International Indirect Taxation - A Report on Single Market Framework

VerifiedAdded on 2022/11/14

|26

|8029

|274

AI Summary

This report discusses the advantages and disadvantages of a single market framework for VAT and Excise taxes in Germany, France, Japan, and Singapore. It covers the technical knowledge on identifying end-users, supplies, distance selling, VAT MOSS, payment on account, flat rate scheme, and more. The objective of a single market is to create a situation where goods and services can be freely circulated as tax-paid commodities and facilitate the system to become a major contributor to revenue collection through a VAT Fiscal Policy.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

international indirect

taxation

A Report on Single

Market Framework

taxation

A Report on Single

Market Framework

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

Contents

Executive Summary...................................................................................................................3

1. Introduction........................................................................................................................4

1.1. VAT and Single Market...............................................................................................4

1.2. Advantages & Disadvantages of a Single Market.........................................................5

1.3. Creating Level Playing Field........................................................................................6

1.4. Key Statement on Single Market..................................................................................6

1.5. Objective of Single Market...........................................................................................6

2. Country Specific.................................................................................................................7

2.1. GERMANY..................................................................................................................7

2.2. FRANCE......................................................................................................................8

2.3. JAPAN.........................................................................................................................9

2.4. SINGAPORE.............................................................................................................11

3. Literature Review.............................................................................................................12

3.1. Rationale for Choice...................................................................................................12

3.2. Creating a Single Market and VAT-Justification........................................................12

3.3. Approach and Results – A Summary..........................................................................13

3.4. EU Council Directive on VAT...................................................................................13

3.5. Academic Paper Sources – Single Market..................................................................14

3.6. Academic Paper Sources – VAT................................................................................14

3.7. Official Journal of EU................................................................................................14

3.8. Scope of VAT for a Single Market.............................................................................14

3.9. Territorial Scope of a Single Market..........................................................................14

4. Technical Knowledge.......................................................................................................15

4.1. Identifying the End-user.............................................................................................15

4.2. Supplies – Full and Partial Exemption........................................................................15

4.3. Distance Selling / Reverse Charges............................................................................15

4.4. VAT MOSS / Digital Supply......................................................................................16

4.5. Payment on Account...................................................................................................16

4.6. Flat Rate Scheme........................................................................................................16

4.7. Differentiating Goods and Services............................................................................16

4.8. Residual Input Tax.....................................................................................................16

Page | 1

A Report on Single Market Framework

Contents

Executive Summary...................................................................................................................3

1. Introduction........................................................................................................................4

1.1. VAT and Single Market...............................................................................................4

1.2. Advantages & Disadvantages of a Single Market.........................................................5

1.3. Creating Level Playing Field........................................................................................6

1.4. Key Statement on Single Market..................................................................................6

1.5. Objective of Single Market...........................................................................................6

2. Country Specific.................................................................................................................7

2.1. GERMANY..................................................................................................................7

2.2. FRANCE......................................................................................................................8

2.3. JAPAN.........................................................................................................................9

2.4. SINGAPORE.............................................................................................................11

3. Literature Review.............................................................................................................12

3.1. Rationale for Choice...................................................................................................12

3.2. Creating a Single Market and VAT-Justification........................................................12

3.3. Approach and Results – A Summary..........................................................................13

3.4. EU Council Directive on VAT...................................................................................13

3.5. Academic Paper Sources – Single Market..................................................................14

3.6. Academic Paper Sources – VAT................................................................................14

3.7. Official Journal of EU................................................................................................14

3.8. Scope of VAT for a Single Market.............................................................................14

3.9. Territorial Scope of a Single Market..........................................................................14

4. Technical Knowledge.......................................................................................................15

4.1. Identifying the End-user.............................................................................................15

4.2. Supplies – Full and Partial Exemption........................................................................15

4.3. Distance Selling / Reverse Charges............................................................................15

4.4. VAT MOSS / Digital Supply......................................................................................16

4.5. Payment on Account...................................................................................................16

4.6. Flat Rate Scheme........................................................................................................16

4.7. Differentiating Goods and Services............................................................................16

4.8. Residual Input Tax.....................................................................................................16

Page | 1

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

4.9. Distance Selling / Cross Border..................................................................................16

4.10. Application of VAT on Import...............................................................................16

5. Conclusion.........................................................................................................................17

5.1. Standard Rate of Tax..................................................................................................17

5.2. Achievements of a Single Market Framework............................................................17

5.3. Objectives Fulfilled and Consequences......................................................................17

5.3.1. Objectives Fulfilled...........................................................................................17

5.3.2. Consequences....................................................................................................18

6. BIBLIOGRAPHY............................................................................................................18

6.1. Academic Paper Sources – Single Market..................................................................18

6.2. Academic Paper Sources – VAT................................................................................20

6.3. Reference List............................................................................................................21

Page | 2

A Report on Single Market Framework

4.9. Distance Selling / Cross Border..................................................................................16

4.10. Application of VAT on Import...............................................................................16

5. Conclusion.........................................................................................................................17

5.1. Standard Rate of Tax..................................................................................................17

5.2. Achievements of a Single Market Framework............................................................17

5.3. Objectives Fulfilled and Consequences......................................................................17

5.3.1. Objectives Fulfilled...........................................................................................17

5.3.2. Consequences....................................................................................................18

6. BIBLIOGRAPHY............................................................................................................18

6.1. Academic Paper Sources – Single Market..................................................................18

6.2. Academic Paper Sources – VAT................................................................................20

6.3. Reference List............................................................................................................21

Page | 2

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

Executive Summary

The four big economies of the world, Germany, France, Japan and Singapore, although

not large enough to compete with the USA, China or Russia, have enough economic

strength to unite as a Single Market and challenge the tycoons. Under such presumption,

their Ministers of Finance agreed to discuss and formulate a fiscal policy, which will be

responding to two of their major challenges: (a) Promotion of their Economic Growth;

and (b) helping them to reduce unemployment in their respective countries.

The basic concept of this policy is to explore considerations for creating a Single

Market. The aim of such a fiscal policy is to convert their respective national markets

into a single market, so that new opportunities are opened for the industries to provide

immediate access to millions of consumers. This will also strengthen the economies of

these four nations and make them stronger to face the emerging competitiveness in

world markets. The Ministers agreed that the purpose of the policy is not to have a

common currency symbol but about bonding their local markets into a single market.

The Ministers also declared that promoting a single market policy has become

necessary, particularly because of differentiating taxes such as VAT and Excise. In this

regard the following reasons were found pertinent –

VAT has emerged as a tax which contributes significantly to every government’s

revenue collection, by including both the goods sold and services provided in the

free markets

A controlled VAT needs to be implemented so that it becomes a basic element in

the development of a single market.

VAT has now emerged, both through its conception and legislations, as a

Community Tax, hence one of the main factor and objective of this single market

policy is to promote a common system of VAT in all the member nations.

The Ministers also agreed unanimously that Excise, when levied disproportionately

on goods produced and sold in the open markets, although increases revenue intake

for the government, it also decreases the purchasing power of the consumer,

thereby indirectly affecting the industry.

Page | 3

A Report on Single Market Framework

Executive Summary

The four big economies of the world, Germany, France, Japan and Singapore, although

not large enough to compete with the USA, China or Russia, have enough economic

strength to unite as a Single Market and challenge the tycoons. Under such presumption,

their Ministers of Finance agreed to discuss and formulate a fiscal policy, which will be

responding to two of their major challenges: (a) Promotion of their Economic Growth;

and (b) helping them to reduce unemployment in their respective countries.

The basic concept of this policy is to explore considerations for creating a Single

Market. The aim of such a fiscal policy is to convert their respective national markets

into a single market, so that new opportunities are opened for the industries to provide

immediate access to millions of consumers. This will also strengthen the economies of

these four nations and make them stronger to face the emerging competitiveness in

world markets. The Ministers agreed that the purpose of the policy is not to have a

common currency symbol but about bonding their local markets into a single market.

The Ministers also declared that promoting a single market policy has become

necessary, particularly because of differentiating taxes such as VAT and Excise. In this

regard the following reasons were found pertinent –

VAT has emerged as a tax which contributes significantly to every government’s

revenue collection, by including both the goods sold and services provided in the

free markets

A controlled VAT needs to be implemented so that it becomes a basic element in

the development of a single market.

VAT has now emerged, both through its conception and legislations, as a

Community Tax, hence one of the main factor and objective of this single market

policy is to promote a common system of VAT in all the member nations.

The Ministers also agreed unanimously that Excise, when levied disproportionately

on goods produced and sold in the open markets, although increases revenue intake

for the government, it also decreases the purchasing power of the consumer,

thereby indirectly affecting the industry.

Page | 3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

A single market will not only remove these disproportionate taxing streams, it will also

give boost to the industries and trading houses by increasing their business volumes. An

increased consumption by the consumers, under a single tax regime, for a single market,

will automatically increase the revenue collection of nations participating in this

amalgamation.

Page | 4

A Report on Single Market Framework

A single market will not only remove these disproportionate taxing streams, it will also

give boost to the industries and trading houses by increasing their business volumes. An

increased consumption by the consumers, under a single tax regime, for a single market,

will automatically increase the revenue collection of nations participating in this

amalgamation.

