A Comparison of Bankruptcy Models

VerifiedAdded on 2023/04/21

|11

|4491

|275

AI Summary

This study analyzes and compares three bankruptcy models - Z-Score model, O-score model, and Zmijewski's model - to predict financial distress and bankruptcy in industrial corporations. The study aims to find the best predictor of bankruptcy and provide suggestions to improve financial performance. The data is collected from Texmo Industries, Coimbatore, and analyzed using Z-score analysis, Ohlson's O-score analysis, and Zmijewski's analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

INTERNATIONAL JOURNAL OF MARKETING,

FINANCIAL SERVICES & MANAGEMENT RESEARCH

Vol.1 No. 4, April 2012, ISSN 2277 3622

Online Available at indianresearchjournals.com

A COMPARISON OF BANKRUPTCY MODELS

*DR. RADHA GANESH KUMAR, **KISHORE KUMAR,

*Associate Professor, Department of Management Studies, Valliammai Engineering College, Kattankulathur

** Managemnet Trainee, Congruent solutions, Chennai

76

ABSTRACT

Financial analysis can be applied in a wide variety of situations to give business managers

the information they need to make crucial decisions. In Texmo there is a need for a pragmatic tool to ma

the prediction of financial distress with a single formula with implementation of information system. An

empirical comparison of Bankruptcy models is done to obtain it. This study analyses three of the venerable

models for assessing the distress of industrial corporations. These are the so-called Z-Score model, O-score

model and Zmijewski's model. Z-Scores, O-score and Zmijewski's model are used to predict the

profitability that a firm will go into bankruptcy within two years, forecast corporate defaults and an easy-

to-calculate control measure for the financial distress status of companies in academic studies.

Bankruptcy, models, distress, corporations, control measures.Keywords:

INTRODUCTION measure of the probability of bankruptcy with Traditional

Academics in the fields of accounting and finance havefinancial analysis. The most important conclusion that the

actively studied bankruptcy prediction since the work ofresults of this study point out is that it is possible to predict

Beaver (1966, 1968), Altman (1968), Ohlson (1980) andfinancial distress and bankruptcy more accurately using the

Zmijewski's (1984). With few exceptions, this literature hasdomestic data through the foundation of new models based

relied on accounting-basedmeasuresas the predictor on different combinationsof financial ratios, when

variables. More recent studies have used proxies for thecompared to the old and more prestigious model proposals.

probability of bankruptcy (PB) as an independent variableIt is so interesting and amazing to have produced a new

rather than as the dependent variable. These latter studiesmodel proposal with a slightly better prediction

frequentlyobtain their PB proxies from the existing performance using the binary logistic regression technique

bankruptcy prediction literature, and hence, have relied onagainst the existing model proposals of the past researchers.

accounting-based measures. Many of these studies have usedOur findings show that none of the existing prediction

compositemeasures that statisticallycombineseveral models could achieve a satisfactory level of prediction

different accountingvariables,with Altman's (1968), performance. The correct-classification percentages of the

Zmijewski's(1984) and an derived from Ohlson's (1980)existing models are all below 96 %. None could generate

Model being the most popular, the performance of theseaccuracy level. The best model among the existing financial

accounting-based composite measures in explaining thedistress prediction models is Ohlson's O-Score Model.

cross-sectionalvariation in the actual probability of Surprisingly, Altman's Z-score Model has produced lower

bankruptcy. levels of accuracy.

REVIEW OF LITERATUREThese models utilises multiple corporate income and balance

Edward I. Altman, Ph.D., a financialeconomistandsheet values to measure the financial health of a company.

professor at New York University's Stern School of Business,These models are still being used by practitioners

developed the Z-Score in 1968 says that Z-Score forecaststhroughout the world. The aim of the study is to assess

the probability of a company entering bankruptcy within awhether three popular accounting-based measures, Altman's

12-month period. Altman's model predicted with 95%(1968) , Ohlson's (1980) and Zmijewski's model (1992)

accuracy which sample companies filed bankruptcy withineffectively summarize publicly-available information about

12 months. In later studies, using broader samples ofthe probability of bankruptcy. The study compares the

companies analyzed during a variety of economic climates,relative information content of these to a market-based

FINANCIAL SERVICES & MANAGEMENT RESEARCH

Vol.1 No. 4, April 2012, ISSN 2277 3622

Online Available at indianresearchjournals.com

A COMPARISON OF BANKRUPTCY MODELS

*DR. RADHA GANESH KUMAR, **KISHORE KUMAR,

*Associate Professor, Department of Management Studies, Valliammai Engineering College, Kattankulathur

** Managemnet Trainee, Congruent solutions, Chennai

76

ABSTRACT

Financial analysis can be applied in a wide variety of situations to give business managers

the information they need to make crucial decisions. In Texmo there is a need for a pragmatic tool to ma

the prediction of financial distress with a single formula with implementation of information system. An

empirical comparison of Bankruptcy models is done to obtain it. This study analyses three of the venerable

models for assessing the distress of industrial corporations. These are the so-called Z-Score model, O-score

model and Zmijewski's model. Z-Scores, O-score and Zmijewski's model are used to predict the

profitability that a firm will go into bankruptcy within two years, forecast corporate defaults and an easy-

to-calculate control measure for the financial distress status of companies in academic studies.

Bankruptcy, models, distress, corporations, control measures.Keywords:

INTRODUCTION measure of the probability of bankruptcy with Traditional

Academics in the fields of accounting and finance havefinancial analysis. The most important conclusion that the

actively studied bankruptcy prediction since the work ofresults of this study point out is that it is possible to predict

Beaver (1966, 1968), Altman (1968), Ohlson (1980) andfinancial distress and bankruptcy more accurately using the

Zmijewski's (1984). With few exceptions, this literature hasdomestic data through the foundation of new models based

relied on accounting-basedmeasuresas the predictor on different combinationsof financial ratios, when

variables. More recent studies have used proxies for thecompared to the old and more prestigious model proposals.

probability of bankruptcy (PB) as an independent variableIt is so interesting and amazing to have produced a new

rather than as the dependent variable. These latter studiesmodel proposal with a slightly better prediction

frequentlyobtain their PB proxies from the existing performance using the binary logistic regression technique

bankruptcy prediction literature, and hence, have relied onagainst the existing model proposals of the past researchers.

accounting-based measures. Many of these studies have usedOur findings show that none of the existing prediction

compositemeasures that statisticallycombineseveral models could achieve a satisfactory level of prediction

different accountingvariables,with Altman's (1968), performance. The correct-classification percentages of the

Zmijewski's(1984) and an derived from Ohlson's (1980)existing models are all below 96 %. None could generate

Model being the most popular, the performance of theseaccuracy level. The best model among the existing financial

accounting-based composite measures in explaining thedistress prediction models is Ohlson's O-Score Model.

cross-sectionalvariation in the actual probability of Surprisingly, Altman's Z-score Model has produced lower

bankruptcy. levels of accuracy.

REVIEW OF LITERATUREThese models utilises multiple corporate income and balance

Edward I. Altman, Ph.D., a financialeconomistandsheet values to measure the financial health of a company.

professor at New York University's Stern School of Business,These models are still being used by practitioners

developed the Z-Score in 1968 says that Z-Score forecaststhroughout the world. The aim of the study is to assess

the probability of a company entering bankruptcy within awhether three popular accounting-based measures, Altman's

12-month period. Altman's model predicted with 95%(1968) , Ohlson's (1980) and Zmijewski's model (1992)

accuracy which sample companies filed bankruptcy withineffectively summarize publicly-available information about

12 months. In later studies, using broader samples ofthe probability of bankruptcy. The study compares the

companies analyzed during a variety of economic climates,relative information content of these to a market-based

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the Z-Score accuracy rate remained in the 82% to 85%the traditional valuation model based on discounted future

range. dividends. Ohlson's O-score model is often referred to as the

residual income model since it expresses firm value as a

The model itself is not complicated. It combines fivefunction of the book value of net assets and the present value

financial ratios using reported accounting information andof expected residual earnings on those net assets. Gary Klein

equity values to produce an objective measure of a firm'smen express the application of the Zmijewski's model is

financial health. Altman's Z-Score remains popular afterslightly more complex due to the methodology used to

almost 30 years because it is easy to calculate. Othergenerate the parameters. Zmijewski's model is also known as

bankruptcy prediction models exist, some of which are moreprobit analysis, which is why two steps are required beyond

accurate, especially over a horizon greater than two years.those applied for discriminant analysis-based models such as

However, they are more complex and most are proprietary.the previously presented Altman Model. First, the constant

Bum J Kim says that while the model was developed toand each parameter of the model must be multiplied by

analyse manufacturing companies, it can also be applied to1.8138 and then multiplied by the financial measure. Two

non-manufacturingorganizations by modifying the alternative sets of parameters are provided, either of which

formula. To do so, the first four components of the formulacan be used for estimation weighted measures are based on

(Xl to X4) are used and the fifth component (x5) is omitted.varying proportions of bankrupt and non bankrupt firms.

