Analyzing Financial Ratios for Effective Hotel Management

VerifiedAdded on 2023/01/10

|13

|3148

|93

Report

AI Summary

This report provides a comprehensive analysis of financial ratios within the context of hotel management, using Gatsby Grange, a boutique hotel chain in the UK and Northern Ireland, as a case study. The report begins with an introduction to financial management and its significance in the hotel and tourism industry. It then delves into the calculation and analysis of various financial ratios, including profitability (net and gross profit margins), liquidity (current and quick ratios), and gearing ratios (debt-equity and equity ratios). The analysis covers trends from 2018 to 2019. The report emphasizes the importance of understanding these ratios and their fluctuations for effective hotel management, highlighting their role in assessing financial solvency, identifying trends, and supporting forecasting and planning. Furthermore, the report discusses the benefits and limitations of ratio analysis in decision-making within the hotel and tourism industry, acknowledging its role in simplifying complex financial statements and facilitating comparisons while also recognizing its limitations in ignoring qualitative aspects and inflation. The report concludes with a summary of the key findings and their implications for hotel management practices.

International hotel

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

a) Calculating and analysing financial ratios...............................................................................1

b) Discussing why an understanding of ratios and their fluctuations is essential for Hotel

management.................................................................................................................................7

c) Benefits and limitations of ratio analysis in decision making within hotel and tourism

industry........................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

a) Calculating and analysing financial ratios...............................................................................1

b) Discussing why an understanding of ratios and their fluctuations is essential for Hotel

management.................................................................................................................................7

c) Benefits and limitations of ratio analysis in decision making within hotel and tourism

industry........................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management is a procedure of managing the financial performance and position of an

organisation (Ahrendsen and Katchova, 2012). This procedure is the combination of various

activities including procuring and utilization of funds, recording and transacting financial records

and many more. The main aim of this report is to build an understanding about the financial

management in hotel and tourism industry. For this purpose, the organisation which has been

given is operating in hotel industry and named as Gatsby Grange. This organisation is a small

chain of Boutique within the region of United Kingdom and Northern Ireland.

In this report, the financial ratios of Gatsby Grange will be calculated by using their financial

statements. This report will include an analysis of ratios and their fluctuations in order to

understand why they are important for hotel management. Lastly in this report, benefits and

limitations of ratio analysis will be identified and analysed that impact the decision making of

hotel and tourism industry (Kansal, Joshi and Batra, 2014).

MAIN BODY

a) Calculating and analysing financial ratios

Ratio analysis is a financial technique to identify the true financial performance and position of a

business organisation (Mathuva, 2015). These ratios are calculated using the financial statements

of a company which are income statement, balance sheet and cash flow statement. In the present

case of Gatsby Grange, the ration analysis has been conducted for three ratio families which are

profitability, liquidity and gearing.

Profitability ratios

This family for the ratios is associated with the profit making ability of an organisation (Olson

and Groves, 2012). The ratios of profitability are the metrics which helps in analyse the relative

income of an organisation against the revenue, costs and assets. Ratios which are selected to

compute profitability of Gatsby Grange are net and gross margin.

Net profit margin

Net profit margin

Formula Net income / net sales * 100

2018 2019

1

Financial management is a procedure of managing the financial performance and position of an

organisation (Ahrendsen and Katchova, 2012). This procedure is the combination of various

activities including procuring and utilization of funds, recording and transacting financial records

and many more. The main aim of this report is to build an understanding about the financial

management in hotel and tourism industry. For this purpose, the organisation which has been

given is operating in hotel industry and named as Gatsby Grange. This organisation is a small

chain of Boutique within the region of United Kingdom and Northern Ireland.

In this report, the financial ratios of Gatsby Grange will be calculated by using their financial

statements. This report will include an analysis of ratios and their fluctuations in order to

understand why they are important for hotel management. Lastly in this report, benefits and

limitations of ratio analysis will be identified and analysed that impact the decision making of

hotel and tourism industry (Kansal, Joshi and Batra, 2014).

MAIN BODY

a) Calculating and analysing financial ratios

Ratio analysis is a financial technique to identify the true financial performance and position of a

business organisation (Mathuva, 2015). These ratios are calculated using the financial statements

of a company which are income statement, balance sheet and cash flow statement. In the present

case of Gatsby Grange, the ration analysis has been conducted for three ratio families which are

profitability, liquidity and gearing.

Profitability ratios

This family for the ratios is associated with the profit making ability of an organisation (Olson

and Groves, 2012). The ratios of profitability are the metrics which helps in analyse the relative

income of an organisation against the revenue, costs and assets. Ratios which are selected to

compute profitability of Gatsby Grange are net and gross margin.

