Analysis of International Financial Statement Contents and Standards

VerifiedAdded on 2020/07/22

|11

|3925

|37

Report

AI Summary

This report provides a comprehensive analysis of International Financial Reporting Standards (IFRS). It begins with an introduction to IFRS and the convergence project between the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB), discussing its objectives, current status, and positive impacts on investors and global entities. The report then examines the financial statements of Ketsu Department Stores, focusing on working capital management and the use of simplified balance sheets. Finally, it analyzes the financial performance of Muji using ratio analysis, including liquidity, profitability, and solvency ratios. The report highlights the advantages of convergence to both investors and entities, emphasizing enhanced comparability, reduced barriers to expansion, and improved capital market efficiency. The report uses the provided financial data to calculate and interpret key financial ratios, providing insights into the financial health of the companies discussed.

International Financial

Statement

Statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION................................................................................................................................3

Question 1.............................................................................................................................................3

Question 2.............................................................................................................................................4

Question 3.............................................................................................................................................5

CONCLUSION..................................................................................................................................10

REFERENCES...................................................................................................................................11

INTRODUCTION................................................................................................................................3

Question 1.............................................................................................................................................3

Question 2.............................................................................................................................................4

Question 3.............................................................................................................................................5

CONCLUSION..................................................................................................................................10

REFERENCES...................................................................................................................................11

INTRODUCTION

International Finance reporting is international accounting framework in which financial

information is properly organised and reported. There is huge requirement of International financial

reporting standards in accounting framework in more than 120 countries. It requires every

businesses to report all of their financial statements and financial position using same rules and

regulations. In this report, there is proper analysis of the convergence project i.e. Being done by

jointly by International accounting standard board and Financial Accounting Standard Board, which

came out of an agreement by the two boards (IASB and FASB) . As in this report, it has clearly

mentioned about that how they are standard setters in a coordinated manner and how they will be

improving the quality and how it had positively impacted on investors and entities . Like

convergence has made the comparison between the organisation who operates globally. In the

second part of this report, it is all about Ketsu Department stores which is one of the Japan's largest

retailer with many stores throughout Japan. The consolidated financial statements have been drawn

up with standards issued by the international Accounting Standards Committee, in that reference

how simplified balance sheet helps in investment decision making. And more preference is been

given to working capital and its need.

In third part, there is an brief analysis of the financial performance of Muji , FMCG

company of Japan with the help of ratio analysis on the basis of three parameter .The parameters are

Liquidity ratio, Profitability ratio and Solvency ratio. These three parameters are also explained

with the subheading i.e. current ratio, acid test ratio, and return on asset, gross margin ratio, profit

margin ratio, debt to equity ratio and equity ratio with proper interpretation.

Question 1

Explain what the convergence project was intended to achieve and briefly explain the current status

of the project?

International Accounting Standards Board is a London based organisation. This organisation

is given full support of industry and government and it also set standards for accounting procedures.

IASB has responsibility for maintaining International Financial Reporting standards. The parent

entity of IASB is International Accounting Standard Committee. Financial Accounting Standard

Board establishes financial reporting and accounting standards for private and public companies and

the organisations who follow Generally Accepted Accounting Principles and that too they must be

not for procure key issues in it organisations. Their main objective was to eliminate the differences

between US GAAP and Financial reporting standards. FASB is one of the most important partner of

IASB. Board works so closely with national standard setters around the world. FASB got to know

that it does not have all solutions for all accounting issue. Some of the areas of US standard could

be improved where International standards can be easily applied (Jaruga and et.al., 2007).

The convergence project was intended to achieve standardisation with high quality foe entire

world, understandable and IFRS to serve lenders, creditors and ones who are in globalized market.

IASB and FASB made their best efforts to make their financial reporting standards fully practical

and compatible. Efforts were also made for coordinating their future work programs and to make

sure that they are achieved or not. Here the standard needs an improvement of both board, for

improvement they need to work jointly. FASB has involved itself in many different activities in the

context of high quality goal, standards and to increase the convergence of accounting standards

which are used in many countries. The most essential activity of FASB is its collaboration with

IASB to make optimum utilisation of resources. For convergence, staff of both boards made short

and long term strategies. In short term attempt was to remove the differences which appeared from

improvements project which were handled by IASB. Under convergence, IASB and FASB has

International Finance reporting is international accounting framework in which financial

information is properly organised and reported. There is huge requirement of International financial

reporting standards in accounting framework in more than 120 countries. It requires every

businesses to report all of their financial statements and financial position using same rules and

regulations. In this report, there is proper analysis of the convergence project i.e. Being done by

jointly by International accounting standard board and Financial Accounting Standard Board, which

came out of an agreement by the two boards (IASB and FASB) . As in this report, it has clearly

mentioned about that how they are standard setters in a coordinated manner and how they will be

improving the quality and how it had positively impacted on investors and entities . Like

convergence has made the comparison between the organisation who operates globally. In the

second part of this report, it is all about Ketsu Department stores which is one of the Japan's largest

retailer with many stores throughout Japan. The consolidated financial statements have been drawn

up with standards issued by the international Accounting Standards Committee, in that reference

how simplified balance sheet helps in investment decision making. And more preference is been

given to working capital and its need.

In third part, there is an brief analysis of the financial performance of Muji , FMCG

company of Japan with the help of ratio analysis on the basis of three parameter .The parameters are

Liquidity ratio, Profitability ratio and Solvency ratio. These three parameters are also explained

with the subheading i.e. current ratio, acid test ratio, and return on asset, gross margin ratio, profit

margin ratio, debt to equity ratio and equity ratio with proper interpretation.

Question 1

Explain what the convergence project was intended to achieve and briefly explain the current status

of the project?

International Accounting Standards Board is a London based organisation. This organisation

is given full support of industry and government and it also set standards for accounting procedures.

IASB has responsibility for maintaining International Financial Reporting standards. The parent

entity of IASB is International Accounting Standard Committee. Financial Accounting Standard

Board establishes financial reporting and accounting standards for private and public companies and

the organisations who follow Generally Accepted Accounting Principles and that too they must be

not for procure key issues in it organisations. Their main objective was to eliminate the differences

between US GAAP and Financial reporting standards. FASB is one of the most important partner of

IASB. Board works so closely with national standard setters around the world. FASB got to know

that it does not have all solutions for all accounting issue. Some of the areas of US standard could

be improved where International standards can be easily applied (Jaruga and et.al., 2007).

The convergence project was intended to achieve standardisation with high quality foe entire

world, understandable and IFRS to serve lenders, creditors and ones who are in globalized market.

IASB and FASB made their best efforts to make their financial reporting standards fully practical

and compatible. Efforts were also made for coordinating their future work programs and to make

sure that they are achieved or not. Here the standard needs an improvement of both board, for

improvement they need to work jointly. FASB has involved itself in many different activities in the

context of high quality goal, standards and to increase the convergence of accounting standards

which are used in many countries. The most essential activity of FASB is its collaboration with

IASB to make optimum utilisation of resources. For convergence, staff of both boards made short

and long term strategies. In short term attempt was to remove the differences which appeared from

improvements project which were handled by IASB. Under convergence, IASB and FASB has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

undertaken many projects like business combinations. After several years, they will require the best

coordination between boards in context of setting and resource allocation.

