Management Accounting for Nero Ltd

VerifiedAdded on 2020/06/06

|15

|4235

|239

AI Summary

This assignment delves into the application of management accounting principles at Nero Ltd. It analyzes various financial issues faced by the company, such as communication gaps in operations and inventory control, and proposes solutions using techniques like key performance indicators (KPIs), benchmarking, and financial governance. The document also explores different costing methods, budgeting, and reporting systems to enhance profitability and decision-making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and its use.....................................................................................1

P2. Different methods used in management accounting reporting.............................................3

M1: Advantages of management accounting system..................................................................4

D1: Critical analysis of reporting systems..................................................................................4

P3: Calculation of net profit by using various costing methods.................................................4

M2: Analysis of various range of accounting techniques...........................................................7

D2: Analysis of financial performance of the company.............................................................8

SECTION 2......................................................................................................................................8

P4: Planning tools used for budgetary control ...........................................................................8

M3: Evaluation of planning tools..............................................................................................10

D3: Analysis of financial issues................................................................................................10

P5: Respond to various issues related with financial aspects...................................................10

M4: Analysis of the financial issues.........................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and its use.....................................................................................1

P2. Different methods used in management accounting reporting.............................................3

M1: Advantages of management accounting system..................................................................4

D1: Critical analysis of reporting systems..................................................................................4

P3: Calculation of net profit by using various costing methods.................................................4

M2: Analysis of various range of accounting techniques...........................................................7

D2: Analysis of financial performance of the company.............................................................8

SECTION 2......................................................................................................................................8

P4: Planning tools used for budgetary control ...........................................................................8

M3: Evaluation of planning tools..............................................................................................10

D3: Analysis of financial issues................................................................................................10

P5: Respond to various issues related with financial aspects...................................................10

M4: Analysis of the financial issues.........................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is that field of accounting which deals with providing message

to managers for their use in planning, decision making, performance evaluation, control activities

and financial reporting. It is an important aspect of any business through which company can

manage and control its daily operations (Siegel and et. al., 2010). Each organisation is trying

hard to achieve the aim and objectives by completing their activities according to framed plan. It

involves furnishing of the financial data to the management in such a way so that it facilitated the

decision making and modify the efficiency inside the organisation's.

The project assignment consists of two sections that talk about accounting functions and

its importance to the management. Different types of accounting systems are discussed in the

project. The understanding of various costing methods and planning tools which are used in

budgetary control are mentioned in this assignment. At last, how financial issues can be

overcome by using appropriate techniques are also explained here.

SECTION 1

P1. Management accounting and its use

In an organisation, there are large number of financial transactions conducted on regular

basis. To manage those transactions, company need a perfect system which can control the entire

operations into correct format. It is because; the managers cannot handle all their accounting

work manually. As accounting is connected with collection of data, recording it into concern

books of company and summarised into correct format. So that future decisions can be made in

order to achieved its long term objectives. Company can use all necessary information in

planning and controlling of their business operations (Talha, Raja and Seetharaman, 2010). It is

mostly related with management because growth and profitability of cited company is identified

through the financial statements.

Company long and short term goals are mostly dependent upon the stability and position

during the past few year. On that basis, most of the investors or stakeholders can make their

investment plans. The main reason to record all financial transactions with using appropriate

accounting system is to get effective results in the coming future. For Nero Ltd, the sole

objective is to incur maximum profit from its limited resources. In that manner, accounting

systems are more valuable to provide correct directions to company’s plan. Financial report is

1

Management accounting is that field of accounting which deals with providing message

to managers for their use in planning, decision making, performance evaluation, control activities

and financial reporting. It is an important aspect of any business through which company can

manage and control its daily operations (Siegel and et. al., 2010). Each organisation is trying

hard to achieve the aim and objectives by completing their activities according to framed plan. It

involves furnishing of the financial data to the management in such a way so that it facilitated the

decision making and modify the efficiency inside the organisation's.

The project assignment consists of two sections that talk about accounting functions and

its importance to the management. Different types of accounting systems are discussed in the

project. The understanding of various costing methods and planning tools which are used in

budgetary control are mentioned in this assignment. At last, how financial issues can be

overcome by using appropriate techniques are also explained here.

SECTION 1

P1. Management accounting and its use

In an organisation, there are large number of financial transactions conducted on regular

basis. To manage those transactions, company need a perfect system which can control the entire

operations into correct format. It is because; the managers cannot handle all their accounting

work manually. As accounting is connected with collection of data, recording it into concern

books of company and summarised into correct format. So that future decisions can be made in

order to achieved its long term objectives. Company can use all necessary information in

planning and controlling of their business operations (Talha, Raja and Seetharaman, 2010). It is

mostly related with management because growth and profitability of cited company is identified

through the financial statements.

Company long and short term goals are mostly dependent upon the stability and position

during the past few year. On that basis, most of the investors or stakeholders can make their

investment plans. The main reason to record all financial transactions with using appropriate

accounting system is to get effective results in the coming future. For Nero Ltd, the sole

objective is to incur maximum profit from its limited resources. In that manner, accounting

systems are more valuable to provide correct directions to company’s plan. Financial report is

1

considered as one of the vital tools of company. On that basis, productivity and growth can be

determined. Accounting systems are useful for the managers to acquire competitive advantages

from other companies. In that process, they prepare regular report to analyse the impact of

implementing systems in company’s growth. It will also help to determine total cost which is

used during the production of products and services (Tayles, 2011). The management accounting

system provides reliable and accurate results from the inputs which are given by the company

during manufacturing process. Some accounting systems which are used in an organisation are

explained underneath:

Price optimisation: It refers to the use of numerical analysis by a company to establish

how customers will react to various prices for the goods and services which are produced by the

company through several modes. It is mainly based on the assumption that to determine those

costs which are more favourable for the client and they can buy it more easily without any

overlooks.

Cost accounting system: Under this accounting system, a complete set of framework is

taken into consideration to determine the overall cost of products for profitability evaluation and

cost control. It is an aim which is guides management on various course of actions that are based

on cost efficiency and its capability.

