Detailed Analysis of Various Payment Methods in International Trade

VerifiedAdded on 2021/08/30

|12

|2442

|463

Report

AI Summary

This report provides a detailed analysis of various payment methods used in international trade. It begins by explaining cash in advance (CA), a secure method for sellers, and open account, which favors buyers. The report then covers bank's documentary collection, where banks facilitate the exchange of documents and payments. Cash against documents (CAD) is also examined, highlighting its advantages and risks. The core of the report delves into letters of credit (LC), outlining their types, including at sight, time/usance, revolving, confirmed, transferable, back-to-back, and standby LCs. Each method's benefits, risks, and operational details are thoroughly discussed, providing a comprehensive understanding of payment mechanisms in global trade. The report also explores standby letters of credit and back-to-back letters of credit. The report also touches on the benefits of confirmed letters of credit and conditions for back-to-back letters of credit.

Table of Contents

1.CASH IN ADVANCE (CA)

2.OPEN ACCOUNT

3.BANK’S DOCUMENTARY COLLECTION

4.CASH AGAINST DOCUMENTS (“CAD” or “DP”)

5.LETTER OF CREDIT

CASH IN ADVANCE (CA)

Cash in advance is one of the most secure payment terms for sellers, and the least

secure for buyers. Indeed, Seller ships the goods to the buyer only after receiving the

full (or partial) payment for the goods (upfront payment).

Payments are made by wire transfer or by company checks (in the US). In the project

materials industry, cash in advance payment terms are rather rare and may occur for

stock and fast-track deliveries only.

What is “TT Payment”?

A bank transfer, otherwise called telegraphic transfer or telex transfer (“T/T”) is the

electronic transfer of funds from a buyer/importer to a seller/exporter, via a bank or a

similar institution.

For most countries and banks, as a buyer confirms a wire transfer, the funds cannot be

recovered from the beneficiary (such payments are irrevocable). ACH payments may be

an exception, i.e., they can be revoked.

T/T payments expose the buyer to high risks.

1.CASH IN ADVANCE (CA)

2.OPEN ACCOUNT

3.BANK’S DOCUMENTARY COLLECTION

4.CASH AGAINST DOCUMENTS (“CAD” or “DP”)

5.LETTER OF CREDIT

CASH IN ADVANCE (CA)

Cash in advance is one of the most secure payment terms for sellers, and the least

secure for buyers. Indeed, Seller ships the goods to the buyer only after receiving the

full (or partial) payment for the goods (upfront payment).

Payments are made by wire transfer or by company checks (in the US). In the project

materials industry, cash in advance payment terms are rather rare and may occur for

stock and fast-track deliveries only.

What is “TT Payment”?

A bank transfer, otherwise called telegraphic transfer or telex transfer (“T/T”) is the

electronic transfer of funds from a buyer/importer to a seller/exporter, via a bank or a

similar institution.

For most countries and banks, as a buyer confirms a wire transfer, the funds cannot be

recovered from the beneficiary (such payments are irrevocable). ACH payments may be

an exception, i.e., they can be revoked.

T/T payments expose the buyer to high risks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alternative payment risks, described below, have been introduced to minimize the

payment risks for buyers (and suppliers) in international trading operations.

OPEN ACCOUNT

Under open account payment terms, the supplier ships the goods to the buyer without

receiving upfront payments and collects the due amounts later (15, 30, 60, 90 days or

more).

Discounts on the invoice face value may be granted, on the sale invoice, for anticipated

payments.

This type of payment, which is quite common, has an opposite nature to “cash in

advance”, as it is very favorable for the buyer and unfavorable for the seller (who bears

the full payment risks).

Payments in open account are generally accepted by suppliers with low negotiation

power or by suppliers that have long-lasting relationships with the buyer.

Credit Insurance

Some sellers subscribe credit insurance contracts believing that they will protect their

“open account” sales.

A common trait of these types of contracts, which are generally expensive, is that they

cover the creditor in case of bankruptcy of the debtor, but they do not cover the seller

when the buyer rejects payment for any due or undue cause.

When a buyer disputes a delivery, the insured seller must turn to the Law, and not to the

credit insurance company, to get the payment.

payment risks for buyers (and suppliers) in international trading operations.

OPEN ACCOUNT

Under open account payment terms, the supplier ships the goods to the buyer without

receiving upfront payments and collects the due amounts later (15, 30, 60, 90 days or

more).

Discounts on the invoice face value may be granted, on the sale invoice, for anticipated

payments.

This type of payment, which is quite common, has an opposite nature to “cash in

advance”, as it is very favorable for the buyer and unfavorable for the seller (who bears

the full payment risks).

Payments in open account are generally accepted by suppliers with low negotiation

power or by suppliers that have long-lasting relationships with the buyer.

Credit Insurance

Some sellers subscribe credit insurance contracts believing that they will protect their

“open account” sales.

A common trait of these types of contracts, which are generally expensive, is that they

cover the creditor in case of bankruptcy of the debtor, but they do not cover the seller

when the buyer rejects payment for any due or undue cause.

When a buyer disputes a delivery, the insured seller must turn to the Law, and not to the

credit insurance company, to get the payment.

