Management Accounting Techniques and Decision Making

VerifiedAdded on 2020/01/23

|17

|5725

|171

Essay

AI Summary

This assignment delves into the crucial role of management accounting techniques in facilitating effective decision-making within organizations. Students are tasked with critically analyzing a selection of research papers that shed light on this topic. The analysis focuses on understanding the contributions of these studies to our comprehension of how management accounting practices influence organizational decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types for Agmet:...........................................................1

P2 Explanation over the different methods used for management accounting reporting.......3

M1 Benefits of management accounting systems and their application within Agmet........4

D1 Management accounting systems and MA reporting is integrated within organisational

processes:................................................................................................................................5

TASK 2............................................................................................................................................6

P3,M2 & D2 Calculation of cost using techniques of absorption and marginal costing........6

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools:...............................8

M3 Different planning tools and their application for preparing and forecasting budgets:. 10

D3 Planning tools used for responding financial problems:...............................................11

TASK 4..........................................................................................................................................11

P5 Comparison how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................11

M4 To analyse financial problems, MA can lead to organisations for sustainable success:12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types for Agmet:...........................................................1

P2 Explanation over the different methods used for management accounting reporting.......3

M1 Benefits of management accounting systems and their application within Agmet........4

D1 Management accounting systems and MA reporting is integrated within organisational

processes:................................................................................................................................5

TASK 2............................................................................................................................................6

P3,M2 & D2 Calculation of cost using techniques of absorption and marginal costing........6

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different types of planning tools:...............................8

M3 Different planning tools and their application for preparing and forecasting budgets:. 10

D3 Planning tools used for responding financial problems:...............................................11

TASK 4..........................................................................................................................................11

P5 Comparison how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................11

M4 To analyse financial problems, MA can lead to organisations for sustainable success:12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting can be specified as the method that has the quality of both

financial system and managerial principle therefore this can be said that these principles of

management accounting can be used by the management for decision making process. This

report contains various concepts about the management accounting and its associated techniques.

For instance forecasting and budgeting techniques can be used for making any plan regarding

any future projects. Management can estimate the total expenditure which is to be made on that

specific project further they can also ascertain the revenue that can be earned through this project

(Baldvinsdottir Mitchell and Nørreklit, 2010). This report is based on the case study of Agmet

which is a small business entity which is employing less than 50 employees and having an

annual net turnover of less than £500,000. This means that in this file it has been mentioned that

how small business enterprises having less resources i.e. financial and non financial both, can

achieve their predetermined criteria and goals. Other than this, in this report there have been

mentioned several methods of management accounting which can be used by the cited entity for

the management of their sources in an effective way so that the owners and the managerial

personnels can manage and exploit the available opportunities.

TASK 1

P1 Management accounting and its types for Agmet:

Report

To General manager,

This is to inform you that company is using old management accounting techniques which are

stale now. So, there is a need to replace them all in order to get the competitive advantages in an

effective manner. However, this also been cited that advantages and limitations of MA system

going to be focused over here. A variety of management accounting principles are present

which shall be utilised by an entity for the management and control of its financial and non

financial sources so that these sources can yield positive result in reference of its

operations(Bennett, Schaltegger and Zvezdov, 2013). This can be classified as the bond of two

subjects from different fields out of which one is financial accounting and other one is

management and its principles to manage the work of organisation or it can be said that through

the information from financial accounting and its data managerial personnels can optimize such

1

Management accounting can be specified as the method that has the quality of both

financial system and managerial principle therefore this can be said that these principles of

management accounting can be used by the management for decision making process. This

report contains various concepts about the management accounting and its associated techniques.

For instance forecasting and budgeting techniques can be used for making any plan regarding

any future projects. Management can estimate the total expenditure which is to be made on that

specific project further they can also ascertain the revenue that can be earned through this project

(Baldvinsdottir Mitchell and Nørreklit, 2010). This report is based on the case study of Agmet

which is a small business entity which is employing less than 50 employees and having an

annual net turnover of less than £500,000. This means that in this file it has been mentioned that

how small business enterprises having less resources i.e. financial and non financial both, can

achieve their predetermined criteria and goals. Other than this, in this report there have been

mentioned several methods of management accounting which can be used by the cited entity for

the management of their sources in an effective way so that the owners and the managerial

personnels can manage and exploit the available opportunities.

TASK 1

P1 Management accounting and its types for Agmet:

Report

To General manager,

This is to inform you that company is using old management accounting techniques which are

stale now. So, there is a need to replace them all in order to get the competitive advantages in an

effective manner. However, this also been cited that advantages and limitations of MA system

going to be focused over here. A variety of management accounting principles are present

which shall be utilised by an entity for the management and control of its financial and non

financial sources so that these sources can yield positive result in reference of its

operations(Bennett, Schaltegger and Zvezdov, 2013). This can be classified as the bond of two

subjects from different fields out of which one is financial accounting and other one is

management and its principles to manage the work of organisation or it can be said that through

the information from financial accounting and its data managerial personnels can optimize such

1

data in the process of decision making(Busco and Scapens, 2011). As through using such

techniques which are supported through some reliable figures then it gets easier for the

management to frame such strategies which can generate better and improved results in

comparison with the techniques which different from the methods of management accounting.

Their are different accounting techniques which can be used by the organisation for carrying on

their organisational activities in a way in which they can utilize their sources for the production

of accurate outcomes as per the desire of their customers and as per the needs of their

organisational structure (Christ and Burritt, 2013). There are various essential requirements in

reference of management accounting. Such essential requirements provide more benefits to the

entity as through this the credibility of information ascertained can be utilized with assurance as

they are credible and reliable. Hence for making financial reporting more appropriate financial

accounting follows the principles of International financial reporting frame work and

management accounting requires to fulfil the requirements which are mentioned below:

Cost Accounting: It can be termed as a control tool for the changes that are made in the

accounting system and control. Measurement of any quantity or price if changes then

through this technique management can cop up with the such changes. Management

needs to face the situations where there is less resources available and as Agmet is a

small business enterprise hence it requires to maintain its limited financial and non

financial sources in a way so that they can generate the best revenue which is desired by

enterprise and the operations which is carried out by it.

Job costing system: This is the MA system which is used by the firm in order to make

their business operations so effective. With the help of this, management accountant

can make lower the cost of product by effectively applying the cost cost accounting

technique.

Inventory management system: this is the system which is used by the firm in order

to control the inventory and other operational expenses so that the firm could attain

business objectives.

Price optimization system: Under this system, company's management accountant fix

the standard for a product so that the potential consumer is able to buy the product in an

effective manner.

2

techniques which are supported through some reliable figures then it gets easier for the

management to frame such strategies which can generate better and improved results in

comparison with the techniques which different from the methods of management accounting.