Net profit margin

Net profit margin

Formula Net income / net sales * 100

2018 2019

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

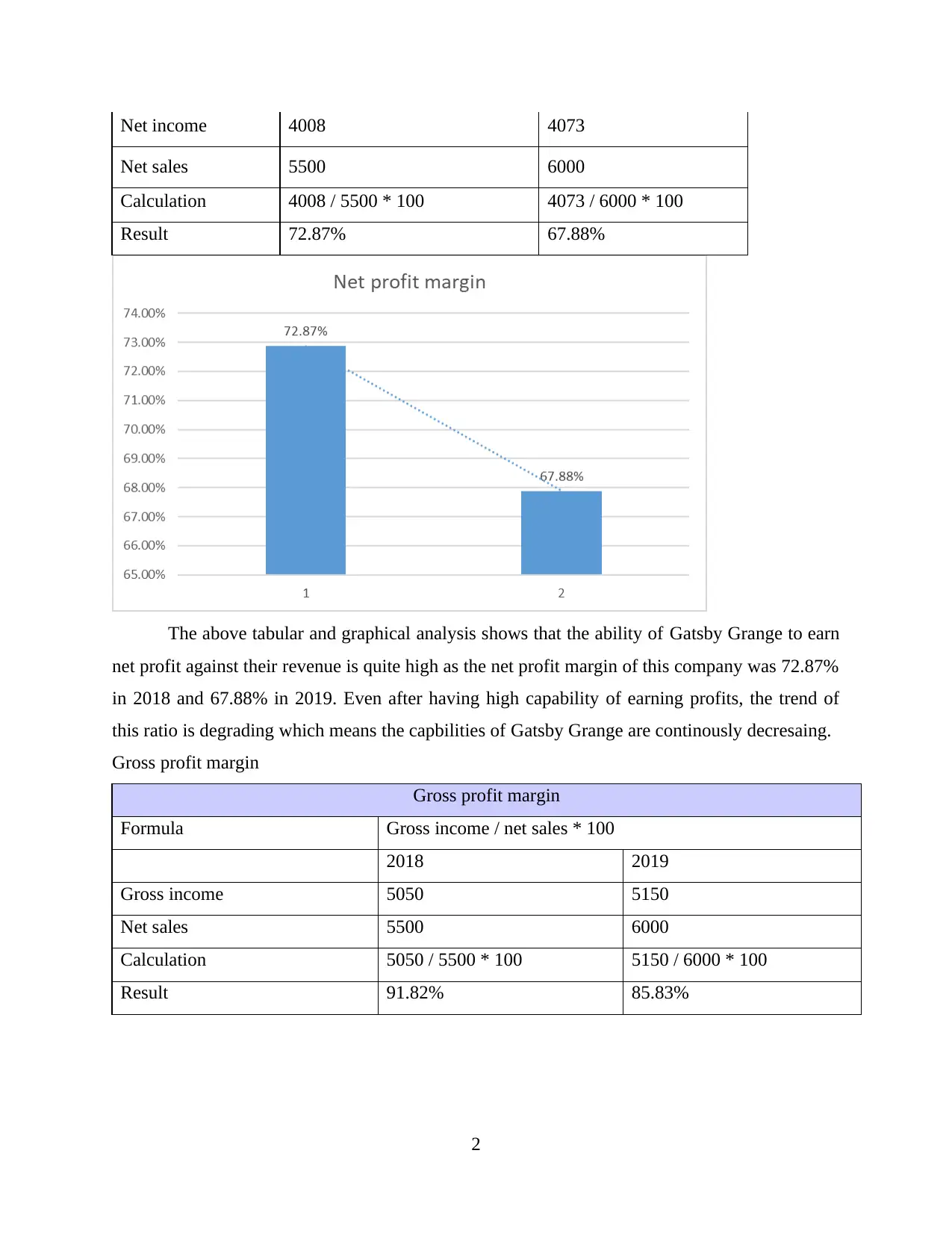

Net income 4008 4073

Net sales 5500 6000

Calculation 4008 / 5500 * 100 4073 / 6000 * 100

Result 72.87% 67.88%

The above tabular and graphical analysis shows that the ability of Gatsby Grange to earn

net profit against their revenue is quite high as the net profit margin of this company was 72.87%

in 2018 and 67.88% in 2019. Even after having high capability of earning profits, the trend of

this ratio is degrading which means the capbilities of Gatsby Grange are continously decresaing.

Gross profit margin

Gross profit margin

Formula Gross income / net sales * 100

2018 2019

Gross income 5050 5150

Net sales 5500 6000

Calculation 5050 / 5500 * 100 5150 / 6000 * 100

Result 91.82% 85.83%

2

Net sales 5500 6000

Calculation 4008 / 5500 * 100 4073 / 6000 * 100

Result 72.87% 67.88%

The above tabular and graphical analysis shows that the ability of Gatsby Grange to earn

net profit against their revenue is quite high as the net profit margin of this company was 72.87%

in 2018 and 67.88% in 2019. Even after having high capability of earning profits, the trend of

this ratio is degrading which means the capbilities of Gatsby Grange are continously decresaing.

