Global Economy Analysis: MAE203 Assignment, Trimester 1, 2019

VerifiedAdded on 2023/01/18

|7

|1838

|100

Homework Assignment

AI Summary

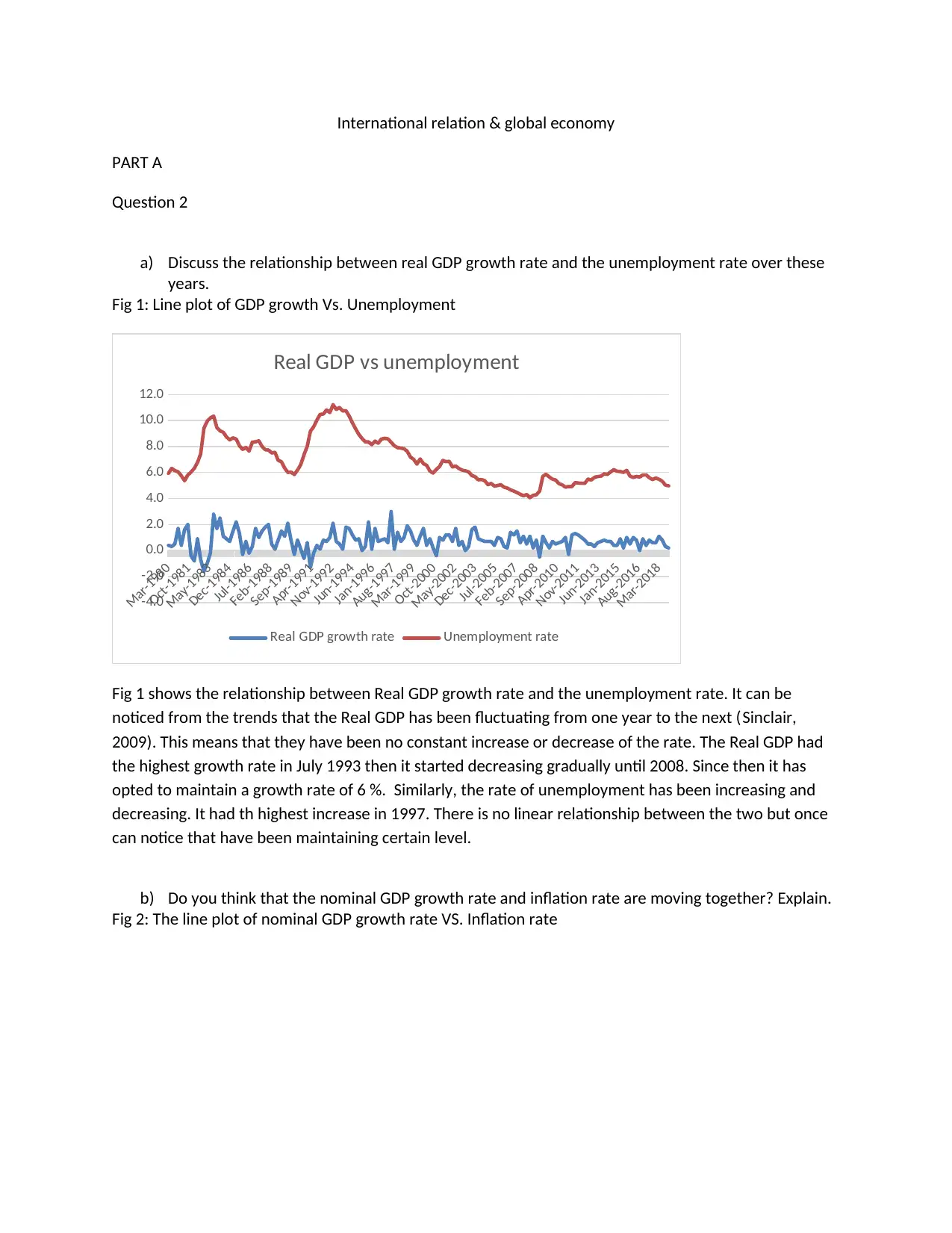

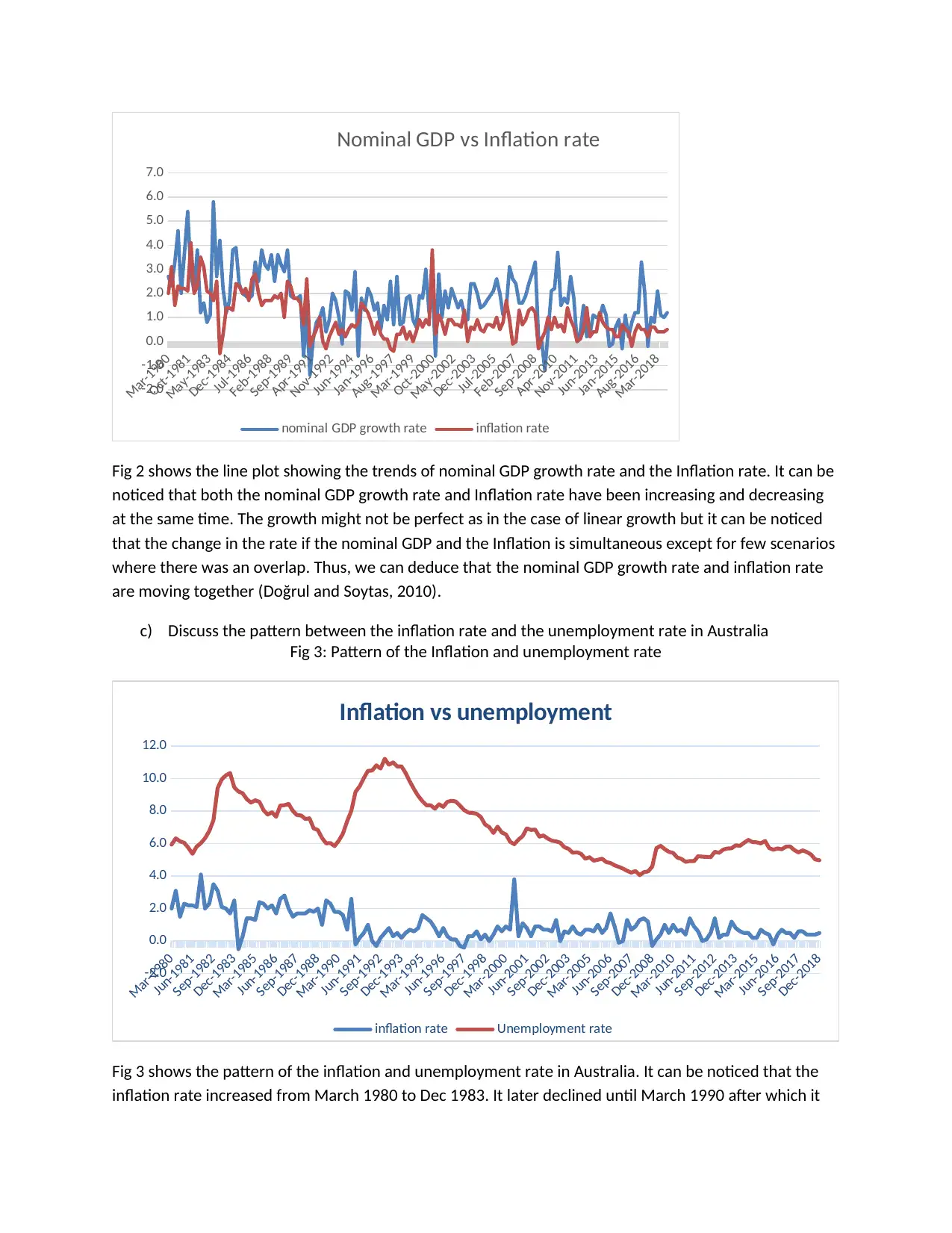

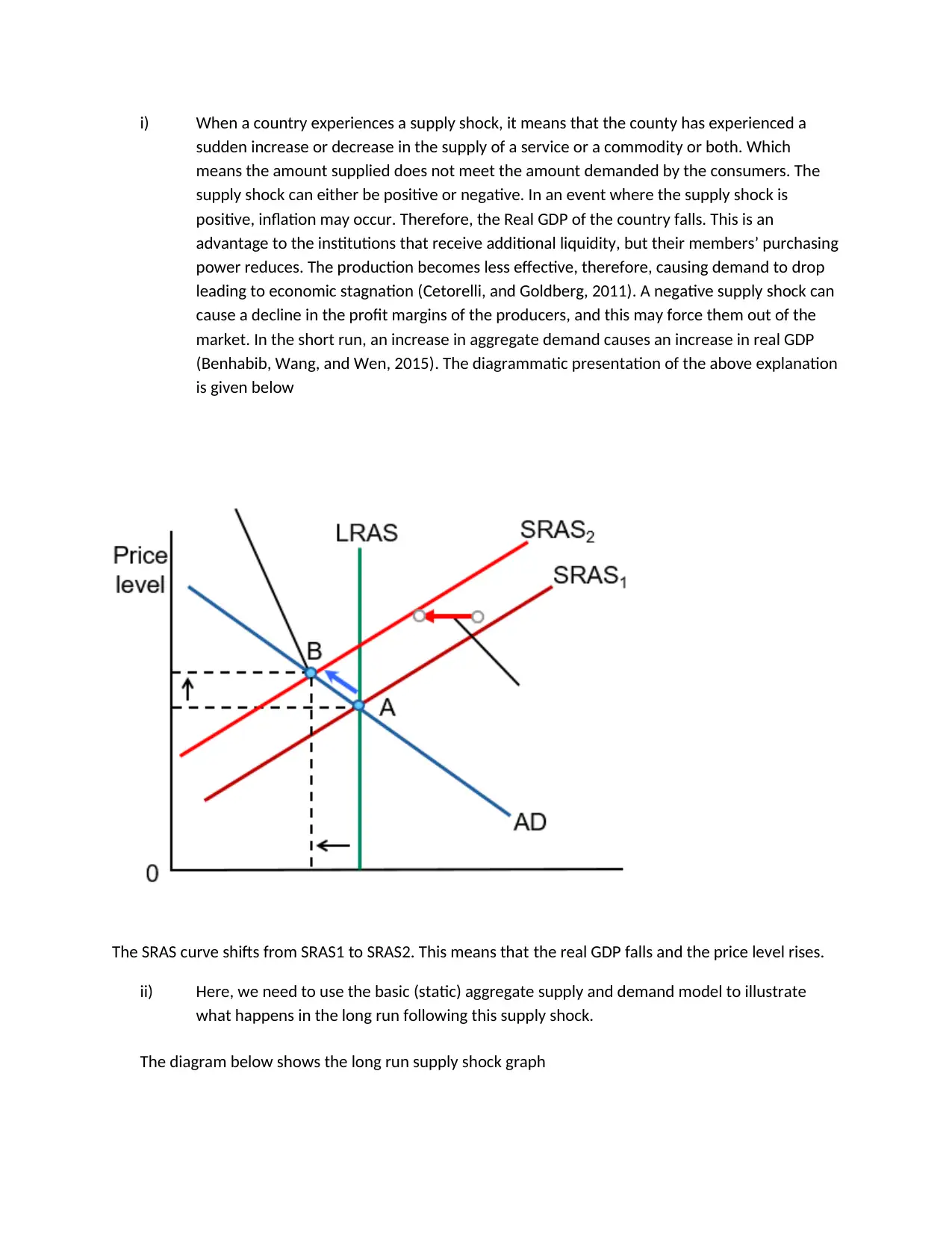

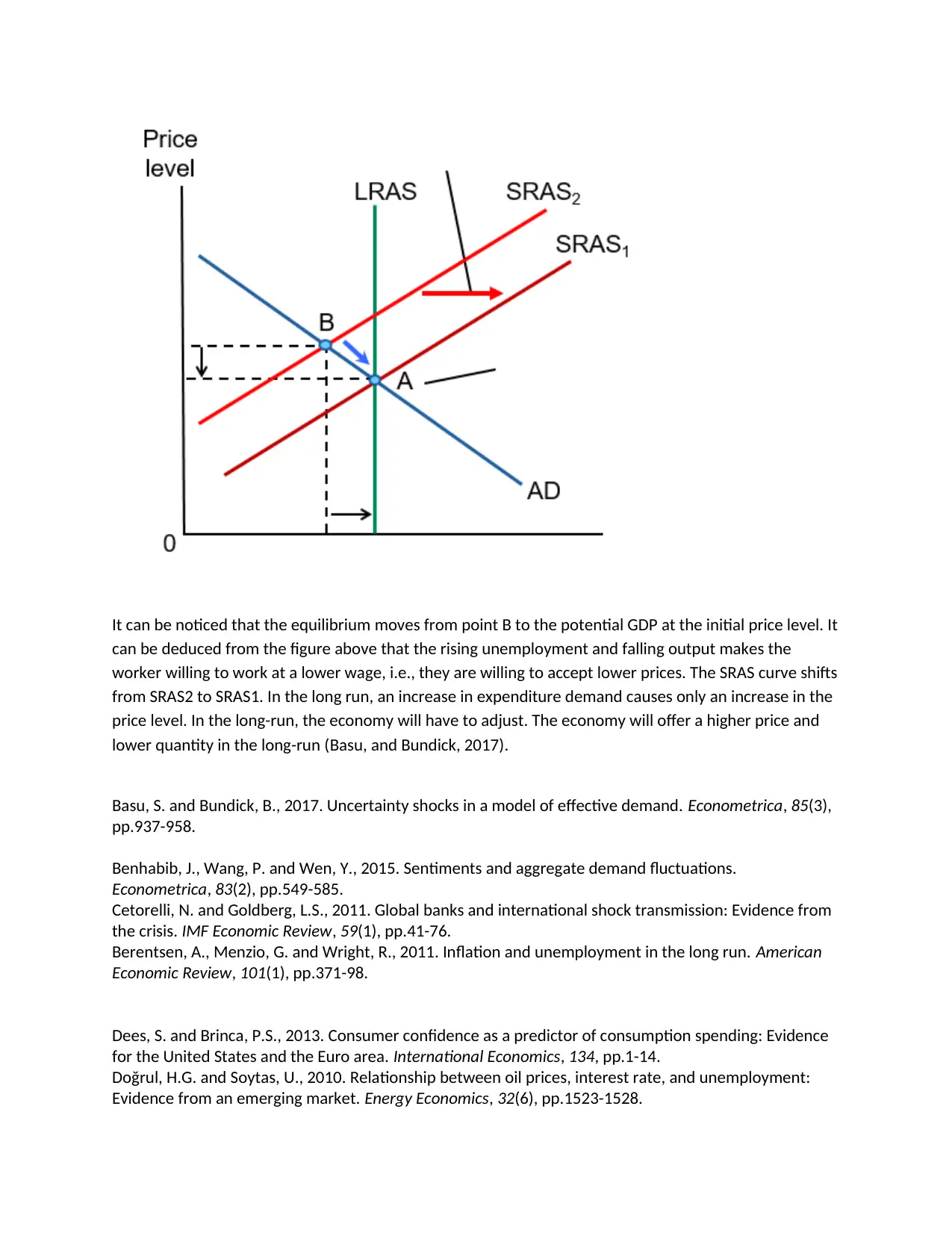

This assignment analyzes the global economy, focusing on the relationship between real GDP growth and unemployment, nominal GDP growth and inflation, and the patterns of inflation and unemployment in Australia. It also explores the factors influencing aggregate expenditure and discusses the impact of supply shocks on an economy, including both short-run and long-run effects. The assignment includes data analysis, graphical representations, and short answer explanations, adhering to the requirements of the MAE203 course, emphasizing data collection, presentation, and analytical skills. Furthermore, it briefly touches upon consumer confidence and the effects of interest rates on investment and consumption. The student utilizes graphs and economic models to explain the concepts and relationships discussed.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.