International Accounting: Costing Methods and Strategic Performance

VerifiedAdded on 2023/06/11

|10

|1872

|356

Report

AI Summary

This report provides a detailed analysis of international managerial accounting practices, focusing on costing methods such as target costing and activity-based costing (ABC), as well as the application of the balanced scorecard for strategic performance management. It includes a cost gap analysis, evaluates the advantages and disadvantages of target costing and life cycle costing, and discusses the benefits, drawbacks, and challenges associated with implementing a balanced scorecard. The report also offers recommendations for Abercrombie Fashion plc based on the costing analysis and emphasizes the importance of aligning strategic plans with organizational activities and employee goals. This student-contributed assignment is available on Desklib, a platform offering a wide range of study resources and AI-based tools for students.

INTERNATIONAL

MANAGERIAL

ACCOUNTING

MANAGERIAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A.....................................................................................................................................3

Question A2.................................................................................................................................3

(a).................................................................................................................................................3

(b).................................................................................................................................................4

(c).................................................................................................................................................4

SECTION B.....................................................................................................................................6

Question B3.................................................................................................................................6

REFERENCES................................................................................................................................1

SECTION A.....................................................................................................................................3

Question A2.................................................................................................................................3

(a).................................................................................................................................................3

(b).................................................................................................................................................4

(c).................................................................................................................................................4

SECTION B.....................................................................................................................................6

Question B3.................................................................................................................................6

REFERENCES................................................................................................................................1

