Financial Analysis of Leadall's FP17 Capital Budgeting Opportunity

VerifiedAdded on 2020/05/08

|11

|1939

|65

Report

AI Summary

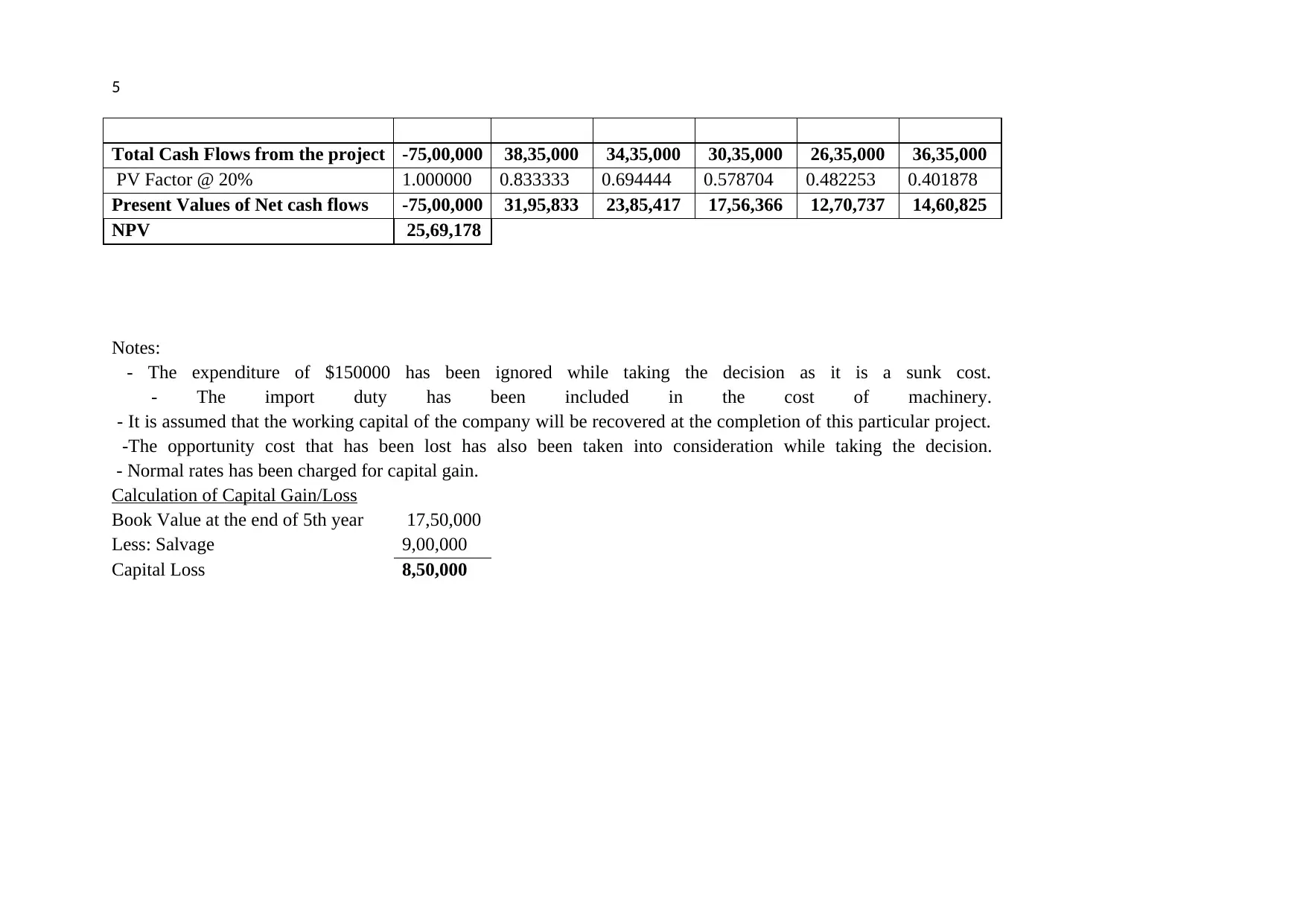

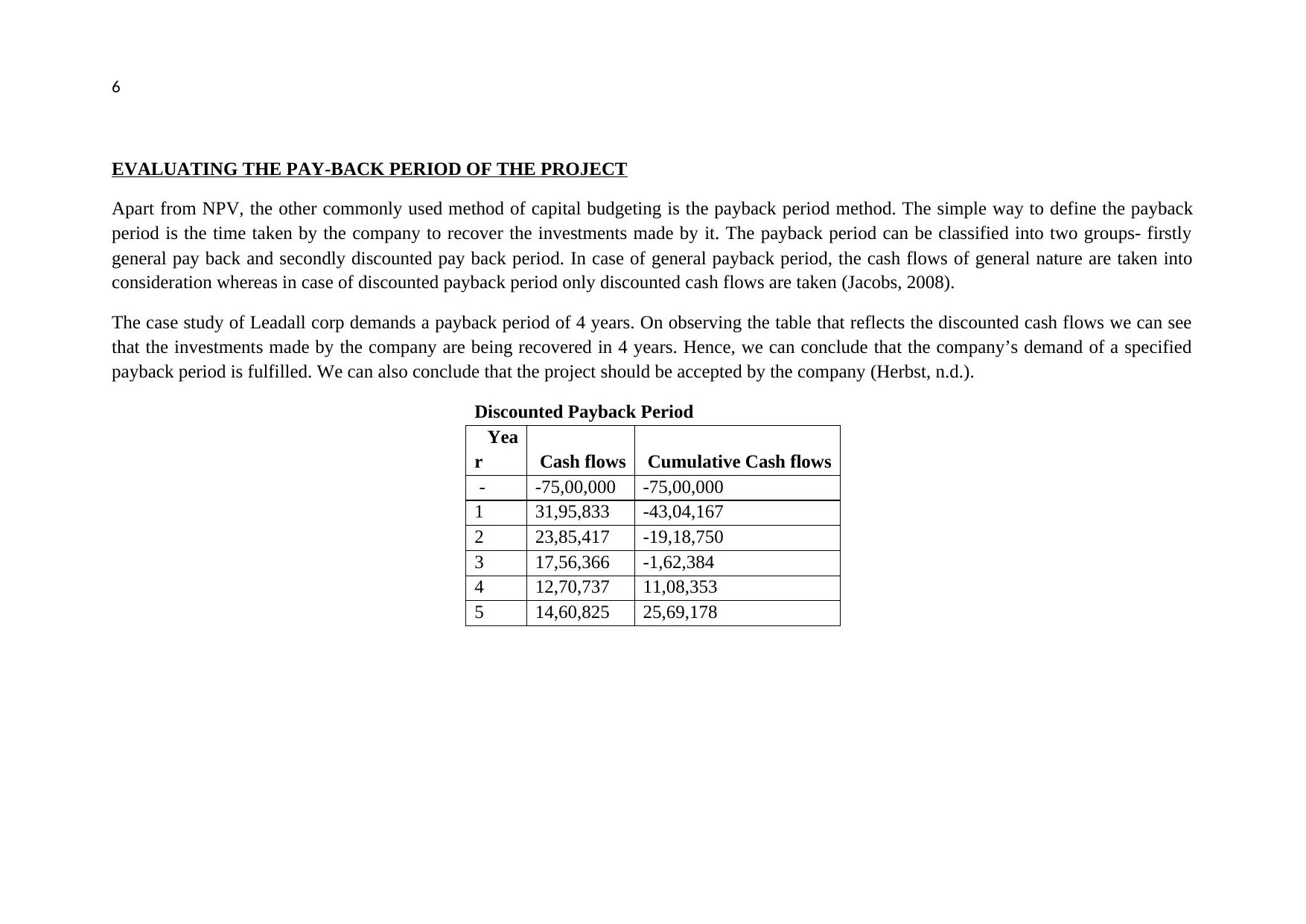

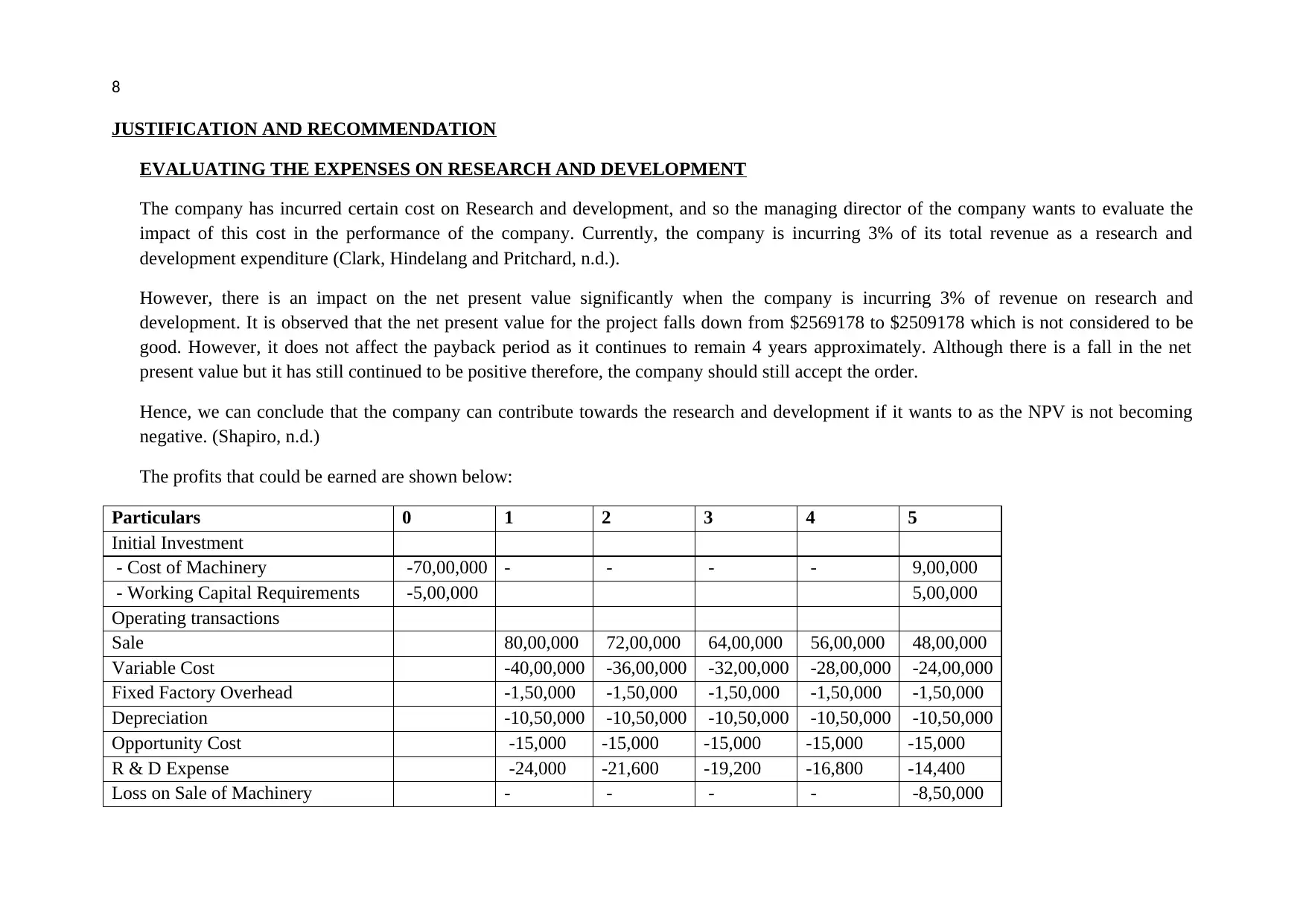

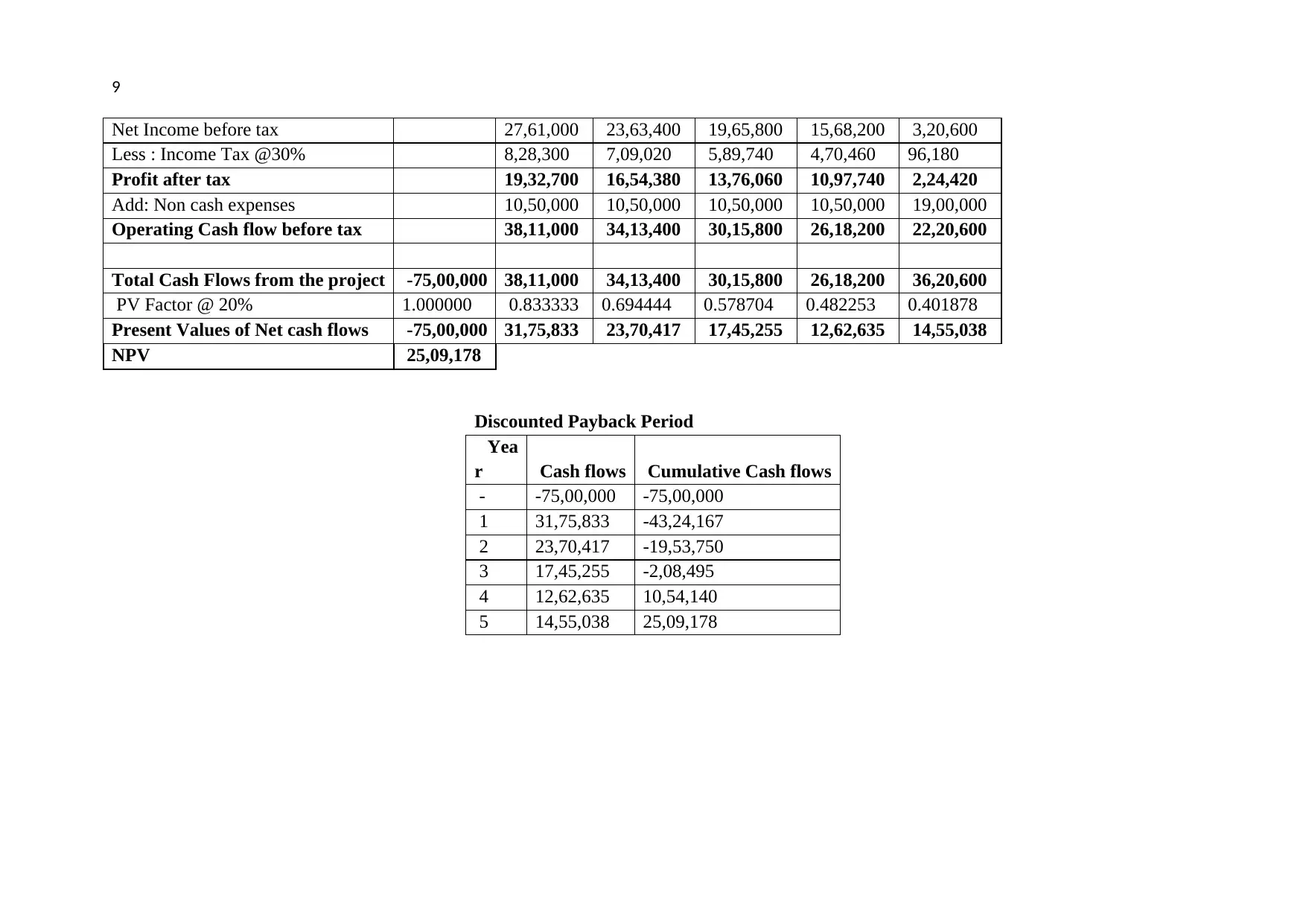

This report provides a financial analysis of Leadall's FP17 project, evaluating its capital budgeting opportunity. The analysis utilizes quantitative methods such as Net Present Value (NPV) and discounted payback period to assess the project's profitability and investment recovery timeline. The report includes detailed calculations of cash flows, considering initial investments, operating transactions, and expenses like depreciation and income tax. Furthermore, the report considers qualitative factors such as fund availability, working capital requirements, government regulations, return on capital, and the use of assumptions. The impact of research and development expenses is also assessed. The report concludes with a recommendation to accept the project based on positive NPV and the fulfillment of the required payback period, while acknowledging the importance of considering both quantitative and qualitative aspects in making a sound investment decision. The report also references several academic sources related to capital budgeting and financial management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.