Detailed Analysis of IFRS Financial Reporting for BHP Billiton Plc

VerifiedAdded on 2021/11/15

|14

|2994

|65

Report

AI Summary

This report provides a detailed analysis of BHP Billiton Plc's financial reporting practices under International Financial Reporting Standards (IFRS). The report examines the company's adherence to key IAS standards, including IAS 36 (Impairment of Assets), IAS 32 (Financial Instruments: Presentation), IAS 39 (Financial Instruments: Recognition and Measurement), and IAS 19 (Employee Benefits). It explores the company's accounting policies related to these standards, focusing on impairment testing, financial instruments, and pension plans. The analysis includes an examination of the financial risks faced by the company, its risk management strategies, and the impact of these factors on its financial position and performance. The report also assesses the company's sensitivity to changes in key assumptions and compares its practices with industry standards, culminating in a conclusion on the overall relevance and quality of the financial reporting framework adopted by BHP Billiton. The report is a valuable resource for students studying finance and accounting, providing insights into real-world application of IFRS.

International Financial

Reporting Standards

International Financial Reporting Standards

International Financial Reporting Standards

Reporting Standards

International Financial Reporting Standards

International Financial Reporting Standards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................3

Answer Given For Question No-1.................................................................................3

Answer Given For Question No 2 (a)...........................................................................4

Answer Given For Question No 2(b).........................................................................6

Answer Given For Question No (2) c).......................................................................8

CONCLUSION..............................................................................................................9

REFERENCES...........................................................................................................10

INTRODUCTION..........................................................................................................3

Answer Given For Question No-1.................................................................................3

Answer Given For Question No 2 (a)...........................................................................4

Answer Given For Question No 2(b).........................................................................6

Answer Given For Question No (2) c).......................................................................8

CONCLUSION..............................................................................................................9

REFERENCES...........................................................................................................10

INTRODUCTION

The current report is depicting the financial reporting requirements that are

laid by the International Financial Reporting Standards (IFRS). The analysis that is

done in the report is on a company which is listed in London Stock Exchange on the

FTSE 100. The report is presented in a format that first introduces the company and

then forms an analysis of the overall financial accounts. The discussion is revolved

basically around a few IAS that are adopted and moulded in accordance with the

IFRS requirements. The main IAS discussed in the report comprises of IAS 36, IAS

32, IAS 39, and IAS 19. The accounting policies relevant to these IAS are also

discussed. A conclusion is presented in the end of the report that deals with the

relevance of the accounting and reporting framework that is adopted in the selected

company.

Answer Given For Question No-1

The company chosen is BHP Billiton Plc. The company deals in resource extraction

and their processing. The extraction and processing of the gas, oil, and minerals is

done. The company’s headquarters are located in Melbourne in Australia (Epstein,

2018). The main subsidiaries of the company in United Kingdom are:

Auvernier Limited

BHP Billiton Agnew Mining Company Pty Ltd

BHP Billiton Aluminium Projects (Pty) Ltd

BHP Billiton Australia Investment 3 Pty Ltd

BHP Billiton Energy Coal (UK) Limited

BHP Billiton Energy Coal Chile Limited

The current report is depicting the financial reporting requirements that are

laid by the International Financial Reporting Standards (IFRS). The analysis that is

done in the report is on a company which is listed in London Stock Exchange on the

FTSE 100. The report is presented in a format that first introduces the company and

then forms an analysis of the overall financial accounts. The discussion is revolved

basically around a few IAS that are adopted and moulded in accordance with the

IFRS requirements. The main IAS discussed in the report comprises of IAS 36, IAS

32, IAS 39, and IAS 19. The accounting policies relevant to these IAS are also

discussed. A conclusion is presented in the end of the report that deals with the

relevance of the accounting and reporting framework that is adopted in the selected

company.

Answer Given For Question No-1

The company chosen is BHP Billiton Plc. The company deals in resource extraction

and their processing. The extraction and processing of the gas, oil, and minerals is

done. The company’s headquarters are located in Melbourne in Australia (Epstein,

2018). The main subsidiaries of the company in United Kingdom are:

Auvernier Limited

BHP Billiton Agnew Mining Company Pty Ltd

BHP Billiton Aluminium Projects (Pty) Ltd

BHP Billiton Australia Investment 3 Pty Ltd

BHP Billiton Energy Coal (UK) Limited

BHP Billiton Energy Coal Chile Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BHP Billiton Group Limited (Burritt, and Christ, 2018).