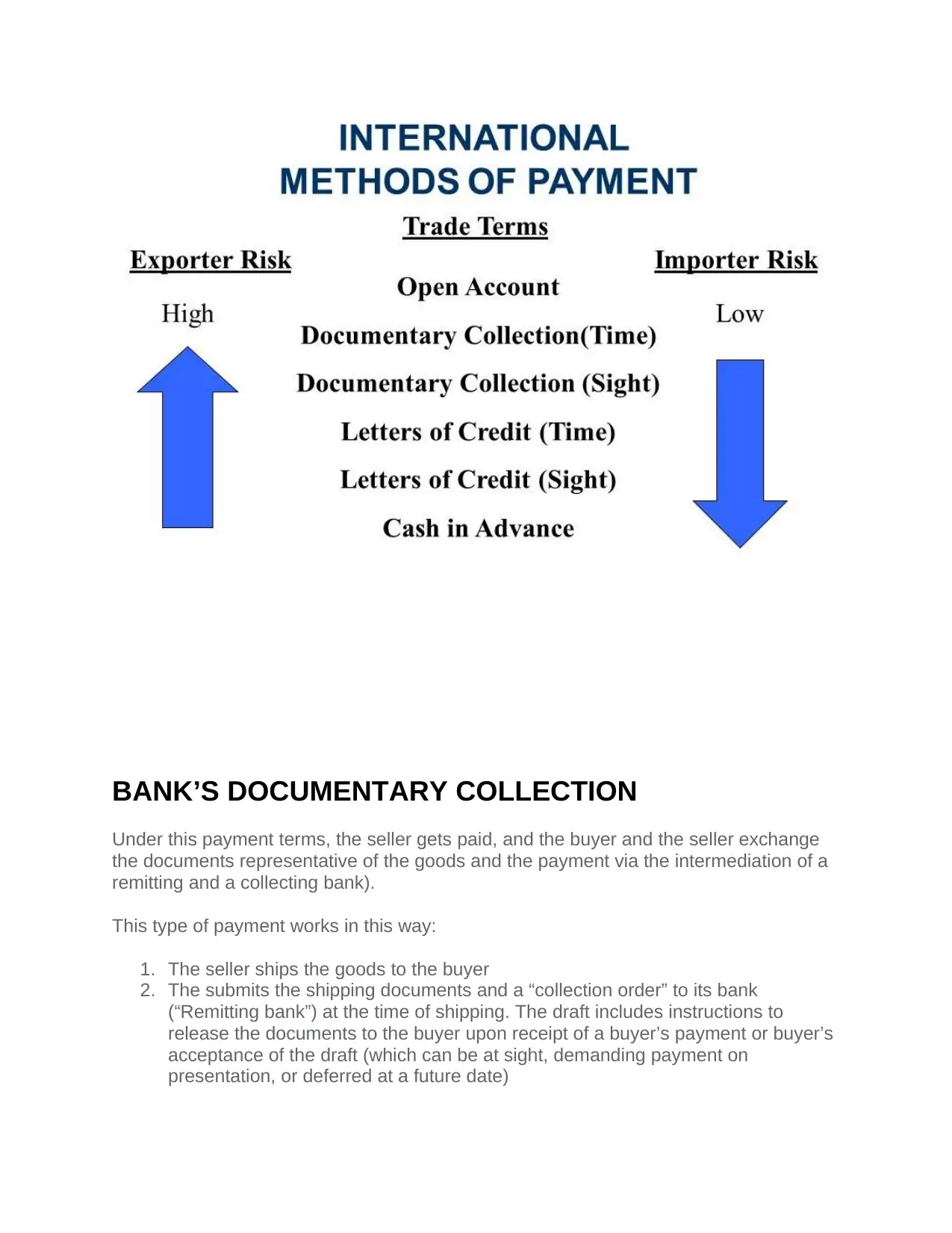

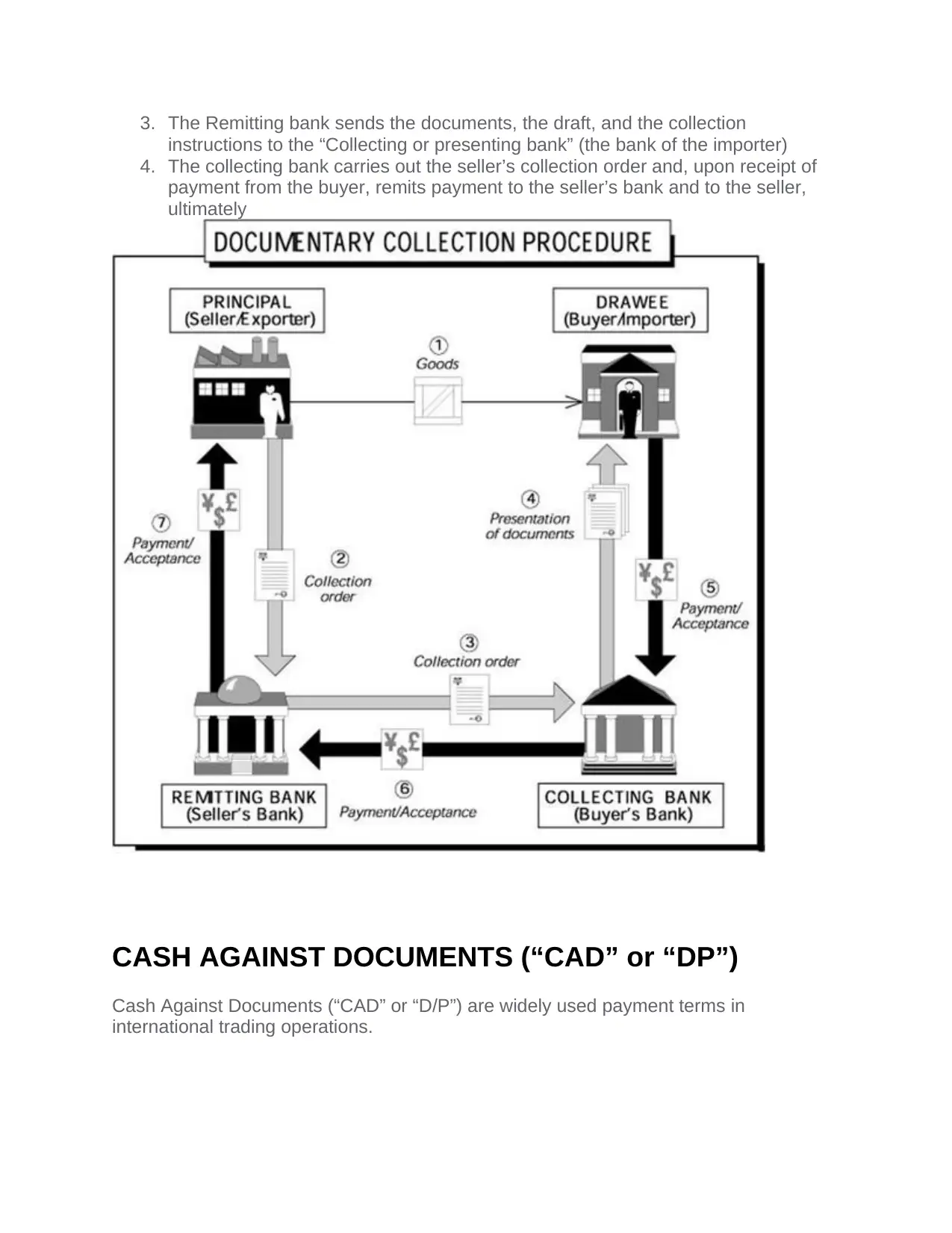

BANK’S DOCUMENTARY COLLECTION

Under this payment terms, the seller gets paid, and the buyer and the seller exchange

the documents representative of the goods and the payment via the intermediation of a

remitting and a collecting bank).

This type of payment works in this way:

1. The seller ships the goods to the buyer

2. The submits the shipping documents and a “collection order” to its bank

(“Remitting bank”) at the time of shipping. The draft includes instructions to

release the documents to the buyer upon receipt of a buyer’s payment or buyer’s

acceptance of the draft (which can be at sight, demanding payment on

presentation, or deferred at a future date)

Under this payment terms, the seller gets paid, and the buyer and the seller exchange

the documents representative of the goods and the payment via the intermediation of a

remitting and a collecting bank).

This type of payment works in this way:

1. The seller ships the goods to the buyer

2. The submits the shipping documents and a “collection order” to its bank

(“Remitting bank”) at the time of shipping. The draft includes instructions to

release the documents to the buyer upon receipt of a buyer’s payment or buyer’s

acceptance of the draft (which can be at sight, demanding payment on

presentation, or deferred at a future date)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. The Remitting bank sends the documents, the draft, and the collection

instructions to the “Collecting or presenting bank” (the bank of the importer)

4. The collecting bank carries out the seller’s collection order and, upon receipt of

payment from the buyer, remits payment to the seller’s bank and to the seller,

ultimately

CASH AGAINST DOCUMENTS (“CAD” or “DP”)

Cash Against Documents (“CAD” or “D/P”) are widely used payment terms in

international trading operations.

instructions to the “Collecting or presenting bank” (the bank of the importer)

4. The collecting bank carries out the seller’s collection order and, upon receipt of

payment from the buyer, remits payment to the seller’s bank and to the seller,

ultimately

CASH AGAINST DOCUMENTS (“CAD” or “DP”)