Current status of convergence

There is a successful implementation of converging or accepting IFRS. At International level

also there is a positive impact of convergence and combination of accounting principle and

standards. Convergence has given most advantage to India in context of growth with globalization.

If any country does not play active role in process of setting standard internationally. There is an

safer route in converging process to IFRS is endorsement process and accepting temporary rid outs.

All countries have faced various difficulties and challenges earlier but after adopting all IFRSs they

got success from some particular date as it is. Many countries have adopted it even ICAI has also

taken decision to adapt IFRSs.

There is proper guidance on tax perspective, IFRS implications are also considered on direct

and indirect taxes. For more successful implementation, if companies use IFRS on daily basis for

financial reporting as well as to track the performance in budget form, management account and

forecasting (Hail, Leuz and Wysocki, 2010). It needs industry expertness but due to deficiency in

guidance in IFRS. There is also a requirement of improving the disclosures which also gives

support in viewing financial statements not for perspective of compliance but also for

communicating the performance. Basic need or compulsory need to make IFRS complaint

statements along with GAAP complaint statements. Because of complaint statements, problems can

be traced at early stage and can be corrected as soon as possible. For implementing IFRS properly

and efficiently, there is an need of deep international understanding about corporate objectives,

harmonisation goals and objectives and financial reporting objectives need to be achieved. Private

sector and government agencies should not be given stress by political pressure on International

Accounting Standards Board. The standards which are developed should be publicize and

accounting profession, corporate management and member countries all over the world should give

support to international Accounting Standard Board. Even the encouragement should be given by

International Accounting standard Board to all member bodies for adopting IFRS and to make and

remake their rules that they are queued along with IFRS. Proper rules and regulations must be

passed to the effect that if in any change or alteration in international Accounting Standard Board,

the local standards should be queued with this and local stock exchange can cooperate in taking step

forward against companies that fail to be with IFRS. To apply disciplinary procedures in non-

convergence with IFRS, governing bodies of accounting profession can be also used. Convergence

makes the reputation and relationship very well between corporate and community. These standards

will improve the efficiency of all global capital markets by improving comparability, decreasing

cost of capital and enhancing capital governance. Till now convergence of IASB and FASB has

become a great success for investor and entities that are operating globally.

Question 2

Critically discuss the advantages of convergence to BOTH investors and entities that operate

globally?

This convergence has specially focused on the big multinational companies. Convergence

helps in removing all weakness and inconsistencies in the existing revenue requirements. For

addressing revenue issues they provide a robust framework (Carmona and Trombetta, 2010). The

biggest advantage of convergence is enhancing comparability between companies in different

countries. Prior accounting standards were differing from country to country, before any of investor

compares two potential investments, they have to make the same format of accounting of both

companies and same for creditors also while evaluating creditworthiness, there are differences in

accounting standards. This brings huge variation in the financials of the company. This convergence

coordination between boards in context of setting and resource allocation.

Current status of convergence

There is a successful implementation of converging or accepting IFRS. At International level

also there is a positive impact of convergence and combination of accounting principle and

standards. Convergence has given most advantage to India in context of growth with globalization.

If any country does not play active role in process of setting standard internationally. There is an

safer route in converging process to IFRS is endorsement process and accepting temporary rid outs.

All countries have faced various difficulties and challenges earlier but after adopting all IFRSs they

got success from some particular date as it is. Many countries have adopted it even ICAI has also

taken decision to adapt IFRSs.

There is proper guidance on tax perspective, IFRS implications are also considered on direct

and indirect taxes. For more successful implementation, if companies use IFRS on daily basis for

financial reporting as well as to track the performance in budget form, management account and

forecasting (Hail, Leuz and Wysocki, 2010). It needs industry expertness but due to deficiency in

guidance in IFRS. There is also a requirement of improving the disclosures which also gives

support in viewing financial statements not for perspective of compliance but also for

communicating the performance. Basic need or compulsory need to make IFRS complaint

statements along with GAAP complaint statements. Because of complaint statements, problems can

be traced at early stage and can be corrected as soon as possible. For implementing IFRS properly

and efficiently, there is an need of deep international understanding about corporate objectives,

harmonisation goals and objectives and financial reporting objectives need to be achieved. Private

sector and government agencies should not be given stress by political pressure on International

Accounting Standards Board. The standards which are developed should be publicize and

accounting profession, corporate management and member countries all over the world should give

support to international Accounting Standard Board. Even the encouragement should be given by

International Accounting standard Board to all member bodies for adopting IFRS and to make and

remake their rules that they are queued along with IFRS. Proper rules and regulations must be

passed to the effect that if in any change or alteration in international Accounting Standard Board,

the local standards should be queued with this and local stock exchange can cooperate in taking step

forward against companies that fail to be with IFRS. To apply disciplinary procedures in non-

convergence with IFRS, governing bodies of accounting profession can be also used. Convergence

makes the reputation and relationship very well between corporate and community. These standards

will improve the efficiency of all global capital markets by improving comparability, decreasing

cost of capital and enhancing capital governance. Till now convergence of IASB and FASB has

become a great success for investor and entities that are operating globally.

Question 2

Critically discuss the advantages of convergence to BOTH investors and entities that operate

globally?

This convergence has specially focused on the big multinational companies. Convergence

helps in removing all weakness and inconsistencies in the existing revenue requirements. For

addressing revenue issues they provide a robust framework (Carmona and Trombetta, 2010). The

biggest advantage of convergence is enhancing comparability between companies in different

countries. Prior accounting standards were differing from country to country, before any of investor

compares two potential investments, they have to make the same format of accounting of both

companies and same for creditors also while evaluating creditworthiness, there are differences in

accounting standards. This brings huge variation in the financials of the company. This convergence

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

put comparison on equal heads, which makes easier to the investors and entity for evaluating

international options for investing and managing cash. Many investors do not have enough

resources to effectively compare so if financial statements are more comparable or on equal heads,

then they will be able to compare the financials in house.

This convergence also helps in removing barriers for expansion of companies. If any

company wants to expand internationally then there is need of compliance of international cost. If

they are in same set of accounting standards, then it will create ease in expanding. It gives high

quality, globally recognised accounting standards which gives transparency, efficiency and

accountability. These standards gives transparency by quality of information and globally

comparability, enables investors and others to make prior informed economic discussions. By

reducing gap in information between the capital providers and people whom they have given surety

for money, strengthen accountability (Jackling, Howieson and Natoli, 2012). These standards gives

all the information that is needed by management. It contributes to economic efficiency by helping

out investors in identifying the opportunities and risk across the world. It improves the allocation of

capital. It gives useful information to users of financial statements through improved disclosed

requirement.

All these things helps industry to grow and all the advantages are related to corporate in

country, they also bring consistency between external and internal reporting aligned with risk rating

with all international investors. This international comparison also improves in benefiting all

industrial and capital markets in the country.

