Exploring Types of Modifications and Qualifications in Audit Reports

VerifiedAdded on 2023/04/19

|5

|4407

|358

Report

AI Summary

This report provides an overview of audit report modifications and qualifications, focusing on explaining the different types of opinions an auditor might issue. It discusses the importance of understanding these modifications for stakeholders and their reliance on financial statements. The report likely covers topics such as qualified opinions, adverse opinions, and disclaimers of opinion, detailing the circumstances under which each type of modification is appropriate. The analysis draws from relevant auditing standards and academic literature to provide a comprehensive understanding of how audit reports can be modified to reflect the auditor's findings and their impact on the reliability of financial information. This document is available on Desklib, a platform offering a wide range of study tools and solved assignments for students.

International Journal of Economics and Financial

Issues

ISSN: 2146-4138

available at http: www.econjournals.com

International Journal of Economics and Financial Issues, 2017, 7(3), 304-308.

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017304

The Impact of Audit Reports on Financial Information Content

Alireza Vaziri1*, Kayhan Azadi2

1Department of Accounting, Islamic Azad University, Rasht Branch, Rasht, Iran, 2Department of Accounting, Islamic Azad

University, Rasht Branch, Rasht, Iran. *Email: ARV.vaziry@gmail.com

ABSTRACT

Investors fund in order to access to more wealth. Financial information of companies is one of the important factors considered by investors in making

decision. According to accounting standards, the major goal of providing forms and financial reports is providing useful information about financial

position and the results of operations of commercial unit for user decision making. Several factors influence on financial information provided by

companies. One of these factors can be audit reports. Therefore, major goal of this research is investigating the effects of audit reports on financial

information reported in Tehran Stock Exchange. Method of this research is practical in goal and is descriptive in type. The types of auditor and auditor’s

assessment (audit organizations or institutions) were proposed as independent variables and financial information (stocks return) was proposed as

dependent variable. In this research 117 accepted companies in Tehran Stock Exchange during 2009-2014 were selected as statistical sample. Research

hypotheses were tested by fitting of linear regression models of combined data. The results showed that the type of auditor and auditor’s assessment

have a significant relationship with stocks return (financial information).

Keywords: The Type of Auditors, Stocks Return, The Type of Auditor’s Assessment, Tehran Stock Exchange

JEL Classifications: E44, M42

1. INTRODUCTION

The existence of vivid and reliable financial information that is

the product of a comprehensive reporting system is considered

as the main elements of assessment of situation and function of

a company and decision-making about the securities exchange

issued by that. In the recent professional societies, from the

perspective of users, the information is considered to be reliable

that an independent organization on the company’s reporting

process and at the gravity center of this process, i.e., to monitor

the financial statements. An example of such independent

organizations are audit firms that mainly in the business units,

the internal control structure of the reporting unit and the final

product of the internal control system, the financial statements are

reviewed and monitored (Hassas and Jafari, 2010). On the other

hand, in the commercial world, transactions and economic events

are documented via assembling evidence by accountants and

recorded in the accounts. The results of transactions and economic

events are available to interested parties out of extracted accounts

and within framework of financial reports. However, the biased

information, misleading, irrelevant or incomplete may cause the

wrong decision-making. Complexity of economics’ issues and

the process of converting them into information also cause the

possibility of appearance of errors in processing information and

as a result, it makes trouble to recognize the quality on presented

reports for the reports’ users. On the other hand, conflict of interest

between producers of fiscal statements and users from them causes

a concern for users. Besides, the lack of direct access of users and

their distances to information producer causes uncertainty and

ambiguity of the financial reports’ users to them. In this situation

the audit is formed on the basis of the above needs and it is a tool

to eliminate the doubt and ambiguity of financial reporting by

confirming their quality. It should be noted that in some conditions

in reporting environment, allowing direct assessment of data

quality by users is very difficult. Despite these circumstances, it

makes indirect evaluation of information quality very necessary.

This is a situation where there is justifying the need for auditing

by independent auditors and making opinion, could be due to a

conflict of interest, important economic consequences, complexity

and lack of direct access. Auditors validate presented financial

information and users can be sure that the using information enjoys

good quality (Hajiha and FeizAbadi, 2013). According to this, the

Issues

ISSN: 2146-4138

available at http: www.econjournals.com

International Journal of Economics and Financial Issues, 2017, 7(3), 304-308.

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017304

The Impact of Audit Reports on Financial Information Content

Alireza Vaziri1*, Kayhan Azadi2

1Department of Accounting, Islamic Azad University, Rasht Branch, Rasht, Iran, 2Department of Accounting, Islamic Azad

University, Rasht Branch, Rasht, Iran. *Email: ARV.vaziry@gmail.com

ABSTRACT

Investors fund in order to access to more wealth. Financial information of companies is one of the important factors considered by investors in making

decision. According to accounting standards, the major goal of providing forms and financial reports is providing useful information about financial

position and the results of operations of commercial unit for user decision making. Several factors influence on financial information provided by

companies. One of these factors can be audit reports. Therefore, major goal of this research is investigating the effects of audit reports on financial

information reported in Tehran Stock Exchange. Method of this research is practical in goal and is descriptive in type. The types of auditor and auditor’s

assessment (audit organizations or institutions) were proposed as independent variables and financial information (stocks return) was proposed as

dependent variable. In this research 117 accepted companies in Tehran Stock Exchange during 2009-2014 were selected as statistical sample. Research

hypotheses were tested by fitting of linear regression models of combined data. The results showed that the type of auditor and auditor’s assessment

have a significant relationship with stocks return (financial information).