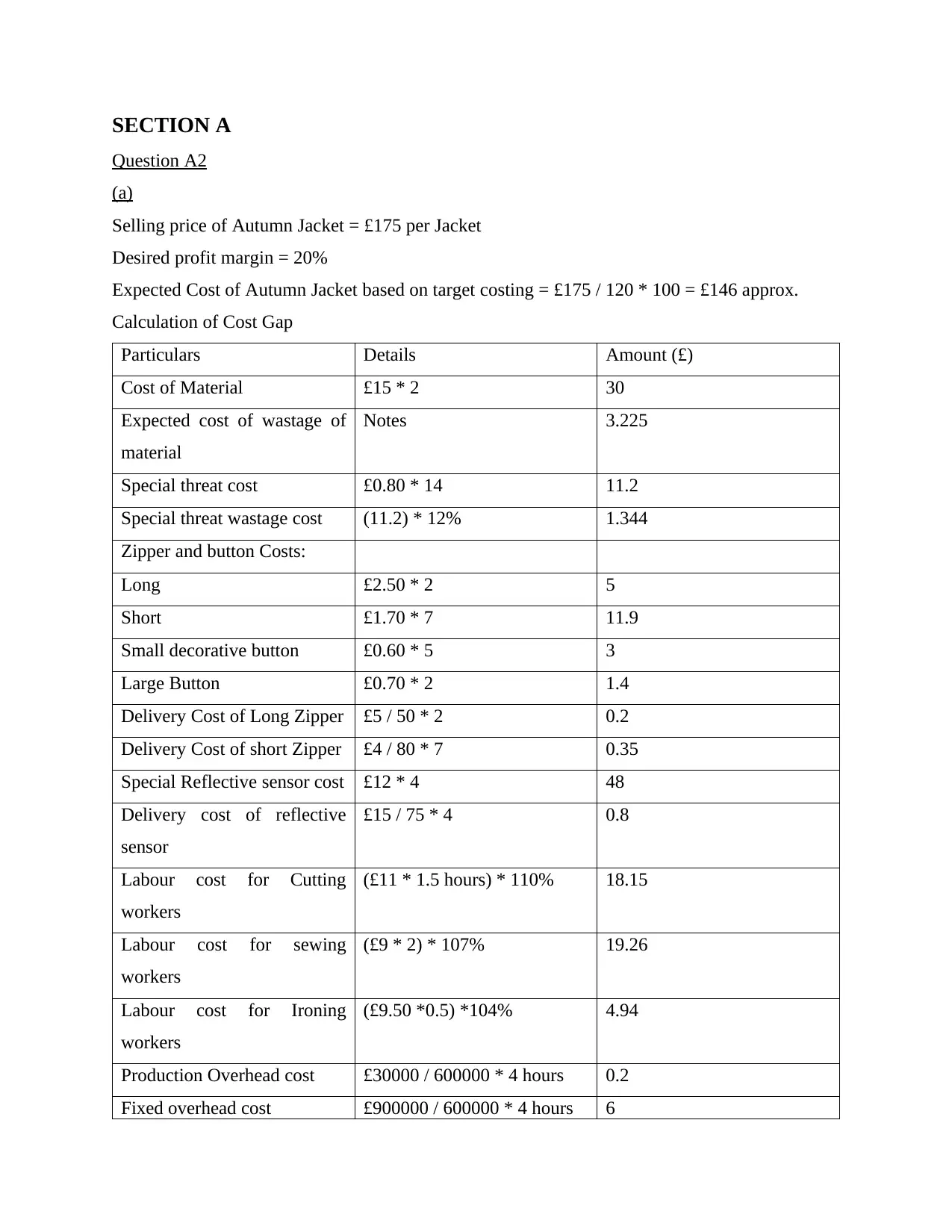

SECTION A

Question A2

(a)

Selling price of Autumn Jacket = £175 per Jacket

Desired profit margin = 20%

Expected Cost of Autumn Jacket based on target costing = £175 / 120 * 100 = £146 approx.

Calculation of Cost Gap

Particulars Details Amount (£)

Cost of Material £15 * 2 30

Expected cost of wastage of

material

Notes 3.225

Special threat cost £0.80 * 14 11.2

Special threat wastage cost (11.2) * 12% 1.344

Zipper and button Costs:

Long £2.50 * 2 5

Short £1.70 * 7 11.9

Small decorative button £0.60 * 5 3

Large Button £0.70 * 2 1.4

Delivery Cost of Long Zipper £5 / 50 * 2 0.2

Delivery Cost of short Zipper £4 / 80 * 7 0.35

Special Reflective sensor cost £12 * 4 48

Delivery cost of reflective

sensor

£15 / 75 * 4 0.8

Labour cost for Cutting

workers

(£11 * 1.5 hours) * 110% 18.15

Labour cost for sewing

workers

(£9 * 2) * 107% 19.26

Labour cost for Ironing

workers

(£9.50 *0.5) *104% 4.94

Production Overhead cost £30000 / 600000 * 4 hours 0.2

Fixed overhead cost £900000 / 600000 * 4 hours 6

Question A2

(a)

Selling price of Autumn Jacket = £175 per Jacket

Desired profit margin = 20%

Expected Cost of Autumn Jacket based on target costing = £175 / 120 * 100 = £146 approx.

Calculation of Cost Gap

Particulars Details Amount (£)

Cost of Material £15 * 2 30

Expected cost of wastage of

material

Notes 3.225

Special threat cost £0.80 * 14 11.2

Special threat wastage cost (11.2) * 12% 1.344

Zipper and button Costs:

Long £2.50 * 2 5

Short £1.70 * 7 11.9

Small decorative button £0.60 * 5 3

Large Button £0.70 * 2 1.4

Delivery Cost of Long Zipper £5 / 50 * 2 0.2

Delivery Cost of short Zipper £4 / 80 * 7 0.35

Special Reflective sensor cost £12 * 4 48

Delivery cost of reflective

sensor

£15 / 75 * 4 0.8

Labour cost for Cutting

workers

(£11 * 1.5 hours) * 110% 18.15

Labour cost for sewing

workers

(£9 * 2) * 107% 19.26

Labour cost for Ironing

workers

(£9.50 *0.5) *104% 4.94

Production Overhead cost £30000 / 600000 * 4 hours 0.2

Fixed overhead cost £900000 / 600000 * 4 hours 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total expected cost of an

Autumn Jacket based on cost

allocation.

164.969 or 165 approx.

Working notes:

40%

case 0.4 1.5 0.6

50%

case 0.5 3 1.5

25%

case 0.25 4.5 1.125

3.225

Cost Gap = Expected cost based on target costing – Expected Cost based as per ABC

= £165 - £146

= £19

(b)

On the basis of above calculation, it is identified that the gap between expected cost of both

scenario is 19. It means the cost as per ABC is higher than the cost as per target costing by £19.

However, on the other hand, it is also analysed that the actual cost is lower than the selling price

where actual cost is £165 while selling price is £175 per Jacket. It means with the sale of one

Jacket, the company will earn the profit of £10. On this basis, it is advisable to Abercrombie

Fashion plc. That they should proceed with the launching with new clothing line of autumn

jacket (Ahn, Clermont and Schwetschke, 2018).