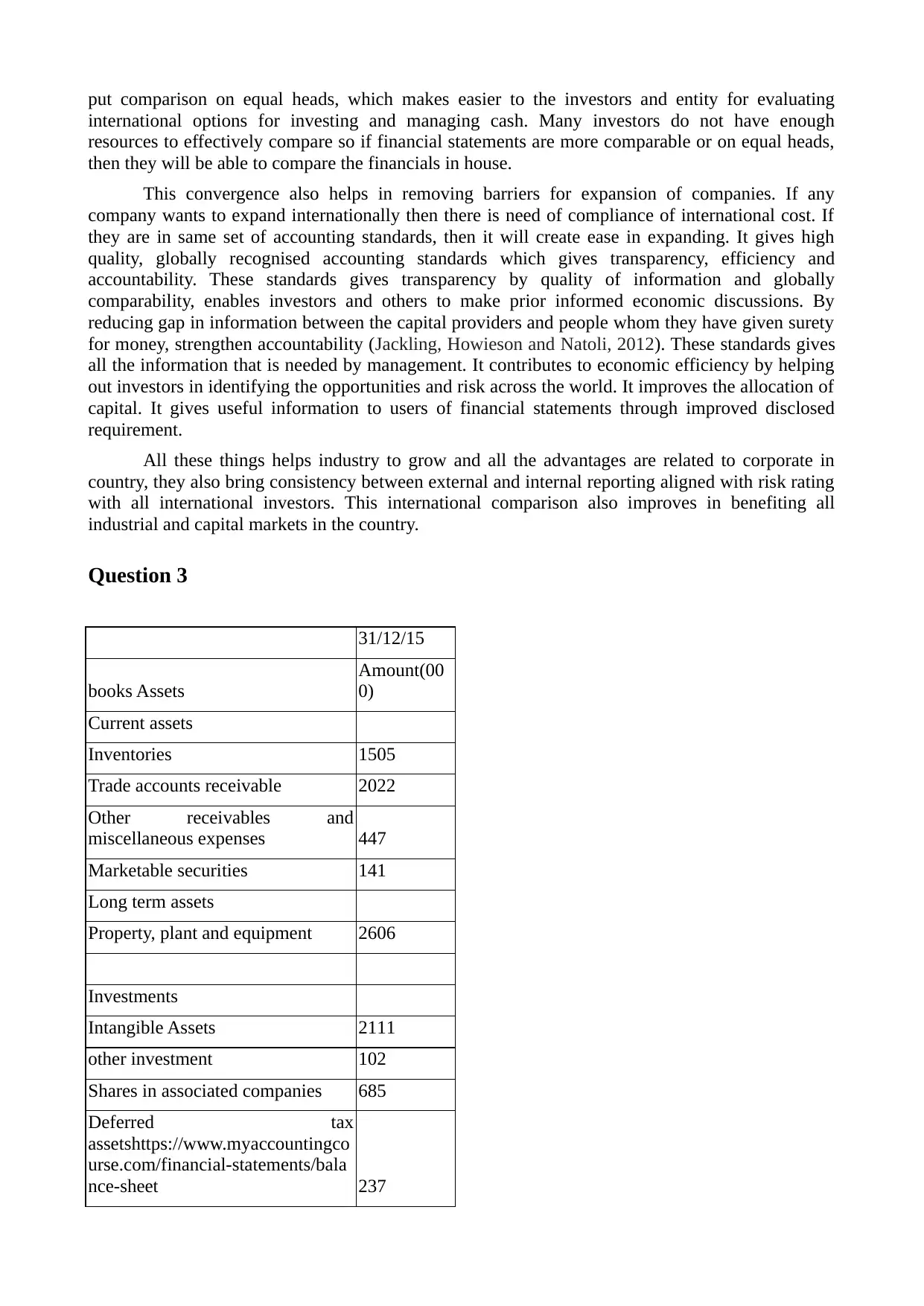

Question 3

31/12/15

books Assets

Amount(00

0)

Current assets

Inventories 1505

Trade accounts receivable 2022

Other receivables and

miscellaneous expenses 447

Marketable securities 141

Long term assets

Property, plant and equipment 2606

Investments

Intangible Assets 2111

other investment 102

Shares in associated companies 685

Deferred tax

assetshttps://www.myaccountingco

urse.com/financial-statements/bala

nce-sheet 237

international options for investing and managing cash. Many investors do not have enough

resources to effectively compare so if financial statements are more comparable or on equal heads,

then they will be able to compare the financials in house.

This convergence also helps in removing barriers for expansion of companies. If any

company wants to expand internationally then there is need of compliance of international cost. If

they are in same set of accounting standards, then it will create ease in expanding. It gives high

quality, globally recognised accounting standards which gives transparency, efficiency and

accountability. These standards gives transparency by quality of information and globally

comparability, enables investors and others to make prior informed economic discussions. By

reducing gap in information between the capital providers and people whom they have given surety

for money, strengthen accountability (Jackling, Howieson and Natoli, 2012). These standards gives

all the information that is needed by management. It contributes to economic efficiency by helping

out investors in identifying the opportunities and risk across the world. It improves the allocation of

capital. It gives useful information to users of financial statements through improved disclosed

requirement.

All these things helps industry to grow and all the advantages are related to corporate in

country, they also bring consistency between external and internal reporting aligned with risk rating

with all international investors. This international comparison also improves in benefiting all

industrial and capital markets in the country.

Question 3

31/12/15

books Assets

Amount(00

0)