Their are different accounting techniques which can be used by the organisation for carrying on

their organisational activities in a way in which they can utilize their sources for the production

of accurate outcomes as per the desire of their customers and as per the needs of their

organisational structure (Christ and Burritt, 2013). There are various essential requirements in

reference of management accounting. Such essential requirements provide more benefits to the

entity as through this the credibility of information ascertained can be utilized with assurance as

they are credible and reliable. Hence for making financial reporting more appropriate financial

accounting follows the principles of International financial reporting frame work and

management accounting requires to fulfil the requirements which are mentioned below:

Cost Accounting: It can be termed as a control tool for the changes that are made in the

accounting system and control. Measurement of any quantity or price if changes then

through this technique management can cop up with the such changes. Management

needs to face the situations where there is less resources available and as Agmet is a

small business enterprise hence it requires to maintain its limited financial and non

financial sources in a way so that they can generate the best revenue which is desired by

enterprise and the operations which is carried out by it.

Job costing system: This is the MA system which is used by the firm in order to make

their business operations so effective. With the help of this, management accountant

can make lower the cost of product by effectively applying the cost cost accounting

technique.

Inventory management system: this is the system which is used by the firm in order

to control the inventory and other operational expenses so that the firm could attain

business objectives.

Price optimization system: Under this system, company's management accountant fix

the standard for a product so that the potential consumer is able to buy the product in an

effective manner.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P2 Explanation over the different methods used for management accounting reporting

Budget report: Budget report helps every type of business enterprise whether is is small

or big to make an estimation of all the expanses happen in their business and at the same

time allocate the funds according to them. Budget reports helps the enterprise to cut down

the cost of every operation of the enterprise(Hiebl, 2014). Budget help the manager of a

small business enterprise in in analysing the performance of his department. When a

organisation is very big than the budget is made according to the department.

Consultation from all the head of the department is taken and than added in the budget

(Ward, 2012). For achieving better results a proper budget should be made according to

the all needs of the department and proper fund should be allocated to them. Budget

report helps in making optimum utilisation of the fund available to the firm. It analysing

all the needs of the enterprise and then allocate the fund to them. Budget report help the

enterprise in making effective decision.

Accounts receivables reports: Accounts receivable helps the enterprise in checking all

the activities related to the inflow and outflow of the fund(Jansen, 2011). It helps the

management of the enterprise to do regular changes or some modifications in the

collecting policy of the enterprise to make it more effective and to collect the funds more

faster from the customers. Accounts receivable helps the enterprise in collecting its funds

from the customers at a faster speed and tries that the debtors of the enterprise should not

be converted into bad debts.

Job cost reports: Job cost is one of the important part of accounting system. It helps in

calculating the profitability generating from each job(Kaplan and Atkinson, 2015). The

main aim of this is to calculate that which job is creating more revenue to the firm or

which job is more profitable, after studying or calculating the profitability related with

each job the managers can give their more attention to the jobs producing more revenue

for the enterprise and at the same time the jobs which are not creating more revenues for

the enterprise can be eliminated by the management of the enterprise .

Inventory management reporting: Inventory and manufacturing is one of the another

more important component of account reporting(Lee, 2011). The main function of this

3

Budget report: Budget report helps every type of business enterprise whether is is small

or big to make an estimation of all the expanses happen in their business and at the same

time allocate the funds according to them. Budget reports helps the enterprise to cut down

the cost of every operation of the enterprise(Hiebl, 2014). Budget help the manager of a

small business enterprise in in analysing the performance of his department. When a

organisation is very big than the budget is made according to the department.

Consultation from all the head of the department is taken and than added in the budget

(Ward, 2012). For achieving better results a proper budget should be made according to

the all needs of the department and proper fund should be allocated to them. Budget

report helps in making optimum utilisation of the fund available to the firm. It analysing

all the needs of the enterprise and then allocate the fund to them. Budget report help the

enterprise in making effective decision.

Accounts receivables reports: Accounts receivable helps the enterprise in checking all

the activities related to the inflow and outflow of the fund(Jansen, 2011). It helps the

management of the enterprise to do regular changes or some modifications in the

collecting policy of the enterprise to make it more effective and to collect the funds more

faster from the customers. Accounts receivable helps the enterprise in collecting its funds

from the customers at a faster speed and tries that the debtors of the enterprise should not

be converted into bad debts.

Job cost reports: Job cost is one of the important part of accounting system. It helps in

calculating the profitability generating from each job(Kaplan and Atkinson, 2015). The

main aim of this is to calculate that which job is creating more revenue to the firm or

which job is more profitable, after studying or calculating the profitability related with

each job the managers can give their more attention to the jobs producing more revenue

for the enterprise and at the same time the jobs which are not creating more revenues for

the enterprise can be eliminated by the management of the enterprise .

Inventory management reporting: Inventory and manufacturing is one of the another

more important component of account reporting(Lee, 2011). The main function of this

3

report is to check the inventory of the organisation and at the same time to maintain a

optimum level of stock in the enterprise (Van Helden and et. al., 2010). It is the

responsibility of inventory manager to always maintain a level of inventory which helps

the enterprise in achieving its objectives more easily. Both under and over stock will give

birth problems in the enterprise like if there is a under stock of an inventory than it will

makes enterprise unable to meet the delivery schedules of the customers on the other

hand over stock of inventory will cost more to the enterprise like storage cost and other.

So the level of the inventory should be in an optimum level.

M1 Benefits of management accounting systems and their application within Agmet

Management accounting system provide several benefits to the Agmet. There are certain

principles of management accounting which provides credibility and reliability to the enterprise

then it may be possible for the entity to cover the information in a more appropriate way so that

the stakeholders can make their decisions in a better and improved way. The system of

management accounting helps in effective decision making as through accounting systems

quality information is received. If in the given organisations judgement are taken on the basis of

data presented through this systems much cost can be saved and profitability of an enterprise

will improve. There are certain other advantage of management accounting system which are

sued which are enlisted below:

Reduction in cost of enterprise: The cost associated with the production and other

activities can be explained as the cost which is there in production of any goods and

services(Fullerton, Kennedy and Widener, 2014). Business owners mostly use

management accounting techniques for the cost control and cost reduction.

Improvement in cash flow: Through using cost accounting techniques the cash flow of

Agmet can be improved easily (Håkansson, Kraus and Lind eds., 2010).

Improvement in fun flow: Through management accounting techniques the fund flow of

any enterprise can be managed in a way in which they have control over such flow of

funds.

Assist in business decision making: Techniques of management accounting can assist any

entity for the decision making process as they have some credible information related

with the accounting data and they can apply managerial principles over it further through

4

optimum level of stock in the enterprise (Van Helden and et. al., 2010). It is the

responsibility of inventory manager to always maintain a level of inventory which helps

the enterprise in achieving its objectives more easily. Both under and over stock will give

birth problems in the enterprise like if there is a under stock of an inventory than it will

makes enterprise unable to meet the delivery schedules of the customers on the other

hand over stock of inventory will cost more to the enterprise like storage cost and other.

