Analyzing Risk Profiles: Rio Tinto vs. BHP Billiton

VerifiedAdded on 2020/05/28

|13

|2193

|141

AI Summary

The analysis compares the risk profiles of Rio Tinto and BHP Billiton by evaluating their strategic, operational, and governance risks alongside financial metrics like debt equity ratios and earnings per share. While both companies face significant risks in mining operations, Rio Tinto exhibits a higher risk profile compared to BHP Billiton, particularly concerning its debt management. Through various control measures including specialized teams and audit systems, each company attempts to mitigate these inherent risks. The study concludes that although Rio Tinto has implemented robust controls, it still holds a relatively higher financial risk than BHP Billiton as evidenced by their respective solvency ratios and earnings performance.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Name of Student:

Name of University:

Author’s Note:

Auditing Theory and Practice

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Table of Contents

Introduction......................................................................................................................................2

Risk Analysis...................................................................................................................................2

Evaluation of risks and control environment...................................................................................4

Interest Coverage Ratio Analysis....................................................................................................7

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Risk Analysis...................................................................................................................................2

Evaluation of risks and control environment...................................................................................4

Interest Coverage Ratio Analysis....................................................................................................7

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2AUDITING THEORY AND PRACTICE

Introduction

RioTinto founded in 1873 is considered as one the leading multinational among the

world’s largest metal and mining industries. The primary focus of the company is identified in

terms of extraction of minerals. Some of the other activities performed by the company includes

refining of the bauxite and iron ore. The operations of the company are spread across continents

which are mainly concentrated in areas of Australia and Canada however the mining operations

is distributed in holy and partly owned subsidiaries various other parts of the world. The

company has been further identified as a dual listed company which trades on both “London

stock exchange” under the “FTSE 100 index” and “Australian securities exchange” under “S&P/

ASX 200 index”. The study aims to analyse the inherent risk along with control measure of Rio

Tinto and compare the same with BHP Billiton (Li, Simunic & Ye, 2017).

Risk Analysis

Inherent Risk Control Measures

Strategic Risk- The company enforces

capital allocation as per the best suited

returning opportunities. The ability to

securely plan the values through successful

divestments and acquisitions may vary

thereby affecting future performance,

solvency, liquidity, group reputation and

business model.

The group has encompassed complete details

about the material potential divestments and

acquisition which includes commercial

review, functional sign-offs, technical review,

and opinion of investment committee (Niemi

et al., 2017). It has further supported the

business resource development team by

external specialists. Rio Tinto has ensured

effective stakeholder management via project

development and following a rigorous

approval process which includes “stage-

gating process, monitoring and status

evaluation, as articulated in Project evaluation

standard

and guidance”.

HSEC Risks- As per the depiction of annual The mitigation of HSEC risks are identified as

Introduction

RioTinto founded in 1873 is considered as one the leading multinational among the

world’s largest metal and mining industries. The primary focus of the company is identified in

terms of extraction of minerals. Some of the other activities performed by the company includes

refining of the bauxite and iron ore. The operations of the company are spread across continents

which are mainly concentrated in areas of Australia and Canada however the mining operations

is distributed in holy and partly owned subsidiaries various other parts of the world. The

company has been further identified as a dual listed company which trades on both “London

stock exchange” under the “FTSE 100 index” and “Australian securities exchange” under “S&P/

ASX 200 index”. The study aims to analyse the inherent risk along with control measure of Rio

Tinto and compare the same with BHP Billiton (Li, Simunic & Ye, 2017).

Risk Analysis

Inherent Risk Control Measures

Strategic Risk- The company enforces

capital allocation as per the best suited

returning opportunities. The ability to

securely plan the values through successful

divestments and acquisitions may vary

thereby affecting future performance,

solvency, liquidity, group reputation and

business model.

The group has encompassed complete details

about the material potential divestments and

acquisition which includes commercial

review, functional sign-offs, technical review,

and opinion of investment committee (Niemi

et al., 2017). It has further supported the

business resource development team by

external specialists. Rio Tinto has ensured

effective stakeholder management via project

development and following a rigorous

approval process which includes “stage-

gating process, monitoring and status

evaluation, as articulated in Project evaluation

standard

and guidance”.

HSEC Risks- As per the depiction of annual The mitigation of HSEC risks are identified as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

report published in 2016 the operations at Rio

Tinto is inherently dangerous and may face

failure to manage “health, safety, environment

or community risks” which may lead to

detrimental effect in the long term. This may

also question on the licence to operate and

financial performance of the company. Some

of the recognised risk factors include

“underground

operations, aviation, pit slope instability,

tailings facilities, vector-borne and pandemic

disease, chemicals, gases and vehicles”.

the core priority all the operations which is

overseen by the sustainability committee

(Chen et al., 2016). The company clearly

defines the groups HSEC performance

standards, strategy and policy as defined

under this committee. In addition to this, Rio

Tinto regularly reviews the HSEC processes

for training, controlling, promoting, and

improving the overall effectiveness of non-

managed operations.

Resources Risks- Rio Tinto is recognised to

substantially invests in materially accurate

operations and projects. However, the

estimates of ore reserves are completely

uncertain in nature (Cohen, Krishnamoorthy

& Wright, 2017). The failure to identify new

viable over bodies may be catastrophic to the

future growth prospects. The risk that future

information comes to light or economic

viability of the mine plans may be restated

downwards. Due to this the project may be

less successful and have shorter duration than

it was initially forecasted thereby leading to

asset impairment.