As far as the regulatory framework of the company is discussed the company is

following the international standards well. The operations are done in line with the

requirements set by the corporation laws lay in market. The financial statements are

prepared on the basis of the UK Companies Act 2006 (Sheth, and Sinha, 2015).

Answer Given For Question No 2 (a)

The company as discussed above is in the line of extraction and processing. The

main product areas dealt by the company are in coal, petroleum, copper, and iron

ore. These are the areas that generate cash for the company. Hence, the company

has selected the cash generating units on the basis of these production areas of

business for impairment purposes (Linnenluecke, et al. 2015).

The management assesses the cash flows for the purpose of impairment review by

the following ways:

The foreign exchange flows from and into business are substantially watched.

The cash flow projections that have been made for the financial year’s performance

must be compared with the actual cash flow position (Banker, Basu¸ Byzalov, 2016).

The market capitalisation of the assets of the company is required to be compared

with the carrying value of the same that is represented in the balance sheet

(Bostwick, Krieger, and Lambert, 2016).

The various indicators that existed on the balance sheet date depicting the necessity

of impairment comprises of both internal and external indicators. The internal

indicators in case of BHP Billiton comprises of the carrying value of the asset being

lower than the amount that can be achieved on sale of the asset. The external

As far as the regulatory framework of the company is discussed the company is

following the international standards well. The operations are done in line with the

requirements set by the corporation laws lay in market. The financial statements are

prepared on the basis of the UK Companies Act 2006 (Sheth, and Sinha, 2015).

Answer Given For Question No 2 (a)

The company as discussed above is in the line of extraction and processing. The

main product areas dealt by the company are in coal, petroleum, copper, and iron

ore. These are the areas that generate cash for the company. Hence, the company

has selected the cash generating units on the basis of these production areas of

business for impairment purposes (Linnenluecke, et al. 2015).

The management assesses the cash flows for the purpose of impairment review by

the following ways:

The foreign exchange flows from and into business are substantially watched.

The cash flow projections that have been made for the financial year’s performance

must be compared with the actual cash flow position (Banker, Basu¸ Byzalov, 2016).

The market capitalisation of the assets of the company is required to be compared

with the carrying value of the same that is represented in the balance sheet

(Bostwick, Krieger, and Lambert, 2016).

The various indicators that existed on the balance sheet date depicting the necessity

of impairment comprises of both internal and external indicators. The internal

indicators in case of BHP Billiton comprises of the carrying value of the asset being

lower than the amount that can be achieved on sale of the asset. The external

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indicators on the other hand consists of the decline in the market value of the assets,

the rise in the interest rate in the economic market, and the various changes that are

being observed in the arena of industry laws and technology (Bond, Govendir, and

Wells, 2016).

The bases of recoverable amount are the fair value after the costs incurred to sale

are deducted from it, and the value in use of the asset. To estimate the value of

assets at the balance sheet date the assumptions made relate to the estimation of

the cash flows that will be generated in future, the estimation of the time value of

money, the relevant and expected variations in the future values, etc. (Lubbe,

Modack, and Watson, 2014).

The key assumptions that are made in the impairment testing have to relate with the

circumstances that are to deal with the future forecasts expected for the company

and the relevant industry. Hence it is clear that the projections shall show a stark

difference if compared with the historical results in case the future scenario is

expected to change. However, if the conditions are likely to remain same except

some general changes, the assumptions used in the impairment testing shall show

similar trends as reflected in the historical results and by the industry performance

(André¸ Dionysiou, and Tsalavoutas, 2018).

The company has performed sensitivity analysis relating to the transactional

exposure and commodity price risk for assessing the recoverable amounts.

The company has impaired goodwill also. The reason is simple as goodwill is also an

asset. It is of no point that it is intangible one. Same impairment applies to goodwill

as other tangible assets (Kabir, Rahman, and Su, 2017).

the rise in the interest rate in the economic market, and the various changes that are

being observed in the arena of industry laws and technology (Bond, Govendir, and

Wells, 2016).

The bases of recoverable amount are the fair value after the costs incurred to sale

are deducted from it, and the value in use of the asset. To estimate the value of

assets at the balance sheet date the assumptions made relate to the estimation of

the cash flows that will be generated in future, the estimation of the time value of

money, the relevant and expected variations in the future values, etc. (Lubbe,

Modack, and Watson, 2014).