So the level of the inventory should be in an optimum level.

M1 Benefits of management accounting systems and their application within Agmet

Management accounting system provide several benefits to the Agmet. There are certain

principles of management accounting which provides credibility and reliability to the enterprise

then it may be possible for the entity to cover the information in a more appropriate way so that

the stakeholders can make their decisions in a better and improved way. The system of

management accounting helps in effective decision making as through accounting systems

quality information is received. If in the given organisations judgement are taken on the basis of

data presented through this systems much cost can be saved and profitability of an enterprise

will improve. There are certain other advantage of management accounting system which are

sued which are enlisted below:

Reduction in cost of enterprise: The cost associated with the production and other

activities can be explained as the cost which is there in production of any goods and

services(Fullerton, Kennedy and Widener, 2014). Business owners mostly use

management accounting techniques for the cost control and cost reduction.

Improvement in cash flow: Through using cost accounting techniques the cash flow of

Agmet can be improved easily (Håkansson, Kraus and Lind eds., 2010).

Improvement in fun flow: Through management accounting techniques the fund flow of

any enterprise can be managed in a way in which they have control over such flow of

funds.

Assist in business decision making: Techniques of management accounting can assist any

entity for the decision making process as they have some credible information related

with the accounting data and they can apply managerial principles over it further through

4

this they can apply various various methods through which they can take decision inn

favour of organisation (Herbert and Seal, 2012).

D1 Management accounting systems and its reporting is integrated within organisational

processes:

In the process of management accounting system, the employees of the company have to

do proper learning as well as transformation(Luft and Shields, 2010). They have to do the

interaction between the accounting system as well as they have to take initiative for the

implementation of Six Sigma. Along with this system of accounting helps in managing the

changes which needs to be done in Agmet. It helps in doing the continuous process of the

transformation so that they can infuse the organisational culture with the financial and non

financial metrics of accountability. To attain the sustainable success in the organisation,

employees have to use the appropriate strategies, models along with the practices so that they

provide proper response to the social and environmental challenges and on the basis of this they

can create a financial success as well as values for the shareholders. The staff members along

with the managers have to develop Key Performance Indicator have to provide appropriate

support so that they can accomplish the strategic and sustainable goals. Implementation of

accounting systems will help in developing efficiency in the workforce as their work will be

assessed on the basis of data received.

TASK 2

P3,M2 & D2 Calculation of cost using techniques of absorption and marginal costing

Selling price per unit £35

Unit costs

Direct materials cost £6

Direct Labour cost £5

Variable Production overhead expenditures £2

Variable sales overhead expenditures £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Standard cost Actual cost

Production overhead expenditure £1,800 £2,000

5

favour of organisation (Herbert and Seal, 2012).

D1 Management accounting systems and its reporting is integrated within organisational

processes:

In the process of management accounting system, the employees of the company have to

do proper learning as well as transformation(Luft and Shields, 2010). They have to do the

interaction between the accounting system as well as they have to take initiative for the

implementation of Six Sigma. Along with this system of accounting helps in managing the

changes which needs to be done in Agmet. It helps in doing the continuous process of the

transformation so that they can infuse the organisational culture with the financial and non

financial metrics of accountability. To attain the sustainable success in the organisation,

employees have to use the appropriate strategies, models along with the practices so that they

provide proper response to the social and environmental challenges and on the basis of this they

can create a financial success as well as values for the shareholders. The staff members along

with the managers have to develop Key Performance Indicator have to provide appropriate

support so that they can accomplish the strategic and sustainable goals. Implementation of

accounting systems will help in developing efficiency in the workforce as their work will be

assessed on the basis of data received.

TASK 2

P3,M2 & D2 Calculation of cost using techniques of absorption and marginal costing

Selling price per unit £35

Unit costs

Direct materials cost £6

Direct Labour cost £5

Variable Production overhead expenditures £2

Variable sales overhead expenditures £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Standard cost Actual cost

Production overhead expenditure £1,800 £2,000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