The group is recognised to comply with the

resource and reserve standards thereby

recruiting and retaining experienced personal

for the same (Contessotto & Moroney, 2014).

Furthermore, the group has been able to

provide stable funding for different

exploration activities and thereby

continuously prioritise the portfolio. It has

further utilised new technologies wherever

appropriate and manage third-party

partnerships. There has been substantial

coordination with the knowledge of ore body

through the active group wide leadership

Forum of the company.

Operations, projects and people risks- The

company aims to achieve commercial and

operational experience to bring in and retain

some of the most eminent people in the

industry (Ruhnke & Schmidt, 2014). The

Rio Tinto is responsible for preserving

geographically diverse portfolio thereby

putting a limitation on the physical nature of

disruptions such as logistical events or single

infrastructure events (Miran, 2017). The

report published in 2016 the operations at Rio

Tinto is inherently dangerous and may face

failure to manage “health, safety, environment

or community risks” which may lead to

detrimental effect in the long term. This may

also question on the licence to operate and

financial performance of the company. Some

of the recognised risk factors include

“underground

operations, aviation, pit slope instability,

tailings facilities, vector-borne and pandemic

disease, chemicals, gases and vehicles”.

the core priority all the operations which is

overseen by the sustainability committee

(Chen et al., 2016). The company clearly

defines the groups HSEC performance

standards, strategy and policy as defined

under this committee. In addition to this, Rio

Tinto regularly reviews the HSEC processes

for training, controlling, promoting, and

improving the overall effectiveness of non-

managed operations.

Resources Risks- Rio Tinto is recognised to

substantially invests in materially accurate

operations and projects. However, the

estimates of ore reserves are completely

uncertain in nature (Cohen, Krishnamoorthy

& Wright, 2017). The failure to identify new

viable over bodies may be catastrophic to the

future growth prospects. The risk that future

information comes to light or economic

viability of the mine plans may be restated

downwards. Due to this the project may be

less successful and have shorter duration than

it was initially forecasted thereby leading to

asset impairment.

The group is recognised to comply with the

resource and reserve standards thereby

recruiting and retaining experienced personal

for the same (Contessotto & Moroney, 2014).

Furthermore, the group has been able to

provide stable funding for different

exploration activities and thereby

continuously prioritise the portfolio. It has

further utilised new technologies wherever

appropriate and manage third-party

partnerships. There has been substantial

coordination with the knowledge of ore body

through the active group wide leadership

Forum of the company.

Operations, projects and people risks- The

company aims to achieve commercial and

operational experience to bring in and retain

some of the most eminent people in the

industry (Ruhnke & Schmidt, 2014). The

Rio Tinto is responsible for preserving

geographically diverse portfolio thereby

putting a limitation on the physical nature of

disruptions such as logistical events or single

infrastructure events (Miran, 2017). The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

operational difficulties such as interruptions

to infrastructure for power, transportation,

water, industrial dispute and several other

bottlenecks in the value chain is identified as

the main risk factor. Moreover, cyber breach

incident in the operational and commercial

system may lead to significant loss of data. In

addition to this, operational incidents such as

failure of safety process or water

impoundment can lead to adverse situations.

company is further able to comply with

tailings management, underground mining

process, safety standards and slope

geotechnical which are supported by subject

matter experts reduce the overall risk impact.

Rio Tinto is seen to comply with IT

infrastructure and security controls which are

suggested by dedicated cyber security team.

Shareholder Risks - There may be

possibility that the joint venture partners may

affect the growth aspect by not agreeing on

the investment decisions. The nonmanaged

operations and the controlling partners may

react on contrary to the group’s interests,

policy or standards which may have adverse

impact on health and “safety, performance,

cyber integrity, reputation or legal liability”.

In order to combat of the aforementioned

risk, the company has approached with long-

term relationship in terms of investments and

partnership (Ghosh & Jarva, 2016). Rio Tinto

has maintained a strong focus on the contract

management and undertaking rigorous third-

party due diligence (Han et al., 2015).

Evaluation of risks and control environment

As per the depiction of the several types of the risk factors it needs to be inferred that Rio

Tinto is facing significant issues. These are evident with “strategic risks, HSEC risks, resources

risks, stakeholder risks and governance risks”. The company’s way of controlling the risks are

depicted with having believing in maintaining long-term relationship during joint ventures. To

address the significant risk associated to Operations, projects and people risks the company has

put restrictions on the physical nature of disruptions such as logistical events or single

infrastructure events. Moreover, Rio Tinto is seen to comply with IT infrastructure and security

controls which are suggested by dedicated cyber security team (Yoon, Hoogduin & Zhang,

2015).

operational difficulties such as interruptions

to infrastructure for power, transportation,

water, industrial dispute and several other

bottlenecks in the value chain is identified as

the main risk factor. Moreover, cyber breach

incident in the operational and commercial

system may lead to significant loss of data. In

addition to this, operational incidents such as

failure of safety process or water

impoundment can lead to adverse situations.

company is further able to comply with

tailings management, underground mining

process, safety standards and slope

geotechnical which are supported by subject

matter experts reduce the overall risk impact.

Rio Tinto is seen to comply with IT

infrastructure and security controls which are

suggested by dedicated cyber security team.

Shareholder Risks - There may be

possibility that the joint venture partners may

affect the growth aspect by not agreeing on

the investment decisions. The nonmanaged

operations and the controlling partners may

react on contrary to the group’s interests,

policy or standards which may have adverse

impact on health and “safety, performance,

cyber integrity, reputation or legal liability”.

