Analysis of Investment Projects in International Financial Management

VerifiedAdded on 2023/01/07

|9

|2020

|83

Report

AI Summary

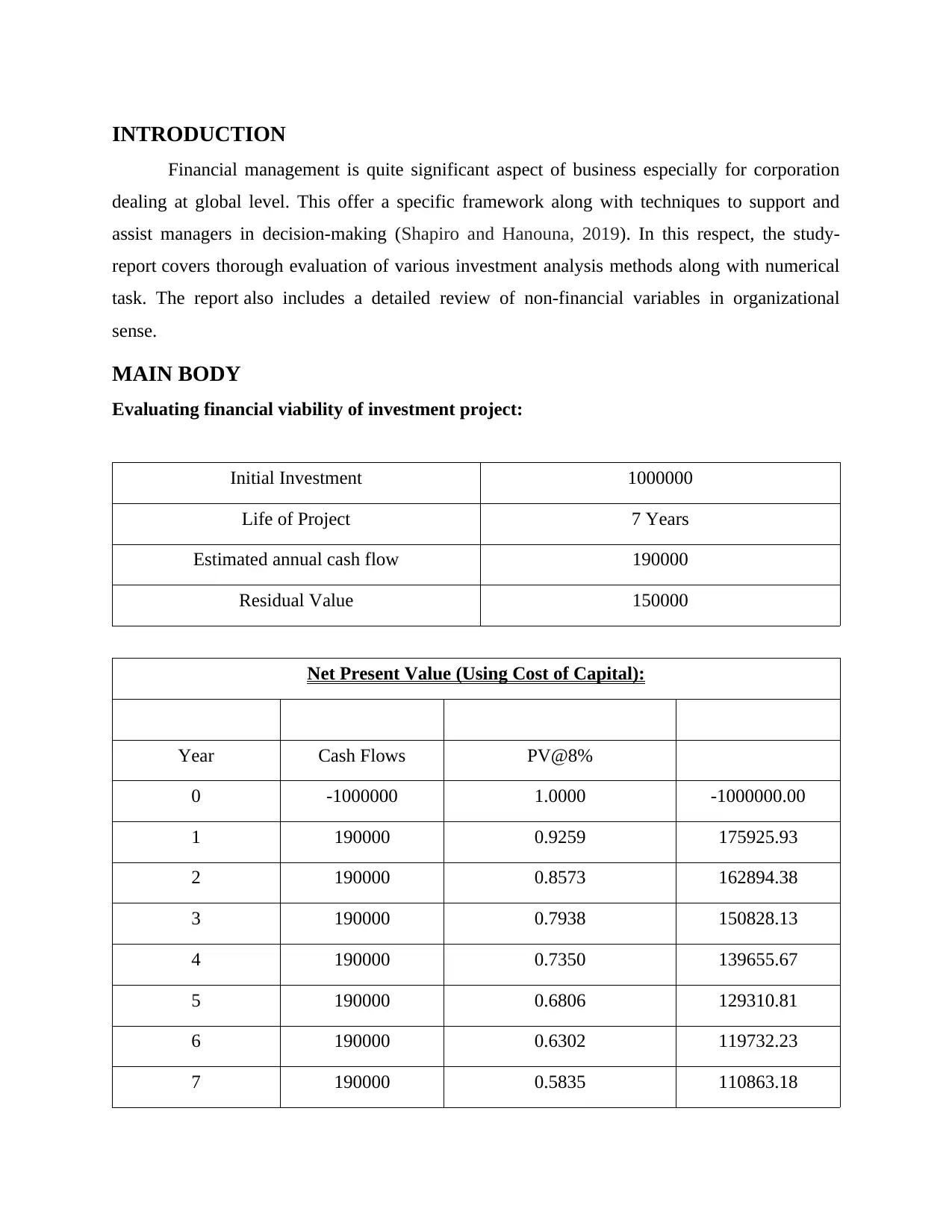

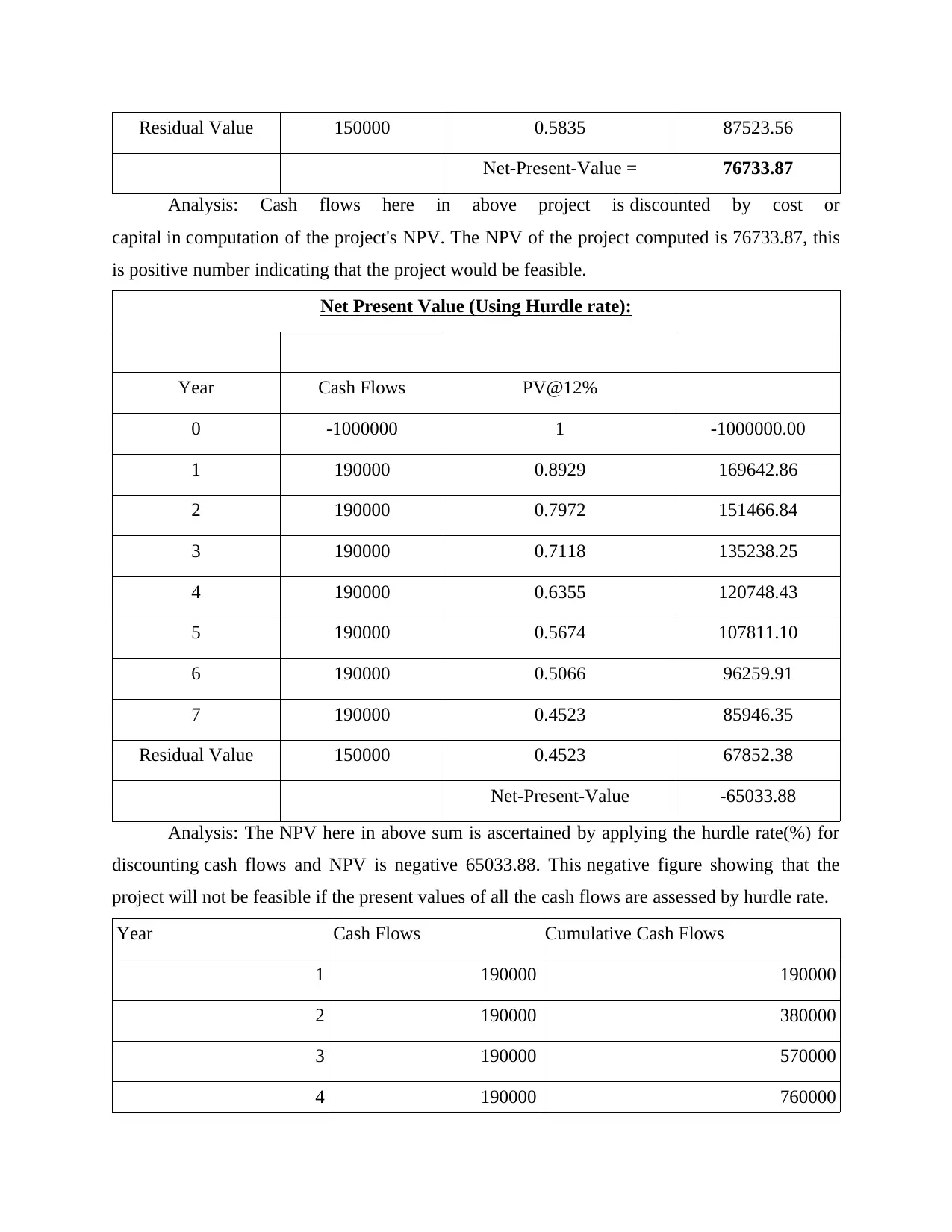

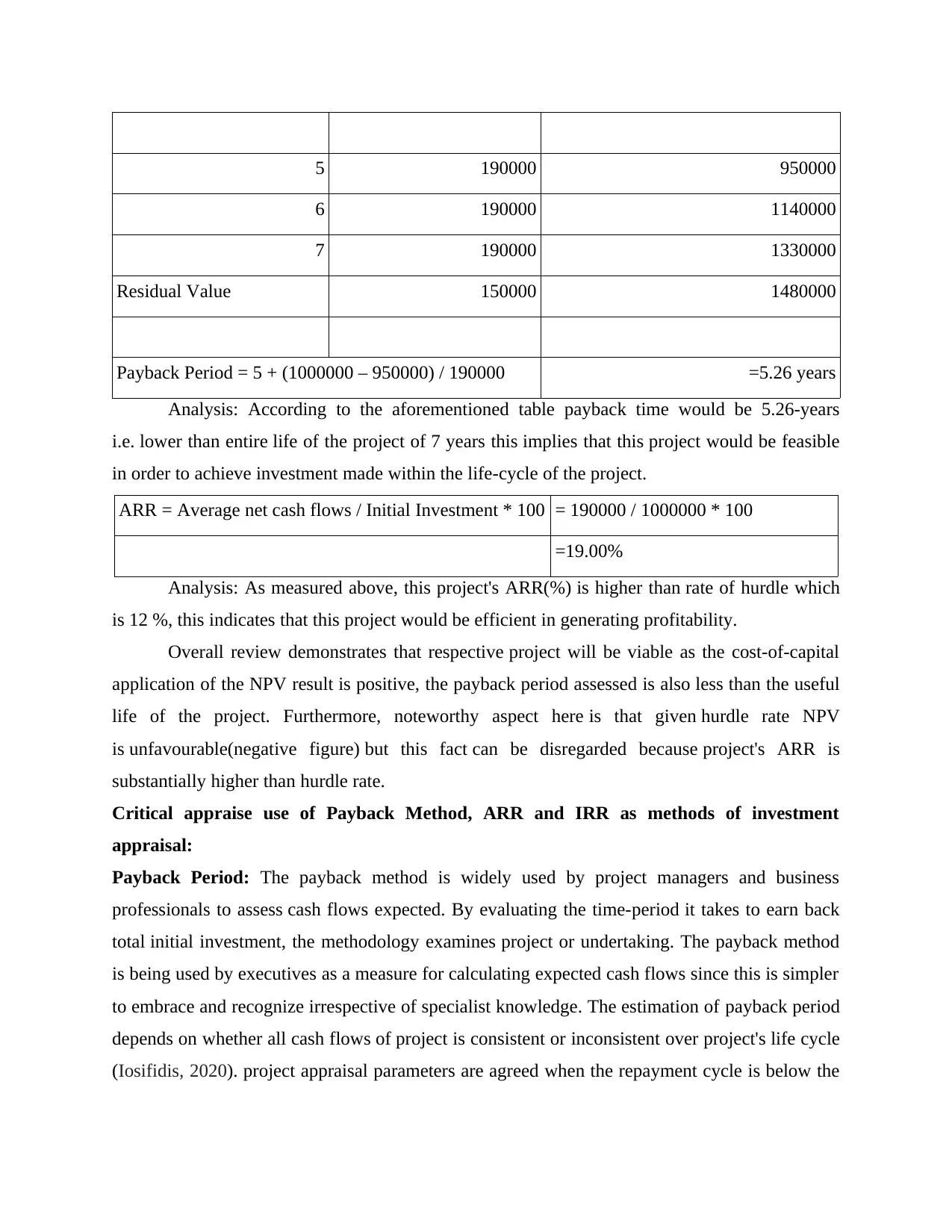

This report provides a comprehensive analysis of international financial management, focusing on investment appraisal techniques. It begins with an introduction to financial management and its importance in a global context. The main body of the report includes a detailed evaluation of investment analysis methods such as Net Present Value (NPV), payback period, Average Rate of Return (ARR), and Internal Rate of Return (IRR), along with numerical examples. The report explores the financial viability of an investment project using different discount rates and analyzes the payback period and ARR. Furthermore, the report critically appraises the use of payback, ARR, and IRR methods, discussing their advantages and disadvantages. It also examines non-financial variables like relationships with vendors and consumers, industry norms, current and future legislation, and external factors like inflation. The report concludes by emphasizing the importance of both financial and non-financial variables in making sound investment decisions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.