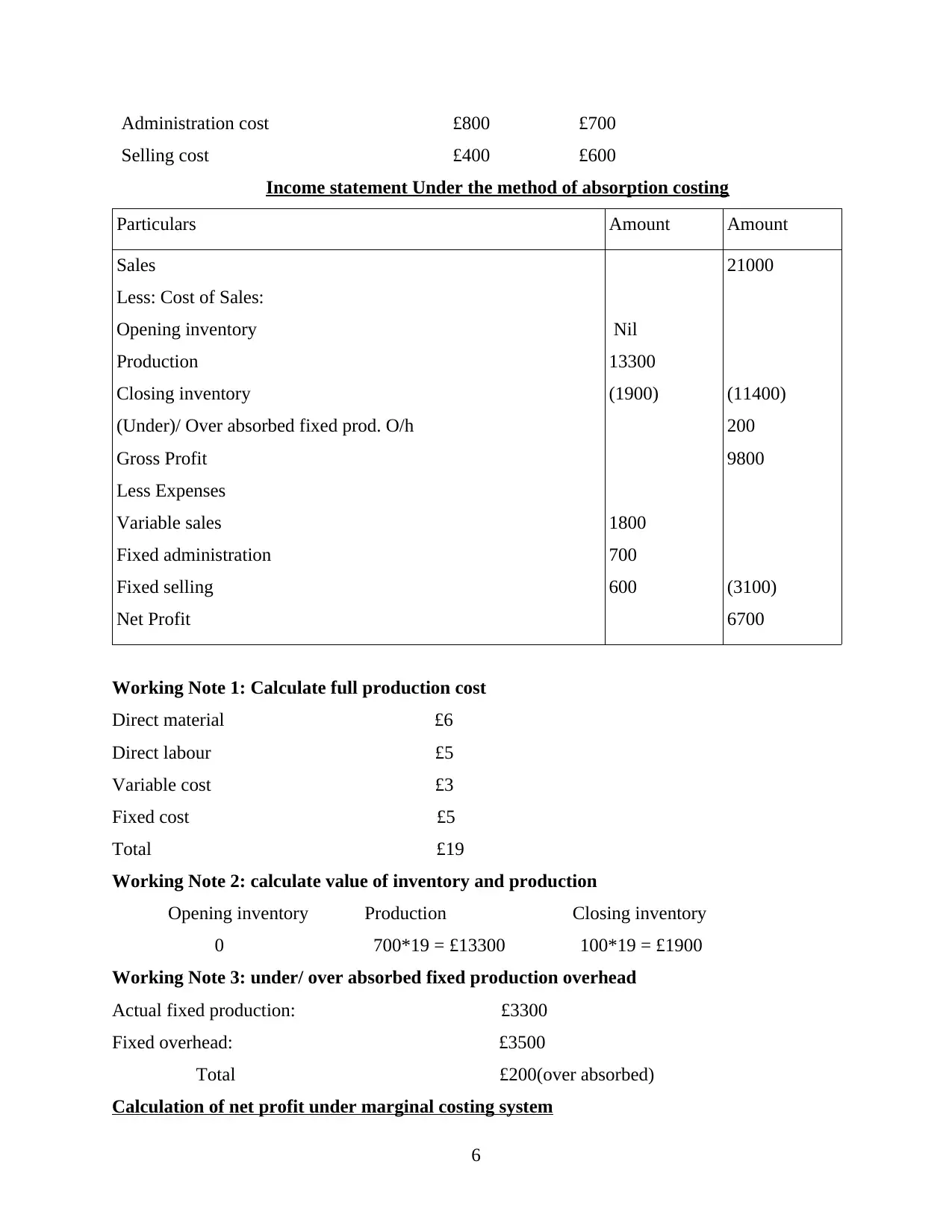

Administration cost £800 £700

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Calculation of net profit under marginal costing system

6

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Calculation of net profit under marginal costing system

6

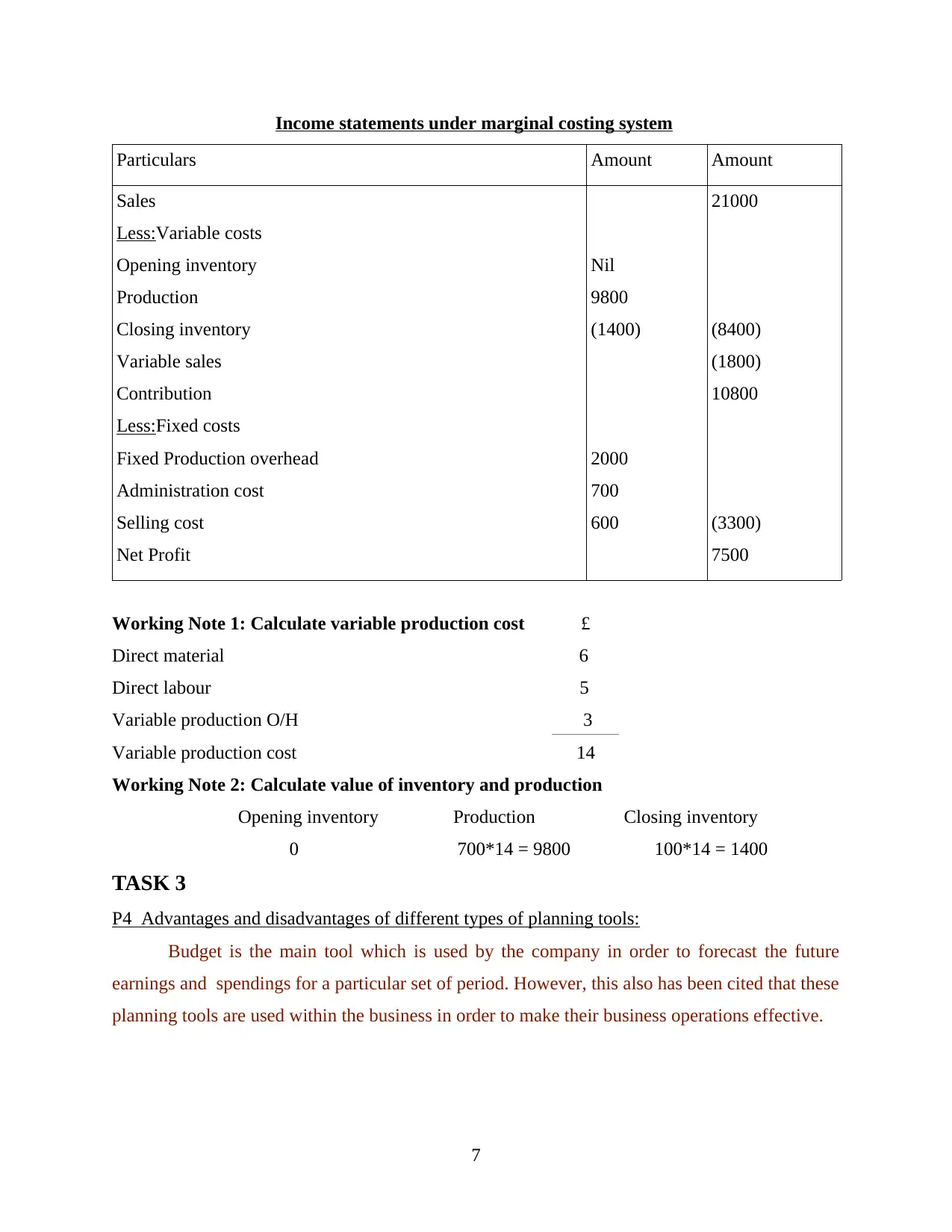

Income statements under marginal costing system

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

TASK 3

P4 Advantages and disadvantages of different types of planning tools:

Budget is the main tool which is used by the company in order to forecast the future

earnings and spendings for a particular set of period. However, this also has been cited that these

planning tools are used within the business in order to make their business operations effective.

7

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

TASK 3

P4 Advantages and disadvantages of different types of planning tools:

Budget is the main tool which is used by the company in order to forecast the future

earnings and spendings for a particular set of period. However, this also has been cited that these

planning tools are used within the business in order to make their business operations effective.

7

Cash budget: This is the budget which is used by the firm in order to assess the actual cash

inflows and cash outflows in order to make their business operations effective for a particular

period of time.

Capital expenditure budget: Under this budget, capital related expenditures are recorded in

order to make their business operations effective and optimize the resources.

Cost plus pricing budget: Under this planning tool, cost plus pricing budget is taken so that the

company would frame cost plus pricing strategy in an effective manner for a particular set of

period.

Master Budget: The easiest way to forecast the performance of the business is to create a

master budget based on the recent performance of the company. The financial document provide

a one time references of how the business will be doing in the coming year based on the future

Forecasting techniques (Quinn, 2011). Master budget helps to discuss the key factors and

anticipate the performance of the new product and the services. It is basically the aggregation of

all the lower budgets produced by a company various functional area and also includes budgeted

financial statement, cash forecast and a financing plan and master budget is mainly presented in

monthly or quarterly format and usually covers a company entire fiscal policy.

There are some advantages and disadvantages as well that can come across by the firm in

order to make operations effective. Some of the advantages of planning tools are:

Coordination-Budgets coordinate the activities across different department and this

helps to keep a link between the activities and thus the flow of activities is maintained in

the organisation.

Strategic Plans: Budget translate the strategic plans into action (Nandan, 2010). They

specify the resources used in the organisation the revenues generated and the activities

required to carry out the specific plans for the coming years.