In order to combat of the aforementioned

risk, the company has approached with long-

term relationship in terms of investments and

partnership (Ghosh & Jarva, 2016). Rio Tinto

has maintained a strong focus on the contract

management and undertaking rigorous third-

party due diligence (Han et al., 2015).

Evaluation of risks and control environment

As per the depiction of the several types of the risk factors it needs to be inferred that Rio

Tinto is facing significant issues. These are evident with “strategic risks, HSEC risks, resources

risks, stakeholder risks and governance risks”. The company’s way of controlling the risks are

depicted with having believing in maintaining long-term relationship during joint ventures. To

address the significant risk associated to Operations, projects and people risks the company has

put restrictions on the physical nature of disruptions such as logistical events or single

infrastructure events. Moreover, Rio Tinto is seen to comply with IT infrastructure and security

controls which are suggested by dedicated cyber security team (Yoon, Hoogduin & Zhang,

2015).

5AUDITING THEORY AND PRACTICE

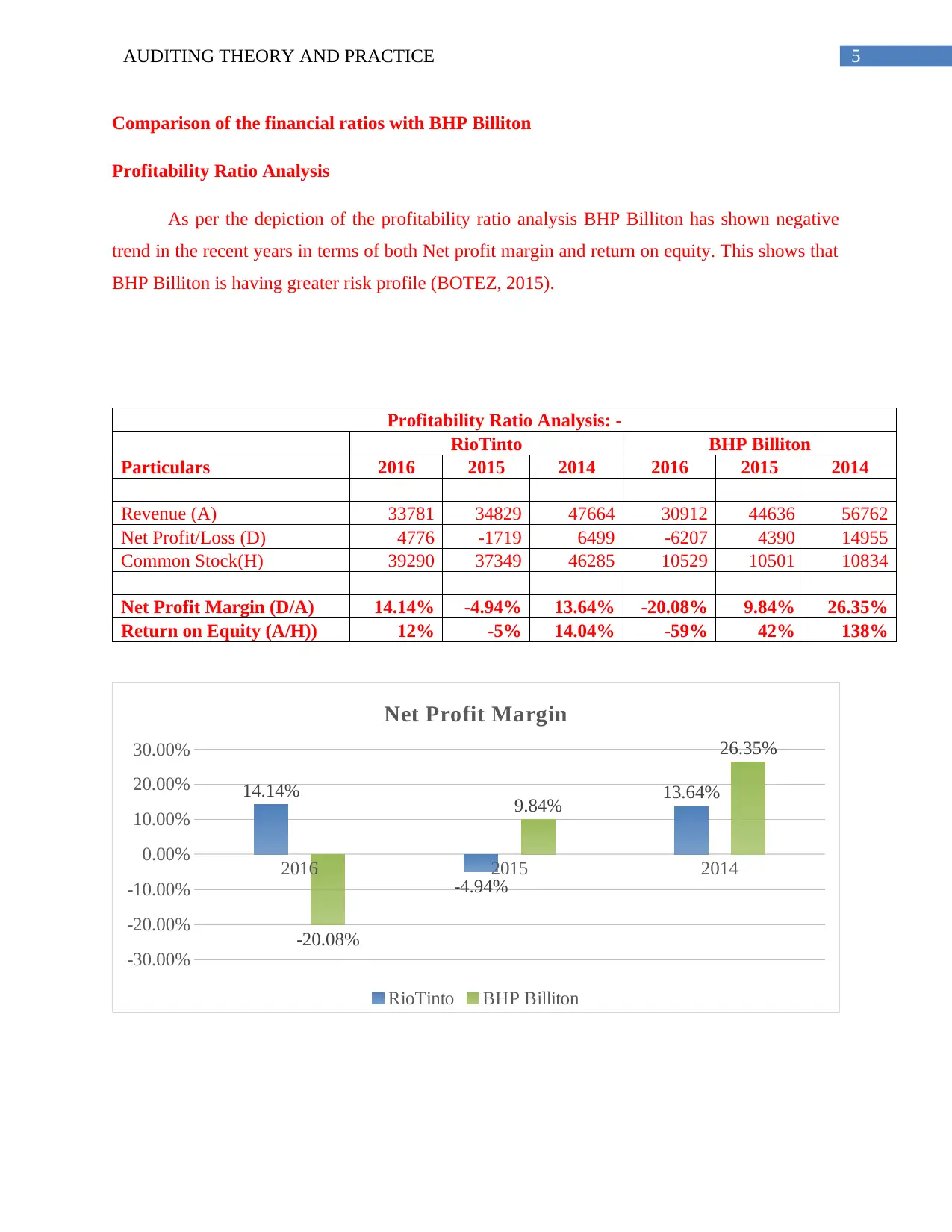

Comparison of the financial ratios with BHP Billiton

Profitability Ratio Analysis

As per the depiction of the profitability ratio analysis BHP Billiton has shown negative

trend in the recent years in terms of both Net profit margin and return on equity. This shows that

BHP Billiton is having greater risk profile (BOTEZ, 2015).