The adjustedformula seemsto provide equally valid

OBJECTIVES OF THE STUDYpredictive result. Altman, Haldeman and Narayanan (1977)

• To perform a comparison of Bankruptcy models withconstructeda second generationmodel with several

traditional analysis in "Texmo Industries, Coimbatore"enhancementsto the original Z-Score approach.The

• To find out the probability of Bankruptcy throughpurpose of this study was to construct, analyze and test a

Altman Z-score, Ohlson's O-score, and Zmijewski'snew bankruptcyclassificationmodel which considers

model at Texmo Industries for the years 2005-2006explicitly recent developments with respect to business

to2009-2010.failures. The new study also incorporated refinements in the

• To compare the Z-score, O-score, and Zmijewski'sutilization of discriminant statistical techniques. Several

score with traditional financial parameters. To find outreasons for building a new model, despite the availability of

the model that is the best predictor of bankruptcy. Toseveral fairly impressive "old" models, are presented below

forecast the probability of bankruptcy for 2010-2011 toand the empirical results seem to substantiate the effort. The

2013-2014.To estimate correlation between net profitnew model, which we call ZETA, was effective in classifying

and probability of bankruptcy prediction model.bankrupt companies up to five years prior to failure on a

• To give suggestionsto improve the financialsample of corporations consisting of manufacturers and

performance of Texmo Industries.retailers. Since the ZETA model is a proprietary effort, I

cannot fully disclose the parameters of the market.

SCOPE OF THE STUDYKin Lo and Thomas Lys", says, review of the Ohlson's

The study is conducted at Texmo Industries. The duration ofModel suggests that it extends the literature on valuation.

the study was confined to about four months .This study isThe revival of residual income valuation is notable on its

based on the collected data for five years i.e., 2005-2006 toown. Added to that, the parsimoniousinformation

2009-2010.The major scope of the study are:dynamics translates expectations of the future to current

• To provide information about the financial position,observables. While the model's core has been known for

performance and changes in financial position of Texmomany decades, the OM is built upon the more solid

Industries that is useful to a wide range of users infoundation of Modigliani and Miller. Finally, the model is

making economic decision.elegant and lends itself to extensions that analyze accounting

• The study will help the company to understand whatissues such as conservatism and growth, as demonstrated by

sort of changes they should make in future.Feltham and Ohlson (1995).

• All the factors are studied based on the past data leavingOhlson (1995) and Feltham and Ohlson (1995)

scope for further research in the field which coulddemonstrate that equation is mathematically equivalent to

DR. RADHA GANESH KUMAR, KISHORE KUMAR

77

range. dividends. Ohlson's O-score model is often referred to as the

residual income model since it expresses firm value as a

The model itself is not complicated. It combines fivefunction of the book value of net assets and the present value

financial ratios using reported accounting information andof expected residual earnings on those net assets. Gary Klein

equity values to produce an objective measure of a firm'smen express the application of the Zmijewski's model is

financial health. Altman's Z-Score remains popular afterslightly more complex due to the methodology used to

almost 30 years because it is easy to calculate. Othergenerate the parameters. Zmijewski's model is also known as

bankruptcy prediction models exist, some of which are moreprobit analysis, which is why two steps are required beyond

accurate, especially over a horizon greater than two years.those applied for discriminant analysis-based models such as

However, they are more complex and most are proprietary.the previously presented Altman Model. First, the constant

Bum J Kim says that while the model was developed toand each parameter of the model must be multiplied by

analyse manufacturing companies, it can also be applied to1.8138 and then multiplied by the financial measure. Two

non-manufacturingorganizations by modifying the alternative sets of parameters are provided, either of which

formula. To do so, the first four components of the formulacan be used for estimation weighted measures are based on

(Xl to X4) are used and the fifth component (x5) is omitted.varying proportions of bankrupt and non bankrupt firms.

The adjustedformula seemsto provide equally valid

OBJECTIVES OF THE STUDYpredictive result. Altman, Haldeman and Narayanan (1977)

• To perform a comparison of Bankruptcy models withconstructeda second generationmodel with several

traditional analysis in "Texmo Industries, Coimbatore"enhancementsto the original Z-Score approach.The

• To find out the probability of Bankruptcy throughpurpose of this study was to construct, analyze and test a

Altman Z-score, Ohlson's O-score, and Zmijewski'snew bankruptcyclassificationmodel which considers

model at Texmo Industries for the years 2005-2006explicitly recent developments with respect to business

to2009-2010.failures. The new study also incorporated refinements in the

• To compare the Z-score, O-score, and Zmijewski'sutilization of discriminant statistical techniques. Several

score with traditional financial parameters. To find outreasons for building a new model, despite the availability of

the model that is the best predictor of bankruptcy. Toseveral fairly impressive "old" models, are presented below

forecast the probability of bankruptcy for 2010-2011 toand the empirical results seem to substantiate the effort. The

2013-2014.To estimate correlation between net profitnew model, which we call ZETA, was effective in classifying

and probability of bankruptcy prediction model.bankrupt companies up to five years prior to failure on a

• To give suggestionsto improve the financialsample of corporations consisting of manufacturers and

performance of Texmo Industries.retailers. Since the ZETA model is a proprietary effort, I

cannot fully disclose the parameters of the market.

SCOPE OF THE STUDYKin Lo and Thomas Lys", says, review of the Ohlson's

The study is conducted at Texmo Industries. The duration ofModel suggests that it extends the literature on valuation.

the study was confined to about four months .This study isThe revival of residual income valuation is notable on its

based on the collected data for five years i.e., 2005-2006 toown. Added to that, the parsimoniousinformation

2009-2010.The major scope of the study are:dynamics translates expectations of the future to current

• To provide information about the financial position,observables. While the model's core has been known for

performance and changes in financial position of Texmomany decades, the OM is built upon the more solid

Industries that is useful to a wide range of users infoundation of Modigliani and Miller. Finally, the model is

making economic decision.elegant and lends itself to extensions that analyze accounting

• The study will help the company to understand whatissues such as conservatism and growth, as demonstrated by

sort of changes they should make in future.Feltham and Ohlson (1995).

• All the factors are studied based on the past data leavingOhlson (1995) and Feltham and Ohlson (1995)

scope for further research in the field which coulddemonstrate that equation is mathematically equivalent to

DR. RADHA GANESH KUMAR, KISHORE KUMAR

77

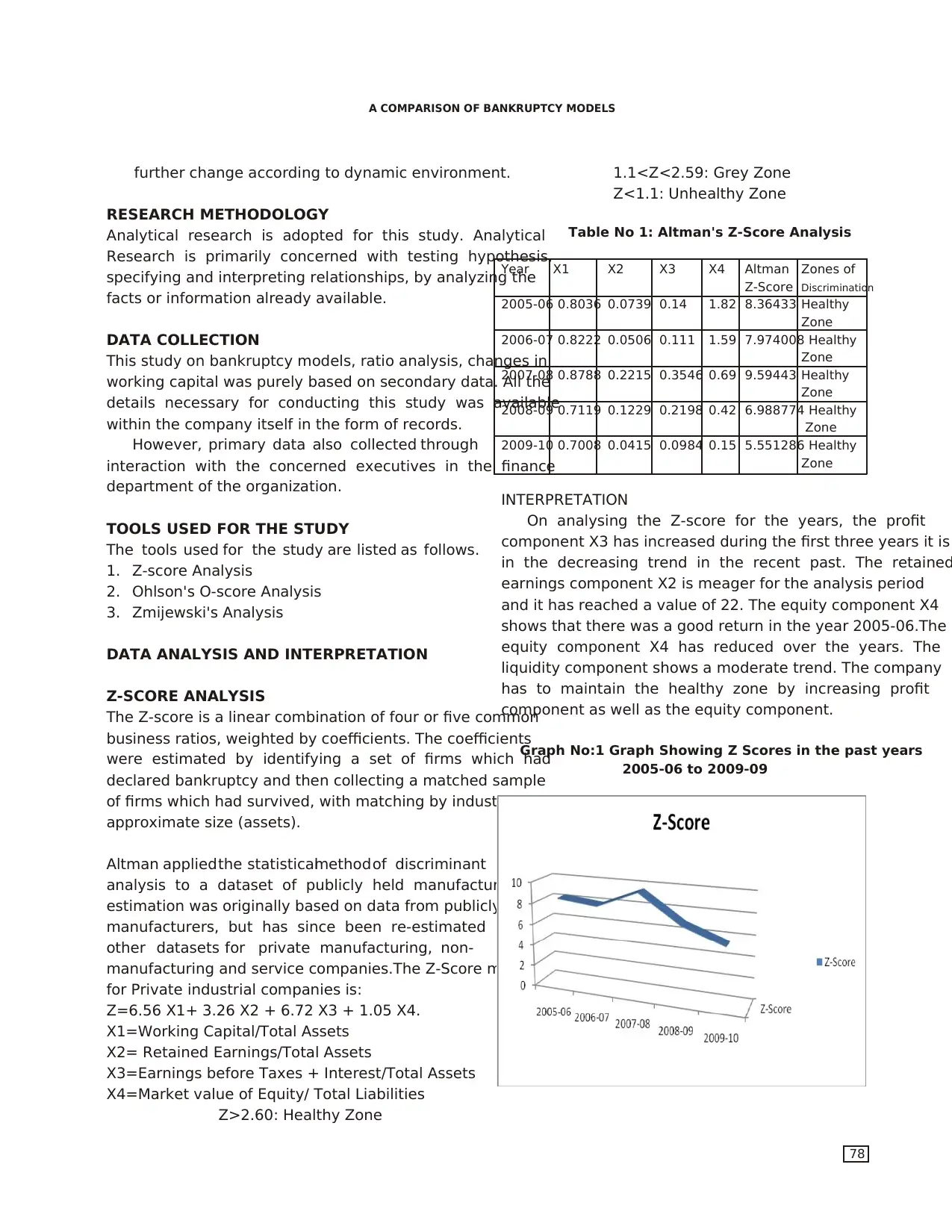

further change according to dynamic environment. 1.1<Z<2.59: Grey Zone

Z<1.1: Unhealthy Zone

RESEARCH METHODOLOGY

Table No 1: Altman's Z-Score AnalysisAnalytical research is adopted for this study. Analytical