Current assets

Inventories 1505

Trade accounts receivable 2022

Other receivables and

miscellaneous expenses 447

Marketable securities 141

Long term assets

Property, plant and equipment 2606

Investments

Intangible Assets 2111

other investment 102

Shares in associated companies 685

Deferred tax

assetshttps://www.myaccountingco

urse.com/financial-statements/bala

nce-sheet 237

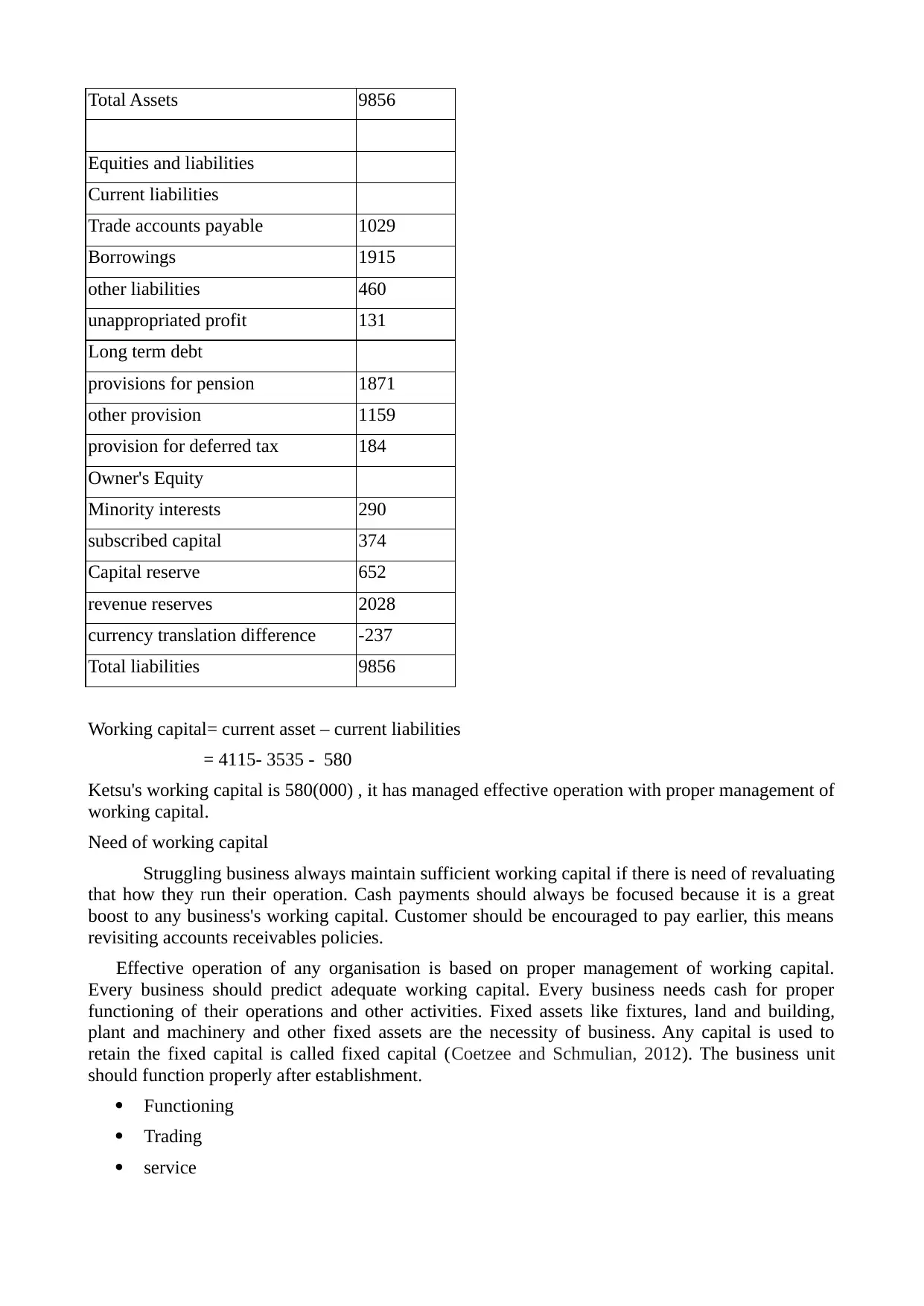

Total Assets 9856

Equities and liabilities

Current liabilities

Trade accounts payable 1029

Borrowings 1915

other liabilities 460

unappropriated profit 131

Long term debt

provisions for pension 1871

other provision 1159

provision for deferred tax 184

Owner's Equity

Minority interests 290

subscribed capital 374

Capital reserve 652

revenue reserves 2028

currency translation difference -237

Total liabilities 9856

Working capital= current asset – current liabilities

= 4115- 3535 - 580

Ketsu's working capital is 580(000) , it has managed effective operation with proper management of

working capital.

Need of working capital

Struggling business always maintain sufficient working capital if there is need of revaluating

that how they run their operation. Cash payments should always be focused because it is a great

boost to any business's working capital. Customer should be encouraged to pay earlier, this means

revisiting accounts receivables policies.

Effective operation of any organisation is based on proper management of working capital.

Every business should predict adequate working capital. Every business needs cash for proper

functioning of their operations and other activities. Fixed assets like fixtures, land and building,

plant and machinery and other fixed assets are the necessity of business. Any capital is used to

retain the fixed capital is called fixed capital (Coetzee and Schmulian, 2012). The business unit

should function properly after establishment.

Functioning

Trading

service

Equities and liabilities

Current liabilities

Trade accounts payable 1029

Borrowings 1915

other liabilities 460

unappropriated profit 131

Long term debt

provisions for pension 1871

other provision 1159

provision for deferred tax 184

Owner's Equity

Minority interests 290

subscribed capital 374

Capital reserve 652

revenue reserves 2028

currency translation difference -237

Total liabilities 9856

Working capital= current asset – current liabilities

= 4115- 3535 - 580

Ketsu's working capital is 580(000) , it has managed effective operation with proper management of

working capital.

Need of working capital

Struggling business always maintain sufficient working capital if there is need of revaluating

that how they run their operation. Cash payments should always be focused because it is a great

boost to any business's working capital. Customer should be encouraged to pay earlier, this means

revisiting accounts receivables policies.

Effective operation of any organisation is based on proper management of working capital.

Every business should predict adequate working capital. Every business needs cash for proper

functioning of their operations and other activities. Fixed assets like fixtures, land and building,

plant and machinery and other fixed assets are the necessity of business. Any capital is used to

retain the fixed capital is called fixed capital (Coetzee and Schmulian, 2012). The business unit

should function properly after establishment.

Functioning

Trading

service

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Functioning means activities like trading, manufacturing or service. Trading is selling and buying of

goods without any alteration in goods and service signifies taking care of all intangible things like

electricity, courier service, lorry service and many more like this. Manufacturing is converting raw

materials into finished product for sale.

Each and every business unit has need of working capital for its proper functioning like to

bear daily expenses. That type of capital is known as working capital. Some other names of working

capital are revolving capital and circulating capital (Jackling, 2013).

Net cash

Net cash implies to the difference between cash and liabilities. It is usually used in business

like to determine the current ratio and the ability of company to pay off its all obligations. It can be

also used to know the amount of cash which is left after all transactions.