Profitability Ratio Analysis: -

RioTinto BHP Billiton

Particulars 2016 2015 2014 2016 2015 2014

Revenue (A) 33781 34829 47664 30912 44636 56762

Net Profit/Loss (D) 4776 -1719 6499 -6207 4390 14955

Common Stock(H) 39290 37349 46285 10529 10501 10834

Net Profit Margin (D/A) 14.14% -4.94% 13.64% -20.08% 9.84% 26.35%

Return on Equity (A/H)) 12% -5% 14.04% -59% 42% 138%

2016 2015 2014

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

14.14%

-4.94%

13.64%

-20.08%

9.84%

26.35%

Net Profit Margin

RioTinto BHP Billiton

Comparison of the financial ratios with BHP Billiton

Profitability Ratio Analysis

As per the depiction of the profitability ratio analysis BHP Billiton has shown negative

trend in the recent years in terms of both Net profit margin and return on equity. This shows that

BHP Billiton is having greater risk profile (BOTEZ, 2015).

Profitability Ratio Analysis: -

RioTinto BHP Billiton

Particulars 2016 2015 2014 2016 2015 2014

Revenue (A) 33781 34829 47664 30912 44636 56762

Net Profit/Loss (D) 4776 -1719 6499 -6207 4390 14955

Common Stock(H) 39290 37349 46285 10529 10501 10834

Net Profit Margin (D/A) 14.14% -4.94% 13.64% -20.08% 9.84% 26.35%

Return on Equity (A/H)) 12% -5% 14.04% -59% 42% 138%

2016 2015 2014

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

14.14%

-4.94%

13.64%

-20.08%

9.84%

26.35%

Net Profit Margin

RioTinto BHP Billiton

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

2016 2015 2014 2016 2015 2014

-100%

-50%

0%

50%

100%

150%

12%

-5%

14%

-59%

42%

138%

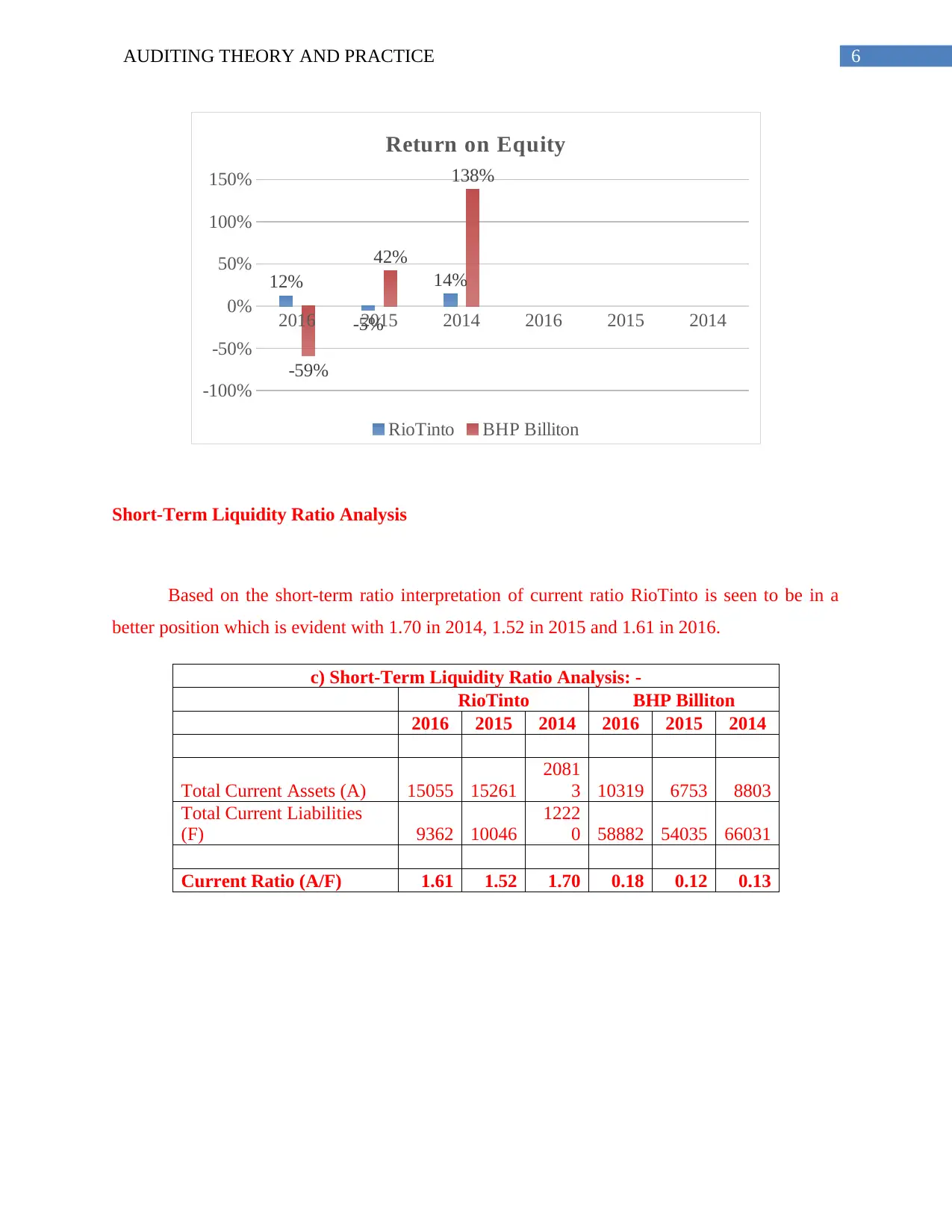

Return on Equity

RioTinto BHP Billiton

Short-Term Liquidity Ratio Analysis

Based on the short-term ratio interpretation of current ratio RioTinto is seen to be in a

better position which is evident with 1.70 in 2014, 1.52 in 2015 and 1.61 in 2016.