Job costing system: It is a system of distribution which is associated with the individual

cost of a product or lot size of goods. Under this, resources are enlarged to bring a well-defined

product or service to market for particular clients.

Inventory system: It is a kind of system used for analysing and tracking of the stock

level, orders and its sales or deliveries. It is the most helpful in production units where the

inventory bills and production related documents are summarised and recorded into the system.

It is a chain from which goods are transferred to industry to storehouse.

Batch costing: It is similar as job costing which is incurred when a group of goods and

services are manufactured and cannot be determined to a particular products and services within

the selected group. A batch number is provided to each lot of products.

The accounting systems are used for making effective future plans for the company. It is

used to analyse the performance so that long term goals can be achieved. Other essential use of

this is to gain competitive advantages over the other companies.

2

determined. Accounting systems are useful for the managers to acquire competitive advantages

from other companies. In that process, they prepare regular report to analyse the impact of

implementing systems in company’s growth. It will also help to determine total cost which is

used during the production of products and services (Tayles, 2011). The management accounting

system provides reliable and accurate results from the inputs which are given by the company

during manufacturing process. Some accounting systems which are used in an organisation are

explained underneath:

Price optimisation: It refers to the use of numerical analysis by a company to establish

how customers will react to various prices for the goods and services which are produced by the

company through several modes. It is mainly based on the assumption that to determine those

costs which are more favourable for the client and they can buy it more easily without any

overlooks.

Cost accounting system: Under this accounting system, a complete set of framework is

taken into consideration to determine the overall cost of products for profitability evaluation and

cost control. It is an aim which is guides management on various course of actions that are based

on cost efficiency and its capability.

Job costing system: It is a system of distribution which is associated with the individual

cost of a product or lot size of goods. Under this, resources are enlarged to bring a well-defined

product or service to market for particular clients.

Inventory system: It is a kind of system used for analysing and tracking of the stock

level, orders and its sales or deliveries. It is the most helpful in production units where the

inventory bills and production related documents are summarised and recorded into the system.

It is a chain from which goods are transferred to industry to storehouse.

Batch costing: It is similar as job costing which is incurred when a group of goods and

services are manufactured and cannot be determined to a particular products and services within

the selected group. A batch number is provided to each lot of products.

The accounting systems are used for making effective future plans for the company. It is

used to analyse the performance so that long term goals can be achieved. Other essential use of

this is to gain competitive advantages over the other companies.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P2. Different methods used in management accounting reporting

Accounting reports are the collection of financial data that is copied from company's

accounting records of a business concern. The company can analysed its performances with the

help of various reporting statements which includes: Income statements and balance sheet.

Starting and keeping perfect accounting practise is necessary for the growth of a concern entity.

The manager are responsible for controlling every transactions into correct manner so that less

chance of mistakes can be arises. This can only be possible for identifying and analysing the plan

through use of accurate accounting reporting (Tucker and Parker, 2014). Reporting is necessary

to evaluate the financial performance of Nero Ltd. The managers look out for all the related

reports which are necessary in order to maintain records according to prescribed policies

regarding records keeping. Investors and stakeholders would make their effective decision on the

basis of those accounting reporting which are prepared by the managers during the year.

Different reporting which are analysed by the managers are discussed as below:

Performance reporting: In this report, performance of employees as well as

organisation is analysed based on the current year’s performance. It is done on the regular or

yearly basis. The individual’s performance is based on the ability and experience that they gain

during the year. While, organisational performances are analysed through its financial position.

Accounts receivable reports: It refers as that report which is summarised with time

duration, amounts collection from the debtors. This is prepared to know about how much funds

are coming with the company from its debtors (Albu and Albu,2012). It provide manager a

complete list of amount and time duration of capital which a company will get from the concern

parties.

Inventory management reporting: In this report, position of inventories are

summarised and recorded in order to maintain balance among demand and supply. It also help to

control the wastage and to organising the resources which are necessary for the company during

the time of delivery. There are some of the methods which are used by the managers in order to

keep its level of inventory. Such as EOQ and ABC controlling.

Job costing reporting: The costs which are related with the individual segment of

products are considered under this report. It also consist of total time and size of lots produce

during the year. An estimation regarding the cost which are incur in that particular process are

recorded into it.

3

Accounting reports are the collection of financial data that is copied from company's

accounting records of a business concern. The company can analysed its performances with the

help of various reporting statements which includes: Income statements and balance sheet.

Starting and keeping perfect accounting practise is necessary for the growth of a concern entity.

The manager are responsible for controlling every transactions into correct manner so that less

chance of mistakes can be arises. This can only be possible for identifying and analysing the plan

through use of accurate accounting reporting (Tucker and Parker, 2014). Reporting is necessary

to evaluate the financial performance of Nero Ltd. The managers look out for all the related

reports which are necessary in order to maintain records according to prescribed policies

regarding records keeping. Investors and stakeholders would make their effective decision on the

basis of those accounting reporting which are prepared by the managers during the year.

Different reporting which are analysed by the managers are discussed as below:

Performance reporting: In this report, performance of employees as well as

organisation is analysed based on the current year’s performance. It is done on the regular or

yearly basis. The individual’s performance is based on the ability and experience that they gain

during the year. While, organisational performances are analysed through its financial position.

Accounts receivable reports: It refers as that report which is summarised with time

duration, amounts collection from the debtors. This is prepared to know about how much funds

are coming with the company from its debtors (Albu and Albu,2012). It provide manager a

complete list of amount and time duration of capital which a company will get from the concern

parties.

Inventory management reporting: In this report, position of inventories are

summarised and recorded in order to maintain balance among demand and supply. It also help to

control the wastage and to organising the resources which are necessary for the company during

the time of delivery. There are some of the methods which are used by the managers in order to

keep its level of inventory. Such as EOQ and ABC controlling.

Job costing reporting: The costs which are related with the individual segment of

products are considered under this report. It also consist of total time and size of lots produce

during the year. An estimation regarding the cost which are incur in that particular process are

recorded into it.