The key assumptions that are made in the impairment testing have to relate with the

circumstances that are to deal with the future forecasts expected for the company

and the relevant industry. Hence it is clear that the projections shall show a stark

difference if compared with the historical results in case the future scenario is

expected to change. However, if the conditions are likely to remain same except

some general changes, the assumptions used in the impairment testing shall show

similar trends as reflected in the historical results and by the industry performance

(André¸ Dionysiou, and Tsalavoutas, 2018).

The company has performed sensitivity analysis relating to the transactional

exposure and commodity price risk for assessing the recoverable amounts.

The company has impaired goodwill also. The reason is simple as goodwill is also an

asset. It is of no point that it is intangible one. Same impairment applies to goodwill

as other tangible assets (Kabir, Rahman, and Su, 2017).

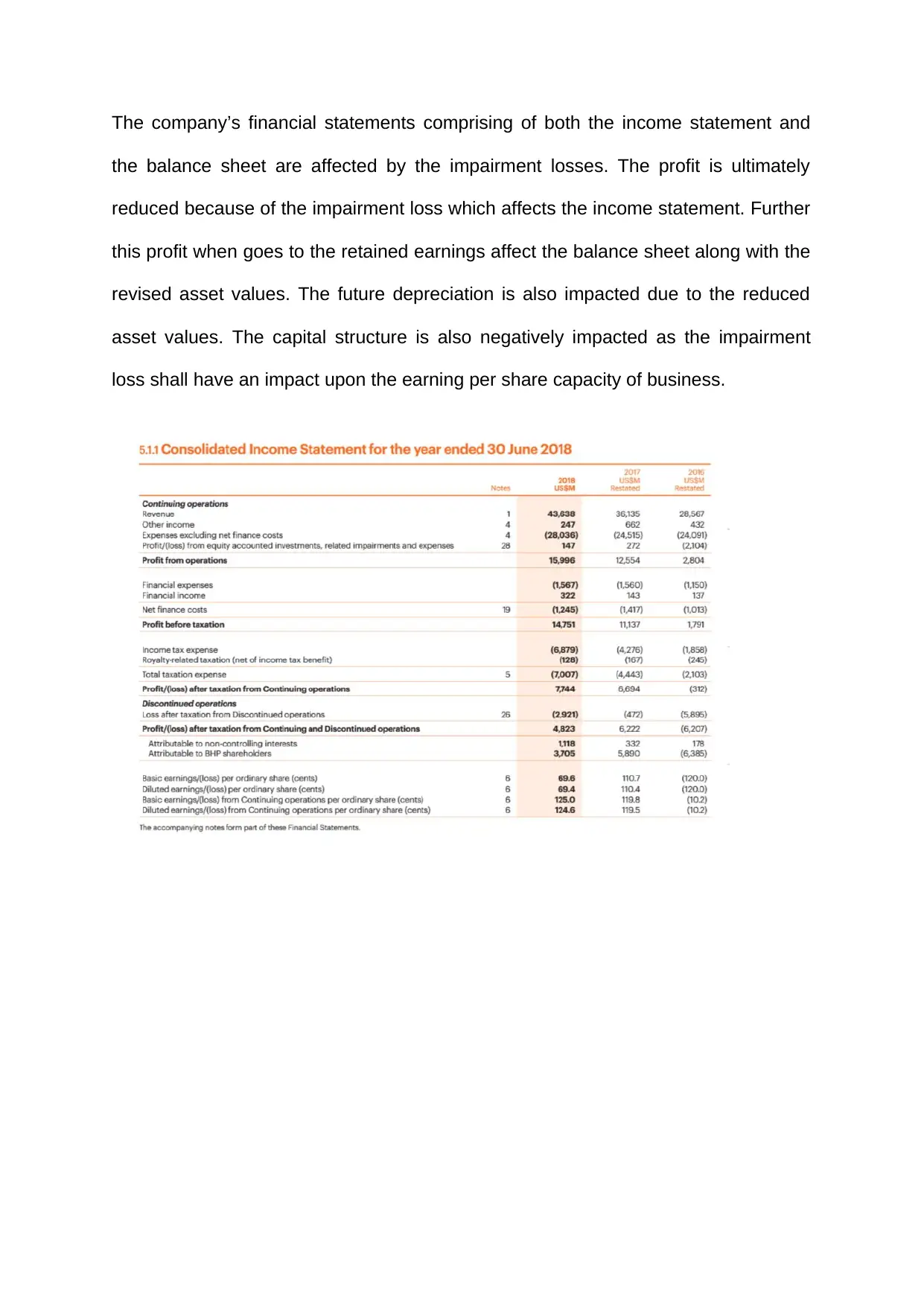

The company’s financial statements comprising of both the income statement and

the balance sheet are affected by the impairment losses. The profit is ultimately