Research is primarily concerned with testing hypothesis,

Year X1 X2 X3 X4 Altman Zones of

specifying and interpreting relationships, by analyzing the Z-Score Discrimination

facts or information already available. 2005-06 0.8036 0.0739 0.14 1.82 8.36433 Healthy

Zone

2006-07 0.8222 0.0506 0.111 1.59 7.974008 HealthyDATA COLLECTION

ZoneThis study on bankruptcy models, ratio analysis, changes in

2007-08 0.8788 0.2215 0.3546 0.69 9.59443 Healthy

working capital was purely based on secondary data. All the Zone

details necessary for conducting this study was available2008-09 0.7119 0.1229 0.2198 0.42 6.988774 Healthy

within the company itself in the form of records. Zone

However, primary data also collected through 2009-10 0.7008 0.0415 0.0984 0.15 5.551286 Healthy

Zoneinteraction with the concerned executives in the finance

department of the organization. INTERPRETATION

On analysing the Z-score for the years, the profit

TOOLS USED FOR THE STUDY component X3 has increased during the first three years it is

The tools used for the study are listed as follows. in the decreasing trend in the recent past. The retained

1. Z-score Analysis earnings component X2 is meager for the analysis period

2. Ohlson's O-score Analysis and it has reached a value of 22. The equity component X4

3. Zmijewski's Analysis shows that there was a good return in the year 2005-06.The

equity component X4 has reduced over the years. The

DATA ANALYSIS AND INTERPRETATION liquidity component shows a moderate trend. The company

has to maintain the healthy zone by increasing profit

Z-SCORE ANALYSIS component as well as the equity component.

The Z-score is a linear combination of four or five common

business ratios, weighted by coefficients. The coefficients

Graph No:1 Graph Showing Z Scores in the past years

were estimated by identifying a set of firms which had 2005-06 to 2009-09

declared bankruptcy and then collecting a matched sample

of firms which had survived, with matching by industry and

approximate size (assets).

Altman applied the statisticalmethod of discriminant

analysis to a dataset of publicly held manufacturers. The

estimation was originally based on data from publicly held

manufacturers, but has since been re-estimated based on

other datasets for private manufacturing, non-

manufacturing and service companies.The Z-Score model

for Private industrial companies is:

Z=6.56 X1+ 3.26 X2 + 6.72 X3 + 1.05 X4.

X1=Working Capital/Total Assets

X2= Retained Earnings/Total Assets

X3=Earnings before Taxes + Interest/Total Assets

X4=Market value of Equity/ Total Liabilities

Z>2.60: Healthy Zone

A COMPARISON OF BANKRUPTCY MODELS

78

Z<1.1: Unhealthy Zone

RESEARCH METHODOLOGY

Table No 1: Altman's Z-Score AnalysisAnalytical research is adopted for this study. Analytical

Research is primarily concerned with testing hypothesis,

Year X1 X2 X3 X4 Altman Zones of

specifying and interpreting relationships, by analyzing the Z-Score Discrimination

facts or information already available. 2005-06 0.8036 0.0739 0.14 1.82 8.36433 Healthy

Zone

2006-07 0.8222 0.0506 0.111 1.59 7.974008 HealthyDATA COLLECTION

ZoneThis study on bankruptcy models, ratio analysis, changes in

2007-08 0.8788 0.2215 0.3546 0.69 9.59443 Healthy

working capital was purely based on secondary data. All the Zone

details necessary for conducting this study was available2008-09 0.7119 0.1229 0.2198 0.42 6.988774 Healthy

within the company itself in the form of records. Zone

However, primary data also collected through 2009-10 0.7008 0.0415 0.0984 0.15 5.551286 Healthy

Zoneinteraction with the concerned executives in the finance

department of the organization. INTERPRETATION

On analysing the Z-score for the years, the profit

TOOLS USED FOR THE STUDY component X3 has increased during the first three years it is

The tools used for the study are listed as follows. in the decreasing trend in the recent past. The retained

1. Z-score Analysis earnings component X2 is meager for the analysis period

2. Ohlson's O-score Analysis and it has reached a value of 22. The equity component X4

3. Zmijewski's Analysis shows that there was a good return in the year 2005-06.The

equity component X4 has reduced over the years. The

DATA ANALYSIS AND INTERPRETATION liquidity component shows a moderate trend. The company

has to maintain the healthy zone by increasing profit

Z-SCORE ANALYSIS component as well as the equity component.

The Z-score is a linear combination of four or five common

business ratios, weighted by coefficients. The coefficients

Graph No:1 Graph Showing Z Scores in the past years

were estimated by identifying a set of firms which had 2005-06 to 2009-09

declared bankruptcy and then collecting a matched sample

of firms which had survived, with matching by industry and

approximate size (assets).

Altman applied the statisticalmethod of discriminant

analysis to a dataset of publicly held manufacturers. The

estimation was originally based on data from publicly held

manufacturers, but has since been re-estimated based on

other datasets for private manufacturing, non-

manufacturing and service companies.The Z-Score model

for Private industrial companies is:

Z=6.56 X1+ 3.26 X2 + 6.72 X3 + 1.05 X4.

X1=Working Capital/Total Assets

X2= Retained Earnings/Total Assets

X3=Earnings before Taxes + Interest/Total Assets

X4=Market value of Equity/ Total Liabilities

Z>2.60: Healthy Zone

A COMPARISON OF BANKRUPTCY MODELS

78

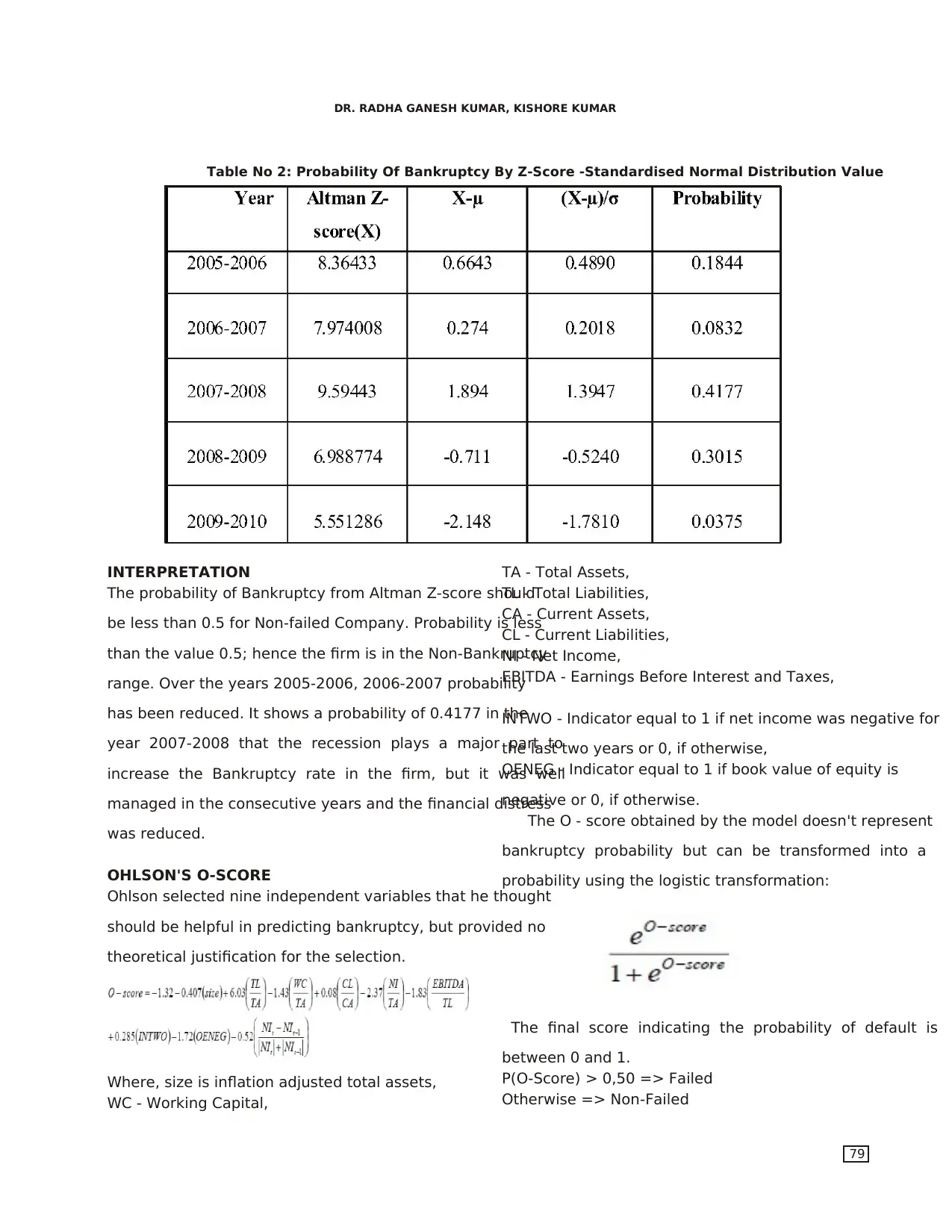

INTERPRETATION TA - Total Assets,

The probability of Bankruptcy from Altman Z-score shouldTL - Total Liabilities,

CA - Current Assets,

be less than 0.5 for Non-failed Company. Probability is less

CL - Current Liabilities,

than the value 0.5; hence the firm is in the Non-BankruptcyNI - Net Income,

EBITDA - Earnings Before Interest and Taxes,range. Over the years 2005-2006, 2006-2007 probability