Page | 4

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

1. Introduction

1.1. VAT and Single Market

It was in April 1973 that Value Added Tax (VAT) was introduced in the European

Union (EU) when Britain joined EU. Since then, till the present, VAT has undergone

many changes and cam to be addressed as Transitional VAT-system in many advanced

economies of the world, assert Hoffman et al, (2015). Although introduction of VAT

was considered as a major forward step for abolishing the irregular Purchase Tax, it

only reflected the process, albeit partly, of the economic integration which was taking

place all across the globe and especially in the EU, as per Bhattacharjee &

Bhattacharya, (2018). The results achieved by the EU, over the last four decades, has

prompted the Finance Ministers of Germany, France, Japan and Singapore to follow in

the steps of the EU and achieve, albeit much more than EU, by integrating the core

market sectors of their respective countries into a Single Market, to be known as

GeFJaS, through a process of consolidating their taxes, especially VAT and Excise by

introducing a single market policy, as explained by Pfeiffer & Ursprung-Steindl (eds.),

(2015). Learning from the EU experience, GeFJaS will not aim at a common currency

or a common flag but will be attempting to consolidate itself into a commercially

managed conglomerate so that it can effectively counter the fast emerging

competitiveness in the world, says CEC, (1996).

Finance Ministers of GeFJaS have agreed in unison, to discuss more specific and

compelling lines on which a Fiscal Policy can be formulated, as detailed by Lang et al

(eds.), (2009), for ably responding to the two most challenging issues which they are

facing in the current economic scenario –

(a) Promotion of Mutually beneficial Economic Growth; and (b) Reduction of

Unemployment Rate in their respective countries. At the core of the Fiscal Policy is the

need of a Single Market, as per OECD, (2014). Aim set by the Finance Ministers is to

help GeFJaS become a professionally and commercially managed Single Market, which

can open up fresh opportunities for the industries falling under GeFJaS. This will not

only bring prosperity to millions of consumers in GeFJaS, it will also strengthen the

economies of the member nations for fighting market competitiveness which is fast

capturing the world economy, assert Pfeiffer & Ursprung-Steindl (eds.), (2015).

Page | 5

A Report on Single Market Framework

1. Introduction

1.1. VAT and Single Market

It was in April 1973 that Value Added Tax (VAT) was introduced in the European

Union (EU) when Britain joined EU. Since then, till the present, VAT has undergone

many changes and cam to be addressed as Transitional VAT-system in many advanced

economies of the world, assert Hoffman et al, (2015). Although introduction of VAT

was considered as a major forward step for abolishing the irregular Purchase Tax, it

only reflected the process, albeit partly, of the economic integration which was taking

place all across the globe and especially in the EU, as per Bhattacharjee &

Bhattacharya, (2018). The results achieved by the EU, over the last four decades, has

prompted the Finance Ministers of Germany, France, Japan and Singapore to follow in

the steps of the EU and achieve, albeit much more than EU, by integrating the core

market sectors of their respective countries into a Single Market, to be known as

GeFJaS, through a process of consolidating their taxes, especially VAT and Excise by

introducing a single market policy, as explained by Pfeiffer & Ursprung-Steindl (eds.),

(2015). Learning from the EU experience, GeFJaS will not aim at a common currency

or a common flag but will be attempting to consolidate itself into a commercially

managed conglomerate so that it can effectively counter the fast emerging

competitiveness in the world, says CEC, (1996).

Finance Ministers of GeFJaS have agreed in unison, to discuss more specific and

compelling lines on which a Fiscal Policy can be formulated, as detailed by Lang et al

(eds.), (2009), for ably responding to the two most challenging issues which they are

facing in the current economic scenario –

(a) Promotion of Mutually beneficial Economic Growth; and (b) Reduction of

Unemployment Rate in their respective countries. At the core of the Fiscal Policy is the

need of a Single Market, as per OECD, (2014). Aim set by the Finance Ministers is to

help GeFJaS become a professionally and commercially managed Single Market, which

can open up fresh opportunities for the industries falling under GeFJaS. This will not

only bring prosperity to millions of consumers in GeFJaS, it will also strengthen the

economies of the member nations for fighting market competitiveness which is fast

capturing the world economy, assert Pfeiffer & Ursprung-Steindl (eds.), (2015).

Page | 5

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

1.2. Advantages & Disadvantages of a Single Market

The decision of GeFJaS Ministers to implement Single Market policy was in earnest

because of the rapid progress taking place in global economy. The member nations of

GeFJaS find implementation of the policy essential so that they can take full advantage

of a strengthened single market right from its inception, as per Ecker, (2013). The

advantage can become manifold once taxes like VAT and Excise are implemented. A

uniform VAT can be helpful because –

Free circulation of goods and services in the entire GeFJaS zone will be benefitted

by uniform VAT

From its implementation through a legislation, VAT can be treated as a Community

Tax as the objective is to implement a common VAT system in GeFJaS.

The present VAT system in GeFJaS shall be under the transitional regime and it is

essential to understand that the present system creates unnecessary costs for the trade

sector and, finally, for the consumers, according to Muller et al (eds.), (2017). The

preliminary estimates made by the Ministers suggest that the direct administrative cost

born by the trade sector on the periodic transactions carried out in the individual

Member Nations is about 5 times more than what they will be bearing after the policy is

implemented in the entire GeFJaS zone, explain Hafner, Robin & Hoorens, (2014).

1.3. Creating Level Playing Field

Eliminating the unnecessary costs will definitely benefit the GeFJaS members in

combating economic competitiveness in the world, as per Mendel & Bevacqua, (2010).

Along with this factor, the cutdown costs will be creating a Level Playing Field for the

entire SME sector in GeFJaS zone. In the final discussions on the White Paper on

Economic Growth, Market Competitiveness and Eradication of Unemployment, the

GeFJaS Ministers unanimously agreed on the results presented for the above three

factors connected with the SME sector, explains Bakker (ed.), (2009).

Another important factor for creating a level playing field is reduction and/or

stabilisation of the individual nation’s budgetary deficits. Hence, the member nations of

GeFJaS must have a Uniform Taxation Policy so that they can contribute towards their

targeted objectives and also stabilise their tax receipts, assert Hoffman et al, (2015).

Page | 6

A Report on Single Market Framework

1.2. Advantages & Disadvantages of a Single Market

The decision of GeFJaS Ministers to implement Single Market policy was in earnest

because of the rapid progress taking place in global economy. The member nations of

GeFJaS find implementation of the policy essential so that they can take full advantage

of a strengthened single market right from its inception, as per Ecker, (2013). The

advantage can become manifold once taxes like VAT and Excise are implemented. A

uniform VAT can be helpful because –

Free circulation of goods and services in the entire GeFJaS zone will be benefitted

by uniform VAT

From its implementation through a legislation, VAT can be treated as a Community

Tax as the objective is to implement a common VAT system in GeFJaS.

The present VAT system in GeFJaS shall be under the transitional regime and it is

essential to understand that the present system creates unnecessary costs for the trade

sector and, finally, for the consumers, according to Muller et al (eds.), (2017). The

preliminary estimates made by the Ministers suggest that the direct administrative cost

born by the trade sector on the periodic transactions carried out in the individual

Member Nations is about 5 times more than what they will be bearing after the policy is

implemented in the entire GeFJaS zone, explain Hafner, Robin & Hoorens, (2014).

1.3. Creating Level Playing Field

Eliminating the unnecessary costs will definitely benefit the GeFJaS members in

combating economic competitiveness in the world, as per Mendel & Bevacqua, (2010).

Along with this factor, the cutdown costs will be creating a Level Playing Field for the

entire SME sector in GeFJaS zone. In the final discussions on the White Paper on

Economic Growth, Market Competitiveness and Eradication of Unemployment, the

GeFJaS Ministers unanimously agreed on the results presented for the above three

factors connected with the SME sector, explains Bakker (ed.), (2009).

Another important factor for creating a level playing field is reduction and/or

stabilisation of the individual nation’s budgetary deficits. Hence, the member nations of

GeFJaS must have a Uniform Taxation Policy so that they can contribute towards their

targeted objectives and also stabilise their tax receipts, assert Hoffman et al, (2015).

Page | 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

1.4. Key Statement on Single Market

This paper, as per Muller et al (eds.), (2017), again stresses that the most suitable way

for achieving the targeted goals lies in promoting economic growth and generating

employment. This will increase tax revenue collection for the member nations and will

also reduce the expenditure, explains Basu, (2013). The other factor which can make tax

revenue collection more effective is a simplified tax system. This also makes

implementing of the policy by strengthening the tax system and combating fraud,

according to Adam, Besley & Blundell, (2011).

1.5. Objective of Single Market

The objective of a Single Market, according to Knodel, (2009), is to –

Create a situation where goods and services can be freely circulated as tax paid

commodities.

Create a simple tax system so that it remains protected from evasion and fraud.

Facilitate the system to become a major contributor to revenue collection

through a VAT Fiscal Policy.

2. Country Specific

2.1. GERMANY

2.1.1. Main Features

Economic Freedom Score of Germany is 73.5 and this ranks Germany’s economy as

24th freest as per 2019 Index. Its ranking in the EU region is 14th among the 44

countries, according to Mendel & Bevacqua, (2010). On the basis of these rankings,

Germany is above the world and regional averages.