(c)

Advantage of Target costing:

It helps the management to process improvement and product innovation to further gain

competitive advantage.

Autumn Jacket based on cost

allocation.

164.969 or 165 approx.

Working notes:

40%

case 0.4 1.5 0.6

50%

case 0.5 3 1.5

25%

case 0.25 4.5 1.125

3.225

Cost Gap = Expected cost based on target costing – Expected Cost based as per ABC

= £165 - £146

= £19

(b)

On the basis of above calculation, it is identified that the gap between expected cost of both

scenario is 19. It means the cost as per ABC is higher than the cost as per target costing by £19.

However, on the other hand, it is also analysed that the actual cost is lower than the selling price

where actual cost is £165 while selling price is £175 per Jacket. It means with the sale of one

Jacket, the company will earn the profit of £10. On this basis, it is advisable to Abercrombie

Fashion plc. That they should proceed with the launching with new clothing line of autumn

jacket (Ahn, Clermont and Schwetschke, 2018).

(c)

Advantage of Target costing:

It helps the management to process improvement and product innovation to further gain

competitive advantage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The product is created as per customer expectation thus customer feels more value is

delivered.

The company’s approach to designing and manufacturing products becomes market-

driven (Gonçalves, Gaio and Silva, 2018).

New market opportunities can be converted into real savings to achieve the best value for

money rather than to simply realize the lowest cost.

Disadvantage of Target costing:

Adopting of this costing is required permanent change of management system which is

one of the disadvantages.

It does not produce required result as it results is based on target profit margin.

Difficult to convince people to buy products at targeted selling price (Aladwan,

Alsinglawi and Alhawatmeh, 2018).

Advantage of Life cycle costing:

The application of life cycle costing is helps in improving the forecasting technique of

company.

Another advantage of life cycle costing is such that it improves awareness of the factors

that drive cost and the resources required by the purchase.

It is not only focus on cost but also consider other factors such as quality of goods, level

of services etc the impact of which performance can be trade-off against cost (De Menna

and et.al., 2018).

Disadvantage of life cycle costing:

Life cycle costing analysis is basically one of the time consuming because it required too

many changes in technology.

It is also costly because the longer the project life time, the more operating cost will be

incurred.

Another disadvantage is such that technology changes day to day (Naves and et.al.,

2019).

delivered.

The company’s approach to designing and manufacturing products becomes market-

driven (Gonçalves, Gaio and Silva, 2018).

New market opportunities can be converted into real savings to achieve the best value for

money rather than to simply realize the lowest cost.

Disadvantage of Target costing:

Adopting of this costing is required permanent change of management system which is

one of the disadvantages.

It does not produce required result as it results is based on target profit margin.

Difficult to convince people to buy products at targeted selling price (Aladwan,

Alsinglawi and Alhawatmeh, 2018).

Advantage of Life cycle costing:

The application of life cycle costing is helps in improving the forecasting technique of

company.

Another advantage of life cycle costing is such that it improves awareness of the factors

that drive cost and the resources required by the purchase.

It is not only focus on cost but also consider other factors such as quality of goods, level

of services etc the impact of which performance can be trade-off against cost (De Menna

and et.al., 2018).

Disadvantage of life cycle costing:

Life cycle costing analysis is basically one of the time consuming because it required too

many changes in technology.

It is also costly because the longer the project life time, the more operating cost will be

incurred.

Another disadvantage is such that technology changes day to day (Naves and et.al.,

2019).

SECTION B

Question B3

Benefits of Balance Scorecard

There are various benefits that balanced score card offers to the company. There are

various approaches that the balanced scorecard provides to the management for planning

strategically. The logical and well structured format of balanced scorecard enable the managers

of the company for ensuring the areas of the management are easily understandable to them. The

management have the advantage of focusing on the goal, and creating out the particular means in

order to manage and keep a track on the progress of the overall organizational activities. It

provides with the proper initiatives that can be followed for tracking the actions.

The management through effective preparation of balanced scorecard ensures that the

formulated strategic plans are easily communicated to the company and other concerned people.

A balanced scorecard is clear and easily interpret able that ensures that the activities of every

department are easily aligned to each of the other department that exists in the company. Clarity

regarding the goals on the end of employees exists (Quesado, Aibar Guzmán and Lima

Rodrigues, 2018)

. So the employees find it easy to work and make efforts that lead to achievement of the goals.