Gross profit margin

Gross profit margin

Formula Gross income / net sales * 100

2018 2019

Gross income 5050 5150

Net sales 5500 6000

Calculation 5050 / 5500 * 100 5150 / 6000 * 100

Result 91.82% 85.83%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

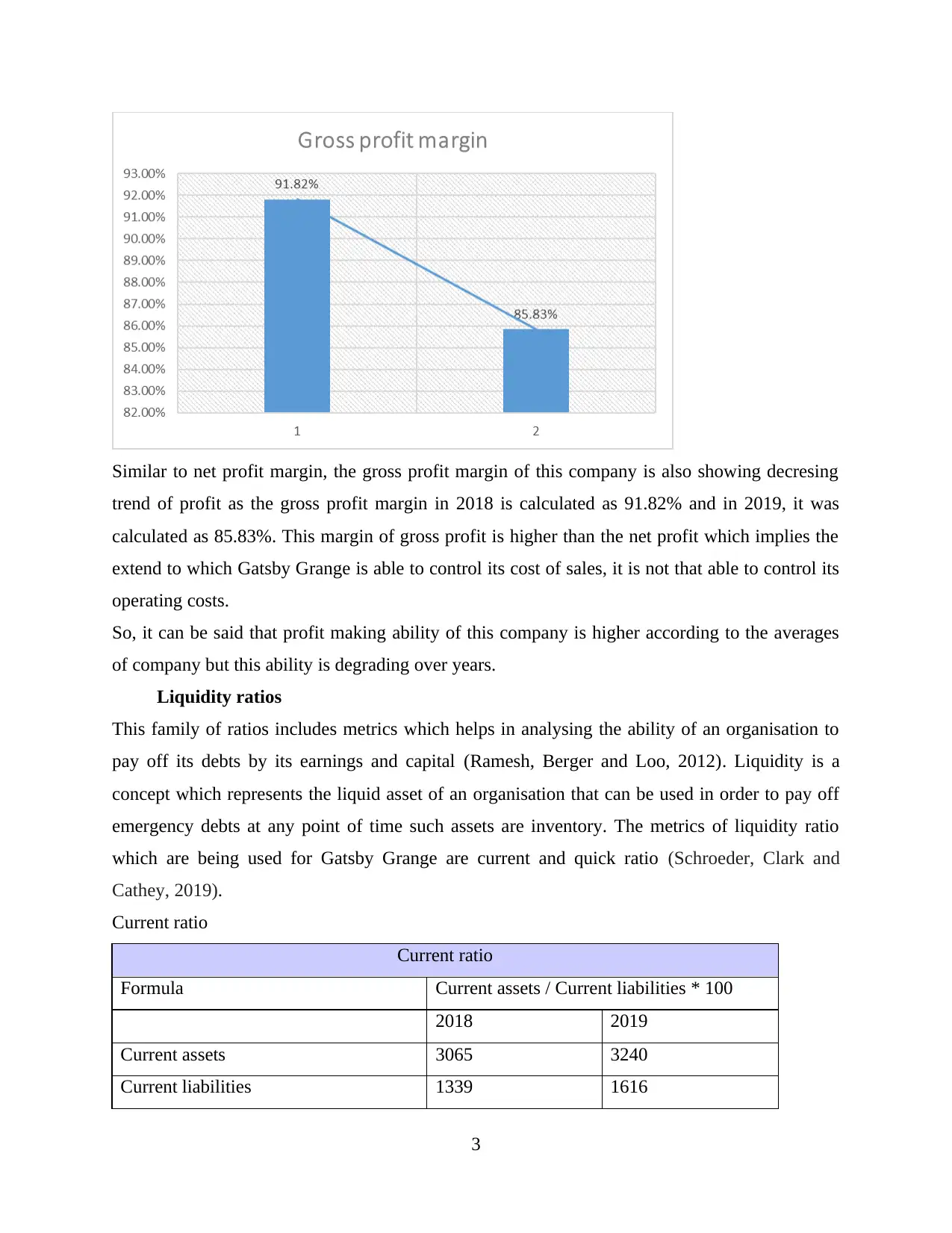

Similar to net profit margin, the gross profit margin of this company is also showing decresing

trend of profit as the gross profit margin in 2018 is calculated as 91.82% and in 2019, it was

calculated as 85.83%. This margin of gross profit is higher than the net profit which implies the

extend to which Gatsby Grange is able to control its cost of sales, it is not that able to control its

operating costs.

So, it can be said that profit making ability of this company is higher according to the averages

of company but this ability is degrading over years.

Liquidity ratios

This family of ratios includes metrics which helps in analysing the ability of an organisation to

pay off its debts by its earnings and capital (Ramesh, Berger and Loo, 2012). Liquidity is a

concept which represents the liquid asset of an organisation that can be used in order to pay off

emergency debts at any point of time such assets are inventory. The metrics of liquidity ratio

which are being used for Gatsby Grange are current and quick ratio (Schroeder, Clark and

Cathey, 2019).

Current ratio

Current ratio

Formula Current assets / Current liabilities * 100

2018 2019

Current assets 3065 3240

Current liabilities 1339 1616

3

trend of profit as the gross profit margin in 2018 is calculated as 91.82% and in 2019, it was

calculated as 85.83%. This margin of gross profit is higher than the net profit which implies the

extend to which Gatsby Grange is able to control its cost of sales, it is not that able to control its

operating costs.

So, it can be said that profit making ability of this company is higher according to the averages

of company but this ability is degrading over years.

Liquidity ratios

This family of ratios includes metrics which helps in analysing the ability of an organisation to

pay off its debts by its earnings and capital (Ramesh, Berger and Loo, 2012). Liquidity is a

concept which represents the liquid asset of an organisation that can be used in order to pay off

emergency debts at any point of time such assets are inventory. The metrics of liquidity ratio

which are being used for Gatsby Grange are current and quick ratio (Schroeder, Clark and

Cathey, 2019).