2.1.2. Trade Features

Germany’s regulatory framework is strong and efficient and facilitates activities of free

enterprises. This allows businesses to operate as dynamically as in other parts of the

world, assert Forte & Oppenheim, (2011). The regulatory changes of 2017 introduced

certain restrictions on temporary employment and this allows the government to

maintain monetary stability, Subsidies have been at all-time high since 2018 and the

subsidy expenditure continues to rise. Germany’s Business Freedom score is 83.3%;

Labor Freedom score is 52.8%; and Monetary Freedom score is 77.9% as per Ault,

Arnold & Gest, (2010).

Page | 7

A Report on Single Market Framework

1.4. Key Statement on Single Market

This paper, as per Muller et al (eds.), (2017), again stresses that the most suitable way

for achieving the targeted goals lies in promoting economic growth and generating

employment. This will increase tax revenue collection for the member nations and will

also reduce the expenditure, explains Basu, (2013). The other factor which can make tax

revenue collection more effective is a simplified tax system. This also makes

implementing of the policy by strengthening the tax system and combating fraud,

according to Adam, Besley & Blundell, (2011).

1.5. Objective of Single Market

The objective of a Single Market, according to Knodel, (2009), is to –

Create a situation where goods and services can be freely circulated as tax paid

commodities.

Create a simple tax system so that it remains protected from evasion and fraud.

Facilitate the system to become a major contributor to revenue collection

through a VAT Fiscal Policy.

2. Country Specific

2.1. GERMANY

2.1.1. Main Features

Economic Freedom Score of Germany is 73.5 and this ranks Germany’s economy as

24th freest as per 2019 Index. Its ranking in the EU region is 14th among the 44

countries, according to Mendel & Bevacqua, (2010). On the basis of these rankings,

Germany is above the world and regional averages.

2.1.2. Trade Features

Germany’s regulatory framework is strong and efficient and facilitates activities of free

enterprises. This allows businesses to operate as dynamically as in other parts of the

world, assert Forte & Oppenheim, (2011). The regulatory changes of 2017 introduced

certain restrictions on temporary employment and this allows the government to

maintain monetary stability, Subsidies have been at all-time high since 2018 and the

subsidy expenditure continues to rise. Germany’s Business Freedom score is 83.3%;

Labor Freedom score is 52.8%; and Monetary Freedom score is 77.9% as per Ault,

Arnold & Gest, (2010).

Page | 7

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

2.1.3. Economic / Political Features

Both, on the economic as well as political front, Germany remains EU’s most influential

member. It has a strong latitude towards freedom of business and investment. The

government’s policies of long-term entrepreneurial growth and competitiveness are

backed by a liberal attitude towards globalisation, well-preserved property rights and a

robust regulatory governance, as per Tiley & Loutzenhiser, (2012).

2.1.4. Import / Export Features

Germany’s total combined value of exports and imports equals to 86.9% of its GDP.

The average of import/export tariff rate is 2.0%. Germany’s FDI Inflow is $34.7 billion.

On the 2019 Index, Germany has Trade Freedom ratio of 86.0%, an Investment

Freedom ratio of 80.0% and a Financial Freedom ratio of 70.0%. Among the GeFJaS

members, Germany has the 2nd rank, asserts Ault, Arnold & Gest, (2010).

2.1.5. Population / GDP Growth Feature

Germany’s population is 82.7 million and its GDP (PPP) is $4.2 trillion. The Per Capita

income of its citizens is $50,425 and the country has an overall growth of 2.5% with an

average 1.7% growth considered on a 5-year compounded annual growth, say Miller &

Oats, (2012).

2.1.6. Employment / Unemployment Feature

Unemployment rate of Germany stands at 3.8% and is lower than the world and region

levels.

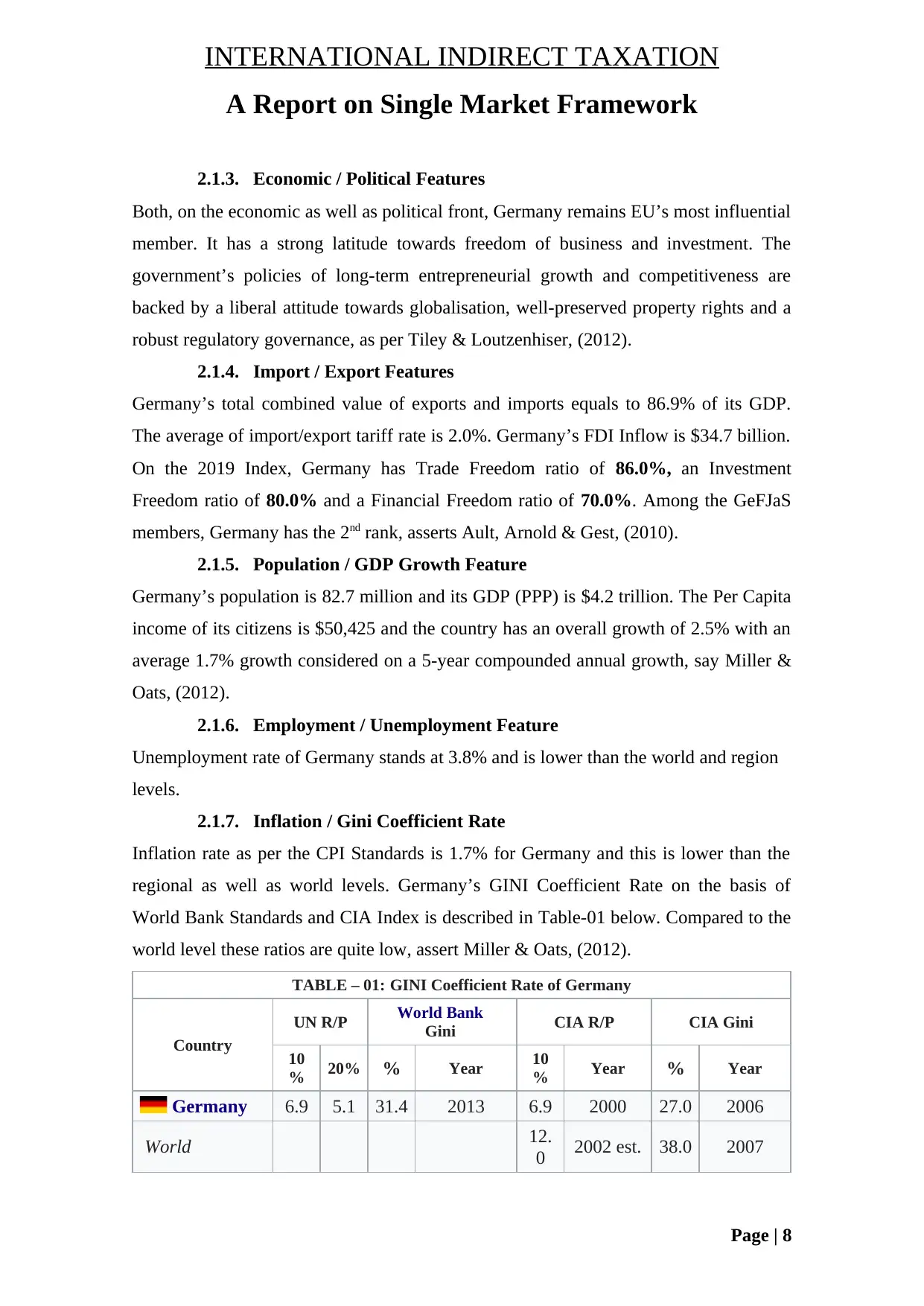

2.1.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 1.7% for Germany and this is lower than the

regional as well as world levels. Germany’s GINI Coefficient Rate on the basis of

World Bank Standards and CIA Index is described in Table-01 below. Compared to the

world level these ratios are quite low, assert Miller & Oats, (2012).

TABLE – 01: GINI Coefficient Rate of Germany

Country

UN R/P World Bank

Gini CIA R/P CIA Gini

10

% 20% % Year 10

% Year % Year

Germany 6.9 5.1 31.4 2013 6.9 2000 27.0 2006

World 12.

0 2002 est. 38.0 2007

Page | 8

A Report on Single Market Framework

2.1.3. Economic / Political Features

Both, on the economic as well as political front, Germany remains EU’s most influential

member. It has a strong latitude towards freedom of business and investment. The

government’s policies of long-term entrepreneurial growth and competitiveness are

backed by a liberal attitude towards globalisation, well-preserved property rights and a

robust regulatory governance, as per Tiley & Loutzenhiser, (2012).

2.1.4. Import / Export Features

Germany’s total combined value of exports and imports equals to 86.9% of its GDP.

The average of import/export tariff rate is 2.0%. Germany’s FDI Inflow is $34.7 billion.

On the 2019 Index, Germany has Trade Freedom ratio of 86.0%, an Investment

Freedom ratio of 80.0% and a Financial Freedom ratio of 70.0%. Among the GeFJaS

members, Germany has the 2nd rank, asserts Ault, Arnold & Gest, (2010).