Records Keeping: Budgets provides an excellent indicator of keeping the records of all

the activities taking place in the organisation and these record helps to keep a track on the

overall activities of the organisation.

Communication: Budgetary tools helps to communicate with the employees so that the

budget can be communicated in advance with the employees of the organisation and this

helps in future planning of budget.

8

inflows and cash outflows in order to make their business operations effective for a particular

period of time.

Capital expenditure budget: Under this budget, capital related expenditures are recorded in

order to make their business operations effective and optimize the resources.

Cost plus pricing budget: Under this planning tool, cost plus pricing budget is taken so that the

company would frame cost plus pricing strategy in an effective manner for a particular set of

period.

Master Budget: The easiest way to forecast the performance of the business is to create a

master budget based on the recent performance of the company. The financial document provide

a one time references of how the business will be doing in the coming year based on the future

Forecasting techniques (Quinn, 2011). Master budget helps to discuss the key factors and

anticipate the performance of the new product and the services. It is basically the aggregation of

all the lower budgets produced by a company various functional area and also includes budgeted

financial statement, cash forecast and a financing plan and master budget is mainly presented in

monthly or quarterly format and usually covers a company entire fiscal policy.

There are some advantages and disadvantages as well that can come across by the firm in

order to make operations effective. Some of the advantages of planning tools are:

Coordination-Budgets coordinate the activities across different department and this

helps to keep a link between the activities and thus the flow of activities is maintained in

the organisation.

Strategic Plans: Budget translate the strategic plans into action (Nandan, 2010). They

specify the resources used in the organisation the revenues generated and the activities

required to carry out the specific plans for the coming years.

Records Keeping: Budgets provides an excellent indicator of keeping the records of all

the activities taking place in the organisation and these record helps to keep a track on the

overall activities of the organisation.

Communication: Budgetary tools helps to communicate with the employees so that the

budget can be communicated in advance with the employees of the organisation and this

helps in future planning of budget.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Resource Allocation: Budget improves resource allocation because the resources are

efficiently and effectively utilised because all the request are clarified and justified.

While on the other hand, this has been argued that these planning tools sometimes,

creates drawbacks as well that is produced in the firm. Some of the drawbacks are mentioned

hereunder:

Application: The leading issue arises at the time of planning of budgets and when they

are applied practically as rigid and thud budget can cause perception of fairness.

Lack of Participation: System of budgeting can develop negative feelings among the

employees as there is lack of participation of employees and if the budgets are forcefully

implemented from the top to the down authority than the employees will find it difficult

to follow budgetary expenditure and thus these expenditure will not be communicated to

them(Pipan and Czarniawska, 2010).

Competition: Budgets can create competition of the resources and the politics of the

organisation and thus it is the main drawback of budget formation(van der Meer-Kooistra

and Vosselman, 2012).

Rigid Budget Structure: The rigid structure of the budget reduces the initiative that

management takes to plan a program at the lower levels that makes it difficult to obtain

money for the new ideas generated.

Coercive: Budget are coercive and although the control is important,good management

should able to control and motivate the workforce without restoring to coercive. Budgets

are always bureaucratic means it relates to a government system in which most of the

decisions are taken by the state government rather than the representatives

M3 Different planning tools and their application for preparing and forecasting budgets:

There are various planning tools which can be used by the firm in order to assess the firm

forecasted budgets. These are the under mentioned technique that can be used by the firm in

order to frame budget. These are:

Real Time Projection Technique: This technique projects the annual performance using

the data as it occurs it allow us to see the data more accurately according to the projects

and the years on which the data has been collected (Talha, Raja and Seetharaman, 2010).

Example: Using the sales figures of the first four month a person might be more

accurately project year end totals than the statistical master budget.

9

efficiently and effectively utilised because all the request are clarified and justified.

While on the other hand, this has been argued that these planning tools sometimes,

creates drawbacks as well that is produced in the firm. Some of the drawbacks are mentioned

hereunder:

Application: The leading issue arises at the time of planning of budgets and when they

are applied practically as rigid and thud budget can cause perception of fairness.

Lack of Participation: System of budgeting can develop negative feelings among the

employees as there is lack of participation of employees and if the budgets are forcefully

implemented from the top to the down authority than the employees will find it difficult

to follow budgetary expenditure and thus these expenditure will not be communicated to

them(Pipan and Czarniawska, 2010).

Competition: Budgets can create competition of the resources and the politics of the

organisation and thus it is the main drawback of budget formation(van der Meer-Kooistra

and Vosselman, 2012).

Rigid Budget Structure: The rigid structure of the budget reduces the initiative that

management takes to plan a program at the lower levels that makes it difficult to obtain

money for the new ideas generated.

Coercive: Budget are coercive and although the control is important,good management

should able to control and motivate the workforce without restoring to coercive. Budgets

are always bureaucratic means it relates to a government system in which most of the

decisions are taken by the state government rather than the representatives

M3 Different planning tools and their application for preparing and forecasting budgets:

There are various planning tools which can be used by the firm in order to assess the firm

forecasted budgets. These are the under mentioned technique that can be used by the firm in

order to frame budget. These are:

Real Time Projection Technique: This technique projects the annual performance using

the data as it occurs it allow us to see the data more accurately according to the projects

and the years on which the data has been collected (Talha, Raja and Seetharaman, 2010).

Example: Using the sales figures of the first four month a person might be more

accurately project year end totals than the statistical master budget.

9

Overhead Projection: the cost of producing an extra unit of output is known as overhead

cost and it accurately counts the profits on each projects that are made in addition to the

cost of the project the overheads must be considered as a part of selling expenses(Renz,

2016).All the overhead cost are identified such as rent, insurance, utilities, phone, office

staff and marketing to define the total overhead cost to the company and the procedure to

calculate the overhead cost is we divide the total number of the units produce to

determine the overhead cost per unit(Why lean accounting?. 2017).

Multiple Scenarios:This technique is used to project the different types of sales activity

and the different prices that will affect the budget (Vaivio and Sirén, 2010). The team

members anticipate on the recent project and find out the market conditions to create a

new project. This will make a person aware about the place where the adjustments have

to be made to make the budgets accurate adjust according to the sales to reflect the prices

of the product .This will help us to know the project sales,profit and margin changes.

Example: If three different types of sales are used in the organisation than the budget will be

made according to the sales technique which is used to make the budget.

D3 Planning tools used for responding financial problems:

Planning tools that leads to organisation success means that the organisation should

sustain its policies for future growth and development of the organisation(Sánchez-Rodríguez

and Spraakman, 2012). It should be preserved so that it does not hampers the resources of the

organisation and maintain its sustainability for the long term. It should promote the

understanding of how effects made at the local level can improve the quality of environment, the

economy and the quality of the citizens. Increase insight in strategies for climate change adaption

and mitigation of the economy. Enhance appreciation of the project environment and create

value. Planning to think about the ways to integrate sustainability development principles in the

municipal policy process and assess design smart action plans (Significance of Management

Accounting Techniques in Decision-making: An Empirical Study on Manufacturing

Organizations in Bangladesh, 2011). Provide tools to enables for participation of the partnership

with various stakeholders of the company in the public and the private sector via dialogues and

priority setting.