Current ratio

Current ratio

Formula Current assets / Current liabilities * 100

2018 2019

Current assets 3065 3240

Current liabilities 1339 1616

3

Calculation 3065 / 1339 3240 / 1616

Result 2.289021658 2.004950495

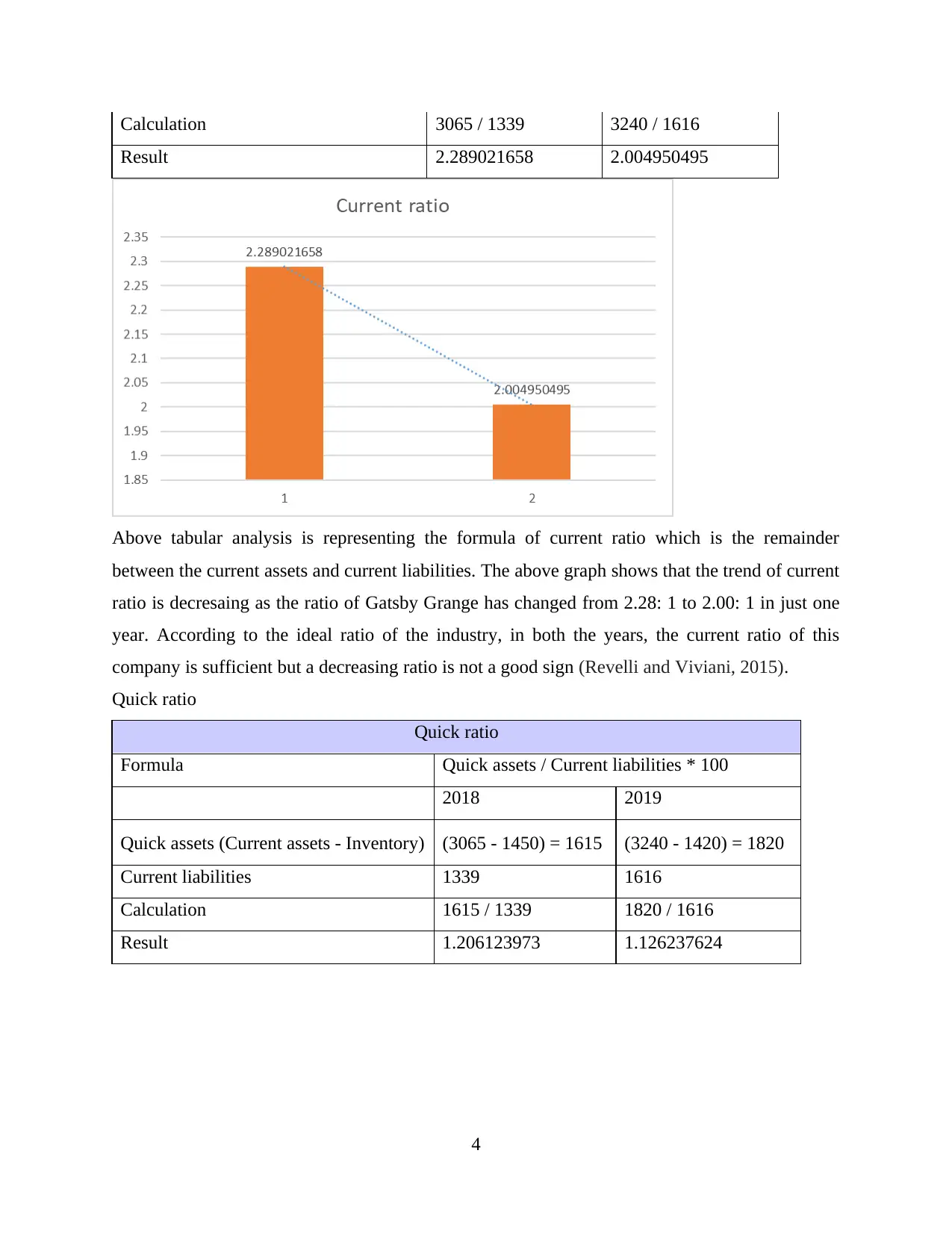

Above tabular analysis is representing the formula of current ratio which is the remainder

between the current assets and current liabilities. The above graph shows that the trend of current

ratio is decresaing as the ratio of Gatsby Grange has changed from 2.28: 1 to 2.00: 1 in just one

year. According to the ideal ratio of the industry, in both the years, the current ratio of this

company is sufficient but a decreasing ratio is not a good sign (Revelli and Viviani, 2015).

Quick ratio

Quick ratio

Formula Quick assets / Current liabilities * 100

2018 2019

Quick assets (Current assets - Inventory) (3065 - 1450) = 1615 (3240 - 1420) = 1820

Current liabilities 1339 1616

Calculation 1615 / 1339 1820 / 1616

Result 1.206123973 1.126237624

4

Result 2.289021658 2.004950495

Above tabular analysis is representing the formula of current ratio which is the remainder

between the current assets and current liabilities. The above graph shows that the trend of current

ratio is decresaing as the ratio of Gatsby Grange has changed from 2.28: 1 to 2.00: 1 in just one

year. According to the ideal ratio of the industry, in both the years, the current ratio of this

company is sufficient but a decreasing ratio is not a good sign (Revelli and Viviani, 2015).

Quick ratio

Quick ratio

Formula Quick assets / Current liabilities * 100

2018 2019

Quick assets (Current assets - Inventory) (3065 - 1450) = 1615 (3240 - 1420) = 1820

Current liabilities 1339 1616

Calculation 1615 / 1339 1820 / 1616

Result 1.206123973 1.126237624

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

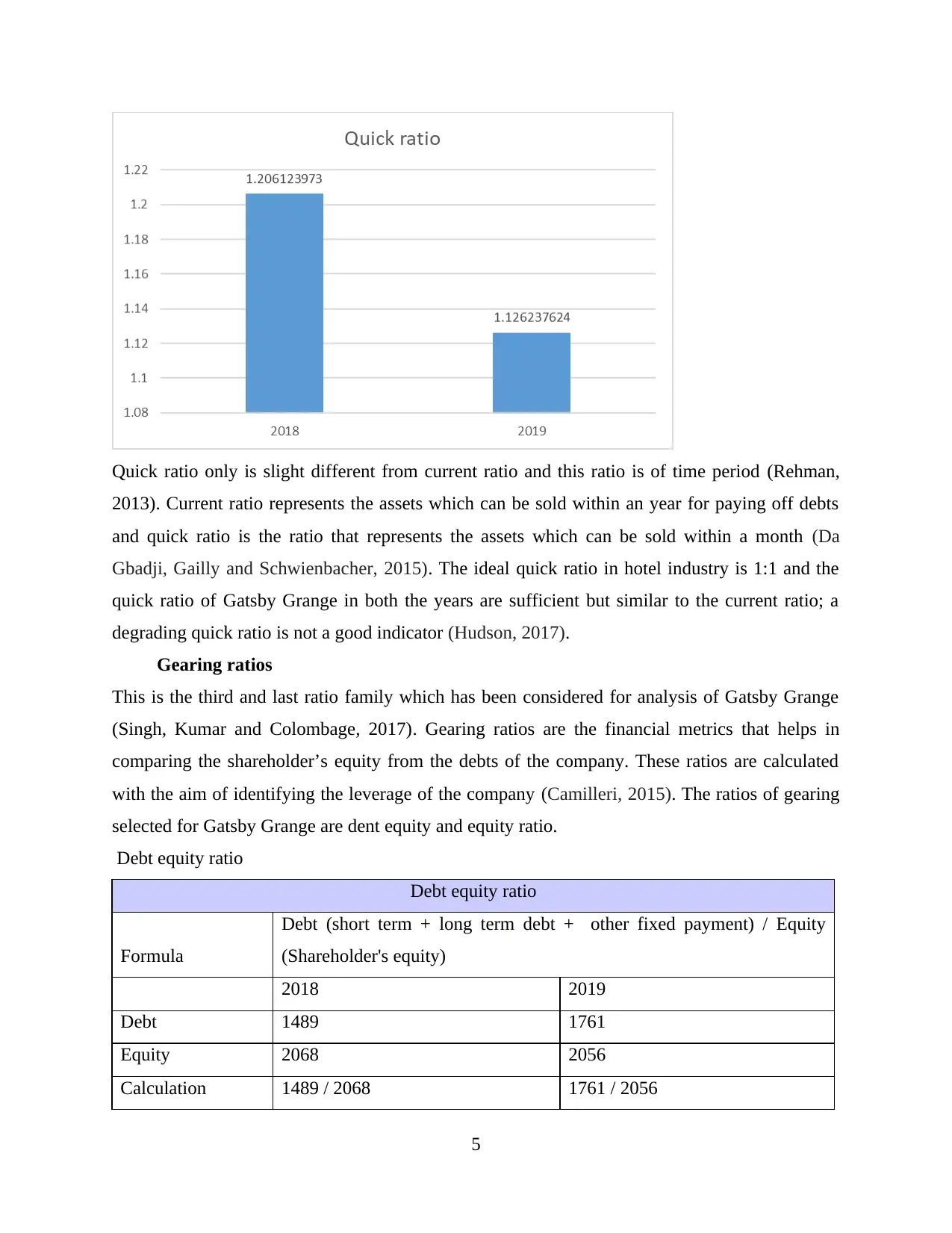

Quick ratio only is slight different from current ratio and this ratio is of time period (Rehman,

2013). Current ratio represents the assets which can be sold within an year for paying off debts

and quick ratio is the ratio that represents the assets which can be sold within a month (Da

Gbadji, Gailly and Schwienbacher, 2015). The ideal quick ratio in hotel industry is 1:1 and the

quick ratio of Gatsby Grange in both the years are sufficient but similar to the current ratio; a

degrading quick ratio is not a good indicator (Hudson, 2017).