3

Operational budgets report: This reports is prepared by analysing the total cost which are

incurred over the production of a products and services. The expenses which are used in that

process are recorded under it (Burritt, Schaltegger and Zvezdov, 2011). The base of net profit are

identified by the use of this reporting system. It includes sales and production budgets.

M1: Advantages of management accounting system

As it has been observed that for any business entity accounting systems are utmost

necessary in order to manage their daily operations. By using such kind of system management

as well as individual both can get effective advantages in their regular course of actions. The

above mentioned accounting system can be more effective to generate maximum profit for the

company. The other benefits are related with developing harmonious relation among its

employees and top authority so that efficiency can be enhanced (Management Accounting,

2017.). With the use of this system, there is huge chance of getting competitive advantages over

the other. For the future expansion these systems can be more crucial for the company.

D1: Critical analysis of reporting systems

The Nero Ltd is trying to grab opportunities which are coming in front of them. In that

process the above used reporting systems can be more useful. As they are prepared after making

overall analysis of costs and expenses which are incurred by the company during the production

process. The job costing and inventory management reporting are more effective tools which

provide more effective results in quick time. According to Cooper-Ezzamel and Qu, 2017 the

extra cost can be minimised by using operation reporting. The major aspects of the reporting

systems are they firstly, analysed and summarised into proper format before posting it to the

books of final accounts.

P3: Calculation of net profit by using various costing methods.

Costing: It is a method and procedures which is used by the company in order to

ascertain costs. The costing techniques consists of various principles and regulations which

regulate the process of estimating costs of goods and services. The costs includes historical or

conventional costing, absorption costing and marginal costing.

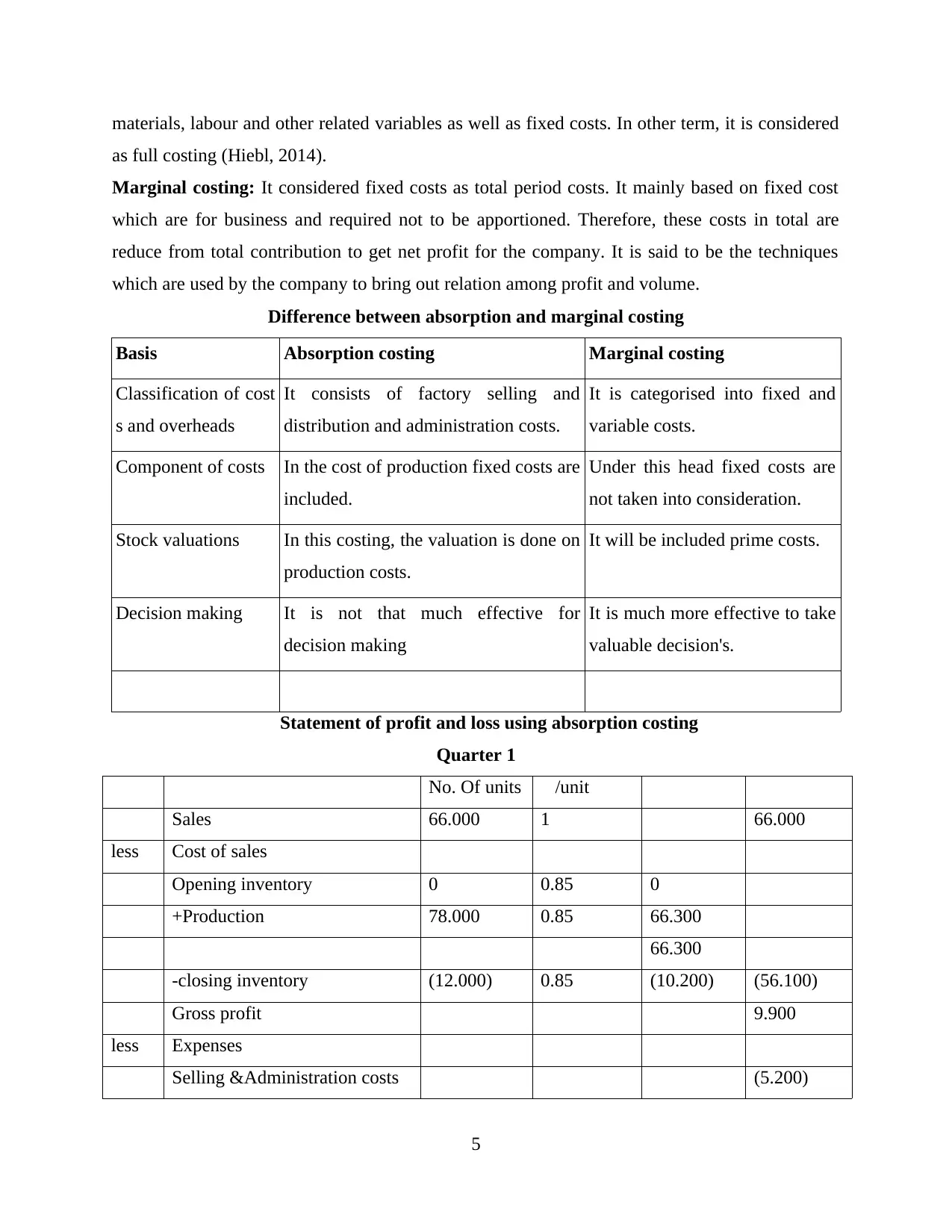

Absorption costing: It refers as all those costs which are related with the production costs are

absorbed by the units produced during time. The cost of final units in stocks are consist of direct

4

incurred over the production of a products and services. The expenses which are used in that

process are recorded under it (Burritt, Schaltegger and Zvezdov, 2011). The base of net profit are

identified by the use of this reporting system. It includes sales and production budgets.