10

cost and it accurately counts the profits on each projects that are made in addition to the

cost of the project the overheads must be considered as a part of selling expenses(Renz,

2016).All the overhead cost are identified such as rent, insurance, utilities, phone, office

staff and marketing to define the total overhead cost to the company and the procedure to

calculate the overhead cost is we divide the total number of the units produce to

determine the overhead cost per unit(Why lean accounting?. 2017).

Multiple Scenarios:This technique is used to project the different types of sales activity

and the different prices that will affect the budget (Vaivio and Sirén, 2010). The team

members anticipate on the recent project and find out the market conditions to create a

new project. This will make a person aware about the place where the adjustments have

to be made to make the budgets accurate adjust according to the sales to reflect the prices

of the product .This will help us to know the project sales,profit and margin changes.

Example: If three different types of sales are used in the organisation than the budget will be

made according to the sales technique which is used to make the budget.

D3 Planning tools used for responding financial problems:

Planning tools that leads to organisation success means that the organisation should

sustain its policies for future growth and development of the organisation(Sánchez-Rodríguez

and Spraakman, 2012). It should be preserved so that it does not hampers the resources of the

organisation and maintain its sustainability for the long term. It should promote the

understanding of how effects made at the local level can improve the quality of environment, the

economy and the quality of the citizens. Increase insight in strategies for climate change adaption

and mitigation of the economy. Enhance appreciation of the project environment and create

value. Planning to think about the ways to integrate sustainability development principles in the

municipal policy process and assess design smart action plans (Significance of Management

Accounting Techniques in Decision-making: An Empirical Study on Manufacturing

Organizations in Bangladesh, 2011). Provide tools to enables for participation of the partnership

with various stakeholders of the company in the public and the private sector via dialogues and

priority setting.

10

TASK 4

P5 Comparison how organisations are adapting management accounting systems to respond to

financial problems

MA system and its various tools are helpful for acting in various financial and non-

financial issues (Setthasakko, 2010). It renders the entity a platform for the sustainable

development so the resources can be secured for the future use. Thus, they could get the

efficiency in the economy in order to make the economy sustainable for long run in the

organisation.

There are certain tools which can be used by the firm in order to address financial problems

culture in a most effective manner. Some of them are as follows:

Key performance indicator: This helps the firm to assess the performance of financial

information so that these business can run for a long time. With the help of this, company would

able to measure quantifiable value which is used by the firm in order to assess the success of a

firm, employee.

Benchmarking: This is the tool which is used by the firm in order to assess the financial

problems. With the help of benchmarking, compare its operational performance metrics to

industry best practices from other firms or industry. So that they could get to know the real

problems which arise in the business and also make certain treatments in order to make their

business operations effective.

The comparison study between the two company which are implementing the management

technique to respond to the financial problems are:

Unicorn Grocery Agmet

This tool is implemented to regulate the future

affairs of budgeting these are used to specific

investment plans for future.

It can also be used to compare the differences

between the standard and the actual data

required by the organisation and helps to detect

the problems.

Cited entity is using capital budgetary

This technique is implemented to point out the

total amount needs to be invested in a project

by the firm.

It is a kind of method which demonstrates the

optimum capital requirement a manager could

implement under the actual outcome which

they want through employing their cost

effective and efficient financial resources in

11

P5 Comparison how organisations are adapting management accounting systems to respond to

financial problems

MA system and its various tools are helpful for acting in various financial and non-

financial issues (Setthasakko, 2010). It renders the entity a platform for the sustainable

development so the resources can be secured for the future use. Thus, they could get the

efficiency in the economy in order to make the economy sustainable for long run in the

organisation.

There are certain tools which can be used by the firm in order to address financial problems

culture in a most effective manner. Some of them are as follows:

Key performance indicator: This helps the firm to assess the performance of financial

information so that these business can run for a long time. With the help of this, company would

able to measure quantifiable value which is used by the firm in order to assess the success of a

firm, employee.

Benchmarking: This is the tool which is used by the firm in order to assess the financial

problems. With the help of benchmarking, compare its operational performance metrics to

industry best practices from other firms or industry. So that they could get to know the real

problems which arise in the business and also make certain treatments in order to make their

business operations effective.

The comparison study between the two company which are implementing the management

technique to respond to the financial problems are:

Unicorn Grocery Agmet

This tool is implemented to regulate the future

affairs of budgeting these are used to specific

investment plans for future.

It can also be used to compare the differences

between the standard and the actual data

required by the organisation and helps to detect

the problems.

Cited entity is using capital budgetary

This technique is implemented to point out the

total amount needs to be invested in a project

by the firm.