has been reduced. It shows a probability of 0.4177 in theINTWO - Indicator equal to 1 if net income was negative for

year 2007-2008 that the recession plays a major part tothe last two years or 0, if otherwise,

OENEG - Indicator equal to 1 if book value of equity isincrease the Bankruptcy rate in the firm, but it was well

negative or 0, if otherwise.managed in the consecutive years and the financial distress

The O - score obtained by the model doesn't represent

was reduced.

bankruptcy probability but can be transformed into a

OHLSON'S O-SCORE probability using the logistic transformation:

Ohlson selected nine independent variables that he thought

should be helpful in predicting bankruptcy, but provided no

theoretical justification for the selection.

The final score indicating the probability of default is

between 0 and 1.

P(O-Score) > 0,50 => FailedWhere, size is inflation adjusted total assets,

Otherwise => Non-FailedWC - Working Capital,

Table No 2: Probability Of Bankruptcy By Z-Score -Standardised Normal Distribution Value

DR. RADHA GANESH KUMAR, KISHORE KUMAR

79

The probability of Bankruptcy from Altman Z-score shouldTL - Total Liabilities,

CA - Current Assets,

be less than 0.5 for Non-failed Company. Probability is less

CL - Current Liabilities,

than the value 0.5; hence the firm is in the Non-BankruptcyNI - Net Income,

EBITDA - Earnings Before Interest and Taxes,range. Over the years 2005-2006, 2006-2007 probability

has been reduced. It shows a probability of 0.4177 in theINTWO - Indicator equal to 1 if net income was negative for

year 2007-2008 that the recession plays a major part tothe last two years or 0, if otherwise,

OENEG - Indicator equal to 1 if book value of equity isincrease the Bankruptcy rate in the firm, but it was well

negative or 0, if otherwise.managed in the consecutive years and the financial distress

The O - score obtained by the model doesn't represent

was reduced.

bankruptcy probability but can be transformed into a

OHLSON'S O-SCORE probability using the logistic transformation:

Ohlson selected nine independent variables that he thought

should be helpful in predicting bankruptcy, but provided no

theoretical justification for the selection.

The final score indicating the probability of default is

between 0 and 1.

P(O-Score) > 0,50 => FailedWhere, size is inflation adjusted total assets,

Otherwise => Non-FailedWC - Working Capital,

Table No 2: Probability Of Bankruptcy By Z-Score -Standardised Normal Distribution Value

DR. RADHA GANESH KUMAR, KISHORE KUMAR

79

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

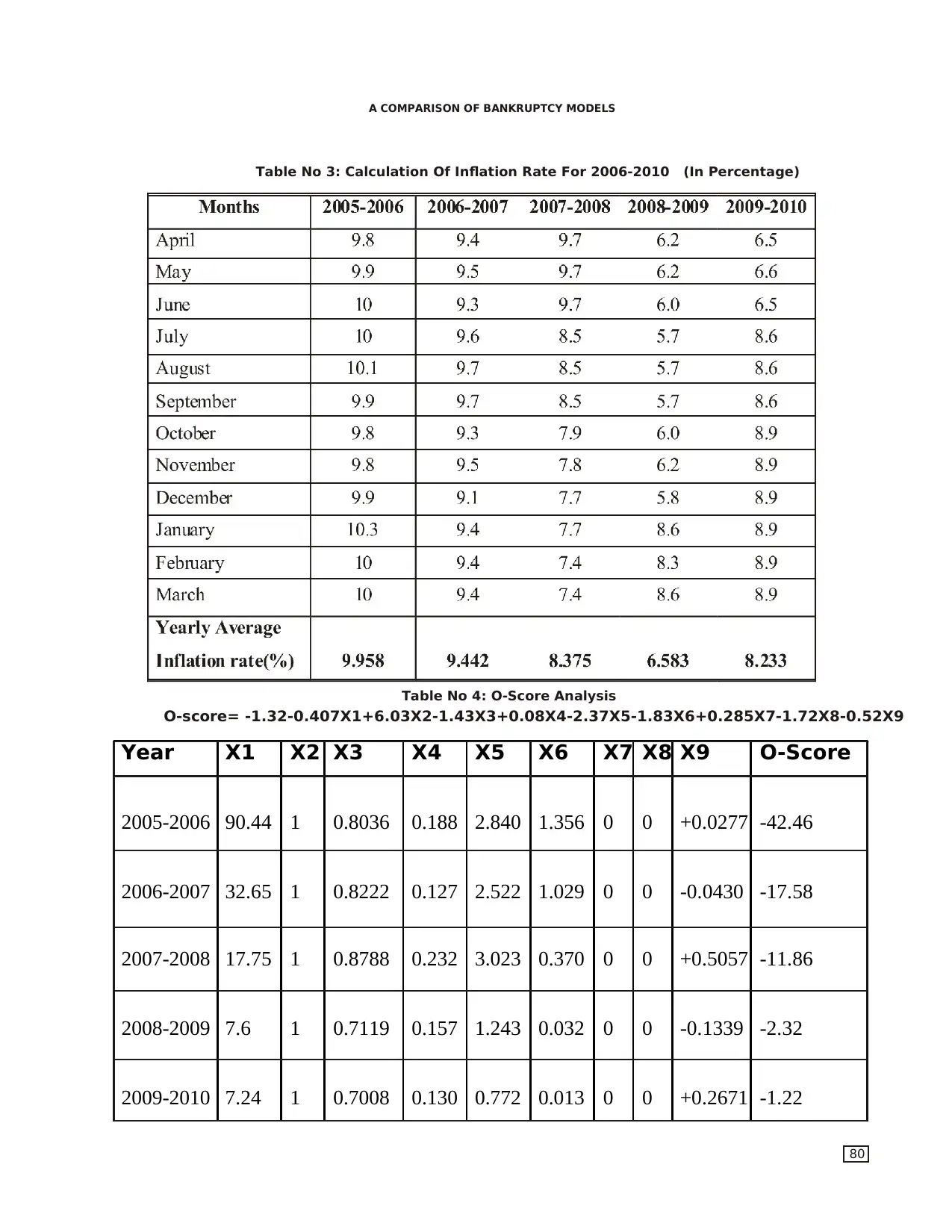

Table No 3: Calculation Of Inflation Rate For 2006-2010 (In Percentage)

Table No 4: O-Score Analysis

O-score= -1.32-0.407X1+6.03X2-1.43X3+0.08X4-2.37X5-1.83X6+0.285X7-1.72X8-0.52X9

Year X1 X2 X3 X4 X5 X6 X7 X8 X9 O-Score

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

90.44

32.65

17.75

7.6

7.24

1

1

1

1

1

0.8036

0.8222

0.8788

0.7119

0.7008

0.188

0.127

0.232

0.157

0.130

2.840

2.522

3.023

1.243

0.772

1.356

1.029

0.370

0.032

0.013

0

0

0

0

0

0

0

0

0

0

+0.0277

-0.0430

+0.5057

-0.1339

+0.2671

-42.46

-17.58

-11.86

-2.32

-1.22

A COMPARISON OF BANKRUPTCY MODELS

80

Table No 4: O-Score Analysis

O-score= -1.32-0.407X1+6.03X2-1.43X3+0.08X4-2.37X5-1.83X6+0.285X7-1.72X8-0.52X9

Year X1 X2 X3 X4 X5 X6 X7 X8 X9 O-Score

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

90.44

32.65

17.75

7.6

7.24

1

1

1

1

1

0.8036

0.8222

0.8788

0.7119

0.7008

0.188

0.127

0.232

0.157

0.130

2.840

2.522

3.023

1.243

0.772

1.356

1.029

0.370

0.032

0.013

0

0

0

0

0

0

0

0

0

0

+0.0277

-0.0430

+0.5057

-0.1339

+0.2671

-42.46

-17.58

-11.86

-2.32

-1.22

A COMPARISON OF BANKRUPTCY MODELS

80

INTERPRETATION the year 2005-2006 indicates that there is no probability of

The O-score has been - 42.46. A big negative O-score inbankruptcy. However the score has declined over the years.