M1: Advantages of management accounting system

As it has been observed that for any business entity accounting systems are utmost

necessary in order to manage their daily operations. By using such kind of system management

as well as individual both can get effective advantages in their regular course of actions. The

above mentioned accounting system can be more effective to generate maximum profit for the

company. The other benefits are related with developing harmonious relation among its

employees and top authority so that efficiency can be enhanced (Management Accounting,

2017.). With the use of this system, there is huge chance of getting competitive advantages over

the other. For the future expansion these systems can be more crucial for the company.

D1: Critical analysis of reporting systems

The Nero Ltd is trying to grab opportunities which are coming in front of them. In that

process the above used reporting systems can be more useful. As they are prepared after making

overall analysis of costs and expenses which are incurred by the company during the production

process. The job costing and inventory management reporting are more effective tools which

provide more effective results in quick time. According to Cooper-Ezzamel and Qu, 2017 the

extra cost can be minimised by using operation reporting. The major aspects of the reporting

systems are they firstly, analysed and summarised into proper format before posting it to the

books of final accounts.

P3: Calculation of net profit by using various costing methods.

Costing: It is a method and procedures which is used by the company in order to

ascertain costs. The costing techniques consists of various principles and regulations which

regulate the process of estimating costs of goods and services. The costs includes historical or

conventional costing, absorption costing and marginal costing.

Absorption costing: It refers as all those costs which are related with the production costs are

absorbed by the units produced during time. The cost of final units in stocks are consist of direct

4

materials, labour and other related variables as well as fixed costs. In other term, it is considered

as full costing (Hiebl, 2014).

Marginal costing: It considered fixed costs as total period costs. It mainly based on fixed cost

which are for business and required not to be apportioned. Therefore, these costs in total are

reduce from total contribution to get net profit for the company. It is said to be the techniques

which are used by the company to bring out relation among profit and volume.

Difference between absorption and marginal costing

Basis Absorption costing Marginal costing

Classification of cost

s and overheads

It consists of factory selling and

distribution and administration costs.

It is categorised into fixed and

variable costs.

Component of costs In the cost of production fixed costs are

included.

Under this head fixed costs are

not taken into consideration.

Stock valuations In this costing, the valuation is done on

production costs.

It will be included prime costs.

Decision making It is not that much effective for

decision making

It is much more effective to take

valuable decision's.

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78.000 0.85 66.300

66.300

-closing inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenses

Selling &Administration costs (5.200)

5

as full costing (Hiebl, 2014).

Marginal costing: It considered fixed costs as total period costs. It mainly based on fixed cost

which are for business and required not to be apportioned. Therefore, these costs in total are

reduce from total contribution to get net profit for the company. It is said to be the techniques

which are used by the company to bring out relation among profit and volume.

Difference between absorption and marginal costing

Basis Absorption costing Marginal costing

Classification of cost

s and overheads

It consists of factory selling and

distribution and administration costs.

It is categorised into fixed and

variable costs.

Component of costs In the cost of production fixed costs are

included.

Under this head fixed costs are

not taken into consideration.

Stock valuations In this costing, the valuation is done on

production costs.

It will be included prime costs.

Decision making It is not that much effective for

decision making

It is much more effective to take

valuable decision's.

Statement of profit and loss using absorption costing

Quarter 1

No. Of units £/unit £ £

Sales 66.000 1 66.000

less Cost of sales

Opening inventory 0 0.85 0

+Production 78.000 0.85 66.300

66.300

-closing inventory (12.000) 0.85 (10.200) (56.100)

Gross profit 9.900

less Expenses

Selling &Administration costs (5.200)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