c) Short-Term Liquidity Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Total Current Assets (A) 15055 15261

2081

3 10319 6753 8803

Total Current Liabilities

(F) 9362 10046

1222

0 58882 54035 66031

Current Ratio (A/F) 1.61 1.52 1.70 0.18 0.12 0.13

2016 2015 2014 2016 2015 2014

-100%

-50%

0%

50%

100%

150%

12%

-5%

14%

-59%

42%

138%

Return on Equity

RioTinto BHP Billiton

Short-Term Liquidity Ratio Analysis

Based on the short-term ratio interpretation of current ratio RioTinto is seen to be in a

better position which is evident with 1.70 in 2014, 1.52 in 2015 and 1.61 in 2016.

c) Short-Term Liquidity Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Total Current Assets (A) 15055 15261

2081

3 10319 6753 8803

Total Current Liabilities

(F) 9362 10046

1222

0 58882 54035 66031

Current Ratio (A/F) 1.61 1.52 1.70 0.18 0.12 0.13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

2016 2015 2014

0.00

0.50

1.00

1.50

2.00

0.18 0.12 0.13

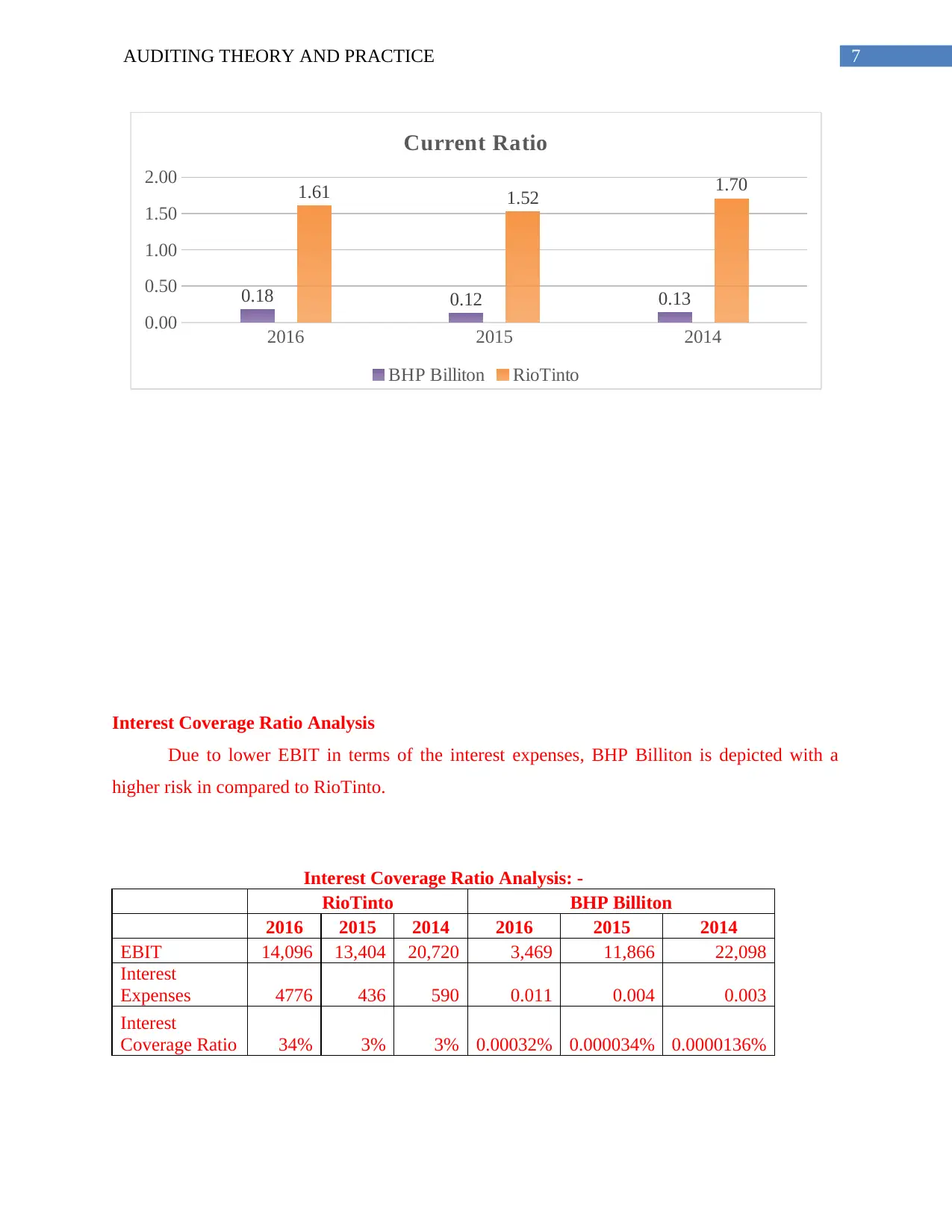

1.61 1.52 1.70

Current Ratio

BHP Billiton RioTinto

Interest Coverage Ratio Analysis

Due to lower EBIT in terms of the interest expenses, BHP Billiton is depicted with a

higher risk in compared to RioTinto.