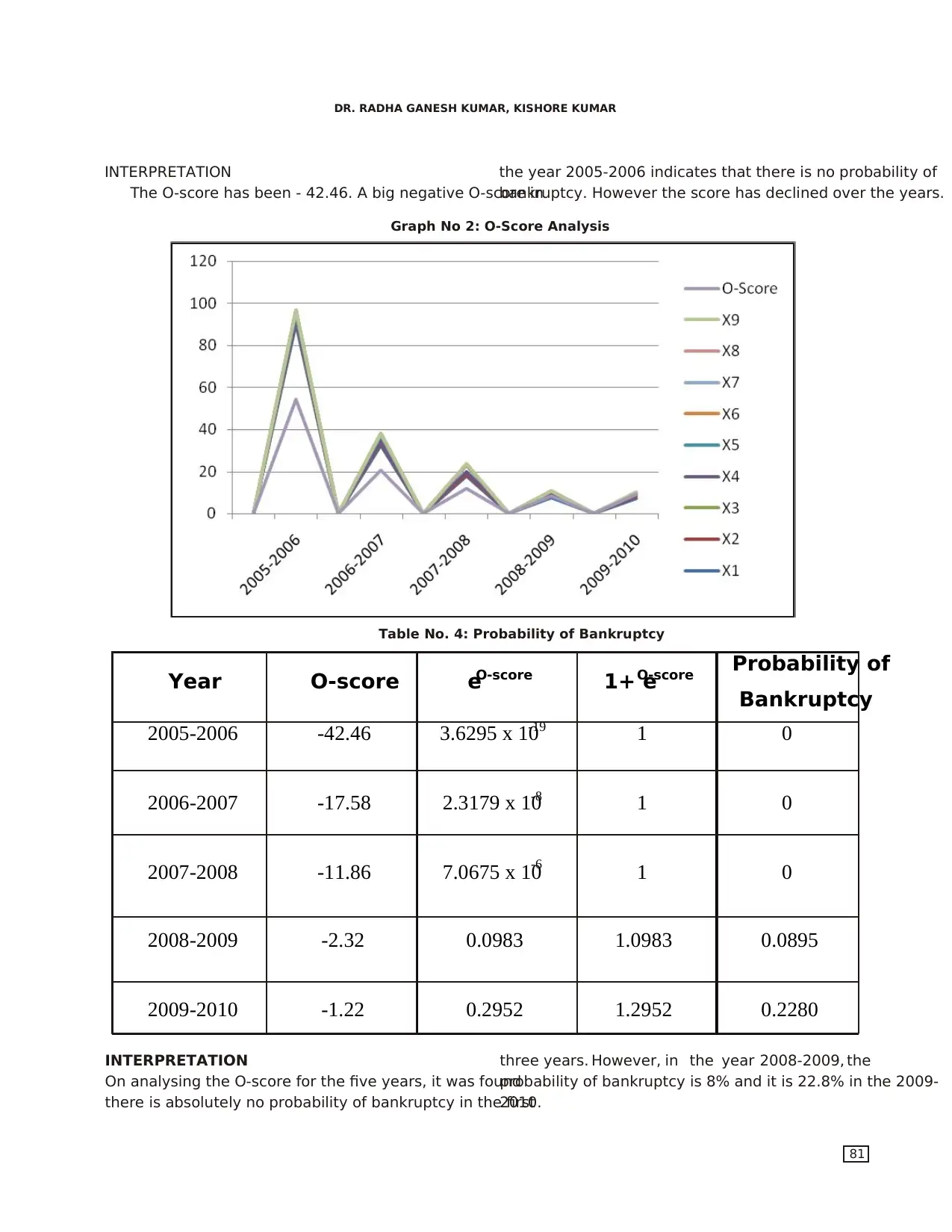

Graph No 2: O-Score Analysis

Year O-score eO-score 1+ eO-score Probability of

Bankruptcy

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

-42.46

-17.58

-11.86

-2.32

-1.22

3.6295 x 10-19

2.3179 x 10-8

7.0675 x 10

-6

0.0983

0.2952

1

1

1

1.0983

1.2952

0

0

0

0.0895

0.2280

Table No. 4: Probability of Bankruptcy

INTERPRETATION three years. However, in the year 2008-2009, the

On analysing the O-score for the five years, it was foundprobability of bankruptcy is 8% and it is 22.8% in the 2009-

there is absolutely no probability of bankruptcy in the first2010.

DR. RADHA GANESH KUMAR, KISHORE KUMAR

81

The O-score has been - 42.46. A big negative O-score inbankruptcy. However the score has declined over the years.

Graph No 2: O-Score Analysis

Year O-score eO-score 1+ eO-score Probability of

Bankruptcy

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

-42.46

-17.58

-11.86

-2.32

-1.22

3.6295 x 10-19

2.3179 x 10-8

7.0675 x 10

-6

0.0983

0.2952

1

1

1

1.0983

1.2952

0

0

0

0.0895

0.2280

Table No. 4: Probability of Bankruptcy

INTERPRETATION three years. However, in the year 2008-2009, the

On analysing the O-score for the five years, it was foundprobability of bankruptcy is 8% and it is 22.8% in the 2009-

there is absolutely no probability of bankruptcy in the first2010.

DR. RADHA GANESH KUMAR, KISHORE KUMAR

81

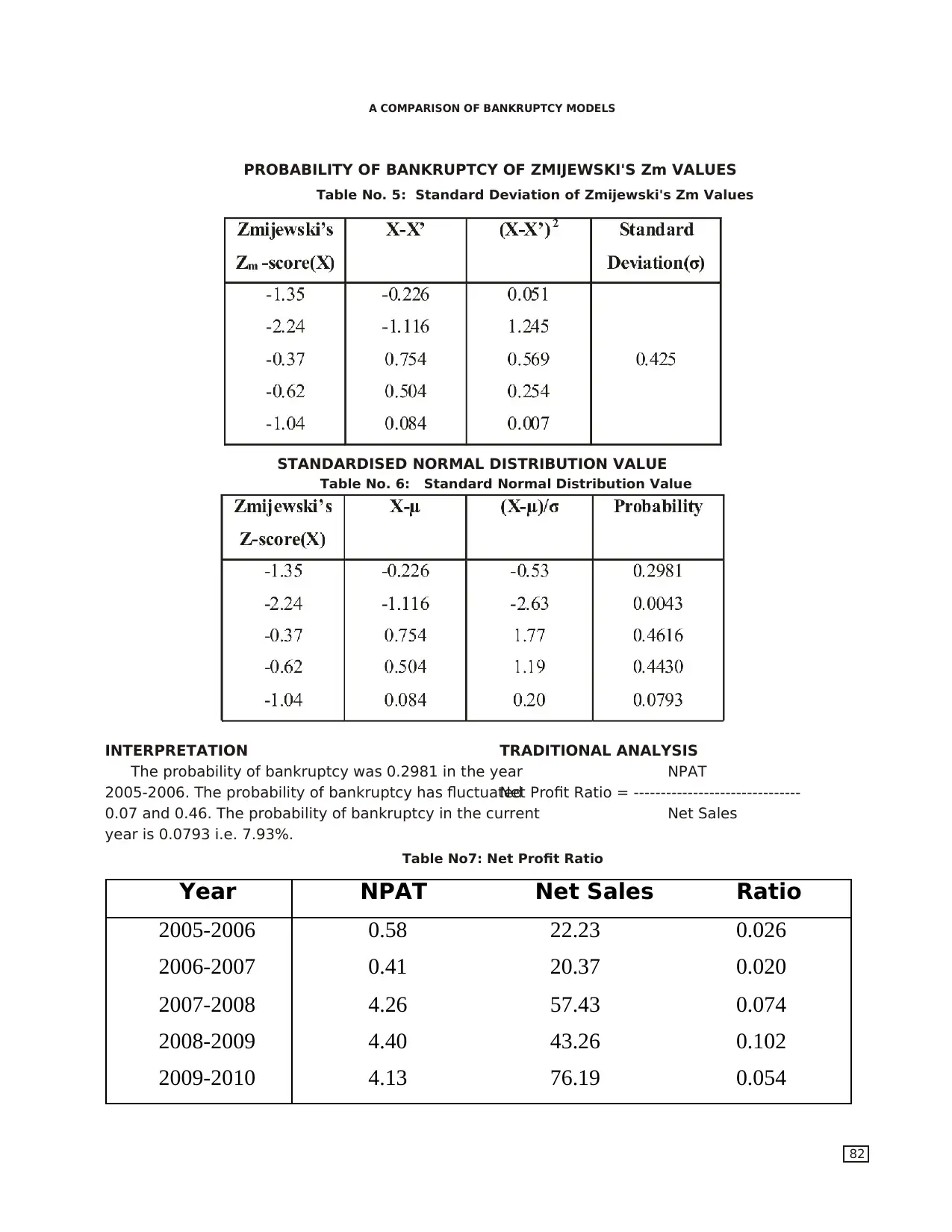

INTERPRETATION TRADITIONAL ANALYSIS

The probability of bankruptcy was 0.2981 in the year NPAT

2005-2006. The probability of bankruptcy has fluctuatedNet Profit Ratio = -------------------------------

0.07 and 0.46. The probability of bankruptcy in the current Net Sales

year is 0.0793 i.e. 7.93%.

