International Financial Accounting Standard and Regulations

Added on 2020-02-24

11 Pages2486 Words87 Views

By student name ProfessorUniversityDate: 25 August 2017.

1ContentsQuestion no 1..............................................................................2Question no 2..............................................................................6Question no 3..............................................................................8Refrences....................................................................................101 | P a g e

2Question no oneWith the release and introduction of International Financial Accounting Standards and otherregulations of Accounting Standard Board, Audit has taken special significance and holds utmostimportance. It gives the reasonable assurance to the users of the financial statements, both internal andexternal, which includes customers, shareholders, creditors, debtors, banks, financial institutions, etc.Audit is an independent check of the financials prepared and reported by the entity, whethergovernment or private, small or large, with a view to express and opinion whether the same has beenprepared on an unbiased basis. Management also makes use of the estimates, assumptions andjudgements in several areas, which cannot be clearly defined, for all such areas; auditor needs to verifywhether the appropriate assumptions have been taken[ CITATION Kne16 \l 1033 ]. There are variousmethods through which the auditor carries out his checking. This includes inspection of the critical andimportant general ledgers, observation of the activities happening within the premises of the client likephysical verification of the stock, taking external confirmation from the banks and financial institutionsand creditors. Along with that inquiring from the external parties and customer about the client businessand it environment, performance of the significant activities and calculations like tax, which may have ahuge bearing on the cash flow and applying further analytical procedures. Auditors generally applysubstantive procedures to see the viability and the existence of the numbers recorded to evidentiatesubstance over form. They want to check the completeness of the transaction along with the supportingand relevant evidences, disclosures which have been given in the financials and whether the valuationhas been correctly and reliably done or not for the cases where it requires so. Substantive auditprocedures included vouching of the expenses and incomes recorded in the books and verification ofthe liabilities and the assets, which are appearing in the statement of affairs as on the reporting date.The sales are checked with the invoice and bills, the costs and expenses incurred are reconciled with thepurchase orders raised and vouchers, etc. The assets are checked from the agreement or lease deed,etc., and for the liabilities, their existence is determined by external confirmation[ CITATION Jon171 \l1033 ].Besides all the above procedures, analytical procedures holds a special significance as todetermine the nature of checking, timing to be assigned and the extent to which the sample verificationis to be done. All this determines the final qualification of the audit report and it is all dependent largelyon the internal control procedures being followed within the company. More effective the test ofcontrol and test of design within the organisation, lesser the risk and lesser is the application of audit2 | P a g e

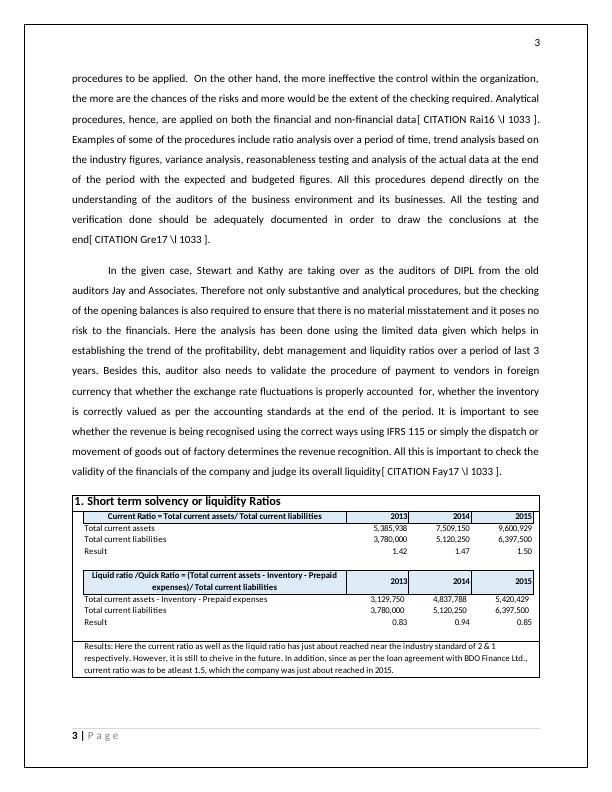

3procedures to be applied. On the other hand, the more ineffective the control within the organization,the more are the chances of the risks and more would be the extent of the checking required. Analyticalprocedures, hence, are applied on both the financial and non-financial data[ CITATION Rai16 \l 1033 ].Examples of some of the procedures include ratio analysis over a period of time, trend analysis based onthe industry figures, variance analysis, reasonableness testing and analysis of the actual data at the endof the period with the expected and budgeted figures. All this procedures depend directly on theunderstanding of the auditors of the business environment and its businesses. All the testing andverification done should be adequately documented in order to draw the conclusions at theend[ CITATION Gre17 \l 1033 ].In the given case, Stewart and Kathy are taking over as the auditors of DIPL from the oldauditors Jay and Associates. Therefore not only substantive and analytical procedures, but the checkingof the opening balances is also required to ensure that there is no material misstatement and it poses norisk to the financials. Here the analysis has been done using the limited data given which helps inestablishing the trend of the profitability, debt management and liquidity ratios over a period of last 3years. Besides this, auditor also needs to validate the procedure of payment to vendors in foreigncurrency that whether the exchange rate fluctuations is properly accounted for, whether the inventoryis correctly valued as per the accounting standards at the end of the period. It is important to seewhether the revenue is being recognised using the correct ways using IFRS 115 or simply the dispatch ormovement of goods out of factory determines the revenue recognition. All this is important to check thevalidity of the financials of the company and judge its overall liquidity[ CITATION Fay17 \l 1033 ].201320142015Total current assets5,385,9387,509,1509,600,929Total current liabilities3,780,0005,120,2506,397,500Result1.421.471.50201320142015Total current assets - Inventory - Prepaid expenses3,129,7504,837,7885,420,429Total current liabilities3,780,0005,120,2506,397,500Result0.830.940.85Results: Here the current ratio as well as the liquid ratio has just about reached near the industry standard of 2 & 1 respectively. However, it is still to cheive in the future. In addition, since as per the loan agreement with BDO Finance Ltd., current ratio was to be atleast 1.5, which the company was just about reached in 2015.1. Short term solvency or liquidity RatiosCurrent Ratio = Total current assets/ Total current liabilitiesLiquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid expenses)/ Total current liabilities3 | P a g e

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

LUBS3550 - Introduction To Audit | Assignmentlg...

|10

|2392

|109

Annual Reports on Paying Corporate Taxeslg...

|10

|2397

|52

Micro and Macro Economic Factors in Audit Reportlg...

|9

|2103

|108

HI6026 - Audit, Assurance and Compliancelg...

|9

|2190

|47

ACC 301 - Assignment On Audit & Factors That Affectslg...

|11

|2503

|65

Auditing assurance and compliance - HI6026lg...

|8

|1161

|38