Employees can clearly visualize how one objective affects the other.

With the correct and proper implementation of the balanced scorecard common strategy

receives aligned actions from each department with the company. The BSC structure further

enables the connecting link between the objectives that are of critical nature and are by the parent

company. The employees can clearly see that their personal goals are how effectively connected

with the overall organizational strategy of the company.

Drawbacks of Balance Scorecard

There are certain disadvantages too that are attached with the balanced scorecard. The

balanced scorecard when used by the company makes the company to expect a framework for

itself. The balanced scorecard however requires customization as per the needs of the

organization. This customization process takes a lot of time (Quesado, Aibar Guzmán and Lima

Rodrigues, 2018). The examples for previously utilization of balanced scorecard are helpful no

doubt but they can not be used without being tailored. The reason being the needs are different

for every organization. So the drawback is the time consumption.

Question B3

Benefits of Balance Scorecard

There are various benefits that balanced score card offers to the company. There are

various approaches that the balanced scorecard provides to the management for planning

strategically. The logical and well structured format of balanced scorecard enable the managers

of the company for ensuring the areas of the management are easily understandable to them. The

management have the advantage of focusing on the goal, and creating out the particular means in

order to manage and keep a track on the progress of the overall organizational activities. It

provides with the proper initiatives that can be followed for tracking the actions.

The management through effective preparation of balanced scorecard ensures that the

formulated strategic plans are easily communicated to the company and other concerned people.

A balanced scorecard is clear and easily interpret able that ensures that the activities of every

department are easily aligned to each of the other department that exists in the company. Clarity

regarding the goals on the end of employees exists (Quesado, Aibar Guzmán and Lima

Rodrigues, 2018)

. So the employees find it easy to work and make efforts that lead to achievement of the goals.

Employees can clearly visualize how one objective affects the other.

With the correct and proper implementation of the balanced scorecard common strategy

receives aligned actions from each department with the company. The BSC structure further

enables the connecting link between the objectives that are of critical nature and are by the parent

company. The employees can clearly see that their personal goals are how effectively connected

with the overall organizational strategy of the company.

Drawbacks of Balance Scorecard

There are certain disadvantages too that are attached with the balanced scorecard. The

balanced scorecard when used by the company makes the company to expect a framework for

itself. The balanced scorecard however requires customization as per the needs of the

organization. This customization process takes a lot of time (Quesado, Aibar Guzmán and Lima

Rodrigues, 2018). The examples for previously utilization of balanced scorecard are helpful no

doubt but they can not be used without being tailored. The reason being the needs are different

for every organization. So the drawback is the time consumption.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The full effectiveness of balanced scorecard requires the need to implemented right from

the lowest level of the organization to the top level, meaning for effective implementation the

implementing approach must down to top approach. This requires effective leadership mind set

and also requires that the management agrees to the approach. So the drawback is the tendency

of the managers to disagree with the approach.

The framework of the balanced scorecard is such that it inclines towards becoming or

getting highly complicated. As the framework requires the providence of time and utmost

dedication to be understood by the user. There number of case studies and resources related to

the reading of the concerned tool are very vast. The reader gets twisted as there exists multiple

number of ways for the methods of the balanced scorecard.

Challenges a company can face

The first challenge that the company can face is regarding the defining of metrics. For

example: If the metrics are not clearly or poorly defined by the firm then the depiction of the

indicators will get difficult to be understood later on affecting the performance of the company.

The frequency of the metrics also plays an important role if the company collects the metrics

regarding information in the wrong frequency then the possible challenges will be regarding the

consistency in the achievement of the planned goals.

The next challenge with the approach implementation is that the lack of availability of

collection of data that is efficient and relevant reporting challenge. The companies for example

tend to overemphasize on the metrics financial aspects and neglects that the system already

provides the framework for the data collection and reporting (Deghash, 2019). Thus the attempt

by the company results in the automation of data regarding its collection and faces challenge in

achievement of the expected results. The companies should make the key performance indicators

(kips) as the priority.