Interest Coverage Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

EBIT 14,096 13,404 20,720 3,469 11,866 22,098

Interest

Expenses 4776 436 590 0.011 0.004 0.003

Interest

Coverage Ratio 34% 3% 3% 0.00032% 0.000034% 0.0000136%

2016 2015 2014

0.00

0.50

1.00

1.50

2.00

0.18 0.12 0.13

1.61 1.52 1.70

Current Ratio

BHP Billiton RioTinto

Interest Coverage Ratio Analysis

Due to lower EBIT in terms of the interest expenses, BHP Billiton is depicted with a

higher risk in compared to RioTinto.

Interest Coverage Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

EBIT 14,096 13,404 20,720 3,469 11,866 22,098

Interest

Expenses 4776 436 590 0.011 0.004 0.003

Interest

Coverage Ratio 34% 3% 3% 0.00032% 0.000034% 0.0000136%

8AUDITING THEORY AND PRACTICE

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0%

10%

20%

30%

40% 34%

3% 3% 0% 0% 0%

Interest Coverage Ratio

Interest Coverage Ratio

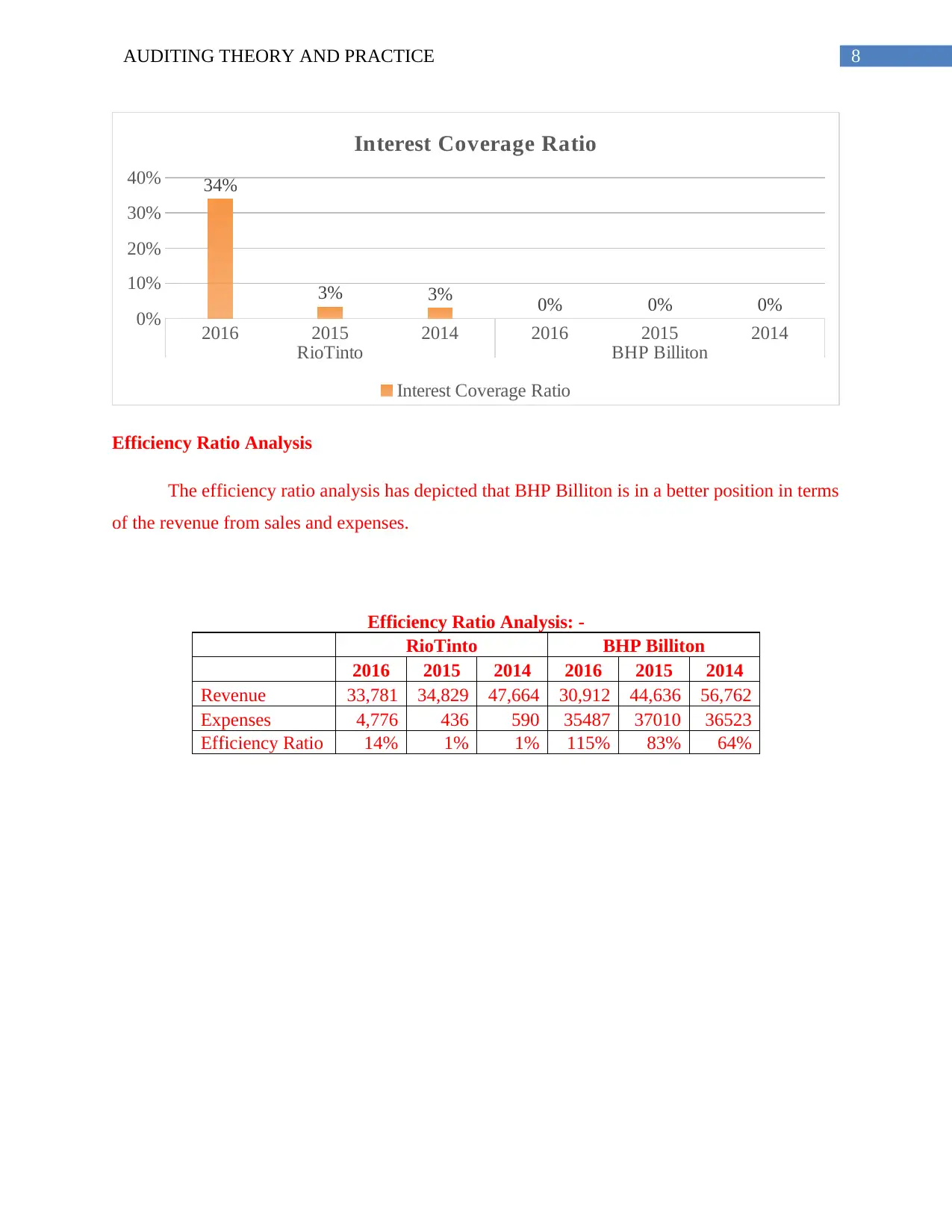

Efficiency Ratio Analysis

The efficiency ratio analysis has depicted that BHP Billiton is in a better position in terms

of the revenue from sales and expenses.

Efficiency Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Revenue 33,781 34,829 47,664 30,912 44,636 56,762

Expenses 4,776 436 590 35487 37010 36523

Efficiency Ratio 14% 1% 1% 115% 83% 64%

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0%

10%

20%

30%

40% 34%

3% 3% 0% 0% 0%

Interest Coverage Ratio

Interest Coverage Ratio

Efficiency Ratio Analysis

The efficiency ratio analysis has depicted that BHP Billiton is in a better position in terms

of the revenue from sales and expenses.