Keywords: The Type of Auditors, Stocks Return, The Type of Auditor’s Assessment, Tehran Stock Exchange

JEL Classifications: E44, M42

1. INTRODUCTION

The existence of vivid and reliable financial information that is

the product of a comprehensive reporting system is considered

as the main elements of assessment of situation and function of

a company and decision-making about the securities exchange

issued by that. In the recent professional societies, from the

perspective of users, the information is considered to be reliable

that an independent organization on the company’s reporting

process and at the gravity center of this process, i.e., to monitor

the financial statements. An example of such independent

organizations are audit firms that mainly in the business units,

the internal control structure of the reporting unit and the final

product of the internal control system, the financial statements are

reviewed and monitored (Hassas and Jafari, 2010). On the other

hand, in the commercial world, transactions and economic events

are documented via assembling evidence by accountants and

recorded in the accounts. The results of transactions and economic

events are available to interested parties out of extracted accounts

and within framework of financial reports. However, the biased

information, misleading, irrelevant or incomplete may cause the

wrong decision-making. Complexity of economics’ issues and

the process of converting them into information also cause the

possibility of appearance of errors in processing information and

as a result, it makes trouble to recognize the quality on presented

reports for the reports’ users. On the other hand, conflict of interest

between producers of fiscal statements and users from them causes

a concern for users. Besides, the lack of direct access of users and

their distances to information producer causes uncertainty and

ambiguity of the financial reports’ users to them. In this situation

the audit is formed on the basis of the above needs and it is a tool

to eliminate the doubt and ambiguity of financial reporting by

confirming their quality. It should be noted that in some conditions

in reporting environment, allowing direct assessment of data

quality by users is very difficult. Despite these circumstances, it

makes indirect evaluation of information quality very necessary.

This is a situation where there is justifying the need for auditing

by independent auditors and making opinion, could be due to a

conflict of interest, important economic consequences, complexity

and lack of direct access. Auditors validate presented financial

information and users can be sure that the using information enjoys

good quality (Hajiha and FeizAbadi, 2013). According to this, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Vaziri and Azadi: The Impact of Audit Reports on Financial Information Content

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017 305

current research is a review of subjective literature of audit report

and the content of reported financial information will influence on

listed companies in Tehran’s Stock Exchange. Then, the impact

of audit report and content of reported financial information and

of companies listed on Tehran Stock Exchange will be discussed.

2. PROBLEM STATEMENT

Today shareholders can use audited financial statements as an

important tool to notice how to operate their assets and ensure the

accuracy of managers’ performance. The usefulness of content of

numbers and submitted figures in the financial statements that is

the final product of accounting is the most controversial issue of

subjects in scientific meetings. In general, the first and foremost

goal is to provide financial statements. From the information

reported to investors and creditors and other current and potential

clients for investment decisions, accreditation and other similar

decisions become beneficial. One of the most useful accounting

information is efficient figure of shares. On the other hand, the

possibility of bad intention in setting and preparation of the

financial statements by the board, led to the need for the audit

profession and individuals called auditor to be felt. Existence of

vivid and comparable financial information is one of the main

pillars to respond the executives and essential needs of economic

decision-making. Done researches show that more disclosure and

transparency will follow many advantages for companies: Long-

term investment by the investors, improving access to new capital,

less capital expenditures, credible and responsible management

and ultimately higher stock price (Banimahd et al., 2014).

In addition, to take the advantage of financial information in

decision-making of mentioned groups, that accounting targets

and financial reporting require to reveal related information to

appropriate species and access this information become feasible for

everyone. Increase of disclosure about information for users who

aren’t able to determine the company future prospects is useful and

this advantage is through reducing the risk of misallocation of their

capital. Moreover, one of the crucial conditions for the confidence

of investors and creditors in constructive economic activity

is sufficient information to make decisions about purchasing,

holding or selling stock and assess the performance of companies’

managers (Hasani and Hoseini, 2010).

Auditor’s report on the process of decision-making by users

of financial statements is considered as one of the most useful

tools. When auditors is not to make an acceptable opinion on the

information given in financial statements, his opinion validate the

financial statements and information contained in the financial

statements remain unchanged, or to be more precise, the registered

information will be approved. If qualified opinion a failed or lacks

of opinion without an impartial financial expert questions all or

part of the information contained in the financial statements.

The effect of the auditing profession’s activities and its role in

the stock returns of companies listed in Tehran Stock Exchange

and the investment process relies on the information provided by

companies’ managers as an evaluator reference and it is judged by

the auditor. Through this result potential and actual shareholders

are reflected (Jamei et al., 2012).

Auditing profession has effective role on improving

informational system and inspiring confidence of each country’s

financial reports. With the increase in the number of users

of the auditor’s report as customers of public goods, has led

the quality of auditors’ work to be paid attention. Quality of

auditors’ work and their remark, can improve the country’s

financial informational system and finally making decision

for an optimal economy. In the recent years the formation of

CPAs, (Certified Public Accountants) a part of the activities

of audit organization has been assigned to private institutions

of its community (Moradzadeh and Rahmannejad, 2011). The

content of accounting information and auditor’s opinion and its

role in decision-making of readers, especially investors in the

stock exchange were the subjects that has been investigated and

studied over the past four decades in the markets of Australia,

Canada, England, France, Spain and the Islamic Republic of

Iran. Now the main question is whether the type of the auditor

and the auditor’s opinion has an impact on stock’s returns?