PROBABILITY OF BANKRUPTCY OF ZMIJEWSKI'S Zm VALUES

Table No. 5: Standard Deviation of Zmijewski's Zm Values

STANDARDISED NORMAL DISTRIBUTION VALUE

Table No. 6: Standard Normal Distribution Value

Year NPAT Net Sales Ratio

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

0.58

0.41

4.26

4.40

4.13

22.23

20.37

57.43

43.26

76.19

0.026

0.020

0.074

0.102

0.054

Table No7: Net Profit Ratio

A COMPARISON OF BANKRUPTCY MODELS

82

The probability of bankruptcy was 0.2981 in the year NPAT

2005-2006. The probability of bankruptcy has fluctuatedNet Profit Ratio = -------------------------------

0.07 and 0.46. The probability of bankruptcy in the current Net Sales

year is 0.0793 i.e. 7.93%.

PROBABILITY OF BANKRUPTCY OF ZMIJEWSKI'S Zm VALUES

Table No. 5: Standard Deviation of Zmijewski's Zm Values

STANDARDISED NORMAL DISTRIBUTION VALUE

Table No. 6: Standard Normal Distribution Value

Year NPAT Net Sales Ratio

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

0.58

0.41

4.26

4.40

4.13

22.23

20.37

57.43

43.26

76.19

0.026

0.020

0.074

0.102

0.054

Table No7: Net Profit Ratio

A COMPARISON OF BANKRUPTCY MODELS

82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

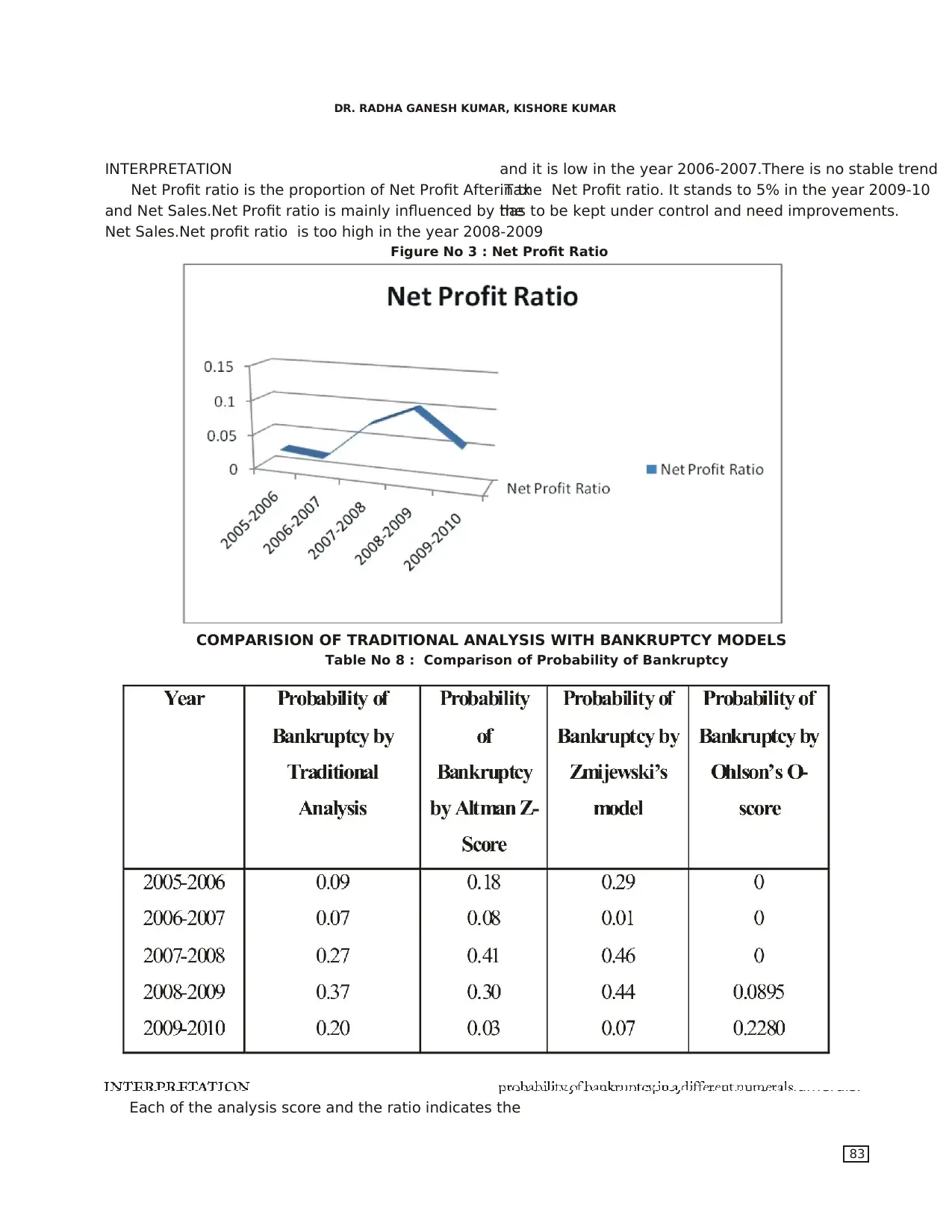

INTERPRETATION and it is low in the year 2006-2007.There is no stable trend

Net Profit ratio is the proportion of Net Profit After Taxin the Net Profit ratio. It stands to 5% in the year 2009-10

and Net Sales.Net Profit ratio is mainly influenced by thehas to be kept under control and need improvements.

Net Sales.Net profit ratio is too high in the year 2008-2009

INTERPRETATION probability of bankruptcy in a different numerals.

Each of the analysis score and the ratio indicates the

Figure No 3 : Net Profit Ratio

COMPARISION OF TRADITIONAL ANALYSIS WITH BANKRUPTCY MODELS

Table No 8 : Comparison of Probability of Bankruptcy

DR. RADHA GANESH KUMAR, KISHORE KUMAR

83

Net Profit ratio is the proportion of Net Profit After Taxin the Net Profit ratio. It stands to 5% in the year 2009-10

and Net Sales.Net Profit ratio is mainly influenced by thehas to be kept under control and need improvements.

Net Sales.Net profit ratio is too high in the year 2008-2009

INTERPRETATION probability of bankruptcy in a different numerals.