reduced because of the impairment loss which affects the income statement. Further

this profit when goes to the retained earnings affect the balance sheet along with the

revised asset values. The future depreciation is also impacted due to the reduced

asset values. The capital structure is also negatively impacted as the impairment

loss shall have an impact upon the earning per share capacity of business.

the balance sheet are affected by the impairment losses. The profit is ultimately

reduced because of the impairment loss which affects the income statement. Further

this profit when goes to the retained earnings affect the balance sheet along with the

revised asset values. The future depreciation is also impacted due to the reduced

asset values. The capital structure is also negatively impacted as the impairment

loss shall have an impact upon the earning per share capacity of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

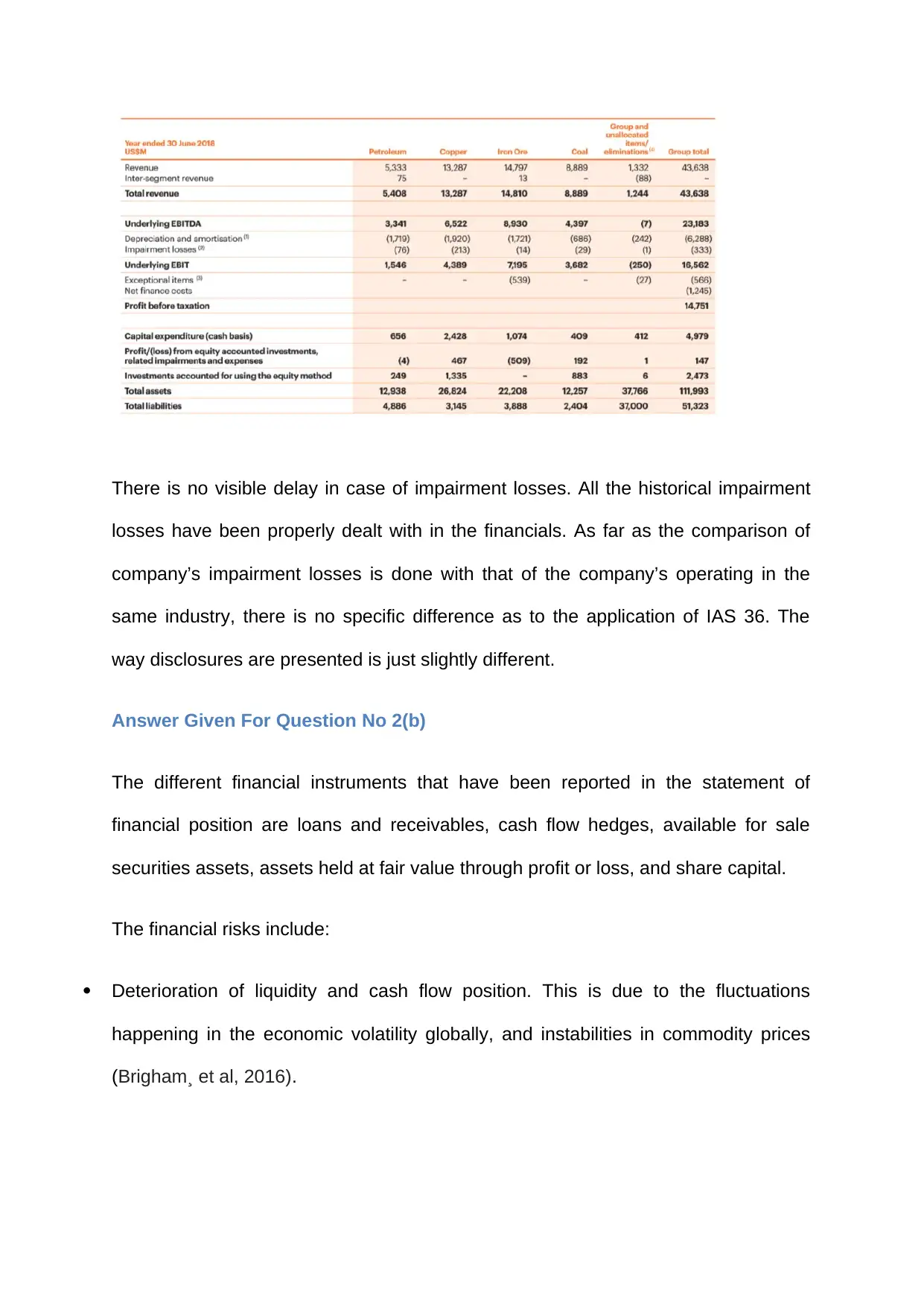

There is no visible delay in case of impairment losses. All the historical impairment

losses have been properly dealt with in the financials. As far as the comparison of

company’s impairment losses is done with that of the company’s operating in the

same industry, there is no specific difference as to the application of IAS 36. The

way disclosures are presented is just slightly different.

Answer Given For Question No 2(b)

The different financial instruments that have been reported in the statement of

financial position are loans and receivables, cash flow hedges, available for sale

securities assets, assets held at fair value through profit or loss, and share capital.

The financial risks include:

Deterioration of liquidity and cash flow position. This is due to the fluctuations

happening in the economic volatility globally, and instabilities in commodity prices

(Brigham¸ et al, 2016).

losses have been properly dealt with in the financials. As far as the comparison of

company’s impairment losses is done with that of the company’s operating in the

same industry, there is no specific difference as to the application of IAS 36. The

way disclosures are presented is just slightly different.

Answer Given For Question No 2(b)

The different financial instruments that have been reported in the statement of

financial position are loans and receivables, cash flow hedges, available for sale

securities assets, assets held at fair value through profit or loss, and share capital.

The financial risks include:

Deterioration of liquidity and cash flow position. This is due to the fluctuations

happening in the economic volatility globally, and instabilities in commodity prices

(Brigham¸ et al, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There is a risk to the recovery of company’s investments that have been made in oil,

mining, and gas assets. This would call the company to write down its financials