3. EXPRESSING MODELS AND VARIABLES

OF THE RESEARCH

1. Yit = β0 + β1DQOit + β2Sizeit + β3Leverageit + β4Growthit

+ β5ROAit + β6ROEit + εit

2. Yit = β0 + β1DUOit + β2Sizeit + β3Leverageit + β4Growthit

+ β5ROAit + β6ROEit + εit

3.1. Financial Information Content (The Dependent

Variable)

The content of financial information is called to the information

that is effective on users’ decisions on assessment of past events,

present and future or assessment and correction of their past

evaluation (Dianati et al., 2012).

3.2. Stock Returns (The Dependent Variable)

It is called to the benefit and profit from an investment. In other

words, return is the ratio of total revenue (loss) from investments

in a specific period to the quantity of the capitals that have been

applied to earn this income initially in the same period and has

been consumed (Robu and Robu, 2015).

3.3. Audit Report (Independent)

The main purpose of an audit is that the auditor declares a

professional concept to the integrity of financial statements

with reviewing the results of the investigation of the registers

and documents that the examined final financial statements

of the institution rely on them, and regarding the information

and different explanation acquired during the process of the

verification. The statement in the report entitled “Audit report” or

the auditor’s report and auditors’ report as the person or authority

who has assigned auditing to the auditor, is presented that may be

issued in two forms either short or detailed in appropriate terms

(Hajiha and Rafiei, 2014).

The auditor’s opinion (independent) auditor’s opinion is said to the

professional reporting process respecting the financial statement

(Rahimian and Hedayati, 2013).

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017 305

current research is a review of subjective literature of audit report

and the content of reported financial information will influence on

listed companies in Tehran’s Stock Exchange. Then, the impact

of audit report and content of reported financial information and

of companies listed on Tehran Stock Exchange will be discussed.

2. PROBLEM STATEMENT

Today shareholders can use audited financial statements as an

important tool to notice how to operate their assets and ensure the

accuracy of managers’ performance. The usefulness of content of

numbers and submitted figures in the financial statements that is

the final product of accounting is the most controversial issue of

subjects in scientific meetings. In general, the first and foremost

goal is to provide financial statements. From the information

reported to investors and creditors and other current and potential

clients for investment decisions, accreditation and other similar

decisions become beneficial. One of the most useful accounting

information is efficient figure of shares. On the other hand, the

possibility of bad intention in setting and preparation of the

financial statements by the board, led to the need for the audit

profession and individuals called auditor to be felt. Existence of

vivid and comparable financial information is one of the main

pillars to respond the executives and essential needs of economic

decision-making. Done researches show that more disclosure and

transparency will follow many advantages for companies: Long-

term investment by the investors, improving access to new capital,

less capital expenditures, credible and responsible management

and ultimately higher stock price (Banimahd et al., 2014).

In addition, to take the advantage of financial information in

decision-making of mentioned groups, that accounting targets

and financial reporting require to reveal related information to

appropriate species and access this information become feasible for

everyone. Increase of disclosure about information for users who

aren’t able to determine the company future prospects is useful and

this advantage is through reducing the risk of misallocation of their

capital. Moreover, one of the crucial conditions for the confidence

of investors and creditors in constructive economic activity

is sufficient information to make decisions about purchasing,

holding or selling stock and assess the performance of companies’

managers (Hasani and Hoseini, 2010).

Auditor’s report on the process of decision-making by users

of financial statements is considered as one of the most useful

tools. When auditors is not to make an acceptable opinion on the

information given in financial statements, his opinion validate the

financial statements and information contained in the financial

statements remain unchanged, or to be more precise, the registered

information will be approved. If qualified opinion a failed or lacks

of opinion without an impartial financial expert questions all or

part of the information contained in the financial statements.

The effect of the auditing profession’s activities and its role in

the stock returns of companies listed in Tehran Stock Exchange

and the investment process relies on the information provided by

companies’ managers as an evaluator reference and it is judged by

the auditor. Through this result potential and actual shareholders

are reflected (Jamei et al., 2012).

Auditing profession has effective role on improving

informational system and inspiring confidence of each country’s

financial reports. With the increase in the number of users

of the auditor’s report as customers of public goods, has led

the quality of auditors’ work to be paid attention. Quality of

auditors’ work and their remark, can improve the country’s

financial informational system and finally making decision

for an optimal economy. In the recent years the formation of

CPAs, (Certified Public Accountants) a part of the activities

of audit organization has been assigned to private institutions

of its community (Moradzadeh and Rahmannejad, 2011). The

content of accounting information and auditor’s opinion and its

role in decision-making of readers, especially investors in the

stock exchange were the subjects that has been investigated and

studied over the past four decades in the markets of Australia,

Canada, England, France, Spain and the Islamic Republic of

Iran. Now the main question is whether the type of the auditor

and the auditor’s opinion has an impact on stock’s returns?

3. EXPRESSING MODELS AND VARIABLES

OF THE RESEARCH

1. Yit = β0 + β1DQOit + β2Sizeit + β3Leverageit + β4Growthit

+ β5ROAit + β6ROEit + εit

2. Yit = β0 + β1DUOit + β2Sizeit + β3Leverageit + β4Growthit

+ β5ROAit + β6ROEit + εit

3.1. Financial Information Content (The Dependent

Variable)

The content of financial information is called to the information

that is effective on users’ decisions on assessment of past events,

present and future or assessment and correction of their past

evaluation (Dianati et al., 2012).

3.2. Stock Returns (The Dependent Variable)

It is called to the benefit and profit from an investment. In other

words, return is the ratio of total revenue (loss) from investments

in a specific period to the quantity of the capitals that have been

applied to earn this income initially in the same period and has

been consumed (Robu and Robu, 2015).