Gearing ratios

This is the third and last ratio family which has been considered for analysis of Gatsby Grange

(Singh, Kumar and Colombage, 2017). Gearing ratios are the financial metrics that helps in

comparing the shareholder’s equity from the debts of the company. These ratios are calculated

with the aim of identifying the leverage of the company (Camilleri, 2015). The ratios of gearing

selected for Gatsby Grange are dent equity and equity ratio.

Debt equity ratio

Debt equity ratio

Formula

Debt (short term + long term debt + other fixed payment) / Equity

(Shareholder's equity)

2018 2019

Debt 1489 1761

Equity 2068 2056

Calculation 1489 / 2068 1761 / 2056

5

2013). Current ratio represents the assets which can be sold within an year for paying off debts

and quick ratio is the ratio that represents the assets which can be sold within a month (Da

Gbadji, Gailly and Schwienbacher, 2015). The ideal quick ratio in hotel industry is 1:1 and the

quick ratio of Gatsby Grange in both the years are sufficient but similar to the current ratio; a

degrading quick ratio is not a good indicator (Hudson, 2017).

Gearing ratios

This is the third and last ratio family which has been considered for analysis of Gatsby Grange

(Singh, Kumar and Colombage, 2017). Gearing ratios are the financial metrics that helps in

comparing the shareholder’s equity from the debts of the company. These ratios are calculated

with the aim of identifying the leverage of the company (Camilleri, 2015). The ratios of gearing

selected for Gatsby Grange are dent equity and equity ratio.

Debt equity ratio

Debt equity ratio

Formula

Debt (short term + long term debt + other fixed payment) / Equity

(Shareholder's equity)

2018 2019

Debt 1489 1761

Equity 2068 2056

Calculation 1489 / 2068 1761 / 2056

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Result 0.720019342 0.85651751

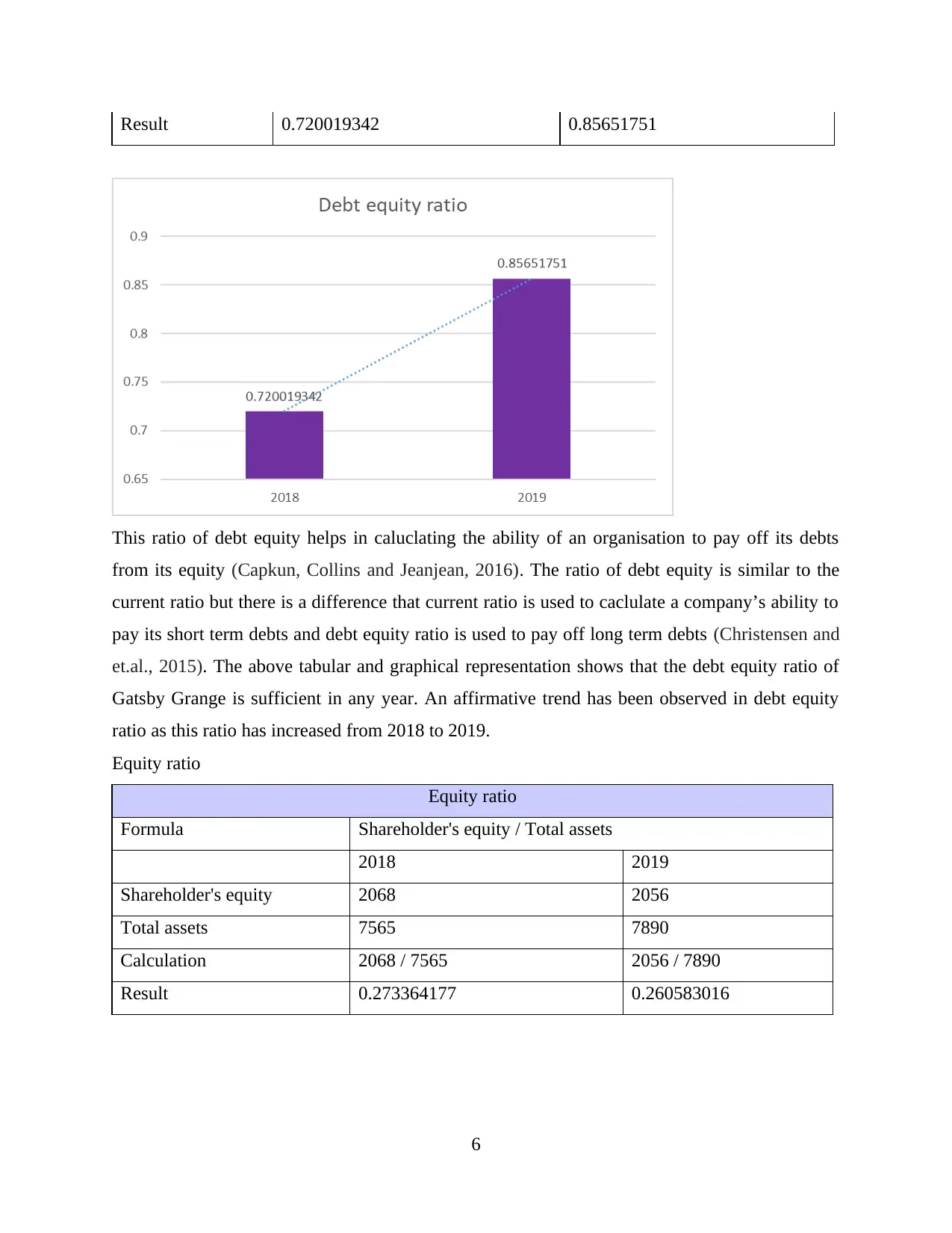

This ratio of debt equity helps in caluclating the ability of an organisation to pay off its debts

from its equity (Capkun, Collins and Jeanjean, 2016). The ratio of debt equity is similar to the

current ratio but there is a difference that current ratio is used to caclulate a company’s ability to

pay its short term debts and debt equity ratio is used to pay off long term debts (Christensen and

et.al., 2015). The above tabular and graphical representation shows that the debt equity ratio of

Gatsby Grange is sufficient in any year. An affirmative trend has been observed in debt equity

ratio as this ratio has increased from 2018 to 2019.