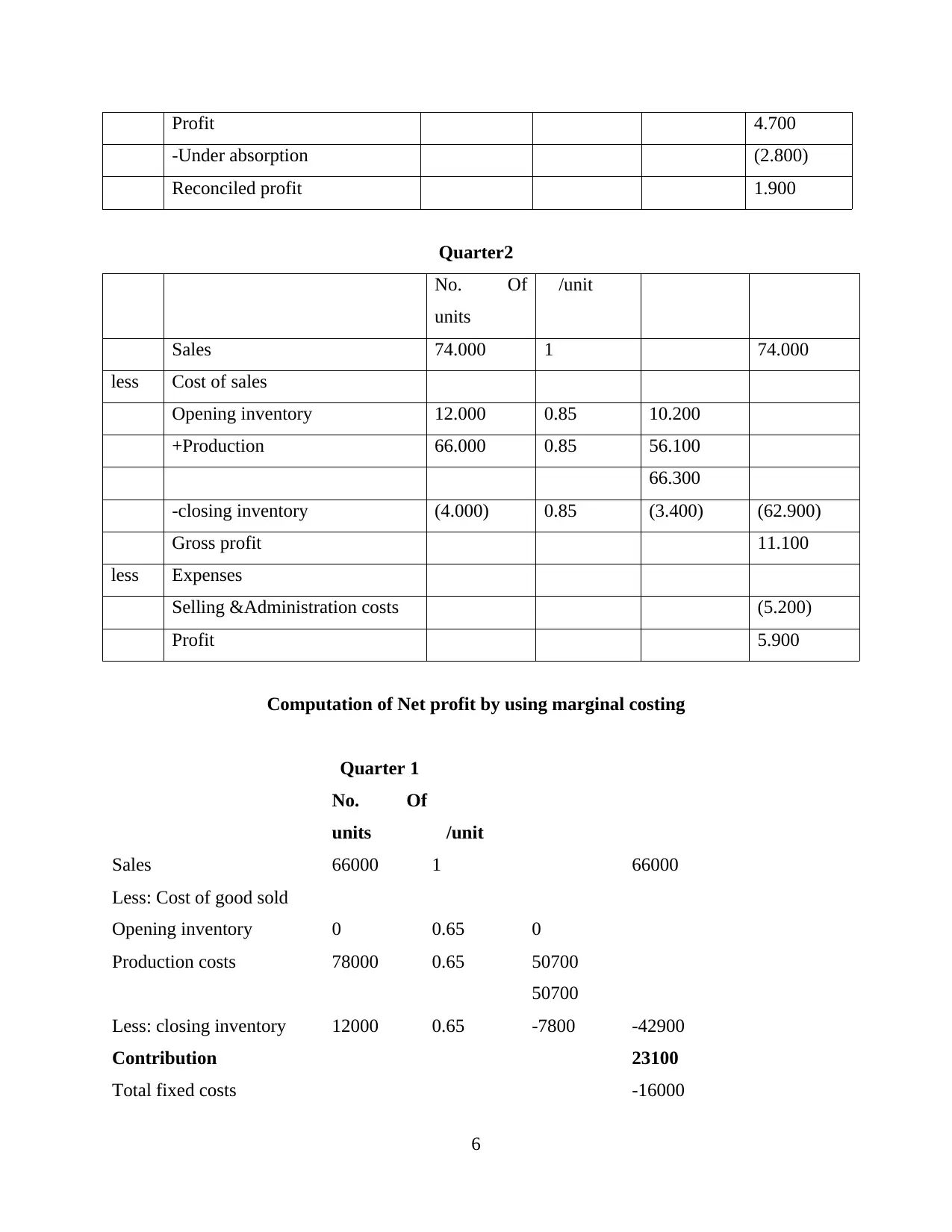

Profit 4.700

-Under absorption (2.800)

Reconciled profit 1.900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.85 10.200

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5.900

Computation of Net profit by using marginal costing

Quarter 1

No. Of

units £/unit £ £

Sales 66000 1 66000

Less: Cost of good sold

Opening inventory 0 0.65 0

Production costs 78000 0.65 50700

50700

Less: closing inventory 12000 0.65 -7800 -42900

Contribution 23100

Total fixed costs -16000

6

-Under absorption (2.800)

Reconciled profit 1.900

Quarter2

No. Of

units

£/unit £ £

Sales 74.000 1 74.000

less Cost of sales

Opening inventory 12.000 0.85 10.200

+Production 66.000 0.85 56.100

66.300

-closing inventory (4.000) 0.85 (3.400) (62.900)

Gross profit 11.100

less Expenses

Selling &Administration costs (5.200)

Profit 5.900

Computation of Net profit by using marginal costing

Quarter 1

No. Of

units £/unit £ £

Sales 66000 1 66000

Less: Cost of good sold

Opening inventory 0 0.65 0

Production costs 78000 0.65 50700

50700

Less: closing inventory 12000 0.65 -7800 -42900

Contribution 23100

Total fixed costs -16000

6

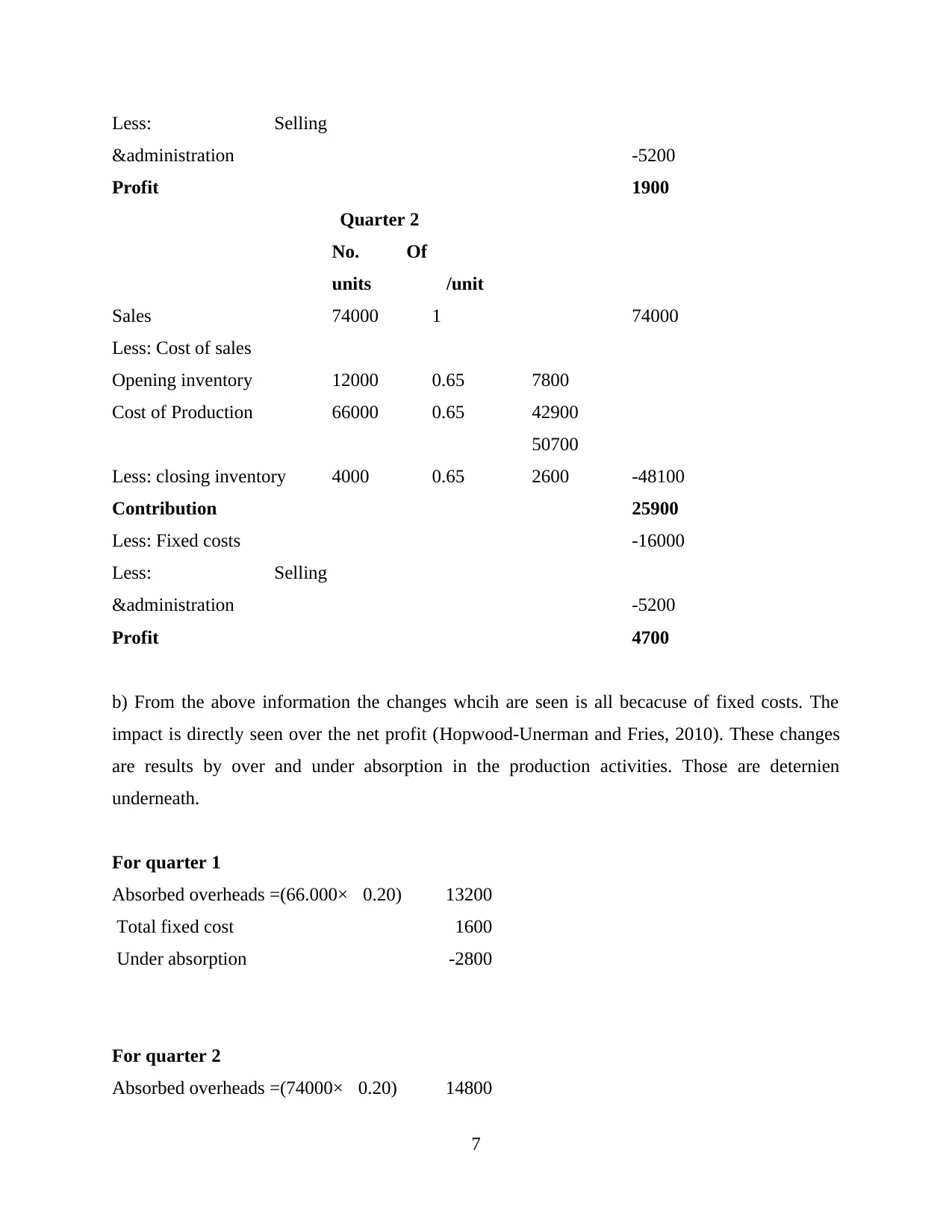

Less: Selling

&administration -5200

Profit 1900

Quarter 2

No. Of

units £/unit £ £

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 12000 0.65 7800

Cost of Production 66000 0.65 42900

50700

Less: closing inventory 4000 0.65 2600 -48100

Contribution 25900

Less: Fixed costs -16000

Less: Selling

&administration -5200

Profit 4700

b) From the above information the changes whcih are seen is all becacuse of fixed costs. The

impact is directly seen over the net profit (Hopwood-Unerman and Fries, 2010). These changes

are results by over and under absorption in the production activities. Those are deternien

underneath.