3.3. Audit Report (Independent)

The main purpose of an audit is that the auditor declares a

professional concept to the integrity of financial statements

with reviewing the results of the investigation of the registers

and documents that the examined final financial statements

of the institution rely on them, and regarding the information

and different explanation acquired during the process of the

verification. The statement in the report entitled “Audit report” or

the auditor’s report and auditors’ report as the person or authority

who has assigned auditing to the auditor, is presented that may be

issued in two forms either short or detailed in appropriate terms

(Hajiha and Rafiei, 2014).

The auditor’s opinion (independent) auditor’s opinion is said to the

professional reporting process respecting the financial statement

(Rahimian and Hedayati, 2013).

Vaziri and Azadi: The Impact of Audit Reports on Financial Information Content

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017306

The type of auditor (independent) the type of auditor is said to

the type of audit institutions that include large and small audit

institutions (Jahanshad and Navaei, 2013).

4. RESEARCH LITERATURE

Callen and Khan (2013) in their research surveyed the quality

of accounting information and delay information affecting this

information on the stock price and its relationship with the future

stock returns. They stated that whatever the quality of accounting

is reduced, the relevance and reliability of it will be reduced and

consequently, prediction accuracy of cash flows and returns will

be reduced for investors.

Noor-ul-Haq et al. (2012) examined the relationship between

economic power and the state auditor in 46 countries. They

showed that whatever the quality of government is politically

and economically powerful, then choosing four large auditing

institutions is plausible. They also confirmed the affluent countries

that have accepted international financial reporting standards,

choosing four large auditing institutions is plausible. The results

of their research confirmed that whatever the government of a

country is stronger the demand is more for higher-quality audit

services (Kadilli, 2015).

Leventis and Dimitropoulos (2010) audit services pricing, the

interest quality and the board independence were examined for 97

companies, between the years 2000 and 2004. The results of this

study show that there is a positive relationship between auditor

independence and audit services pricing. Moreover, there is a

positive relationship between audit services pricing and interest

management that the result is for the companies with small size

(Kausar et al., 2015).

Chen et al. (2010) examined the effect of auditor size (as a factor

of audit quality) on interest management and capital costs for

the two categories of Chinese companies. A group of companies

owned by the states and others non-state-owned companies. The

results of this study showed that the impact of auditing quality in

reducing interest management is stronger in private companies

than public companies. In addition, cost of capital, that investor

consider for the information risk as a value. Private companies

are more influenced by the quality audit than public companies.

5. RESEARCH HYPOTHESES

H1: There is a significant relationship between type of auditor’s

opinion and stock returns.

H2: There is a significant relationship between type of auditor

(audit organization or institution) and stock returns.

6. RESEARCH METHODOLOGY

This study is considered descriptive in terms of type of research

and applicable, in terms of category of researches based on

purpose. The statistical community this research includes all the

companies listed in Tehran Stock Exchange from 2009 and after

that until 2014 which were present in stock exchange including

463 companies. In this study, sampling method is elimination

systematic as following conditions:

1. Not to be among insurance companies, investment, leasing,

banks and financial institutions, financial moderators, because

these companies have the nature of the different activities

2. The companies that their financial data can be written during

this 6 years and in this period have not had out of stock

exchange and entered stock exchange or even have not have

stock exchange interruptions and other transactions

3. In order to ensure comparability and avoid the heterogeneity

of its fiscal year ending March 18th and financial year should

not be changed during the years 2009-2014

4. Financial statements and explanatory notes are available

accompanying them.

In this study, the panel data is applied using software Eviews 7.