consisting of goodwill and etc.

There is a risk that the suppliers, customers or the financers may not stand by their

commitments and cast an adverse impact on the company’s business (Matiin,

Ratnawati, and Riyadi, 2018).

To manage the financial risks the company is facing a financial risk management

company is being established. The focus is on monitoring the volatilities and

maintaining the key financial ratios. To reduce overall volatility the company focuses

to diversify the investment portfolio (Reason, 2016).

The financial risks have a significant impact on the future financial position of the

company. The impact is to be seen mainly upon the position of the cash flows, credit

rating and the company’s capacity to secure capital from market. The whole budget

shall get disrupted by any volatility that market experiences (Barakat, 2014).

The company has material sensitivity to the changes in financial risks that relate to

the market volatility.

The measurement basis used to recognise the financial instruments except the

derivatives is done on the basis of fair value reduced by the transaction costs at the

first instance. Now the subsequent recognition is done either on amortised cost or

fair value. As far as the derivative recognition is considered, the initial recognition is

done on fair value basis for the contract entering date and any future valuation is

done by measuring the Fair value again.

mining, and gas assets. This would call the company to write down its financials

consisting of goodwill and etc.

There is a risk that the suppliers, customers or the financers may not stand by their

commitments and cast an adverse impact on the company’s business (Matiin,

Ratnawati, and Riyadi, 2018).

To manage the financial risks the company is facing a financial risk management

company is being established. The focus is on monitoring the volatilities and

maintaining the key financial ratios. To reduce overall volatility the company focuses

to diversify the investment portfolio (Reason, 2016).

The financial risks have a significant impact on the future financial position of the

company. The impact is to be seen mainly upon the position of the cash flows, credit

rating and the company’s capacity to secure capital from market. The whole budget

shall get disrupted by any volatility that market experiences (Barakat, 2014).

The company has material sensitivity to the changes in financial risks that relate to

the market volatility.

The measurement basis used to recognise the financial instruments except the

derivatives is done on the basis of fair value reduced by the transaction costs at the

first instance. Now the subsequent recognition is done either on amortised cost or

fair value. As far as the derivative recognition is considered, the initial recognition is

done on fair value basis for the contract entering date and any future valuation is

done by measuring the Fair value again.