It is a kind of method which demonstrates the

optimum capital requirement a manager could

implement under the actual outcome which

they want through employing their cost

effective and efficient financial resources in

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

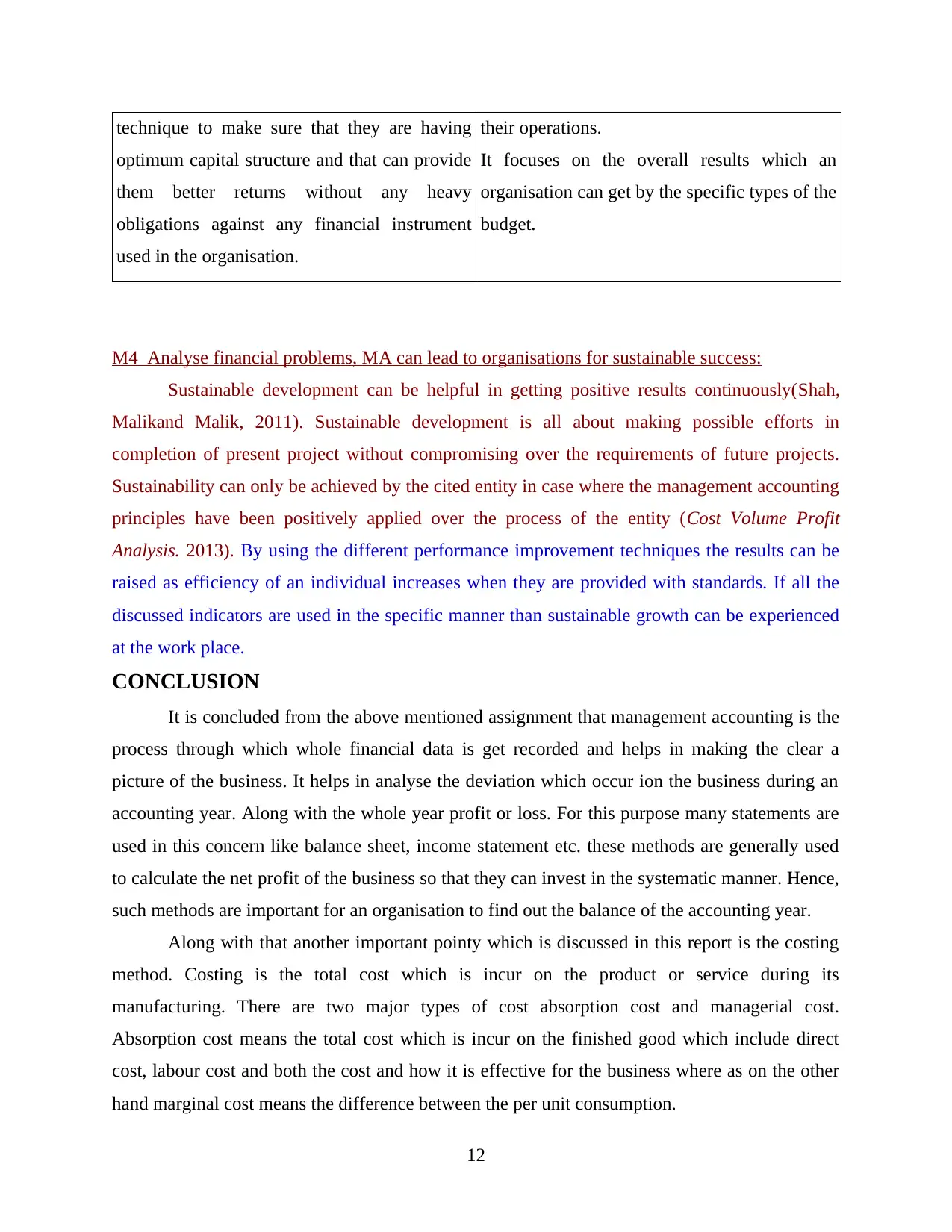

technique to make sure that they are having

optimum capital structure and that can provide

them better returns without any heavy

obligations against any financial instrument

used in the organisation.

their operations.

It focuses on the overall results which an

organisation can get by the specific types of the

budget.

M4 Analyse financial problems, MA can lead to organisations for sustainable success:

Sustainable development can be helpful in getting positive results continuously(Shah,

Malikand Malik, 2011). Sustainable development is all about making possible efforts in

completion of present project without compromising over the requirements of future projects.

Sustainability can only be achieved by the cited entity in case where the management accounting

principles have been positively applied over the process of the entity (Cost Volume Profit

Analysis. 2013). By using the different performance improvement techniques the results can be

raised as efficiency of an individual increases when they are provided with standards. If all the

discussed indicators are used in the specific manner than sustainable growth can be experienced

at the work place.

CONCLUSION

It is concluded from the above mentioned assignment that management accounting is the

process through which whole financial data is get recorded and helps in making the clear a

picture of the business. It helps in analyse the deviation which occur ion the business during an

accounting year. Along with the whole year profit or loss. For this purpose many statements are

used in this concern like balance sheet, income statement etc. these methods are generally used

to calculate the net profit of the business so that they can invest in the systematic manner. Hence,

such methods are important for an organisation to find out the balance of the accounting year.

Along with that another important pointy which is discussed in this report is the costing

method. Costing is the total cost which is incur on the product or service during its

manufacturing. There are two major types of cost absorption cost and managerial cost.

Absorption cost means the total cost which is incur on the finished good which include direct

cost, labour cost and both the cost and how it is effective for the business where as on the other

hand marginal cost means the difference between the per unit consumption.

12

optimum capital structure and that can provide

them better returns without any heavy

obligations against any financial instrument

used in the organisation.

their operations.

It focuses on the overall results which an

organisation can get by the specific types of the

budget.

M4 Analyse financial problems, MA can lead to organisations for sustainable success:

Sustainable development can be helpful in getting positive results continuously(Shah,

Malikand Malik, 2011). Sustainable development is all about making possible efforts in

completion of present project without compromising over the requirements of future projects.

Sustainability can only be achieved by the cited entity in case where the management accounting

principles have been positively applied over the process of the entity (Cost Volume Profit

Analysis. 2013). By using the different performance improvement techniques the results can be

raised as efficiency of an individual increases when they are provided with standards. If all the

discussed indicators are used in the specific manner than sustainable growth can be experienced

at the work place.

CONCLUSION

It is concluded from the above mentioned assignment that management accounting is the

process through which whole financial data is get recorded and helps in making the clear a

picture of the business. It helps in analyse the deviation which occur ion the business during an

accounting year. Along with the whole year profit or loss. For this purpose many statements are

used in this concern like balance sheet, income statement etc. these methods are generally used

to calculate the net profit of the business so that they can invest in the systematic manner. Hence,

such methods are important for an organisation to find out the balance of the accounting year.

Along with that another important pointy which is discussed in this report is the costing

method. Costing is the total cost which is incur on the product or service during its

manufacturing. There are two major types of cost absorption cost and managerial cost.

Absorption cost means the total cost which is incur on the finished good which include direct

cost, labour cost and both the cost and how it is effective for the business where as on the other

hand marginal cost means the difference between the per unit consumption.

12

REFERENCES

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability. (pp. 1-56). London: ICAEW.

Busco, C. and Scapens, R.W., 2011. Management accounting systems and organisational culture:

Interpreting their linkages and processes of change. Qualitative Research in Accounting

& Management. 8(4). pp.320-357.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting: the significance of

contingent variables for adoption. Journal of Cleaner Production. 41. pp.163-173.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a

loose coupling?. Journal of Accounting & organizational change. 6(2). pp.228-259.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research.

24(4). pp.349-365.

Dillard, J. and Roslender, R., 2011. Taking pluralism seriously: embedded moralities in

management accounting and control systems. Critical Perspectives on Accounting.

22(2). pp.135-147.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices.

Journal of Operations Management. 32(7). pp.414-428.

Håkansson, H., Kraus, K. and Lind, J. eds., 2010. Accounting in networks. Routledge.

Herbert, I.P and Seal, W.B., 2012. Shared services as a new organisational form: Some

implications for management accounting. The British Accounting Review. 44(2). pp.83-

97.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Jansen, E. P., 2011. The effect of leadership style on the information receivers’ reaction to

management accounting change. Management Accounting Research. 22(2). pp.105-124.

Kaplan, R. S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

13

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability. (pp. 1-56). London: ICAEW.

Busco, C. and Scapens, R.W., 2011. Management accounting systems and organisational culture:

Interpreting their linkages and processes of change. Qualitative Research in Accounting

& Management. 8(4). pp.320-357.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting: the significance of

contingent variables for adoption. Journal of Cleaner Production. 41. pp.163-173.