7. THE RESULTS OF HYPOTHESIS TEST

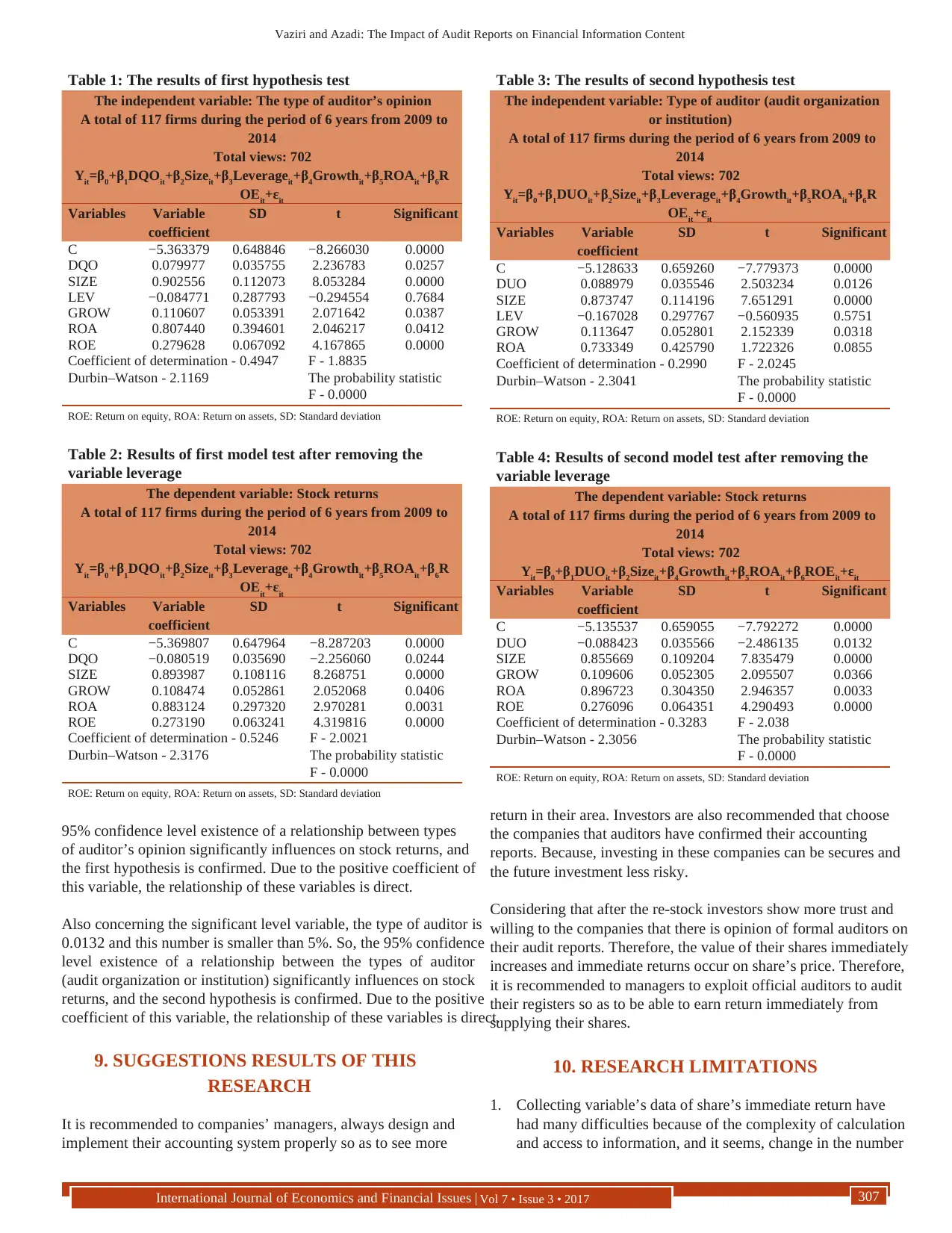

7.1. The Results of First Hypothesis Test

After the initial analysis of the regression model output as the

Table 1 were determined after an examination of the research’s

variables, it was revealed that fiscal leverage is not effective on

stock exchange’s returns in this model that with elimination of this

variable the underneath right model was analyzed.

As it is observed in Table 2, based on the results of initial model’s

estimation, regarding to P value. Statistic F is proved that the model

is approved by 99% confidence.

Durbin–Watson with 2.3176 shows lack of correlation between

the errors. In addition, according to the obtained coefficient of

determination, used variables in the model explains totally 0.52%

of the dependent variable’s behavior.

7.2. The Results of Second Hypothesis Test

After the initial analysis of the regression model output as the

Table 3 were determined after an examination of the research’s

variables, it was revealed that fiscal leverage is not effective on

stock exchange’s returns in this model that with elimination of this

variable the underneath right model was analyzed.

As it is observed in Table 4, based on the results of initial model’s

estimation, regarding to P value. Statistic F is proved that the model

is approved by 99% confidence.

Durbin–Watson with 2.30 shows lack of correlation between

the errors. In addition, according to the obtained coefficient of

determination, used variables in the model explains totally 0.32%

of the dependent variable’s behavior.

8. CONCLUSION

Concerning the significant level variable, the type of auditor’s

opinion is 0.0244 and this number is smaller than 5%. So, the

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017306

The type of auditor (independent) the type of auditor is said to

the type of audit institutions that include large and small audit

institutions (Jahanshad and Navaei, 2013).

4. RESEARCH LITERATURE

Callen and Khan (2013) in their research surveyed the quality

of accounting information and delay information affecting this

information on the stock price and its relationship with the future

stock returns. They stated that whatever the quality of accounting

is reduced, the relevance and reliability of it will be reduced and

consequently, prediction accuracy of cash flows and returns will

be reduced for investors.

Noor-ul-Haq et al. (2012) examined the relationship between

economic power and the state auditor in 46 countries. They

showed that whatever the quality of government is politically

and economically powerful, then choosing four large auditing

institutions is plausible. They also confirmed the affluent countries

that have accepted international financial reporting standards,

choosing four large auditing institutions is plausible. The results

of their research confirmed that whatever the government of a

country is stronger the demand is more for higher-quality audit

services (Kadilli, 2015).

Leventis and Dimitropoulos (2010) audit services pricing, the

interest quality and the board independence were examined for 97

companies, between the years 2000 and 2004. The results of this

study show that there is a positive relationship between auditor

independence and audit services pricing. Moreover, there is a

positive relationship between audit services pricing and interest

management that the result is for the companies with small size

(Kausar et al., 2015).

Chen et al. (2010) examined the effect of auditor size (as a factor

of audit quality) on interest management and capital costs for

the two categories of Chinese companies. A group of companies

owned by the states and others non-state-owned companies. The

results of this study showed that the impact of auditing quality in

reducing interest management is stronger in private companies

than public companies. In addition, cost of capital, that investor

consider for the information risk as a value. Private companies

are more influenced by the quality audit than public companies.

5. RESEARCH HYPOTHESES

H1: There is a significant relationship between type of auditor’s

opinion and stock returns.

H2: There is a significant relationship between type of auditor

(audit organization or institution) and stock returns.

6. RESEARCH METHODOLOGY

This study is considered descriptive in terms of type of research

and applicable, in terms of category of researches based on

purpose. The statistical community this research includes all the

companies listed in Tehran Stock Exchange from 2009 and after

that until 2014 which were present in stock exchange including

463 companies. In this study, sampling method is elimination

systematic as following conditions:

1. Not to be among insurance companies, investment, leasing,

banks and financial institutions, financial moderators, because

these companies have the nature of the different activities

2. The companies that their financial data can be written during

this 6 years and in this period have not had out of stock

exchange and entered stock exchange or even have not have

stock exchange interruptions and other transactions

3. In order to ensure comparability and avoid the heterogeneity

of its fiscal year ending March 18th and financial year should

not be changed during the years 2009-2014

4. Financial statements and explanatory notes are available

accompanying them.