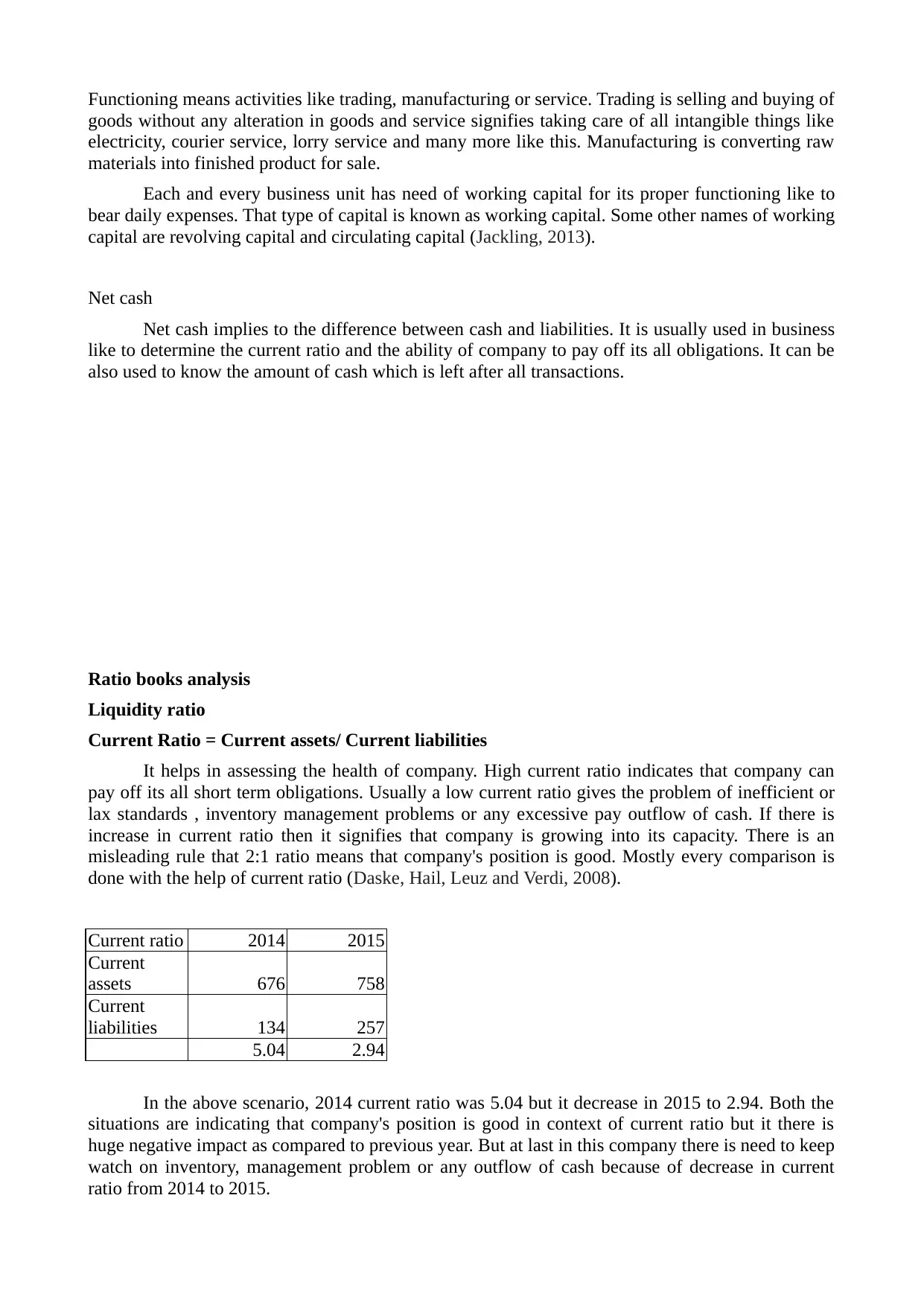

Ratio books analysis

Liquidity ratio

Current Ratio = Current assets/ Current liabilities

It helps in assessing the health of company. High current ratio indicates that company can

pay off its all short term obligations. Usually a low current ratio gives the problem of inefficient or

lax standards , inventory management problems or any excessive pay outflow of cash. If there is

increase in current ratio then it signifies that company is growing into its capacity. There is an

misleading rule that 2:1 ratio means that company's position is good. Mostly every comparison is

done with the help of current ratio (Daske, Hail, Leuz and Verdi, 2008).

Current ratio 2014 2015

Current

assets 676 758

Current

liabilities 134 257

5.04 2.94

In the above scenario, 2014 current ratio was 5.04 but it decrease in 2015 to 2.94. Both the

situations are indicating that company's position is good in context of current ratio but it there is

huge negative impact as compared to previous year. But at last in this company there is need to keep

watch on inventory, management problem or any outflow of cash because of decrease in current

ratio from 2014 to 2015.

goods without any alteration in goods and service signifies taking care of all intangible things like

electricity, courier service, lorry service and many more like this. Manufacturing is converting raw

materials into finished product for sale.

Each and every business unit has need of working capital for its proper functioning like to

bear daily expenses. That type of capital is known as working capital. Some other names of working

capital are revolving capital and circulating capital (Jackling, 2013).

Net cash

Net cash implies to the difference between cash and liabilities. It is usually used in business

like to determine the current ratio and the ability of company to pay off its all obligations. It can be

also used to know the amount of cash which is left after all transactions.

Ratio books analysis

Liquidity ratio

Current Ratio = Current assets/ Current liabilities

It helps in assessing the health of company. High current ratio indicates that company can

pay off its all short term obligations. Usually a low current ratio gives the problem of inefficient or

lax standards , inventory management problems or any excessive pay outflow of cash. If there is

increase in current ratio then it signifies that company is growing into its capacity. There is an

misleading rule that 2:1 ratio means that company's position is good. Mostly every comparison is

done with the help of current ratio (Daske, Hail, Leuz and Verdi, 2008).

Current ratio 2014 2015

Current

assets 676 758

Current

liabilities 134 257

5.04 2.94

In the above scenario, 2014 current ratio was 5.04 but it decrease in 2015 to 2.94. Both the

situations are indicating that company's position is good in context of current ratio but it there is

huge negative impact as compared to previous year. But at last in this company there is need to keep

watch on inventory, management problem or any outflow of cash because of decrease in current

ratio from 2014 to 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

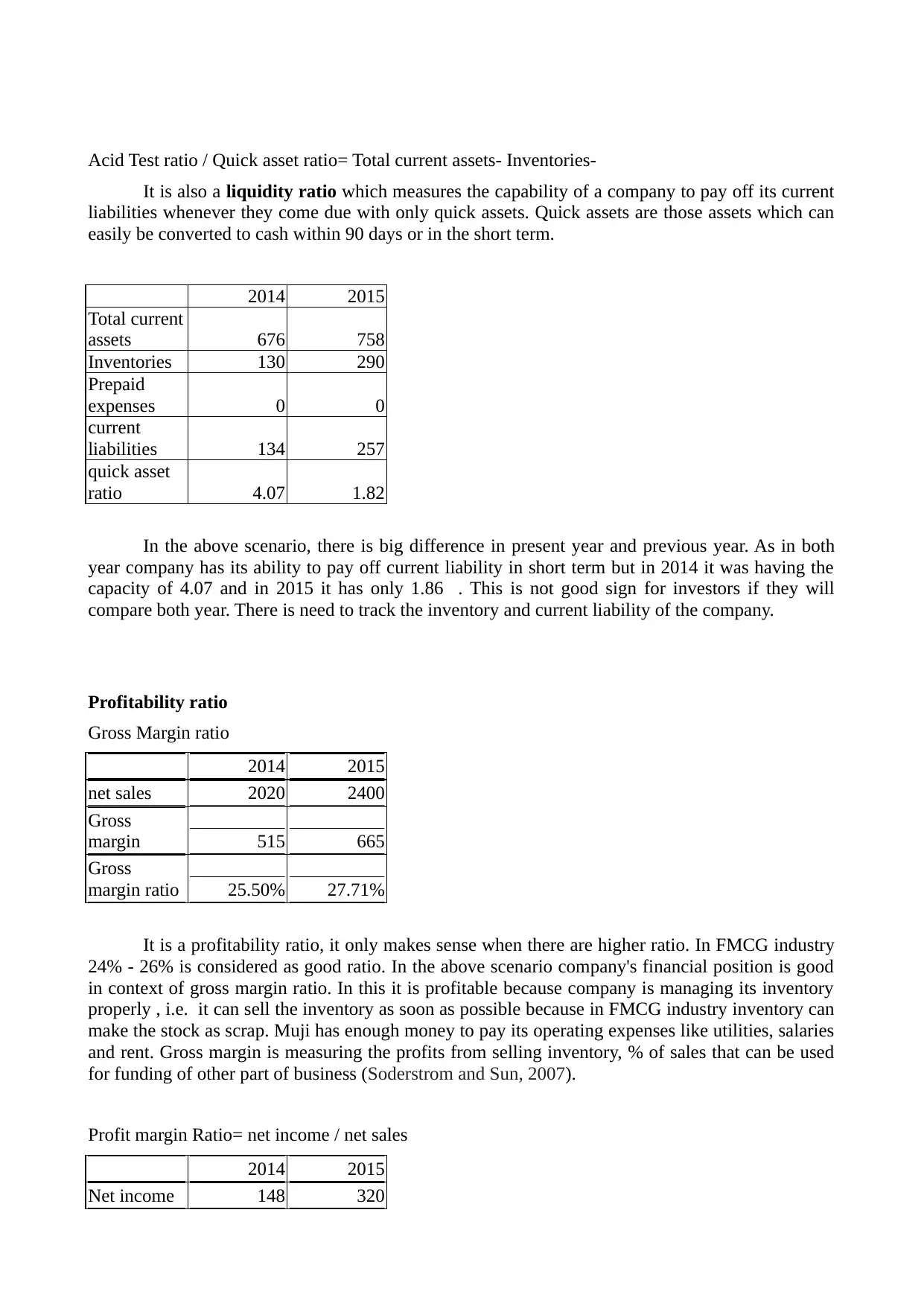

Acid Test ratio / Quick asset ratio= Total current assets- Inventories-

It is also a liquidity ratio which measures the capability of a company to pay off its current