Cinquini, L. and Tenucci, A., 2010. Strategic management accounting and business strategy: a

loose coupling?. Journal of Accounting & organizational change. 6(2). pp.228-259.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research.

24(4). pp.349-365.

Dillard, J. and Roslender, R., 2011. Taking pluralism seriously: embedded moralities in

management accounting and control systems. Critical Perspectives on Accounting.

22(2). pp.135-147.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices.

Journal of Operations Management. 32(7). pp.414-428.

Håkansson, H., Kraus, K. and Lind, J. eds., 2010. Accounting in networks. Routledge.

Herbert, I.P and Seal, W.B., 2012. Shared services as a new organisational form: Some

implications for management accounting. The British Accounting Review. 44(2). pp.83-

97.

Hiebl, M. R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Jansen, E. P., 2011. The effect of leadership style on the information receivers’ reaction to

management accounting change. Management Accounting Research. 22(2). pp.105-124.

Kaplan, R. S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

13

Lee, K.H., 2011. Motivations, barriers, and incentives for adopting environmental management

(cost) accounting and related guidelines: a study of the Republic of Korea. Corporate

Social Responsibility and Environmental Management. 18(1). pp.39-49.

Luft, J and Shields, M. D., 2010. Psychology models of management accounting. Foundations

and Trends® in Accounting. 4(3–4). pp.199-345.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Macintosh, N. B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional

accountants: A renewed research agenda. Journal of applied management accounting

research. 8(1). p.65.

Pipan, T. and Czarniawska, B., 2010. How to construct an actor-network: Management

accounting from idea to practice. Critical Perspectives on Accounting. 21(3). pp.243-

251.

Quinn, M., 2011. Routines in management accounting research: further exploration. Journal of

Accounting & Organizational Change. 7(4). pp.337-357.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Sánchez-Rodríguez, C. and Spraakman, G., 2012. ERP systems and management accounting: A

multiple case study. Qualitative Research in Accounting & Management. 9(4). pp.398-

414.

Setthasakko, W., 2010. Barriers to the development of environmental management accounting:

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business. 5(3). pp.315-331.

Shah, H., Malik, A. and Malik, M.S., 2011. Strategic Management Accounting-A Messiah For

Management Accounting?. Australian Journal of Business and Management Research.

1(4). p.1.

Talha, M., Raja, J.B. and Seetharaman, A., 2010. A new look at management accounting.

Journal of Applied Business Research. 26(4). p.83.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

van der Meer-Kooistra, J. and Vosselman, E., 2012. Research paradigms, theoretical pluralism

and the practical relevance of management accounting knowledge. Qualitative Research

in Accounting & Management. 9(3). pp.245-264.

Van Helden, G.J. and et. al., 2010. Knowledge creation for practice in public sector management

accounting by consultants and academics: Preliminary findings and directions for future

research. Management Accounting Research. 21(2). pp.83-94.

Ward, K., 2012. Strategic management accounting. Routledge.

Weißenberger, B.E. and Angelkort, H., 2011. Integration of financial and management

accounting systems: The mediating influence of a consistent financial language on

controllership effectiveness. Management Accounting Research. 22(3). pp.160-180.

Online

14

(cost) accounting and related guidelines: a study of the Republic of Korea. Corporate

Social Responsibility and Environmental Management. 18(1). pp.39-49.

Luft, J and Shields, M. D., 2010. Psychology models of management accounting. Foundations

and Trends® in Accounting. 4(3–4). pp.199-345.

Lukka, K. and Modell, S., 2010. Validation in interpretive management accounting research.

Accounting, Organizations and Society. 35(4). pp.462-477.

Macintosh, N. B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional

accountants: A renewed research agenda. Journal of applied management accounting

research. 8(1). p.65.

Pipan, T. and Czarniawska, B., 2010. How to construct an actor-network: Management

accounting from idea to practice. Critical Perspectives on Accounting. 21(3). pp.243-

251.

Quinn, M., 2011. Routines in management accounting research: further exploration. Journal of

Accounting & Organizational Change. 7(4). pp.337-357.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Sánchez-Rodríguez, C. and Spraakman, G., 2012. ERP systems and management accounting: A

multiple case study. Qualitative Research in Accounting & Management. 9(4). pp.398-

414.

Setthasakko, W., 2010. Barriers to the development of environmental management accounting:

An exploratory study of pulp and paper companies in Thailand. EuroMed Journal of

Business. 5(3). pp.315-331.

Shah, H., Malik, A. and Malik, M.S., 2011. Strategic Management Accounting-A Messiah For

Management Accounting?. Australian Journal of Business and Management Research.

1(4). p.1.

Talha, M., Raja, J.B. and Seetharaman, A., 2010. A new look at management accounting.

Journal of Applied Business Research. 26(4). p.83.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

van der Meer-Kooistra, J. and Vosselman, E., 2012. Research paradigms, theoretical pluralism

and the practical relevance of management accounting knowledge. Qualitative Research

in Accounting & Management. 9(3). pp.245-264.

Van Helden, G.J. and et. al., 2010. Knowledge creation for practice in public sector management

accounting by consultants and academics: Preliminary findings and directions for future

research. Management Accounting Research. 21(2). pp.83-94.

Ward, K., 2012. Strategic management accounting. Routledge.

Weißenberger, B.E. and Angelkort, H., 2011. Integration of financial and management

accounting systems: The mediating influence of a consistent financial language on

controllership effectiveness. Management Accounting Research. 22(3). pp.160-180.

Online

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Why lean accounting?. 2017. [Online]. Available

through :<http://www.ame.org/target/articles/2016/why-lean-accounting>. [Accessed on

30th March 2017].

Cost Volume Profit Analysis. 2013. [Online]. Available through

:<http://accountingexplained.com/managerial/cvp-analysis/>. [Accessed on 30th March

2017].

Significance of Management Accounting Techniques in Decision-making: An Empirical Study on

Manufacturing Organizations in Bangladesh. 2011. [Online]. Available through

:<https://pdfs.semanticscholar.org/007d/bdfd7e299156cadf2097bf160d77be7b4e4d.pdf

>. [Accessed on 30th March 2017].

15

through :<http://www.ame.org/target/articles/2016/why-lean-accounting>. [Accessed on

30th March 2017].

Cost Volume Profit Analysis. 2013. [Online]. Available through

:<http://accountingexplained.com/managerial/cvp-analysis/>. [Accessed on 30th March

2017].

Significance of Management Accounting Techniques in Decision-making: An Empirical Study on

Manufacturing Organizations in Bangladesh. 2011. [Online]. Available through

:<https://pdfs.semanticscholar.org/007d/bdfd7e299156cadf2097bf160d77be7b4e4d.pdf

>. [Accessed on 30th March 2017].

15

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.