In this study, the panel data is applied using software Eviews 7.

7. THE RESULTS OF HYPOTHESIS TEST

7.1. The Results of First Hypothesis Test

After the initial analysis of the regression model output as the

Table 1 were determined after an examination of the research’s

variables, it was revealed that fiscal leverage is not effective on

stock exchange’s returns in this model that with elimination of this

variable the underneath right model was analyzed.

As it is observed in Table 2, based on the results of initial model’s

estimation, regarding to P value. Statistic F is proved that the model

is approved by 99% confidence.

Durbin–Watson with 2.3176 shows lack of correlation between

the errors. In addition, according to the obtained coefficient of

determination, used variables in the model explains totally 0.52%

of the dependent variable’s behavior.

7.2. The Results of Second Hypothesis Test

After the initial analysis of the regression model output as the

Table 3 were determined after an examination of the research’s

variables, it was revealed that fiscal leverage is not effective on

stock exchange’s returns in this model that with elimination of this

variable the underneath right model was analyzed.

As it is observed in Table 4, based on the results of initial model’s

estimation, regarding to P value. Statistic F is proved that the model

is approved by 99% confidence.

Durbin–Watson with 2.30 shows lack of correlation between

the errors. In addition, according to the obtained coefficient of

determination, used variables in the model explains totally 0.32%

of the dependent variable’s behavior.

8. CONCLUSION

Concerning the significant level variable, the type of auditor’s

opinion is 0.0244 and this number is smaller than 5%. So, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Vaziri and Azadi: The Impact of Audit Reports on Financial Information Content

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017 307

95% confidence level existence of a relationship between types

of auditor’s opinion significantly influences on stock returns, and

the first hypothesis is confirmed. Due to the positive coefficient of

this variable, the relationship of these variables is direct.

Also concerning the significant level variable, the type of auditor is

0.0132 and this number is smaller than 5%. So, the 95% confidence

level existence of a relationship between the types of auditor

(audit organization or institution) significantly influences on stock

returns, and the second hypothesis is confirmed. Due to the positive

coefficient of this variable, the relationship of these variables is direct.

9. SUGGESTIONS RESULTS OF THIS

RESEARCH

It is recommended to companies’ managers, always design and

implement their accounting system properly so as to see more

return in their area. Investors are also recommended that choose

the companies that auditors have confirmed their accounting

reports. Because, investing in these companies can be secures and

the future investment less risky.

Considering that after the re-stock investors show more trust and

willing to the companies that there is opinion of formal auditors on

their audit reports. Therefore, the value of their shares immediately

increases and immediate returns occur on share’s price. Therefore,

it is recommended to managers to exploit official auditors to audit

their registers so as to be able to earn return immediately from

supplying their shares.

10. RESEARCH LIMITATIONS

1. Collecting variable’s data of share’s immediate return have

had many difficulties because of the complexity of calculation

and access to information, and it seems, change in the number

Table 3: The results of second hypothesis test

The independent variable: Type of auditor (audit organization

or institution)

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DUOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.128633 0.659260 −7.779373 0.0000

DUO 0.088979 0.035546 2.503234 0.0126

SIZE 0.873747 0.114196 7.651291 0.0000

LEV −0.167028 0.297767 −0.560935 0.5751

GROW 0.113647 0.052801 2.152339 0.0318

ROA 0.733349 0.425790 1.722326 0.0855

Coefficient of determination - 0.2990 F - 2.0245

Durbin–Watson - 2.3041 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 4: Results of second model test after removing the

variable leverage

The dependent variable: Stock returns

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DUOit+β2Sizeit+β4Growthit+β5ROAit+β6ROEit+εit

Variables Variable

coefficient

SD t Significant

C −5.135537 0.659055 −7.792272 0.0000

DUO −0.088423 0.035566 −2.486135 0.0132

SIZE 0.855669 0.109204 7.835479 0.0000

GROW 0.109606 0.052305 2.095507 0.0366

ROA 0.896723 0.304350 2.946357 0.0033

ROE 0.276096 0.064351 4.290493 0.0000

Coefficient of determination - 0.3283 F - 2.038

Durbin–Watson - 2.3056 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 2: Results of first model test after removing the

variable leverage

The dependent variable: Stock returns

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DQOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.369807 0.647964 −8.287203 0.0000

DQO −0.080519 0.035690 −2.256060 0.0244

SIZE 0.893987 0.108116 8.268751 0.0000

GROW 0.108474 0.052861 2.052068 0.0406

ROA 0.883124 0.297320 2.970281 0.0031

ROE 0.273190 0.063241 4.319816 0.0000

Coefficient of determination - 0.5246 F - 2.0021

Durbin–Watson - 2.3176 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 1: The results of first hypothesis test

The independent variable: The type of auditor’s opinion

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DQOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.363379 0.648846 −8.266030 0.0000

DQO 0.079977 0.035755 2.236783 0.0257

SIZE 0.902556 0.112073 8.053284 0.0000

LEV −0.084771 0.287793 −0.294554 0.7684

GROW 0.110607 0.053391 2.071642 0.0387

ROA 0.807440 0.394601 2.046217 0.0412

ROE 0.279628 0.067092 4.167865 0.0000

Coefficient of determination - 0.4947 F - 1.8835

Durbin–Watson - 2.1169 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017 307

95% confidence level existence of a relationship between types

of auditor’s opinion significantly influences on stock returns, and

the first hypothesis is confirmed. Due to the positive coefficient of

this variable, the relationship of these variables is direct.