The company’s financial instruments that do not have an active market consist of the

loans and receivables, and the cash and cash equivalents. The valuation of the loan

and receivables is done initially on the basis of the fair value for which the payment

of consideration is done. After subsequent time, any valuation is carried at their fair

value or their amortised cost that is reduced by impairment.

There are certainly provisions that exist for the impairment of the financial

instruments. The measurement of the impairment loss is done by deducting the

present value of the future cash flows expected from the financial instrument from its

carrying amount that is highlighted in the balance sheet. The company’s financial

position is affected by a reduction that is observed in the carrying amount of the

financial instrument and the financial performance is impacted by the reduction in the

year’s profit due to impairment losses. Industry practice is almost similar to the

impairment practice that the company follows.

The company uses hedge accounting. The hedge accounting incorporates

adjustments to be made in the carrying amount of the hedged instruments. Any

adjustments in the carrying amount have an effect over the profit and loss statement

of the company. Hence both the financial position and performance is impacted by

this (Singh, 2017). The company’s hedging policies comprises of cash flow hedge

and the fair value hedge. Further, any impact occurred due to the hedge practices

areaffected in the income statement. The company’s hedge practices are in line with

the industry practice (Campbell, 2015).

loans and receivables, and the cash and cash equivalents. The valuation of the loan

and receivables is done initially on the basis of the fair value for which the payment

of consideration is done. After subsequent time, any valuation is carried at their fair

value or their amortised cost that is reduced by impairment.

There are certainly provisions that exist for the impairment of the financial

instruments. The measurement of the impairment loss is done by deducting the

present value of the future cash flows expected from the financial instrument from its

carrying amount that is highlighted in the balance sheet. The company’s financial

position is affected by a reduction that is observed in the carrying amount of the

financial instrument and the financial performance is impacted by the reduction in the

year’s profit due to impairment losses. Industry practice is almost similar to the

impairment practice that the company follows.

The company uses hedge accounting. The hedge accounting incorporates

adjustments to be made in the carrying amount of the hedged instruments. Any

adjustments in the carrying amount have an effect over the profit and loss statement

of the company. Hence both the financial position and performance is impacted by

this (Singh, 2017). The company’s hedging policies comprises of cash flow hedge

and the fair value hedge. Further, any impact occurred due to the hedge practices

areaffected in the income statement. The company’s hedge practices are in line with

the industry practice (Campbell, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer Given For Question No (2) c)

Benefit pension plan is used to identify the benefits available to employees and set

accounting policies are followed for the same. The accounting policy to recognise the

defined benefit pension plan is:

The cost of pension provision is charged to income statement.

Any loss or gain on re-measurement in charged to equity

The recognition value means present value of defined obligations as reduced by the

plan assets’ fair value (Mohan, and Zhang, 2014).

The assumptions made relate to the fair value of the plan assets, discount rates,

years of service and etc. The assumptions seem realistic. The whole post-

employment benefit is dependent upon the assumptions that are discussed. Hence

the complete expenditure that is laid in the income statement and the value for the

employee benefits in form of plan assets reflected in balance sheet is dependent

upon those assumptions (Cadman, and Vincent, 2015).

The discount rate is usually the market yield of the corporate bonds. Else the

government bond discount rate is preferred. It is completely realistic as their maturity

is compared first before choosing. These assumptions are same as followed since

ages and in the industry (Andonov, Bauer, and Cremers, 2017).

The company does have complete sensitivity to the changes that may take in the key

assumptions. The current financial status of the employee benefit plan is US$1232

million. There has been improvement over financial year 2017. In 2017 it was

US$1177 million. The improvement is on account of raise in the employee base and

inflationary trends.

Benefit pension plan is used to identify the benefits available to employees and set

accounting policies are followed for the same. The accounting policy to recognise the

defined benefit pension plan is:

The cost of pension provision is charged to income statement.

Any loss or gain on re-measurement in charged to equity

The recognition value means present value of defined obligations as reduced by the

plan assets’ fair value (Mohan, and Zhang, 2014).

The assumptions made relate to the fair value of the plan assets, discount rates,

years of service and etc. The assumptions seem realistic. The whole post-

employment benefit is dependent upon the assumptions that are discussed. Hence

the complete expenditure that is laid in the income statement and the value for the

employee benefits in form of plan assets reflected in balance sheet is dependent

upon those assumptions (Cadman, and Vincent, 2015).