Efficiency Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Revenue 33,781 34,829 47,664 30,912 44,636 56,762

Expenses 4,776 436 590 35487 37010 36523

Efficiency Ratio 14% 1% 1% 115% 83% 64%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0%

20%

40%

60%

80%

100%

120%

140%

14% 1% 1%

115%

83%

64%

Efficiency Ratio

Efficiency Ratio

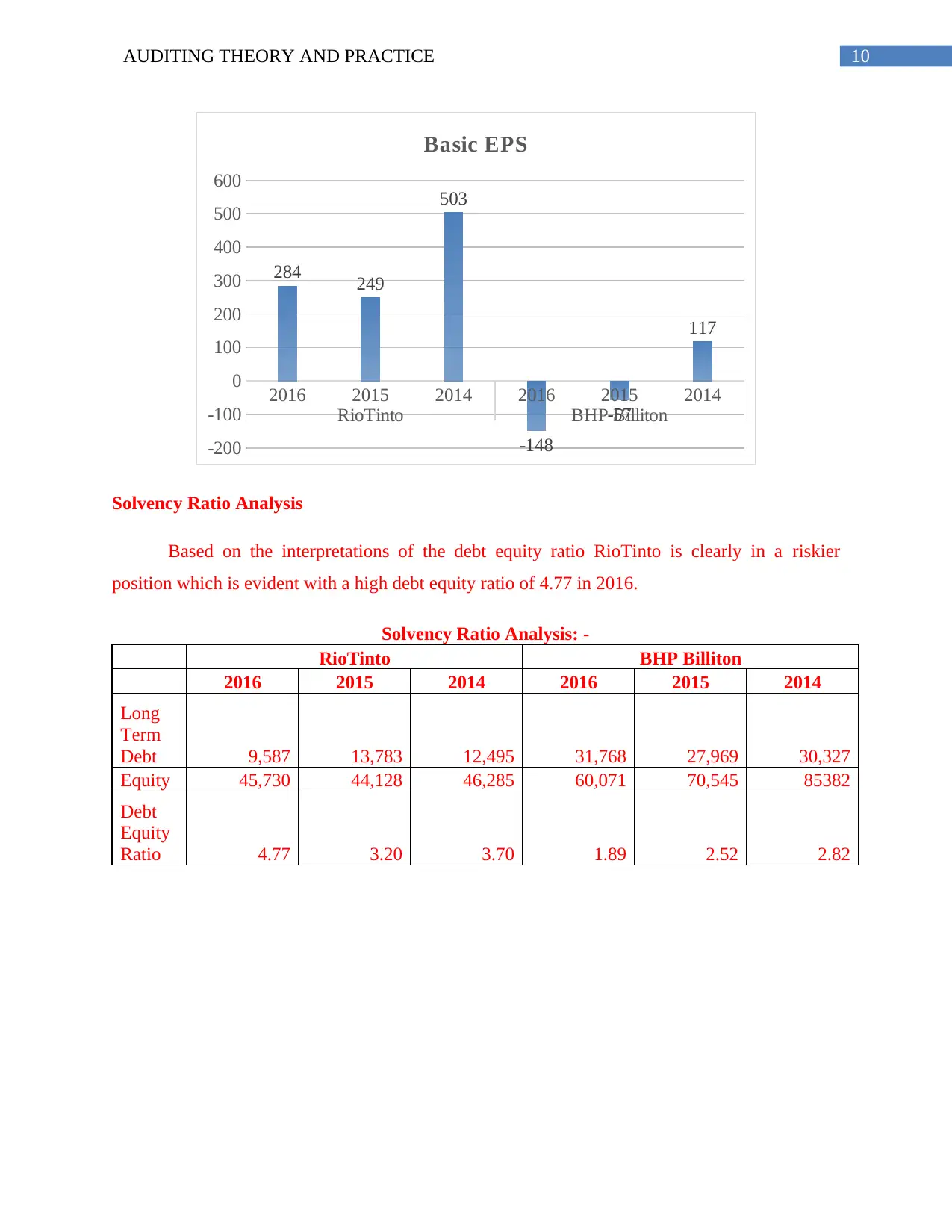

Market Performance Analysis

The market performance ratio analysis has depicted that despite of reducing trend of EPS

in both the companies, RioTinto has a better EPS in compared to BHP Billiton.

Earnings per share Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Basic

EPS 284 249 503 -148 -57 117

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0%

20%

40%

60%

80%

100%

120%

140%

14% 1% 1%

115%

83%

64%

Efficiency Ratio

Efficiency Ratio

Market Performance Analysis

The market performance ratio analysis has depicted that despite of reducing trend of EPS

in both the companies, RioTinto has a better EPS in compared to BHP Billiton.