Also concerning the significant level variable, the type of auditor is

0.0132 and this number is smaller than 5%. So, the 95% confidence

level existence of a relationship between the types of auditor

(audit organization or institution) significantly influences on stock

returns, and the second hypothesis is confirmed. Due to the positive

coefficient of this variable, the relationship of these variables is direct.

9. SUGGESTIONS RESULTS OF THIS

RESEARCH

It is recommended to companies’ managers, always design and

implement their accounting system properly so as to see more

return in their area. Investors are also recommended that choose

the companies that auditors have confirmed their accounting

reports. Because, investing in these companies can be secures and

the future investment less risky.

Considering that after the re-stock investors show more trust and

willing to the companies that there is opinion of formal auditors on

their audit reports. Therefore, the value of their shares immediately

increases and immediate returns occur on share’s price. Therefore,

it is recommended to managers to exploit official auditors to audit

their registers so as to be able to earn return immediately from

supplying their shares.

10. RESEARCH LIMITATIONS

1. Collecting variable’s data of share’s immediate return have

had many difficulties because of the complexity of calculation

and access to information, and it seems, change in the number

Table 3: The results of second hypothesis test

The independent variable: Type of auditor (audit organization

or institution)

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DUOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.128633 0.659260 −7.779373 0.0000

DUO 0.088979 0.035546 2.503234 0.0126

SIZE 0.873747 0.114196 7.651291 0.0000

LEV −0.167028 0.297767 −0.560935 0.5751

GROW 0.113647 0.052801 2.152339 0.0318

ROA 0.733349 0.425790 1.722326 0.0855

Coefficient of determination - 0.2990 F - 2.0245

Durbin–Watson - 2.3041 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 4: Results of second model test after removing the

variable leverage

The dependent variable: Stock returns

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DUOit+β2Sizeit+β4Growthit+β5ROAit+β6ROEit+εit

Variables Variable

coefficient

SD t Significant

C −5.135537 0.659055 −7.792272 0.0000

DUO −0.088423 0.035566 −2.486135 0.0132

SIZE 0.855669 0.109204 7.835479 0.0000

GROW 0.109606 0.052305 2.095507 0.0366

ROA 0.896723 0.304350 2.946357 0.0033

ROE 0.276096 0.064351 4.290493 0.0000

Coefficient of determination - 0.3283 F - 2.038

Durbin–Watson - 2.3056 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 2: Results of first model test after removing the

variable leverage

The dependent variable: Stock returns

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DQOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.369807 0.647964 −8.287203 0.0000

DQO −0.080519 0.035690 −2.256060 0.0244

SIZE 0.893987 0.108116 8.268751 0.0000

GROW 0.108474 0.052861 2.052068 0.0406

ROA 0.883124 0.297320 2.970281 0.0031

ROE 0.273190 0.063241 4.319816 0.0000

Coefficient of determination - 0.5246 F - 2.0021

Durbin–Watson - 2.3176 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Table 1: The results of first hypothesis test

The independent variable: The type of auditor’s opinion

A total of 117 firms during the period of 6 years from 2009 to

2014

Total views: 702

Yit=β0+β1DQOit+β2Sizeit+β3Leverageit+β4Growthit+β5ROAit+β6R

OEit+εit

Variables Variable

coefficient

SD t Significant

C −5.363379 0.648846 −8.266030 0.0000

DQO 0.079977 0.035755 2.236783 0.0257

SIZE 0.902556 0.112073 8.053284 0.0000

LEV −0.084771 0.287793 −0.294554 0.7684

GROW 0.110607 0.053391 2.071642 0.0387

ROA 0.807440 0.394601 2.046217 0.0412

ROE 0.279628 0.067092 4.167865 0.0000

Coefficient of determination - 0.4947 F - 1.8835

Durbin–Watson - 2.1169 The probability statistic

F - 0.0000

ROE: Return on equity, ROA: Return on assets, SD: Standard deviation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Vaziri and Azadi: The Impact of Audit Reports on Financial Information Content

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017308

of days after the meeting could change the results.

2. Management and political problems and macro-economic

indexes such as changes in the company’s managers after a

general meeting is an issue that can affect the research’s results

by interfering in share’s returns.

REFERENCES

Banimahd, B., Yahya, H.Y., Yazdanian, N. (2014), Earnings management

and auditor’s opinion: Evidence from the private sector auditing.

Journal of Management Accounting, 21, 32-17.

Callen, J., Khan, M. (2013), Accounting quality, stock price delay

and future stock returns. Temporary Accounting Research, 30(1),

269-295.

Chen, H., Chen, J.Z., Lobo, G.J., Wang, Y. (2010), Effects of audit quality

on earnings management and cost of equity capital: Evidence from

China. Contemporary Accounting Research, 28(3), 892-925.

Dianati, Z., Alemi, M.R., Samiran, B.P. (2012), Relationship between

quality of financial information and risk measures in the Tehran

stock exchange. Journal of Stock Exchange Quarterly, 17(5), 41-23.

Hajiha, Z., Feizabadi, F. (2013), Relationship between liquidity ratios

and profitability and ability to pay obligations. Journal of Financial

Accounting and Auditing Research, 19, 127-151.

Hajiha, Z., Rafiei, A. (2014), The impact on the quality of the internal

audit function when the independent audit report. Journal of Financial

Accounting and Auditing, 6(24), 137-121.

Hasani, M., Hosseini, M.B. (2010), Exploring the relationship between

accounting information disclosure level and volatility of stock prices

in companies listed on Tehran stock exchange. Journal of Economics

and Business, 75, 84-75.