liabilities whenever they come due with only quick assets. Quick assets are those assets which can

easily be converted to cash within 90 days or in the short term.

2014 2015

Total current

assets 676 758

Inventories 130 290

Prepaid

expenses 0 0

current

liabilities 134 257

quick asset

ratio 4.07 1.82

In the above scenario, there is big difference in present year and previous year. As in both

year company has its ability to pay off current liability in short term but in 2014 it was having the

capacity of 4.07 and in 2015 it has only 1.86 . This is not good sign for investors if they will

compare both year. There is need to track the inventory and current liability of the company.

Profitability ratio

Gross Margin ratio

2014 2015

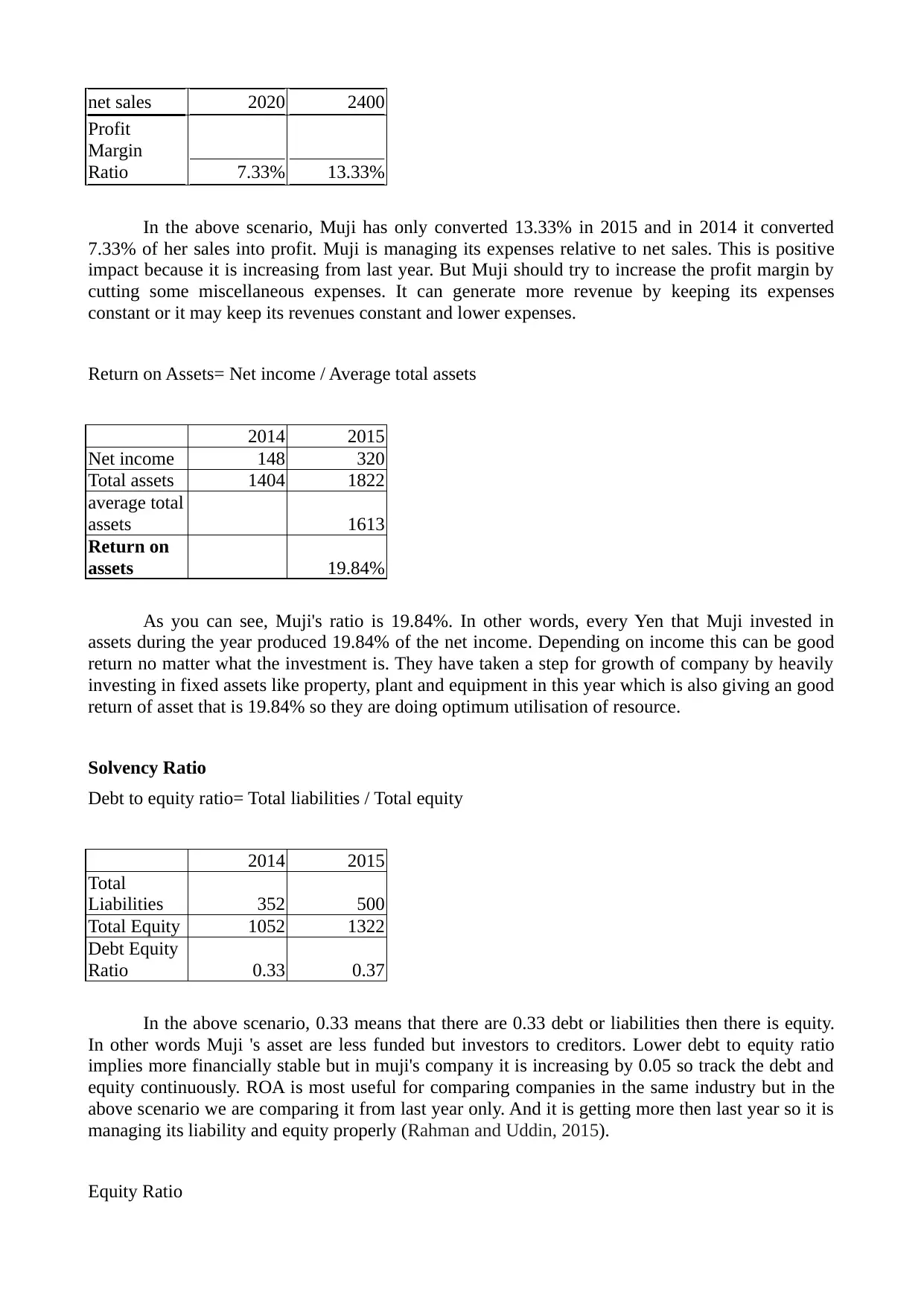

net sales 2020 2400

Gross

margin 515 665

Gross

margin ratio 25.50% 27.71%

It is a profitability ratio, it only makes sense when there are higher ratio. In FMCG industry

24% - 26% is considered as good ratio. In the above scenario company's financial position is good

in context of gross margin ratio. In this it is profitable because company is managing its inventory

properly , i.e. it can sell the inventory as soon as possible because in FMCG industry inventory can

make the stock as scrap. Muji has enough money to pay its operating expenses like utilities, salaries

and rent. Gross margin is measuring the profits from selling inventory, % of sales that can be used

for funding of other part of business (Soderstrom and Sun, 2007).

Profit margin Ratio= net income / net sales

2014 2015

Net income 148 320

It is also a liquidity ratio which measures the capability of a company to pay off its current

liabilities whenever they come due with only quick assets. Quick assets are those assets which can

easily be converted to cash within 90 days or in the short term.

2014 2015

Total current

assets 676 758

Inventories 130 290

Prepaid

expenses 0 0

current

liabilities 134 257

quick asset

ratio 4.07 1.82

In the above scenario, there is big difference in present year and previous year. As in both

year company has its ability to pay off current liability in short term but in 2014 it was having the

capacity of 4.07 and in 2015 it has only 1.86 . This is not good sign for investors if they will

compare both year. There is need to track the inventory and current liability of the company.