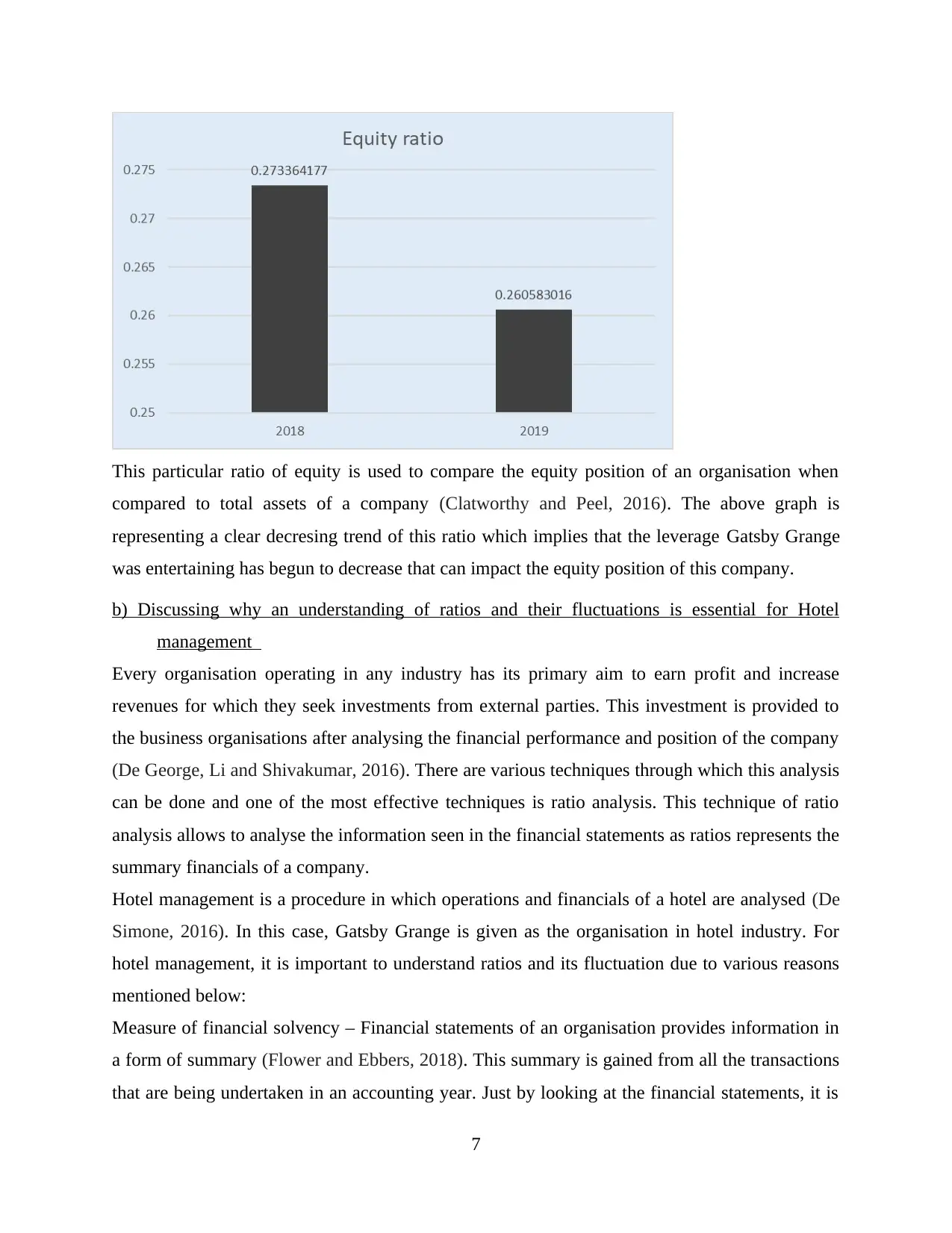

Equity ratio

Equity ratio

Formula Shareholder's equity / Total assets

2018 2019

Shareholder's equity 2068 2056

Total assets 7565 7890

Calculation 2068 / 7565 2056 / 7890

Result 0.273364177 0.260583016

6

This ratio of debt equity helps in caluclating the ability of an organisation to pay off its debts

from its equity (Capkun, Collins and Jeanjean, 2016). The ratio of debt equity is similar to the

current ratio but there is a difference that current ratio is used to caclulate a company’s ability to

pay its short term debts and debt equity ratio is used to pay off long term debts (Christensen and

et.al., 2015). The above tabular and graphical representation shows that the debt equity ratio of

Gatsby Grange is sufficient in any year. An affirmative trend has been observed in debt equity

ratio as this ratio has increased from 2018 to 2019.

Equity ratio

Equity ratio

Formula Shareholder's equity / Total assets

2018 2019

Shareholder's equity 2068 2056

Total assets 7565 7890

Calculation 2068 / 7565 2056 / 7890

Result 0.273364177 0.260583016

6

This particular ratio of equity is used to compare the equity position of an organisation when

compared to total assets of a company (Clatworthy and Peel, 2016). The above graph is

representing a clear decresing trend of this ratio which implies that the leverage Gatsby Grange

was entertaining has begun to decrease that can impact the equity position of this company.

b) Discussing why an understanding of ratios and their fluctuations is essential for Hotel

management

Every organisation operating in any industry has its primary aim to earn profit and increase

revenues for which they seek investments from external parties. This investment is provided to

the business organisations after analysing the financial performance and position of the company

(De George, Li and Shivakumar, 2016). There are various techniques through which this analysis

can be done and one of the most effective techniques is ratio analysis. This technique of ratio

analysis allows to analyse the information seen in the financial statements as ratios represents the

summary financials of a company.

