International Taxation: Group Structure, Loss Relief, Capital Transactions

Added on 2023-01-07

11 Pages2478 Words30 Views

INTERNATIONAL

TAXATION

TAXATION

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................3

a. Diagram of the group structure and the limit for tax rates.......................................................3

b. Loss relief groups and maximum amount...............................................................................4

c. Tax treatment of the capital transactions.................................................................................5

d. UK mainstream corporation tax liabilities...............................................................................6

e. Income tax consequences.........................................................................................................6

f. Tax implications.......................................................................................................................6

QUESTION 2..................................................................................................................................7

a. Comparison of expansion options............................................................................................7

b. Advice......................................................................................................................................7

c. Loss relief.................................................................................................................................7

d. VAT registration......................................................................................................................8

QUESTION 3..................................................................................................................................8

a. Domicile status of each employee...........................................................................................8

b. Claim to remittance..................................................................................................................9

c. Calculation of UK tax payable.................................................................................................9

REFERENCES..............................................................................................................................11

QUESTION 1..................................................................................................................................3

a. Diagram of the group structure and the limit for tax rates.......................................................3

b. Loss relief groups and maximum amount...............................................................................4

c. Tax treatment of the capital transactions.................................................................................5

d. UK mainstream corporation tax liabilities...............................................................................6

e. Income tax consequences.........................................................................................................6

f. Tax implications.......................................................................................................................6

QUESTION 2..................................................................................................................................7

a. Comparison of expansion options............................................................................................7

b. Advice......................................................................................................................................7

c. Loss relief.................................................................................................................................7

d. VAT registration......................................................................................................................8

QUESTION 3..................................................................................................................................8

a. Domicile status of each employee...........................................................................................8

b. Claim to remittance..................................................................................................................9

c. Calculation of UK tax payable.................................................................................................9

REFERENCES..............................................................................................................................11