Cash Against Documents (“CAD” or “D/P”) are widely used payment terms in

international trading operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

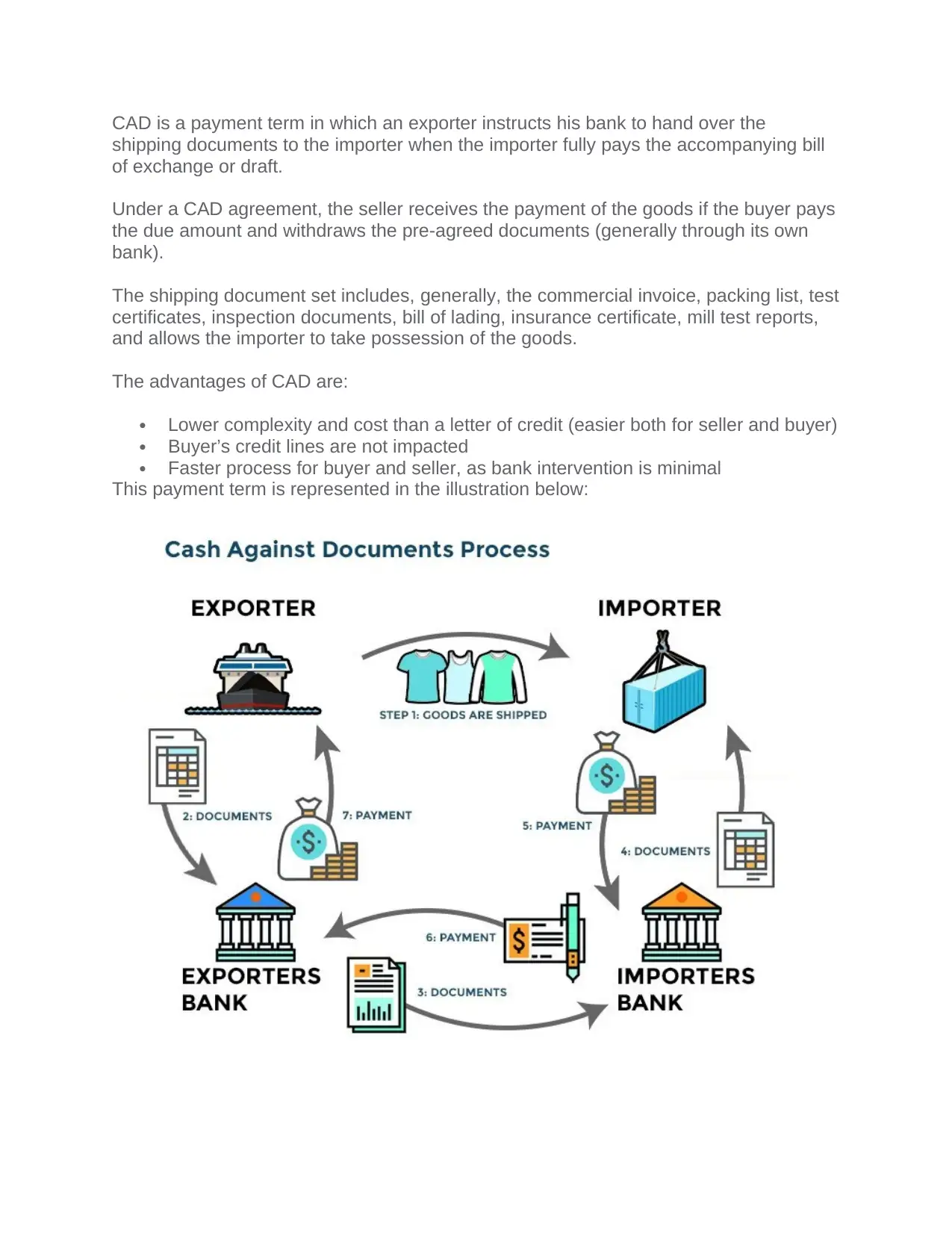

CAD is a payment term in which an exporter instructs his bank to hand over the

shipping documents to the importer when the importer fully pays the accompanying bill

of exchange or draft.

Under a CAD agreement, the seller receives the payment of the goods if the buyer pays

the due amount and withdraws the pre-agreed documents (generally through its own

bank).

The shipping document set includes, generally, the commercial invoice, packing list, test

certificates, inspection documents, bill of lading, insurance certificate, mill test reports,

and allows the importer to take possession of the goods.

The advantages of CAD are:

Lower complexity and cost than a letter of credit (easier both for seller and buyer)

Buyer’s credit lines are not impacted

Faster process for buyer and seller, as bank intervention is minimal

This payment term is represented in the illustration below:

shipping documents to the importer when the importer fully pays the accompanying bill

of exchange or draft.

Under a CAD agreement, the seller receives the payment of the goods if the buyer pays

the due amount and withdraws the pre-agreed documents (generally through its own

bank).

The shipping document set includes, generally, the commercial invoice, packing list, test

certificates, inspection documents, bill of lading, insurance certificate, mill test reports,

and allows the importer to take possession of the goods.

The advantages of CAD are:

Lower complexity and cost than a letter of credit (easier both for seller and buyer)

Buyer’s credit lines are not impacted

Faster process for buyer and seller, as bank intervention is minimal

This payment term is represented in the illustration below:

Risks of Cash Against Document Payment:

The main risk of CAD payment term is that buyers may not collect the goods and the

shipping documents after the shipment has taken place.

Hence, DAP is a very different arrangement than the payment by letter of credit, where

the seller basically no payment risk in case compliant documents are sent to the issuing

bank within the validity of the credit.

Due to this fact, sellers shall be very careful with DAP payment terms as they generate

unpaid invoices and excess stock.

LETTER OF CREDIT

A Letter of Credit, simply defined, is a written instrument issued by a bank at the request

of its customer, the Importer (Buyer), whereby the bank promises to pay the Exporter

(Beneficiary) for goods or services, provided that the Exporter presents all documents

called for, exactly as stipulated in the Letter of Credit, and meet all other terms and

conditions set out in the letter of Credit.

A Letter of Credit is also commonly referred to as a Documentary Credit.

Letters of credit are used between trade partners that do not know themselves well, are

in remote locations and do not accept the payment risks of other payment terms as

open account, bank transfer, and cash against documents.

The terms “Letters of Credit” /or L/C) and “Documentary Credit” (D/C) have the same

exact meaning. The first is more common in USA and Asia, whereas the latter is

common terminology in Europe.