Earnings per share Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Basic

EPS 284 249 503 -148 -57 117

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

-200

-100

0

100

200

300

400

500

600

284 249

503

-148

-57

117

Basic EPS

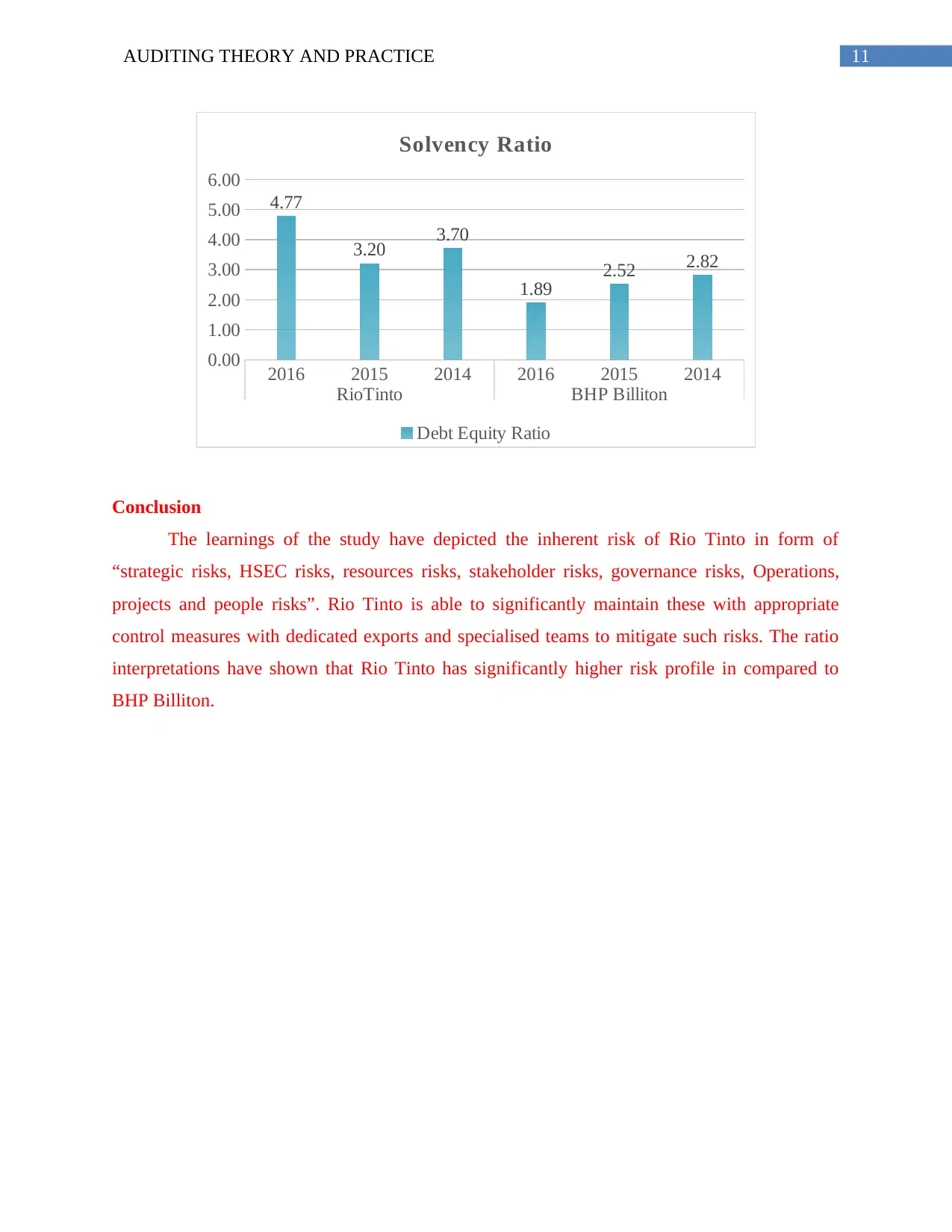

Solvency Ratio Analysis

Based on the interpretations of the debt equity ratio RioTinto is clearly in a riskier

position which is evident with a high debt equity ratio of 4.77 in 2016.

Solvency Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Long

Term

Debt 9,587 13,783 12,495 31,768 27,969 30,327

Equity 45,730 44,128 46,285 60,071 70,545 85382

Debt

Equity

Ratio 4.77 3.20 3.70 1.89 2.52 2.82

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

-200

-100

0

100

200

300

400

500

600

284 249

503

-148

-57

117

Basic EPS

Solvency Ratio Analysis

Based on the interpretations of the debt equity ratio RioTinto is clearly in a riskier

position which is evident with a high debt equity ratio of 4.77 in 2016.

Solvency Ratio Analysis: -

RioTinto BHP Billiton

2016 2015 2014 2016 2015 2014

Long

Term

Debt 9,587 13,783 12,495 31,768 27,969 30,327

Equity 45,730 44,128 46,285 60,071 70,545 85382

Debt

Equity

Ratio 4.77 3.20 3.70 1.89 2.52 2.82

11AUDITING THEORY AND PRACTICE

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0.00

1.00

2.00

3.00

4.00

5.00

6.00

4.77

3.20 3.70

1.89

2.52 2.82

Solvency Ratio

Debt Equity Ratio

Conclusion

The learnings of the study have depicted the inherent risk of Rio Tinto in form of

“strategic risks, HSEC risks, resources risks, stakeholder risks, governance risks, Operations,

projects and people risks”. Rio Tinto is able to significantly maintain these with appropriate

control measures with dedicated exports and specialised teams to mitigate such risks. The ratio

interpretations have shown that Rio Tinto has significantly higher risk profile in compared to

BHP Billiton.

2016 2015 2014 2016 2015 2014

RioTinto BHP Billiton

0.00

1.00

2.00

3.00

4.00

5.00

6.00

4.77

3.20 3.70

1.89

2.52 2.82

Solvency Ratio

Debt Equity Ratio

Conclusion

The learnings of the study have depicted the inherent risk of Rio Tinto in form of

“strategic risks, HSEC risks, resources risks, stakeholder risks, governance risks, Operations,

projects and people risks”. Rio Tinto is able to significantly maintain these with appropriate

control measures with dedicated exports and specialised teams to mitigate such risks. The ratio

interpretations have shown that Rio Tinto has significantly higher risk profile in compared to

BHP Billiton.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.