Hassas, Y.Y., Jafari, V. (2010), Effect of rotating audit firms audit report

on the quality of listed companies in Tehran stock exchange. Journal

of Stock Exchange Quarterly, 9, 42-25.

Houqe, N., Zijl, M., Tony van. Monem, Reza. (2012), Government quality,

auditor choice and adoption of IFRS: A cross country analysis,

Journal of Accounting Research, No. 4, PP. 233-251.

Jahanshad, A., Navaei, L.M. (2013), The effect of auditor tenure and type

of conservative profit auditing and reporting. Journal of Financial

Accounting and Auditing Research, 18, 107-128.

Jamei, R., Halshi, M., Abdollah, H.E. (2012), Evaluate the performance

of managers on independent auditor’s report on companies listed

on the Tehran stock exchange. Journal of Accounting and Audit

Review, 19(4), 1-14.

Kadilli, A. (2015), Predictability of stock returns of financial companies

and the role of investor sentiment: A multi-country analysis. Journal

of Financial Stability, 5(3), 1-62.

Kausar, A., Shroff, N., White, H. (2015), Real effects of the audit choice.

Journal of Accounting and Economics, 8, 1-63.

Leventis S., Dimitropoulos, P.E. ( 2010), Audit pricing, quality of earning

and board independence: The cose of the Athens stock exchange,

International Journal of Cardiology 26, pp. 325-332.

Moradzadeh, F.M., Rahmannejad, G. (2011), Evaluate the effect of the

auditor on the value relevance of earnings in companies listed on

the Tehran stock exchange. Journal of Accounting Management,

1, 62-51.

Rahimian, N., Hedayati, A. (2013), The factors affecting the auditor’s

professional opinion. Journal of Chartered Accountant, 12, 85-77.

Robu, M.A., Robu, I.B. (2015), The influence of the audit report on the

relevance of accounting information reported by listed Romanian

companies. Procedia Economics and Finance, 20, 562-570.

International Journal of Economics and Financial Issues | Vol 7 • Issue 3 • 2017308

of days after the meeting could change the results.

2. Management and political problems and macro-economic

indexes such as changes in the company’s managers after a

general meeting is an issue that can affect the research’s results

by interfering in share’s returns.

REFERENCES

Banimahd, B., Yahya, H.Y., Yazdanian, N. (2014), Earnings management

and auditor’s opinion: Evidence from the private sector auditing.

Journal of Management Accounting, 21, 32-17.

Callen, J., Khan, M. (2013), Accounting quality, stock price delay

and future stock returns. Temporary Accounting Research, 30(1),

269-295.

Chen, H., Chen, J.Z., Lobo, G.J., Wang, Y. (2010), Effects of audit quality

on earnings management and cost of equity capital: Evidence from

China. Contemporary Accounting Research, 28(3), 892-925.

Dianati, Z., Alemi, M.R., Samiran, B.P. (2012), Relationship between

quality of financial information and risk measures in the Tehran

stock exchange. Journal of Stock Exchange Quarterly, 17(5), 41-23.

Hajiha, Z., Feizabadi, F. (2013), Relationship between liquidity ratios

and profitability and ability to pay obligations. Journal of Financial

Accounting and Auditing Research, 19, 127-151.

Hajiha, Z., Rafiei, A. (2014), The impact on the quality of the internal

audit function when the independent audit report. Journal of Financial

Accounting and Auditing, 6(24), 137-121.

Hasani, M., Hosseini, M.B. (2010), Exploring the relationship between

accounting information disclosure level and volatility of stock prices

in companies listed on Tehran stock exchange. Journal of Economics

and Business, 75, 84-75.

Hassas, Y.Y., Jafari, V. (2010), Effect of rotating audit firms audit report

on the quality of listed companies in Tehran stock exchange. Journal

of Stock Exchange Quarterly, 9, 42-25.

Houqe, N., Zijl, M., Tony van. Monem, Reza. (2012), Government quality,

auditor choice and adoption of IFRS: A cross country analysis,

Journal of Accounting Research, No. 4, PP. 233-251.

Jahanshad, A., Navaei, L.M. (2013), The effect of auditor tenure and type

of conservative profit auditing and reporting. Journal of Financial

Accounting and Auditing Research, 18, 107-128.

Jamei, R., Halshi, M., Abdollah, H.E. (2012), Evaluate the performance

of managers on independent auditor’s report on companies listed

on the Tehran stock exchange. Journal of Accounting and Audit

Review, 19(4), 1-14.

Kadilli, A. (2015), Predictability of stock returns of financial companies

and the role of investor sentiment: A multi-country analysis. Journal

of Financial Stability, 5(3), 1-62.

Kausar, A., Shroff, N., White, H. (2015), Real effects of the audit choice.

Journal of Accounting and Economics, 8, 1-63.

Leventis S., Dimitropoulos, P.E. ( 2010), Audit pricing, quality of earning

and board independence: The cose of the Athens stock exchange,

International Journal of Cardiology 26, pp. 325-332.

Moradzadeh, F.M., Rahmannejad, G. (2011), Evaluate the effect of the

auditor on the value relevance of earnings in companies listed on

the Tehran stock exchange. Journal of Accounting Management,

1, 62-51.

Rahimian, N., Hedayati, A. (2013), The factors affecting the auditor’s

professional opinion. Journal of Chartered Accountant, 12, 85-77.

Robu, M.A., Robu, I.B. (2015), The influence of the audit report on the

relevance of accounting information reported by listed Romanian

companies. Procedia Economics and Finance, 20, 562-570.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.