Profitability ratio

Gross Margin ratio

2014 2015

net sales 2020 2400

Gross

margin 515 665

Gross

margin ratio 25.50% 27.71%

It is a profitability ratio, it only makes sense when there are higher ratio. In FMCG industry

24% - 26% is considered as good ratio. In the above scenario company's financial position is good

in context of gross margin ratio. In this it is profitable because company is managing its inventory

properly , i.e. it can sell the inventory as soon as possible because in FMCG industry inventory can

make the stock as scrap. Muji has enough money to pay its operating expenses like utilities, salaries

and rent. Gross margin is measuring the profits from selling inventory, % of sales that can be used

for funding of other part of business (Soderstrom and Sun, 2007).

Profit margin Ratio= net income / net sales

2014 2015

Net income 148 320

net sales 2020 2400

Profit

Margin

Ratio 7.33% 13.33%

In the above scenario, Muji has only converted 13.33% in 2015 and in 2014 it converted

7.33% of her sales into profit. Muji is managing its expenses relative to net sales. This is positive

impact because it is increasing from last year. But Muji should try to increase the profit margin by

cutting some miscellaneous expenses. It can generate more revenue by keeping its expenses

constant or it may keep its revenues constant and lower expenses.

Return on Assets= Net income / Average total assets

2014 2015

Net income 148 320

Total assets 1404 1822

average total

assets 1613

Return on

assets 19.84%

As you can see, Muji's ratio is 19.84%. In other words, every Yen that Muji invested in

assets during the year produced 19.84% of the net income. Depending on income this can be good

return no matter what the investment is. They have taken a step for growth of company by heavily

investing in fixed assets like property, plant and equipment in this year which is also giving an good

return of asset that is 19.84% so they are doing optimum utilisation of resource.

Solvency Ratio

Debt to equity ratio= Total liabilities / Total equity

2014 2015

Total

Liabilities 352 500

Total Equity 1052 1322

Debt Equity

Ratio 0.33 0.37

In the above scenario, 0.33 means that there are 0.33 debt or liabilities then there is equity.

In other words Muji 's asset are less funded but investors to creditors. Lower debt to equity ratio

implies more financially stable but in muji's company it is increasing by 0.05 so track the debt and

equity continuously. ROA is most useful for comparing companies in the same industry but in the

above scenario we are comparing it from last year only. And it is getting more then last year so it is

managing its liability and equity properly (Rahman and Uddin, 2015).

Equity Ratio

Profit

Margin

Ratio 7.33% 13.33%

In the above scenario, Muji has only converted 13.33% in 2015 and in 2014 it converted

7.33% of her sales into profit. Muji is managing its expenses relative to net sales. This is positive

impact because it is increasing from last year. But Muji should try to increase the profit margin by

cutting some miscellaneous expenses. It can generate more revenue by keeping its expenses

constant or it may keep its revenues constant and lower expenses.

Return on Assets= Net income / Average total assets

2014 2015

Net income 148 320

Total assets 1404 1822

average total

assets 1613

Return on

assets 19.84%

As you can see, Muji's ratio is 19.84%. In other words, every Yen that Muji invested in

assets during the year produced 19.84% of the net income. Depending on income this can be good

return no matter what the investment is. They have taken a step for growth of company by heavily

investing in fixed assets like property, plant and equipment in this year which is also giving an good

return of asset that is 19.84% so they are doing optimum utilisation of resource.

Solvency Ratio

Debt to equity ratio= Total liabilities / Total equity

2014 2015

Total

Liabilities 352 500

Total Equity 1052 1322

Debt Equity

Ratio 0.33 0.37

In the above scenario, 0.33 means that there are 0.33 debt or liabilities then there is equity.

In other words Muji 's asset are less funded but investors to creditors. Lower debt to equity ratio

implies more financially stable but in muji's company it is increasing by 0.05 so track the debt and

equity continuously. ROA is most useful for comparing companies in the same industry but in the

above scenario we are comparing it from last year only. And it is getting more then last year so it is

managing its liability and equity properly (Rahman and Uddin, 2015).

Equity Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

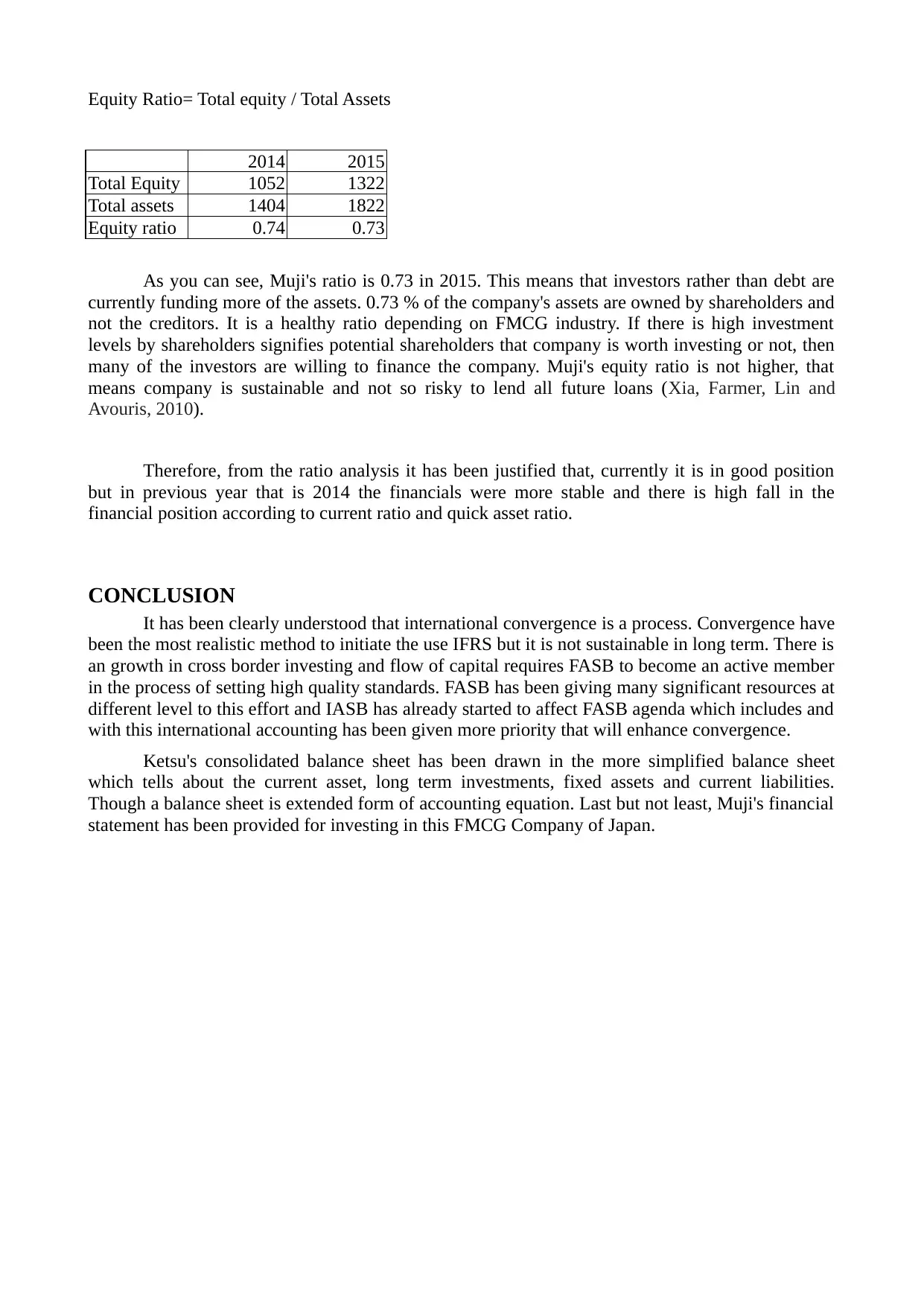

Equity Ratio= Total equity / Total Assets

2014 2015

Total Equity 1052 1322

Total assets 1404 1822

Equity ratio 0.74 0.73

As you can see, Muji's ratio is 0.73 in 2015. This means that investors rather than debt are

currently funding more of the assets. 0.73 % of the company's assets are owned by shareholders and

not the creditors. It is a healthy ratio depending on FMCG industry. If there is high investment

levels by shareholders signifies potential shareholders that company is worth investing or not, then

many of the investors are willing to finance the company. Muji's equity ratio is not higher, that

means company is sustainable and not so risky to lend all future loans (Xia, Farmer, Lin and

Avouris, 2010).