The another challenge is regarding the lack of review structure that is formalized. The approach

does not provide the formal structure regarding the review mechanism. For the best working of

the balanced scorecard there must be a proper review structure. The change in the data on regular

basis requires the reviewing on the regular basis too. The further challenge that the organization

is likely to face is that the system leads to over focus on the internal processes of the company.

the lowest level of the organization to the top level, meaning for effective implementation the

implementing approach must down to top approach. This requires effective leadership mind set

and also requires that the management agrees to the approach. So the drawback is the tendency

of the managers to disagree with the approach.

The framework of the balanced scorecard is such that it inclines towards becoming or

getting highly complicated. As the framework requires the providence of time and utmost

dedication to be understood by the user. There number of case studies and resources related to

the reading of the concerned tool are very vast. The reader gets twisted as there exists multiple

number of ways for the methods of the balanced scorecard.

Challenges a company can face

The first challenge that the company can face is regarding the defining of metrics. For

example: If the metrics are not clearly or poorly defined by the firm then the depiction of the

indicators will get difficult to be understood later on affecting the performance of the company.

The frequency of the metrics also plays an important role if the company collects the metrics

regarding information in the wrong frequency then the possible challenges will be regarding the

consistency in the achievement of the planned goals.

The next challenge with the approach implementation is that the lack of availability of

collection of data that is efficient and relevant reporting challenge. The companies for example

tend to overemphasize on the metrics financial aspects and neglects that the system already

provides the framework for the data collection and reporting (Deghash, 2019). Thus the attempt

by the company results in the automation of data regarding its collection and faces challenge in

achievement of the expected results. The companies should make the key performance indicators

(kips) as the priority.

The another challenge is regarding the lack of review structure that is formalized. The approach

does not provide the formal structure regarding the review mechanism. For the best working of

the balanced scorecard there must be a proper review structure. The change in the data on regular

basis requires the reviewing on the regular basis too. The further challenge that the organization

is likely to face is that the system leads to over focus on the internal processes of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Ahn, H., Clermont, M. and Schwetschke, S., 2018. Research on target costing: past, present and

future. Management Review Quarterly, 68(3), pp.321-354.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster

analysis. Journal of Business Research, 89, pp.378-384.

Aladwan, M., Alsinglawi, O. and Alhawatmeh, O., 2018. The applicability of target costing in

Jordanian hotels industry. Academy of Accounting and Financial Studies Journal, 22(3),

pp.1-13.

De Menna, F. and et.al., 2018. Life cycle costing of food waste: A review of methodological

approaches. Waste Management, 73, pp.1-13.

Naves, A.X. and et.al., 2019. Life cycle costing as a bottom line for the life cycle sustainability

assessment in the solar energy sector: A review. Solar Energy, 192, pp.238-262.

Fatima, T. and Elbanna, S., 2020. Balanced scorecard in the hospitality and tourism industry:

Past, present and future. International Journal of Hospitality Management. 91. p.102656.

Quesado, P. R., Aibar Guzmán, B. and Lima Rodrigues, L., 2018. Advantages and contributions

in the balanced scorecard implementation. Intangible capital. 14(1). pp.186-201.

Deghash, A., 2019. Balanced scorecard application and its challenges. International Journal of

Business Ethics and Governance. 2(1). pp.33-58.

1

Books and journals

Ahn, H., Clermont, M. and Schwetschke, S., 2018. Research on target costing: past, present and

future. Management Review Quarterly, 68(3), pp.321-354.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster

analysis. Journal of Business Research, 89, pp.378-384.

Aladwan, M., Alsinglawi, O. and Alhawatmeh, O., 2018. The applicability of target costing in

Jordanian hotels industry. Academy of Accounting and Financial Studies Journal, 22(3),

pp.1-13.

De Menna, F. and et.al., 2018. Life cycle costing of food waste: A review of methodological

approaches. Waste Management, 73, pp.1-13.

Naves, A.X. and et.al., 2019. Life cycle costing as a bottom line for the life cycle sustainability

assessment in the solar energy sector: A review. Solar Energy, 192, pp.238-262.

Fatima, T. and Elbanna, S., 2020. Balanced scorecard in the hospitality and tourism industry:

Past, present and future. International Journal of Hospitality Management. 91. p.102656.

Quesado, P. R., Aibar Guzmán, B. and Lima Rodrigues, L., 2018. Advantages and contributions

in the balanced scorecard implementation. Intangible capital. 14(1). pp.186-201.

Deghash, A., 2019. Balanced scorecard application and its challenges. International Journal of

Business Ethics and Governance. 2(1). pp.33-58.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.