2.1.5. Population / GDP Growth Feature

Germany’s population is 82.7 million and its GDP (PPP) is $4.2 trillion. The Per Capita

income of its citizens is $50,425 and the country has an overall growth of 2.5% with an

average 1.7% growth considered on a 5-year compounded annual growth, say Miller &

Oats, (2012).

2.1.6. Employment / Unemployment Feature

Unemployment rate of Germany stands at 3.8% and is lower than the world and region

levels.

2.1.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 1.7% for Germany and this is lower than the

regional as well as world levels. Germany’s GINI Coefficient Rate on the basis of

World Bank Standards and CIA Index is described in Table-01 below. Compared to the

world level these ratios are quite low, assert Miller & Oats, (2012).

TABLE – 01: GINI Coefficient Rate of Germany

Country

UN R/P World Bank

Gini CIA R/P CIA Gini

10

% 20% % Year 10

% Year % Year

Germany 6.9 5.1 31.4 2013 6.9 2000 27.0 2006

World 12.

0 2002 est. 38.0 2007

Page | 8

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

2.2. FRANCE

2.2.1. Main Features

Economic Freedom Score of France is 63.8 and this ranks its economy as 71st freest as

per 2019 Index. Its ranking in the EU region is 35th among the 44 countries, as per

Mendel & Bevacqua, (2010). On the basis of these rankings, France is above the world

but is below the regional averages, as per Campbell (ed), (2011).

2.2.2. Trade Features

Overall, the regulatory framework of France is relatively efficient, although its labour

market remains burdened because of strict regulations, hence its lacks in capacity of

generating a vibrant employment growth, assert Forte & Oppenheim, (2011). France’s

Business Freedom score is 81.2%; Labor Freedom score is 45.2%; and Monetary

Freedom score is 79.1% as per Campbell (ed), (2011).

2.2.3. Economic / Political Features

Although France has partial or fully privatized large enterprises, the government still

plays a strong role in sectors such as public transport, power and arms manufacturing, as

per Tiley & Loutzenhiser, (2012).

2.2.4. Import / Export Features

France’s total combined value of exports and imports equals to 62.9% of its GDP. The

average of import/export tariff rate is 2.0%. France’s FDI Inflow is $49.8 billion. France

imposes a number of non-tariff trade barriers and these include regulations related to

technical and product-specific subsidies and quotas. It also restricts investments in

selected sectors, declares Wheelright, (2013). On the 2019 Index, France has Trade

Freedom ratio of 81.0%, an Investment Freedom ratio of 75.0% and a Financial

Freedom ratio of 70.0%. Among the GeFJaS members, France stands at the 3rd rank.

2.2.5. Population / GDP Growth Feature

France’s population is 64.8 million and its GDP (PPP) is $2.8 trillion. The Per Capita

income of its citizens is $43,761 and the country has an overall growth of 1.8% with an

average 1.1% growth considered on a 5-year compounded annual growth, states

Wheelright, (2013).

2.2.6. Employment / Unemployment Feature

Unemployment rate of France stands at 9.4% and is quite high compared to the world

and region levels, asserts Wheelright, (2013).

Page | 9

A Report on Single Market Framework

2.2. FRANCE

2.2.1. Main Features

Economic Freedom Score of France is 63.8 and this ranks its economy as 71st freest as

per 2019 Index. Its ranking in the EU region is 35th among the 44 countries, as per

Mendel & Bevacqua, (2010). On the basis of these rankings, France is above the world

but is below the regional averages, as per Campbell (ed), (2011).

2.2.2. Trade Features

Overall, the regulatory framework of France is relatively efficient, although its labour

market remains burdened because of strict regulations, hence its lacks in capacity of

generating a vibrant employment growth, assert Forte & Oppenheim, (2011). France’s

Business Freedom score is 81.2%; Labor Freedom score is 45.2%; and Monetary

Freedom score is 79.1% as per Campbell (ed), (2011).

2.2.3. Economic / Political Features

Although France has partial or fully privatized large enterprises, the government still

plays a strong role in sectors such as public transport, power and arms manufacturing, as

per Tiley & Loutzenhiser, (2012).

2.2.4. Import / Export Features

France’s total combined value of exports and imports equals to 62.9% of its GDP. The

average of import/export tariff rate is 2.0%. France’s FDI Inflow is $49.8 billion. France

imposes a number of non-tariff trade barriers and these include regulations related to

technical and product-specific subsidies and quotas. It also restricts investments in

selected sectors, declares Wheelright, (2013). On the 2019 Index, France has Trade

Freedom ratio of 81.0%, an Investment Freedom ratio of 75.0% and a Financial

Freedom ratio of 70.0%. Among the GeFJaS members, France stands at the 3rd rank.

2.2.5. Population / GDP Growth Feature

France’s population is 64.8 million and its GDP (PPP) is $2.8 trillion. The Per Capita

income of its citizens is $43,761 and the country has an overall growth of 1.8% with an

average 1.1% growth considered on a 5-year compounded annual growth, states

Wheelright, (2013).

2.2.6. Employment / Unemployment Feature

Unemployment rate of France stands at 9.4% and is quite high compared to the world

and region levels, asserts Wheelright, (2013).

Page | 9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

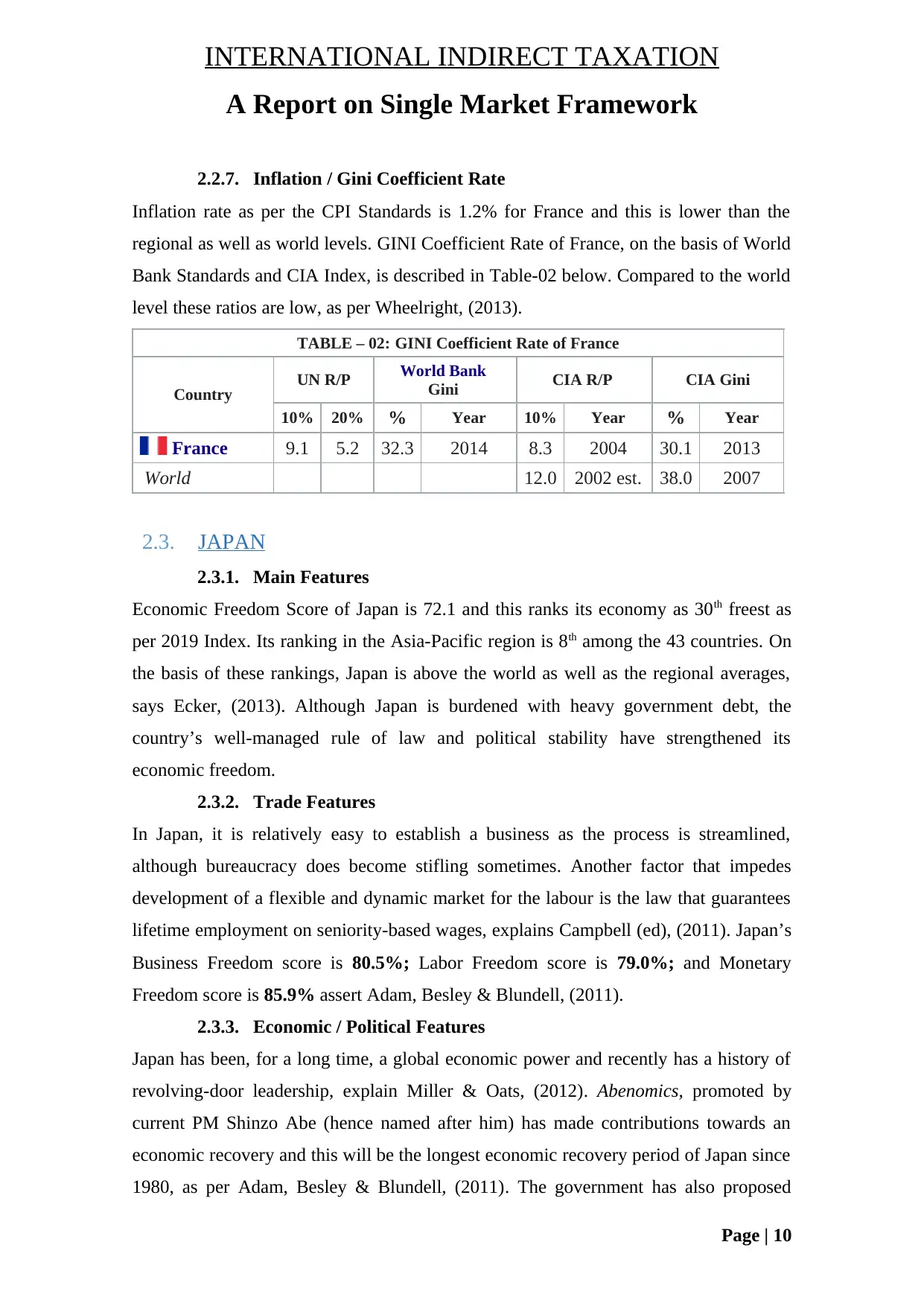

2.2.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 1.2% for France and this is lower than the

regional as well as world levels. GINI Coefficient Rate of France, on the basis of World

Bank Standards and CIA Index, is described in Table-02 below. Compared to the world

level these ratios are low, as per Wheelright, (2013).