QUESTION 1

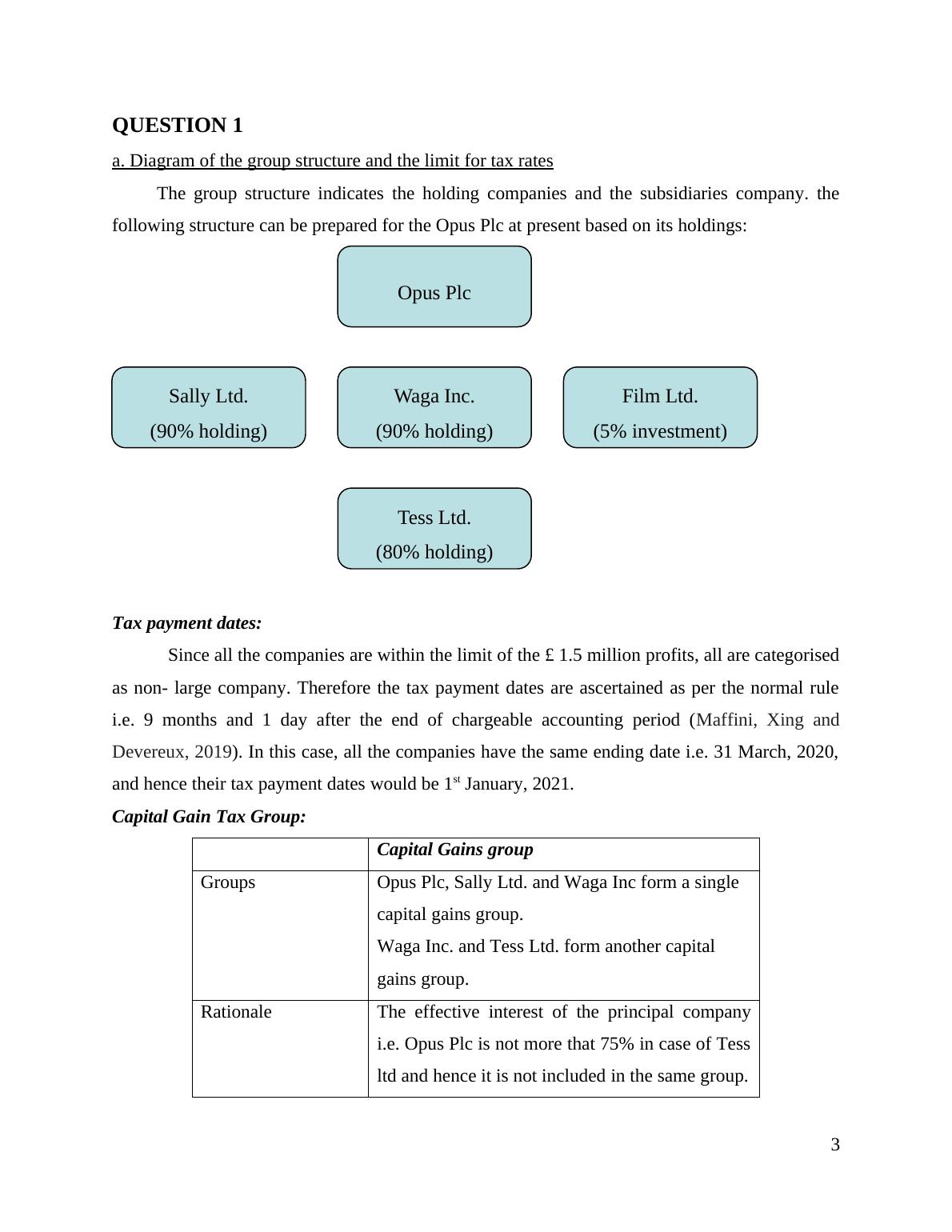

a. Diagram of the group structure and the limit for tax rates

The group structure indicates the holding companies and the subsidiaries company. the

following structure can be prepared for the Opus Plc at present based on its holdings:

Tax payment dates:

Since all the companies are within the limit of the £ 1.5 million profits, all are categorised

as non- large company. Therefore the tax payment dates are ascertained as per the normal rule

i.e. 9 months and 1 day after the end of chargeable accounting period (Maffini, Xing and

Devereux, 2019). In this case, all the companies have the same ending date i.e. 31 March, 2020,

and hence their tax payment dates would be 1st January, 2021.

Capital Gain Tax Group:

Capital Gains group

Groups Opus Plc, Sally Ltd. and Waga Inc form a single

capital gains group.

Waga Inc. and Tess Ltd. form another capital

gains group.

Rationale The effective interest of the principal company

i.e. Opus Plc is not more that 75% in case of Tess

ltd and hence it is not included in the same group.

3

Opus Plc

Sally Ltd.

(90% holding)

Waga Inc.

(90% holding)

Film Ltd.

(5% investment)

Tess Ltd.

(80% holding)

a. Diagram of the group structure and the limit for tax rates

The group structure indicates the holding companies and the subsidiaries company. the

following structure can be prepared for the Opus Plc at present based on its holdings:

Tax payment dates:

Since all the companies are within the limit of the £ 1.5 million profits, all are categorised

as non- large company. Therefore the tax payment dates are ascertained as per the normal rule

i.e. 9 months and 1 day after the end of chargeable accounting period (Maffini, Xing and

Devereux, 2019). In this case, all the companies have the same ending date i.e. 31 March, 2020,

and hence their tax payment dates would be 1st January, 2021.

Capital Gain Tax Group:

Capital Gains group

Groups Opus Plc, Sally Ltd. and Waga Inc form a single

capital gains group.

Waga Inc. and Tess Ltd. form another capital

gains group.

Rationale The effective interest of the principal company

i.e. Opus Plc is not more that 75% in case of Tess

ltd and hence it is not included in the same group.

3

Opus Plc

Sally Ltd.

(90% holding)

Waga Inc.

(90% holding)

Film Ltd.

(5% investment)

Tess Ltd.

(80% holding)

Note: In the entire evaluation Waga Inc. has been included in the capital gains group

because despite being a non- resident of UK, the company has a permanent establishment in UK

only. Therefore, these companies are allowed in the group and are treated as residents.