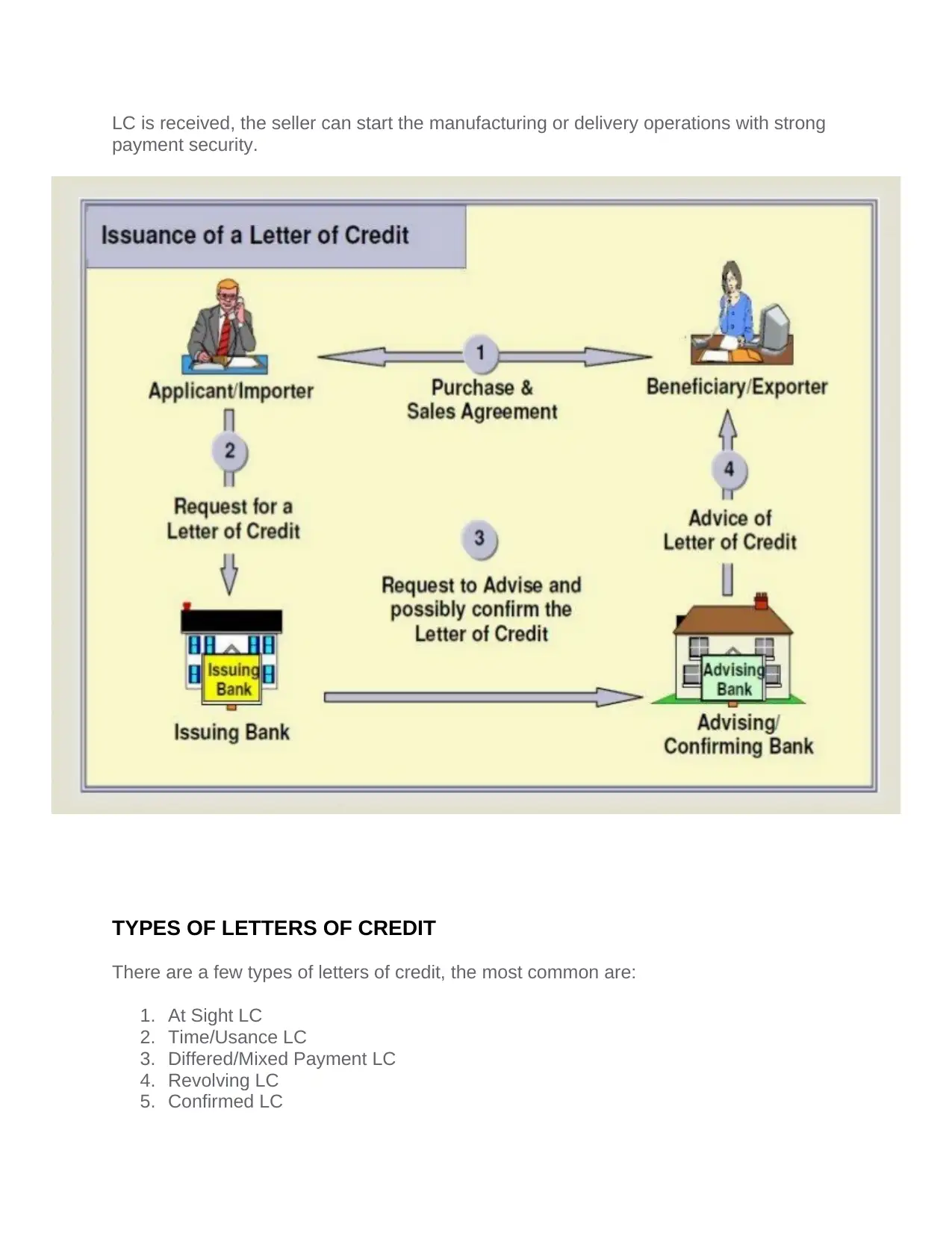

HOW TO ISSUE AN LC

Before issuing an LC, the importer shall have approved credit limits sanctioned by the

issuing bank.

Moreover, imports and exports transactions that involve foreign currencies are subject

to foreign exchange regulations and other international rules like UCPDC 600, URR etc.

Generally, the issuing bank requires the importer to submit an LC Application form to

issue a Letter of Credit.

After receiving the application, the bank issues a draft LC that the importer and exporter

can review and, in case, amend. As the LC is agreed between the parties, the issuing

bank submits the LC to the exporter advising bank, who in turn informs the seller. As an

The main risk of CAD payment term is that buyers may not collect the goods and the

shipping documents after the shipment has taken place.

Hence, DAP is a very different arrangement than the payment by letter of credit, where

the seller basically no payment risk in case compliant documents are sent to the issuing

bank within the validity of the credit.

Due to this fact, sellers shall be very careful with DAP payment terms as they generate

unpaid invoices and excess stock.

LETTER OF CREDIT

A Letter of Credit, simply defined, is a written instrument issued by a bank at the request

of its customer, the Importer (Buyer), whereby the bank promises to pay the Exporter

(Beneficiary) for goods or services, provided that the Exporter presents all documents

called for, exactly as stipulated in the Letter of Credit, and meet all other terms and

conditions set out in the letter of Credit.

A Letter of Credit is also commonly referred to as a Documentary Credit.

Letters of credit are used between trade partners that do not know themselves well, are

in remote locations and do not accept the payment risks of other payment terms as

open account, bank transfer, and cash against documents.

The terms “Letters of Credit” /or L/C) and “Documentary Credit” (D/C) have the same

exact meaning. The first is more common in USA and Asia, whereas the latter is

common terminology in Europe.

HOW TO ISSUE AN LC

Before issuing an LC, the importer shall have approved credit limits sanctioned by the

issuing bank.

Moreover, imports and exports transactions that involve foreign currencies are subject

to foreign exchange regulations and other international rules like UCPDC 600, URR etc.

Generally, the issuing bank requires the importer to submit an LC Application form to

issue a Letter of Credit.

After receiving the application, the bank issues a draft LC that the importer and exporter

can review and, in case, amend. As the LC is agreed between the parties, the issuing

bank submits the LC to the exporter advising bank, who in turn informs the seller. As an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LC is received, the seller can start the manufacturing or delivery operations with strong

payment security.

TYPES OF LETTERS OF CREDIT

There are a few types of letters of credit, the most common are:

1. At Sight LC

2. Time/Usance LC

3. Differed/Mixed Payment LC

4. Revolving LC

5. Confirmed LC

payment security.

TYPES OF LETTERS OF CREDIT

There are a few types of letters of credit, the most common are:

1. At Sight LC

2. Time/Usance LC

3. Differed/Mixed Payment LC

4. Revolving LC

5. Confirmed LC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Transferable LC

7. Back-to-Back LC

8. Advance Payment LC

9. Discounting LC

10. Standby LC

STANDBY LETTER OF CREDIT

A standby letter of credit is a guarantee of payment by a bank on behalf of a client. It is

a loan of last resort in which the bank fulfills payment obligations at the end of a contract

in case of failed payment by the bank’s client.

Standby letters of credit are issued not to be used, normally. Standby letters of credit

help prove a business’ creditworthiness and pay back ability.