For quarter 1

Absorbed overheads =(66.000×£0.20) 13200

Total fixed cost 1600

Under absorption -2800

For quarter 2

Absorbed overheads =(74000×£0.20) 14800

7

&administration -5200

Profit 1900

Quarter 2

No. Of

units £/unit £ £

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 12000 0.65 7800

Cost of Production 66000 0.65 42900

50700

Less: closing inventory 4000 0.65 2600 -48100

Contribution 25900

Less: Fixed costs -16000

Less: Selling

&administration -5200

Profit 4700

b) From the above information the changes whcih are seen is all becacuse of fixed costs. The

impact is directly seen over the net profit (Hopwood-Unerman and Fries, 2010). These changes

are results by over and under absorption in the production activities. Those are deternien

underneath.

For quarter 1

Absorbed overheads =(66.000×£0.20) 13200

Total fixed cost 1600

Under absorption -2800

For quarter 2

Absorbed overheads =(74000×£0.20) 14800

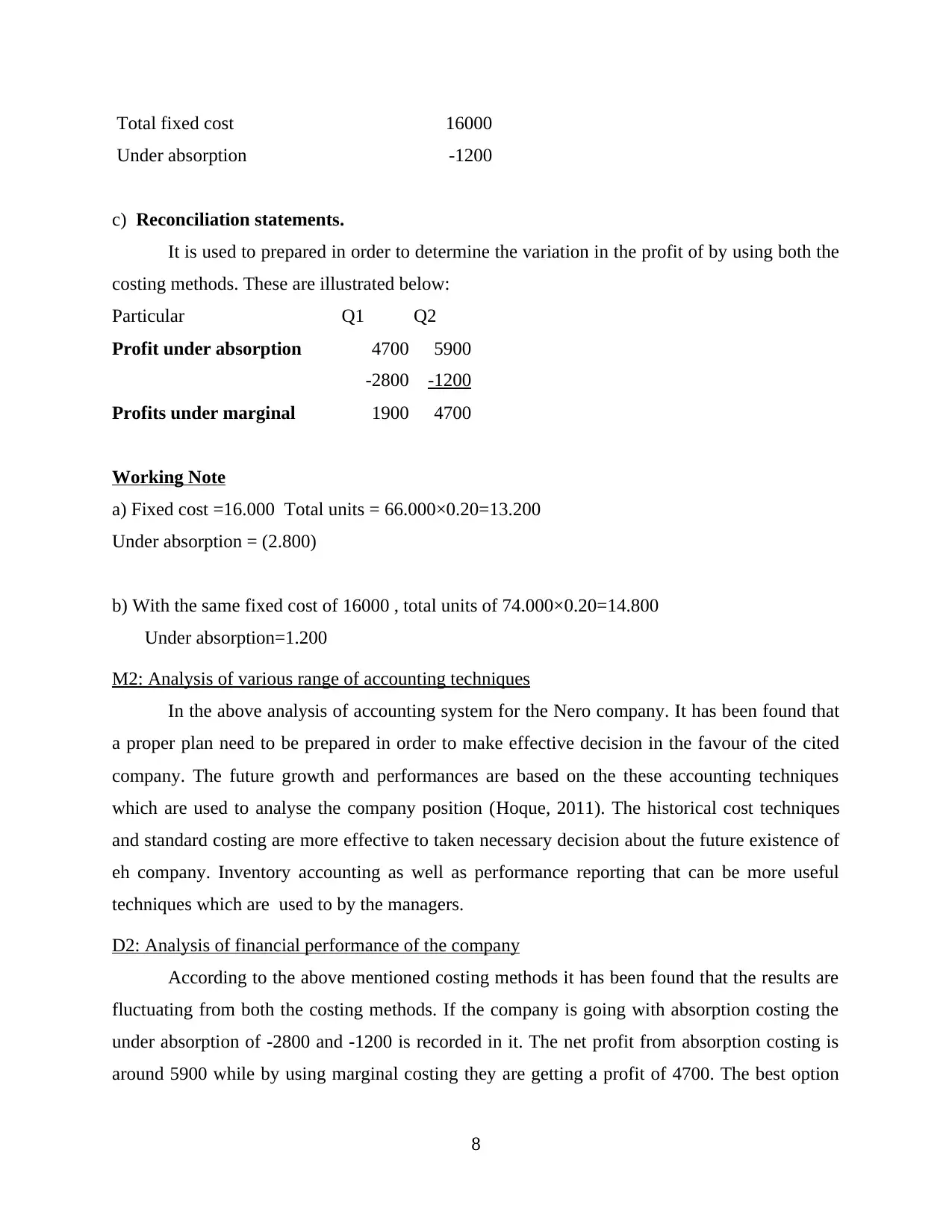

7

Total fixed cost 16000

Under absorption -1200

c) Reconciliation statements.

It is used to prepared in order to determine the variation in the profit of by using both the

costing methods. These are illustrated below:

Particular Q1 Q2

Profit under absorption 4700 5900

-2800 -1200

Profits under marginal 1900 4700

Working Note

a) Fixed cost =16.000 Total units = 66.000×0.20=13.200

Under absorption = (2.800)

b) With the same fixed cost of 16000 , total units of 74.000×0.20=14.800

Under absorption=1.200

M2: Analysis of various range of accounting techniques

In the above analysis of accounting system for the Nero company. It has been found that

a proper plan need to be prepared in order to make effective decision in the favour of the cited

company. The future growth and performances are based on the these accounting techniques

which are used to analyse the company position (Hoque, 2011). The historical cost techniques

and standard costing are more effective to taken necessary decision about the future existence of

eh company. Inventory accounting as well as performance reporting that can be more useful

techniques which are used to by the managers.