Each of the analysis score and the ratio indicates the

Figure No 3 : Net Profit Ratio

COMPARISION OF TRADITIONAL ANALYSIS WITH BANKRUPTCY MODELS

Table No 8 : Comparison of Probability of Bankruptcy

DR. RADHA GANESH KUMAR, KISHORE KUMAR

83

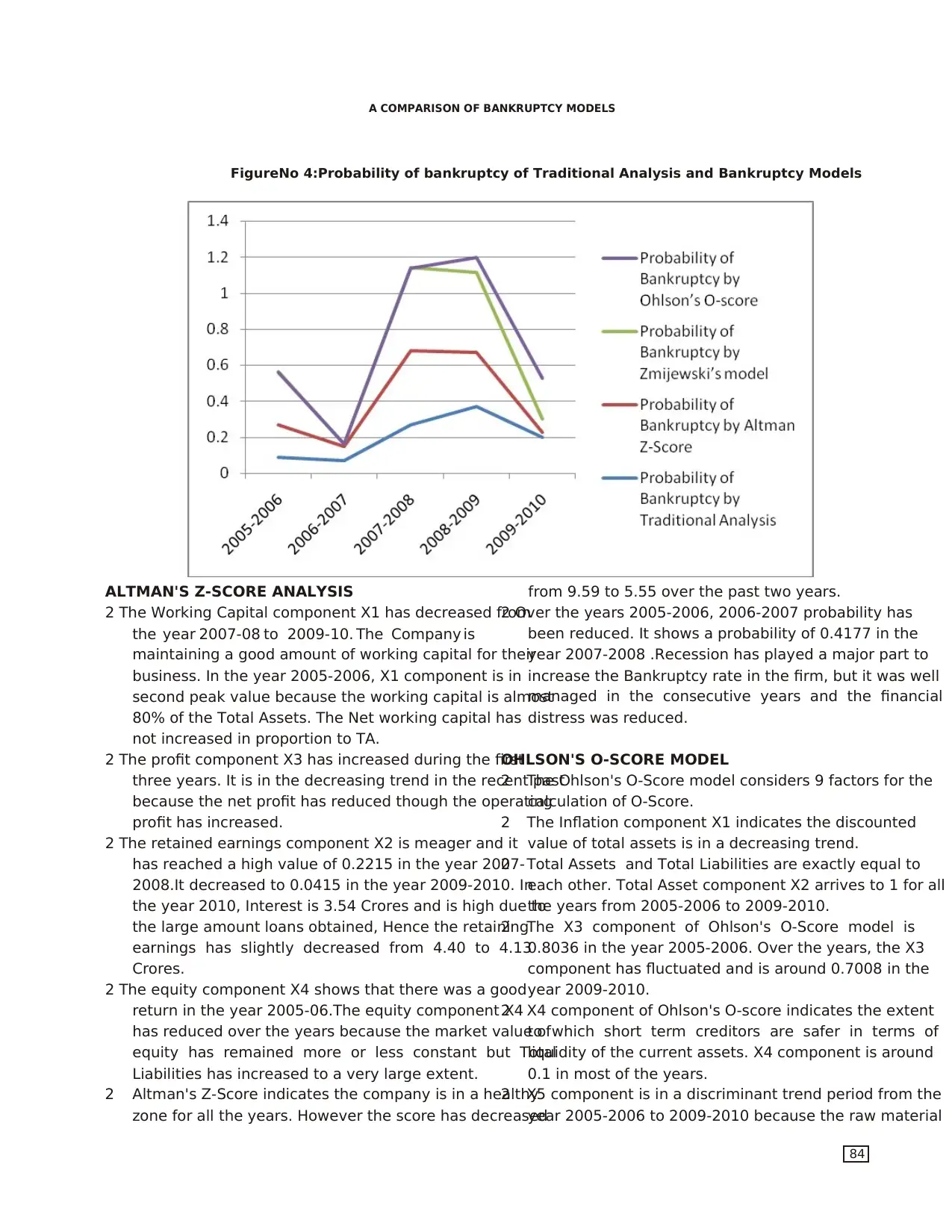

ALTMAN'S Z-SCORE ANALYSIS from 9.59 to 5.55 over the past two years.

2 The Working Capital component X1 has decreased from2 Over the years 2005-2006, 2006-2007 probability has

the year 2007-08 to 2009-10. The Company is been reduced. It shows a probability of 0.4177 in the

maintaining a good amount of working capital for theiryear 2007-2008 .Recession has played a major part to

business. In the year 2005-2006, X1 component is in increase the Bankruptcy rate in the firm, but it was well

second peak value because the working capital is almostmanaged in the consecutive years and the financial

80% of the Total Assets. The Net working capital has distress was reduced.

not increased in proportion to TA.

2 The profit component X3 has increased during the firstOHLSON'S O-SCORE MODEL

The Ohlson's O-Score model considers 9 factors for thethree years. It is in the decreasing trend in the recent past2

calculation of O-Score.because the net profit has reduced though the operating

The Inflation component X1 indicates the discountedprofit has increased. 2

value of total assets is in a decreasing trend.2 The retained earnings component X2 is meager and it

Total Assets and Total Liabilities are exactly equal tohas reached a high value of 0.2215 in the year 2007-2

each other. Total Asset component X2 arrives to 1 for all2008.It decreased to 0.0415 in the year 2009-2010. In

the years from 2005-2006 to 2009-2010.the year 2010, Interest is 3.54 Crores and is high due to

The X3 component of Ohlson's O-Score model isthe large amount loans obtained, Hence the retaining2

0.8036 in the year 2005-2006. Over the years, the X3earnings has slightly decreased from 4.40 to 4.13

component has fluctuated and is around 0.7008 in theCrores.

year 2009-2010.2 The equity component X4 shows that there was a good

X4 component of Ohlson's O-score indicates the extentreturn in the year 2005-06.The equity component X42

to which short term creditors are safer in terms ofhas reduced over the years because the market value of

liquidity of the current assets. X4 component is aroundequity has remained more or less constant but Total

0.1 in most of the years.Liabilities has increased to a very large extent.

X5 component is in a discriminant trend period from theAltman's Z-Score indicates the company is in a healthy22

year 2005-2006 to 2009-2010 because the raw materialzone for all the years. However the score has decreased

FigureNo 4:Probability of bankruptcy of Traditional Analysis and Bankruptcy Models

A COMPARISON OF BANKRUPTCY MODELS

84

2 The Working Capital component X1 has decreased from2 Over the years 2005-2006, 2006-2007 probability has

the year 2007-08 to 2009-10. The Company is been reduced. It shows a probability of 0.4177 in the

maintaining a good amount of working capital for theiryear 2007-2008 .Recession has played a major part to

business. In the year 2005-2006, X1 component is in increase the Bankruptcy rate in the firm, but it was well

second peak value because the working capital is almostmanaged in the consecutive years and the financial

80% of the Total Assets. The Net working capital has distress was reduced.

not increased in proportion to TA.

2 The profit component X3 has increased during the firstOHLSON'S O-SCORE MODEL

The Ohlson's O-Score model considers 9 factors for thethree years. It is in the decreasing trend in the recent past2

calculation of O-Score.because the net profit has reduced though the operating

The Inflation component X1 indicates the discountedprofit has increased. 2

value of total assets is in a decreasing trend.2 The retained earnings component X2 is meager and it

Total Assets and Total Liabilities are exactly equal tohas reached a high value of 0.2215 in the year 2007-2

each other. Total Asset component X2 arrives to 1 for all2008.It decreased to 0.0415 in the year 2009-2010. In

the years from 2005-2006 to 2009-2010.the year 2010, Interest is 3.54 Crores and is high due to

The X3 component of Ohlson's O-Score model isthe large amount loans obtained, Hence the retaining2

0.8036 in the year 2005-2006. Over the years, the X3earnings has slightly decreased from 4.40 to 4.13

component has fluctuated and is around 0.7008 in theCrores.

year 2009-2010.2 The equity component X4 shows that there was a good

X4 component of Ohlson's O-score indicates the extentreturn in the year 2005-06.The equity component X42

to which short term creditors are safer in terms ofhas reduced over the years because the market value of

liquidity of the current assets. X4 component is aroundequity has remained more or less constant but Total

0.1 in most of the years.Liabilities has increased to a very large extent.

X5 component is in a discriminant trend period from theAltman's Z-Score indicates the company is in a healthy22

year 2005-2006 to 2009-2010 because the raw materialzone for all the years. However the score has decreased

FigureNo 4:Probability of bankruptcy of Traditional Analysis and Bankruptcy Models

A COMPARISON OF BANKRUPTCY MODELS

84

consumptionis high.X5 component has ranged predict bankruptcy, O-Score uses nine components for

between 3.023 and 0.772 and has much impact to thepredictionof bankruptcywhich includesinflation

value of O-Score. adjusted Total assets, short term and long term liquidity,

2 X6 component has declined over the years. It has profit before tax and after tax in the current year as well

reduced from 1.356 to 0.013 due to high operatingas previous year and market value.

expenses. 2 An attempt is made to reduce the X1 component and is

2 X7 and X8 component is 0 for all the years because thewell appreciated.

Net profit and the market value of the firm is positive.2 X3 Component has been reduced and the NWC has

2 X9 component of O-Score model is positive in three outincreased less proportionately than increase in Total

of 5 years because the income of the current period hasAssets.

been greater than the income of the previous period.2 X5, X6 and X9 component must be improved by

2 The O-score has been -42.46 , a big negative O-score inincreasing the net profit. Net Profit can be reduced by

the year 2005-2006 indicates that there is no probabilityreducing the raw material consumption, administration

of bankruptcy. However the score has declined over theand selling expenses. Interest expenses must be reduced

years. to enhance the profit of the firm.

2 It was found there is absolutely no probability of2 Current Assets must be reduced. Steps might be taken to

bankruptcy in the first three years. However, in the yearreduce the Inventory.

2008-2009, the probability of bankruptcy is 8% and it is2 Loans and advances must be collected speedily since it

22.8% in the 2009-2010. forms a great portion of Current Asset leading to very

high Current ratio.

ZMIJEWSKI'S MODEL 2 Cash balance may be reduced .Cash may be diverted to

2 X1 component of Zmijewski's was initially 0.5267 in theshort term investments.

year 2005-2006.It increased to 0.54 in the year 2006-

2007.Later, there has been a deep decline and X1CONCLUSION

component is currently 0.0006 because NPAT hasThe most important conclusion is that it is possible to

declined in the past two years. ¢ Zm Score is negative inpredict financial distress and bankruptcy more accurately

all years indicating that the firm has not failed. using the domestic data through new models based on

2 The probability of bankruptcy was 0.2981 in the yeardifferent combinations of financial ratios, when compared to

2005-2006. The probability of bankruptcy has the old and more prestigious model proposals. O-Score

fluctuated 0.07 and 0.46. The probability of bankruptcymodel is a proposalwith a slightly better prediction

in the current year is 0.0793 i.e. 7.93%. performance since it uses the binary logistic regression

technique against the existing model proposals of the past

SUGGESTIONS: researchers.Findings show that none of the existing

2 O-score is the best model for the predictionof prediction models could achieve a satisfactory level of

bankruptcy on two reasons: prediction performance.