TABLE – 02: GINI Coefficient Rate of France

Country UN R/P World Bank

Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

France 9.1 5.2 32.3 2014 8.3 2004 30.1 2013

World 12.0 2002 est. 38.0 2007

2.3. JAPAN

2.3.1. Main Features

Economic Freedom Score of Japan is 72.1 and this ranks its economy as 30th freest as

per 2019 Index. Its ranking in the Asia-Pacific region is 8th among the 43 countries. On

the basis of these rankings, Japan is above the world as well as the regional averages,

says Ecker, (2013). Although Japan is burdened with heavy government debt, the

country’s well-managed rule of law and political stability have strengthened its

economic freedom.

2.3.2. Trade Features

In Japan, it is relatively easy to establish a business as the process is streamlined,

although bureaucracy does become stifling sometimes. Another factor that impedes

development of a flexible and dynamic market for the labour is the law that guarantees

lifetime employment on seniority-based wages, explains Campbell (ed), (2011). Japan’s

Business Freedom score is 80.5%; Labor Freedom score is 79.0%; and Monetary

Freedom score is 85.9% assert Adam, Besley & Blundell, (2011).

2.3.3. Economic / Political Features

Japan has been, for a long time, a global economic power and recently has a history of

revolving-door leadership, explain Miller & Oats, (2012). Abenomics, promoted by

current PM Shinzo Abe (hence named after him) has made contributions towards an

economic recovery and this will be the longest economic recovery period of Japan since

1980, as per Adam, Besley & Blundell, (2011). The government has also proposed

Page | 10

A Report on Single Market Framework

2.2.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 1.2% for France and this is lower than the

regional as well as world levels. GINI Coefficient Rate of France, on the basis of World

Bank Standards and CIA Index, is described in Table-02 below. Compared to the world

level these ratios are low, as per Wheelright, (2013).

TABLE – 02: GINI Coefficient Rate of France

Country UN R/P World Bank

Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

France 9.1 5.2 32.3 2014 8.3 2004 30.1 2013

World 12.0 2002 est. 38.0 2007

2.3. JAPAN

2.3.1. Main Features

Economic Freedom Score of Japan is 72.1 and this ranks its economy as 30th freest as

per 2019 Index. Its ranking in the Asia-Pacific region is 8th among the 43 countries. On

the basis of these rankings, Japan is above the world as well as the regional averages,

says Ecker, (2013). Although Japan is burdened with heavy government debt, the

country’s well-managed rule of law and political stability have strengthened its

economic freedom.

2.3.2. Trade Features

In Japan, it is relatively easy to establish a business as the process is streamlined,

although bureaucracy does become stifling sometimes. Another factor that impedes

development of a flexible and dynamic market for the labour is the law that guarantees

lifetime employment on seniority-based wages, explains Campbell (ed), (2011). Japan’s

Business Freedom score is 80.5%; Labor Freedom score is 79.0%; and Monetary

Freedom score is 85.9% assert Adam, Besley & Blundell, (2011).

2.3.3. Economic / Political Features

Japan has been, for a long time, a global economic power and recently has a history of

revolving-door leadership, explain Miller & Oats, (2012). Abenomics, promoted by

current PM Shinzo Abe (hence named after him) has made contributions towards an

economic recovery and this will be the longest economic recovery period of Japan since

1980, as per Adam, Besley & Blundell, (2011). The government has also proposed

Page | 10

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

Trade Liberalization as a goal. Political stability, combined with a well-maintained rule

of law, has strengthened the country’s economic freedom, explain Miller & Oats,

(2012).

2.3.4. Import / Export Features

Japan’s total combined value of exports and imports equals to 31.3% of its GDP. The

average of import/export tariff rate is 2.5%. Japan’s FDI Inflow is $10.4 billion.

According to WTO, Japan had imposed 381 non-tariff measures. On the 2019 Index,

Japan has Trade Freedom ratio of 80.0%, an Investment Freedom ratio of 70.0% and a

Financial Freedom ratio of 60.0%. Among the GeFJaS members, Japan stands at the 4th

rank, as per Forte & Oppenheim, (2011).

2.3.5. Population / GDP Growth Feature

Japan’s population is 126.7 million and its GDP (PPP) is $5.4 trillion. The Per Capita

income of its citizens is $42,832 and the country has an overall growth of 1.7% with an

average 1.3% growth considered on a 5-year compounded annual growth, asserts

Hoffman et al, (2015).

2.3.6. Employment / Unemployment Feature

Unemployment rate of Japan stands at 2.8% and is very low compared to the world and

region levels, as per Forte & Oppenheim, (2011).

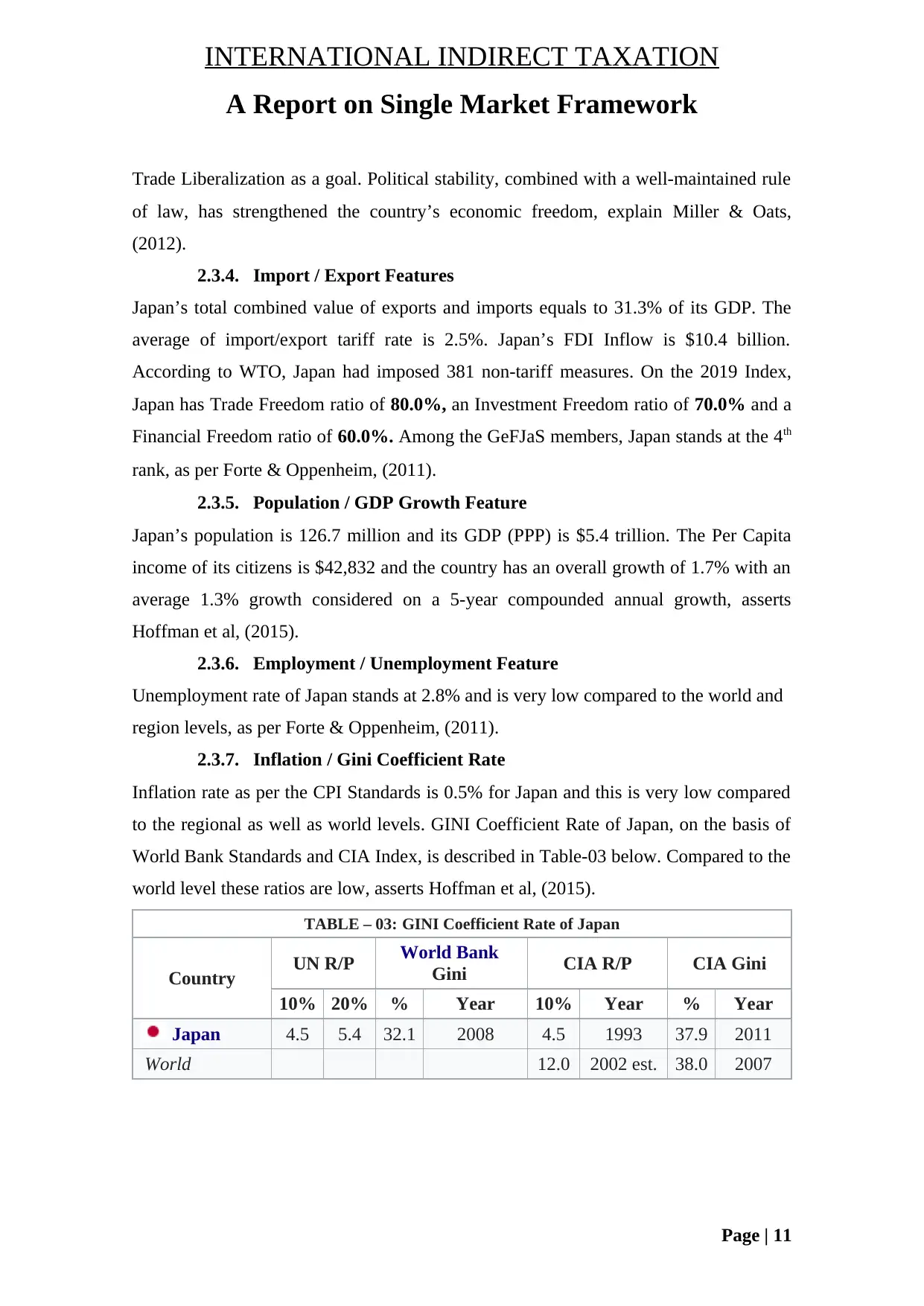

2.3.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 0.5% for Japan and this is very low compared

to the regional as well as world levels. GINI Coefficient Rate of Japan, on the basis of

World Bank Standards and CIA Index, is described in Table-03 below. Compared to the

world level these ratios are low, asserts Hoffman et al, (2015).

TABLE – 03: GINI Coefficient Rate of Japan

Country UN R/P World Bank

Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

Japan 4.5 5.4 32.1 2008 4.5 1993 37.9 2011

World 12.0 2002 est. 38.0 2007

Page | 11

A Report on Single Market Framework

Trade Liberalization as a goal. Political stability, combined with a well-maintained rule

of law, has strengthened the country’s economic freedom, explain Miller & Oats,

(2012).

2.3.4. Import / Export Features

Japan’s total combined value of exports and imports equals to 31.3% of its GDP. The

average of import/export tariff rate is 2.5%. Japan’s FDI Inflow is $10.4 billion.