Hotel management is a procedure in which operations and financials of a hotel are analysed (De

Simone, 2016). In this case, Gatsby Grange is given as the organisation in hotel industry. For

hotel management, it is important to understand ratios and its fluctuation due to various reasons

mentioned below:

Measure of financial solvency – Financial statements of an organisation provides information in

a form of summary (Flower and Ebbers, 2018). This summary is gained from all the transactions

that are being undertaken in an accounting year. Just by looking at the financial statements, it is

7

compared to total assets of a company (Clatworthy and Peel, 2016). The above graph is

representing a clear decresing trend of this ratio which implies that the leverage Gatsby Grange

was entertaining has begun to decrease that can impact the equity position of this company.

b) Discussing why an understanding of ratios and their fluctuations is essential for Hotel

management

Every organisation operating in any industry has its primary aim to earn profit and increase

revenues for which they seek investments from external parties. This investment is provided to

the business organisations after analysing the financial performance and position of the company

(De George, Li and Shivakumar, 2016). There are various techniques through which this analysis

can be done and one of the most effective techniques is ratio analysis. This technique of ratio

analysis allows to analyse the information seen in the financial statements as ratios represents the

summary financials of a company.

Hotel management is a procedure in which operations and financials of a hotel are analysed (De

Simone, 2016). In this case, Gatsby Grange is given as the organisation in hotel industry. For

hotel management, it is important to understand ratios and its fluctuation due to various reasons

mentioned below:

Measure of financial solvency – Financial statements of an organisation provides information in

a form of summary (Flower and Ebbers, 2018). This summary is gained from all the transactions

that are being undertaken in an accounting year. Just by looking at the financial statements, it is

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not possible to identify the solvency position of an organisation. In order to identify the solvency

position of the company by looking at their financial statements, it is important to calculate ratios

of debt equity and others. These ratios compare the debt position and equity position of the

company that is not facilitated in financial statements itself. So, it can be said that it is important

for hotel management to understand ratios as these ratios can provide information of solvency

which is not provided in financial statements.

Trend analysis – Hotel management involves managing the financial position of a hotel and

ensuring that the ability of earn profit and effective operations of the company are being

maintained every year. Only by looking at financial statements, it is not possible to analyse

whether company is enhancing is financial position year by year or not (Henderson and et.al.,

2015). And due to this, the ratio analysis is used. It is important to understand the fluctuations or

changes in the ratios as these fluctuations helps in identifying the trends; these trends assist in

gaining the information about whether the position of company is enhancing or is degrading in

the market.

Forecasting and planning – Hotel and tourism industry is a marketplace that needs to be

constantly analysed as the advancements in this industry are usual. Considering this, in hotel

management, it is important to plan for future by effectively forecasting the future situations and

scenarios (Kraft, Vashishtha and Venkatachalam, 2017). Ratios are the base of planning as the

ratios can be predicted by analysing the yearly trend within them. So, it can be said that the

fluctuations in ratio analysis are important to understood as these are used to predict the future

organisational aspects.

Gatsby Grange must also understand ratios and its fluctuations to analyse the information

in their financial statements.

c) Benefits and limitations of ratio analysis in decision making within hotel and tourism industry

Similar to any other analytical technique, ratio analysis also has few merits and demerits

which can be used as the aid for decision making within the hotel and tourism industry in which

Gatsby Grange operates.

Benefits of ratio analysis

Simplifies complex financial statements – Ratio analysis helps hotel and tourism industry to

make decisions by effectively analysing the financial position of their companies (Lang and

Stice-Lawrence, 2015). Financial statements are difficult to be understood and in order to

8

position of the company by looking at their financial statements, it is important to calculate ratios

of debt equity and others. These ratios compare the debt position and equity position of the

company that is not facilitated in financial statements itself. So, it can be said that it is important

for hotel management to understand ratios as these ratios can provide information of solvency

which is not provided in financial statements.

Trend analysis – Hotel management involves managing the financial position of a hotel and

ensuring that the ability of earn profit and effective operations of the company are being

maintained every year. Only by looking at financial statements, it is not possible to analyse

whether company is enhancing is financial position year by year or not (Henderson and et.al.,

2015). And due to this, the ratio analysis is used. It is important to understand the fluctuations or

changes in the ratios as these fluctuations helps in identifying the trends; these trends assist in

gaining the information about whether the position of company is enhancing or is degrading in

the market.

Forecasting and planning – Hotel and tourism industry is a marketplace that needs to be

constantly analysed as the advancements in this industry are usual. Considering this, in hotel

management, it is important to plan for future by effectively forecasting the future situations and

scenarios (Kraft, Vashishtha and Venkatachalam, 2017). Ratios are the base of planning as the

ratios can be predicted by analysing the yearly trend within them. So, it can be said that the

fluctuations in ratio analysis are important to understood as these are used to predict the future

organisational aspects.

Gatsby Grange must also understand ratios and its fluctuations to analyse the information

in their financial statements.

c) Benefits and limitations of ratio analysis in decision making within hotel and tourism industry

Similar to any other analytical technique, ratio analysis also has few merits and demerits

which can be used as the aid for decision making within the hotel and tourism industry in which

Gatsby Grange operates.

Benefits of ratio analysis

Simplifies complex financial statements – Ratio analysis helps hotel and tourism industry to

make decisions by effectively analysing the financial position of their companies (Lang and

Stice-Lawrence, 2015). Financial statements are difficult to be understood and in order to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

simplify them ratio analysis is used. These ratios help in making decision regarding relevant

investments that can provide valid returns.

Helps to compare inter and intra firm – Hotel and tourism industry can also be benefitted by

ratio analysis through comparing their financial performance by other companies and through

comparing their financial performance by their past year’s financial performance (Li, Sougiannis

and Wang, 2017). This comparison provides a base to make decisions of selecting a benchmark

of effective performance.

Limitations of ratio analysis

Ignores qualitative aspects – Ratio analysis only accounts for quantitative aspects due to which

the decisions made by the hotel and tourism industry based on the ratios can result into

ineffective decisions (Maynard, 2017).

Ignores inflation – The predictions made by ratio analysis does not involve time value of money

or inflation due to which decisions made by hotel and tourism industry using ratio analysis can

result into inaccuracies (Michelon, Pilonato and Ricceri, 2015).