D2: Analysis of financial performance of the company

According to the above mentioned costing methods it has been found that the results are

fluctuating from both the costing methods. If the company is going with absorption costing the

under absorption of -2800 and -1200 is recorded in it. The net profit from absorption costing is

around 5900 while by using marginal costing they are getting a profit of 4700. The best option

8

Under absorption -1200

c) Reconciliation statements.

It is used to prepared in order to determine the variation in the profit of by using both the

costing methods. These are illustrated below:

Particular Q1 Q2

Profit under absorption 4700 5900

-2800 -1200

Profits under marginal 1900 4700

Working Note

a) Fixed cost =16.000 Total units = 66.000×0.20=13.200

Under absorption = (2.800)

b) With the same fixed cost of 16000 , total units of 74.000×0.20=14.800

Under absorption=1.200

M2: Analysis of various range of accounting techniques

In the above analysis of accounting system for the Nero company. It has been found that

a proper plan need to be prepared in order to make effective decision in the favour of the cited

company. The future growth and performances are based on the these accounting techniques

which are used to analyse the company position (Hoque, 2011). The historical cost techniques

and standard costing are more effective to taken necessary decision about the future existence of

eh company. Inventory accounting as well as performance reporting that can be more useful

techniques which are used to by the managers.

D2: Analysis of financial performance of the company

According to the above mentioned costing methods it has been found that the results are

fluctuating from both the costing methods. If the company is going with absorption costing the

under absorption of -2800 and -1200 is recorded in it. The net profit from absorption costing is

around 5900 while by using marginal costing they are getting a profit of 4700. The best option

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

for the Nero company is the marginal costing as they are getting more effective results from this

only. These are more effectively tools for making proper decision making for the coming future.

SECTION 2

P4: Planning tools used for budgetary control

Budget: It refers as the balance estimation of expenses and receipts of a given period of

time. It is prepared by taking support of past data. In the other words, a budgets is a set of pre-

determine report of management decisions and polices for the coming time period. The budget is

the highlight of the company's financial positions and it potentials. In relation to manage its

operations company need to prepare various budgets (Jansen, 2011).

Signification of budgets are:

Budgets are more useful for the company in order to determine its future and to increase

the market reputation in front of others.

One of the major aspect of the Nero company is to enhance the productivity through using right

techniques and budgets which will increase the profitability of the company.

Those costs which are incurred heavily on the production of products can be reduced so

that more effective results can be generated.

Budgets are said to be the values base for the decision making for future forecasting and growth.

Types of budgets are:

Operating budgets: It is mostly associated with the expenses which are incur by Nero

company in their production process. It include total estimation of the values of resources which

are needed for the performances of the company. It also consist of estimates of work load in

relation with the total cost accounts. It consist of sales and production budgets (Macintosh and

Quattrone, 2010).

Advantages

It will make the organisations respondent to environment.

It makes the organisations to determine their basic structure and control the extra costs by using

right kind of decision.

Disadvantage

It is more difficult to make because collection of information from each departments are not so

easy tasks.

9

only. These are more effectively tools for making proper decision making for the coming future.

SECTION 2

P4: Planning tools used for budgetary control

Budget: It refers as the balance estimation of expenses and receipts of a given period of

time. It is prepared by taking support of past data. In the other words, a budgets is a set of pre-

determine report of management decisions and polices for the coming time period. The budget is

the highlight of the company's financial positions and it potentials. In relation to manage its

operations company need to prepare various budgets (Jansen, 2011).

Signification of budgets are:

Budgets are more useful for the company in order to determine its future and to increase

the market reputation in front of others.

One of the major aspect of the Nero company is to enhance the productivity through using right

techniques and budgets which will increase the profitability of the company.

Those costs which are incurred heavily on the production of products can be reduced so

that more effective results can be generated.

Budgets are said to be the values base for the decision making for future forecasting and growth.

Types of budgets are:

Operating budgets: It is mostly associated with the expenses which are incur by Nero

company in their production process. It include total estimation of the values of resources which

are needed for the performances of the company. It also consist of estimates of work load in

relation with the total cost accounts. It consist of sales and production budgets (Macintosh and

Quattrone, 2010).

Advantages

It will make the organisations respondent to environment.

It makes the organisations to determine their basic structure and control the extra costs by using

right kind of decision.

Disadvantage

It is more difficult to make because collection of information from each departments are not so

easy tasks.

9

There is huge chance of bias among managers and top level managements.

Cash budget: It refers as the total cash inflows and out flows which are generated by the

company from its various activities. Such as investing, operational and financing. It is said to be

detailed budget determination which is incorporating both revenue and capital products. It

provided forewarning of potential issues that are arises in an organisation.

Advantages:

Company expenses are grouped by the organisation and objectives of expenses are categories

into these budgets (Pitkänen and Lukka, 2011).

Under this appropriation are made on the cash basis and also determine the annual payment.

Disadvantages

Cash deficiency can be reduce through an well planned system.

The manager need to apply correct and proper format to record cash transaction.

Master budgets: It is said to be the combination of all budgets which are made by the company

after make suggestion and collecting necessary information from the various departments

Advantages

It identified the various issues in an single sheet of report that a company is facing during the

year.

Disadvantage

It takes more time and cost to prepared such kind of budgets.

Budgeting process: It is necessary for the cited company to prepare a well classified

budget process which will help them to work according to the set plan. The past data of the

company is analysed by taking base for the year. It is techniques which every managers need to

follow during preparation of budget for the company. All the initial to ending process are need to

be considered (Quinn, 2011).