Types of Standby Letters of Credit

Performance Standby letter of credit

o Performance standby letters of credit ensure the nonfinancial contractual

obligations (quality of work, amount of work, time, cost, etc.) are

performed in a timely and satisfactory manner. If these obligations are not

met, the bank will pay the third party in full.

The financial Standby letter of credit

o Financial standby letters of credit ensure financial contractual obligations

are fulfilled. Most SLOCs are financial.

o Financial SLOCs are often required when performing an international

trade or other large purchase contracts under which other forms of

payment protections (such as litigation in the event of non-payment) can

be difficult to obtain.

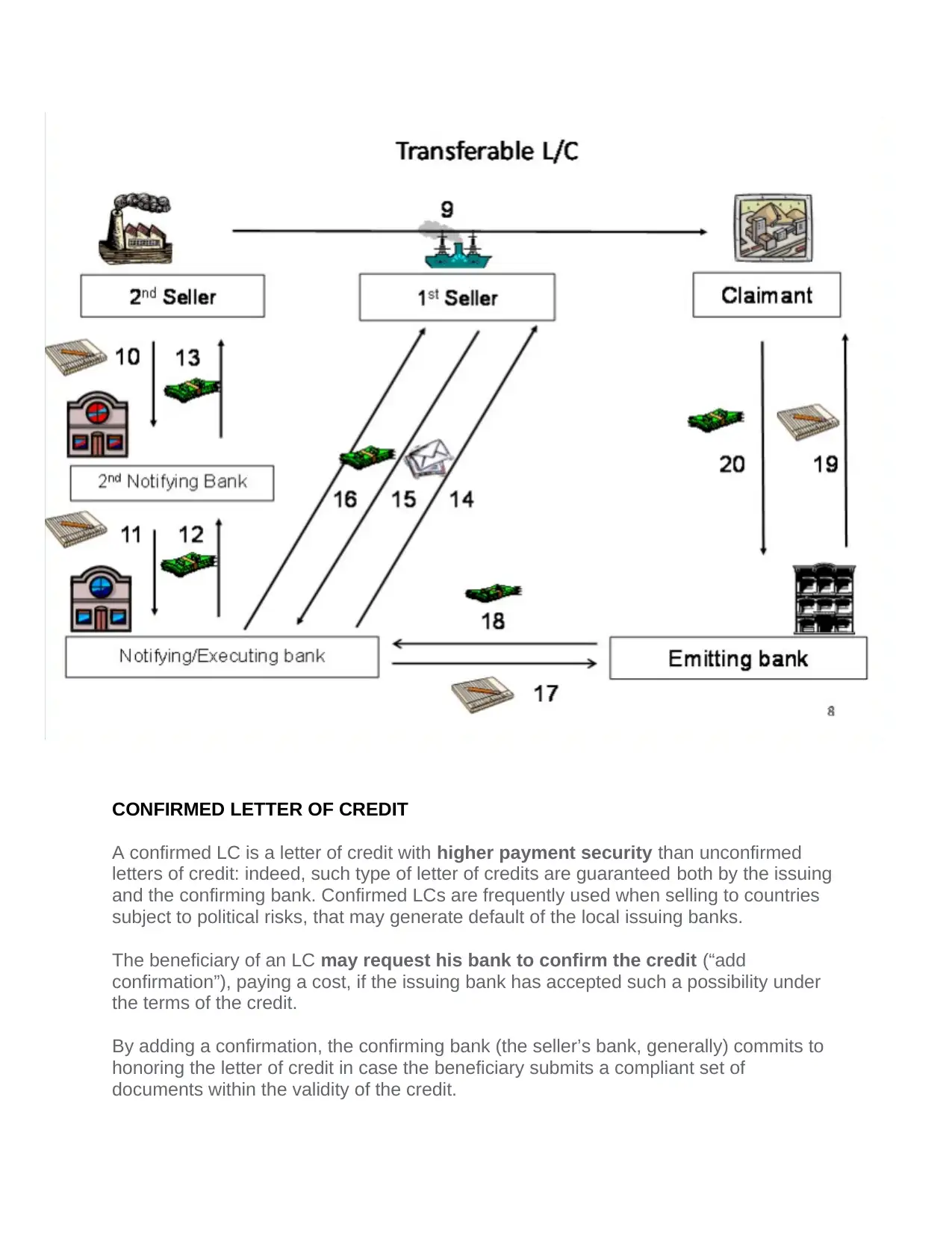

TRANSFERABLE LETTER OF CREDIT

A transferable letter of credit is a special transferable form of a documentary letter of

credit opened for the benefit of the intermediate seller (the first beneficiary).

The transferable form allows the intermediate seller to apply to the nominated bank with

a request of transferring the letter of credit in whole or in part to the supplier (the second

beneficiary).

In case the intermediate seller purchases products from multiple suppliers, it has the

right to instruct the nominated bank to transfer the letter of credit by parts to each of the

suppliers.

7. Back-to-Back LC

8. Advance Payment LC

9. Discounting LC

10. Standby LC

STANDBY LETTER OF CREDIT

A standby letter of credit is a guarantee of payment by a bank on behalf of a client. It is

a loan of last resort in which the bank fulfills payment obligations at the end of a contract

in case of failed payment by the bank’s client.

Standby letters of credit are issued not to be used, normally. Standby letters of credit

help prove a business’ creditworthiness and pay back ability.

Types of Standby Letters of Credit

Performance Standby letter of credit

o Performance standby letters of credit ensure the nonfinancial contractual

obligations (quality of work, amount of work, time, cost, etc.) are

performed in a timely and satisfactory manner. If these obligations are not

met, the bank will pay the third party in full.

The financial Standby letter of credit

o Financial standby letters of credit ensure financial contractual obligations

are fulfilled. Most SLOCs are financial.

o Financial SLOCs are often required when performing an international

trade or other large purchase contracts under which other forms of

payment protections (such as litigation in the event of non-payment) can

be difficult to obtain.