According to WTO, Japan had imposed 381 non-tariff measures. On the 2019 Index,

Japan has Trade Freedom ratio of 80.0%, an Investment Freedom ratio of 70.0% and a

Financial Freedom ratio of 60.0%. Among the GeFJaS members, Japan stands at the 4th

rank, as per Forte & Oppenheim, (2011).

2.3.5. Population / GDP Growth Feature

Japan’s population is 126.7 million and its GDP (PPP) is $5.4 trillion. The Per Capita

income of its citizens is $42,832 and the country has an overall growth of 1.7% with an

average 1.3% growth considered on a 5-year compounded annual growth, asserts

Hoffman et al, (2015).

2.3.6. Employment / Unemployment Feature

Unemployment rate of Japan stands at 2.8% and is very low compared to the world and

region levels, as per Forte & Oppenheim, (2011).

2.3.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 0.5% for Japan and this is very low compared

to the regional as well as world levels. GINI Coefficient Rate of Japan, on the basis of

World Bank Standards and CIA Index, is described in Table-03 below. Compared to the

world level these ratios are low, asserts Hoffman et al, (2015).

TABLE – 03: GINI Coefficient Rate of Japan

Country UN R/P World Bank

Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

Japan 4.5 5.4 32.1 2008 4.5 1993 37.9 2011

World 12.0 2002 est. 38.0 2007

Page | 11

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

2.4. SINGAPORE

2.4.1. Main Features

Economic Freedom Score of Singapore is 89.4 and this ranks its economy as 2nd freest

as per 2019 Index. Its ranking in the Asia-Pacific region is 2nd among the 43 countries,

as per Ecker, (2013). On the basis of these rankings, Singapore is well above the world

and regional averages.

2.4.2. Trade Features

Singapore has the most transparent and efficient entrepreneurial environment in the

world. It has a simple business start-up process and does impose a minimum capital

requirement, as per Campbell (ed), (2011). The flexible labour market regulations are

supported by vibrant functions. The government generously funds the health care,

transport and housing through various subsidy programs and also controls prices

through different regulations and state-linked enterprises. Singapore’s Business

Freedom score is 90.8%; Labor Freedom score is 91.0%; and Monetary Freedom score

is 85.3%.

2.4.3. Economic / Political Features

Singapore is the perfect example of how to become a prosperous nation. Although

Service Industry dominates Singapore’s economy, the country also plays a major role in

the global electronics and chemicals industry and has one of world’s largest seaport, as

per Miller & Oats, (2012). This has helped the government in maintaining the lowest

unemployment rate in the developed world.

2.4.4. Import / Export Features

Singapore’s total combined value of exports and imports equals to 322.4% of its GDP.

The average of import/export tariff rate is 0.1 percent. Singapore’s FDI Inflow is $62.0

billion. Singapore had imposed 182 non-tariff measures as of June 30, 2018, as reported

by the WTO, Singapore’s global investment attitude has encouraged a vibrant

commercial activity. On the 2019 Index, Singapore has Trade Freedom ratio of 94.8%,

an Investment Freedom ratio of 85.0% and a Financial Freedom ratio of 80.0%. Among

the GeFJaS members, Singapore stands at 1st rank, as detailed by Bakker (ed.), (2009).

2.4.5. Population / GDP Growth Feature

Page | 12

A Report on Single Market Framework

2.4. SINGAPORE

2.4.1. Main Features

Economic Freedom Score of Singapore is 89.4 and this ranks its economy as 2nd freest

as per 2019 Index. Its ranking in the Asia-Pacific region is 2nd among the 43 countries,

as per Ecker, (2013). On the basis of these rankings, Singapore is well above the world

and regional averages.

2.4.2. Trade Features

Singapore has the most transparent and efficient entrepreneurial environment in the

world. It has a simple business start-up process and does impose a minimum capital

requirement, as per Campbell (ed), (2011). The flexible labour market regulations are

supported by vibrant functions. The government generously funds the health care,

transport and housing through various subsidy programs and also controls prices

through different regulations and state-linked enterprises. Singapore’s Business

Freedom score is 90.8%; Labor Freedom score is 91.0%; and Monetary Freedom score

is 85.3%.

2.4.3. Economic / Political Features

Singapore is the perfect example of how to become a prosperous nation. Although

Service Industry dominates Singapore’s economy, the country also plays a major role in

the global electronics and chemicals industry and has one of world’s largest seaport, as

per Miller & Oats, (2012). This has helped the government in maintaining the lowest

unemployment rate in the developed world.

2.4.4. Import / Export Features

Singapore’s total combined value of exports and imports equals to 322.4% of its GDP.

The average of import/export tariff rate is 0.1 percent. Singapore’s FDI Inflow is $62.0

billion. Singapore had imposed 182 non-tariff measures as of June 30, 2018, as reported

by the WTO, Singapore’s global investment attitude has encouraged a vibrant

commercial activity. On the 2019 Index, Singapore has Trade Freedom ratio of 94.8%,

an Investment Freedom ratio of 85.0% and a Financial Freedom ratio of 80.0%. Among

the GeFJaS members, Singapore stands at 1st rank, as detailed by Bakker (ed.), (2009).

2.4.5. Population / GDP Growth Feature

Page | 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

Singapore’s population is 5.6 million and its GDP (PPP) is $527.0 billion. The Per

Capita income of its citizens is $93,906 and the country has an overall growth of 3.6%

with an average 3.5% growth considered on a 5-year compounded annual growth.

2.4.6. Employment / Unemployment Feature

Unemployment rate of Singapore stands at 2.0% and is very low compared to the world

and region levels, details Bakker (ed.), (2009).

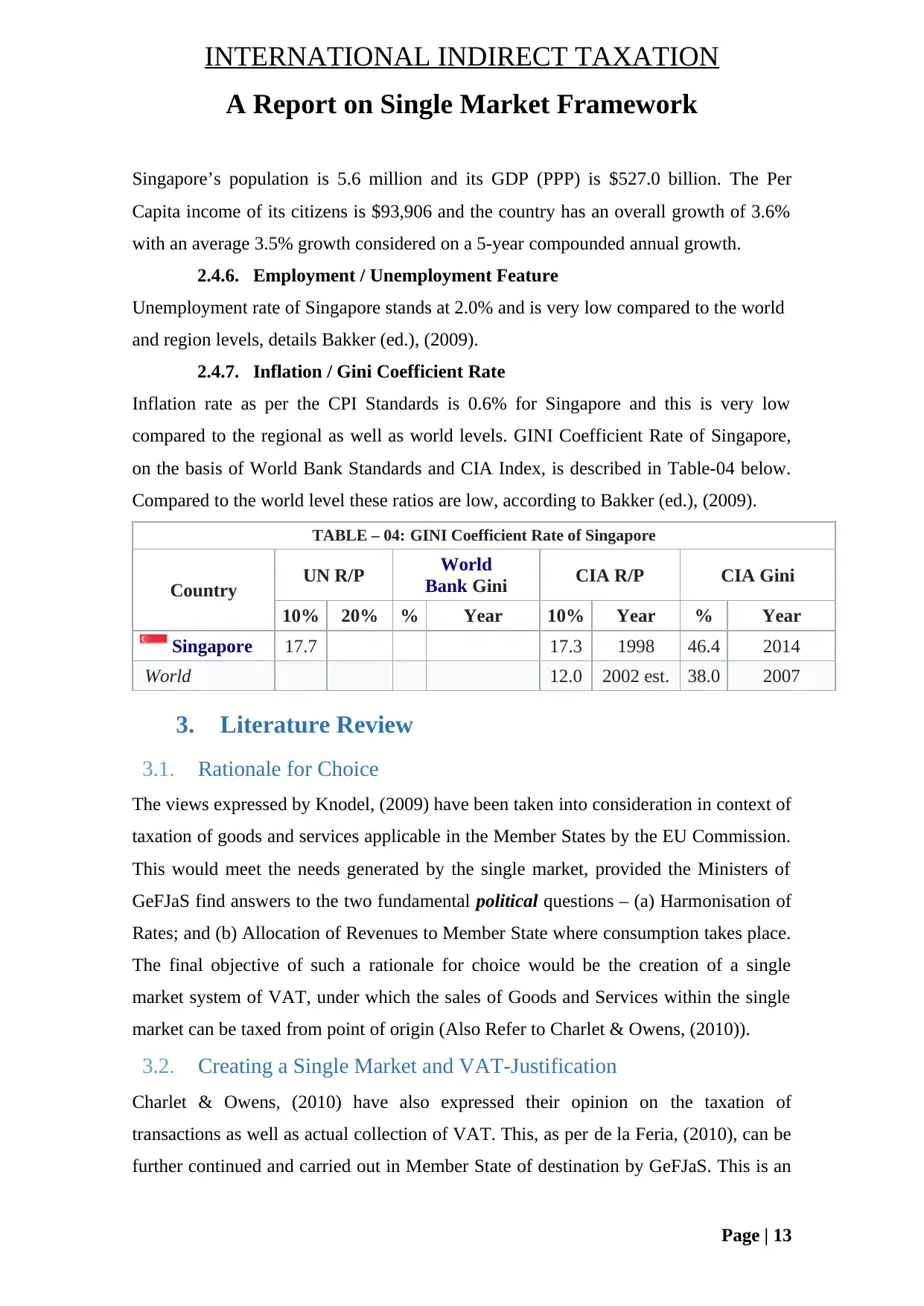

2.4.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 0.6% for Singapore and this is very low

compared to the regional as well as world levels. GINI Coefficient Rate of Singapore,

on the basis of World Bank Standards and CIA Index, is described in Table-04 below.