M3: Evaluation of planning tools

According to above mentioned planning tools for the cited company. It can be used for its

analysis the growth and productivity. The operating and cash budgets are necessary for the

company to manage and control is daily operations.

D3: Analysis of financial issues

An organisation is facing so many financial or non financial issues. The accounting systems are

used by the company in order to overcome those issues. Different financial problems are can be

10

Cash budget: It refers as the total cash inflows and out flows which are generated by the

company from its various activities. Such as investing, operational and financing. It is said to be

detailed budget determination which is incorporating both revenue and capital products. It

provided forewarning of potential issues that are arises in an organisation.

Advantages:

Company expenses are grouped by the organisation and objectives of expenses are categories

into these budgets (Pitkänen and Lukka, 2011).

Under this appropriation are made on the cash basis and also determine the annual payment.

Disadvantages

Cash deficiency can be reduce through an well planned system.

The manager need to apply correct and proper format to record cash transaction.

Master budgets: It is said to be the combination of all budgets which are made by the company

after make suggestion and collecting necessary information from the various departments

Advantages

It identified the various issues in an single sheet of report that a company is facing during the

year.

Disadvantage

It takes more time and cost to prepared such kind of budgets.

Budgeting process: It is necessary for the cited company to prepare a well classified

budget process which will help them to work according to the set plan. The past data of the

company is analysed by taking base for the year. It is techniques which every managers need to

follow during preparation of budget for the company. All the initial to ending process are need to

be considered (Quinn, 2011).

M3: Evaluation of planning tools

According to above mentioned planning tools for the cited company. It can be used for its

analysis the growth and productivity. The operating and cash budgets are necessary for the

company to manage and control is daily operations.

D3: Analysis of financial issues

An organisation is facing so many financial or non financial issues. The accounting systems are

used by the company in order to overcome those issues. Different financial problems are can be

10

solved by applying correct techniques. Key performances indicators and benchmarking is an

importance techniques of solving financial problems of a company. It will help to increase the

growth and profitability of the company as well as correct the pattern of decision making

process.

P5: Respond to various issues related with financial aspects

Every businesses entity is facing the problem of financial problems which are arises

during the production activities. It is the role of the managers to identified all those issues and

plan to overcome it. There are necessary process to be taken in order to resolve company

problems. In the above mentioned Nero Ltd is facing lack of communication in managing its

operations as well as control the inventory positions. It is considered as one of the major issues

for the managers that has to be resolved as soon as possible so that more accurate results can be

achieved (Quinn, 2014). The prime objective of the company is to manage its operations in well

planned manner so that less chance of mistakes can be seen. The other issues that Nero Ltd is

facing at the time of operations are appropriate correspondence and utilisation of resources. With

the useful implementation of effective bookkeeping can be implemented by the company. Some

of the financial techniques which are used by the company to solve financial issues are:

Key performance indicators: It is used to measure the performance of the individual as

well as the organisation. The main objectives of this techniques are to analyse the progressivism

of the company performances during the year.

Benchmarking: As per this techniques, company can used to compare their own

operations with the other so that they can react to those problems which are faced by the

company (Setthasakko, 2010).

Financial governance: Under this different statements such as income statements and

balance sheets are need to be prepared according to the set guidelines which are prescribed by

the government.

M4: Analysis of the financial issues

In the above mentioned various financial issues which a company is facing in managing

its day to day operations. The performance and growth is mostly imbalance with the decision

taken on the base of financial position. All those issues which are associated with net profit of

the company can be solve through applying absorption and marginal costing. It will help to

increase the efficiency and effectiveness of the company.

11

importance techniques of solving financial problems of a company. It will help to increase the

growth and profitability of the company as well as correct the pattern of decision making

process.

P5: Respond to various issues related with financial aspects

Every businesses entity is facing the problem of financial problems which are arises

during the production activities. It is the role of the managers to identified all those issues and

plan to overcome it. There are necessary process to be taken in order to resolve company

problems. In the above mentioned Nero Ltd is facing lack of communication in managing its

operations as well as control the inventory positions. It is considered as one of the major issues

for the managers that has to be resolved as soon as possible so that more accurate results can be

achieved (Quinn, 2014). The prime objective of the company is to manage its operations in well

planned manner so that less chance of mistakes can be seen. The other issues that Nero Ltd is

facing at the time of operations are appropriate correspondence and utilisation of resources. With

the useful implementation of effective bookkeeping can be implemented by the company. Some

of the financial techniques which are used by the company to solve financial issues are:

Key performance indicators: It is used to measure the performance of the individual as

well as the organisation. The main objectives of this techniques are to analyse the progressivism

of the company performances during the year.

Benchmarking: As per this techniques, company can used to compare their own

operations with the other so that they can react to those problems which are faced by the

company (Setthasakko, 2010).

Financial governance: Under this different statements such as income statements and

balance sheets are need to be prepared according to the set guidelines which are prescribed by

the government.

M4: Analysis of the financial issues

In the above mentioned various financial issues which a company is facing in managing

its day to day operations. The performance and growth is mostly imbalance with the decision

taken on the base of financial position. All those issues which are associated with net profit of

the company can be solve through applying absorption and marginal costing. It will help to

increase the efficiency and effectiveness of the company.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above project report it has been concluded that management accounting is an

crucial aspects of any business inn order to manage and formulated its daily operations. The

project summarised with management accounting system types and its usefulness to the Nero

company. It also concluded the various reporting and costing methods which are used to find out

net profit for the company. The understanding of budgets are various financial tools are

explained in the above. It also present the techniques which are used to solve financial problems

which are arises in an organisations.

12

From the above project report it has been concluded that management accounting is an

crucial aspects of any business inn order to manage and formulated its daily operations. The

project summarised with management accounting system types and its usefulness to the Nero

company. It also concluded the various reporting and costing methods which are used to find out

net profit for the company. The understanding of budgets are various financial tools are

explained in the above. It also present the techniques which are used to solve financial problems

which are arises in an organisations.

12

REFERENCES

Books and Journals:

13

Books and Journals:

13

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.