TRANSFERABLE LETTER OF CREDIT

A transferable letter of credit is a special transferable form of a documentary letter of

credit opened for the benefit of the intermediate seller (the first beneficiary).

The transferable form allows the intermediate seller to apply to the nominated bank with

a request of transferring the letter of credit in whole or in part to the supplier (the second

beneficiary).

In case the intermediate seller purchases products from multiple suppliers, it has the

right to instruct the nominated bank to transfer the letter of credit by parts to each of the

suppliers.

CONFIRMED LETTER OF CREDIT

A confirmed LC is a letter of credit with higher payment security than unconfirmed

letters of credit: indeed, such type of letter of credits are guaranteed both by the issuing

and the confirming bank. Confirmed LCs are frequently used when selling to countries

subject to political risks, that may generate default of the local issuing banks.

The beneficiary of an LC may request his bank to confirm the credit (“add

confirmation”), paying a cost, if the issuing bank has accepted such a possibility under

the terms of the credit.

By adding a confirmation, the confirming bank (the seller’s bank, generally) commits to

honoring the letter of credit in case the beneficiary submits a compliant set of

documents within the validity of the credit.

A confirmed LC is a letter of credit with higher payment security than unconfirmed

letters of credit: indeed, such type of letter of credits are guaranteed both by the issuing

and the confirming bank. Confirmed LCs are frequently used when selling to countries

subject to political risks, that may generate default of the local issuing banks.

The beneficiary of an LC may request his bank to confirm the credit (“add

confirmation”), paying a cost, if the issuing bank has accepted such a possibility under

the terms of the credit.

By adding a confirmation, the confirming bank (the seller’s bank, generally) commits to

honoring the letter of credit in case the beneficiary submits a compliant set of

documents within the validity of the credit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Such undertaking from the confirming bank is separate from, and in addition to, the

undertaking of the issuing bank.

BENEFITS OF CONFIRMED LC

The exporter may be interested in adding confirmation to the letter of credit in the

following cases:

when the creditworthiness of the issuing bank is uncertain

when selling to politically unstable countries

to prevent the risk of default of the issuing bank

to execute the LC faster

undertaking of the issuing bank.

BENEFITS OF CONFIRMED LC

The exporter may be interested in adding confirmation to the letter of credit in the

following cases:

when the creditworthiness of the issuing bank is uncertain

when selling to politically unstable countries

to prevent the risk of default of the issuing bank

to execute the LC faster

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banks confirm LCs at a cost that is expressed as an interest rate or a fixed fee (or a

combination of both). Generally, the cost is an interest rate ratio (example Libor) plus a

spread (confirmation fee). The higher the risk for the confirming bank, the higher the

cost.

