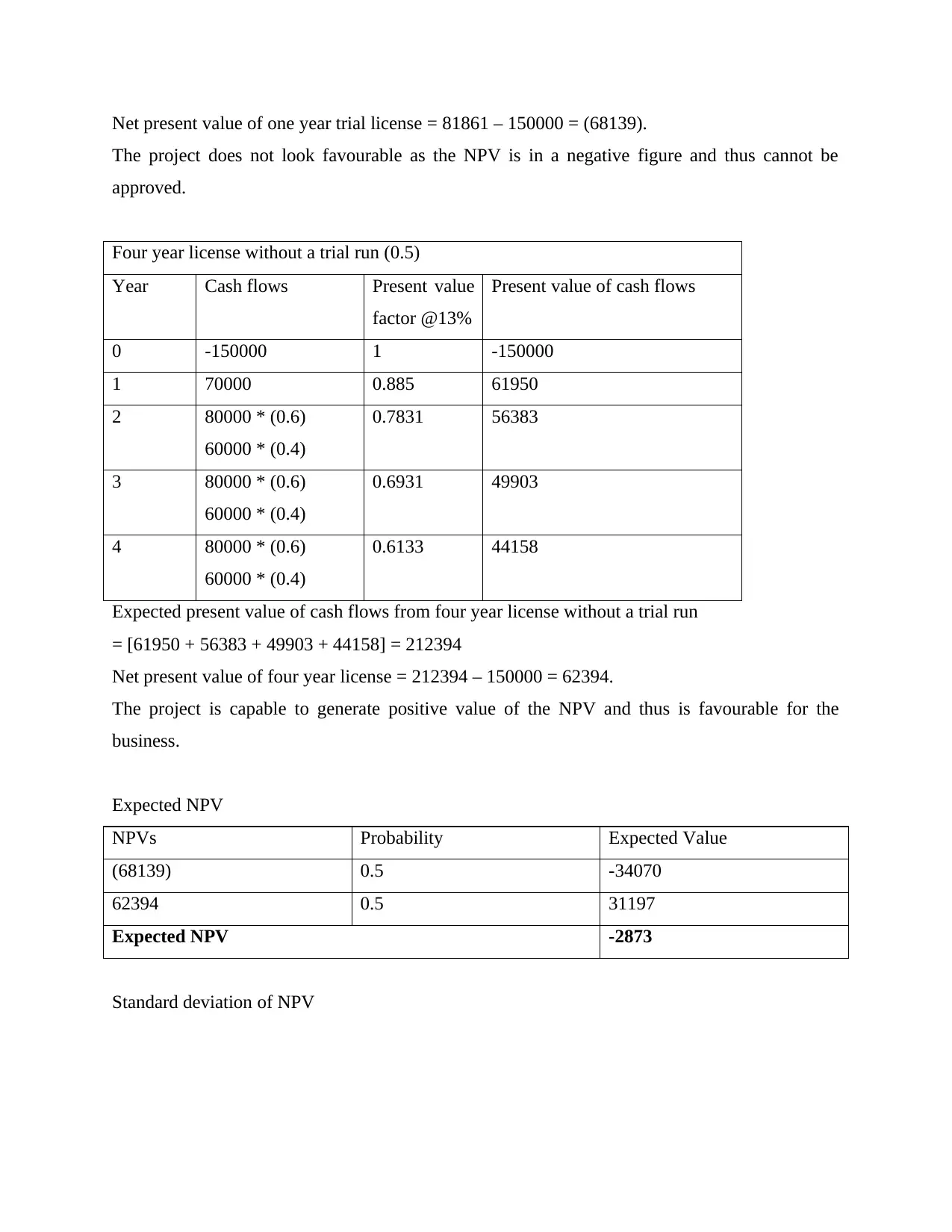

Standard deviation of NPV

Events NPVs D = (NPV –

Expected

NPV)

D2 P =

Probability

PD2

One year trial (68139) -65266 4,259,650,756 0.5 2,129,825,378

Four year

license

62394 65231 4,255,083,361 0.5 2,127,541,680

Variance 4257367058

Standard deviation 65248

Calculation of z-score, where it is know that all the values below 0 will results in negative NPV.

So, here X is equals to 0.

Z – Score = 0 – expected NPV / standard deviation of NPV = 0 – (-2873) / 65248 = 2873 / 65248

= 0.044.

Probability of negative NPV from 0 till Expected NPV = 0.017548 or 1.7548 %.

Therefore, Probability of negative NPV = 0.5 + 0.017548 = 0.5175 or 51.75%.

Each proposal contains some element which is negative that denotes it being against the

investment making decision and being necessary to overcome the possibility of negative present

value. The important point to get noted is that NPV gives the information clear about the

expected benefits for organisation (Creemers, 2018).

CONCLUSION

Investment decision is assessing the situation by various factors of the business entity and the

proposal evaluation which can bring the best results in monetary decisions. Investment decision

is taken on return generated by proposal available in front of business entity. The best method

giving returns with less risks is to be chosen. NPV is the most preferred method among

investment decisions and the most relied upon.

Expected

NPV)

D2 P =

Probability

PD2

One year trial (68139) -65266 4,259,650,756 0.5 2,129,825,378

Four year

license

62394 65231 4,255,083,361 0.5 2,127,541,680

Variance 4257367058

Standard deviation 65248

Calculation of z-score, where it is know that all the values below 0 will results in negative NPV.

So, here X is equals to 0.

Z – Score = 0 – expected NPV / standard deviation of NPV = 0 – (-2873) / 65248 = 2873 / 65248

= 0.044.

Probability of negative NPV from 0 till Expected NPV = 0.017548 or 1.7548 %.

Therefore, Probability of negative NPV = 0.5 + 0.017548 = 0.5175 or 51.75%.

Each proposal contains some element which is negative that denotes it being against the

investment making decision and being necessary to overcome the possibility of negative present

value. The important point to get noted is that NPV gives the information clear about the

expected benefits for organisation (Creemers, 2018).

CONCLUSION

Investment decision is assessing the situation by various factors of the business entity and the

proposal evaluation which can bring the best results in monetary decisions. Investment decision

is taken on return generated by proposal available in front of business entity. The best method

giving returns with less risks is to be chosen. NPV is the most preferred method among

investment decisions and the most relied upon.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.