Compared to the world level these ratios are low, according to Bakker (ed.), (2009).

TABLE – 04: GINI Coefficient Rate of Singapore

Country UN R/P World

Bank Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

Singapore 17.7 17.3 1998 46.4 2014

World 12.0 2002 est. 38.0 2007

3. Literature Review

3.1. Rationale for Choice

The views expressed by Knodel, (2009) have been taken into consideration in context of

taxation of goods and services applicable in the Member States by the EU Commission.

This would meet the needs generated by the single market, provided the Ministers of

GeFJaS find answers to the two fundamental political questions – (a) Harmonisation of

Rates; and (b) Allocation of Revenues to Member State where consumption takes place.

The final objective of such a rationale for choice would be the creation of a single

market system of VAT, under which the sales of Goods and Services within the single

market can be taxed from point of origin (Also Refer to Charlet & Owens, (2010)).

3.2. Creating a Single Market and VAT-Justification

Charlet & Owens, (2010) have also expressed their opinion on the taxation of

transactions as well as actual collection of VAT. This, as per de la Feria, (2010), can be

further continued and carried out in Member State of destination by GeFJaS. This is an

Page | 13

A Report on Single Market Framework

Singapore’s population is 5.6 million and its GDP (PPP) is $527.0 billion. The Per

Capita income of its citizens is $93,906 and the country has an overall growth of 3.6%

with an average 3.5% growth considered on a 5-year compounded annual growth.

2.4.6. Employment / Unemployment Feature

Unemployment rate of Singapore stands at 2.0% and is very low compared to the world

and region levels, details Bakker (ed.), (2009).

2.4.7. Inflation / Gini Coefficient Rate

Inflation rate as per the CPI Standards is 0.6% for Singapore and this is very low

compared to the regional as well as world levels. GINI Coefficient Rate of Singapore,

on the basis of World Bank Standards and CIA Index, is described in Table-04 below.

Compared to the world level these ratios are low, according to Bakker (ed.), (2009).

TABLE – 04: GINI Coefficient Rate of Singapore

Country UN R/P World

Bank Gini CIA R/P CIA Gini

10% 20% % Year 10% Year % Year

Singapore 17.7 17.3 1998 46.4 2014

World 12.0 2002 est. 38.0 2007

3. Literature Review

3.1. Rationale for Choice

The views expressed by Knodel, (2009) have been taken into consideration in context of

taxation of goods and services applicable in the Member States by the EU Commission.

This would meet the needs generated by the single market, provided the Ministers of

GeFJaS find answers to the two fundamental political questions – (a) Harmonisation of

Rates; and (b) Allocation of Revenues to Member State where consumption takes place.

The final objective of such a rationale for choice would be the creation of a single

market system of VAT, under which the sales of Goods and Services within the single

market can be taxed from point of origin (Also Refer to Charlet & Owens, (2010)).

3.2. Creating a Single Market and VAT-Justification

Charlet & Owens, (2010) have also expressed their opinion on the taxation of

transactions as well as actual collection of VAT. This, as per de la Feria, (2010), can be

further continued and carried out in Member State of destination by GeFJaS. This is an

Page | 13

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

acceptable consideration to the country, in which the sold goods or services have to be

finally consumed. As per CEC, (1996), this is where the VAT revenue generated should

be accruing. Under this given situation of VAT collection at destination, CEC, (1996)

says it is possible to make all arrangements with minimum rules about VAT rates and

the applicable legislations, so that the autonomy of all the Member States is preserved.

3.3. Approach and Results – A Summary

It has been observed that there has not been much change in the situation since the

initial discussions took place between the Ministers. Now that the introductory phase

has been completed, the Minister's initial proposal on the single market is being

accepted for application. There is no need for approximating all the Member States'

laws. As detailed by de la Feria, (2010), the member states have formalised an initial

level of harmonisation of the VAT rates. This summary, made as per the suggestions

formulated by the Ministers under the historical background, will help the

administrators of the policy document, to understand what to expect from the policy and

to come forward with their proposals, which would definitely be based on their

understanding of the policy document, asserts Bakker (ed.), (2009). The main criteria of

approach taken for implementing the policy would be as summarised below –

Taxation format at place of origin. This will be the place where goods and

services are situated at the time of sale by the enterprise.

Approximation of the VAT Rates and the concerned legislation. This is to be

implemented for limiting the risks and competition does not get distorted.

Formulating a Mechanism of Compensation, which can be commonly accepted

by all the Member States. This is for ensuring that the collection of revenue

continues to accrue to Member State where consumption of goods or services is

proposed to take place, as explained by Mendel & Bevacqua, (2010).

3.4. EU Council Directive on VAT

This paper’s suggestions put forward to the Ministers of the member states are being

accepted without going into the detailed observations which were presented by the EU

Council in its Directive Report (COM (94) 515 of 23 November 1994), which

concerned the transitional arrangements of operations, as detailed by Mendel &

Bevacqua, (2010). The Ministers expressed that their experience about the transitional

system has been fundamentally used to change the assessments which were made to the

Page | 14

A Report on Single Market Framework

acceptable consideration to the country, in which the sold goods or services have to be

finally consumed. As per CEC, (1996), this is where the VAT revenue generated should

be accruing. Under this given situation of VAT collection at destination, CEC, (1996)

says it is possible to make all arrangements with minimum rules about VAT rates and

the applicable legislations, so that the autonomy of all the Member States is preserved.

3.3. Approach and Results – A Summary

It has been observed that there has not been much change in the situation since the

initial discussions took place between the Ministers. Now that the introductory phase

has been completed, the Minister's initial proposal on the single market is being

accepted for application. There is no need for approximating all the Member States'

laws. As detailed by de la Feria, (2010), the member states have formalised an initial

level of harmonisation of the VAT rates. This summary, made as per the suggestions

formulated by the Ministers under the historical background, will help the

administrators of the policy document, to understand what to expect from the policy and

to come forward with their proposals, which would definitely be based on their

understanding of the policy document, asserts Bakker (ed.), (2009). The main criteria of

approach taken for implementing the policy would be as summarised below –

Taxation format at place of origin. This will be the place where goods and

services are situated at the time of sale by the enterprise.

Approximation of the VAT Rates and the concerned legislation. This is to be

implemented for limiting the risks and competition does not get distorted.

Formulating a Mechanism of Compensation, which can be commonly accepted

by all the Member States. This is for ensuring that the collection of revenue

continues to accrue to Member State where consumption of goods or services is

proposed to take place, as explained by Mendel & Bevacqua, (2010).

3.4. EU Council Directive on VAT

This paper’s suggestions put forward to the Ministers of the member states are being

accepted without going into the detailed observations which were presented by the EU

Council in its Directive Report (COM (94) 515 of 23 November 1994), which

concerned the transitional arrangements of operations, as detailed by Mendel &

Bevacqua, (2010). The Ministers expressed that their experience about the transitional

system has been fundamentally used to change the assessments which were made to the

Page | 14

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

solution previously put forward. This has finally led the Policy Document to be

redefined with new characteristics which have introduced a common system of VAT for

the proposed single market, according to Bhattacharjee & Bhattacharya, (2018).

3.5. Academic Paper Sources – Single Market

Please Refer to Bibliography Section at the end of this Report.

3.6. Academic Paper Sources – VAT

Please Refer to Bibliography Section at the end of this Report.

3.7. Official Journal of EU

The EU Council Directive 77/388/EEC of 17 May 1977, which concerned

harmonisation of laws connected with the Member States and related to turnover taxes

such as Common System of VAT: Uniform Basis of Assessment”, has now been

significantly amended, as detailed by Bhattacharjee & Bhattacharya, (2018). When new

amendments have been made to this Directive, it becomes necessary that for reasons of

rationalisation and clarity, the old Directive must be recast. The suggestions of the

Ministers that the Common System of VAT should be, even if VAT Rates and the

concerned exemptions cannot be fully harmonised, implemented after amendments, as

per Basu, (2013).

3.8. Scope of VAT for a Single Market

The present VAT system had been designed so that VAT revenues could be collected

directly in the state where the goods or services are consumed or is deemed to take

place. In the present context, this objective can only be achieved by the member states

of GeFJaS, by simplifying the complex rules which had to be introduced to define the

final destination of a transaction, as detailed by Pfeiffer & Ursprung-Steindl (eds.),

(2015).

On the basis of the data collected, there will be about 25 different rules which need to be

simplified by the Ministers of GeFJaS member states to finally determine the place

where the transaction has to be taxed. This will ultimately mean, inter alia, that all the

trade houses will be required to divide their turnover between various Member States of

GeFJaS, especially those which are competent for taxing and this will divert the efforts

of compartmentalising the concept of a single market, explains Campbell (ed), (2011).

