International Financial Reporting Standards: Doc

Added on 2021-02-20

22 Pages3336 Words34 Views

International FinancialReporting

Table of Content

INTRODUCTIONInternational financial reporting provides a framework to the business organization toassess about they way in which IFRS are are applied in order to produce financial statements. Afirm by implementing such reporting system may diversifies its business beyond its domesticterritory. Various standards such as IFRS and IAS are formulated by international board andcommittee to regulating and providing assistance in the field of financial reporting. For thispurpose, a company named MAZARS which is engaged in providing accountancy consultancyservices to its clients. This report defines the term international financial reporting and itsseveral regulatory, conceptual frameworks along with features of financial data. Keystakeholder of a company and role to them from these information is also explained in thisreport.TASK 1P1.Context of financial reporting with their regulatory frameworks and governance:Financial reporting may be defined as framework that provides way to present andcommunicate the relevant monetary data to different stakeholders. Financial reporting assist anorganization in preparing its financial statements for particular time period, such financialstatements consists P&L a/c, statement of change in financial position, cash flow statement etc.It has several conceptual and regulatory frameworks that a company shall require to follow, thedetails discussion about these frameworks are as follows:Conceptual framework:These frameworks assist the companies like MAZARS in knowing the objectives of thefinancial reporting acts as a tool for formulation and issuance of several accounting standards.Therefore, it assists the MAZARS in developing a essential theoretical foundation so that it ableto evaluate, recording and represent the various financial transactions related to its businessoperations. In relation to financial reporting, a conceptual framework may be understandable asa statement of generally accepted accounting principles (GAAP). These conceptual frameworkshelp in evaluating yardsticks as well as determine point of references for comparison andimprovement in current accounting practices. Due to non-availability of these frameworks, thereare chances of increasing numbers of accounting scandals by doing wrong practices to

misappropriate the profits of an organization. In an understanding point of view, they assist anorganization by following ways:Improvement in current standards along with issuance of new accountingstandards as per requirements.Boost coordination between accounting rules and regulation with severalstandards.Preparation and presentation of financial statements for various key stakeholders.Regulatory framework:These are the frameworks that determine the way through which financial information of anorganization is recorded and reported. in other words, it offers different rules and frameworks offinancial transactions of an organization at international level. These are applicable to allEuropean listed companies, including UK companies. For issuance of these frameworks, IASBto offer regulating standards for the companies like MAZARS and in response of this, IASBissued various IFRS that aims to encourage collaboration, investor engagement andtransparency in accounting process. This framework is considered necessary for correctpresentation of financial information of a company for fulfilling needs adequately of keystakeholders. In such process IASB issues some IFRS which are as follows:IFRS 1: Implementation of IFRS IFRS 10 : Consolidated financial StatementsIFRS 13 : Fair value measurementThe primary objective of regulating framework is to facilitate understanding andrevision of GAAP as well as IFRS (Abeysekera, 2013). Qualitative characteristics that makes financial information more reliable:For making financial information more reliable and understandable, companies likeMAZARS shall require to have some qualitative characteristics in its financial informationwhich are as follows:Relevance: It is associated with providing useful information that is included inthe financial statements. Relevance implies that financial information which shall be reportedshould add some vale in decision making of users of such financial statements.

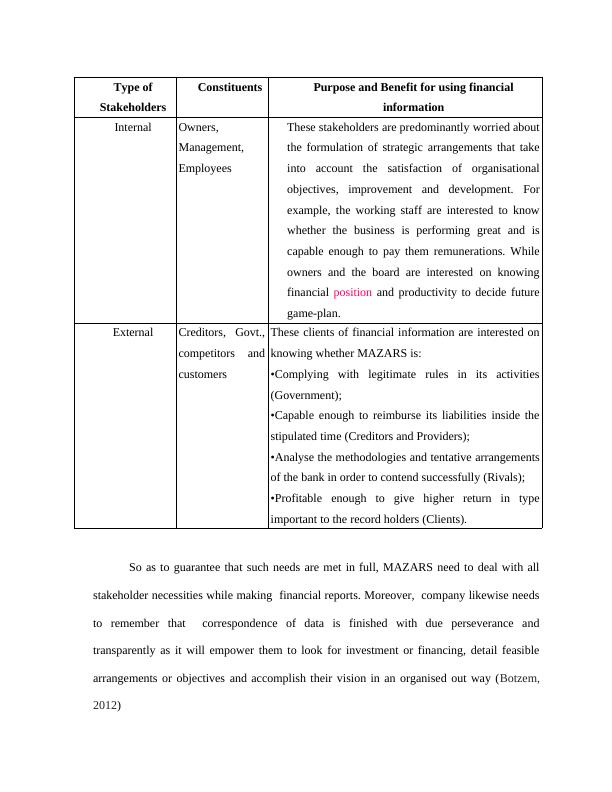

Understandability: This is an important quality of financial information thatenables the users in understanding its significance. For this, such information shall be presentedin such a way that facilitate easy understanding and avoids any incorrect interpretation.Comparability: A financial information must be capable of providing appropriatecomparison in effective decision making. If information is comparable then it assists thedecision maker to evaluate and estimate the key strengths and weaknesses of an organizationrelated to its business operations (Albu and Albu, 2012).P2.Role of financial-reporting to achieve goals and objectives of businesses. The primary role of financial-reporting is to record and report the key informationregarding business operations, performances and cash flows in a predefined format. Financialreporting aims is to providing information to the investors, track cash flows of a company likeMAZARS and analysis assets, liabilities and owner’s equity. Thus, it helps a company likeMAZARS in meeting its objectives and assist in its development and growth.Key stakeholders:

So as to guarantee that such needs are met in full, MAZARS need to deal with allstakeholder necessities while making financial reports. Moreover, company likewise needsto remember that correspondence of data is finished with due perseverance andtransparently as it will empower them to look for investment or financing, detail feasiblearrangements or objectives and accomplish their vision in an organised out way (Botzem,2012)Type ofStakeholdersConstituentsPurpose and Benefit for using financialinformationInternalOwners,Management,EmployeesThese stakeholders are predominantly worried aboutthe formulation of strategic arrangements that takeinto account the satisfaction of organisationalobjectives, improvement and development. Forexample, the working staff are interested to knowwhether the business is performing great and iscapable enough to pay them remunerations. Whileowners and the board are interested on knowingfinancial position and productivity to decide futuregame-plan.ExternalCreditors, Govt.,competitors andcustomersThese clients of financial information are interested onknowing whether MAZARS is: •Complying with legitimate rules in its activities(Government); •Capable enough to reimburse its liabilities inside thestipulated time (Creditors and Providers); •Analyse the methodologies and tentative arrangementsof the bank in order to contend successfully (Rivals); •Profitable enough to give higher return in typeimportant to the record holders (Clients).

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Reporting - Oliver Wymanlg...

|17

|4690

|31

The Conceptual Framework of Financial Reporting and Its Roleslg...

|9

|2479

|382

Content and Application of the IASB Conceptual Frameworklg...

|10

|2213

|351

Theoretical Principles for Accounting - Doclg...

|7

|1957

|92

Financial Reporting Assignment Sample (Doc)lg...

|9

|1957

|54

Financial Reporting Assignment : IFRSlg...

|9

|1901

|173