From the above analysis of benefits and limitations, it can be said that there are few benefits

which encourage hotel and tourism industry to use ratio analysis but in hand of this, there are

certain limitations as well which limit and discourage hotel and tourism industry to use ratio

analyses (Progunova and et.al., 2018).

CONCLUSION

From the above report, it has been analysed that ratio analysis is a technique that helps an

organisation to summarise their financial position and performance in order to compare with past

year’s performance. The organisation considered in above report was Gatsby Grange which is a

financially stable organisation but the financial performance of this company is decreasing

gradually.

9

investments that can provide valid returns.

Helps to compare inter and intra firm – Hotel and tourism industry can also be benefitted by

ratio analysis through comparing their financial performance by other companies and through

comparing their financial performance by their past year’s financial performance (Li, Sougiannis

and Wang, 2017). This comparison provides a base to make decisions of selecting a benchmark

of effective performance.

Limitations of ratio analysis

Ignores qualitative aspects – Ratio analysis only accounts for quantitative aspects due to which

the decisions made by the hotel and tourism industry based on the ratios can result into

ineffective decisions (Maynard, 2017).

Ignores inflation – The predictions made by ratio analysis does not involve time value of money

or inflation due to which decisions made by hotel and tourism industry using ratio analysis can

result into inaccuracies (Michelon, Pilonato and Ricceri, 2015).

From the above analysis of benefits and limitations, it can be said that there are few benefits

which encourage hotel and tourism industry to use ratio analysis but in hand of this, there are

certain limitations as well which limit and discourage hotel and tourism industry to use ratio

analyses (Progunova and et.al., 2018).

CONCLUSION

From the above report, it has been analysed that ratio analysis is a technique that helps an

organisation to summarise their financial position and performance in order to compare with past

year’s performance. The organisation considered in above report was Gatsby Grange which is a

financially stable organisation but the financial performance of this company is decreasing

gradually.

9

REFERENCES

Books and Journals

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS data (No.

1639-2016-135182).

Kansal, M., Joshi, M. and Batra, G.S., 2014. Determinants of corporate social responsibility

disclosures: Evidence from India. Advances in Accounting. 30(1). pp.217-229.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Olson, K. and Groves, R.M., 2012. An examination of within-person variation in response

propensity over the data collection field period.

Ramesh, A., Berger, P.R. and Loo, R., 2012. High 5.2 peak-to-valley current ratio in Si/SiGe

resonant interband tunnel diodes grown by chemical vapor deposition. Applied Physics

Letters. 100(9). p.092104.

Rehman, S.S.F.U., 2013. Relationship between financial leverage and financial performance:

Empirical evidence of listed sugar companies of Pakistan. Global Journal of

Management and Business Research.

Singh, H.P., Kumar, S. and Colombage, S., 2017. Working capital management and firm

profitability: a meta-analysis. Qualitative Research in Financial Markets.

Camilleri, M.A., 2015. Valuing stakeholder engagement and sustainability reporting. Corporate

Reputation Review. 18(3). pp.210-222.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of

Accounting and Public Policy. 35(4). pp.352-394.

Christensen, H. B. and et.al., 2015. Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). pp.31-61.

Clatworthy, M.A. and Peel, M.J., 2016. The timeliness of UK private company financial

reporting: Regulatory and economic influences. The British Accounting Review.48(3).

pp.297-315.

De George, E. T., Li, X. and Shivakumar, L., 2016. A review of the IFRS adoption

literature. Review of Accounting Studies. 21(3). pp.898-1004.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated income

shifting for multinational firms?. Journal of Accounting and Economics. 61(1). pp.145-

165.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Kraft, A. G., Vashishtha, R. and Venkatachalam, M., 2017. Frequent financial reporting and

managerial myopia. The Accounting Review. 93(2). pp.249-275.

Lang, M. and Stice-Lawrence, L., 2015. Textual analysis and international financial reporting:

Large sample evidence. Journal of Accounting and Economics. 60(2-3). pp.110-135.

Li, S., Sougiannis, T. and Wang, S., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows. Available at

SSRN 2948775.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

10

Books and Journals

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS data (No.

1639-2016-135182).

Kansal, M., Joshi, M. and Batra, G.S., 2014. Determinants of corporate social responsibility

disclosures: Evidence from India. Advances in Accounting. 30(1). pp.217-229.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Olson, K. and Groves, R.M., 2012. An examination of within-person variation in response

propensity over the data collection field period.

Ramesh, A., Berger, P.R. and Loo, R., 2012. High 5.2 peak-to-valley current ratio in Si/SiGe

resonant interband tunnel diodes grown by chemical vapor deposition. Applied Physics

Letters. 100(9). p.092104.

Rehman, S.S.F.U., 2013. Relationship between financial leverage and financial performance:

Empirical evidence of listed sugar companies of Pakistan. Global Journal of

Management and Business Research.

Singh, H.P., Kumar, S. and Colombage, S., 2017. Working capital management and firm

profitability: a meta-analysis. Qualitative Research in Financial Markets.

Camilleri, M.A., 2015. Valuing stakeholder engagement and sustainability reporting. Corporate

Reputation Review. 18(3). pp.210-222.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of

Accounting and Public Policy. 35(4). pp.352-394.

Christensen, H. B. and et.al., 2015. Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). pp.31-61.

Clatworthy, M.A. and Peel, M.J., 2016. The timeliness of UK private company financial

reporting: Regulatory and economic influences. The British Accounting Review.48(3).

pp.297-315.

De George, E. T., Li, X. and Shivakumar, L., 2016. A review of the IFRS adoption

literature. Review of Accounting Studies. 21(3). pp.898-1004.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated income

shifting for multinational firms?. Journal of Accounting and Economics. 61(1). pp.145-

165.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Kraft, A. G., Vashishtha, R. and Venkatachalam, M., 2017. Frequent financial reporting and

managerial myopia. The Accounting Review. 93(2). pp.249-275.

Lang, M. and Stice-Lawrence, L., 2015. Textual analysis and international financial reporting:

Large sample evidence. Journal of Accounting and Economics. 60(2-3). pp.110-135.

Li, S., Sougiannis, T. and Wang, S., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows. Available at

SSRN 2948775.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.