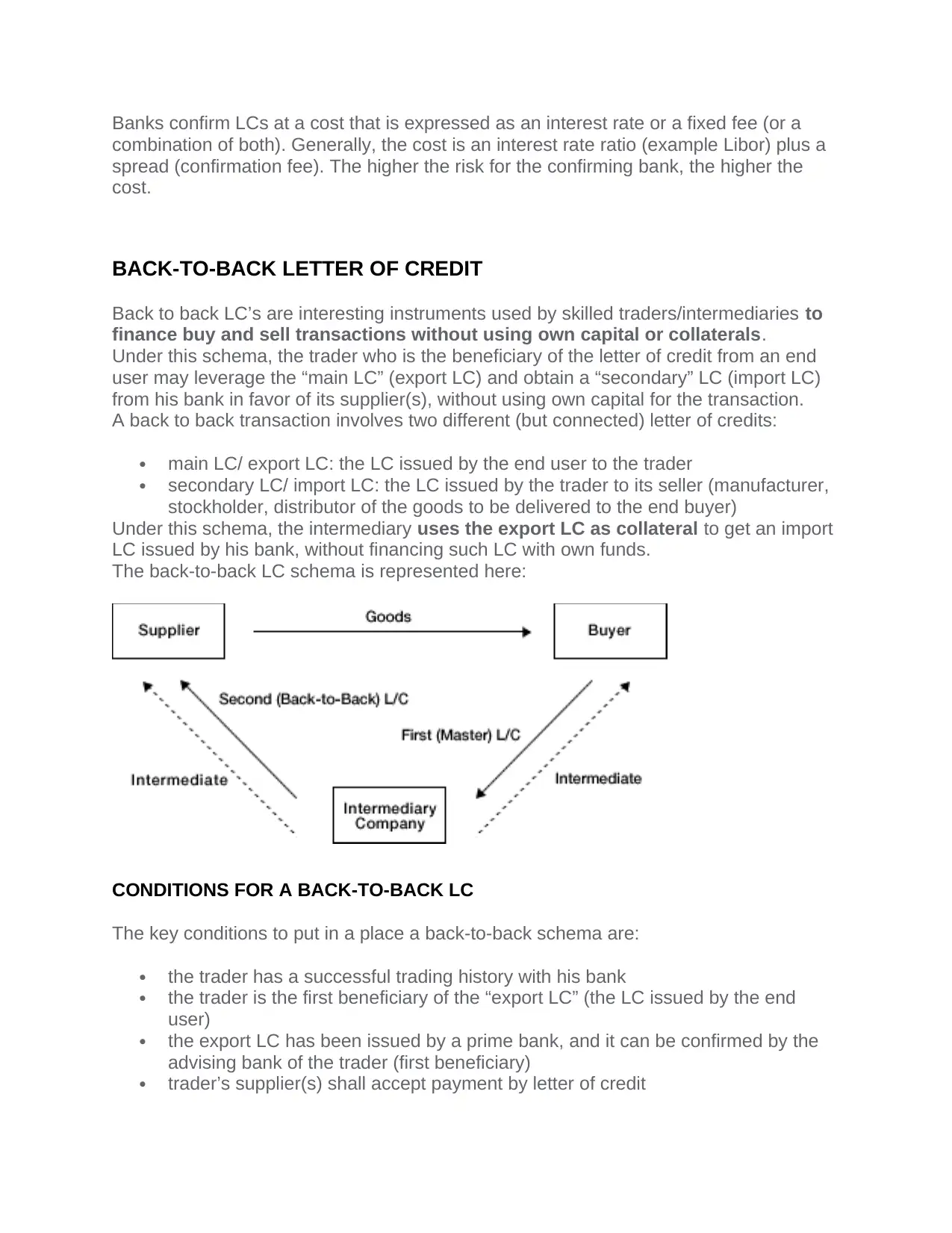

BACK-TO-BACK LETTER OF CREDIT

Back to back LC’s are interesting instruments used by skilled traders/intermediaries to

finance buy and sell transactions without using own capital or collaterals.

Under this schema, the trader who is the beneficiary of the letter of credit from an end

user may leverage the “main LC” (export LC) and obtain a “secondary” LC (import LC)

from his bank in favor of its supplier(s), without using own capital for the transaction.

A back to back transaction involves two different (but connected) letter of credits:

main LC/ export LC: the LC issued by the end user to the trader

secondary LC/ import LC: the LC issued by the trader to its seller (manufacturer,

stockholder, distributor of the goods to be delivered to the end buyer)

Under this schema, the intermediary uses the export LC as collateral to get an import

LC issued by his bank, without financing such LC with own funds.

The back-to-back LC schema is represented here:

CONDITIONS FOR A BACK-TO-BACK LC

The key conditions to put in a place a back-to-back schema are:

the trader has a successful trading history with his bank

the trader is the first beneficiary of the “export LC” (the LC issued by the end

user)

the export LC has been issued by a prime bank, and it can be confirmed by the

advising bank of the trader (first beneficiary)

trader’s supplier(s) shall accept payment by letter of credit

combination of both). Generally, the cost is an interest rate ratio (example Libor) plus a

spread (confirmation fee). The higher the risk for the confirming bank, the higher the

cost.

BACK-TO-BACK LETTER OF CREDIT

Back to back LC’s are interesting instruments used by skilled traders/intermediaries to

finance buy and sell transactions without using own capital or collaterals.

Under this schema, the trader who is the beneficiary of the letter of credit from an end

user may leverage the “main LC” (export LC) and obtain a “secondary” LC (import LC)

from his bank in favor of its supplier(s), without using own capital for the transaction.

A back to back transaction involves two different (but connected) letter of credits:

main LC/ export LC: the LC issued by the end user to the trader

secondary LC/ import LC: the LC issued by the trader to its seller (manufacturer,

stockholder, distributor of the goods to be delivered to the end buyer)

Under this schema, the intermediary uses the export LC as collateral to get an import

LC issued by his bank, without financing such LC with own funds.

The back-to-back LC schema is represented here:

CONDITIONS FOR A BACK-TO-BACK LC

The key conditions to put in a place a back-to-back schema are:

the trader has a successful trading history with his bank

the trader is the first beneficiary of the “export LC” (the LC issued by the end

user)

the export LC has been issued by a prime bank, and it can be confirmed by the

advising bank of the trader (first beneficiary)

trader’s supplier(s) shall accept payment by letter of credit

import and export LC’s show same terms and conditions, except for the price of

the goods (nature of goods, delivery place, and terms, pay location, documents,

etc.)

Not all banks accept a back-to-back schema, as it involves some degree of risk for the

bank itself. However, when banks can ensure a consequential cash in and cash out,

and know the terms of the transaction well, a back-to-back LC may be arranged.

BENEFITS OF BACK-TO-BACK LETTER OF CREDIT

The trader may finance the transaction without impacting own funds or credit

lines

buyer may not know the identity of the seller, and the seller may not know the

identity of the end buyer

The trader may expand the business beyond its financial capacity

TRANSFERABLE VS BACK-TO-BACK LETTER OF CREDIT

Differently from “transferrable” LCs, which require the end user to approve the transfer

of the credit from the original beneficiary to a new beneficiary (condition that is seldom

accepted, as risky), a back-to-back LC does not require such approval and is a private

arrangement between the beneficiary of the “main LC” /” export LC” and its bank.

The end user and the manufacturer of the goods may be totally unaware of the fact that

a back-to-back arrangement has been put in place to execute the transaction.

the goods (nature of goods, delivery place, and terms, pay location, documents,

etc.)

Not all banks accept a back-to-back schema, as it involves some degree of risk for the

bank itself. However, when banks can ensure a consequential cash in and cash out,

and know the terms of the transaction well, a back-to-back LC may be arranged.

BENEFITS OF BACK-TO-BACK LETTER OF CREDIT

The trader may finance the transaction without impacting own funds or credit

lines

buyer may not know the identity of the seller, and the seller may not know the

identity of the end buyer

The trader may expand the business beyond its financial capacity

TRANSFERABLE VS BACK-TO-BACK LETTER OF CREDIT

Differently from “transferrable” LCs, which require the end user to approve the transfer

of the credit from the original beneficiary to a new beneficiary (condition that is seldom

accepted, as risky), a back-to-back LC does not require such approval and is a private

arrangement between the beneficiary of the “main LC” /” export LC” and its bank.

The end user and the manufacturer of the goods may be totally unaware of the fact that

a back-to-back arrangement has been put in place to execute the transaction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.