4 The correlation between the Z-Score and the net profit The best model among the existing financial distress

is 0.72; Zmijewski's model and the net profit is 0.48; O-prediction models is Ohlson's O-Score Model. Surprisingly,

Score and the net profit is 0.95.The Correlation betweenAltman's Z-score Model has produced lower levels of

the bankruptcyprediction models and traditional correlation with traditional analysis while O-Score analysis

analysis ranges from 0.48 to 0.95. There is very highhas a very high positive correlation with traditional analysis.

positive correlation between Ohlson's O-score modelTexmo Industries should use O-Score model for prediction

and traditional analysis and the value is 0.95.Texmoof bankruptcy. The probability of bankruptcy is increased

Industries may use Ohlson's O-score model for theover the years and hence steps must be taken to improve the

prediction of bankruptcy. profit. The company that predicts the future and works

4 Z score model is based on four components whileperfectly in the present shall win at any time .

Zmijewski's model is based on three components to

DR. RADHA GANESH KUMAR, KISHORE KUMAR

85

between 3.023 and 0.772 and has much impact to thepredictionof bankruptcywhich includesinflation

value of O-Score. adjusted Total assets, short term and long term liquidity,

2 X6 component has declined over the years. It has profit before tax and after tax in the current year as well

reduced from 1.356 to 0.013 due to high operatingas previous year and market value.

expenses. 2 An attempt is made to reduce the X1 component and is

2 X7 and X8 component is 0 for all the years because thewell appreciated.

Net profit and the market value of the firm is positive.2 X3 Component has been reduced and the NWC has

2 X9 component of O-Score model is positive in three outincreased less proportionately than increase in Total

of 5 years because the income of the current period hasAssets.

been greater than the income of the previous period.2 X5, X6 and X9 component must be improved by

2 The O-score has been -42.46 , a big negative O-score inincreasing the net profit. Net Profit can be reduced by

the year 2005-2006 indicates that there is no probabilityreducing the raw material consumption, administration

of bankruptcy. However the score has declined over theand selling expenses. Interest expenses must be reduced

years. to enhance the profit of the firm.

2 It was found there is absolutely no probability of2 Current Assets must be reduced. Steps might be taken to

bankruptcy in the first three years. However, in the yearreduce the Inventory.

2008-2009, the probability of bankruptcy is 8% and it is2 Loans and advances must be collected speedily since it

22.8% in the 2009-2010. forms a great portion of Current Asset leading to very

high Current ratio.

ZMIJEWSKI'S MODEL 2 Cash balance may be reduced .Cash may be diverted to

2 X1 component of Zmijewski's was initially 0.5267 in theshort term investments.

year 2005-2006.It increased to 0.54 in the year 2006-

2007.Later, there has been a deep decline and X1CONCLUSION

component is currently 0.0006 because NPAT hasThe most important conclusion is that it is possible to

declined in the past two years. ¢ Zm Score is negative inpredict financial distress and bankruptcy more accurately

all years indicating that the firm has not failed. using the domestic data through new models based on

2 The probability of bankruptcy was 0.2981 in the yeardifferent combinations of financial ratios, when compared to

2005-2006. The probability of bankruptcy has the old and more prestigious model proposals. O-Score

fluctuated 0.07 and 0.46. The probability of bankruptcymodel is a proposalwith a slightly better prediction

in the current year is 0.0793 i.e. 7.93%. performance since it uses the binary logistic regression

technique against the existing model proposals of the past

SUGGESTIONS: researchers.Findings show that none of the existing

2 O-score is the best model for the predictionof prediction models could achieve a satisfactory level of

bankruptcy on two reasons: prediction performance.

4 The correlation between the Z-Score and the net profit The best model among the existing financial distress

is 0.72; Zmijewski's model and the net profit is 0.48; O-prediction models is Ohlson's O-Score Model. Surprisingly,

Score and the net profit is 0.95.The Correlation betweenAltman's Z-score Model has produced lower levels of

the bankruptcyprediction models and traditional correlation with traditional analysis while O-Score analysis

analysis ranges from 0.48 to 0.95. There is very highhas a very high positive correlation with traditional analysis.

positive correlation between Ohlson's O-score modelTexmo Industries should use O-Score model for prediction

and traditional analysis and the value is 0.95.Texmoof bankruptcy. The probability of bankruptcy is increased

Industries may use Ohlson's O-score model for theover the years and hence steps must be taken to improve the

prediction of bankruptcy. profit. The company that predicts the future and works

4 Z score model is based on four components whileperfectly in the present shall win at any time .

Zmijewski's model is based on three components to

DR. RADHA GANESH KUMAR, KISHORE KUMAR

85

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BIBLIOGRAPHY 14. Pandey. I.M., Financial Management, 10th Ed., New

1. Altman, Edward I. (1968). Financial Ratios, Delhi: McGraw-Hill Publishing Co. Ltd.,1998

Discriminant Analysis, and Prediction of Corporate

Bankruptcy, Journal of Finance, Vol. 4, 1968, pp. 589 -

609

2. Altman, Edward I. (1993). Corporate Financial

Distress: A Complete Guide to Predicting, Avoiding,

and Dealing with Bankruptcy, 1st Edition, New York:

John Wiley and Sons.

3. Altman, Edward, R. Haldeman, and P. Narayanan.

(1977). ZETA Analysis: A New Model to Identify

Bankruptcy Risk of Corporations, Journal of Banking

and Finance, March, pp. 29 - 54

4. Argenti, J. (1991). PredictingCorporate Failure,

Accountants Digest, Vol. 138, p. 3

5. Beaver,William H. (1966). Financial Ratios as

Predictors of Failures, Journal of Accounting

Researchpp.71 - 111

6. Deakin, Edward B. (1972). A Discriminant Analysis of

Predictors of Business Failure, Journal of Accounting

Research, Vol. 10, No. 1, pp. 167 - 179

7. Keasey,K. and Robert Watson (1991). Financial

Distress Prediction Models: A Review of Their

Usefulness, British Journal of Management, Vol 2, pp.

89 - 102

8. Maddala, G.S. (2004). Introduction to Econometrics,

3rd Edition, Wiley, New York,

9. Ohlson, James A. (1980). Financial Ratios and the

Probabilistic Prediction of Bankruptcy, Journal of

Accounting Research, Vol. 18, No.1, pp. 109 - 131

10. Scott, J. (1981). The Probability of Bankruptcy: A

Comparison of Empirical Predictions and Theoretical

Models, Journal of Banking and Finance, Summer, pp.

317 - 344

11. Zavgren, Christine (1985). Assessing the Vulnerability

to Failure of American industrial Firms: A Logistic

Analysis, Journal of Business Finance & Accounting,

Vol. 12, No. 1, pp. 19 - 45

12. Zmijewski, Mark E. (1984). Methodological Issues

Related to the Estimation of Financial Distress

Prediction Models, Journal of Accounting Research,

Vol. 22 Supplement, pp. 59 - 82 Anadolu

ÜniversitesiSosyal Bilimler Dergisi

13. Khan M.Y and Jain P.K., Financial Management Text

and Problems, 3rd Edition, New Delhi: Tata McGraw-

Hill Publishing Co.Ltd. 1999.

A COMPARISON OF BANKRUPTCY MODELS

86

1. Altman, Edward I. (1968). Financial Ratios, Delhi: McGraw-Hill Publishing Co. Ltd.,1998

Discriminant Analysis, and Prediction of Corporate

Bankruptcy, Journal of Finance, Vol. 4, 1968, pp. 589 -

609

2. Altman, Edward I. (1993). Corporate Financial

Distress: A Complete Guide to Predicting, Avoiding,

and Dealing with Bankruptcy, 1st Edition, New York:

John Wiley and Sons.

3. Altman, Edward, R. Haldeman, and P. Narayanan.

(1977). ZETA Analysis: A New Model to Identify

Bankruptcy Risk of Corporations, Journal of Banking

and Finance, March, pp. 29 - 54

4. Argenti, J. (1991). PredictingCorporate Failure,

Accountants Digest, Vol. 138, p. 3

5. Beaver,William H. (1966). Financial Ratios as

Predictors of Failures, Journal of Accounting

Researchpp.71 - 111

6. Deakin, Edward B. (1972). A Discriminant Analysis of

Predictors of Business Failure, Journal of Accounting

Research, Vol. 10, No. 1, pp. 167 - 179

7. Keasey,K. and Robert Watson (1991). Financial

Distress Prediction Models: A Review of Their

Usefulness, British Journal of Management, Vol 2, pp.

89 - 102

8. Maddala, G.S. (2004). Introduction to Econometrics,

3rd Edition, Wiley, New York,

9. Ohlson, James A. (1980). Financial Ratios and the

Probabilistic Prediction of Bankruptcy, Journal of

Accounting Research, Vol. 18, No.1, pp. 109 - 131

10. Scott, J. (1981). The Probability of Bankruptcy: A

Comparison of Empirical Predictions and Theoretical

Models, Journal of Banking and Finance, Summer, pp.

317 - 344

11. Zavgren, Christine (1985). Assessing the Vulnerability

to Failure of American industrial Firms: A Logistic

Analysis, Journal of Business Finance & Accounting,

Vol. 12, No. 1, pp. 19 - 45

12. Zmijewski, Mark E. (1984). Methodological Issues

Related to the Estimation of Financial Distress

Prediction Models, Journal of Accounting Research,

Vol. 22 Supplement, pp. 59 - 82 Anadolu

ÜniversitesiSosyal Bilimler Dergisi

13. Khan M.Y and Jain P.K., Financial Management Text

and Problems, 3rd Edition, New Delhi: Tata McGraw-

Hill Publishing Co.Ltd. 1999.

A COMPARISON OF BANKRUPTCY MODELS

86

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.