The discount rate is usually the market yield of the corporate bonds. Else the

government bond discount rate is preferred. It is completely realistic as their maturity

is compared first before choosing. These assumptions are same as followed since

ages and in the industry (Andonov, Bauer, and Cremers, 2017).

The company does have complete sensitivity to the changes that may take in the key

assumptions. The current financial status of the employee benefit plan is US$1232

million. There has been improvement over financial year 2017. In 2017 it was

US$1177 million. The improvement is on account of raise in the employee base and

inflationary trends.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The actual and the forecasted parameters have laid the assumptions on which the

employee benefit calculations have been made. The pension contributions have

been approximately 25% to the whole employee benefits. The pension contribution

amount expenditure and reduce the profit reflected in the income statement. This

affects the overall financial position.

CONCLUSION

The company has incorporated in its financials all the aspects that may be

useful and add quality for the readers. The financial information that is provided in

the financial accounts comprises of the qualitative characteristics of faithfulness and

reliability. The IASB’s conceptual framework is completely being followed. All the

accounts have been prepared in accordance with the IAS that has been given the

affect in accordance with the IFRS (Choudhary, Merkley, andSchipper, 2017).

employee benefit calculations have been made. The pension contributions have

been approximately 25% to the whole employee benefits. The pension contribution

amount expenditure and reduce the profit reflected in the income statement. This

affects the overall financial position.

CONCLUSION

The company has incorporated in its financials all the aspects that may be

useful and add quality for the readers. The financial information that is provided in

the financial accounts comprises of the qualitative characteristics of faithfulness and

reliability. The IASB’s conceptual framework is completely being followed. All the

accounts have been prepared in accordance with the IAS that has been given the

affect in accordance with the IFRS (Choudhary, Merkley, andSchipper, 2017).

REFERENCES

Andonov, A., Bauer, R. M., and Cremers, K. M. (2017). Pension fund asset allocation and

liability discount rates. The Review of Financial Studies, 30(8), 2555-2595.

André, P., Dionysiou, D., and Tsalavoutas, I. (2018). Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics, 50(7), 707-725.

Banker, R. D., Basu, S., and Byzalov, D. (2016). Implications of Impairment Decisions and

Assets' Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2),

41-67.

Barakat, A. (2014). The impact of financial structure, financial leverage and profitability on

industrial companies shares value (Applied study on a sample of saudi industrial

companies). Research Journal of Finance and Accounting, 5(1), 55-66.

Bond, D., Govendir, B., and Wells, P. (2016). An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting and

Finance, 56(1), 259-288.

Bostwick, E. D., Krieger, K., and Lambert, S. L. (2016). Relevance of goodwill impairments

to cash flow prediction and forecasting. Journal of Accounting, Auditing and Finance, 31(3),

339-364.

Brigham, E. F., Ehrhardt, M. C., Nason, R. R., and Gessaroli, J. (2016). Financial

Managment: Theory And Practice, Canadian Edition. UK: Nelson Education.

Andonov, A., Bauer, R. M., and Cremers, K. M. (2017). Pension fund asset allocation and

liability discount rates. The Review of Financial Studies, 30(8), 2555-2595.

André, P., Dionysiou, D., and Tsalavoutas, I. (2018). Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on

analysts’ forecasts. Applied Economics, 50(7), 707-725.

Banker, R. D., Basu, S., and Byzalov, D. (2016). Implications of Impairment Decisions and

Assets' Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2),

41-67.

Barakat, A. (2014). The impact of financial structure, financial leverage and profitability on

industrial companies shares value (Applied study on a sample of saudi industrial

companies). Research Journal of Finance and Accounting, 5(1), 55-66.

Bond, D., Govendir, B., and Wells, P. (2016). An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting and

Finance, 56(1), 259-288.

Bostwick, E. D., Krieger, K., and Lambert, S. L. (2016). Relevance of goodwill impairments

to cash flow prediction and forecasting. Journal of Accounting, Auditing and Finance, 31(3),

339-364.

Brigham, E. F., Ehrhardt, M. C., Nason, R. R., and Gessaroli, J. (2016). Financial

Managment: Theory And Practice, Canadian Edition. UK: Nelson Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.