Page | 15

A Report on Single Market Framework

solution previously put forward. This has finally led the Policy Document to be

redefined with new characteristics which have introduced a common system of VAT for

the proposed single market, according to Bhattacharjee & Bhattacharya, (2018).

3.5. Academic Paper Sources – Single Market

Please Refer to Bibliography Section at the end of this Report.

3.6. Academic Paper Sources – VAT

Please Refer to Bibliography Section at the end of this Report.

3.7. Official Journal of EU

The EU Council Directive 77/388/EEC of 17 May 1977, which concerned

harmonisation of laws connected with the Member States and related to turnover taxes

such as Common System of VAT: Uniform Basis of Assessment”, has now been

significantly amended, as detailed by Bhattacharjee & Bhattacharya, (2018). When new

amendments have been made to this Directive, it becomes necessary that for reasons of

rationalisation and clarity, the old Directive must be recast. The suggestions of the

Ministers that the Common System of VAT should be, even if VAT Rates and the

concerned exemptions cannot be fully harmonised, implemented after amendments, as

per Basu, (2013).

3.8. Scope of VAT for a Single Market

The present VAT system had been designed so that VAT revenues could be collected

directly in the state where the goods or services are consumed or is deemed to take

place. In the present context, this objective can only be achieved by the member states

of GeFJaS, by simplifying the complex rules which had to be introduced to define the

final destination of a transaction, as detailed by Pfeiffer & Ursprung-Steindl (eds.),

(2015).

On the basis of the data collected, there will be about 25 different rules which need to be

simplified by the Ministers of GeFJaS member states to finally determine the place

where the transaction has to be taxed. This will ultimately mean, inter alia, that all the

trade houses will be required to divide their turnover between various Member States of

GeFJaS, especially those which are competent for taxing and this will divert the efforts

of compartmentalising the concept of a single market, explains Campbell (ed), (2011).

Page | 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

3.9. Territorial Scope of a Single Market

A system from the past will always prevent VAT to be based on commercial

transactions which are accounted by firms. This will prove to be a major obstacle in the

development of a genuine single market system. A new, remodelled system, will enable

each entrepreneur to achieve, particular the small and medium-sized enterprises

(SMEs), which would be major beneficiaries of the new opportunities which will be

available after the formation of a single market system involving GeFJaS. Maintenance

of status quo will also become a source for legal uncertainty for the operators as well as

the administrators, as detailed by Campbell (ed), (2011). This is because both will face

the difficulty of satisfying themselves with the factual points, such as whether the goods

or services were indeed transported to the receiving Member State, without providing a

real way of proving an absolutely conclusive result, explains Campbell (ed), (2011).

4. Technical Knowledge

4.1. Identifying the End-user

When the single market system comes into application all across the GeFJaS Zone, it

will become impractical for a supplier to declare all of its sales made to various places

in the zone, where it has customers, as per Lang et al (eds.), (2009). This is the

prevailing practice in all member nations’ own territory and this has to be abolished. In

the Community Level system, a supplier will be registered only in one member nation

and operate in the entire GeFJaS Zone as if this supplier is registered all over the zone,

asserts Knodel, (2009). The following are the practical explanations for this practice –

This practice makes it easier for the supplier to exercise its rights of declaration

and deduction at one place.

This practice makes it easier for the consumer who can obtain goods from the

supplier of its choice without any constraint.

This practice makes it more efficient for the tax administrators as they can

monitor all activities of the taxable entity.

4.2. Supplies – Full and Partial Exemption

If a supplier deals in the sale of goods and services which are exempt from VAT, then

the supplier is exempt from registering for VAT. However, such a supplier cannot claim

input VAT paid on purchase or expenses. In case the supplier deals both in VAT

Page | 16

A Report on Single Market Framework

3.9. Territorial Scope of a Single Market

A system from the past will always prevent VAT to be based on commercial

transactions which are accounted by firms. This will prove to be a major obstacle in the

development of a genuine single market system. A new, remodelled system, will enable

each entrepreneur to achieve, particular the small and medium-sized enterprises

(SMEs), which would be major beneficiaries of the new opportunities which will be

available after the formation of a single market system involving GeFJaS. Maintenance

of status quo will also become a source for legal uncertainty for the operators as well as

the administrators, as detailed by Campbell (ed), (2011). This is because both will face

the difficulty of satisfying themselves with the factual points, such as whether the goods

or services were indeed transported to the receiving Member State, without providing a

real way of proving an absolutely conclusive result, explains Campbell (ed), (2011).

4. Technical Knowledge

4.1. Identifying the End-user

When the single market system comes into application all across the GeFJaS Zone, it

will become impractical for a supplier to declare all of its sales made to various places

in the zone, where it has customers, as per Lang et al (eds.), (2009). This is the

prevailing practice in all member nations’ own territory and this has to be abolished. In

the Community Level system, a supplier will be registered only in one member nation

and operate in the entire GeFJaS Zone as if this supplier is registered all over the zone,

asserts Knodel, (2009). The following are the practical explanations for this practice –

This practice makes it easier for the supplier to exercise its rights of declaration

and deduction at one place.

This practice makes it easier for the consumer who can obtain goods from the

supplier of its choice without any constraint.

This practice makes it more efficient for the tax administrators as they can

monitor all activities of the taxable entity.

4.2. Supplies – Full and Partial Exemption

If a supplier deals in the sale of goods and services which are exempt from VAT, then

the supplier is exempt from registering for VAT. However, such a supplier cannot claim

input VAT paid on purchase or expenses. In case the supplier deals both in VAT

Page | 16

INTERNATIONAL INDIRECT TAXATION

A Report on Single Market Framework

applicable as well as VAT exempt goods and services, then he supplier is classified as

partly exempt, as per Muller et al (eds.), (2017).

4.3. Distance Selling / Reverse Charges

A transaction will be subjected to Reverse Charges when the recipient of the goods or

services makes a report of both the purchase (for input VAT) and the sale (for output

VAT) in its VAT return. Reverse Charge transactions reduces the requirement of the

supplier to get itself registered for VAT in country of supply, as described by Muller et

al (eds.), (2017).

4.4. VAT MOSS / Digital Supply

In case the supplier is making a Digital Supply to a customer within the GeFJaS Zone,

as per Hafner, Robin & Hoorens, (2014) the transaction is liable for VAT MOSS

payment which stands for Value Added Tax: Mini One Stop Shop.

4.5. Payment on Account

When a self-employed taxpayer wishes to make VAT payments on bi-annual basis, it is

known as Payment on Account. The authorities determine the amount on the basis of

the taxpayer’s previous year tax bill, as per Hafner, Robin & Hoorens, (2014).

4.6. Flat Rate Scheme

Under the Flat Rate Scheme, a supplier is allowed to retain the difference between

amount paid to the tax authorities and the amount of VAT which is charged to the

consumer, according to Charlet & Owens, (2010).

4.7. Differentiating Goods and Services

Goods are usually tangible, meaning the buyer can see them and include a chair or a

computer, explain Charlet & Owens, (2010). Whereas services are non-tangible

meaning they are not visible to the buyer such as services offered by barristers and

accountants. In case of goods, the recipient pays for the material and in case of services

the payment is for the skills of the seller as detailed by Charlet & Owens, (2010).

4.8. Residual Input Tax

In cases where the goods or services are partly used for recoverable supplies and partly

for the non-recoverable supplies, the incurred input tax is termed as residual or

overhead input tax. In these cases, the recovery of tax is restricted to the specific portion

which is subject to VAT recovery, as explained by de la Feria, (2010); CEC, (1996).

Page | 17

A Report on Single Market Framework

applicable as well as VAT exempt goods and services, then he supplier is classified as

partly exempt, as per Muller et al (eds.), (2017).

4.3. Distance Selling / Reverse Charges

A transaction will be subjected to Reverse Charges when the recipient of the goods or

services makes a report of both the purchase (for input VAT) and the sale (for output

VAT) in its VAT return. Reverse Charge transactions reduces the requirement of the

supplier to get itself registered for VAT in country of supply, as described by Muller et

al (eds.), (2017).

4.4. VAT MOSS / Digital Supply

In case the supplier is making a Digital Supply to a customer within the GeFJaS Zone,

as per Hafner, Robin & Hoorens, (2014) the transaction is liable for VAT MOSS

payment which stands for Value Added Tax: Mini One Stop Shop.

4.5. Payment on Account

When a self-employed taxpayer wishes to make VAT payments on bi-annual basis, it is

known as Payment on Account. The authorities determine the amount on the basis of

the taxpayer’s previous year tax bill, as per Hafner, Robin & Hoorens, (2014).

4.6. Flat Rate Scheme

Under the Flat Rate Scheme, a supplier is allowed to retain the difference between

amount paid to the tax authorities and the amount of VAT which is charged to the

consumer, according to Charlet & Owens, (2010).

4.7. Differentiating Goods and Services

Goods are usually tangible, meaning the buyer can see them and include a chair or a

computer, explain Charlet & Owens, (2010). Whereas services are non-tangible

meaning they are not visible to the buyer such as services offered by barristers and

accountants. In case of goods, the recipient pays for the material and in case of services

the payment is for the skills of the seller as detailed by Charlet & Owens, (2010).