Therefore, from the ratio analysis it has been justified that, currently it is in good position

but in previous year that is 2014 the financials were more stable and there is high fall in the

financial position according to current ratio and quick asset ratio.

CONCLUSION

It has been clearly understood that international convergence is a process. Convergence have

been the most realistic method to initiate the use IFRS but it is not sustainable in long term. There is

an growth in cross border investing and flow of capital requires FASB to become an active member

in the process of setting high quality standards. FASB has been giving many significant resources at

different level to this effort and IASB has already started to affect FASB agenda which includes and

with this international accounting has been given more priority that will enhance convergence.

Ketsu's consolidated balance sheet has been drawn in the more simplified balance sheet

which tells about the current asset, long term investments, fixed assets and current liabilities.

Though a balance sheet is extended form of accounting equation. Last but not least, Muji's financial

statement has been provided for investing in this FMCG Company of Japan.

2014 2015

Total Equity 1052 1322

Total assets 1404 1822

Equity ratio 0.74 0.73

As you can see, Muji's ratio is 0.73 in 2015. This means that investors rather than debt are

currently funding more of the assets. 0.73 % of the company's assets are owned by shareholders and

not the creditors. It is a healthy ratio depending on FMCG industry. If there is high investment

levels by shareholders signifies potential shareholders that company is worth investing or not, then

many of the investors are willing to finance the company. Muji's equity ratio is not higher, that

means company is sustainable and not so risky to lend all future loans (Xia, Farmer, Lin and

Avouris, 2010).

Therefore, from the ratio analysis it has been justified that, currently it is in good position

but in previous year that is 2014 the financials were more stable and there is high fall in the

financial position according to current ratio and quick asset ratio.

CONCLUSION

It has been clearly understood that international convergence is a process. Convergence have

been the most realistic method to initiate the use IFRS but it is not sustainable in long term. There is

an growth in cross border investing and flow of capital requires FASB to become an active member

in the process of setting high quality standards. FASB has been giving many significant resources at

different level to this effort and IASB has already started to affect FASB agenda which includes and

with this international accounting has been given more priority that will enhance convergence.

Ketsu's consolidated balance sheet has been drawn in the more simplified balance sheet

which tells about the current asset, long term investments, fixed assets and current liabilities.

Though a balance sheet is extended form of accounting equation. Last but not least, Muji's financial

statement has been provided for investing in this FMCG Company of Japan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Carmona, S. and Trombetta, M., 2010. The IASB and FASB convergence process and the need for

‘concept-based’accounting teaching. Advances in Accounting. 26(1). pp.1-5.

Coetzee, S. A. and Schmulian, A., 2012. A critical analysis of the pedagogical approach employed

in an introductory course to IFRS. Issues in accounting Education. 27(1). pp.83-100.

Daske, H., Hail, L., Leuz, C. and Verdi, R., 2008. Mandatory IFRS reporting around the world:

Early evidence on the economic consequences. Journal of accounting research. 46(5). pp.1085-

1142.

Hail, L., Leuz, C. and Wysocki, P., 2010. Global accounting convergence and the potential adoption

of IFRS by the US (Part II): Political factors and future scenarios for US accounting

standards. Accounting Horizons. 24(4). pp.567-588.

Jackling, B., 2013. Global adoption of International Financial Reporting Standards: implications for

accounting education. Issues in Accounting Education. 28(2). pp.209-220.

Jackling, B., Howieson, B. and Natoli, R., 2012. Some implications of IFRS adoption for

accounting education. Australian Accounting Review. 22(4). pp.331-340.

Jaruga, A. and et.al., 2007. The impact of IAS/IFRS on Polish accounting regulations and their

practical implementation in Poland. Accounting in Europe. 4(1). pp.67-78.

Rahman, M. M. and Uddin, M. N., 2015. Measuring the relationship between working capital

management and profitability: Empirical evidence from Bangladesh. Journal of Accounting and

Finance. 15(8). p.120.

Soderstrom, N. S. and Sun, K .J., 2007. IFRS adoption and accounting quality: a review. European

Accounting Review. 16(4). pp.675-702.

Xia, F., Farmer, D. B., Lin, Y. M. and Avouris, P., 2010. Graphene field-effect transistors with high

on/off current ratio and large transport band gap at room temperature. Nano letters. 10(2). pp.715-

718.

Carmona, S. and Trombetta, M., 2010. The IASB and FASB convergence process and the need for

‘concept-based’accounting teaching. Advances in Accounting. 26(1). pp.1-5.

Coetzee, S. A. and Schmulian, A., 2012. A critical analysis of the pedagogical approach employed

in an introductory course to IFRS. Issues in accounting Education. 27(1). pp.83-100.

Daske, H., Hail, L., Leuz, C. and Verdi, R., 2008. Mandatory IFRS reporting around the world:

Early evidence on the economic consequences. Journal of accounting research. 46(5). pp.1085-

1142.

Hail, L., Leuz, C. and Wysocki, P., 2010. Global accounting convergence and the potential adoption

of IFRS by the US (Part II): Political factors and future scenarios for US accounting

standards. Accounting Horizons. 24(4). pp.567-588.

Jackling, B., 2013. Global adoption of International Financial Reporting Standards: implications for

accounting education. Issues in Accounting Education. 28(2). pp.209-220.

Jackling, B., Howieson, B. and Natoli, R., 2012. Some implications of IFRS adoption for

accounting education. Australian Accounting Review. 22(4). pp.331-340.

Jaruga, A. and et.al., 2007. The impact of IAS/IFRS on Polish accounting regulations and their

practical implementation in Poland. Accounting in Europe. 4(1). pp.67-78.

Rahman, M. M. and Uddin, M. N., 2015. Measuring the relationship between working capital

management and profitability: Empirical evidence from Bangladesh. Journal of Accounting and

Finance. 15(8). p.120.

Soderstrom, N. S. and Sun, K .J., 2007. IFRS adoption and accounting quality: a review. European

Accounting Review. 16(4). pp.675-702.

Xia, F., Farmer, D. B., Lin, Y. M. and Avouris, P., 2010. Graphene field-effect transistors with high

on/off current ratio and large transport band gap at room temperature. Nano letters. 10(2). pp.715-

718.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.