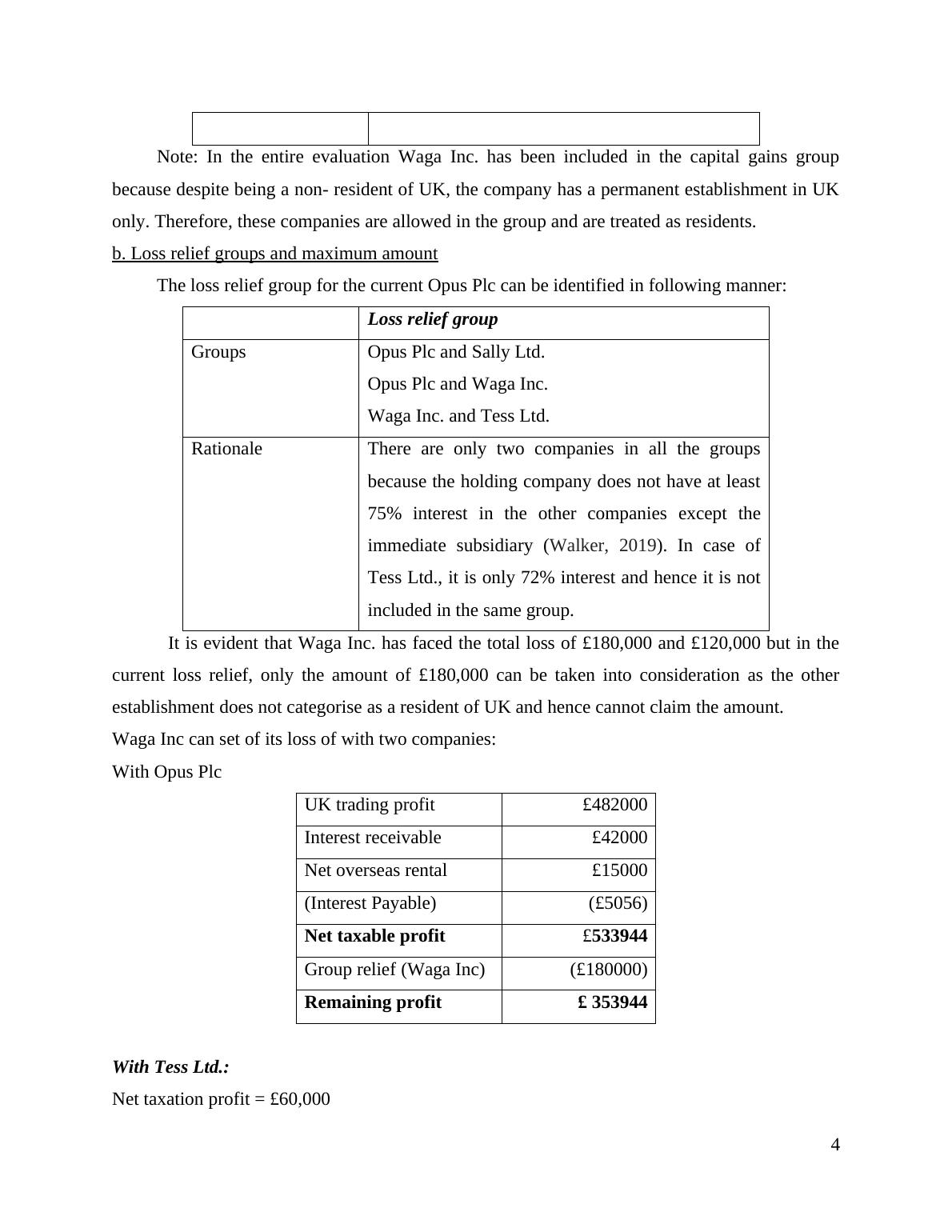

b. Loss relief groups and maximum amount

The loss relief group for the current Opus Plc can be identified in following manner:

Loss relief group

Groups Opus Plc and Sally Ltd.

Opus Plc and Waga Inc.

Waga Inc. and Tess Ltd.

Rationale There are only two companies in all the groups

because the holding company does not have at least

75% interest in the other companies except the

immediate subsidiary (Walker, 2019). In case of

Tess Ltd., it is only 72% interest and hence it is not

included in the same group.

It is evident that Waga Inc. has faced the total loss of £180,000 and £120,000 but in the

current loss relief, only the amount of £180,000 can be taken into consideration as the other

establishment does not categorise as a resident of UK and hence cannot claim the amount.

Waga Inc can set of its loss of with two companies:

With Opus Plc

UK trading profit £482000

Interest receivable £42000

Net overseas rental £15000

(Interest Payable) (£5056)

Net taxable profit £533944

Group relief (Waga Inc) (£180000)

Remaining profit £ 353944

With Tess Ltd.:

Net taxation profit = £60,000

4

because despite being a non- resident of UK, the company has a permanent establishment in UK

only. Therefore, these companies are allowed in the group and are treated as residents.

b. Loss relief groups and maximum amount

The loss relief group for the current Opus Plc can be identified in following manner:

Loss relief group

Groups Opus Plc and Sally Ltd.

Opus Plc and Waga Inc.

Waga Inc. and Tess Ltd.

Rationale There are only two companies in all the groups

because the holding company does not have at least

75% interest in the other companies except the

immediate subsidiary (Walker, 2019). In case of

Tess Ltd., it is only 72% interest and hence it is not

included in the same group.

It is evident that Waga Inc. has faced the total loss of £180,000 and £120,000 but in the

current loss relief, only the amount of £180,000 can be taken into consideration as the other

establishment does not categorise as a resident of UK and hence cannot claim the amount.

Waga Inc can set of its loss of with two companies:

With Opus Plc

UK trading profit £482000

Interest receivable £42000

Net overseas rental £15000

(Interest Payable) (£5056)

Net taxable profit £533944

Group relief (Waga Inc) (£180000)

Remaining profit £ 353944

With Tess Ltd.:

Net taxation profit = £60,000

4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation of the chargeable asset of Brownleas plc to Retro Ltd for the year ended 31 March 2015lg...

|15

|4528

|319

Taxation Law: Analysis of Case Facts and Tax Advice for Elwoodlg...

|6

|1416

|298

Memorandum and Consolidated Worksheet Entries for Palvidia Ltdlg...

|9

|1258

|317

Explaining nature of goodwill and its accountinglg...

|5

|887

|279

Consolidation of Financials and Calculation of Depreciation - Deskliblg...

|10

|1235

|235

TAXATION IN ACCOUNTING TABLE OF CONTENTS Question 1 3 Question 2 4 Question 4 5 Question 5 6.6 Corporate Tax Incentives for Promoting Business Growth, Investment and Entrepreneurshiplg...

|12

|2336

|185